Sample Category Title

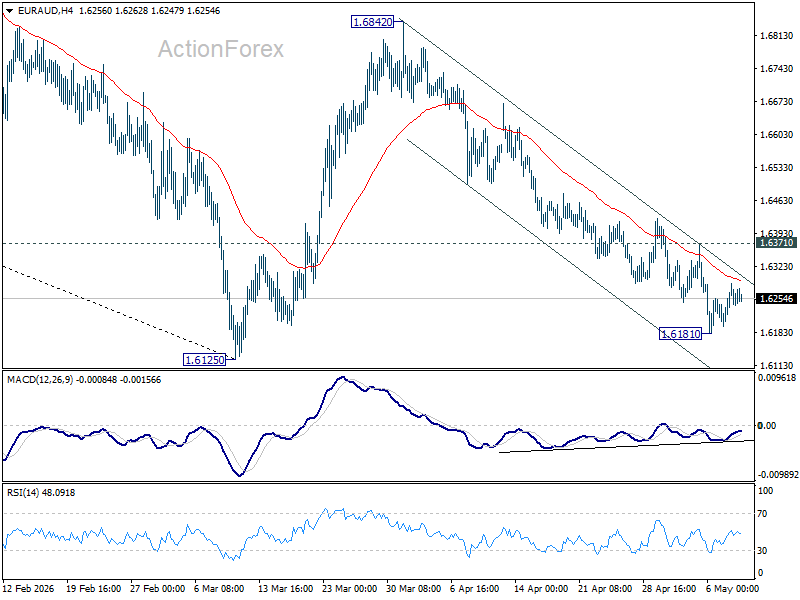

EUR/AUD Weekly Outlook

EUR/AUD's fall from 1.6842 extended lower last week but recovered ahead of 1.6125 low. Initial bias is turned neutral this week first. On the downside, decisive break of 1.6125 will resume larger fall from 1.8554. Nevertheless, break of 1.6371 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound to 55 D EMA (now at 1.6525).

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7068) holds, even in case of strong rebound.

In the longer term picture, fall from 1.8554 is seen as the third leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). Sustained trading below 55 M EMA (now at 1.6590) will confirm this bearish case, and pave the way back towards 1.4281.

