Sample Category Title

Sunset Market Commentary

Markets

US payrolls for April printed a stronger-than-expected 115k, easily topping the 65k consensus bar. This solid employment growth followed a strong March as well (185k vs 178k in the initial release) and resulted in the first back-to-back gains in over a year. The increase was widespread in the services sector. Trade & transport (60k) led with private education & health (46k) as the runner-up. IT and financial services were the outliers shedding jobs with the pace in the former sector having accelerated since the turn of the year (AI impact?). The manufacturing sector also forfeited some jobs. Pay growth came in slightly sub-par at 0.2% m/m and 3.6% y/y – hovering near five-year lows. The unemployment rate steadied at 4.3% while the participation rate fell to 61.8%. The labour market environment is still considered as a fragile “low hire, low fire” by the likes of Fed Hammack as of yesterday. Today’s numbers do seem to confirm Fed chair Powell’s message of a labour market that is showing “more and more signs of stability” last week after a year of near-zero job growth. A near-term rate cut in such circumstances is unnecessary, particularly given upside inflation risks posed by the Iran war. US money markets hold on to their view of a long rates status quo at least through 2026 after the labour market report. Rates trade a couple of bps lower to the tune of 4.5 bps. German rates are going nowhere. This paralysis isn’t surprising with the bigger question still unanswered: Iran’s response to the US 14-point MoU. Secretary of State Rubio said “we should be hearing something today” but it’s really anyone’s guess, both on the timing and the actual reply. Oil prices are testing the $100 barrier (Brent) for a third day straight. Stocks lose ground in Europe but gain on WS. The euro takes the lead against most peers, including the USD. EUR/USD rises to 1.1777. DXY is struggling around the 98 big figure.

Gilts rally today, strongly outperforming core peers. Yields drop almost 9 bps at the long end of the curve. With 51 of the 136 English councils already declared, Labour lost 234 seats while Reform UK secured a whopping 380, setting Starmer’s party up for a heavy defeat. The results appear less worse than forecast, though, and the PM already insisted he’s not going anywhere. Regardless of the value of such a statement, it is easing some of the concerns markets had going into the elections vs. a potential follow-up to Starmer and his/her view on fiscal policy. Sterling barely reacted to the election outcome with EUR/GBP treading water around 0.864.

News & Views

The pace of Hungarian headline inflation held steady at 0.4% M/M in April, defying expectations for an acceleration to 0.6% M/M. Prices are 2.1% higher Y/Y. That’s more than in March (1.8%) but also below consensus (2.2%). Accelerating food price inflation was partly offset by disinflation in regulated prices. Core inflation rose by 0.3% M/M and 2.2% Y/Y with core inflation excluding indirect tax effects also printing at 2.2%. Incoming data were below the Hungarian central bank’s forecasts in the March inflation report. The MNB’s measures of underlying inflation developments capturing persistent inflationary trends declined. The inflation of sticky price products was down to 4% Y/Y. Core inflation excluding processed food decreased to 3%. Further MNB analysis showed tradables (goods) inflation rising by 0.7% M/M and 1.4% Y/Y. Services inflation rose by 0.5% M/M and 4.6% Y/Y. Hungarian swap rate dropped significantly after the CPI release, falling by 15 bps (10-yr) to 19 bps (2-yr). The forint shrugged off the loss of interest rate support (and the largest ever YtD Hungarian budget deficit; 70% of the annual target; also released today) with the Hungarian currency testing the strongest levels against the euro since early 2022 at EUR/HUF 355. Ever since Fidesz lost power, Hungarian assets profited from EMU-convergence vibes.

The United Nation’s FAO Food Price Index rose for a third consecutive month, with the index hitting its highest level since February 2023. Food prices rose by 2% Y/Y in April. Details showed a mixed picture. Especially vegetable oils are responsible (+5.9% M/M; index hit highest since July 2022) though meat (+1.2% M/M with index hitting record high) and cereal prices (+0.8% M/M) increased as well. The continued increase in vegetable oil was driven by higher prices of palm, soy, sunflower and rapeseeds oils. Higher demand from the biofuel sector, higher crude prices and fears over lower Asian production in coming months all play their part. Dairy prices fell on a monthly basis (-1.1% M/M) are 21.1% lower than a year ago. Finally, ample global supplies drove sugar prices 4.7% down in April and 21.2% below last year’s price level.

