Sample Category Title

US Payrolls Beat Expectations With 115k Growth, But Wage Growth Stays Calm

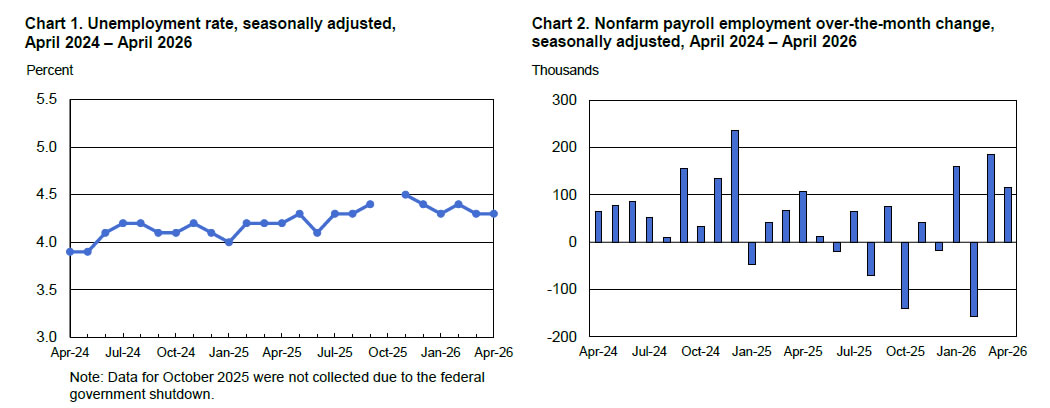

US job growth slowed in April but remained significantly stronger than expectes. Non-Farm Payrolls increased by 115k during the month, comfortably above consensus forecasts near 60k, while March payrolls were revised higher from 178k to 185k.

The unemployment rate held steady at 4.3% as expected, although the labor force participation rate edged lower from 61.9% to 61.8%. The labor market continues to show resilience despite elevated interest rates and heightened geopolitical uncertainty.

Wage growth was relatively contained. Average hourly earnings rose 0.2% mom for a second consecutive month, undershooting expectations for a 0.3% increase. On an annual basis, wage growth ticked up from 3.4% yoy to 3.6% yoy.

| Indicator | Previous | Latest | Expectation |

|---|---|---|---|

| Non-Farm Payrolls | 185k | 115k | 60k |

| Unemployment Rate | 4.3% | 4.3% | 4.3% |

| Participation Rate | 61.9% | 61.8% | — |

| Avg Hourly Earnings (MoM) | +0.2% | +0.2% | +0.3% |

| Avg Hourly Earnings (YoY) | +3.4% | +3.6% | +3.8% |

Chart Alert: Nasdaq 100 Bulls Still in Control Above 28,280 Key Support Amid US-Iran Tensions

Key takeaways

- Nasdaq 100 remains in a bullish structure despite short-term volatility driven by US–Iran geopolitical tensions and profit-taking, with price action stabilising above key support at 28,280.

- Market sentiment was briefly pressured by conflict-related headlines, but losses were largely recovered as ceasefire stability expectations improved and risk appetite returned.

- Market breadth is healthy but not euphoric, with broad participation across components and technical indicators supporting near-term upside continuation.

The US stock market saw profit-taking on Thursday, 7 May 2026, as traders grew increasingly concerned over the fragility of the month-long US-Iran ceasefire after both sides exchanged fire.

Market sentiment was further unsettled by uncertainty surrounding Washington’s latest proposal to Iran to reopen the Strait of Hormuz, which Tehran has yet to respond to.

The leading Nasdaq 100 dropped by 1.3% intraday from its all-time intraday high of 28,825, but trimmed its losses to end Thursday’s US session with a marginal loss of only 0.1% and underperformed against other US stock indices; S&P 500 (-0.4%), Dow Jones Industrial Average (-0.6%), and small-cap Russell 2000 (-1.6%).

In today's (Friday, 8 May 2026), the Nasdaq 100 E-min futures recovered by 0.5% at this time of writing and almost recovered Thursday’s US session losses, reinforced by US President Trump's remarks that stated the ceasefire agreement “remains intact”.

Aside from this piece of “Trump’s positive news flow”, several technical elements are also advocating for another potential round of fresh short-term bullish impulsive up move sequence for the Nasdaq 100.

Let’s decipher them.

