Sample Category Title

NFP Takes Back Seat as Hormuz Clash Keeps Markets on Edge

The US Non-Farm Payrolls report may be today’s headline event on the economic calendar, but markets are behaving as though the real story lies thousands of miles away in the Strait of Hormuz. For much of the past two days, investors had embraced a growing “peace trade,” betting that Washington and Tehran were moving closer to a deal that could end the conflict and fully reopen one of the world’s most critical energy chokepoints. Oil prices plunged, equities surged to record highs, and markets increasingly positioned for a post-conflict normalization phase.

But overnight events served as a reminder that the path toward peace remains highly unstable. Reports emerged that US and Iranian forces exchanged fire directly in the Strait of Hormuz, with both sides accusing the other of triggering the confrontation.

According to US Central Command, three American destroyers — USS Truxtun, USS Rafael Peralta, and USS Mason — intercepted coordinated drone and missile attacks while passing through the Strait late Thursday. Iran, meanwhile, accused Washington of violating the fragile ceasefire by striking multiple targets around the waterway earlier in the day.

The exchange suggests that the current situation is not yet a genuine normalization, but still a highly fragile form of managed confrontation. The deeper disagreement between Washington and Tehran remains unresolved. The core friction is not merely about ending military operations, but about Iran’s nuclear program itself.

Adding to tensions, US President Donald Trump renewed his threat of overwhelming military escalation if Iran refuses to sign the proposed agreement quickly. “Just like we knocked them out again today, we’ll knock them out a lot harder, and a lot more violently, in the future,” Trump warned overnight.

Yet despite the dramatic rhetoric and naval clashes, markets are not fully returning to panic mode. Instead, investors appear stuck between optimism and caution. US stocks only eased modestly overnight after recent record-breaking rallies, while Asian equities traded mildly lower. Major currency pairs also stayed trapped within yesterday ranges. Brent crude rebounded back to $100 after briefly collapsing to $96 yesterday. Gold also remained relatively steady around $4,700.

For the week so far, Kiwi is currently the strongest, followed by Aussie, and then Swiss Franc. Loonie is the worst, followed by Sterling, and then Dollar. Euro and Yen are positioning in the middle.

In Asia, at the time of writing, Nikkei is down -0.47%. Hong Kong HSI is down -1.14%. China Shanghai SSE is down -0.33%. Singapore Strait TImes is down -0.60%. Japan 10-year JGB yield is down -0.002 at 2.481. Overnight, DOW fell -0.63%. S&P 500 fell -0.38%. NASDAQ fell -0.13%. 10-year yield rose 0.03 to 4.39.

Dollar Faces Key NFP Test as Risk Sentiment Threatens Renewed Selloff

Today’s US payrolls report could determine whether the current risk-on rally keeps running. Markets are looking for a “Goldilocks” jobs number—soft enough to ease Fed pressure, but strong enough to avoid recession fears—which may leave Dollar vulnerable to renewed selling. Read More.

Japan Real Wage Growth Extends Gains Despite Slower Nominal Pay Growth

Japan’s real wages rose for a third consecutive month in March, supported by easing inflation and the strongest stretch of base pay growth in more than three decades. Read More.

Japan PMI Services Finalized at 51.0 as Middle East War Fuels Cost Pressures

Japan’s services sector lost momentum in April just as inflation pressures intensified sharply. Rising energy costs linked to the Middle East conflict pushed input prices to a three-and-a-half-year high and selling prices to their steepest increase in nearly two decades. Read More.

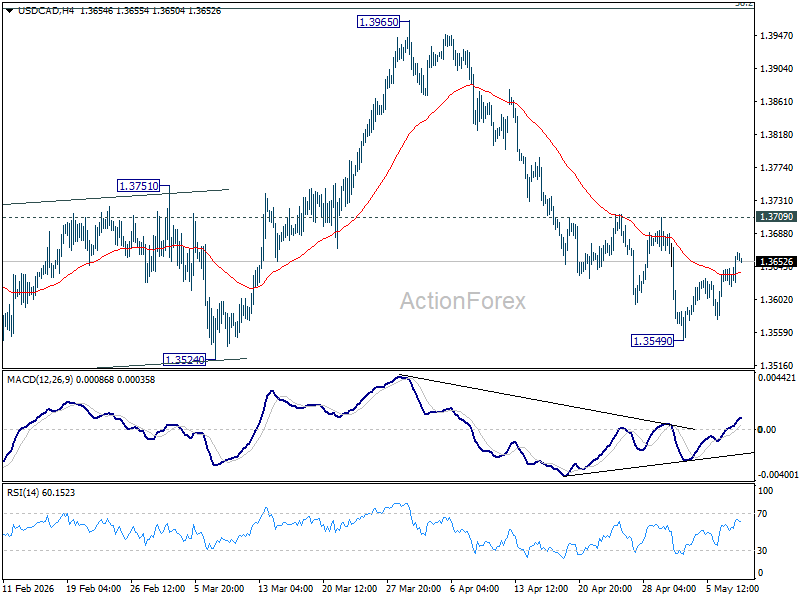

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3634; (P) 1.3651; (R1) 1.3683; More...

