Sample Category Title

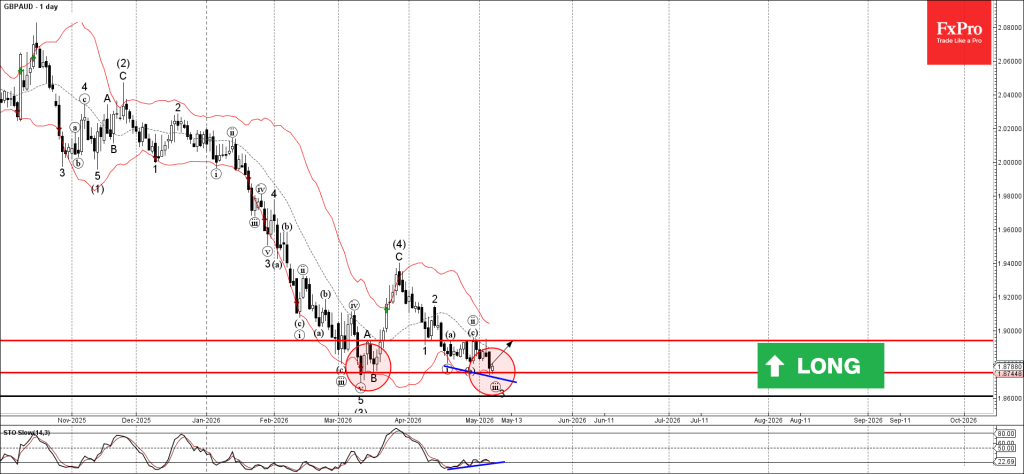

GBPAUD Wave Analysis

GBPAUD: ⬆️ Buy

- GBPAUD reversed from support zone

- Likely to rise to resistance level 1.8940

GBPAUD currency pair recently reversed from the support zone between the support level 1.875 (which stopped sharp daily downtrend in March) and the lower daily Bollinger Band.

The upward reversal from this support zone stopped the previous minor impulse wave iii of the downward impulse wave 3 from April.

Given the strength of the support level 1.875 and the bullish divergence on the daily Stochastic indicator, GBPAUD currency pair can be expected to rise to the next resistance level 1.8940 (top of earlier waves a and ii).

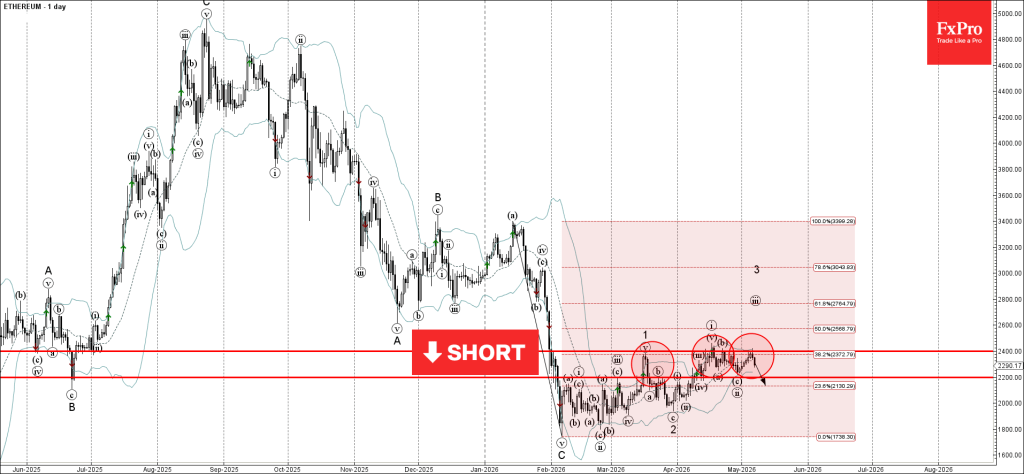

Ethereum Wave Analysis

Ethereum: ⬇️ Sell

- Ethereum reversed from pivotal resistance level 2400.00

- Likely to fall to support level 2200.00.

Ethereum cryptocurrency recently reversed up from the resistance zone between the pivotal resistance level 2400.00 (which has been reversing price from March), upper daily Bollinger Band and the 38.2% Fibonacci correction of the downward impulse from January.

The downward reversal from this resistance zone stopped the previous minor impulse wave 3 from the end of March.

Given the strong daily downtrend and the bearish sentiment seen across the crypto markets today, Ethereum can be expected to fall to the next support level 2200.00.