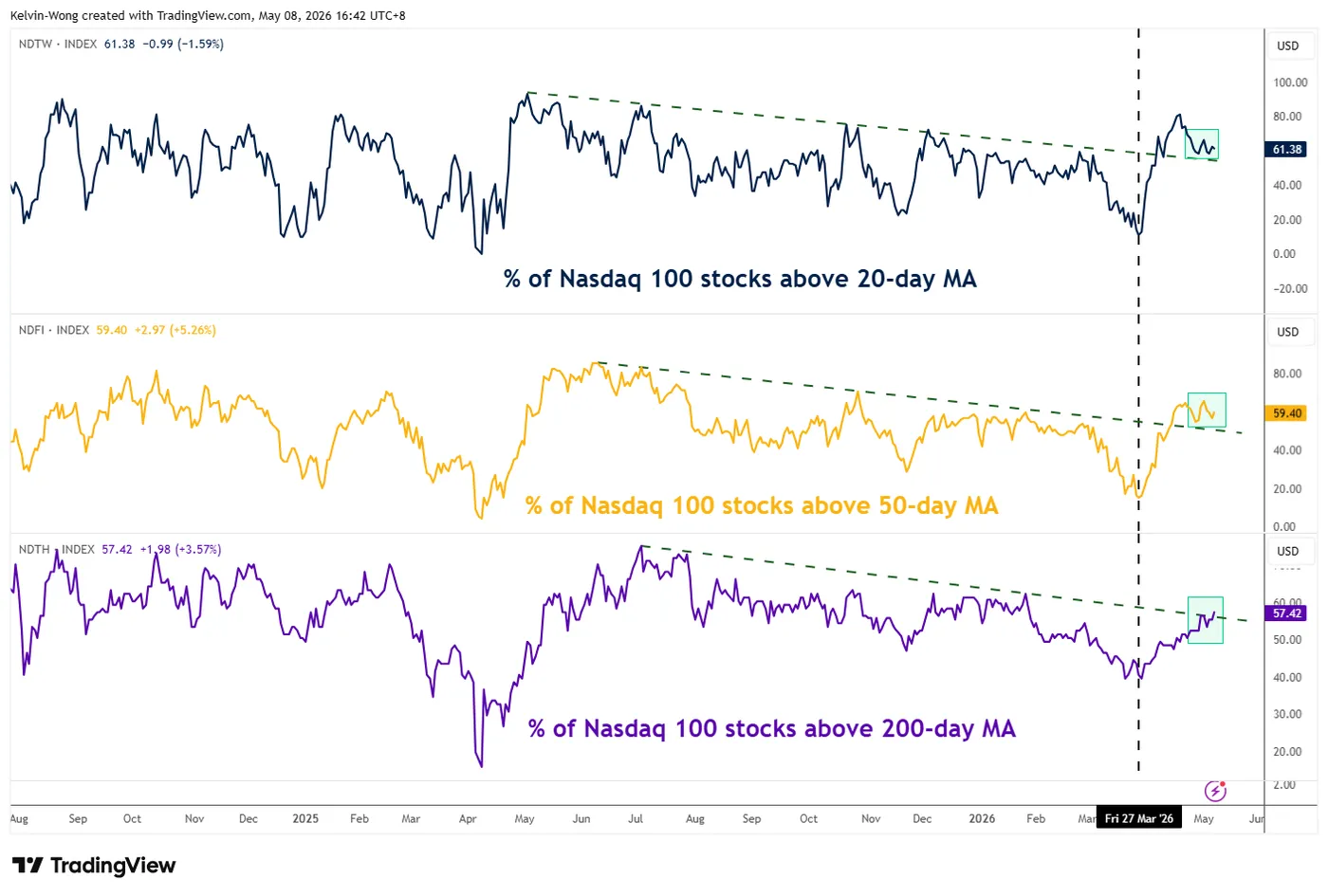

Nasdaq 100’s Market Breadth Remains Healthy, Not Euphoric

Fig. 1: Nasdaq 100 component stocks above 20-day, 50-day & 200-day moving averages as of 7 May 2026 (Source: TradingView).

Even though in the past four weeks, the performance of the Nasdaq 100 has been primarily driven by several AI-related semiconductors and chip stocks such as Intel (+111%), SanDisk (+87%), and Advanced Micro Devices (+87%), the percentage of Nasdaq 100 component stocks trading above their respective 20-day and 50-day moving averages is steady at 61% and 59%, not yet at euphoric levels of 80%-90%.

In addition, the percentage of Nasdaq 100 component stocks trading above the key 200-day moving averages has increased steadily from 47% on 15 April 2026 to 57% as of Thursday, 7 May 2026 (below euphoric levels of 80%-90%), which indicates that a broader set of Nasdaq 100 is taking part in this ongoing rally since the end of March 2026 (see Fig. 1).

Let's now focus on the short-term trajectory (1 to 3 days) of the US Nasdaq 100 CFD index (a proxy of the Nasdaq 100 E-mini futures).

Nasdaq 100 – Looking to Break Above 28,890 with Bullish Momentum

Fig. 2: US Nasdaq 100 CFD index minor trend as of 8 May 2026 (Source: TradingView).

Trend bias: Bullish above 28,280 short-term pivotal support within an uptrend phase (see Fig. 2).

Resistances: 28,860/890, 29,150, and 29,505/615

Next supports: 27,850, 27,540, and 27,255

Key Elements to Support the Near-Term Bullish Bias on the Nasdaq 100

- Price actions continue to oscillate within a medium-term ascending channel from the 31 March 2026 low.

- Current price actions of the Nasdaq 100 CFD index are trading at the upper half of the ascending channel, with the upper boundary of the channel coming in at around 29,505.

- The hourly MACD trend indicator has just flashed out a bullish crossover condition above its centreline.

