Sample Category Title

Dollar Recovers as Iran Talks Stall, Focus Turns to Trump-Xi Summit

The market narrative is becoming more complicated. Dollar and oil are rising again as Iran negotiations stall, yet semiconductor-driven equity rallies continue pushing Asian tech markets higher, highlighting how AI momentum is still partially insulating risk assets from geopolitical stress.

Markets entered the weekend expecting at least some form of diplomatic breakthrough between Washington and Tehran. Instead, they woke up Monday facing another reminder that the Middle East crisis may be drifting into something much longer and more dangerous than a simple “deal or war” scenario. Oil prices jumped sharply, Dollar rebounded broadly, and traders began rebuilding geopolitical risk premium after the highly anticipated US-Iran agreement failed to materialize.

Brent crude surged back above $105 after Iran rejected the Trump administration’s hardline 14-point memorandum of understanding. Tehran responded with its own counterproposal, reportedly demanding immediate sanctions relief, a broader regional military halt, and a phased long-term approach toward nuclear restrictions. US President Donald Trump responded late Sunday with a series of Truth Social posts calling the proposal “TOTALLY UNACCEPTABLE,” signaling that negotiations remain deeply deadlocked.

Yet the broader market reaction was far from classic panic. Gold softened and slipped back below $4700, while Asian technology stocks continued powering higher. South Korea’s KOSPI exploded another 4.5% to fresh record highs as semiconductor names extended their AI-fueled rally. Strong leads from US technology stocks again overwhelmed regional geopolitical concerns. Japan’s Nikkei also briefly touched fresh record highs before pulling back modestly.

The divergence across asset classes was striking. Oil and Dollar traded like geopolitical stress mattered again. Equities, particularly semiconductors, continued trading as though the AI cycle remained the dominant force in global markets. That split may continue to be the defining theme for the week ahead.

Attention is now shifting toward Trump’s upcoming state visit to China from May 13–15, the first trip by a US president to Beijing in nearly nine years. Trump and Xi Jinping are expected to discuss trade, Taiwan, artificial intelligence competition, rare earth export restrictions, and perhaps most critically, the Iran conflict and Hormuz security situation.

There is also a growing theory circulating across markets that Iran may intentionally be delaying negotiations until after the Trump-Xi summit. That could be referred to as the “Dragon Factor” — the belief that Tehran hopes China could negotiate some form of energy-security arrangement or oil corridor that weakens US leverage over Hormuz and sanctions enforcement. Whether realistic or not, the theory highlights how deeply interconnected geopolitics, trade, and energy markets have become.

Before the summit itself, Chinese Vice Premier He Lifeng and US Treasury Secretary Scott Bessent are expected to meet in South Korea on Wednesday for preliminary trade discussions. Any signs of coordination between Washington and Beijing regarding energy stability could quickly become the single most important driver for oil markets.

Meanwhile, this week also carries major monetary policy implications. On Tuesday, the US Senate is expected to approve Kevin Warsh as the next Federal Reserve Chair ahead of Jerome Powell’s departure later this week. Inflation data will follow closely behind, with April CPI forecast to rise to 3.7% yoy while Core CPI could accelerate to 2.9%. If energy-driven inflation begins spilling further into core prices, markets may have to reassess whether the current “Fed on hold” consensus can survive a prolonged oil shock.

Other major releases include the BoC Summary of Deliberations, which is expected to reinforce a cautious hold stance despite mounting oil-driven inflation pressure. German ZEW sentiment is likely to deteriorate further as industrial weakness deepens, while UK GDP later this week may show the first meaningful “war drag” from higher energy cost

In currency markets today, Dollar is currently the strongest performer, followed by Loonie and Euro. Kiwi is the weakest, followed by Swiss Franc and Sterling. Aussie and Yen are trading more mixed.

In Asia, at the time of writing, Nikkei is down -0.37%. Hong Kong HSI is down -0.36%. China Shanghai SSE is down -0.31%. China Shanghai SSE is up 0.64%. Singapore Strait Times is up 0.35%. Japan 10-year JGB yield is up 0.033 at 2.510.

| Event | Timing | Market Focus |

|---|---|---|

| Trump-Xi Summit | May 13–15 | Trade, AI, Taiwan, rare earths, Iran/Hormuz |

| He Lifeng–Bessent Meeting | May 13 | Pre-summit US-China economic and trade discussions |

| Fed Chair Transition Vote | May 12 | Senate vote on Kevin Warsh replacing Powell |

| US CPI | May 12 | Headline CPI expected at 3.7% yoy. Core at 2.9%. |

| BoC Summary of Deliberations | May 13 | Oil shock vs rate hold debate |

| German ZEW Sentiment | May 12 | Weak industrial outlook and trade deterioration |

| UK GDP | May 14 | Economic impact of energy shock |

US-Iran Peace Deal Failed — Brent Oil’s Triangle Pattern Warns Bigger Shock Ahead

Markets spent last week betting the US-Iran conflict was moving toward controlled de-escalation. That assumption is now under pressure after Trump rejected Tehran’s counterproposal and Brent oil surged back toward $105. More importantly, crude’s tightening triangle pattern suggests the market may be “storing energy” for a much larger move ahead. Read More.