Eco Data 5/8/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Mar | 2.70% | 3.20% | 3.30% | 3.40% |

| 00:30 | JPY | Services PMI Apr F | 51 | 51.2 | 51.2 | |

| 06:00 | EUR | Germany Industrial Production M/M Mar | -0.70% | 0.40% | -0.30% | -0.50% |

| 06:00 | EUR | Germany Trade Balance (EUR) Mar | 14.3B | 18.9B | 19.8B | |

| 12:30 | CAD | Net Change in Employment Apr | -17.7K | 5.1K | 14.1K | |

| 12:30 | CAD | Unemployment Rate Apr | 6.90% | 6.70% | 6.70% | |

| 12:30 | USD | Nonfarm Payrolls Apr | 115K | 60K | 178K | 185K |

| 12:30 | USD | Unemployment Rate Apr | 4.30% | 4.30% | 4.30% | |

| 12:30 | USD | Average Hourly Earnings M/M Apr | 0.20% | 0.30% | 0.20% | |

| 14:00 | USD | UoM Consumer Sentiment P | 48.2 | 49.7 | 49.8 | |

| 14:00 | USD | UoM Inflation Expectations P | 4.50% | 4.70% |

| 23:30 | JPY |

| Labor Cash Earnings Y/Y Mar | |

| Actual | 2.70% |

| Consensus | 3.20% |

| Previous | 3.30% |

| Revised | 3.40% |

| 00:30 | JPY |

| Services PMI Apr F | |

| Actual | 51 |

| Consensus | 51.2 |

| Previous | 51.2 |

| 06:00 | EUR |

| Germany Industrial Production M/M Mar | |

| Actual | -0.70% |

| Consensus | 0.40% |

| Previous | -0.30% |

| Revised | -0.50% |

| 06:00 | EUR |

| Germany Trade Balance (EUR) Mar | |

| Actual | 14.3B |

| Consensus | 18.9B |

| Previous | 19.8B |

| 12:30 | CAD |

| Net Change in Employment Apr | |

| Actual | -17.7K |

| Consensus | 5.1K |

| Previous | 14.1K |

| 12:30 | CAD |

| Unemployment Rate Apr | |

| Actual | 6.90% |

| Consensus | 6.70% |

| Previous | 6.70% |

| 12:30 | USD |

| Nonfarm Payrolls Apr | |

| Actual | 115K |

| Consensus | 60K |

| Previous | 178K |

| Revised | 185K |

| 12:30 | USD |

| Unemployment Rate Apr | |

| Actual | 4.30% |

| Consensus | 4.30% |

| Previous | 4.30% |

| 12:30 | USD |

| Average Hourly Earnings M/M Apr | |

| Actual | 0.20% |

| Consensus | 0.30% |

| Previous | 0.20% |

| 14:00 | USD |

| UoM Consumer Sentiment P | |

| Actual | 48.2 |

| Consensus | 49.7 |

| Previous | 49.8 |

| 14:00 | USD |

| UoM Inflation Expectations P | |

| Actual | 4.50% |

| Consensus | |

| Previous | 4.70% |

Sunset Market Commentary

Markets

Markets today basically do what they got used to during the previous two months: waiting for the next batch of news headlines on the war between the US and Iran. Especially some more concrete news on the opening of the Strait of Hormuz (or the failure to do so) should help to make an estimate/guess on the impact on prices and activity in the short-to-medium term. Whatever the outcome of this process, this estimate will remain a complicated exercise, both for markets and central bankers. Even in case of a political solution/opening of the Strait in the ‘near future’, question will remain to what extent oil and other commodities will return and how quick this will go. Maybe/likely we have already passed the point where some further indirect and second round inflation effects have affected the economic chain anyway. In that scenario, (some) central banks still have to adjust policy, especially if the feared for deceleration in activity would turn out to be more modest then feared. For now this is all no more ‘than hypothetical thinking’. The US and Iran reportedly are considering a short term memorandum that aims to end hostilities and resolve the (mutual) blocking of the Strait of Hormuz. Other key issues including Iran’s nuclear program, will have to be addressed in talks over the next months. Markets yesterday saw enough signs (especially from President Trump’s communication) to anticipate a positive outcome. Inflation and other risk premia declined substantially. This gain is easily maintained, even extended today, as the waiting game continues. Brent oil tries a new attempt to settle below the $100 p/b level (currently $97). EMU swap yields still decline between 4 (2-y) and 2.5 (30-y) bps. Markets have scaled back ECB rate hike expectations. A next step is only fully discounted for July (70% June) and markets see only slightly more than one additional step toward the end of the year. US yields in a similar move also ease between 3 bps (2-y) and 1 bp (30-y). Money markets still hold a highly agnostic view whether the next step of the Fed should be a rate hike or a rate cut. (US) data in the current context mostly have limited market impact. Still preliminary US Q1 Unit Labour Costs eased more than expected (2.3% ann from 4.6%). At the same time, weekly jobless claims remained very low. (200k). The focus now turns to tomorrow’s April US payrolls report. UK markets for now join the broader ‘easing’ rally (yield declines of 3.5-2.5 bps) as investors look out for any potential impact of today’s regional election on the position of PM Starmer (and on fiscal policy). Both US and EMU equity indices mostly hold yesterday’s gains, with limited, mixed moves today. The dollar softens further. Some technical support levels are nearby, but haven’t really been challenged yet (DXY at 97.85 with recent lows near 97.63; EUR/USD at 1.175 with wartime top at 1.1849). Minimal moves intraday in the ERU/GBP cross rate too (0.864)