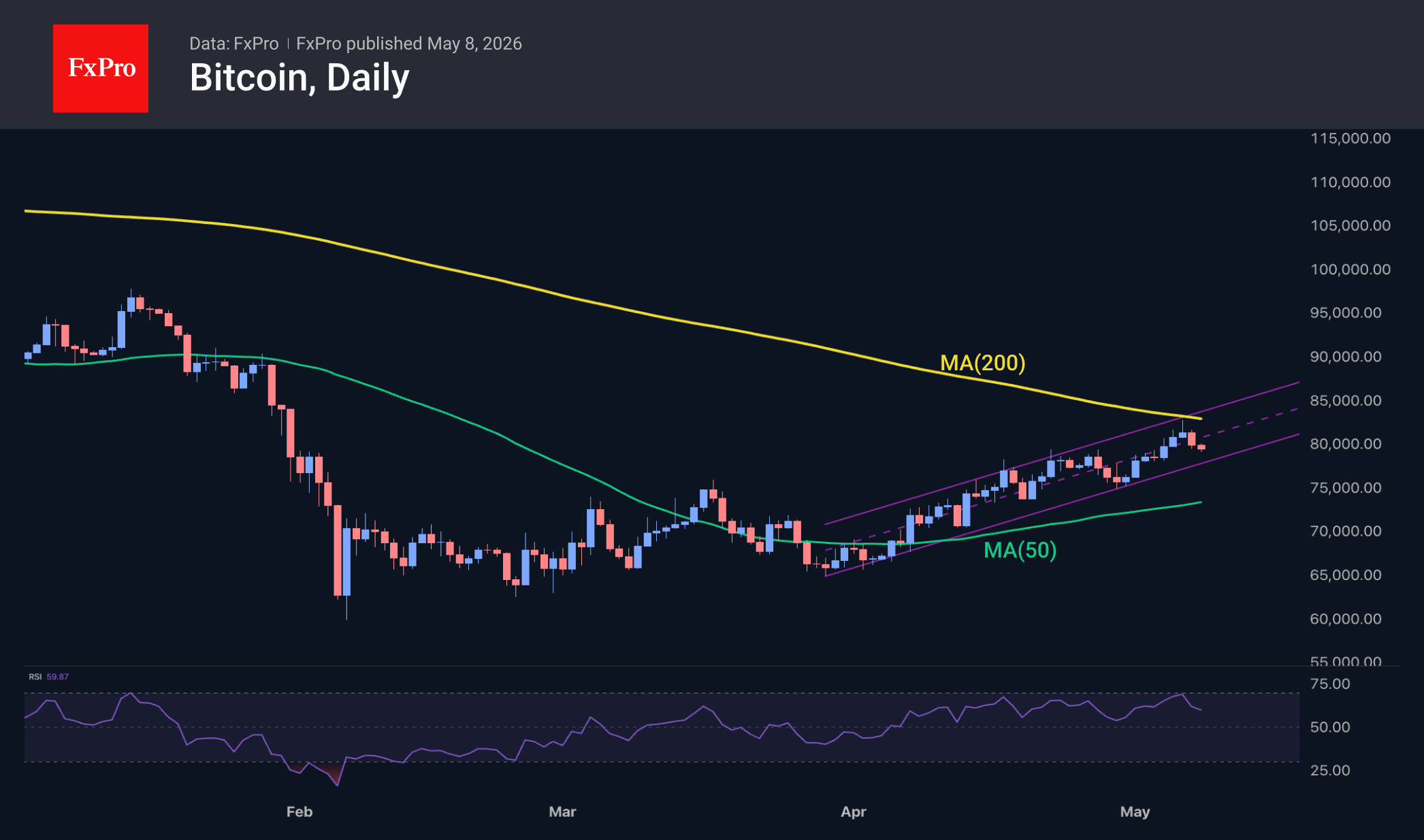

Crypto Market Has Retreated, Taking Its Cue from Equities

Market Overview

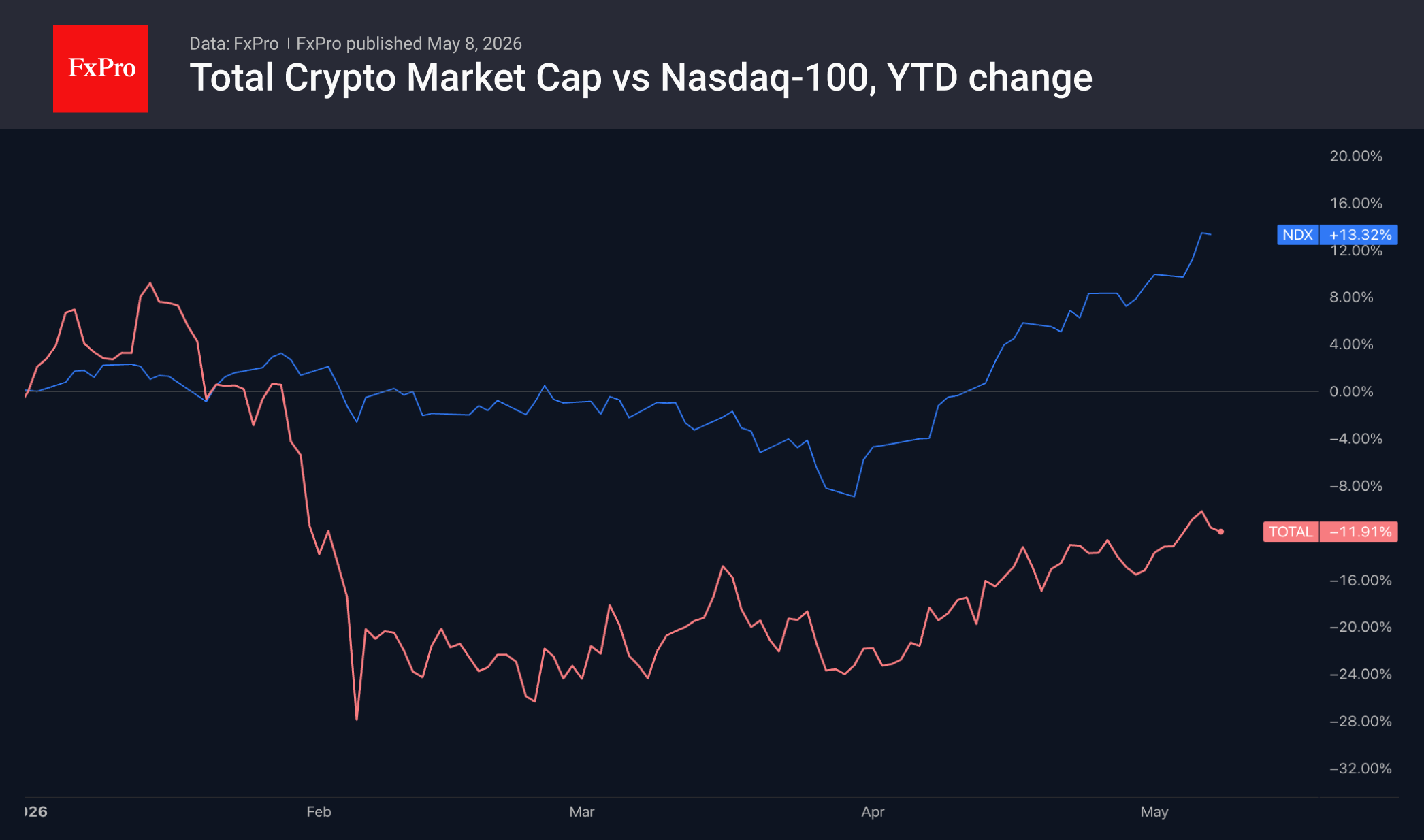

The crypto market capitalisation has fallen by around 2% over the past 24 hours to $2.62 trillion, amid a renewed flight to safety in global markets. The leaders were Internet Computer (+9%), Zcash (+3.6%) and Tron (+1.4%); the laggards were Doge (-4.7%), Toncoin (-3.7%) and Dash (-3.5%). Since hitting lows at the end of March, the cryptocurrency market has been rising at roughly the same pace as the S&P 500, but at about half the speed of its more familiar bellwether – the Nasdaq 100. Since the start of the year, the Nasdaq 100 has gained 13%, while the crypto market has declined 12%.

Bitcoin has returned to levels below $80K, extending its retreat from the 200-day moving average and after touching the overbought zone as part of a pullback from the upper boundary of the uptrend channel. The lower boundary of this channel lies near $77.5K, but a break in this trend would require a fall below the recent lows near $75K.

News Background

Crypto whales on Hyperliquid have significantly increased their long positions in Bitcoin over the past two months, signalling strong bullish sentiment among large BTC holders, according to Glassnode.

Galaxy Digital notes a reduction in selling pressure on Bitcoin, while the number of potential buyers continues to grow. To reach $100K, the asset needs to consolidate above $84K.