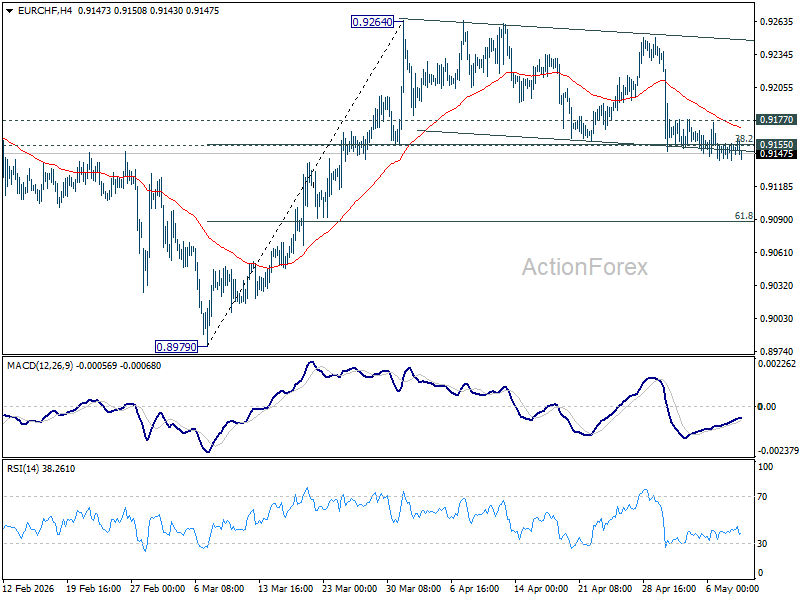

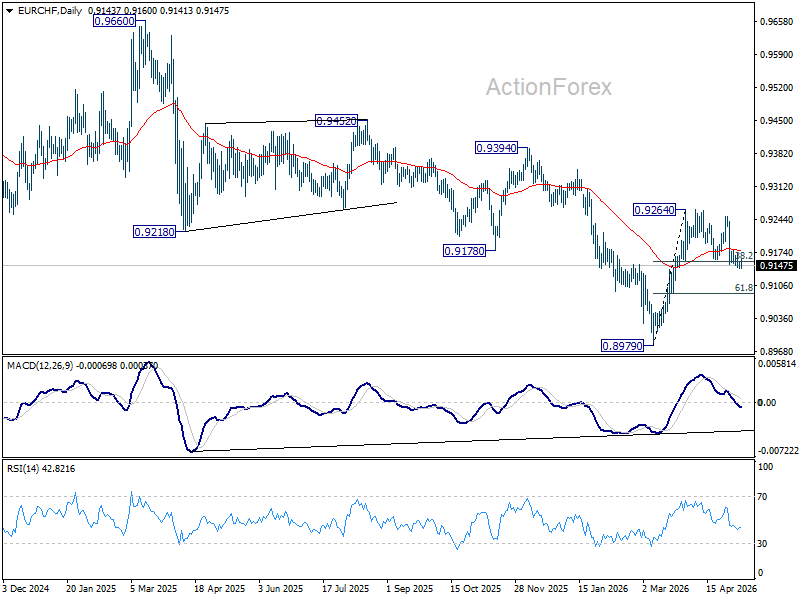

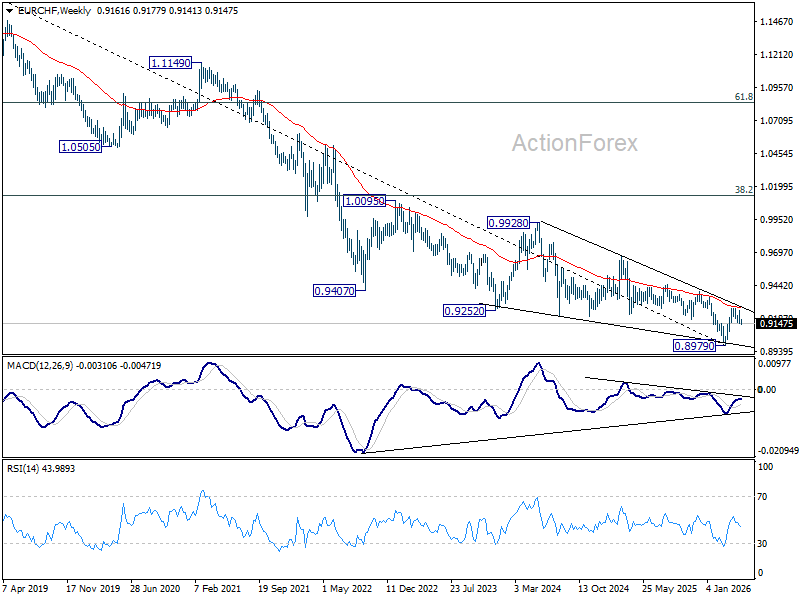

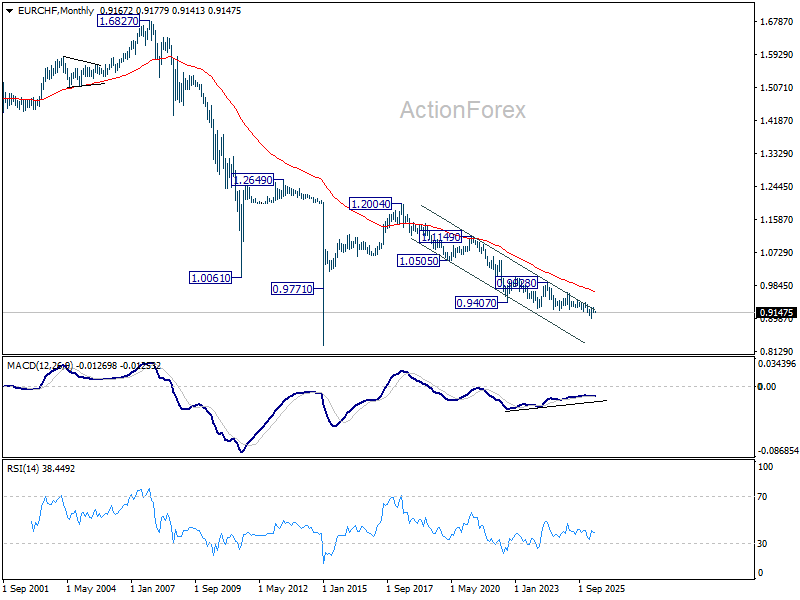

EUR/CHF Weekly Outlook

EUR/CHF edged lower last week but failed to get rid of 0.9155 cluster support (38.2% retracement of 0.8979 to 0.9264 at 0.9155) cleanly. Initial bias stays neutral this week first. On the upside, break of 0.9177 minor resistance will turn bias back to the upside for 0.9264 resistance. However, sustained trading below 0.9155 will turn bias back to the downside for deeper pullback to 61.8% retracement at 0.9088 and possibly below.

In the bigger picture, considering bullish convergence condition in W MACD, a medium term bottom should be in place at 0.8979. Sustained trading above 55 W EMA (now at 0.9268) will add more credence to this case. Further break of 0.9394 resistance will pave the way to 0.9660 resistance next. However rejection by the 55 W EMA will set up another fall through 0.8979 low at a later stage.

In the long term picture, outlook will stay bearish as long as 0.9407 support turned resistance (2022 low) holds. However, firm break of 0.9407 will argue that the down trend from 1.2004 (2018 high) has completed with five waves down to 0.8979. Stronger rebound should then be seen to 38.2% retracement of 1.2004 to 0.8979 at 1.0135 in the medium term.

Markets Weekly Outlook – Is the ‘Risk-On’ Rally Sustainable with Rates and Energy Elevated?

- Equities maintain a "risk-on" rally, defying the market disconnect from elevated oil prices and rising interest rate expectations.

- The US market faces a pivotal week with the final Powell-led CPI report expected on Tuesday, ahead of the Fed Chair handover to Kevin Warsh on May 15.

- Geopolitical tensions remain high following US/Iran strikes, though a 3-day Russia-Ukraine ceasefire was announced.

- The US Dollar Index (DXY) is showing a bearish technical breakdown, with a cooler CPI likely to lead to a move toward the 96.901 support level.

Week in Review: Equities Defy Gravity as Oil and Rates Realign

The start of May has left market participants with more questions than answers. In a striking display of resilience or perhaps denial, US stock markets have surged to fresh highs, seemingly shrugging off the geopolitical tensions that briefly rattled indices mid-war.

However, this "risk-on" euphoria sits in uncomfortable contrast with the reality of the energy market. Oil prices have refused to retreat to pre-conflict levels, and interest rate expectations are being recalibrated higher across the board.

The disconnect is clear: can equities continue to climb while the cost of capital and energy remain elevated?

Geopolitical Developments

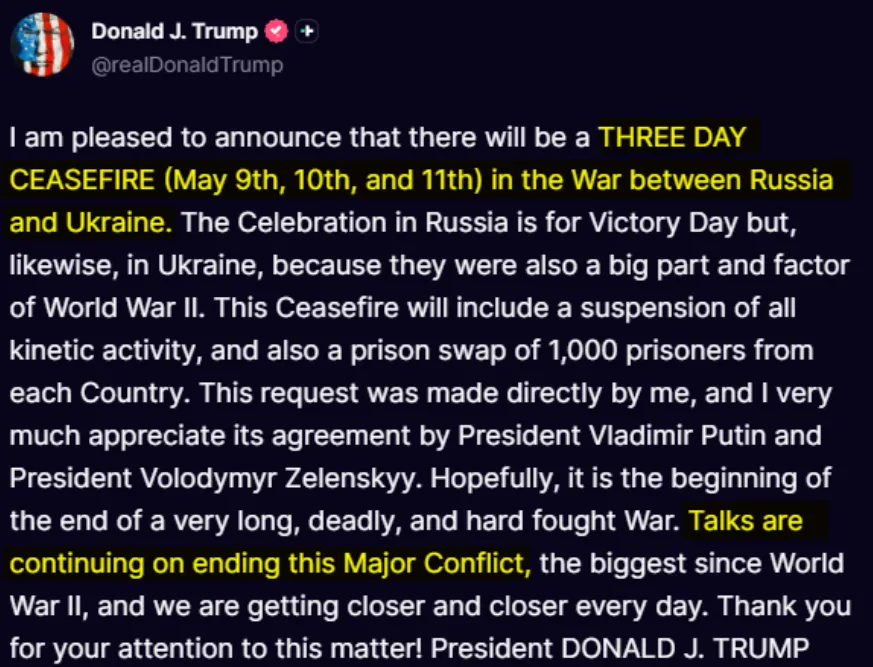

Markets continue to hang on every word of US President Donald Trump and the ongoing situation in the Middle East. Markets are rightly on edge heading into the weekend given the tit-for-tat strikes between Iran and the US on Thursday and Friday, May 7 and 8 respectively. Any significant developments over the weekend could drive early week volatility and price action.

Late on Friday, President Trump announced a 3 day ceasefire between Russia-Ukraine for the 9th, 10th and 11th of May.

Source: TruthSocial

Week Ahead: Central Bank Divergence and Inflation Storms Loom Large

As we look toward the week starting May 10, the focus remains on geopolitical nut markets, which are also debating whether central banks will follow the market’s hawkish lead or if a reality check is overdue.

This makes for interesting viewing and will likely lead to significant market movement.

US: The Fed’s Final Changing of the Guard

The coming week is a momentous one for the Federal Reserve. Not only do we face critical data points, but we also mark a transition in leadership. Jerome Powell is set to conclude his tenure as Fed Chair, with Kevin Warsh scheduled to take the reins on Friday, May 15.

On the data front, Tuesday’s Inflation report is the headliner. We are bracing for a second consecutive 0.9% MoM print at the headline level, largely fueled by the surge in gasoline and diesel prices. While the core reading is expected at a more modest 0.3%, the annual rate could push up to 2.7%. The Fed has recently made a concerted effort to talk up rate expectations, ditching their previous easing bias as the US economy continues to hold up better than its peers. However, with labor supply growth effectively stalled due to collapsing net migration (projected at near zero this year), the "hot" jobs numbers we’ve seen may be less a sign of strength and more a symptom of a tightening supply constraint.

UK & Europe: A Strange Case of Mispricing

Across the Atlantic, the Bank of England (BoE) and the European Central Bank (ECB) find themselves in different boats, though markets are currently pricing them as if they are in the same storm.