News & Views

The Norwegian central bank surprised with a 25 bps rate hike to 4.25% today. Although it stated in March that such a move would be appropriate “at one of the forthcoming” meetings, not everyone assumed that it would be already be at the next one this month. Underpinning the decision was high and above-target inflation, rising energy prices and commodity prices in general as well as elevated wage growth all the while the economy operates near capacity with higher energy prices at least partially offsetting its negative economic impact. “High inflation over time can lead firms and households to plan for persistently high inflation. It may then become more difficult to bring inflation down again.” The Norges Bank responded by tightening policy further and stuck to its March guidance that projected rates going as high as 4.5% this year. Norwegian swap yields briefly rallied several bps, going against the broader trend, but failed to hold on to those gains. The NOK does appreciate to EUR/NOK 10.85.

Sweden’s policy rate, by contrast, was kept at 1.75% and is expected to remain there over the coming period. The Riksbank offered a dual risk assessment. The initial energy-related inflation could prompt a broad and persistent rise in other goods and services, warranting a potential monetary tightening. Risks of that happening have increased compared to the March meeting. At the same time, an already sluggish economy is performing weaker than expected and inflation came in well below expectations. Yesterday’s headline number eased to 0.8%, the lowest since December 2020 while the core gauge showed prices stagnating for the first time in three decades. The Riksbank said this means “there is scope to wait until there is a clearer picture of the effects of the war and the supply shocks it entails.” The Swedish krone shrugged at the decision with EUR/SEK trading little changed around 10.83.

Gold on the Rise

- The precious metal has benefited from rumours of a de-escalation of the conflict in the Middle East.

- The US and Japan may agree on coordinated currency interventions.

