Sample Category Title

GOLD (XAUUSD) Found Buyers After Elliott Wave Zig Zag Pattern

Hello fellow traders. In this technical blog we’re going to take a quick look at the Elliott Wave charts of GOLD (XAUUSD), published in members area of the website. As our members know the pair is showing impulsive bullish sequences in the cycle from the 2537.3 low. Consequently , we were calling for the further rally in the commodity. Recently GOLD made a pull back that has had a form of Elliott Wave Zig Zag pattern. In the further text we are going to explain the Elliott Wave Pattern and the forecast

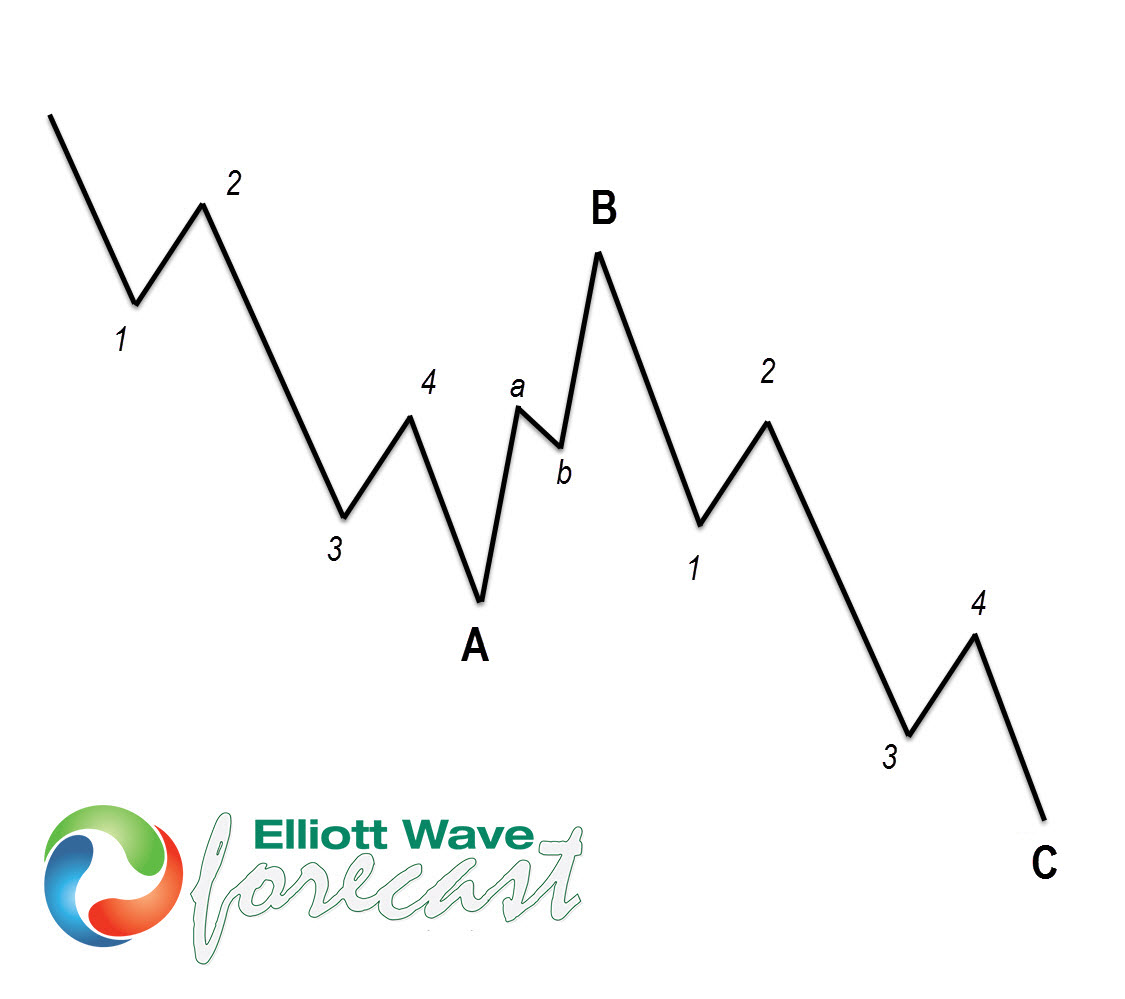

Before we take a look at the real market example, let’s explain Elliott Wave Zigzag.