Markets are pricing in a significantly more hawkish path for the UK than the Eurozone—a move that looks overdone. While the UK is energy-dependent, this is not a repeat of the 2022 gas crisis; natural gas prices remain relatively contained compared to the spike in oil. We believe the ECB is actually more likely to deliver on its hawkish rhetoric in June, whereas the BoE may view "not cutting" as enough tightening for now. Watch the Euro and Sterling closely as this pricing discrepancy begins to unwind.

Asia: Inflation Fallout and Trade Tensions

In Asia, the focus is squarely on the fallout from the Middle East through the lens of inflation.

- China: We are looking for trade data on Saturday and inflation data on Monday. Exports are expected to grow by roughly 6.5%, but the real story lies in the PPI, which is accelerating. Markets will be hyper-sensitive to how China handles the impact of higher energy costs and the lingering effects of the "Liberation Day" tariffs.

India: Expect a modest rise in inflation. While gasoline prices remain capped by the government, the second-round effects of oil prices are starting to bleed into food costs, which could test the Reserve Bank of India’s patience.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week - US Dollar Index (DXY)

The US Dollar Index (DXY) finds itself in a precarious position as we head into a pivotal week. Between the transition in Fed leadership and a looming inflation print, the technicals are flashing signs of exhaustion, suggesting the "Dollar King" crown might be slipping.

On the daily timeframe, the indexes break below its ascending channel, signaling a shift in momentum remains intact.

We are currently seeing the DXY trade below key Moving Averages:

The 50-day MA (Yellow) at 98.459 and the 200-day MA (Purple) at 98.538 have converged, effectively acting as a "ceiling" for recent price action.

The fact that price is struggling to reclaim these MAs suggests that the path of least resistance remains to the downside in the near term.

Support Watch: The immediate floor sits at 97.702. A daily close below this level would confirm the Double Top and likely open the trapdoor for a deeper correction toward the 96.901 handle.

Scenarios for the Week Ahead

Given the fundamental backdrop of the final Powell-led CPI print and the handover to Kevin Warsh, I see two primary technical paths:

Scenario 1: The Bearish Confirmation (High Probability)

If Tuesday’s US CPI data comes in cooler than expected—or even just meets estimates—the DXY is likely to break the 97.702 support. This would confirm the Daily Double Top and trigger a move toward 96.901. In this scenario, the convergence of the 50 and 200 SMAs on the daily will remain the ultimate barrier, cementing a medium-term bearish outlook.

Scenario 2: The "Sticky Inflation" Spike (Low Probability)

Should we get a significant beat in inflation (above the 0.9% MoM forecast), we could see a knee-jerk spike in the Dollar. The bulls would need to reclaim and hold above 98.729 on a daily closing basis to invalidate the bearish setup. However, even with a spike, the psychological resistance at 100.00 remains a massive hurdle that would likely attract heavy selling.

US Dollar Index (DXY) Daily Chart, May 8, 2026

Source:TradingView.Com (click to enlarge)

The market is currently betting on a "perfect landing" where growth stays firm despite rising rates. However, with the energy channel remaining hot and central banks diverging, the margin for error is becoming razor-thin. Stay disciplined and watch those support levels.

The Weekly Bottom Line: Labor Market Resilient Despite Energy Shock

Canadian Highlights

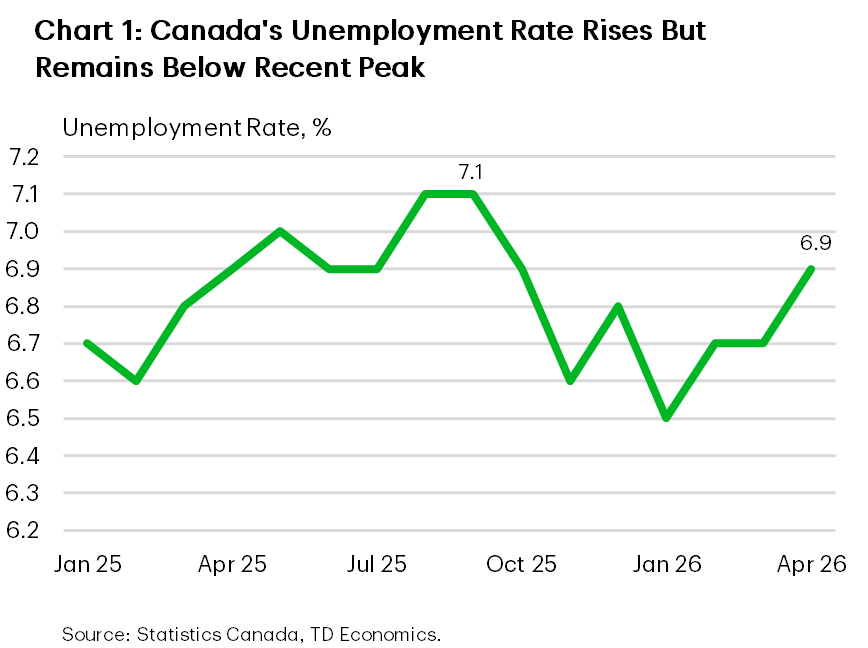

- Canada’s labour market remained soft in April, with employment down and the unemployment rate rising to 6.9%.

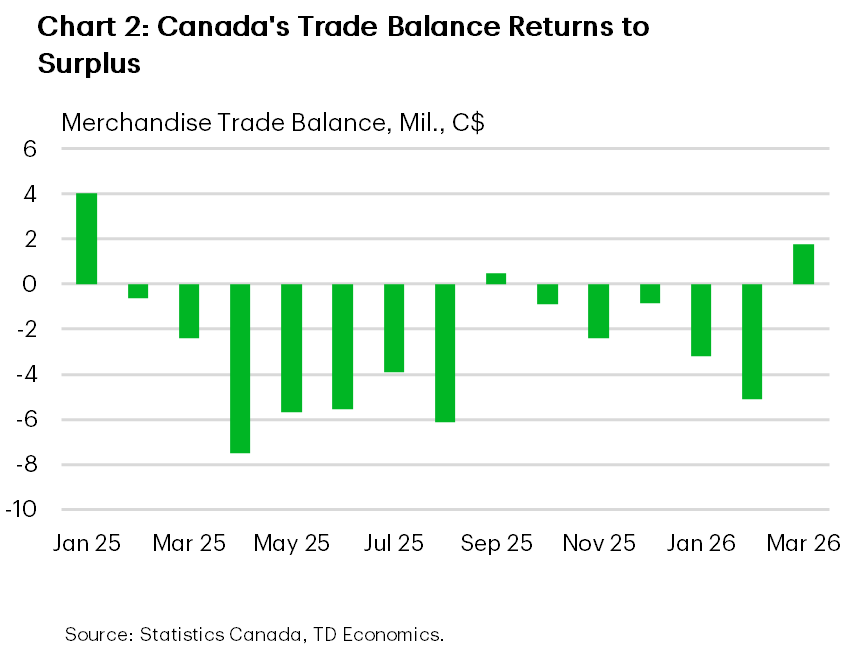

- Canada’s trade balance returned to surplus in March on stronger commodity exports, though net trade is still likely to subtract from Q1 GDP growth.

- A soft labour market and weak ex-energy trade should keep the Bank of Canada in a wait-and-see mode despite energy prices.