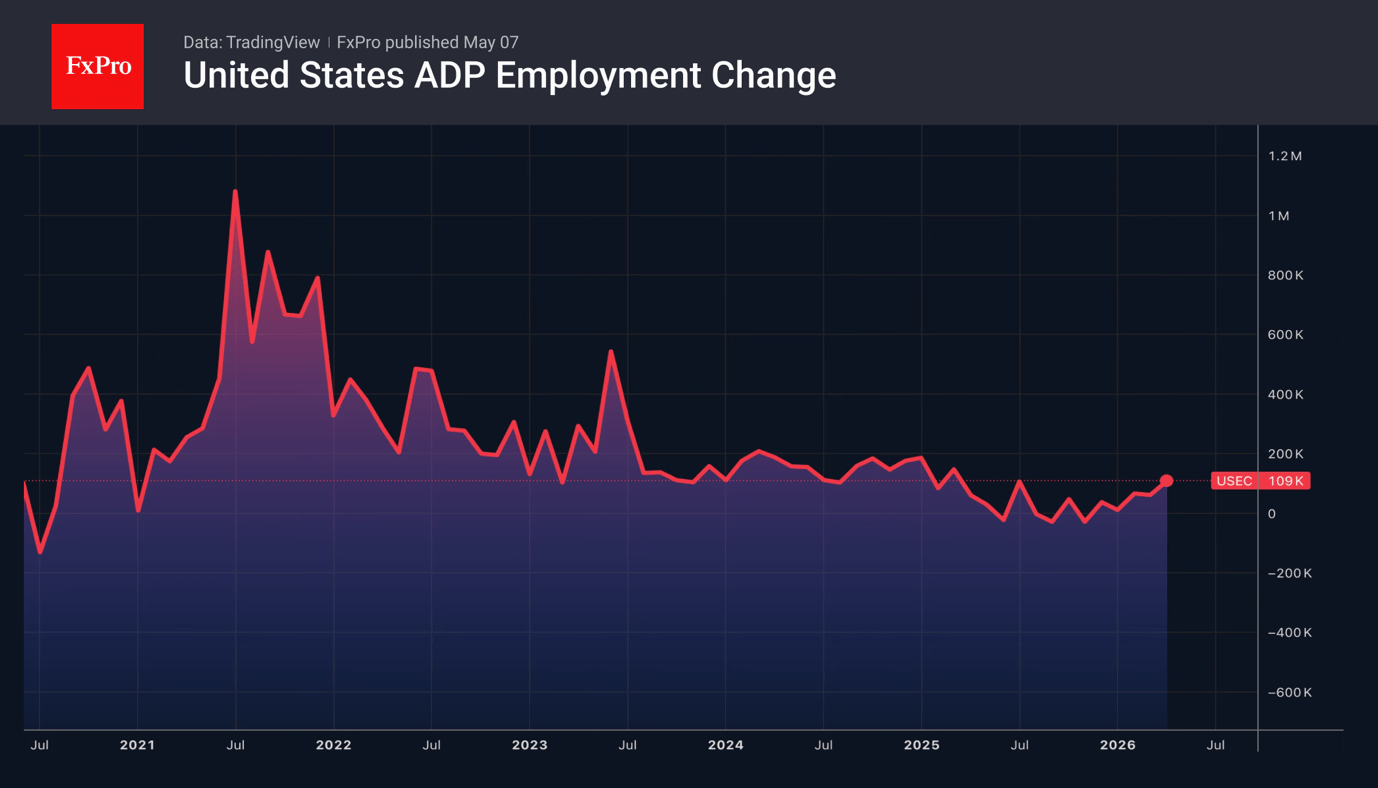

The US dollar bounced back from sellers amid doubts about a swift resolution to the Middle East conflict and positive US economic data. ADP reported a 109K increase in private sector employment in April, the best performance since the start of 2025. The stabilisation of the labour market against a backdrop of accelerating inflation allowed the DXY to rebound by 0.5% from the day’s lows, recouping half of its losses since the start of the day on Wednesday. However, this was short-lived.

The US and Iran are working to resume talks, which are due to take place by 15 May. Markets react first and ask questions later. Consequently, rumours of a de-escalation of the conflict in the Middle East initially pushed the EURUSD pair to its highest level since February, near 1.1800. However, subsequent doubts caused the pair to retreat.

Geopolitics will cause more pain for Europe than for the US. All the more so, as Donald Trump threatens to raise tariffs on European cars from 15% to 25%. The economic slowdown, coupled with rising inflation due to higher energy prices, is creating stagflationary risks, forcing the ECB to tread carefully. Even if rates are raised, it is unlikely to be by much. The differential will remain in favour of the Americans, limiting the upside potential of EURUSD.

Apart from geopolitics, the dollar has also been influenced by Japanese government actions. From a fundamental perspective, the US dollar is stronger than the yen. However, a successful market reversal in favour of a stronger yen and a weaker dollar could place a heavy burden on Tokyo. The White House may opt for coordinated intervention with many countries, following the Plaza Accord model of 1985. Scott Bessent intends to visit Japan to meet with Prime Minister Sanae Takaichi and Finance Minister Satsuki Katayama to discuss, among other things, the foreign exchange market.