Bitcoin Core developers have fixed a critical memory safety vulnerability. A significant proportion of nodes are still running the vulnerable software.

According to a study by Project Eleven, quantum computers will be able to break the cryptographic security of Bitcoin and other blockchains by 2033. The aggressive scenario points to 2030, the conservative one to 2042.

The Chicago Mercantile Exchange has announced plans to launch the first regulated Bitcoin volatility futures on 1 June. The BVX index, calculated from the exchange’s options market data, will serve as the basis for pricing.

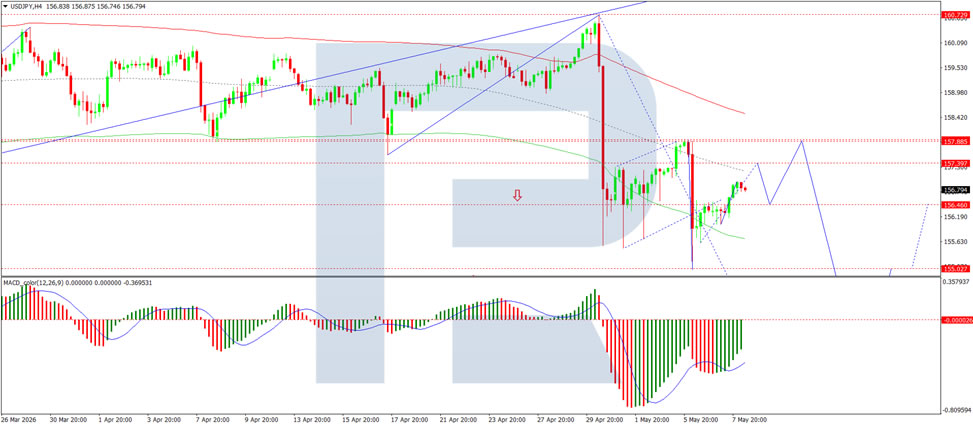

Yen Stabilises, But Intervention Risks Remain

USD/JPY is holding near 156.83 on Friday. Despite heightened volatility in recent sessions, the yen is set to end the week broadly unchanged. Fears of intervention and Tokyo's firm rhetoric have failed to support a sustained strengthening of the currency.

Japanese authorities have stated that they are not constrained by the frequency of their interventions in the foreign exchange market and remain in constant contact with the US. Earlier, the yen rose sharply amid suspected interventions on 30 April and 6 May, but there was no official confirmation of these actions.

Domestic data has been stronger. Real wages rose for the third consecutive month, supporting expectations of further tightening by the Bank of Japan (BoJ).

Nevertheless, the external backdrop remains negative. A stronger dollar and tensions around the Strait of Hormuz continue to weigh on the yen.

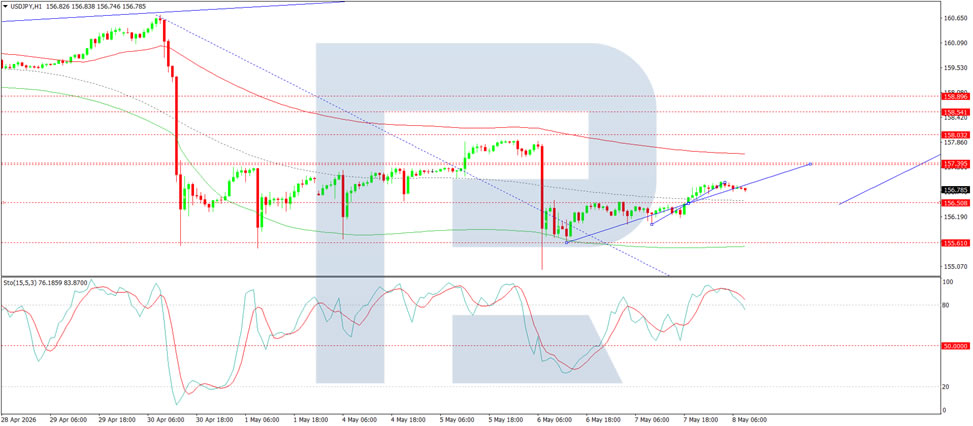

Technical Analysis

On the H4 chart, USD/JPY is trading within a consolidation range around 156.50 and is moving higher towards 157.39. A test of this level is likely, followed by a possible pullback to 156.50 before a further move higher towards 157.90. The MACD indicator supports this scenario, with its signal line below zero and pointing firmly upwards, indicating that bullish momentum is building.

On the H1 chart, USD/JPY has reached 156.95 and is now pulling back towards 156.50. A rebound towards 157.00 may follow, with a possible extension to 157.39. The Stochastic oscillator confirms this view, with its signal line below 80 and pointing firmly downwards towards 20, indicating that short-term downside pressure remains.

Conclusion

The yen has stabilised near 156.83 against the dollar, but intervention risks persist despite Tokyo's verbal warnings. Domestic wage growth supports BoJ tightening expectations, yet external factors such as a strong dollar and geopolitical tensions continue to weigh on the currency. Technically, a short-term rise to 157.39 may be followed by a pullback to 156.50 before any further upside develops.

US Jobs Data Takes Focus Amid Fragile US-Iran Peace Hopes

In focus today

- The key release today is the US April jobs report. We expect a solid report with NFP growth of 80k and unemployment rate unchanged at 4.3%. High-frequency indicators have generally been strong despite the uncertainty related to the war in Iran. The Fed puts more emphasis on the unemployment rate, as NFP growth is heavily (negatively) affected by the slowdown in labour supply growth.

- In Sweden, more detail on the preliminary GDP figures will become available when production and consumption data are published.

Economic and market news

What happened overnight

In the US-Iran conflict, the two sides exchanged fire overnight in the Strait of Hormuz (SOH), but Trump says that the ceasefire is still in effect. Trump has again threatened to resume attacks if no nuclear deal is reached, although similar threats have not always materialised. Talks remain stuck on uranium stocks, sanctions relief, SOH access and sequencing, and trust. Iran's response to the latest US proposal to end the war is expected shortly and will be key for markets to look out for.

In the oil market, Brent crude briefly fell below USD97/bbl yesterday before recovering above USD100/bbl. The renewed tensions around the SOH have caused markets to reassess the likelihood of a diplomatic breakthrough. If hostilities intensify, Brent could revisit the USD110‑115/bbl range seen earlier this week.