Intraday bias in USD/CAD remains neutral as consolidations continue above 1.3549. Further decline is expected as long as 1.3709 resistance holds. Below 1.3549 will resume the fall from 1.3965 to retest 1.3480 low. Decisive break there will resume whole down trend from 1.4791. However, firm break of 1.3709 will turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already.

Dollar Faces Key NFP Test as Risk Sentiment Threatens Renewed Selloff

Dollar is heading into today’s US payrolls report in a vulnerable position—not necessarily because the labor market is collapsing, but because markets are currently focused on risk appetite rather than pure Federal Reserve pricing.

Markets are expecting a sharp moderation in hiring after March’s surprisingly strong 178k payroll gain. Consensus forecasts point to job growth around 60k–65k in April, with the unemployment rate seen holding steady at 4.3%. Average hourly earnings are expected to rise 0.3% mom, while annual wage growth is projected to ease slightly toward the 3.5%–3.7% range.

Ironically, that softer range may actually be exactly what risk markets want. A “Goldilocks” payrolls report—cooler but not recessionary—could remove another layer of macro uncertainty and allow the powerful global risk-on rally to continue running.

| Indicator | March | April Forecast |

|---|---|---|

| Non-Farm Payrolls | +178k | +60k to +65k |

| Unemployment Rate | 4.3% | 4.3% |

| Average Hourly Earnings (MoM) | +0.3% | +0.3% |

| Average Hourly Earnings (YoY) | ~3.8% | 3.5%–3.7% |

The key complication is that leading indicators are not fully supporting the slowdown narrative. ADP private employment rebounded strongly to 109k from 61k previously, while the four-week average of initial jobless claims fell back toward historically low levels around 203k. ISM Services employment also remained in expansion territory at 53.6. The main soft spot came from ISM Manufacturing employment, which slipped further into contraction at 46.4. The broader labor market picture still looks resilient enough to create upside surprise risk for the headline payrolls number.

| Indicator | Latest Reading | Signal |

|---|---|---|

| ADP Employment | 109k | Stronger than expected |

| ISM Manufacturing Employment | 46.4 | Contraction |

| ISM Services Employment | 53.6 | Expansion |

| 4-Week Avg Initial Claims | 203k | Historically low |

But the bigger issue for markets may not be the jobs number itself. NFP trading is often less about economics and more about positioning psychology. The initial one-to-five-minute spike after release is frequently dominated by algorithmic stop-hunting and violent reversals. The more important move usually emerges later, during the so-called “NFP drift,” when traders digest revisions, wage growth, and what the data actually means for the broader market environment.

That environment currently remains heavily tilted toward risk-taking. Equities continue hovering near record highs as investors increasingly price a de-escalation in the US-Iran conflict, lower oil prices, and a broader normalization of global conditions. In that context, even a moderately soft payrolls report may be interpreted positively if it reduces fears of renewed Fed hawkishness without triggering recession concerns.

That creates an unusual setup for Dollar. Under normal circumstances, stronger payrolls would support the greenback through higher yields and tighter Fed expectations. But today, stronger data could simply reinforce risk appetite and encourage more flows into equities and higher-beta currencies instead. Conversely, a modestly softer report may weaken Dollar directly by supporting the view that the Fed can eventually pivot without the economy collapsing.

Technically, Dollar Index's recent decline from 100.64 has stabilized temporarily just ahead 61.8% retracement of 95.55 to 100.64 at 97.49. But the broader near-term trend still favors further downside while 99.09 resistance holds. Decisive break below 97.49 could trigger another leg lower toward the 95.55 area.