Elliott Wave Zigzag is the most popular corrective pattern in Elliott Wave theory . It’s made of 3 swings which have 5-3-5 inner structure. Inner swings are labeled as A,B,C where A =5 waves, B=3 waves and C=5 waves. That means A and C can be either impulsive waves or diagonals. (Leading Diagonal in case of wave A or Ending in case of wave C) . Waves A and C must meet all conditions of being 5 wave structure, such as: having RSI divergency between wave subdivisions, ideal Fibonacci extensions and ideal retracements.

At the chart below we can see what Elliott Wave Zig Zag pattern looks like in real market.

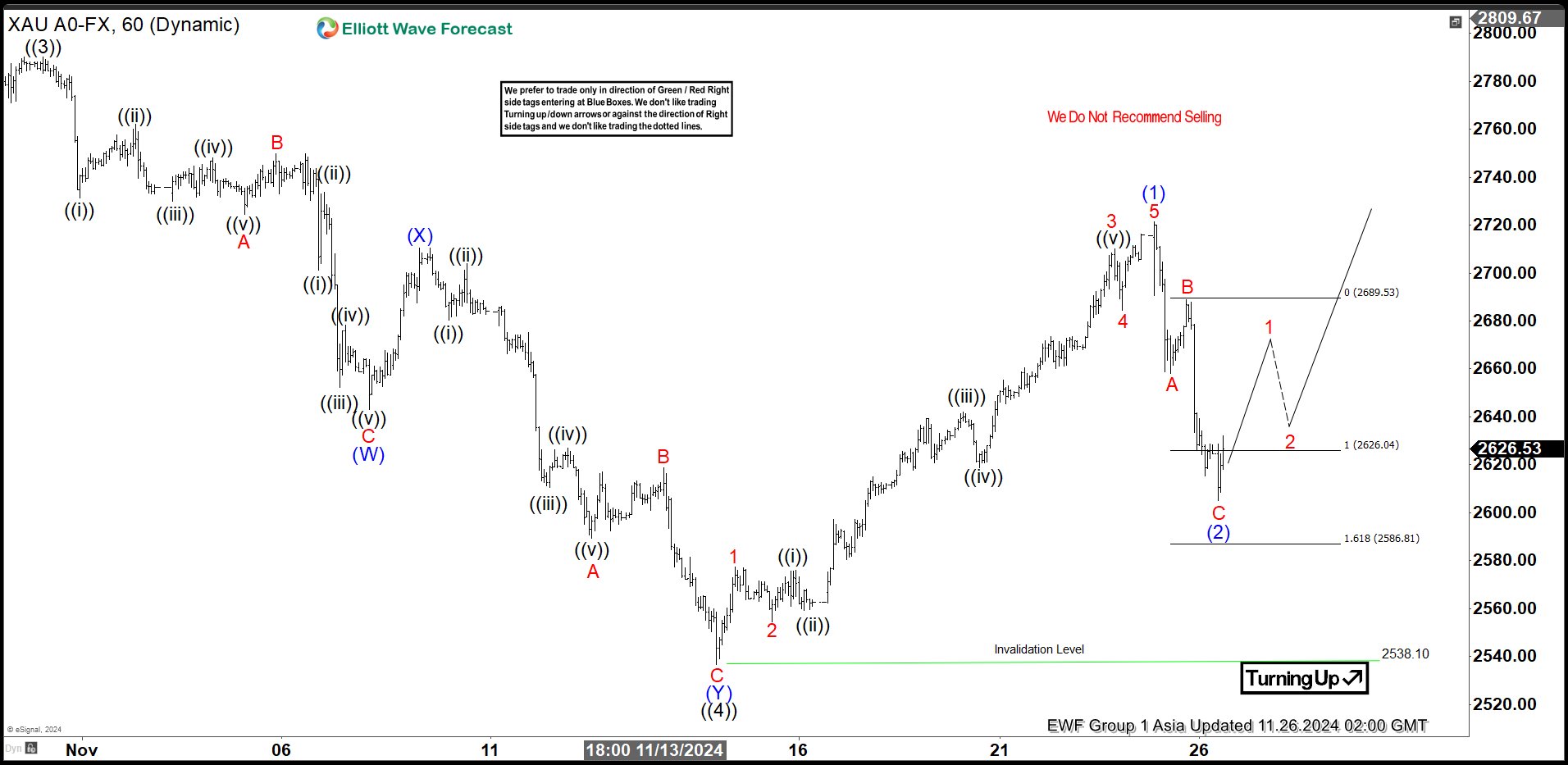

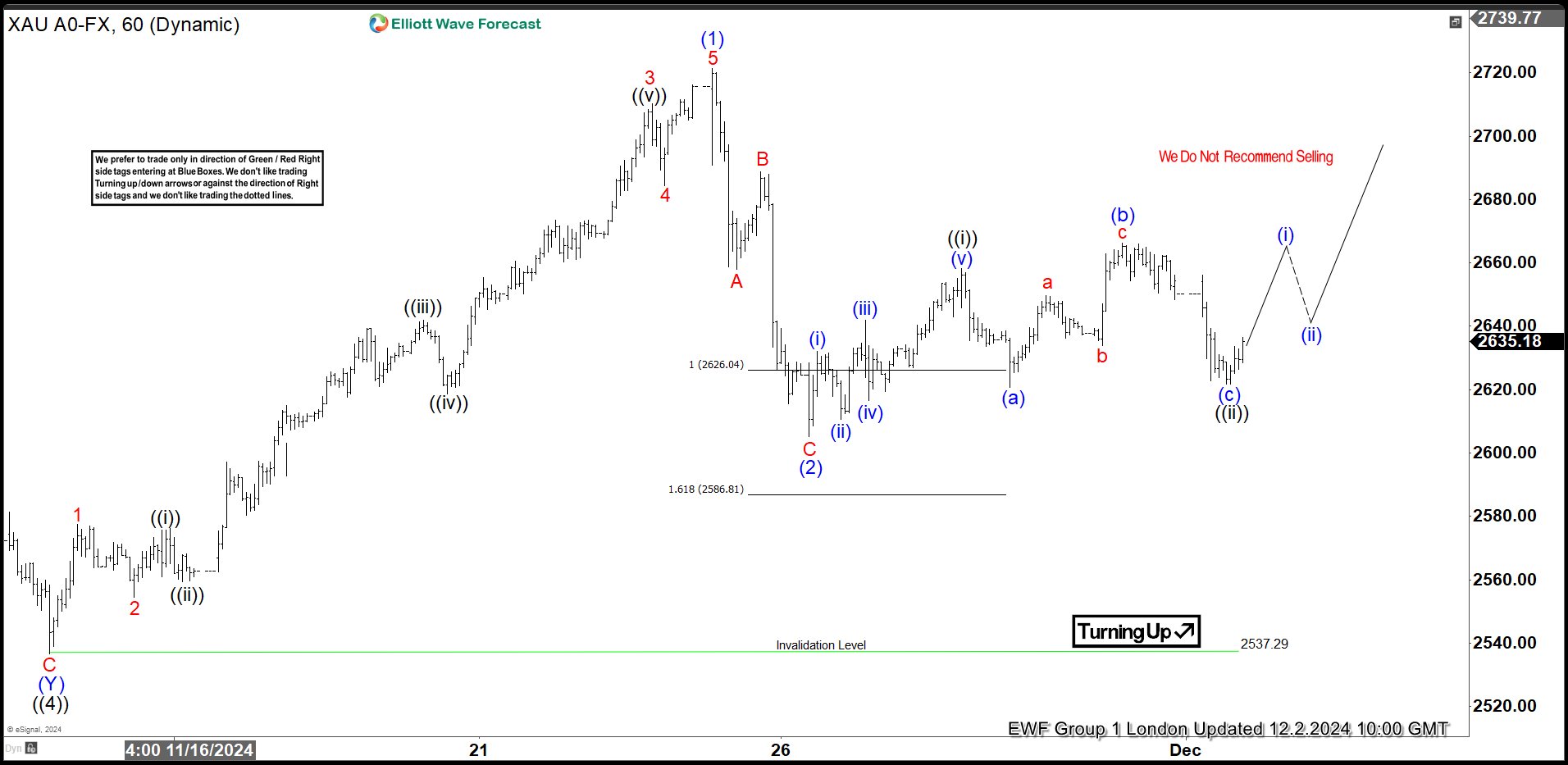

GOLD H1 London Update 11.26.2024

GOLD ended cycle from the 2538 low as 5 waves structure. The commodity has given us pull back against the 2538 low that unfolded as Zig Zag pattern. Extreme zone has been already reached at 2626.04-2586.8 ( buying zone) We don’t recommend selling the commodity and expect further rally to resume from the marked area.