US-EU tariffs: Trump has set a 4 July deadline for full implementation of last year's trade deal after speaking with von der Leyen, threatening "much higher" duties on EU goods, including raising car tariffs from 15% to 25%, if EU levies on US industrial products are not cut to zero. The automotive sector is the main pressure point. The Commission reports "good progress", but the European Parliament still sees "some way to go", keeping timing risks elevated. Separately, Trump's 10% tariffs under section 122 were ruled unlawful by a US trade court, underlining ongoing legal constraints on his unilateral tariff agenda from not only the IEEPA tariffs that the supreme court ruled against. For now, the ruling only directly covers the two companies that brought the case and the state of Washington, and it can still be appealed by the US Justice Department.

What happened yesterday

In Norway, Norges Bank (NB) hiked policy rates by 25bp to 4.25%. It was an interim meeting with only a press release, a brief policy assessment and minutes, but no report or rate path. Hence, the amount of new information was limited. However, NB provided more neutral guidance on the policy rate outlook compared to March. The decision was a big event risk for markets going into the decision with both markets and analysts split on an "unchanged" decision and a hike.

In Sweden, the Riksbank kept its policy rate unchanged at 1.75% as widely expected. The press release struck a balanced tone, suggesting that low spot inflation and somewhat sluggish growth in Sweden weigh against higher energy prices, elevated cost pressure and rising international inflation, such as seen in the euro area.

In the US, April's Challenger report showed job cuts of around 83k, as layoff announcements rose from 61k in March, in contrast to the decline seen recently in jobless claims. AI is accounting for a growing share of announced job cuts: last year, less than 10% of all layoffs were attributed to AI in Challenger's statistics, whereas in both March and April the share exceeded 25%. US jobless claims increased less than expected amid low layoffs. The number of people receiving unemployment benefits fell by 10k to a seasonally adjusted 1.766 million in the week ending 25 April, taking continuing claims to their lowest level since early 2024. Meanwhile, Q1 flash productivity growth slowed as expected to 0.8% q/q AR from 1.8% in Q4 2025. Despite this, unit labour cost growth also slowed to 2.3%, which should be consistent with only 2% inflation.

In the UK, more than 5,000 council seats were up for grabs at local elections in England. The Scottish and the Welsh were also at the polls. Early results suggest the Labour Party is facing a big setback as expected, while Reform UK is on the rise. The Conservatives are also looking at a loss. Election results are being announced throughout today and some tomorrow. The big question for markets is whether the Labour setback will be so extensive that PM Starmer could be forced to resign, in which case we would expect another leg higher in Gilt yields.

Equities: Wednesday's over-excitement faded, with Stoxx 600 -1.1% lower and S&P 500 -0.4%. Energy heavy sectors underperformed, including materials and industrials at the bottom. Tech has been the standout in recent weeks. What's interesting is how the tech sector takes turn pulling in current markets. While the semis rally retreated -2% yesterday, in line with performance in other heavy cyclicals, software bounced 3.5% and thereby led the market. As such, tech and in the end, US has been a relative winner recently in risk-on and risk-off markets.

FI and FX: US and Iranian hostilities resumed overnight as Iran launched attacks on US warships, with the US responding by striking Iran military sites. President Trump however stated that the ceasefire is still in effect, while Iran says that the ceasefire has been broken. Brent crude briefly fell below USD97/bbl yesterday but has rebounded back above the USD100/bbl mark. Yields rose over the US session, with the 2Y UST at 3.91% and the 10Y UST at 4.39% and trading sideways overnight. EUR/USD continues range-trading just above 1.17. The US April Jobs Report is set to be released in the afternoon and recent labour market signals have generally been strong. We forecast NFP slightly above consensus at +80k, and unemployment rate steady at 4.3%, which could add some near-term support for broad USD. Also keep an eye out for the UK local election. Early results suggest the Labour Party is facing a big setback, which could add to pressures for PM Starmer to resign.

Norges Bank hiked policy rates by 25bp yesterday but also struck a slightly more neutral tone compared to that of the March meeting. We still pencil in the second and final 25bp hike to 4.50% in June, but we acknowledge that the probability has fallen with yesterday's decision, i.e. we might already have hit a peak in policy rates. The Riksbank left the policy rate at 1.75%. The statement struck a balanced tone, weighing the softer-than-expected inflation against risks of higher inflation going forward. Governor Erik Thedéen offered little forward guidance, with the board instead aligning around a statement weighing the (modestly) increased upside risks to inflation against the recent downside surprise in spot prints, concluding that the Riksbank is well positioned to await further data.

Silver: Structural Deficit Amid Declining Demand

Fundamental Background

The structural deficit in the silver market has now persisted for a sixth consecutive year. According to forecasts by the Silver Institute, the gap between supply and demand in 2026 is expected to reach 67 million ounces, forcing the market to rely on accumulated reserves. However, the demand picture remains uneven.

Industrial consumption continues to decline, primarily due to the photovoltaic sector, where solar panel manufacturers are actively reducing the amount of silver used per cell in response to elevated prices. Against this backdrop, investment demand remains resilient: global ETP holdings have reached approximately 1.31 billion ounces, while silver lease rates in London have climbed to record highs amid a growing physical shortage.

Technical Picture

On the daily chart of XAG/USD, a two-phase structure is visible. From 21 November 2025, the instrument formed a strong upward impulse along an ascending trend line, reaching a peak on 29 January 2026. This was followed by a sharp collapse and a break below the trend line, with the low recorded on 6 February near the 64 level. A rebound then followed, and on 2 March a local recovery high was established — this area now corresponds to resistance around 96. A retest of the lows took place on 23 March 2026.

The horizontal volume profile spans the 68.300–89.000 range, with the point of control (POC) concentrated between 79.100 and 81.000. The price is currently trading below the lower boundary of this zone and remains under selling pressure. The nearest support lies at 68.300, followed by stronger support at 61.000, corresponding to the February crash low.

The RSI + MAs indicator shows readings of 55, 47 and 47. RSI remains above both moving averages; however, all indicators are within neutral territory, with no strong directional momentum currently visible.