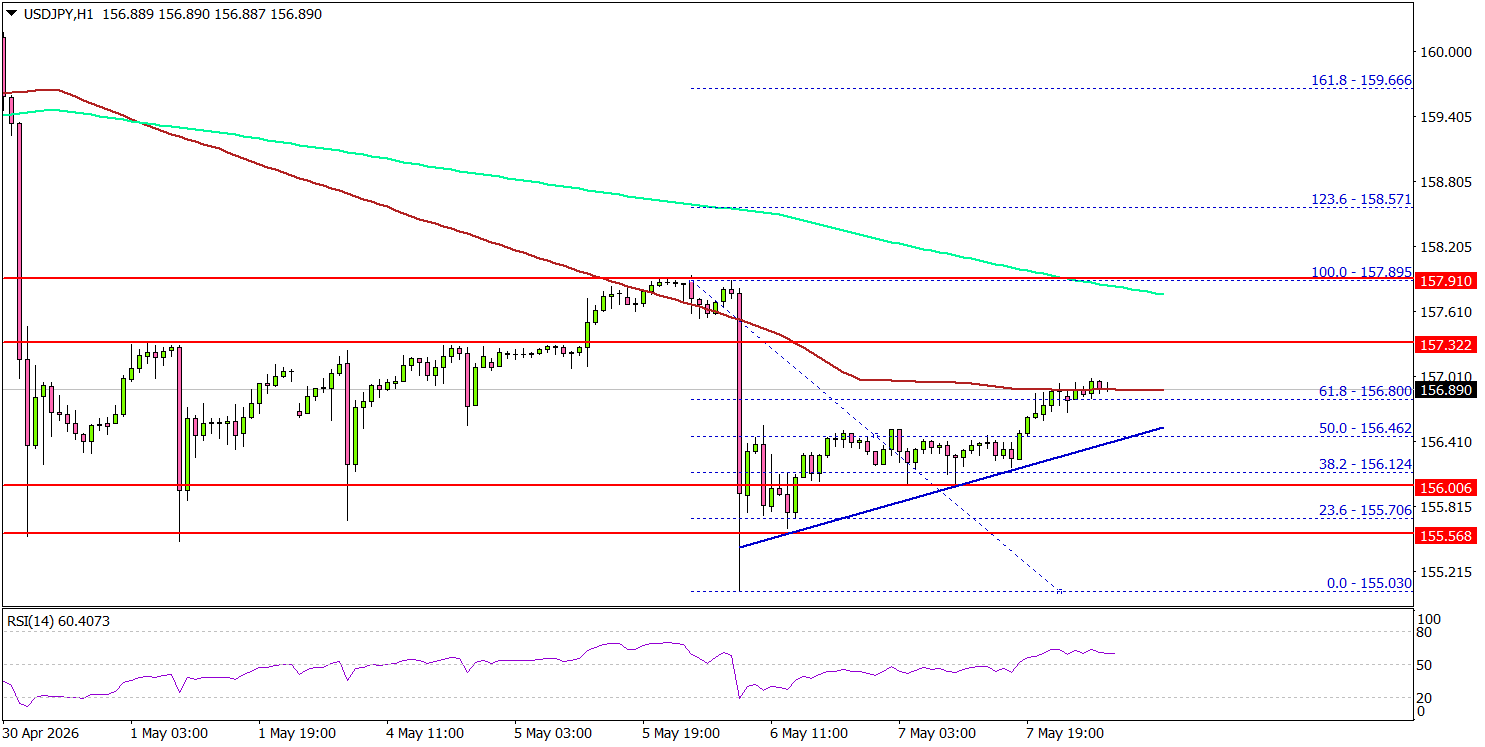

USD/JPY Recovery Strengthens As Markets Await Key NFP Catalyst

Key Highlights

- USD/JPY started a recovery wave from the 155.00 support zone.

- A bullish trend line is forming with support at 156.45 on the 4-hour chart.

- EUR/USD is now at risk of a downside break below 1.1700.

- The US nonfarm payrolls could change by 62K in April 2026.

USD/JPY Technical Analysis

The US Dollar found support near 155.00 against the Japanese Yen. USD/JPY started a recovery wave above 155.50 and 156.00.

Looking at the 4-hour chart, the pair cleared the 50% Fib retracement level of the downward move from the 157.89 swing high to the 155.03 low. The pair is now trading above the 100 simple moving average (red, 4-hour), but it is still well below the 200 simple moving average (green, 4-hour).

On the upside, the pair faces resistance at 157.00. The first major resistance sits at 157.20 and the 76.4% Fib retracement level of the downward move from the 157.89 swing high to the 155.03 low.

The main resistance could be 158.0. A close above 158.00 could open doors for gains above 158.80. In the stated case, the bulls could aim for a move to 159.20.

Immediate support is seen near 156.40. The next support could be 156.00. A close below 156.00 might push the pair toward 155.50. Any more losses could initiate a fresh move to 152.00 in the coming days.

Looking at EUR/USD, the pair failed to stay above 1.1750 and now remains at risk of more losses below 1.1700.

Upcoming Key Economic Events:

- US nonfarm payrolls for April 2026 – Forecast 62K, versus 178K previous.

- US Unemployment Rate for April 2026 - Forecast 4.3%, versus 4.3% previous.