China Inflation Heats Up as PPI Hits 45-Month High

China’s inflation rebound accelerated sharply in April, with producer prices hitting a 45-month high and consumer inflation also beating expectations. Rising fuel costs helped drive the move, but core inflation data suggested price pressures are now spreading more broadly across the economy. The data strengthens the view that China’s long deflation cycle may finally be ending. Read More.

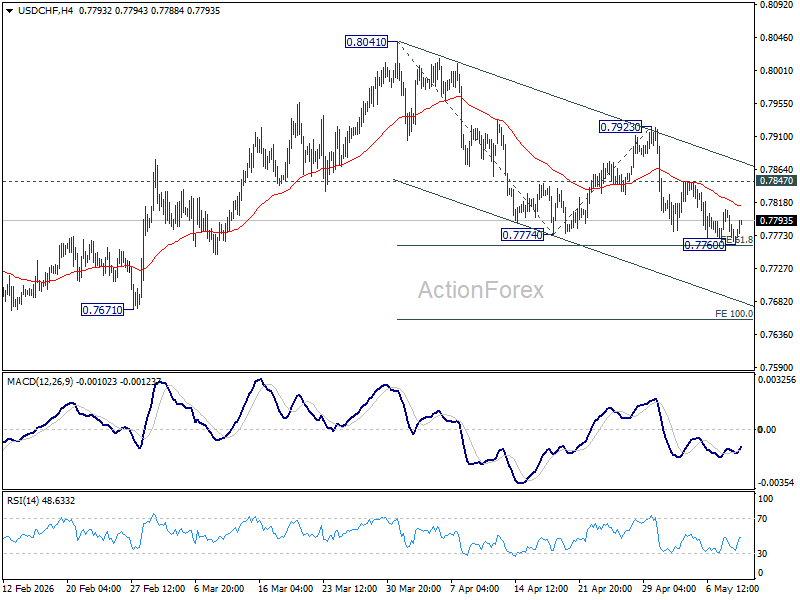

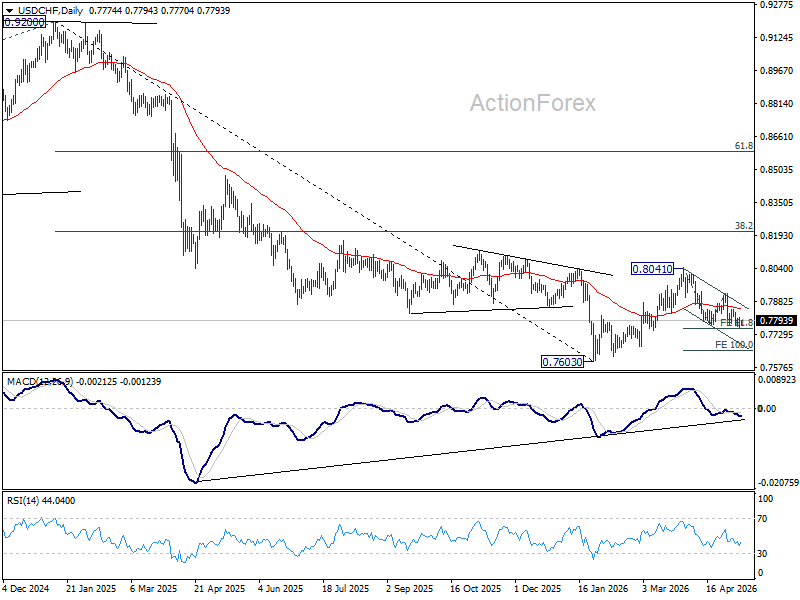

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7746; (P) 0.7777; (R1) 0.7793; More….

Intraday bias in USD/CHF is turned neutral again with current recovery. On the downside, decisive break of 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758 will resume the whole decline form 0.8041, and target 100% projection at 0.7656. However, firm break of 0.7847 resistance will indicate short term bottoming, and bring stronger rebound back to 0.7923 resistance.

In the bigger picture, as long as 55 W EMA (now at 0.8051) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

China Plays to Its Comparative Advantage

In trade, investment and, with time, via financial flows, China has a considerable long-term advantage that is set to grow their real economy and national wealth.

This week, President Xi and President Trump are due to meet and discuss China/US relations, developments in the global economy and, barring a resolution before, likely the conflict in the Middle East. This meeting will not materially change the status quo, being one of a number of in-person meetings planned for this year. But it will guide on the opportunities and risks ahead. Available data points to a stark difference in perspective and each nation’s outlook.

As the US continues to focus on controlling trade across its borders in pursuit of greater domestic investment and production, China has instead enticed investment at home by encouraging foreign trade. To date in 2026, China’s trade surplus has averaged US$88bn per month after holding around US$99bn in 2025, both outcomes roughly three times the 2018-19 average of US$32bn.

The US trade position has, in contrast, deteriorated from an average deficit of US$47bn per month in 2018-19 to US$73bn in 2025-26. This US data admittedly pre-dates the surge in energy exports seen through April and May, but China has also temporarily pulled back on their supply of energy goods to other nations, reducing export revenue.