Key Takeaways

The silver market continues to be influenced by two opposing fundamental forces: a structural supply deficit supported by investment demand, and weakening industrial consumption from the photovoltaic sector. The resolution of this imbalance is likely to determine the future direction and character of the market.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Chart Alert: GBP/USD Potential Bullish Reversal Above 20-Day Moving Average

Key takeaways

- GBP/USD remains supported despite renewed US-Iran tensions, with traders now closely focused on upcoming US labour market data and University of Michigan consumer sentiment figures that could drive near-term volatility in the pair.

- Intermarket dynamics favour further upside for sterling, as the UK-US implied interest rate spread has steepened significantly, reinforcing expectations that the Bank of England may stay relatively more hawkish than the Federal Reserve.

- Technical indicators suggest a potential bullish reversal is underway, with GBP/USD rebounding from its ascending channel support, holding above its 20-day and 50-day moving averages, while momentum indicators point to strengthening upside momentum above the 1.3530 support zone.

After the sterling hit a 2-month high of 1.3658 on 1 May 2026 against the US dollar, the GBP/USD has traded sideways, and on Thursday, 7 May 2026, it declined by 0.2% to print an intraday low of 1.1723 on the backdrop of an uptick in US-Iran tension after both sides exchanged fire.

In addition to the latest developments surrounding the US-Iran conflict, where markets are awaiting Iran’s response to Washington’s latest proposal to reopen the Strait of Hormuz, traders will also be closely watching several key US economic releases today that may influence the short-term direction of GBP/USD.

These include the April non-farm payrolls and unemployment rate data at 8:30 pm SGT, followed by the preliminary University of Michigan consumer sentiment report for May at 10:00 pm SGT.

Interestingly, intermarket and technical factors are now supporting a potential bullish reversal in the GBP/USD at this juncture.

Let’s unpack in greater detail.

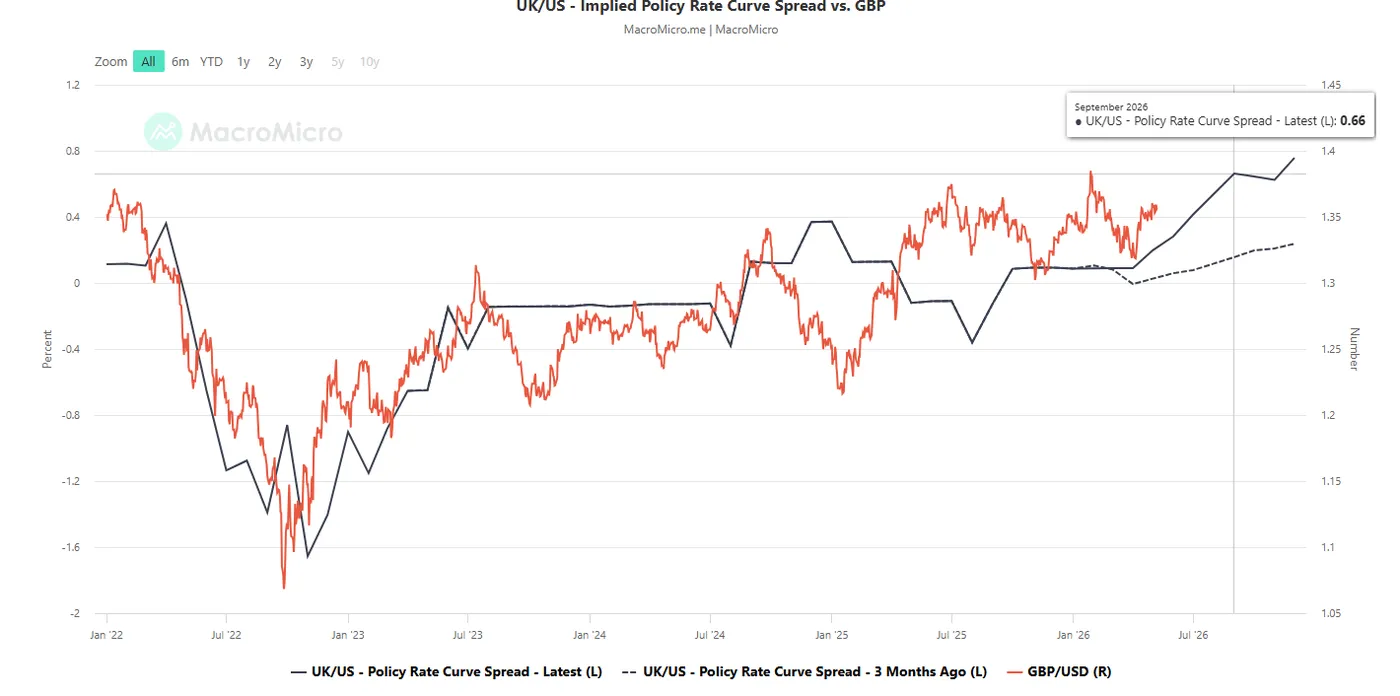

The UK/US Implied Interest Rate Policy Curve Spread Has Steepened

Fig. 1: UK-US implied interest rate policy curve spread as of 7 May 2026 (Source: MacroMicro).

Interest rate futures markets indicate that the Bank of England (BoE) will likely hike in July after being on hold at 3.75% since December 2025.

The current Eurozone/US implied interest rate policy curve spread for the period from June 2026 to September 2026 has steepened significantly.

In addition, the curve has also shifted upwards, with the current September 2026 reading standing at 0.66% compared to 0.16% three months ago (see Fig. 1).

These observations suggest that the BoE is likely to be less dovish or more hawkish than the Fed, which in turn could provide support for a potentially firmer GBP/USD.

The monthly implied future monetary policy interest rate curves for the UK and the US are calculated using short-term interest rate futures that are highly sensitive to the expectations on these countries’ central banks' respective monetary policies.

Let’s focus now on the short-term trajectory (1 to 3 days) of the GBP/USD from a technical analysis perspective.

GBP/USD – Holding Above 1.3530, Watch the 1.3640/3665 Range Resistance Next

Fig. 2: GBP/USD minor trend as of 8 May 2026 (Source: TradingView).

Trend bias: Bullish above 1.3530 short-term pivotal support within an uptrend phase (see Fig. 2).

Resistances: 1.3590, 1.3640/3665 (upside trigger), and 1.3730

Next supports: 1.3490 and 1.3450

Key Elements to Support the Near-Term Bullish Bias on GBP/USD

- Price actions have managed to stage a rebound after a retest on the lower boundary of the medium-term ascending channel from the 6 April 2026 low.