Japan Real Wage Growth Extends Gains Despite Slower Nominal Pay Growth

Japan’s real wages rose 1.0% yoy in March, marking the third consecutive monthly increase as moderating inflation helped household purchasing power improve. The data suggest that wage growth is increasingly starting to outpace consumer price pressures, supporting hopes for a more sustainable recovery in domestic demand.

Nominal wages increased 2.7% yoy, extending gains to a 51st straight month, though the pace slowed from February’s 3.4% yoy increase. Scheduled earnings, which include base pay and family allowances, rose 3.2% yoy, marking the first time in more than 33 years that regular pay growth has exceeded 3% for three consecutive months. Overtime pay also increased 1.9%, while special payments such as bonuses fell -1.5%.

Consumer inflation used in the wage calculation slowed to 1.6%, staying below 2% for a third straight month thanks partly to government utility and gas subsidies.

A labor ministry official said authorities do not yet see a significant impact from the Middle East conflict on wages or prices but are monitoring developments closely.

The figures are likely to support the BoJ’s view that a positive wage-price cycle is gradually taking hold, though uncertainty tied to rising energy costs remains an important risk.

| Indicator | Previous | Latest |

|---|---|---|

| Real Wages (YoY) | +1.0% | +1.0% |

| Nominal Wages (YoY) | +3.4% | +2.7% |

| Scheduled Pay (YoY) | +3.0% | +3.2% |

| Overtime Pay (YoY) | — | +1.9% |

| Special Payments (YoY) | — | -1.5% |

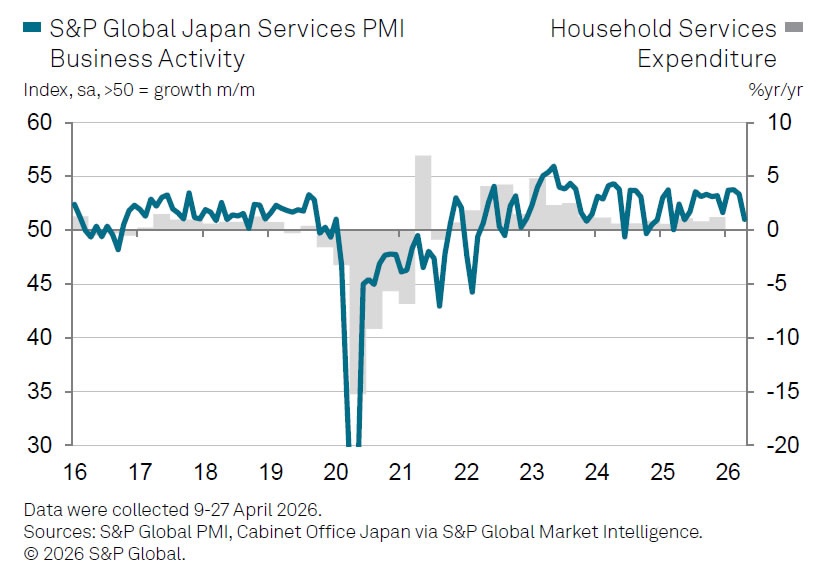

Japan PMI Services Finalized at 51.0 as Middle East War Fuels Cost Pressures

Japan’s service sector growth slowed notably in April as the impact of the Middle East conflict weighed on demand and business confidence, while sharply higher costs pushed inflation pressures to near-record levels. PMI Services was finalized at 51.0, down from 53.4 in March, while PMI Composite eased to 52.2 from 53.0, pointing to softer overall private-sector momentum after a strong start to 2026.

The slowdown was concentrated in the services sector, where business activity growth weakened to an 11-month low amid a softer rise in new orders. According to S&P Global, overseas demand for Japanese services also declined again, adding further pressure to momentum. In contrast, manufacturers reported the fastest increase in output in more than 12 years, partly reflecting front-loading activity linked to disruptions and uncertainty caused by the Middle East war.

At the same time, inflation pressures accelerated sharply across the economy. Input costs rose at the fastest pace in three-and-a-half years as higher energy and commodity prices fed through supply chains. Firms responded by raising selling prices at the steepest pace in nearly two decades of data collection, reinforcing concerns that official inflation could accelerate further in coming months.

Business sentiment also deteriorated noticeably. Companies cited ongoing uncertainty surrounding the Middle East conflict, rising costs, and concerns about weaker customer demand. Optimism for the year ahead fell to its lowest level since the COVID-19 pandemic in August 2020, highlighting growing anxiety that Japan may face a more difficult balance between slowing growth and rising inflation pressures later this year.

| Indicator | March | April Final |

|---|---|---|

| PMI Services | 53.4 | 51.0 |

| PMI Composite | 53.0 | 52.2 |

| Indicator | Details |

|---|---|

| Input Costs | Fastest increase in 3.5 years |

| Selling Prices | Steepest rise in nearly 20 years |

| Main Driver | Higher energy and commodity prices |

Cliff Notes: Dynamic Risks

Key insights from the week that was.