GOLD H1 London Update 10.24.2023

The commodity has given us nice reaction from the marked extreme zone. Now, as far as the price holds above 2606 low, we can have correction completed and see the further strength. We need to see break above (1) blue – 11.22 high to confirm next leg up is in progress.

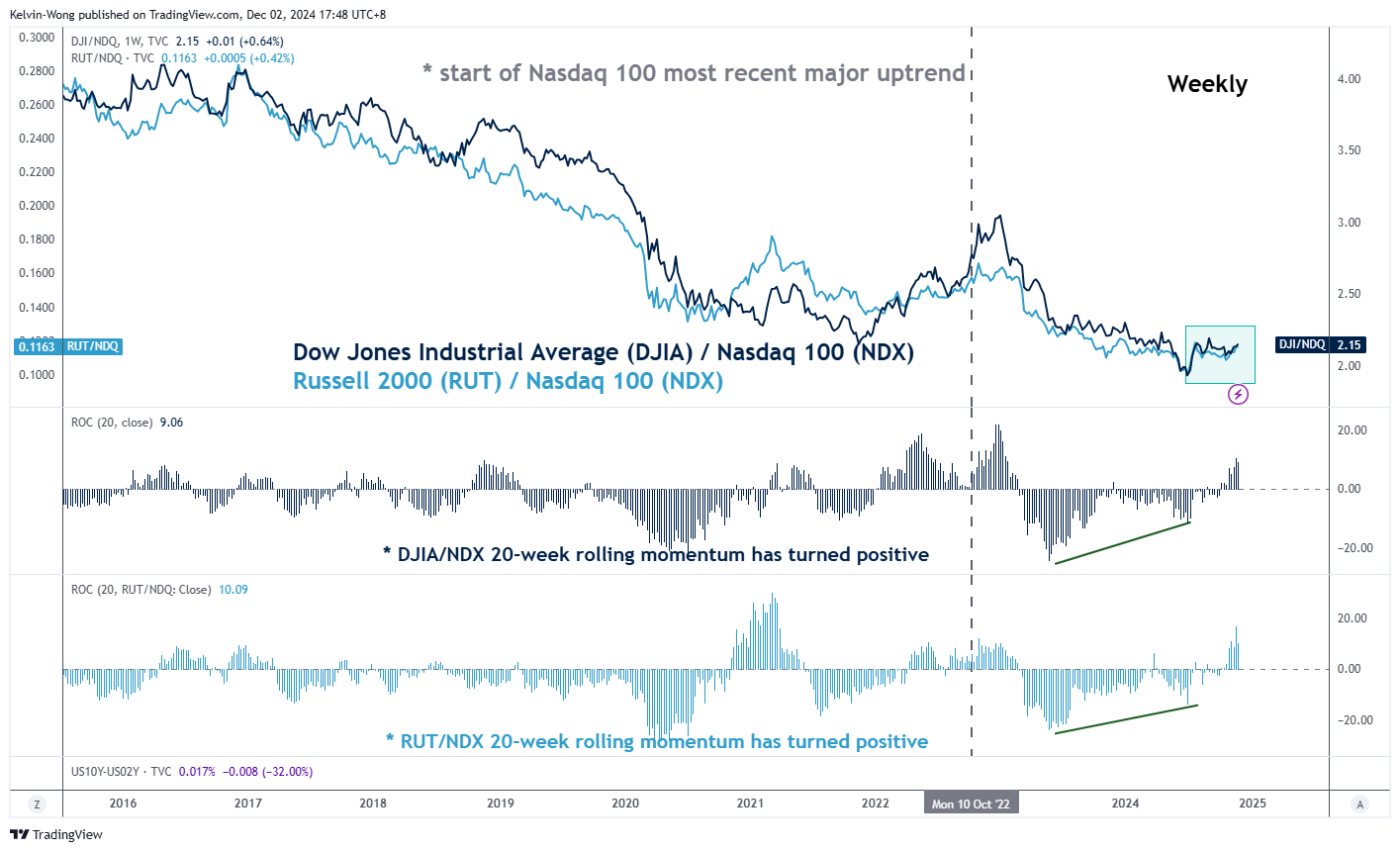

Russell 2000: On Sight for a Potential Fresh All-Time High

- Russell 2000 outperformance against S&P 500 and Nasdaq continued to persist since Q3 2024.