US UoM Consumer Sentiment Falls to 48.2, Near 2022 Lows as Inflation Concerns Persist

US consumer sentiment weakened slightly in May, remaining near the depressed levels last seen during the 2022 inflation shock as households continued expressing concern about high prices and deteriorating buying conditions.

The University of Michigan Consumer Sentiment index fell from 49.8 to 48.2, while the Current Economic Conditions index dropped sharply from 52.5 to 47.8.

The decline in current conditions reflected rising concern over personal finances and affordability, particularly for major household purchases. Survey respondents continued citing elevated prices as a key pressure point, even though headline inflation expectations eased modestly during the month.

One-year inflation expectations slipped from 4.7% to 4.5%, while long-run inflation expectations edged lower from 3.5% to 3.4%. Still, inflation expectations remain well above pre-Iran war levels and continue exceeding the ranges seen before the pandemic.

The data suggest consumers are becoming somewhat less pessimistic about the future, with the Expectations index ticking up slightly from 48.1 to 48.5, but confidence overall remains fragile as households continue adjusting to higher prices and geopolitical uncertainty.

| Indicator | Previous | Latest |

|---|---|---|

| Consumer Sentiment | 49.8 | 48.2 |

| Current Conditions | 52.5 | 47.8 |

| Expectations Index | 48.1 | 48.5 |

| 1-Year Inflation Expectations | 4.7% | 4.5% |

| Long-Run Inflation Expectations | 3.5% | 3.4% |

US: Payrolls Remain Firm in April, Unemployment Rate Holds Steady at 4.3%

Nonfarm payrolls rose by 115k in April, down from March's gain of 185k but ahead of the consensus forecast calling for a smaller print of 65k. Revisions to the two prior months subtracted a total of 16k from the previously reported figures, with February revised lower (-156k from -133k) and March slightly higher (+185k from +178k).

- Smoothing through the volatility, nonfarm payrolls averaged 48k per-month over the last three months, up from the -39k averaged through the three months ending in December 2025.

Private payrolls rose 123k, following a stronger gain of 190k in March. Job gains were concentrated in health care & social assistance (+53.9k), transportation & warehousing (+30.3k) and retail trade (+21.8k). Federal government hiring (-9k) continued to decline.

In the household survey, the unemployment rate was unchanged at 4.3% as the number of unemployed were little changed amid a small decline in the labor force (-92k). The labor force participation rate fell to 61.8% (from 61.9% the month prior), which is its lowest level since late-2021.

Average hourly earnings (AHE) rose a "soft" 0.2% month-on-month (m/m), matching March's gain. On a twelve-month basis, AHE ticked up to 3.6% (from 3.4% the month prior).

Key Implications

Payrolls were volatile through Q1, largely due to temporary factors like inclement weather and a healthcare strike in California. With those effects now in the rearview mirror, April provided as the first "clean" read on hiring for 2026 and the underlying details were reasonably constructive, despite the recent surge in energy prices. Job growth appears to have picked up from its anemic pace at the end of last year and is now running reasonably close to its breakeven rate – holding the unemployment rate steady.

It's too soon to say whether the labor market is regaining momentum, but this morning's report alongside other recent data points including initial jobless claims and job posting data by Indeed certainly help to assuage any fears that conditions have continued to cool. From the Fed's perspective, this means they can sit tight to better assess the extent to which higher energy prices bleed through to core measures of inflation in the months ahead. Yields were relatively muted post-payrolls, with Fed futures priced for the FOMC to remain on hold into next year.