U.S. Highlights

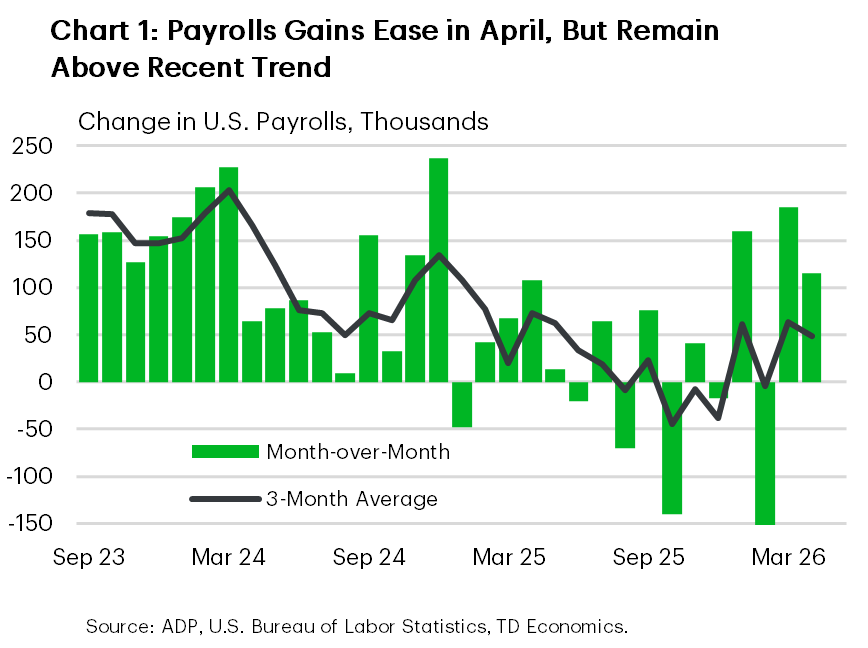

- U.S. payroll growth was solid in April, defying market expectations, while the unemployment rate held steady at 4.3%.

- Historically lean jobless claims reaffirmed a muted environment for layoffs, while the ISM Services Index signaled continued expansion in the services side of the economy.

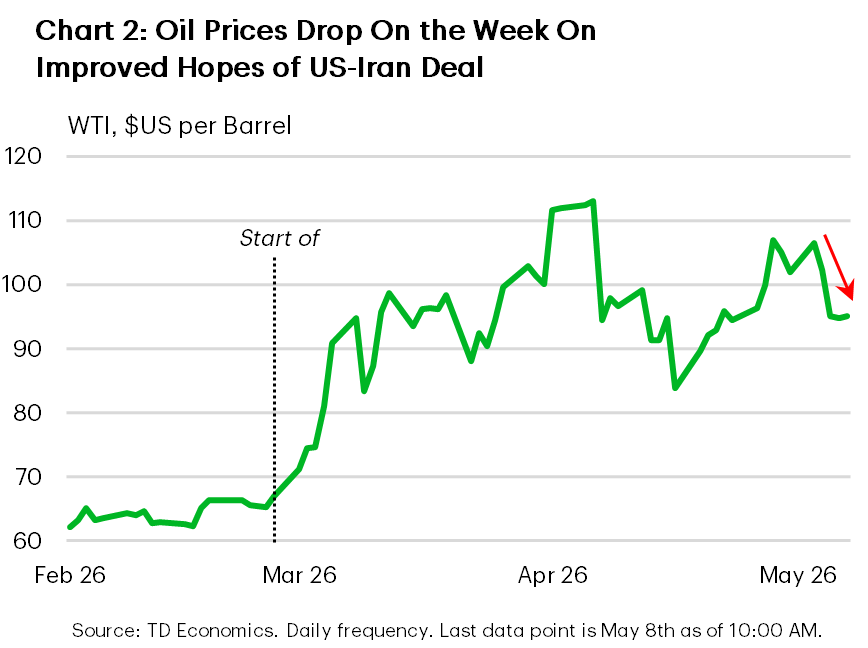

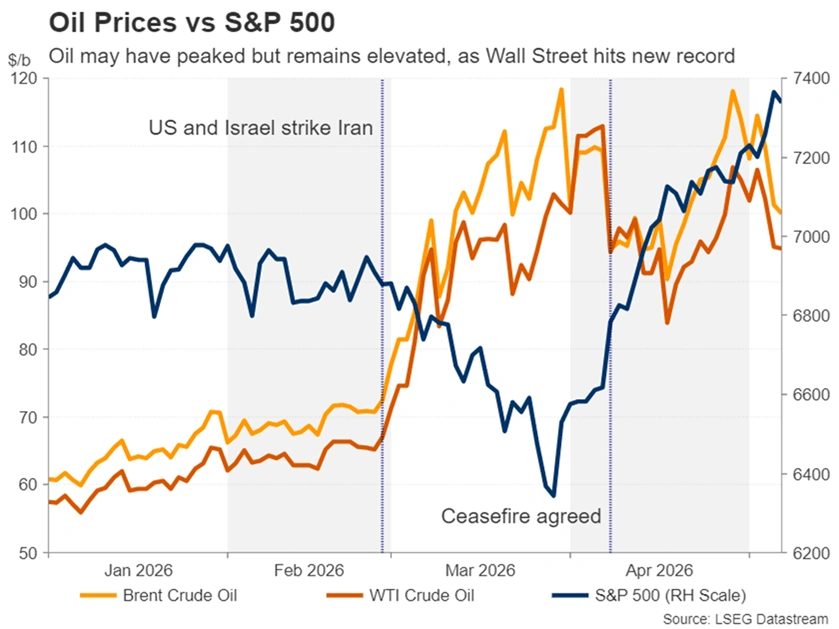

- Volatility in oil prices continued this week as WTI crude oil retreated from $105 per barrel to the mid-$90s later in the week on hopes of a breakthrough in U.S.-Iran negotiations.

Canada – More Reason to Wait and See

The price of oil prices slid below $100 this week (WTI benchmark) on optimism surrounding a potential U.S.-Iran deal, helping both bond and equity markets regain their footing. Canada’s S&P/TSX Composite Index rose 0.6% on the week, though the gain was not enough to prevent it from surrendering its position as the world’s seventh-largest equity market to South Korea (the KOSPI). Bond markets also rallied, pushing 5- and 10-year Government of Canada benchmark yields down 9 basis points to 3.5% and 3.1%, respectively.

April’s jobs report provided a softer read on the economy. According to Statistics Canada, employment was little changed in April, declining by 18k versus expectations for a 10k gain, while the unemployment rate edged up to 6.9% (Chart 1). The labour force participation rate ticked up to 65.0%, contributing to the rise in unemployment. The increase in participation could be viewed as a modest positive, with workers being drawn into the labour market often a vote of confidence in job prospects. That said, there was little evidence of broader momentum beneath the surface. Meanwhile, wage growth decelerated in April, with constant-composition measures showing little improvement.

To some extent, this lack of labour market dynamism works in the Bank of Canada’s favour by helping contain broader price pressures from the energy price shock. The Bank has continued to characterize labour conditions as “soft”, reflecting subdued hiring and weaker demand for workers. As such, this report is unlikely to materially alter its current wait-and-see approach.