- Price actions continue to trade above their 20-day and 50-day moving averages, which support an ongoing medium-term uptrend phase.

- The hourly RSI momentum indicator has just exited from its oversold region (below the 30 level) in today’s Asian session (Friday, 8 May 2026).

Sunrise Market Commentary

Markets

The shaky ceasefire between the US and Iran stumbled again late last night. Iran fired on three US Navy destroyers sailing in the Strait of Hormuz. The US responded by targeting the launching facilities in what it said is self-defense and not an attempt to escalate. US president Trump afterwards said the truce remains in place but warned for the consequences if Iran doesn’t agree to a deal. “Just like we knocked them out again today, we’ll knock them out a lot harder, and a lot more violently, in the future, if they don’t get their Deal signed, FAST!”, Trump wrote in a social media post. The events and language used are a reminder of the unpredictable nature of the conflict. Markets just a day earlier rallied on the hope that both sides were closing in on a deal. That optimism faded somewhat yesterday with European stocks returning around 1% of the +/- 3% gains. US equities finished between 0.1-0.6% lower. Brent oil lost some further ground. It dropped to as low as $96 but clawed back above $100 into the close. Last night’s hostilities caused a higher open to around $103 before paring gains, suggesting markets don’t consider them as triggering a new all-out (bombing) campaign. For investors, the direction (towards a peace deal) is clear but the road bumpy. The intraday reversal in Brent yesterday forced core bonds to forfeit earlier gains. That resulted in some marginal bear flattening in Europe with the front-end adding less than 2 bps. Treasuries underperformed by adding 2.5 (30-yr) to 4.6 bps (2-yr) in yields. The US dollar strengthened modestly against G10 peers. DXY held above 98, EUR/USD eased from 1.1748 to 1.1726 – both in technically insignificant trading. USD/JPY bounced back on the first day of Japanese investors returning from holidays. The couple rose from 156.39 towards 157.

Though not a formal deadline according to president Trump, the US does expect an Iranian response within 48 hours after the 14-point MoU was handed over. That should be today. While awaiting the answer, US April payrolls enter the mix. The expected 65k following a strong 178k print in March is a feasible bar, based on other labour market data (ADP in particular). The unemployment rate is seen at matching March’s 4.3%. A solid report should not per se trigger immediate rate hike bets but could keep the bottom below front-end US yields supported around current levels (3.9-4%). We’ll admit that daily oil price swings will be at least if not more important though. First results of the local UK elections meanwhile point at a heavy, if not record defeat for Starmer’s Labour party with Reform UK and the Greens being the main benefiter in the English Council elections. Parliamentary elections in Scotland and Wales have yet to produce the first preliminary results. Even though Starmer’s position looks increasingly unsustainable, sterling holds on. EUR/GBP eases slightly to 0.865.

News & Views

• The April consumer expectations survey of the New York Fed showed some mixed signals. One-year ahead inflation expectations rose further by 0.2 ppt to 3.6%. Inflation expectations at the 3- & 5-y ahead horizon were unchanged at respectively 3.1% and 3%. Expectations for the year ahead gas price growth eased from a March peak at 5.1% to 4.3%. One-year-ahead earnings growth expectations increased by 0.3 ppt to 2.7 percent but unemployment expectations (probability it will be higher one year from now) increased by 0.4 ppt to 43.9 percent, the highest reading of the series since April 2025. Participants see a higher change of losing its own job. The quit rate eased marginally. Perceptions about credit access compared to a year ago and expectations for future credit availability both deteriorated but the perceived probability of missing a minimum debt payment over the next three months decreased by 0.9 ppt to 11.4%, the lowest in more than two years.

The Czech National bank (CNB) yesterday left its policy rate unchanged at 3.5% in an unanimous decision. CNB assesses that inflation has been close to target since January 2024 as new forecasts indicated that it will be in the upper half of the tolerance band (2% +/- 1%pt) for the rest of this year due to higher fuel prices. It expects core inflation to remain elevated holding near 3%. In this new forecast, CNB now sees GDP 2026 growth at 2.5% (from 2.9%) and 2027 growth at 2.7% (from 2.9%). Headline CPI inflation was upwardly revised from 1.6% to 2.2% and from 2.1% to 2.4% for the same periods. Aside from the impact of higher energy prices, the CNB mentions a series of upward inflation risks, including an acceleration in money supply, growth public sector spending, a tight labour market and rapid wage growth and inertia in elevated services inflation. This requires relatively tight monetary policy. However, a good starting position provides room for thorough analysis and an appropriate response should it be necessary. KBC expects an unchanged policy rate for the remainder of the year.

‘Iran Deal’ Headlines Replaced by ‘US Had Struck Military Targets in Iran’

What a week it has been – and it is not over! It started with renewed Middle East tensions, sending oil prices up to $115pb, then tensions eased and markets breathed a sigh of relief thanks to the US’ unwillingness to escalate, while euphoria kicked in on news that even a peace proposal had come to the table.

Meanwhile, the week’s most closely monitored earnings went extremely well. Chip stocks rallied on better-than-expected results from Samsung and AMD, while the Nasdaq renewed record after record. The good mood got a further sugar coating from falling sovereign yields, as declining oil prices also pulled inflation expectations lower and softened central banks’ policy outlooks.

All of a sudden, the potential ‘Iran deal’ headlines are replaced by news that the US had ‘struck military targets in Iran after the country fired on three Navy destroyers sailing in the Strait of Hormuz’, suggesting that we’re back to square one. US crude rebounded past the $98pb level and is consolidating just below the $97pb mark, while Brent is settling above $101pb at the time of writing.

We have no idea how the situation will evolve, but the track record of the past two months is not really encouraging, and the Friday close is always a critical moment as the US tends to make decisive moves during no-market hours to give investors time to digest the information, hoping to push volatility into Monday and eventually drown out bad news with encouraging — often unfounded — announcements.

It has admittedly worked well so far… Since the start of the war, the S&P 500 has hit fresh record highs nine times, if my count is right. US futures are in positive territory this morning, European appetite is somewhat less.

On the earnings front, Whirlpool warned that record-low sentiment — due to the Iranian war and the doubling of gasoline prices — has plunged demand for appliances to a level the company says could lead to a ‘recession-level industry decline’. The stock plunged 12%, while the tech-heavy S&P 500 was busy flirting with fresh ATHs. Oh well...