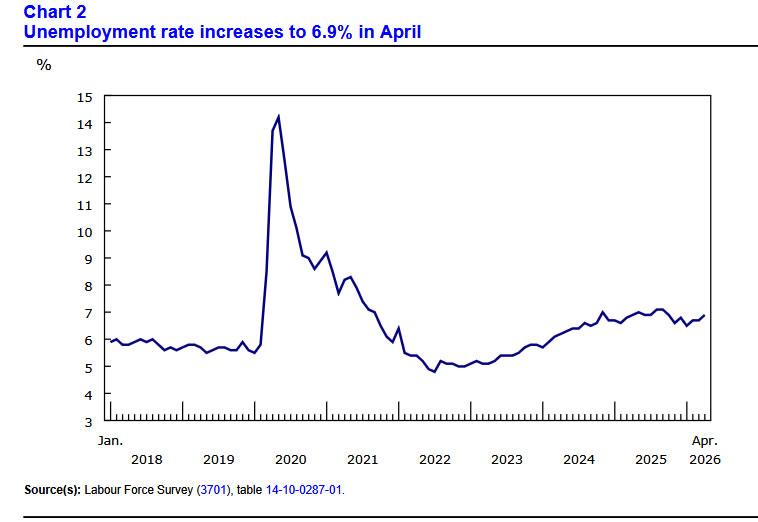

Canada’s Unemployment Rate Rises as More People Look for Work

Canada’s economy lost 18k jobs in April (-0.1% m/m), undershooting consensus expectations for a 10k gain. Employment is now virtually unchanged following February’s sharp decline. Full‑time employment fell by 47k, while the number of private‑sector workers was essentially flat (-2.6k).

The unemployment rate rose to 6.9% from 6.7%, as labour supply increased faster than job creation. The number of people in the labour force grew by 33.5k, pushing the labour force participation rate up 0.1 percentage point to 65.0%. The monthly layoff rate (0.6%) remained in-line with the pre-pandemic average.

Job losses were concentrated in services-producing industries, led by information, culture and recreation (-25k), construction (-16k), and other services (-13k). These declines were partially offset by gains in business, building and other support services (+22k), health care and social assistance (+18k), and accommodation and food services (+13k).

Average hourly wages were up 4.5% year-on-year (y/y) down from 4.7% in March. Importantly, the elevated wage gain reflects compositional shifts, with fewer employees with shorter job tenures.

Key Implications

A modest drop in employment coupled with a sizeable jump in the labour force drove up the unemployment rate two ticks this month. Although the monthly data reflect a high degree of variability, the persistently elevated unemployment rate is reflective of a job market that continues to struggle to absorb labour supply. In the coming months we expect the labour force increases to lose steam and help cap further rises in the unemployment rate.

The economic outlook is far from rosy and the ongoing slack in the labour market is reflective of an economy that is still struggling to gain traction. However, with the labour market still soft, the ability of firms to pass on cost increases from the inflation shock to consumers is more limited. This is a key factor that underpins our view that if the sharp rise in oil prices begins to reverse in the coming weeks, the Bank of Canada will be able to stay on hold this year.