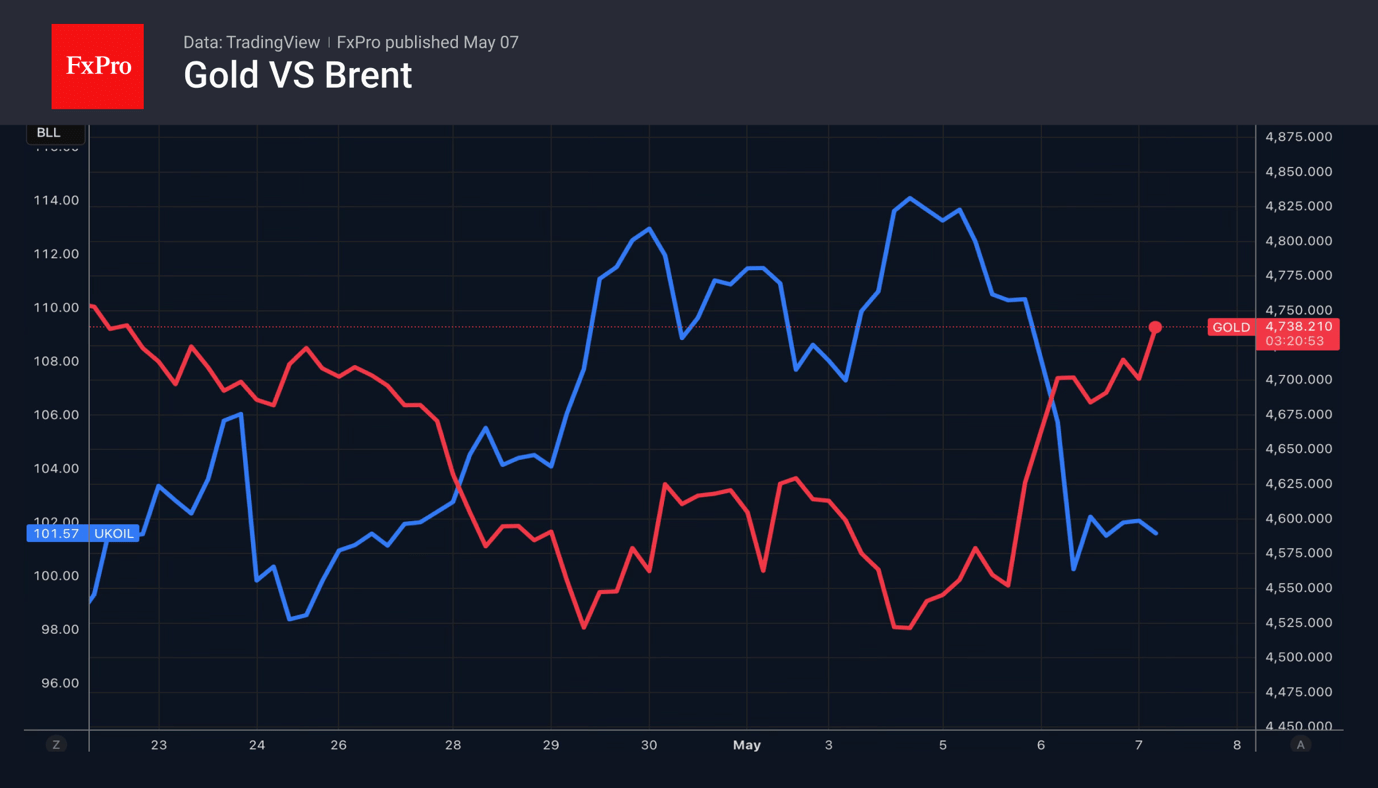

Rumours of de-escalation in the Middle East have allowed gold to post its best daily performance since late March. The precious metal is reacting sensitively to the market’s reduced inflation expectations following the fall in oil prices. This makes a Fed rate hike in 2026 inadvisable. If, however, official data on Friday disappoints, gold will gain fresh momentum.

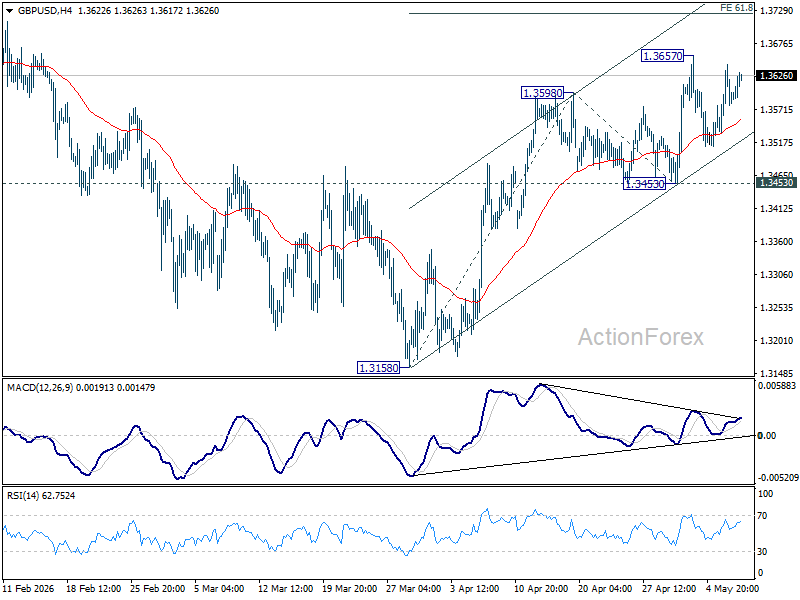

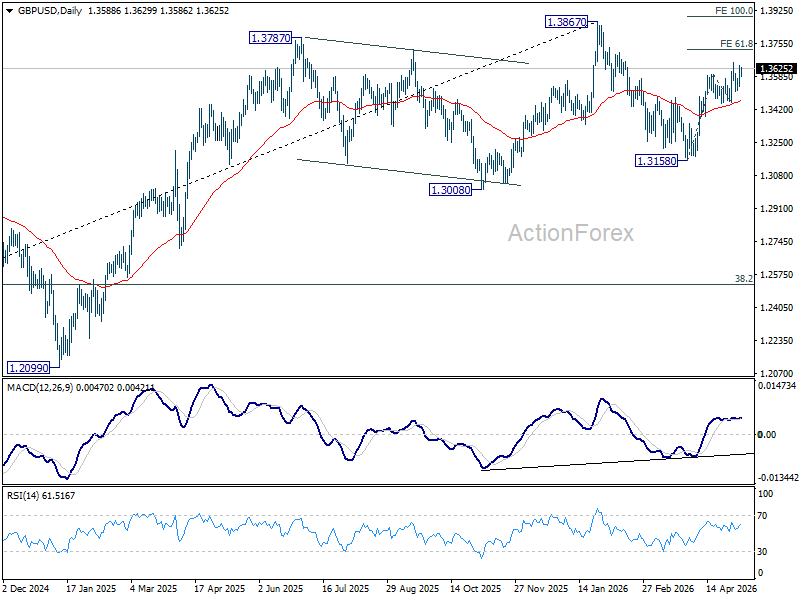

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3539; (P) 1.3591; (R1) 1.3646; More...

Outlook in GBP/USD remains unchanged as range trading continues. Intraday bias stays neutral, and further rise is expected with 1.3453 support intact. On the upside, above 1.3657 will target 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high. However, break of 1.3453 will turn bias back to the downside for 1.3158 support instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).