A similar message came from the trade report. Canada’s trade balance moved back into surplus in March after five consecutive monthly deficits (Chart 2). However, the improvement was largely driven by commodity prices and precious metals rather than broad-based external demand. Export values surged on higher crude oil prices and increased gold shipments, while imports pulled back following February’s outsized gain.

Excluding metal, mineral, and energy products, export growth was far more moderate. As a result, March’s trade report likely overstates the strength of the external sector. We continue to expect net trade to subtract from Q1 2026 real GDP growth, reflecting stronger imports over the quarter. If energy prices remain elevated, nominal exports and the trade balance should improve further in Q2 even if real export volumes remain subdued

Higher energy exports, however, offer little consolation to consumers. Our proprietary card-spending data show gas station spending rising 3.6% on the month and 16.7% on the year in April, before the gas tax holiday took effect, adding pressure to household budgets. The Bank of Canada has indicated it stands ready to respond should higher energy prices feed more broadly into inflation, but for now there is little reason for policymakers to move decisively in either direction.

U.S. – Labor Market Resilient Despite Energy Shock

U.S. financial markets remained firm this week. The S&P 500 advanced roughly 2% to new record highs, supported by a pullback in oil prices and a better-than-expected jobs report. Long-term Treasury yields eased later in the week, with the 10-year note hovering near 4.35% – a hair below last week’s close. Market pricing continues to reflect limited expectations for near-term rate cuts amid ongoing energy market uncertainty and a relatively resilient economy.

Resiliency was on display in the April jobs report, where nonfarm payrolls rose 115,000 – almost double the market consensus forecast. The unemployment rate held steady at 4.3% amid modest declines in both household employment and the labour force. Payrolls were volatile through the first quarter, due in part to factors like inclement weather and a healthcare strike in California. Looking through the volatility, it appears that job growth has picked up from its anemic trend at the end of last year and is now running at a decent pace that’s allowing it to hold the unemployment rate steady (Chart 1). High-frequency indicators reinforced this resilient labour market picture: initial jobless claims remained very low by historical standards, while continuing claims fell to 1.77 million – a new two-year low.

Other economic data lent further support to the resilience theme. The ISM Services Index eased modestly in April but remained comfortably above the 50-point expansion threshold. The details of the report, however, had a few blemishes. New orders recorded a notable pullback, while the prices-paid component remained elevated at 70.7 – the highest level since late 2022 and up notably from earlier this year – pointing to persistent cost pressures in the services sector.

With respect to prices, the good news is that the price of WTI crude oil, which had surged above $105/barrel late last week, fell back to the mid-$90s over the course of this week (Chart 2). This followed reports of U.S.–Iran negotiations and tentative de-escalation signals around the Strait of Hormuz. While constructive for inflation expectations, sustained disinflation will depend on a more durable resolution to the tensions.

These developments are likely front-of-mind for Fed Chair-nominee Kevin Warsh as he prepares to take the helm. Communication from the Fed this week maintained a cautious stance, with New York Fed President John Williams emphasizing that policy is “well positioned” to balance the risks to the dual mandate. Under the current backdrop, market odds remain strongly in favor of no Fed action over the near term, with the probability that rates are held steady this year still sitting at over 70%. Ultimately, this morning’s better-than-expected jobs report, alongside other high-frequency indicators, helps ease concerns that the U.S. labour market has continued to deteriorate. This should give policymakers more breathing room to assess the extent to which higher energy prices filter into core inflation over the coming months.

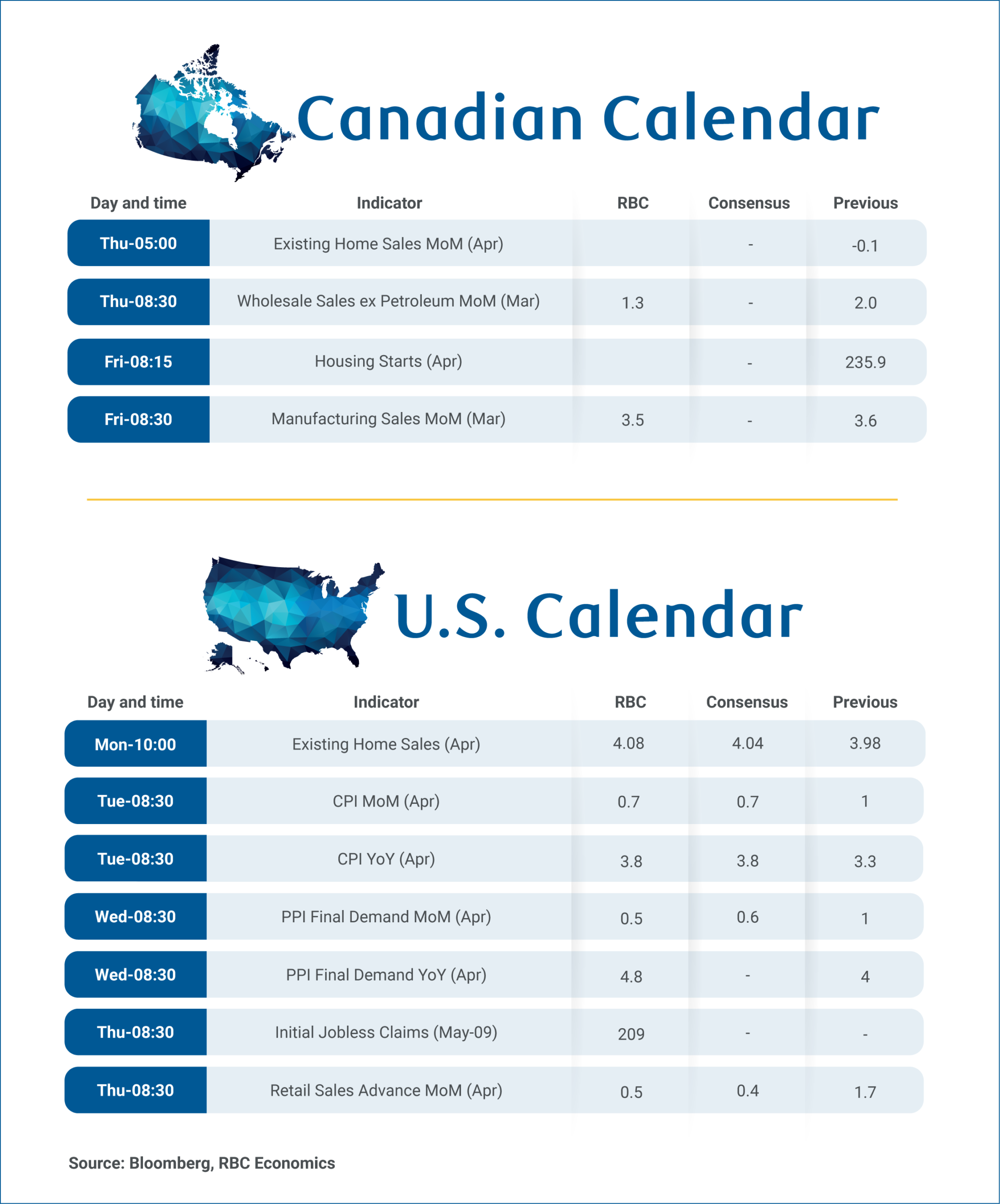

Canada’s Industry Data to Show Steadiness Amid Pressure from Tariffs, Disruptions

The week ahead is relatively quiet for major Canadian data releases, but industry reports will offer important signals about the economy’s momentum heading into spring.