In an 8-1 vote, the RBA Monetary Policy Board (MPB) delivered its third consecutive rate hike, raising the cash rate by 25bps to its prior peak of 4.35%. The MPB stated that “the conflict in the Middle East has resulted in sharply higher fuel and related commodity prices” and that “this is likely to have second-round effects on prices for goods and services more broadly.” Inflation is now expected “to remain above target for some time”. The MPB are also attune to the risk of “price rises get[ting] built into longer term inflation expectations” in the event of a longer, or more severe, conflict.

In a video update midweek, Chief Economist Luci Ellis noted that Governor Bullock’s press conference was a bit more dovish than we had anticipated, with the last three hikes framed as giving some space for the MPB to assess how the risks evolve. That said, the staff’s forecasts – which are predicated on an assumption of around one-and-a-half more rate hikes – have underlying inflation peaking at 3.8%yr in Q2 2026 and not returning to target until the end of its forecast horizon at June 2028. Inflation risks are firmly skewed towards a higher peak and potentially a slower return to target. We therefore continue to expect another two rate hikes from the RBA in coming months. But, given Governor Bullock’s somewhat more cautious tone, we admit the case for June is now more finely balanced.

Rate hikes already look to be having an effect on the housing market, with national dwelling price growth slowing from a monthly pace of 0.6% in January to 0.2% in April. Performance across the capital cities is mixed, with prices down in Sydney and Melbourne prices but still rising in Brisbane, Adelaide and Perth. While a firming uptrend for dwelling approvals bodes well for supply, cost pressures stemming from the Middle East conflict will likely cause delays and some second thoughts on projects planned but not commenced.

Trends across other parts of the economy are also starting to shift. The ABS’ nominal household spending indicator bounced 1.6% in March on account of higher fuel costs, mirroring our own consumer card activity data. Abstracting from price effects, we expect real consumption to gain 0.6% in Q1; however, outside of fuel and electricity (buoyed by the rebate roll-off), the spending pulse looks faint. This speaks to the more challenging economic outlook taking hold across the nation, particularly in non-mining states where revenue constraints and higher expenses provide less scope for fiscal support.

Before moving offshore, a final note on trade. Unlike the shocks of recent years which benefitted Australia’s net trade position, recent data revealed the nominal goods trade surplus buckled into deficit in March for the first time since 2017. Higher fuel import costs (+37.4%) and volatility in gold played important roles. But the chief culprit behind the surprise was a remarkable surge in data processing machine imports, up $2.9bn or 300% in the month. While noisy and likely a wash for GDP – being offset by inventories or investment – this is clear evidence of the global AI investment drive reaching Australia’s shores.

Offshore, markets have been pre-occupied by developments in the Middle East. At the beginning of the week, President Trump announced Project Freedom, an initiative to provide safe passage through the Strait of Hormuz to ships stuck in the Persian Gulf. As soon as the operation commenced though, skirmishes were seen between the US and Iranian military. UAE energy infrastructure was also targeted.

The US did not retaliate, however, instead referencing an end to the offensive portion of this war. And, within two days, Project Freedom was suspended indefinitely to make way for further intermediated negotiations. Reports suggest progress has been made, albeit without detail. Iran is arguably coming under greater pressure to make a deal, with China’s Foreign Minister emphasising this week the need for a quick end to the conflict and re-opening of the Strait while meeting Iran’s Foreign Minister. The timing of this development is not a surprise considering President Trump and President Xi are due to meet mid-month.

Data releases were uneventful this week. The ISM services index for April eased slightly to 53.6. The new orders index fell 7.1pts to 53.5, slightly below its 10-year pre-COVID average, and the employment indicator rose 4pts but remained weak versus history. The latest JOLTS job openings data and ADP private payrolls release were broadly consistent with balance between labour demand and supply. For the FOMC, this will keep the focus on inflation risks. Guidance given by FOMC members this week was consistent with this view.

A full update on our expectations for the global economy, Australia and New Zealand will be released later today on Westpac IQ in our May Westpac Market Outlook.

Crude Oil on Path to $90 as the Peace Trade Continues – WTI Technical Analysis

- WTI Oil took a significant hit throughout yesterday's session as Axios revealed a more US-Iran deal under construction, and these flows are extending in today's session

- Confirming its price action below $100, sellers are attempting a push towards $90. Will momentum be enough to break the key level?