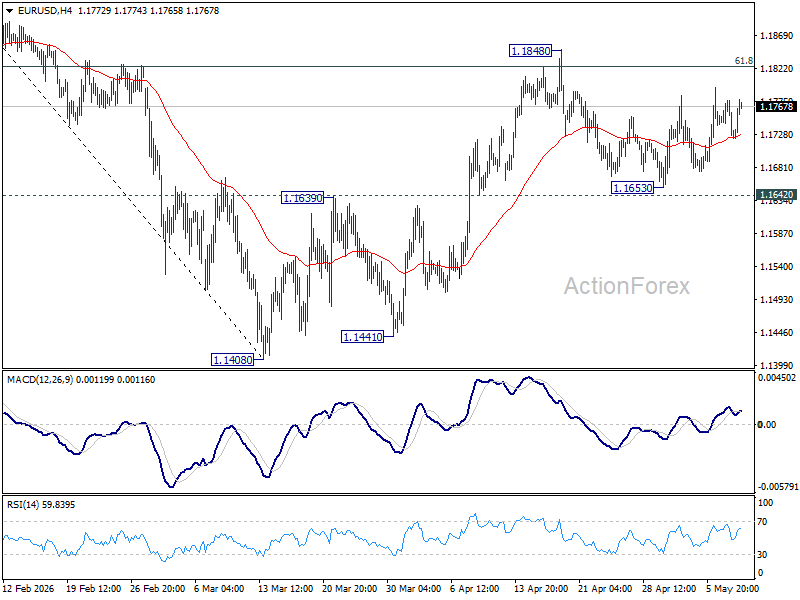

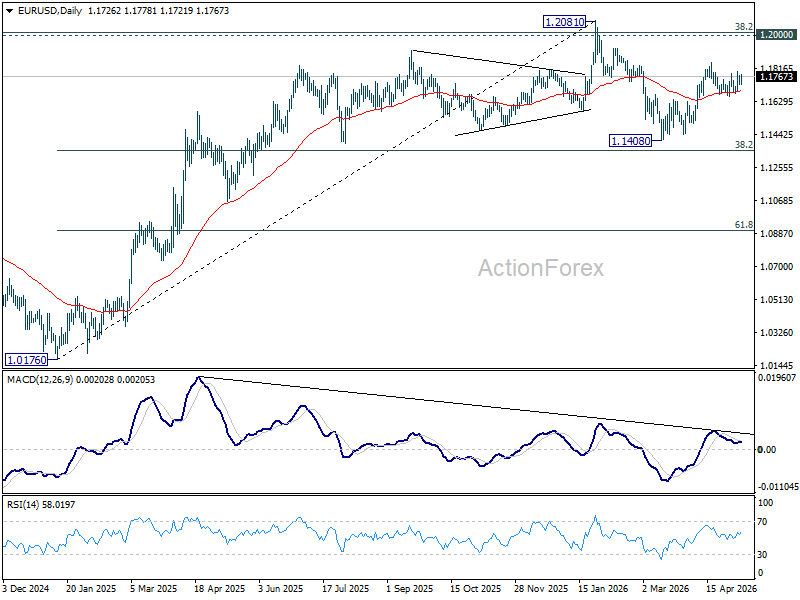

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1705; (P) 1.1743; (R1) 1.1762; More….

EUR/USD is still bounded in range trading and intraday bias remains neutral. With 1.1642 support intact, rise from 1.1408 is expected to continue. On the upside, firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1537). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

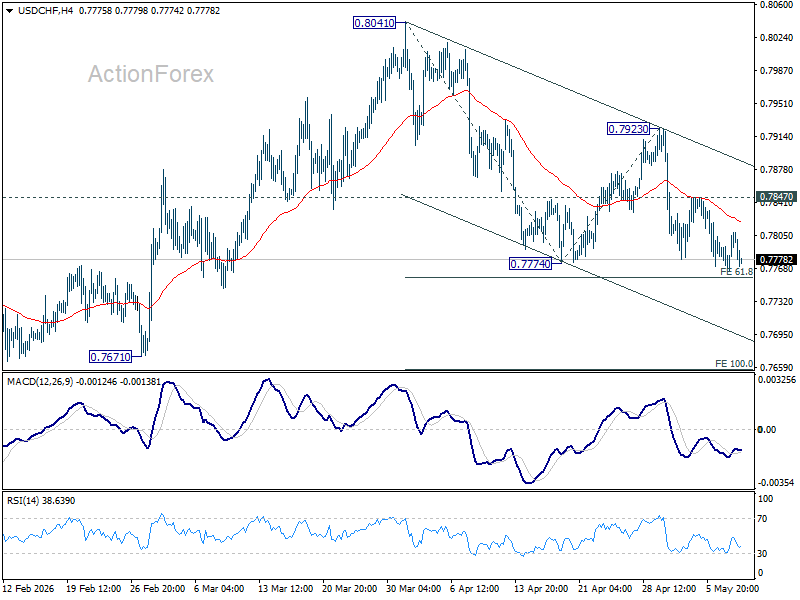

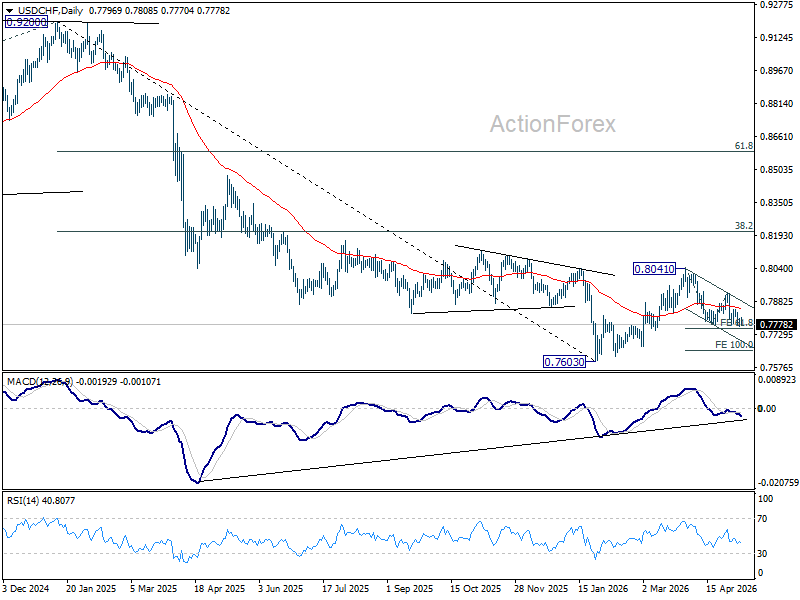

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7778; (P) 0.7793; (R1) 0.7822; More….