With future export opportunities remaining the focus, Chinese fixed asset investment continues to grow after rapidly scaling through 2020-2025. Of particular note, transport and storage-related infrastructure spending surged in early-2026, and utilities investment has continued to compound around 9%ytd.

Within the manufacturing sector, stronger demand for green technology goods and refined energy products is likely to elicit a sustained upturn in capital expenditure through 2026, with the key investment sub-categories of electrical machinery, automobiles (EVs) and chemicals all showing evidence of stabilisation in Q1, and global demand receiving strong support from elevated energy prices and open-ended uncertainty over Middle East supply.

In contrast, in the US, investment remains highly concentrated in AI-related infrastructure and conversely is weak in areas related to trade and the domestic real economy. Lingering uncertainty related to tariffs and elevated long-term yields are also at play, in addition to businesses’ focus on technology – US for-profit entities need greater surety over expected returns than China’s state-owned and state-linked entities.

An additional element to consider is the benefit China may receive from the US’ souring relationship with other nations, particularly Europe. This month, President Trump has continued to spar with European leaders, threatening to pull US troops from Germany and other major nations in the region. He then threatened a 10 percentage point increase in the US tariff rate for European cars and trucks, purportedly because the EU had failed to live up to their side of the agreed trade deal.

The EU labelled the US as an “unreliable” trading partner and vowed to respond. Ahead of this development, Chinese authorities were acting to strengthen ties with European leaders, publicly via a number of high-profile visits from European leaders, and behind the scenes by encouraging Chinese firms to invest in Europe and vice versa. There is strong evidence of an integrated, mutually-beneficial trade relationship taking shape between China and Europe.

As we have highlighted frequently, Chinese investment is not concentrated in one jurisdiction, however. It has also spread widely across Asia, Latin America and Africa, targeting not only the production of finished goods, but also the production of supply inputs – from raw materials to high-tech components.

While not their initial intent, over time this project will justify a material increase in the use of the Renminbi in trade, and will also strengthen demand for real and financial investment within China.

These trends will see greater depth and liquidity for China’s onshore financial markets, as well as scope to offer global investments to Chinese investors through the issuance of Renminbi denominated debt and equity instruments. The larger these flows become, the greater the opportunity for Chinese banks and financial entities to facilitate flows, provide capital and manage risk, both on and, more importantly, offshore.

Overall then, in trade, investment and, with time, via financial flows, China has a considerable long-term competitive advantage that is set to benefit their real economy and national wealth.

This analysis initially appeared in Westpac Economics’ May Market Outlook.

For the US, Economic Opportunity is Narrow and Increasingly Brittle

US tech investment has scale and is delivering, but growth elsewhere in the economy is challenged.

The US has exhibited both strength and frailty over the past month. Backed by earnings beats and despite a new cycle high for Brent oil, its equity markets have rebounded strongly to record levels. At the same time though, growth in consumer demand has fallen below trend and housing investment is contracting. In many respects, the outlook is highly uncertain.

Beginning with the positives. The confidence financial markets have shown amid open-ended uncertainty for energy supply, the pass-through to consumer inflation and elevated yields is jarring. Participants’ responses to recent earnings results and news of the build out of AI infrastructure helps to make sense of these outcomes, however.

Simply, there is a dominant belief that the US’ real economy can be protected from the worst of the supply disruptions by its domestic energy production and refining capacity. And, both now and in the long run, is at the forefront of productivity and profitability enhancement through technology. The surge in energy exports as well as intangibles and equipment investment supports both notions. The strength of these investment sub-types arguably also warrants expectations of sustainable income gains and an ability to, in time, contain inflationary pressures, providing scope for persistent, robust returns.

We do not doubt the strength of tech-related investment or the capacity it is creating. But we see a need to caution on the sustainability of its contribution to GDP growth because momentum tends to moderate as an industry matures, and owing to the concern being shown by investors over the financing terms and lifecycle of assets within the sector. We also believe it is important to recognise that, outside of AI infrastructure and related equipment investment, business investment is soft. Indeed, at circa 6%yr, annual growth in total business investment is broadly in line with the historic depreciation rate for the US capital stock, implying no net increase in functional capacity. Also, in the public sector, while activity rebounded in Q1 2026 following Q4’s shutdown, the level of spending is unchanged over the year.

At the same time, the pulse of consumer demand has continued to soften, from an above-trend annualised pace of 3.2% through 2023 and 2024 to a sub-par 2.1% annualised in 2025, and now 1.6% in Q1 2026. This is despite the unemployment rate remaining consistent with full employment, the drag on real discretionary income fading and as real wealth accrues. Also affected by elevated term interest rates, housing construction continues to contract to now be down more than 18% since early 2021, even with solid population growth.

It is extremely difficult, if not impossible, for an economy to grow at or above trend when sectors representing 72% of total activity are experiencing a sub-par performance, or contracting outright. The import component of the above activity is an additional headwind for GDP growth which is unlikely to subside, even if President Trump finds a way to permanently impose tariffs and entice new investment.