- The recent monthly Russell 2000 stellar performance of 10.8% in November has been reinforced by the incoming Trump administration’s “America First” policy.

- Watch the 2,288 key medium-term support on the Russell 2000.

Since our last publication, the price actions of the Russell 2000 comprised of small-cap listed companies in the US rallied as expected and finally retested its current intraday all-time high of 2,458 made three years ago on 5 November 2021 on Monday, 25 November.

The Russell 2000 is the only major US stock index that has not made fresh all-time highs in the past three years versus the S&P 500, Nasdaq 100, and Dow Jones Industrial Average which have skyrocketed to a series of fresh all-time highs in 2024.

Interestingly, the small-cap Russell 2000 has started to outperform the mega-cap technology-centric S&P 500 and Nasdaq 100 since the third quarter of 2024.

In November, Russell 2000 outperformance continued to persist where it recorded a monthly gain of 10.8%, almost double the monthly returns of the S&P 500 (5.7%) and Nasdaq 100 (5.2%). In addition, the Dow Jones Industrial Average also surpassed the S&P 500 and Nasdaq 100 with a monthly gain of 7.5% in November.

Trump’s “American First” policy reinforces Russell 2000 outperformance

Fig 1: Ratio charts of Russell 2000 & DJIA over Nasdaq 100 as of 29 Nov 2024 (Source: TradingView, click to enlarge chart)

The incoming Trump administration has vowed to enact generous corporate tax cuts and deregulation policies with the support of a Republican congress, it has created tailwinds for small-cap companies in the US.

In addition, recent trade tariff threats from US President-elect Trump towards China, Canada, Mexico, and the BRICS grouping of emerging economies have also provided a potential defensive impetus for Russell 2000 outperformance over the S&P 500 and Nasdaq 100 as Russell 200 component stocks derived most of their respective revenue streams (close to 80% on the aggregate) domestically in the US (see Fig 1).

The information technology sector has the largest market capitalization weightage in the S&P 500 and the Nasdaq 100 derives around 57% of its revenue from international markets that may be subject to headwinds from a potentially stronger US dollar, triggered by the effects of higher trade tariffs that may be imposed by the Trump administration.

Supported by rising 50-day and 200-day moving averages

Fig 2: US Russell 2000 CFD Index major and medium-term trends as of 2 Dec 2024 (Source: TradingView, click to enlarge chart)

In the lens of the technical analysis, the price actions of the US Russell 2000 CFD Index (a proxy of the E-mini Russell 2000 futures) have continued to be supported by upward-sloping 50-day and 200-day moving averages that suggest its medium-term and major uptrend phases remain intact.

Watch the 2,288 tightened key medium-term support and clearance above the 2,450 key intermediate resistance (also the current all-time area) may see the next medium-term resistance zone coming in at 2,625/655 for the US Russell 2000 CFD Index (see Fig 2).

However, failure to hold the 2,288 key support negates the bullish tone to kickstart a potential medium-term (multi-week) corrective decline sequence within its major uptrend phase to expose the next supports at 2,170 and 2,080.

Australian Retail Sales Jump But Aussie Dips

The Australian dollar is in negative territory on Monday. In the European session, AUD/USD is trading at 0.6491, down 0.26% on the day.

Australia’s retail sales rise to 0.6%

Australian events started the week on a strong note, as retail sales were higher than expected. October retail sales jumped 3.4% y/y in October, up sharply from the September gain of 1.2%. Monthly, retail sales climbed 0.6%, compared to 0.1% in September.

Retail sales have accelerated for three successive months as consumers are feeling more optimistic, with expectations that the central bank’s next move will be a rate cut. Retailers have been offering discounts ahead of the holiday season which contributed to a stronger than usual retail sales for October. Ironically, the strong retail sales report will reduce pressure on the Reserve Bank of Australia to cut rates.

The RBA has maintained the cash rate at 4.35% for over a year and has sounded hawkish about rate policy, saying that a rate hike remains on the table. The markets aren’t buying it and expect the next move to be a hike, likely in mid-2025. The RBA meets on Dec. 10 and is widely expected to stay on the sidelines and hold rates.

Inflation has been on the decline in recent months but the RBA has warned that underlying inflation remains too high. In October, headline inflation was unchanged at 2.1%, the lowest level since 2021and around the midpoint of the RBA’s target of 1%-3%. The trimmed mean rate, an indicator of underlying inflation, accelerated to 3.5% in October, up from 3.2% a month earlier.