- Exploring an in-depth Technical Analysis of the commodity

WTI Crude Oil dropped sharply yesterday after Axios reported that the US and Iran are working on a broad peace deal. The strong selling pressure is continuing into today.

After falling 8% yesterday, WTI is down another 5% today. Sellers are clearly getting in control of the market.

For months, prices rose steadily due to geopolitical tensions. Now, the trend has quickly shifted to a clear downward move. Now that prices have dropped below the key $100 level, the pressure is falling, and sellers are pushing toward $90.

The main question is whether this momentum will break that important support, as momentum becomes slightly oversold and Participants will look to confirm the latest narratives.

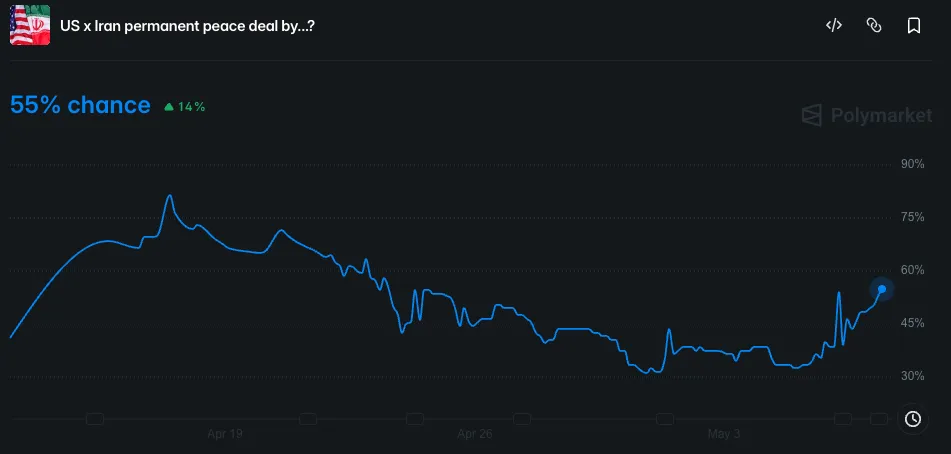

Peace Deal odds for June 30 – Source: Polymarket

The prediction-market odds US-Iran peace deal by June 30 are currently around 55% after remaining around 30% for a while – A peace deal by May 31 is quite optimistic, but the odds are also rising above 40%.

Traders are selling oil mainly because negotiations are moving toward an agreement to reopen the Strait of Hormuz, as confirmed by a report from Al Arabiya . Allowing normal shipping through this key route is a major reason for the drop in oil prices.

But for oil to fall another $20 and for gas prices to drop for consumers, a formal deal still needs to be signed.

This possible peace will need to be confirmed during the coming weeks of diplomatic talks, which recent statements have hinted at – With the much anticipated Trump-Xi meeting taking place next week, this could be an important date for the Oil Market.

Now, let's take a closer look at the technical analysis for WTI Crude to see if sellers can push prices below the $90 support level.

US Oil Intraday Timeframe Analysis

WTI 4H Chart and Technical Levels

WTI Oil 4H Chart – May 7, 2026. Source: TradingView

WTI has officially formed a decent looking top, with a lower high throughout the past week leading to the ongoing tumble, down 19% since its April 29 top.

Now breaking the key $93 Pivot zone with momentum, establishing below this area will be essential to confirm more downside ahead.

Higher timeframe traders will want to see a break and close below $90 to confirm.

WTI Technical Levels:

Resistance Levels

- Momentum Support now pivot $93 - $95 (breaking)

- $98 to $100 Pivotal Resistance

- $104 next-mini resistance (morning highs!)

- 2022 and Monday highs $117 to $120 (larger channel top)

Support Levels

- $90 Psychological level and past session's lows

- $87 to $90 mini-Support

- $82 Friday 17 lows

- 2025 Highs Key Support $78 to $80

1H Chart and Action Levels

WTI Oil 1H Chart – May 7, 2026. Source: TradingView

Swing trading such erratic Markets remain a fantasy, hence it could always be wiser to capture quick moves and re-assess with the news.

The action is currently oversold on most shorter timeframes, a reason why the selloff has somewhat stalled in the last hour. But Traders should still look at these elements:

- As long as the price action remains below $94.00, bears remain in control.

- Watch out for minor upside consolidation around here; if the action stays stuck below the level, this adds to odds of a downside break.

- The selloff should accelerate if heavy volume sales occur below $90.

- Breaking back above $95 would hint at more rangebound or rallying action ahead (all the way to $103)

Safe Trades and Keep your eyes on the news!