Our take on the above positives and negatives is that the US economy finds itself with the capacity to grow at or near trend through 2026-2028, but momentum is likely to be concentrated amongst a sub-set of tech-centric businesses and higher-income households, with volatile outcomes around a broadly flat trend anticipated elsewhere. Meanwhile, limits on capacity outside of technology is, all else equal, likely to hold inflation consistently above target. As we have emphasised repeatedly, the adoption of AI and related technology offers the opportunity for greater productivity from labour. But limits on migration are likely to create offsetting wage pressures and frictions in production.

For US monetary policy, known risks are therefore set to remain skewed towards misses on inflation versus a material increase in labour market slack. The market is likely to price in at least a chance of a rate hike over the forecast period, and term interest rates a lasting hawkish tilt. For the long end of the yield curve, the effect of higher inflation expectations will be magnified by the implications for Government servicing costs – a higher share of expenditure going to interest payments, increasing the stock of debt and reducing the Government’s capacity to invest for growth. In our view, this uptrend for interest rates is unlikely to boost the US dollar, being paired with modest US economic growth and opportunities in other parts of the world, for businesses and investors alike.

This analysis initially appeared in Westpac Economics’ May Market Outlook.

US Futures Dipped as US-Iran Peace Deal Hopes Dimmed

Key takeaways

- US futures edged lower in the early Asian session: Donald Trump rejected Iran’s latest peace response, dampening hopes for a formal US-Iran agreement and keeping geopolitical risk premiums elevated.

- Stronger-than-expected US April jobs data: Reinforced the “higher for longer” interest rate narrative, reducing expectations for Federal Reserve rate cuts in 2026 and supporting elevated Treasury yields.

- The AI-driven equity rally remains intact globally: Supported by semiconductor momentum, expanding hyperscaler AI capex, and new industrial AI initiatives involving Apple, Intel, and Jeff Bezos.

- Chart of the day: Nasdaq 100’s bullish impulsive up move looks overstretched, raising the risk of a minor corrective decline below the 29,505/615 key short-term resistance zone. Intermediate supports stand at 28,835 and 28,460/280.

Top macro headlines

- Trump rejects Iran peace response: US President Donald Trump described Iran’s response to Washington’s latest peace proposal as “unacceptable” over the weekend. The setback clouds the near-term prospects for a formalized agreement and keeps a floor under geopolitical risk premiums even as direct military engagements remain limited.

- US jobs report defies expectations: A stronger-than-expected April employment report (115K versus 62K consensus) reinforced the view that the Federal Reserve may avoid cutting rates in 2026 as labor market resilience and sticky inflation keep policy restrictive.

- US-Iran ceasefire holds after latest test: Reuters reported that despite exchanges of fire late last week in the most serious test of the ceasefire so far, both sides signaled a desire to avoid escalation and tensions later stabilized.

- Apple & Intel AI chip pact: The AI hardware supercycle continues to dominate market leadership after reports emerged that Apple has reached a preliminary agreement with Intel on chip production initiatives.

- Yuan hits three-year highs ahead of Trump-Xi summit: China’s yuan strengthened to fresh three-year highs against the dollar ahead of the highly anticipated Trump-Xi summit scheduled for May 14–15 in Beijing.

- Bezos expands into industrial AI: Reuters Breakingviews highlighted that Amazon founder Jeff Bezos is raising $10 billion to help build AI models focused on industrial production and physical-world applications, signaling the next phase of AI capital expenditure expansion.

Key macro themes

- The “No Rate Cuts” reality: The combination of stronger labor data and persistent inflation pressures has reinforced the “higher for longer” narrative. Markets are increasingly pricing out the likelihood of Federal Reserve easing for the remainder of 2026.

- Complex geopolitics: Equity investors continue to navigate a difficult balance between a fragile ceasefire and stalled diplomacy. While the absence of a major escalation prevents oil from exploding higher, Trump’s rejection of Iran’s latest proposal means energy and defense sectors are likely to retain a geopolitical premium.

- AI Capex broadens beyond Silicon Valley: The AI boom continues to widen across sectors. Morgan Stanley expects top-tier hyperscaler AI capex to exceed $1.1 trillion next year, while capital increasingly flows into industrial and real-world AI applications.

Global market impact (last 48 hours)

Equities: Wall Street ended Friday on a firm footing, with semiconductor giants such as AMD and Micron continuing to lead gains as the AI trade remained the dominant market driver. However, in Monday’s early Asian session, S&P 500 and Nasdaq 100 E-mini futures slipped around 0.2% after Trump rejected Iran’s peace proposal.

Fixed Income: The stronger jobs report continues to pressure the bond market. The US 30-year Treasury yield remains supported around 4.90%, near its 50-day moving average, highlighting persistent inflation concerns and elevated long-term yield expectations.

FX: The Japanese Yen remains highly volatile following Japan’s suspected $67 billion intervention campaign over the past two weeks. Meanwhile, the Chinese Yuan continues to act as a regional anchor near three-year highs.

Commodities: Gold remains capped below its 50-day moving average near $4,775, while ongoing bullion purchases from China’s PBOC for an 18th consecutive month continue to provide structural support. Crude oil fluctuates around the $100 level as traders monitor Middle East developments.