AUD/USD Technical

- AUD/USD is testing support at 0.6506. Next, there is resistance at 0.6485

- 0.6533 and 0.6554 are the next resistance lines

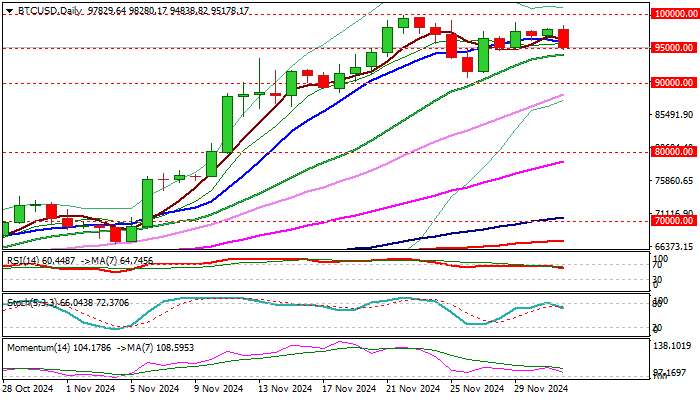

Bitcoin Eases But Overall Picture Remains Bullish Above 90K and Keeps 100K Target in Focus

Bitcoin price fell 2.6% in Asian / European trading on Monday, after the dollar received fresh boost from the latest comments from Donald Trump.

Although today’s dip was the biggest in one week, the price so far stays above significant 95K support (psychological / floor of congestion that extends into fifth consecutive day) keeping near-term bias with bulls.

Bitcoin hit new record high at 99800 vs dollar recently that increased pressure on magical 100K barrier, but expected strong headwinds at this zone, pushed the price lower, to hold in prolonged consolidation within 90K/100K range.

This was seen as logical reaction on recent strong post-US election rally, with crypto market being well supported by expected measures from pro-crypto Trump’s administration, but awaiting policies that Trump promised during the campaign, to be implemented that would provide fresh and significant support to bitcoin.

Near-term action shown bitcoin in defensive, but overall, in sideways mode and awaiting fresh direction signals.

Larger bulls to remain intact above 90K, with markets focusing on economic data (US Nov labor report is in focus) and political / geopolitical news.

Res: 95935; 98280; 98800; 99032

Sup: 95000; 94199; 91501; 90000

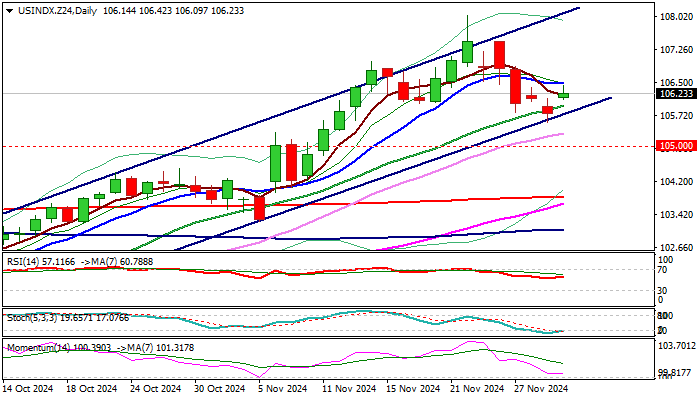

Dollar Index Outlook: Dollar Rose in Reaction to Shift in Trump’s Rhetoric

The dollar index edged higher after opening with gap higher on Monday, lifted by a significant shift in rhetorics pf President-elect Donald Trump, who turned his aims for weaker dollar to fight trade war, to threats to BRICS member countries of facing a 100% tariffs if create new or support another currency in attempts to replace dollar.

Fresh rise of dollar generated initial signal of reversal after a four-day pullback was contained rising channel support trendline, reinforced by daily Kijun-sen (at 105.60 zone), although more work at the upside is required to confirm signal.

Break of immediate resistances at 106.50 zone (Fibo 38.2% of 108.04/105.57 bear-leg / 10DMA) to firm near-term structure for attack at next pivot at 106.81 (50% retracement / daily Tenkan-sen), violation of which to shift near term focus to the upside and signal that corrective phase might be over.

Technical picture on daily chart is overall bullish, as 14-d momentum is in positive territory and turning up, stochastic is emerging from oversold zone and converging 55/200DMA’s are signaling possible formation of Golden Cross.