Intraday bias in USD/CHF remains mildly on the downside at this point. Decisive break of 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758 will extend the fall from 0.8041 to 100% projection at 0.7656. On the upside, above 0.7847 minor resistance will turn bias neutral again.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8042) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

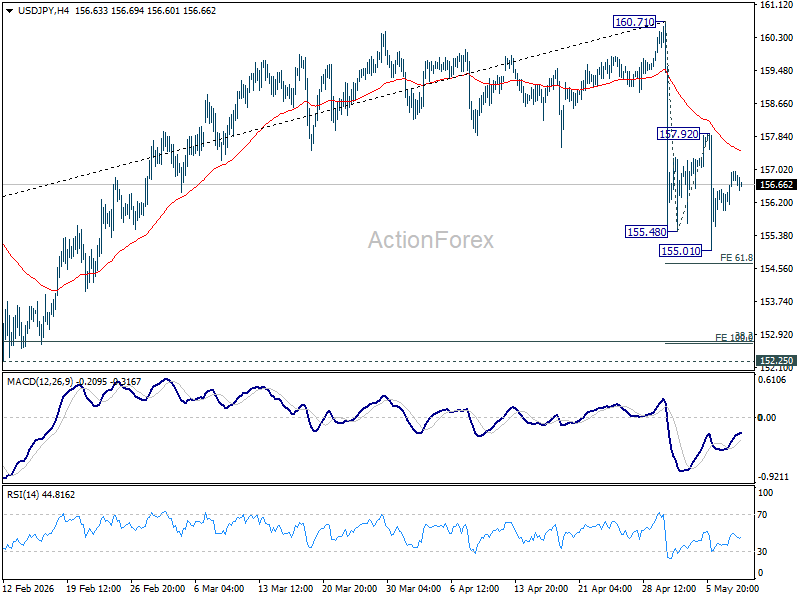

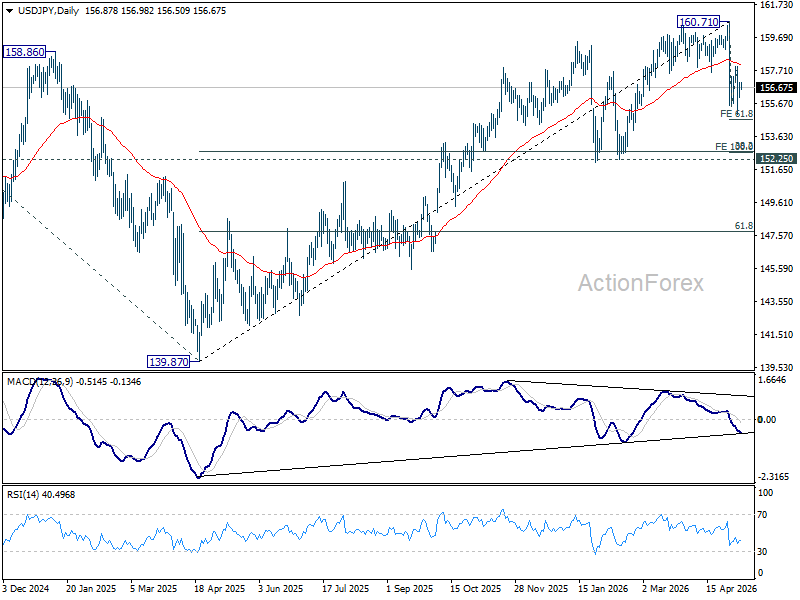

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.32; (P) 156.64; (R1) 157.26; More...

Range trading continues in USD/JPY and intraday bias stays neutral. Risk will stay on the downside as long as 157.92 resistance holds. Below 155.01 will resume the fall from 160.71 to 61.8% projection of 160.71 to 155.48 from 157.92 at 154.68. Firm break there will target 100% projection at 152.69. That would be close to key 152.25 cluster support (38.2% retracement of 139.87 to 160.71 at 152.74). However, firm break of 157.92 will turn bias back to the upside for stronger rebound.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.01) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