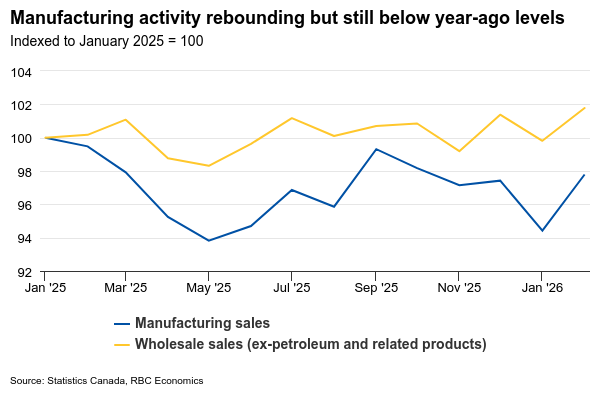

Early signs from Statistics Canada’s advance estimates suggest wholesale trade for April on Thursday and manufacturing sales next Friday should show the sectors finding their footing after significant disruptions to motor vehicle production earlier in the year.

Early estimates showed March manufacturing sales rising 3.5%, lifted by the petroleum and coal product subsector as energy prices surged amid escalating Middle East conflicts, along with further recovery in the transportation sector. Separately reported data from the Industrial Product Price Index suggests about half the increase was due to higher prices, but that would still leave ‘real’ sales up about 1.7%.

This is significant, because the sector has been under pressure. As of February, manufacturing was still running below levels a year ago, weighed down by product specific tariffs on products like steel and aluminum as well as the motor vehicle sector. Yet, recent data points to a steadying trend. Both trade flows and manufacturing output have shown signs of stabilization, and U.S. tariffs have been broadly edging lower.

Wholesale trade tells a similar story. The advance indicator showed core sales (which exclude the price-related increases in petroleum and related products) rose 1.3% in March.

Housing data for April will also be released next week. Early results from local real estate boards show more sellers entering the market, with new listings reaching record levels in Montreal and Ottawa. Home resales rose month-over-month in Toronto (up 6.1%), Calgary and Edmonton, though remained weaker year-over-year in most markets. Buyers continue to hold stronger negotiating power in Vancouver and Toronto where ample inventory is sustaining price corrections—Toronto’s MLS HPI fell 6.5% year-over-year while Vancouver’s dropped 6.9%. The spring season has yet to deliver a clear boost to demand, with confidence constrained by trade uncertainty, job market concerns and affordability challenges.

South of the border, U.S. consumer prices data for April are expected to show headline inflation ticking higher to 3.8% year-over-year, driven by rising gasoline prices. Core inflation, which strips out volatile food and energy categories, is expected to remain more subdued, edging to 2.7% year-over-year.

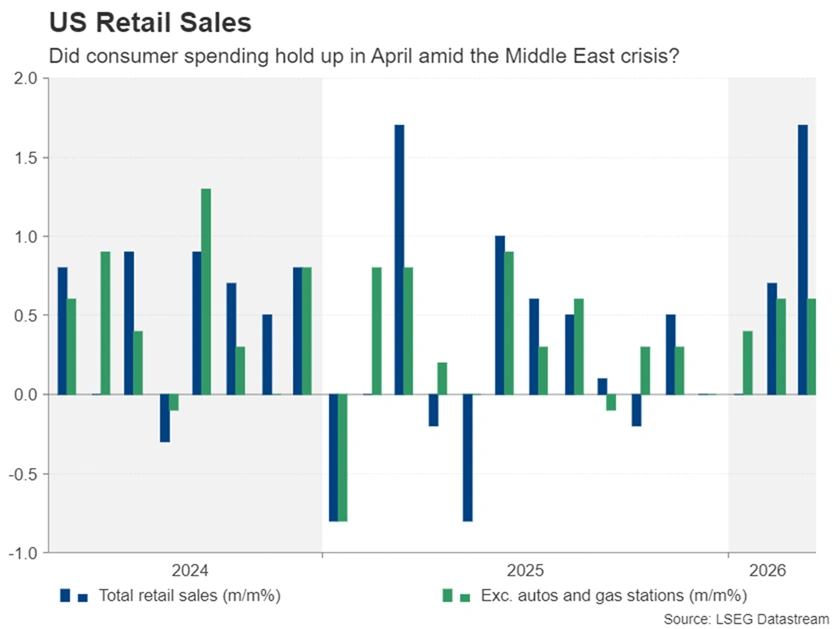

U.S. retail sales are expected to tick up 0.5% in April, decelerating from the robust 1.7% in the prior month. Unit auto sales posted a decline in April following two consecutive months of growth, but that was offset by higher sales at gas stations due to higher prices.

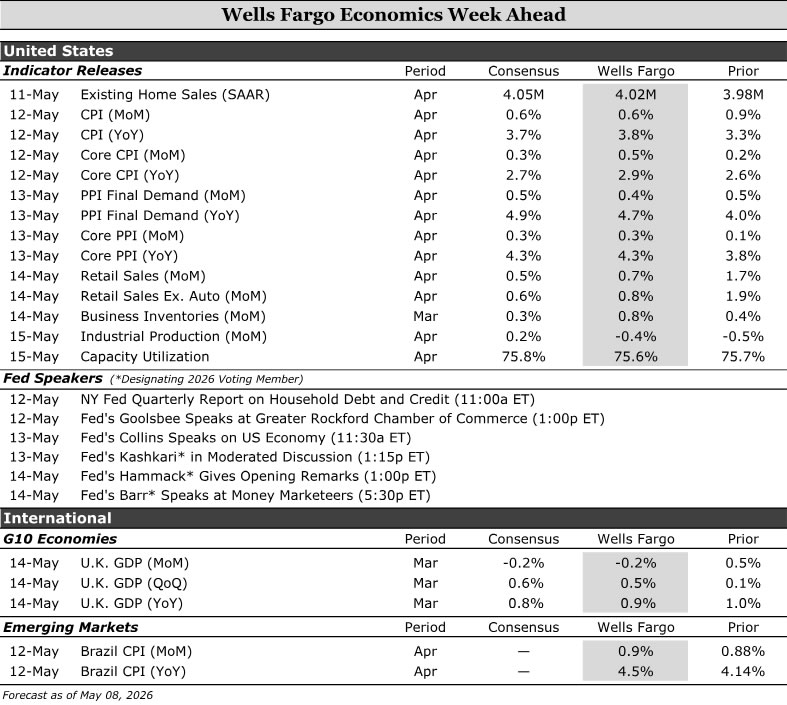

Economics Week Ahead

U.S. inflation data are set to firm modestly in April, with headline CPI rising toward 3.8% year-over-year and core holding near 2.9%, reflecting energy‑related pressures spilling into food, services and some goods even as shelter inflation continues to cool. Retail sales, meanwhile, are likely to show headline growth of about 0.7% month-over-month, but largely due to higher prices rather than stronger volumes, pointing to steady but increasingly price‑constrained consumer demand. In the UK, growth appears to be cooling after early‑quarter strength, with Q1 GDP tracking around 0.5%, consistent with a slowing but still stable economy and reinforcing the Bank of England’s cautious, data‑dependent stance. In Brazil, inflation is picking up more decisively, with April IPCA inflation near 0.9% month-over-month and around 4.5% year-over-year, highlighting rising energy and food pressures that complicate, but do not yet derail, a still‑cautious path toward policy easing.