Asia Pacific impact

- Stock markets: Asian technology shares remain the core engine behind the global equity rally. South Korea’s KOSPI recently crossed the historic 7,000 level as Samsung’s market capitalization surpassed $1 trillion amid surging memory-chip demand. Mixed performances were seen across the region, with the KOSPI up 4% and Nikkei 225 gaining 0.5%, while the Hang Seng Index fell 0.9% and ASX 200 slipped 0.8% during Monday’s Asian session.

- Currencies: The PBOC’s management of the Yuan continues to stabilize regional FX markets ahead of the Trump-Xi summit, while the Yen’s sharp swings near the 155 level keep carry-trade investors cautious.

- Economic outlook: The region continues to benefit from the AI-driven export boom, particularly in Taiwan and South Korea, while simultaneously facing structural pressure from elevated energy import costs.

Top 3 events to watch today

- China Inflation Rate & PPI (Apr) – 9:30 am SGT (consensus: CPI 0.8% y/y, PPI 1.5% y/y)

Impact: USD/CNH, Hang Seng, China A50, AUD/USD - US Existing Home Sales (Apr) – 10:00 pm SGT (consensus: 4.05M, previous: 3.98M)

Impact: US stock indices, USD - Geopolitical updates on the US-Iran peace proposal

Impact: All asset classes

Chart of the day - Nasdaq 100 due for a minor corrective decline

Fig. 1: Nasdaq 100 CFD index minor trend as of 11 May 2026 (Source: TradingView).

The US Nasdaq 100 CFD index, a proxy for Nasdaq 100 E-mini futures, has experienced a steep bullish impulsive rally since 30 April 2026. However, two key technical developments now suggest the index may face the risk of a near-term corrective pullback.

Friday’s rally pushed the Nasdaq 100 toward the upper boundary of its medium-term ascending channel in place since the 30 March 2026 low. At the same time, the hourly RSI momentum indicator has started to reverse lower after reaching extremely overbought territory near the 85 level.

Watch the 29,505/615 key short-term pivotal resistance zone. A break below the 28,835 downside trigger may expose the next intermediate support area at 28,460/280, which also coincides with the lower boundary of the ascending channel from the 30 March 2026 low.

On the other hand, a sustained break and hourly close above 29,615 would invalidate the minor bearish scenario and instead reinforce continuation of the bullish impulsive uptrend toward the next resistance levels at 29,893/953 and 30,410/417.

US-Iran Peace Deal Failed — Brent Oil’s Triangle Pattern Warns Bigger Shock Ahead

The market spent the last week behaving as though a US-Iran deal was only a matter of time. That assumption just took a major hit. Instead of accepting Washington’s 14-point peace framework, Tehran pushed back with its own proposal: lift sanctions, ease the blockade around Hormuz, and negotiate nuclear restrictions over the next 12 to 15 years. Trump’s answer came quickly and bluntly on Truth Social: “TOTALLY UNACCEPTABLE.”

That rejection undermines the entire market thesis that geopolitical tensions were gradually moving toward controlled de-escalation. Investors had increasingly convinced themselves that even if fighting continued, the conflict would stay economically contained. That belief helped fuel relentless buying in AI stocks, record highs in NASDAQ, and persistent Dollar weakness despite ongoing military clashes around the Gulf.

Oil never fully bought into that optimism. Brent held stubbornly elevated even while equities celebrated the “peace trade.” Today’s sharp rebound toward $105 suggests energy markets are still pricing in a different reality — not peace, not full war, but a drawn-out confrontation where shipping risks, military threats, sanctions pressure, and nuclear brinkmanship become semi-permanent features of the global economy.

The emerging reality looks messy. Iran appears to be trying to institutionalize leverage through Hormuz while buying time on nuclear concessions. Meanwhile, Israeli Prime Minister Benjamin Netanyahu openly says the war is “not over,” insisting enriched uranium still has to be physically removed from Iran. Trump himself continues threatening much harder military action if Tehran refuses to comply. That creates a far more dangerous macro backdrop because prolonged instability can be worse for inflation than a short shock.

The technical picture in Brent crude is also becoming increasingly unsettling. Since topping at 119.50 in March, prices have compressed into what appears to be a symmetrical triangle — one of the market’s classic “stored energy” patterns. Every ceasefire rumor has pulled prices lower. Every diplomatic failure has pulled them back higher. But the overall range keeps tightening.

Technically, that type of compression rarely lasts forever. The tighter the triangle becomes, the more violent the eventual breakout tends to be. Brent now appears to be starting another rising leg toward 115.30 resistance zone, and if the upper boundary eventually gives way, the measured move projects toward the 135–140 area. That is the real risk oil markets may now be warning about.