Near-term action is expected to remain biased higher while holding within month long bull-channel and pointing to steady uptrend.

Res: 106.50; 106.81; 107.10; 107.46.

Sup: 106.09; 105.60; 105.32; 105.00.

UK PMI Manufacturing finalized at 48.0, to 48.0, high costs, low demand and raised uncertainty

UK PMI Manufacturing was finalized to 48.0 in November, marking a nine-month low and reflecting a deepening contraction in the sector. The decline from October's 49.9 underscores persistent challenges, including high costs, subdued demand, and a "bleak" export environment.

Rob Dobson, Director at S&P Global Market Intelligence, noted that conditions "deteriorated again" as manufacturers faced falling output, reduced orders, and cutbacks in purchasing, jobs, and inventories.

Exports remained under pressure, with weaker demand from key markets in the US, China, and the EU driving a further decline in new export business. Supply chain disruptions also intensified, fueled by the ongoing Red Sea crisis, port delays, and border regulation challenges.

Looking ahead, the manufacturing sector faces additional headwinds. Recent UK budget measures, including higher labor costs and employer national insurance contributions, are expected to increase operational expenses in 2025.

Combined with rising geopolitical tensions and the threat of heightened global protectionism, manufacturers are bracing for an extended period of "high costs, low demand and raised uncertainty".

Eurozone PMI manufacturing finalized at 45.2, recession looks never going to end

Eurozone Manufacturing PMI slipped to 45.2 in November, down from October’s 46.0, reflecting deepening contraction in the sector.

The downturn remains widespread, with manufacturing activity deteriorating across major economies. Germany and France recorded PMI readings of 43.0 and 43.1 (a 10-month low), respectively, indicating severe weaknesses. Italy followed closely at 44.5, hitting a 12-month low, while the Netherlands posted a reading of 46.6, an 11-month low. Spain and Greece maintained levels above 50, but both fell to two-month lows at 53.1 and 50.9, respectively.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, described the figures as "terrible," suggesting the manufacturing recession “is never going to end.”

De la Rubia forecasted a -0.7% contraction in manufacturing output for Q4, with the slump likely "going to drag into next year". The capital goods sector is bearing the brunt of the downturn, while companies continue to trim staff, signaling rising unemployment ahead.

Full Eurozone PMI manufacturing final release here.

XAG/USD Analysis: Silver Price Balances at Key Support

As reflected in the XAG/USD chart, the price of silver this morning is trading near $30.2, just above a critical support zone formed by:

→ The psychological level of $30.00;

→ The lower boundary of the ascending channel. As indicated by the blue arrows, this lower boundary has consistently provided support, enabling bullish reversals in silver prices throughout 2024.

However, the price is currently below the 200-day moving average (MA), which is trending downward. An examination of price action in November reveals a lack of sustained growth following two breaches of the psychological level. As the red arrows illustrate:

→ On the first occasion, the price encountered resistance near $31.50;

→ On the second, it failed to rise above $31.

This could indicate weak demand, increasing the risk of a bearish breakout below the key support zone, potentially breaking the 2024 uptrend.

Meanwhile, analysts remain optimistic, citing strong fundamentals. According to media reports:

→ ANZ Research analysts forecast silver prices reaching $35.4 in 2025;

→ JP Morgan analysts predict silver at $36;

→ Saxo Bank analysts anticipate prices climbing to $40 by 2025.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

AUD/USD Stabilises Amid US Dollar Pressures and Domestic Economic Strength

On Monday, the AUD/USD pair remains stable around the 0.6450 mark. After benefiting from the US dollar's weakness during the extended US holiday weekend, the currency pair faced new pressures following remarks by US President-elect Donald Trump. Trump's threat to impose 100% trade tariffs on BRICS nations if they pursue a universal currency to replace the US dollar has sparked a renewed demand for safe-haven assets, bolstering the USD.

October's retail sales figures exceeded expectations, supporting the Australian dollar, and reinforcing the market's belief that the Reserve Bank of Australia (RBA) may not cut rates soon. RBA Governor Michele Bullock recently highlighted that core inflation remains elevated, which justifies continuing a restrictive monetary policy stance. The RBA believes it will take some time before inflation stabilises near its target.