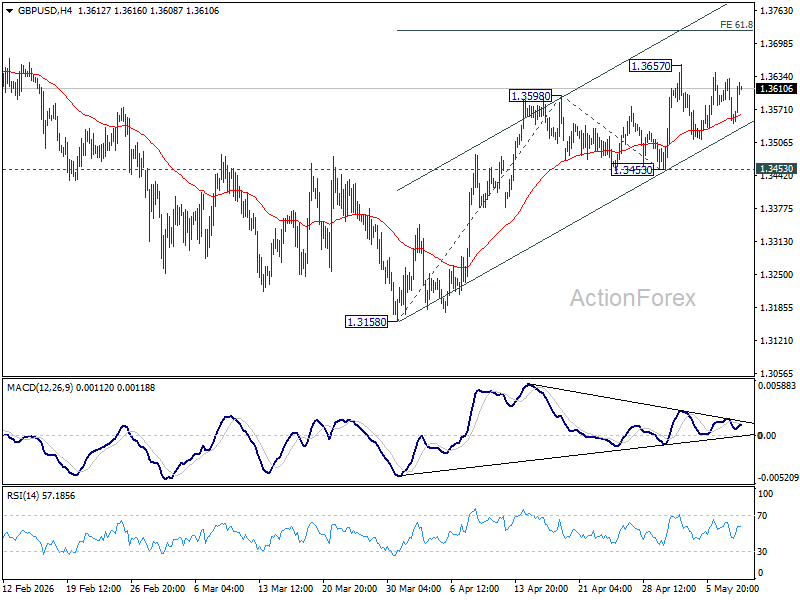

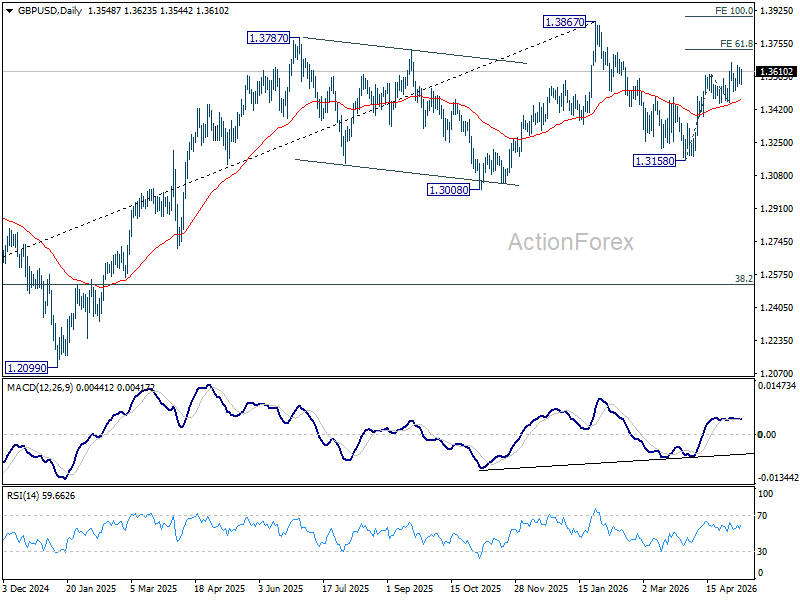

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3522; (P) 1.3577; (R1) 1.3607; More...

GBP/USD rebounded after drawing support from 55 4H EMA, but stays below 1.3657 resistance. Intraday bias remains neutral and more consolidations could still be seen. Further rise is expected with 1.3453 support intact. On the upside, above 1.3657 will target 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high. However, break of 1.3453 will turn bias back to the downside for 1.3158 support instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).

Markets Embrace Strong US Employment Report, but Iran Remains the Bigger Risk

The US jobs report gave stock markets exactly what they wanted — proof the economy is still holding up without reigniting fears of runaway inflation. Stocks liked it, the Fed will likely like it, and recession fears eased further. Yet despite the upbeat reaction, traders still seem unwilling to fully commit because the biggest market risk remains geopolitical, not economic.

Dollar slipped broadly in early US trading after the payrolls release, though the move lacked strong follow-through against most major currencies. That hesitation says a lot about the current market environment. Even after a stronger-than-expected jobs report, investors are still treating developments surrounding the US-Iran conflict as the dominant macro driver.

The April payrolls report itself was clearly solid. Non-Farm Payrolls rose by 115k, almost double market expectations, while March’s already strong reading was revised higher to 185k. The unemployment rate held steady at 4.3%, suggesting the labor market continues showing resilience despite geopolitical uncertainty and slowing global growth concerns.