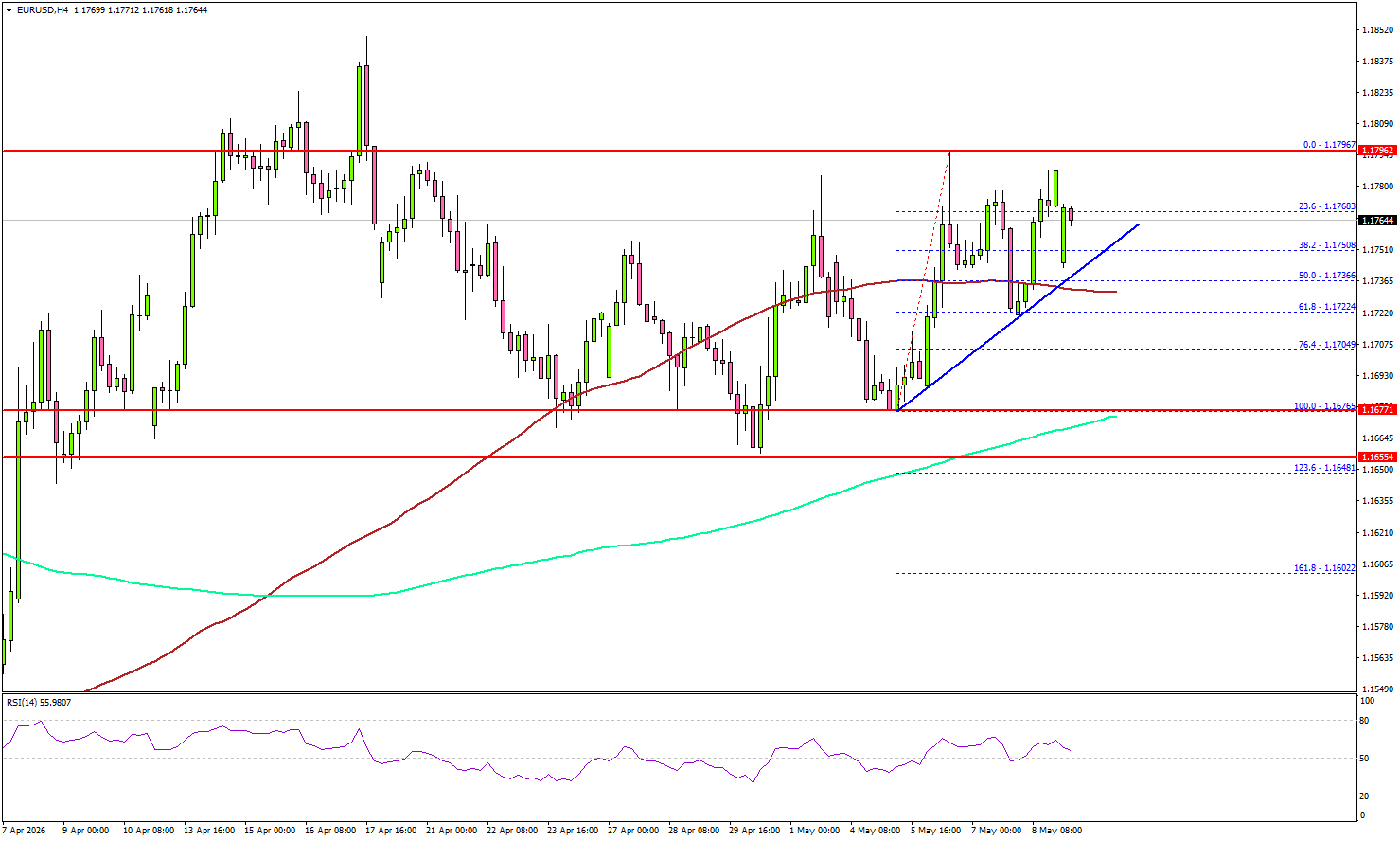

EUR/USD Poised For Upside Break As Buying Pressure Builds

Key Highlights

- EUR/USD stayed above 1.1675 and might attempt another increase.

- A bullish trend line is forming with support at 1.1750 on the 4-hour chart.

- GBP/USD seems to be consolidating gains above 1.3520.

- Bitcoin remains supported and might aim for a move above $82,000.

EUR/USD Technical Analysis

The Euro found support near 1.1675 against the US Dollar. EUR/USD started a fresh increase above the 1.1700 and 1.1720 resistance levels.

Looking at the 4-hour chart, the pair settled above the 1.1750 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). However, the bears are still active near the 1.1800 zone.

A high was formed at 1.1796, and the pair is now consolidating gains above 1.1750. There is also a bullish trend line forming with support at 1.1750 on the same chart.

On the upside, the pair faces resistance at 1.1780. The first major resistance sits at 1.1800. The main resistance could be 1.1840. A close above 1.1840 could open doors for gains above 1.1880. In the stated case, the bulls could aim for a move to 1.1950.

Immediate support is seen at 1.1750. The next support could be 1.1720. A close below 1.1720 might push the pair toward 1.1675. Any more losses could initiate a fresh move to 1.1550 in the coming days.

Looking at GBP/USD, the pair is showing positive signs, and the bulls could aim for a move above the 1.3650 resistance.

Upcoming Key Economic Events:

- US Existing Home Sales for April 2026 (MoM) - Forecast -1.1%, versus -3.6% previous.

China Inflation Heats Up as PPI Hits 45-Month High

China’s inflation data surprised to the upside in April, with both consumer and producer prices accelerating more than expected. CPI rose from 1.0% yoy to 1.2% yoy, beating forecasts of 0.9% yoy, while PPI surged from 0.5% yoy to 2.8% yoy, far above expectations of 1.7% yoy. The producer price reading marked a 45-month high and extended the sharp turnaround seen in March, when factory-gate prices finally ended a 41-month deflation streak with a 0.5% increase.