United States:

- CPI (Tuesday), Retail Sales (Thursday)

G10 Economies:

- U.K. GDP (Thursday)

Emerging Markets:

- Brazil CPI (Tuesday)

U.S. Week Ahead

CPI • Tuesday

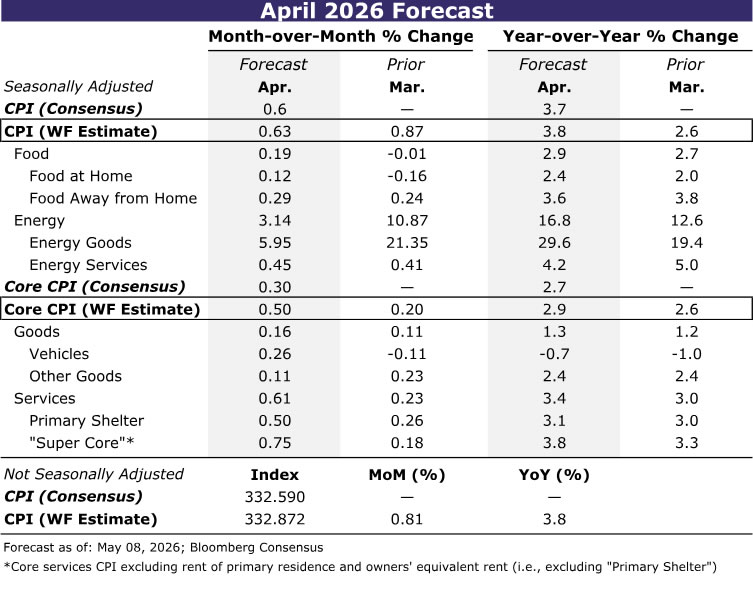

April's CPI report will be more interesting than usual. The ongoing conflict in the Middle East has kept energy prices elevated, which will start to generate more obvious spillovers into other areas of inflation. We estimate headline CPI to rise 0.63% over the month, lifting the year-over-year pace to 3.8%.

Energy goods are poised for a 6% monthly gain as the jump in crude oil prices continues to pass through to the pump. Food at home is likely to accelerate after March’s pullback, with grocery prices set to strengthen later this year amid rising transportation costs and higher fuel and fertilizer input prices.

Excluding food and energy, we look for core CPI to increase 0.50% in April and 2.9% on a year-ago basis. The monthly pop is expected to be driven by core services, where strength will be partly—but not entirely—a mirage. The unwinding of a government shutdown-related survey quirk is expected to lead primary shelter to increase at twice its recent pace. We expect shelter inflation to quickly resume its moderation in May though, as real-time rent measures point to further softening. Excluding shelter, services should be genuinely hot thanks to higher jet fuel costs leading to a jump in airfares.

Meantime, a rebound in used vehicle prices will boost core goods inflation, though price growth for other core goods is likely to cool following March’s out-sized gains in apparel and recreational goods.

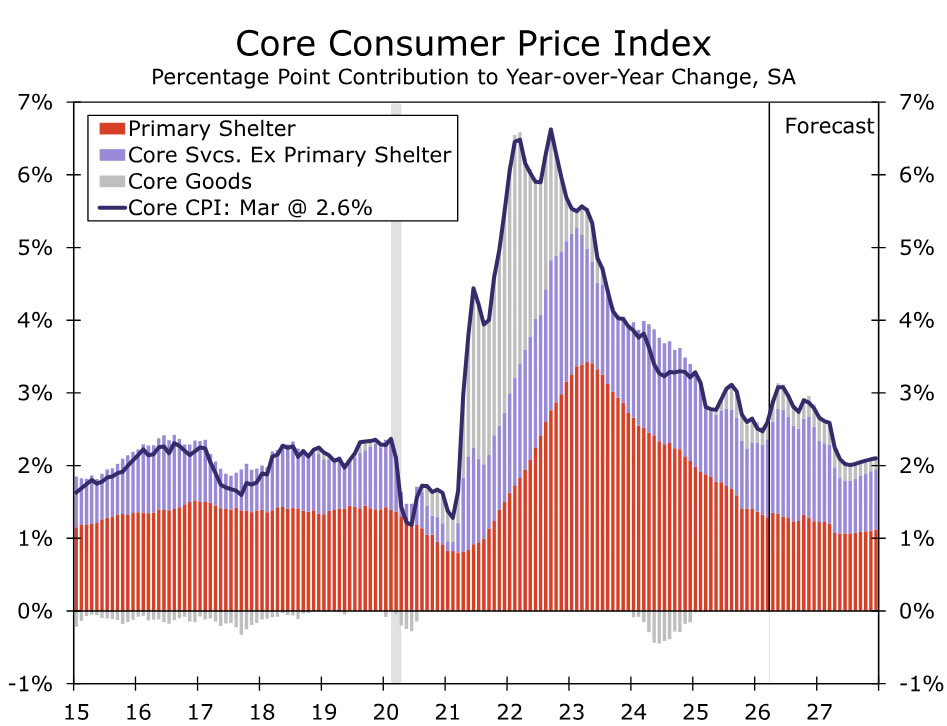

Looking ahead, we continue to forecast the year‑over‑year rate of core CPI to remain stuck close to 3.0% this year. Shelter inflation should continue to cool, but progress elsewhere is proving harder to come by. At the same time, slowing wage growth has weighed on consumer purchasing power and will likely limit firms’ ability to pass along higher costs. That should help temper broader inflation by year-end even as underlying pressures remain firm.

Retail Sales • Thursday

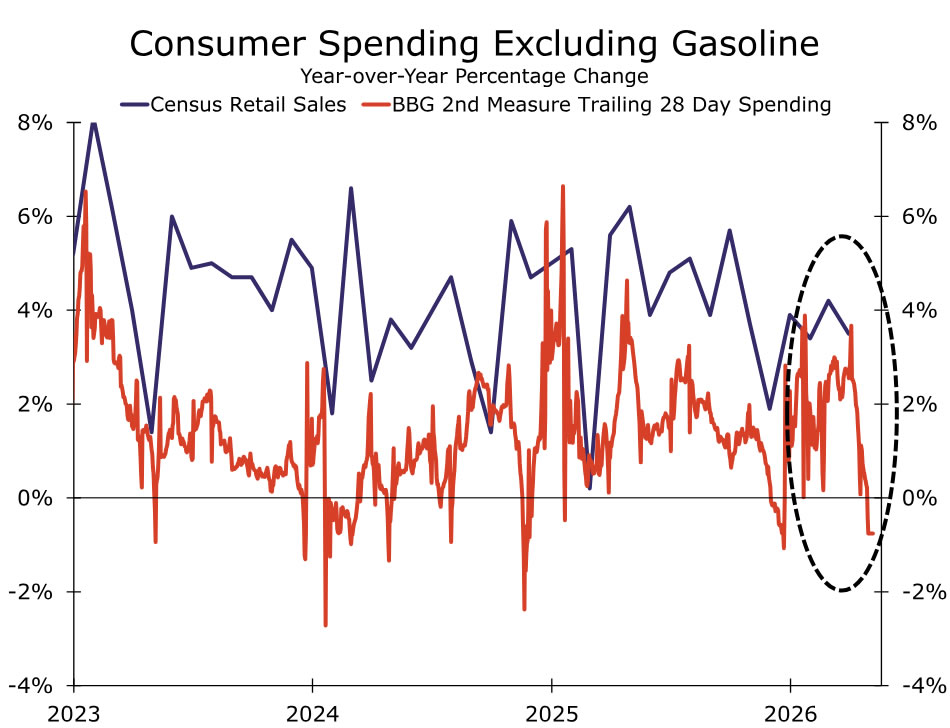

April retail sales data will be misleading at first glance as they will largely reflect higher prices rather than volumes. The data are reported nominally, thus not adjusted for inflation. While we forecast total retail sales rose 0.7% last month, after accounting for an around 0.7% gain in consumer goods prices, real retail sales were likely much weaker, potentially negative.