At the same time, the inflation side of the report stayed relatively calm. Average hourly earnings increased just 0.2% mom, below expectations, even though annual wage growth ticked up modestly to 3.6% yoy. For markets, that combination created the ideal “Goldilocks” outcome: strong enough to reassure investors the economy is not sliding toward recession, but soft enough to avoid reviving fears of a more hawkish Federal Reserve.

That dynamic helped reinforce the powerful risk-on environment that has driven S&P 500 and NASDAQ toward repeated record highs in recent sessions. Investors could believe the Fed can comfortably stay on hold for the rest of the year without needing to either rescue the economy or aggressively tighten policy further. Market pricing now shows more than 70% probability that rates remain unchanged through year-end.

Meanwhile, Canadian Dollar became the major underperformer after Canada’s labor market delivered a sharp negative surprise. Employment fell by -17.7k in April instead of posting expected gains, while unemployment rose to 6.9%. The report reinforced concerns that Canada’s economy is losing momentum more quickly than the US.

While BoC Governor Tiff Macklem has warned that persistent inflation could eventually require multiple rate hikes, deteriorating employment conditions make it increasingly difficult for the central bank to realistically follow through on that threat.

Still, even the strong US payrolls report failed to fully dominate market attention. Markets are now turning back toward geopolitics as the dominant macro driver. US Secretary of State Marco Rubio said Washington expects a response from Tehran later Friday regarding the proposed agreement aimed at ending the conflict. “We’ll see what the response entails. The hope is it’s something that can put us into a serious process in negotiation,” Rubio said.

For now, the broader market tone remains cautiously constructive. Kiwi leads currency gains for the week, followed by Aussie and Swiss Franc, while Loonie, Dollar, and Yen underperform. But despite the encouraging payrolls report, investors appear unwilling to fully extend risk positioning until there is greater clarity on whether the fragile path toward a US-Iran agreement can hold.

US Payrolls Beat Expectations With 115k Growth, But Wage Growth Stays Calm

US payrolls surprised to the upside in April, reinforcing the view that the labor market remains resilient despite slowing growth concerns. At the same time, softer monthly wage growth helped keep the broader “Goldilocks” soft-landing narrative intact. Read More.

Canada Employment Falls -17.7k as Unemployment Rises to 6.9%

Canada’s labor market weakened in April. Employment unexpectedly fell, full-time jobs dropped heavily, and unemployment climbed to 6.9%, adding to concerns about slowing economic momentum. Read More.

Japan Real Wage Growth Extends Gains Despite Slower Nominal Pay Growth

Japan’s real wages rose for a third consecutive month in March, supported by easing inflation and the strongest stretch of base pay growth in more than three decades. Read More.

Japan PMI Services Finalized at 51.0 as Middle East War Fuels Cost Pressures

Japan’s services sector lost momentum in April just as inflation pressures intensified sharply. Rising energy costs linked to the Middle East conflict pushed input prices to a three-and-a-half-year high and selling prices to their steepest increase in nearly two decades. Read More.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3522; (P) 1.3577; (R1) 1.3607; More...

GBP/USD rebounded after drawing support from 55 4H EMA, but stays below 1.3657 resistance. Intraday bias remains neutral and more consolidations could still be seen. Further rise is expected with 1.3453 support intact. On the upside, above 1.3657 will target 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high. However, break of 1.3453 will turn bias back to the downside for 1.3158 support instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).

Canada Employment Falls -17.7k as Unemployment Rises to 6.9%

Canada’s labor market weakened notably in April as employment unexpectedly declined and the unemployment rate climbed to its highest level in months. Total employment fell by -17.7k during the month, sharply missing expectations for a modest gain of 5.1k. The weakness was concentrated in full-time positions, which dropped by -47k, while part-time employment rose by 29k.

Unemployment rate increased from 6.7% to 6.9%, above market expectations, while employment rate slipped to 60.5%. At the same time, participation rate edged higher to 65.0%, suggesting more people entered the labor force despite deteriorating hiring conditions.

Wage growth remained relatively elevated but showed signs of gradual moderation. Average hourly wages rose 4.5% yoy in April, slowing slightly from March’s 4.7% increase.

| Indicator | Previous | Latest | Expectation |

|---|---|---|---|

| Employment Change | +14.1K | -17.7k | +5.1k |

| Unemployment Rate | 6.7% | 6.9% | 6.7% |

| Employment Rate | 60.6% | 60.5% | — |

| Participation Rate | 64.9% | 65.0% | — |