A major driver behind the CPI acceleration was transportation and communication costs, which jumped 4.6% amid higher fuel prices linked to ongoing energy market tensions. However, the data also pointed to broader inflation pressures emerging within the economy. Core CPI, which strips out volatile food and energy components, rose around 1.1%, suggesting price gains are not confined to commodities alone.

The stronger-than-expected inflation readings may reinforce expectations that China’s prolonged disinflation cycle has now decisively turned. Rising factory-gate prices could eventually feed further into consumer inflation in coming months, especially if energy costs stay elevated and domestic demand continues stabilizing.

| Indicator | Previous | Expected | Latest |

|---|---|---|---|

| CPI YoY | 1.0% | 0.9% | 1.2% |

| Core CPI YoY | 1.1% | 1.1% | 1.1% |

| PPI YoY | 0.5% | 1.7% | 2.8% |

BoJ Intervenes Again as Equities Surge

USD/JPY remained volatile last week as another suspected round of Bank of Japan intervention triggered sharp intraday swings during Japan’s Golden Week holiday period, when thinner liquidity amplified market moves. The pair briefly tested the 155 area before recovering to close the week little changed overall. Reports suggest Japanese authorities may have spent close to ¥10 trillion, or roughly $64–65 billion, supporting the yen since April 30, reinforcing the message that officials are determined to resist excessive currency weakness.

At the same time, resilient U.S. economic data continued to support the dollar. April nonfarm payrolls rose by 115,000, well above expectations of 62,000, marking a second consecutive upside surprise in labor market data. The stronger employment backdrop complicates the Federal Reserve’s path toward rate cuts, particularly as inflation risks tied to elevated energy prices continue to linger.

Despite these macro headwinds, global equities extended their rally. Strong corporate earnings and persistent enthusiasm around AI-related technology shares kept investor sentiment firmly risk-positive. The Nasdaq advanced for a sixth consecutive week, while Japan’s Nikkei 225 surged to fresh record highs, driven by semiconductor and technology stocks.

Bitcoin also continued to trend higher as broader “risk-on” sentiment encouraged flows into higher-beta assets. Meanwhile, WTI crude oil retreated back below the $100 handle as markets continued to price in hopes of a potential U.S.–Iran agreement. Traders remain focused on Tehran’s response to Washington’s latest 14-point memorandum proposal, with expectations for a diplomatic breakthrough helping to reduce part of the geopolitical risk premium embedded in energy markets.

However, beneath the surface, cracks in sentiment remain visible. The University of Michigan consumer sentiment index fell sharply to 48.2 in early May, its lowest reading on record, highlighting growing concerns among consumers over inflation and purchasing power pressures.

Markets This Week

U.S. Stocks

U.S. equities remained firm last week, with the Nasdaq once again reaching fresh record highs. However, the Dow Jones Industrial Average continues to struggle below its February highs, reflecting a more selective rally beneath the surface.

Strong earnings results and lower oil prices supported risk appetite as traders continued to anticipate a relatively quick resolution to the Middle East conflict. For now, buying on weakness remains the preferred strategy while momentum stays constructive.

Resistance levels are located at 50,000, 50,500, and 51,000. Support is seen at 49,000, 48,500, 48,000, 47,000, and 46,000.

Japanese Stocks

Following the Golden Week holiday, the Nikkei 225 surged to fresh all-time highs, supported by ongoing optimism around AI and semiconductor-related shares. Notably, the stronger yen following suspected intervention had little impact on Japanese equities, highlighting the strength of underlying bullish momentum.

The breakout to new highs remains technically positive, suggesting traders may prefer to avoid fighting the uptrend. Waiting for pullbacks toward the 10-day moving average could provide more attractive entry opportunities this week.

Resistance is seen at 64,000, 65,000, 66,000, 67,000, and 68,000, while support is located at 62,000, 61,000, 60,000, 58,500, and 57,000.

USD/JPY

Another apparent round of yen-buying intervention from the Bank of Japan triggered several sharp declines in USD/JPY during the holiday period, when thinner market liquidity increased the effectiveness of official action.

However, despite repeated warnings from Japanese officials and persistent intervention risk, USD/JPY still finished the week broadly unchanged. This suggests underlying demand for dollars remains firm while U.S. yields stay elevated.

The upside may remain capped while intervention fears persist, but buying interest continues to emerge on dips. In the current environment, range trading and taking advantage of short-term volatility may remain the more effective strategy.

Resistance levels are at 157.00, 158.00, 159.00, 160.00, and 160.50, while support is seen at 156.00, 155.00, 154.00, and 152.50.

Gold

Gold found support last week as WTI oil prices eased lower and long-term U.S. yields softened modestly. The move helped bullion break above its recent downtrend and encouraged some longer-term buyers to re-enter the market.

However, with the 10-day moving average still tracking sideways, the broader structure continues to favor range trading rather than a sustained breakout.

Resistance levels are located at $4,750, $4,900, $5,000, and $5,100, while support sits at $4,550, $4,500, and $4,400.