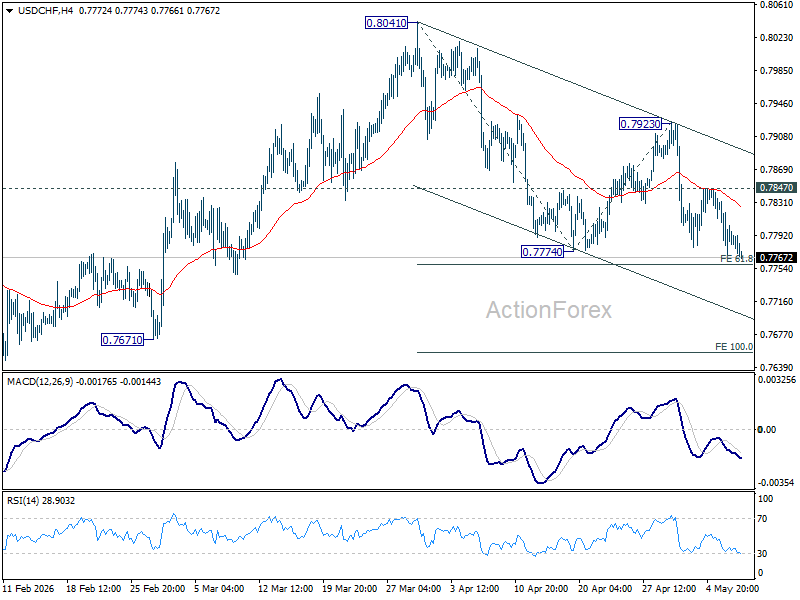

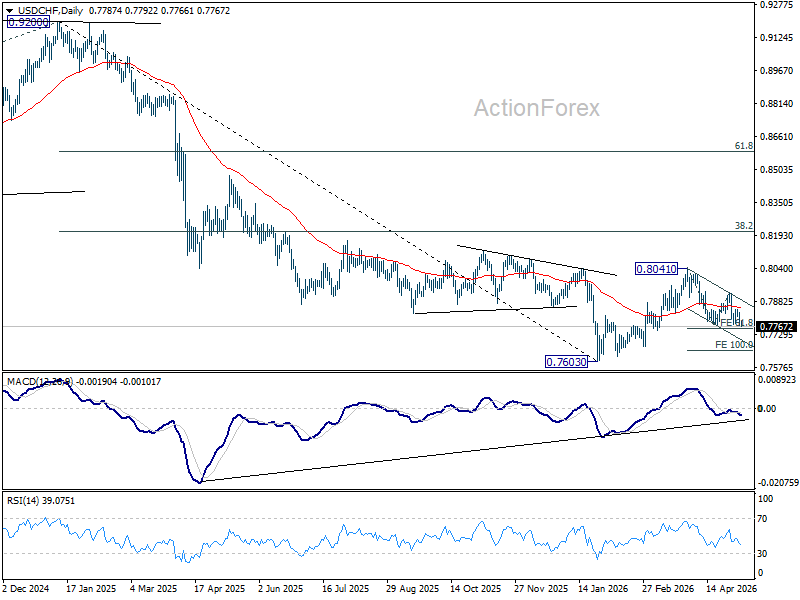

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7759; (P) 0.7801; (R1) 0.7829; More….

Intraday bias in USD/CHF stays on the downside for 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758. Firm break there will extend the fall from 0.8041 to 100% projection at 0.7656. On the upside, above 0.7847 minor resistance will turn bias neutral again.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8042) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