Technical analysis of AUD/USD

H4 chart: the AUD/USD is currently in the first phase of a correction wave, having achieved a local target at 0.6527. The market is now forming a decline structure towards 0.6466, and once this level is reached, a new growth phase will begin, aiming for 0.6542. This scenario is supported by the MACD indicator, which shows the signal line above zero and trending upwards, indicating potential for continued growth.

H1 chart: the pair has nearly reached the local growth target of 0.6527. A decline to 0.6470 is expected shortly, followed potentially by a rise to 0.6500 and then a drop to 0.6466. If this level is achieved, the market may prepare for another upward movement towards 0.6542. The Stochastic oscillator supports this outlook, with its signal line currently below 50 and expected to drop to 20, suggesting a forthcoming reversal and potential for growth.

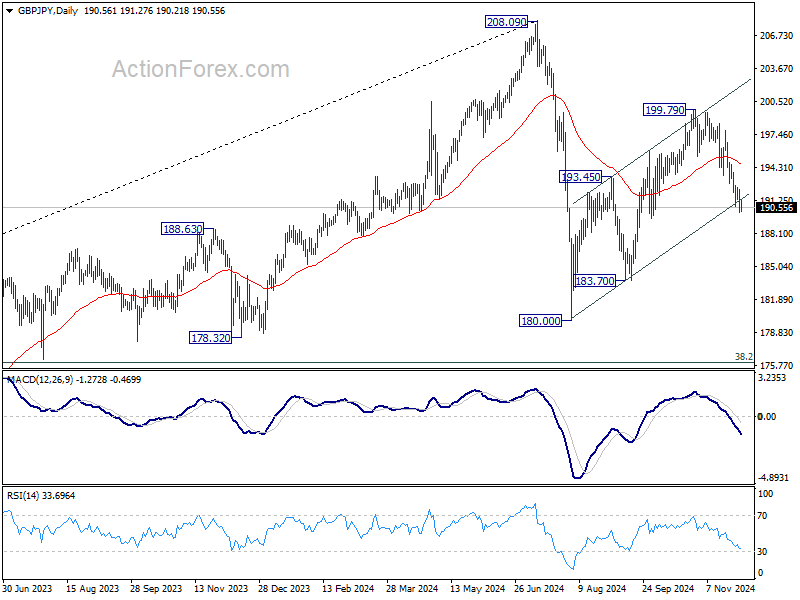

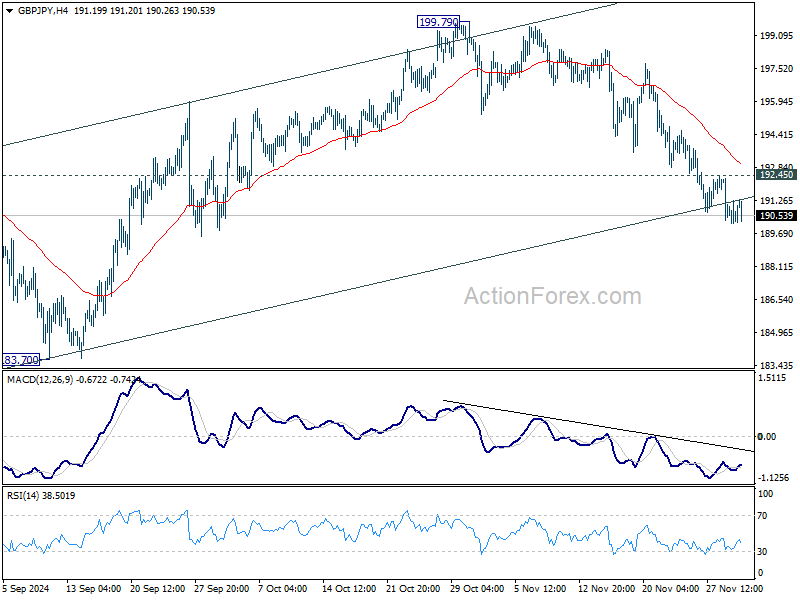

GBP/JPY Daily Outlook

Daily Pivots: (S1) 189.79; (P) 191.07; (R1) 192.00; More...

Intraday bias in GBP/JPY remains on the downside at this point. Fall from 199.79 should target 183.70 support. Break there will bring retest of 180.00 low. On the downside, above 192.45 minor resistance will turn intraday bias neutral first. But risk will now stay on the downside as long as 55 D EMA (now at 194.73) holds, in case of recovery.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.