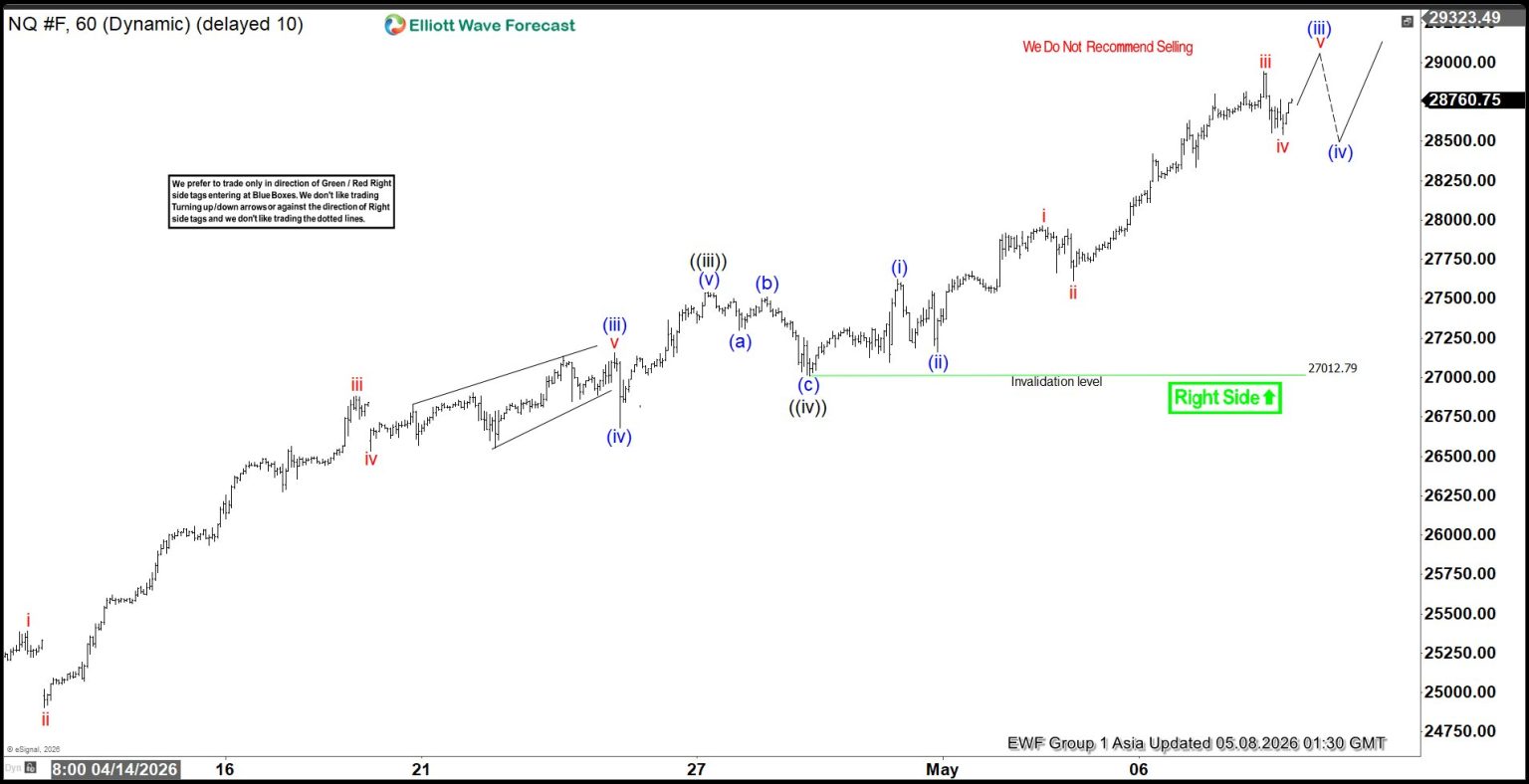

Elliott Wave View: Nasdaq Futures (NQ) Cycle Maturing from March 2026 Low

The short‑term Elliott Wave analysis of Nasdaq Futures (NQ) suggests the Index is close to completing its cycle from the March 31, 2026 low. The rally from that level has developed into a five‑wave impulsive structure, which is typical of a strong upward trend. Wave ((i)) concluded at 24,348.25, followed by a corrective decline in wave ((ii)) that ended at 23,666. The Index then advanced in wave ((iii)) to 27,542.5 before retracing in wave ((iv)), which terminated at 27,012.79.

Wave ((v)) is now unfolding and subdivides into a smaller five‑wave impulse, consistent with Elliott Wave principles. From the end of wave ((iv)), wave (i) advanced to 27,622.75, while wave (ii) corrected to 27,163.25. The Index is expected to push higher through waves (iii), (iv), and (v), completing wave ((v)) of 1 at a larger degree. Once this sequence finishes, a corrective wave 2 should emerge, retracing part of the cycle that began on March 31. This correction would provide consolidation before the Index resumes its upward path. In the near term, as long as price remains above 27,012.79, Nasdaq Futures retain potential for further upside. Traders should anticipate that once the five‑wave sequence of wave ((v)) concludes, a larger degree pullback will likely follow.