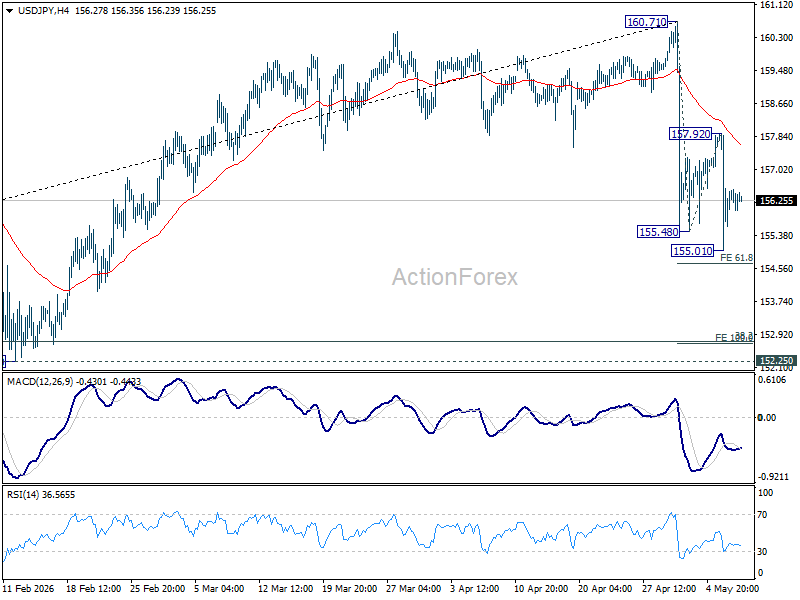

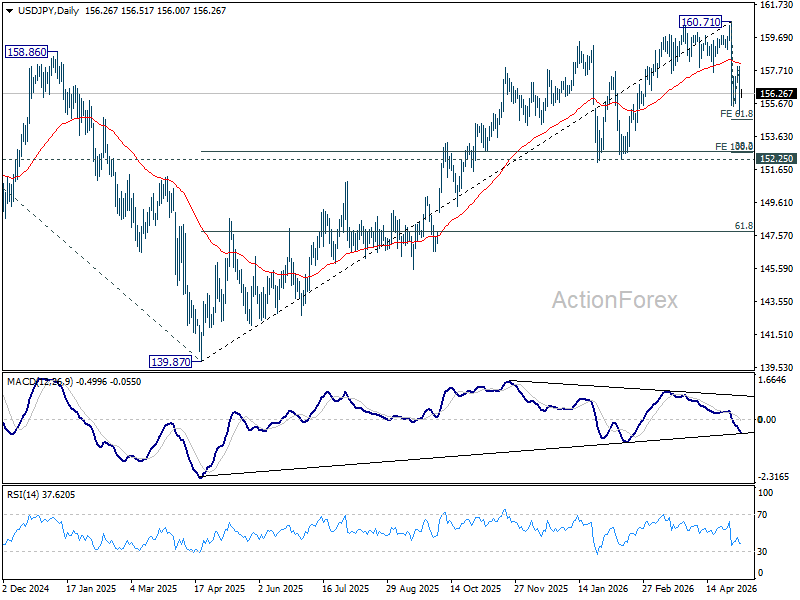

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.95; (P) 156.46; (R1) 157.90; More...

Intraday bias in USD/JPY is turned neutral first and some sideway trading could be seen. Risk will stay on the downside as long as 157.92 resistance holds. Below 155.01 will resume the fall from 160.71 to 61.8% projection of 160.71 to 155.48 from 157.92 at 154.68. Firm break there will target 100% projection at 152.69. That would be close to key 152.25 cluster support (38.2% retracement of 139.87 to 160.71 at 152.74).

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.01) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

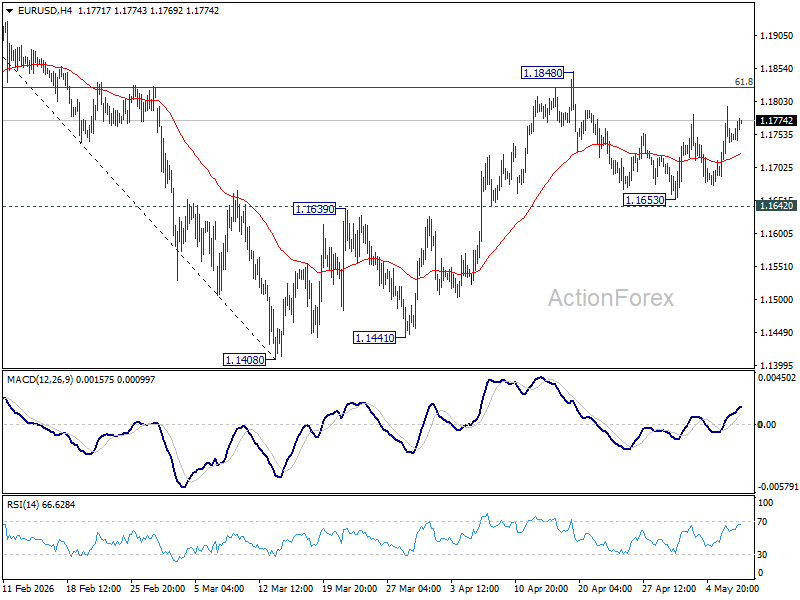

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1693; (P) 1.1746; (R1) 1.1801; More….

Outlook in EUR/USD is unchanged as range trading continues. Intraday bias remains neutral, and with 1.1642 support intact, rise from 1.1408 is expected to continue. On the upside, firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1537). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

From War Panic to Post-Conflict Positioning: Oil Falls, Silver Surges

Markets appear to be entering a new phase of post-conflict positioning, with oil prices falling again on hopes of a full reopening of the Strait of Hormuz while precious metals begin rebuilding bullish momentum. The sharp moves across commodities suggest investors are increasingly looking beyond the immediate US-Iran conflict and starting to reposition for a more normalized global macro environment.

The clearest signal is coming from oil markets. Brent crude extended its decline again today and broke below the $97 level, while WTI moved closer toward the key $90 handle. The price action suggests traders are becoming increasingly confident that the Strait of Hormuz could soon reopen fully to international shipping and energy flows if a peace agreement between Washington and Tehran materializes.

Oil traders now appear increasingly hopeful that commercial normalization could return to the region, allowing tankers to move freely again without disruption or informal “tolls” imposed by Iran’s Islamic Revolutionary Guard Corps on vessels passing through the Strait. That shift represents a major unwind of the geopolitical premium that had fueled the earlier oil surge.

Elsewhere, equities and currencies were notably calmer today after this week’s powerful risk-on rally. US stock futures traded largely steady following the record-breaking gains in S&P 500 and NASDAQ earlier in the week. Dollar also stabilized within recent ranges and appears to be awaiting a fresh directional catalyst from broader market sentiment.