Crude Oil

Negotiations between the U.S. and Iran remained the dominant driver for WTI crude oil last week, with markets increasingly pricing in the possibility of a diplomatic breakthrough in the coming weeks.

Those expectations helped push WTI back below the $100 level as traders reduced part of the geopolitical premium built into prices during the conflict escalation.

However, negotiations are still expected to take time, and headline-driven volatility is likely to remain elevated. In this environment, fading extreme short-term moves may continue to be the preferred strategy for active traders.

Resistance is located at $100, $110, and $120, while support sits at $90, $80, $75, $70, and $67.50.

Bitcoin

Bitcoin continued to grind higher last week as improving market sentiment and renewed appetite for risk assets supported demand. Optimism surrounding a possible easing in geopolitical tensions also helped sentiment across crypto markets.

However, ETF-related selling flows continued to limit upside momentum at times during the week.

The broader outlook remains constructive while Bitcoin holds above the key $75,000 support zone, suggesting buying opportunities may still be favored on pullbacks.

Resistance levels are at $82,500, $85,000, and $90,000, while support is located at $75,000, $65,000, $60,000, and $55,000.

This Week’s Focus

- Monday: China CPI and PPI, U.S. Existing Home Sales

- Tuesday: Japan Household Spending, German CPI, E.U. ZEW Economic Sentiment, U.S. CPI

- Wednesday: Japan Current Account, E.U. GDP and Industrial Production, U.S. PPI

- Thursday: U.K. GDP, Industrial Production and Trade Balance, U.S. Retail Sales

- Friday: U.S. NY Empire State Manufacturing Index and Industrial Production

USD/JPY will remain a major focus this week as traders continue to test whether Japanese authorities are prepared to defend the yen aggressively around the 157 area, or whether intervention activity begins to fade.

At the same time, ongoing U.S.–Iran negotiations will continue to shape broader market sentiment, particularly through their impact on oil prices and inflation expectations. Equity markets will attempt to extend recent gains, while upcoming U.S. inflation and retail sales data could prove critical in determining whether higher energy prices are beginning to materially impact inflation trends and consumer demand.

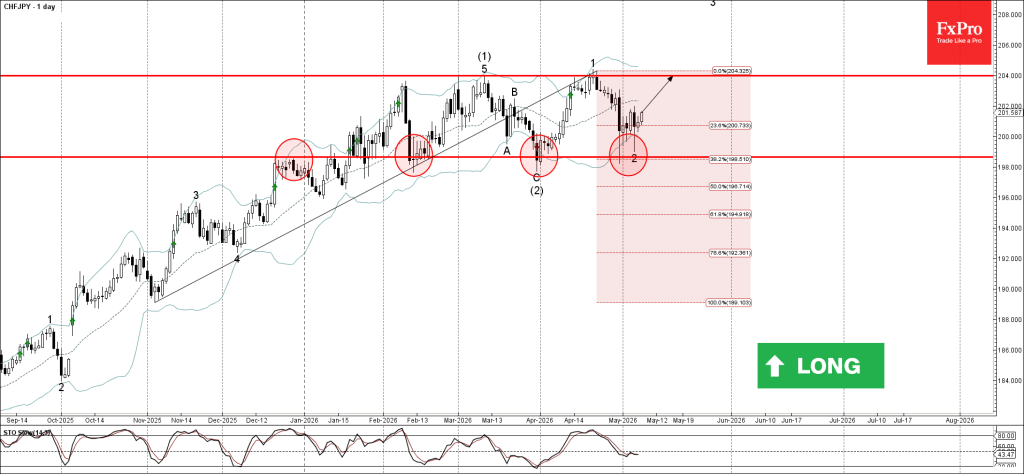

CHFJPY Wave Analysis

CHFJPY: ⬆️ Buy

- CHFJPY reversed from support zone

- Likely to rise to resistance level 204.00

CHFJPY currency pair recently reversed from the support zone between the support level 198.65 (which has been reversing the price from the middle of February), 38.2% Fibonacci correction of the upward impulse from November and the lower daily Bollinger Band.

The upward reversal from this support zone created the daily Hammer, which stopped the previous minor correction 2.

Given the strong daily uptrend, CHFJPY currency pair can be expected to rise to the next resistance level 204.00 (which stopped impulses (1) and 1).

Eco Data 5/11/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 01:30 | CNY | CPI Y/Y Apr | 1.20% | 0.90% | 1.00% | |

| 01:30 | CNY | PPI Y/Y Apr | 2.80% | 1.70% | 0.50% | |

| 14:00 | USD | Existing Home Sales Apr | 4.02M | 4.05M | 3.98M | 4.01M |

| 01:30 | CNY |

| CPI Y/Y Apr | |

| Actual | 1.20% |

| Consensus | 0.90% |

| Previous | 1.00% |

| 01:30 | CNY |

| PPI Y/Y Apr | |

| Actual | 2.80% |

| Consensus | 1.70% |

| Previous | 0.50% |

| 14:00 | USD |

| Existing Home Sales Apr | |

| Actual | 4.02M |

| Consensus | 4.05M |

| Previous | 3.98M |

| Revised | 4.01M |