Nasdaq Futures (NQ) 60-Minute Elliott Wave Chart

NQ Elliott Wave Video:

https://www.youtube.com/watch?v=9tHHD_W0m4s

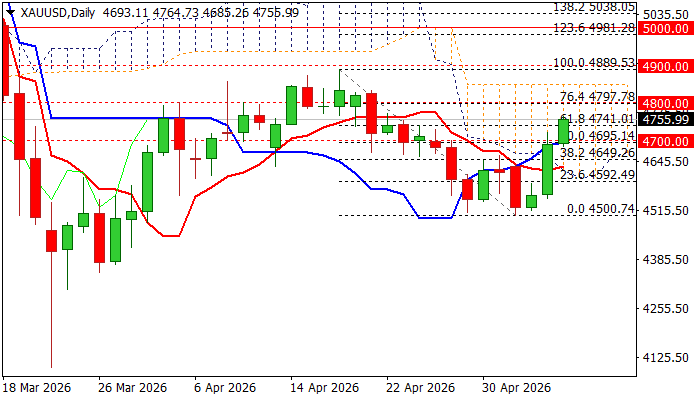

Gold Hits Two-Week High as Dollar/Crude Prices Fall on Growing Peace Optimism

Gold advanced 5% in past three sessions and hit two-week high on Thursday, as fresh waves of optimism about potential end of US-Iran war revived risk appetite and deflated prices of crude oil and dollar.

The metal rose further on Thursday, extending Wednesday’s 3% rally (the biggest daily gain since Mar 31, when bulls penetrated and closed within thick daily cloud) rising above $4700 (round-figure) and breaking Fibo 61.8% of $4889/$4500 ($4741).

Daily studies have improved on completion of higher base at $4500 zone and formation of reversal pattern on strong three-day rally, although caution is required as daily MAs are in mixed setup and 14-d momentum is still in negative territory.

Extension and close above $4741 Fibo level and nearby 100DMA ($4775) is needed to further strengthen near-term structure for attack at pivotal barriers at $4800 (round-figure and daily cloud top ($4848).

However, most of focus should remain on developments in geopolitics, as one of key factors that influence the price action nowadays.

Res: 4775; 4800; 4848; 4889

Sup: 4741; 4700; 4649; 4632

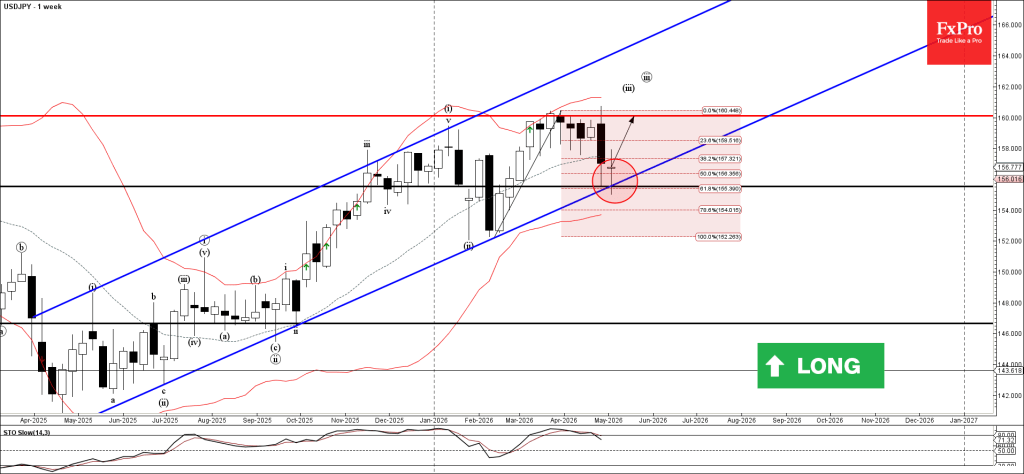

USDJPY Wave Analysis

USDJPY: ⬆️ Buy

- USDJPY reversed from support zone

- Likely to rise to resistance level 160.00

USDJPY currency pair recently reversed up from the support zone between the support level 155.5, support trendline of the weekly up channel from the start of 2025 and the 61.8% Fibonacci correction of the upward impulse from February.

The upward reversal from this support zone continues the active minor impulse wave iii from the start of this year.

Given the strong daily uptrend, USDJPY currency pair can be expected to rise to the next resistance level 160.00 (which has been reversing the pair from March).