Meanwhile, the strongest momentum today has shifted toward precious metals, particularly Silver. Silver surged above the psychologically important $80 mark, significantly outperforming Gold and reinforcing the idea that investors are increasingly rotating back into higher-beta opportunities rather than pure defensive positioning.

Some investors are already beginning to argue that the record-breaking bull markets in Gold and Silver could resume later this year if a durable US-Iran peace settlement is achieved and the temporary pressure from higher interest rates fades. Both metals posted extraordinary gains during 2025, with Gold surging 66% and Silver soaring 135%, before experiencing sharp and volatile corrections this year.

Recent declines in precious metals had been driven by fears of higher interest rates, a stronger Dollar linked to rising oil prices, and heavy position liquidation during periods of market stress. But as oil retreats and the inflation shock potentially eases, investors are revisiting the longer-term structural bullish case for metals.

That longer-term story remains centered on central bank diversification away from US government debt, persistent physical Silver supply tightness, and expanding demand tied to green energy technologies and AI infrastructure. In many ways, the US-Iran conflict may have strengthened rather than weakened those structural themes by reinforcing the strategic importance of energy diversification and renewable technologies.

For now, markets appear to be transitioning away from “war panic” and toward “post-conflict positioning.” Oil is pricing normalization, equities are consolidating record highs, and Silver’s breakout suggests investors are once again willing to chase higher-beta opportunities tied to long-term structural growth themes.

In the currency markets, for the week so far, Kiwi is the best performer, followed by Aussie, and then Swiss Franc. Loonie is the worst, followed by Dollar, and then Sterling. Euro and Yen are positioning in the middle.

In Europe, at the time of writing, FTSE is down -0.53%. DAX is down -0.05%. CAC is up 0.09%. UK 10-year yield is down -0.035 at 4.913. Germany 10-year yield is down -0.026 at 2.980. Earlier in Asia, Nikkei surged 5.58%. Hong Kong HSI rose 1.57%. China Shanghai SSE rose 0.48%. Singapore Strait Times rose 0.30%. Japan 10-year JGB yield fell -0.023 to 2.483.

Silver Breaks 80 as Markets Rotate From Defense to Offense

Silver’s breakout above 80 may be signaling a major shift in market psychology. As Iran de-escalation hopes fuel a global risk-on rally, investors are rotating away from defensive Gold positioning and into higher-beta opportunities, with Silver emerging as one of the clearest beneficiaries. Read More.

US Jobless Claims Edge Higher to 200k, Labor Market Still Stable

US jobless claims rose slightly last week, but the broader labor market picture remains stable. Continuing claims declined and trend measures improved, reinforcing the view that layoffs remain contained despite slower economic momentum and geopolitical uncertainty. Read More.

Eurozone Retail Sales Slip -0.1% mom in March as Fuel Demand Weakens

Eurozone consumer spending remains fragile. Retail sales slipped again in March as falling fuel and food purchases offset resilient non-food demand, while Germany’s sharp decline highlighted persistent weakness in the region’s largest economy. Read More.

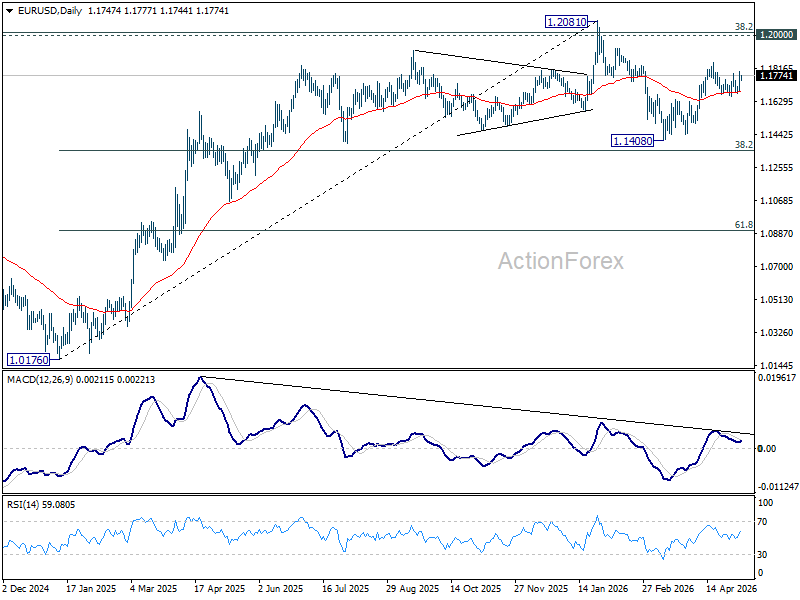

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1693; (P) 1.1746; (R1) 1.1801; More….

Outlook in EUR/USD is unchanged as range trading continues. Intraday bias remains neutral, and with 1.1642 support intact, rise from 1.1408 is expected to continue. On the upside, firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1537). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.