Anyway, we have one more thing to watch before this week’s closing bell, and that’s the US jobs report. The US economy has been in a phase of low hiring and low firing, with the latest jobs data suggesting that the slowdown is not as bad as feared. Earlier this week, the ADP report printed lower-than-expected job additions of 109K, but the number did not sound alarming — and the data certainly got diluted amid more exciting war and tech earnings headlines.

Headlines remain dominated by geopolitical tensions, but today’s official jobs data still deserves attention. The median forecast in the latest Bloomberg survey points to 65K new nonfarm job additions in the US last month, with average wage growth rebounding from 3.5% to 3.8% y-o-y.

As I repeated several times earlier this week, estimates diverge remarkably. Some expect the US jobs market to have added a significantly lower number of jobs compared to the median forecast, pointing to thousands of job cuts from Big Tech names due to AI replacement and the ongoing immigration struggle, while others predict that massive AI spending is creating jobs and should at least limit the AI-related slowdown. We will see where the data lands today.

As for the market reaction, I would expect a stronger-than-expected set of figures to keep Federal Reserve (Fed) hawks in charge, without necessarily taming equity appetite — the latter will likely depend on war headlines.

A softer-than-expected set of jobs figures, on the other hand, could revive dovish Fed expectations and provide further support to equity valuations, provided that war headlines leave some room for reaction and wage growth remains reasonable. By reasonable, I mean a figure in line with — or ideally softer than — the 3.8% yearly expectation, while uncertainty about oil prices remains very, very high.

And this last part is important, because some Fed members are growing more concerned about the inflation outlook than the health of the jobs market — a notable shift compared to the pre-war narrative, mind you. That change — from worrying about a softening labour market to worrying about overheating price pressures — puts inflation/wages figures front and centre, while making the headline NFP somewhat secondary when it comes to guessing the Fed’s next move. The best outcome for the market would be relatively strong job additions paired with relatively softer wage growth.

Speaking of good data, here’s something that made me smile. Bank of England (BoE) officials are apparently worried that the UK’s economic data looks too good to be true — and, more importantly, that it may be sending a misleading signal to markets, making the job of setting monetary policy even trickier than it already is amid Middle East jitters. In fact, first-quarter growth has consistently come in strong since 2022, only to fade later in the year. It probably has to do with consumer behaviour and post-Covid spending habits — or so it is said — and the fact that the ONS has not found a way to smooth out the numbers enough for seasonally adjusted figures to be fully consistent. If that pattern repeats again, the BoE could end up tightening policy more than necessary in its fight against inflation, and into a more rapidly deteriorating UK economic outlook than early-year data suggests.

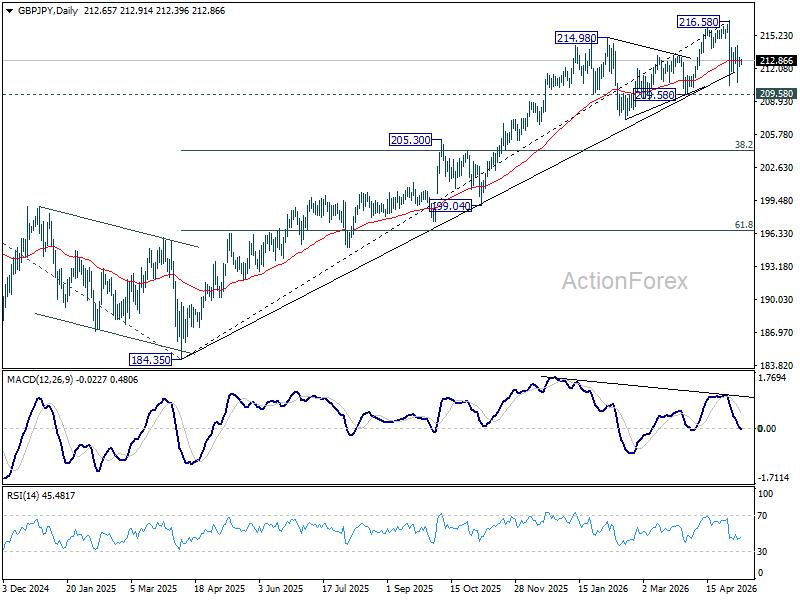

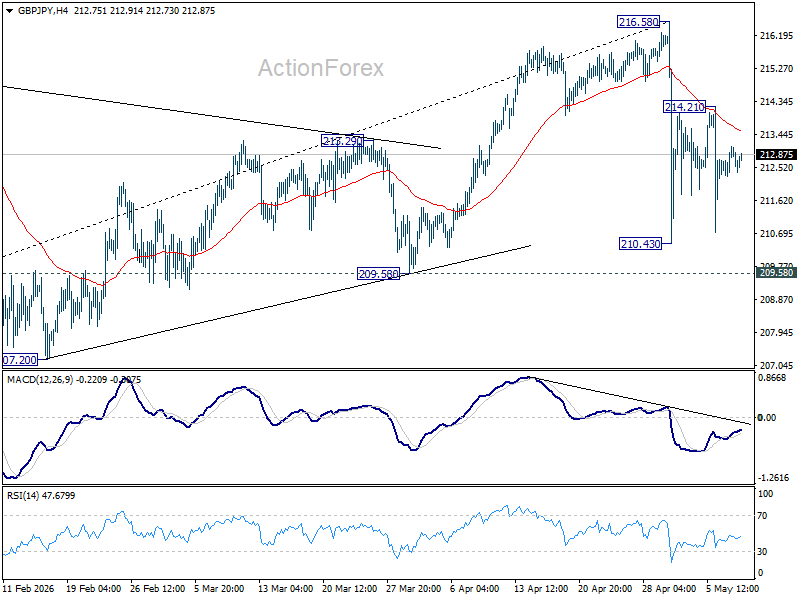

GBP/JPY Daily Outlook

Daily Pivots: (S1) 212.27; (P) 212.70; (R1) 213.11; More...

Intraday bias in GBP/JPY remains neutral and outlook is unchanged. Further decline is expected as long as 214.21 holds. Below 210.43 will target 209.58 support first. Break will target 38.2% retracement of 184.35 to 216.58 at 204.28. However, firm break of 214.21 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, while the fall from 216.58 is steep, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 205.45) will argue that it's already in medium term down trend for 184.35 support.