That's the signal we're getting from high-frequency credit card data, where spending outside gasoline collapsed last month (chart). While more volatile, the card data track decently well with the contours of retail spending.

The spending environment has ultimately grown more challenging as higher gas prices weigh on consumer purchasing power. Real household income, excluding transfer payments like unemployment benefits and social security, has trended lower and now turned modestly negative on a year-ago basis, signaling that compensation remains a key risk to households' ability to spend ahead. Consumers are saving less as a result to keep spending, and they're also relying on credit and/or their balance sheets. This all suggests a slower spending environment ahead.

G10 Week Ahead

U.K. GDP • Thursday

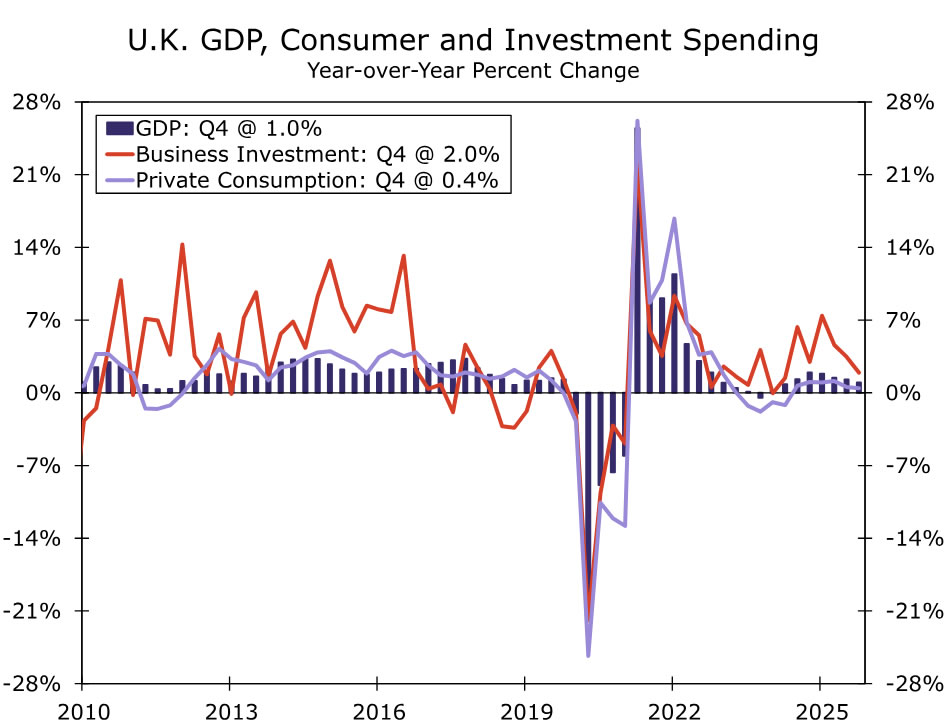

Next week brings the release of UK GDP data for March and Q1-2026. February growth surprised to the upside, with output rising 0.5% month-over-month (aside from manufacturing). For March, we expect GDP to contract by around 0.2%. That would still leave Q1 growth at 0.5%, in line with Bank of England (BoE) recent projections.

March PMIs were weak across manufacturing and services, reflecting softer sentiment and elevated uncertainty tied to the war in the Middle East. Construction was the exception, though that was supported by energy-related demand and a return to more typical weather conditions after February's unusually wet weather.

Against this backdrop, the BoE’s recent 8–1 vote to hold the Bank Rate at 3.75% struck us as broadly balanced with a slight hawkish lean. Greater emphasis on scenario-based forecasts highlighted optionality rather than a single outlook, while growth concerns partly offset inflation risks. As such, an upside GDP surprise next week would likely be treated cautiously, especially as anecdotal evidence suggests household and business activity may have been pulled forward, which could have boosted late‑March data and skewed risks to the upside. A weaker print would reinforce the Bank’s wait-and-see stance. That said, rising fertilizer prices and persistently high energy costs increase the risk of second-round inflation effects. We have therefore revised our Bank Rate outlook to include two hikes this year, up from a baseline of no changes. While uncertainty remains high and tied to developments in the Middle East, even with a rapid resolution, at least one hike may be needed to prevent second-round effects from becoming entrenched.

EM Week Ahead

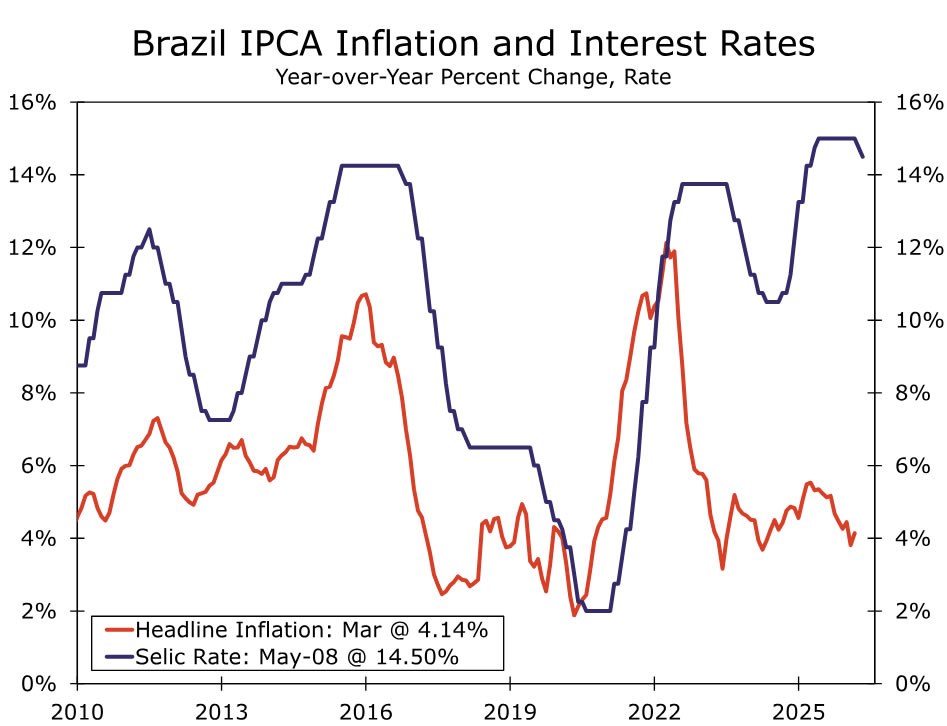

Brazil IPCA • Tuesday

We expect Brazil’s April IPCA to rise a sharp 0.9% month-over-month, pushing headline inflation to around or slightly above the top of the target band at 4.5% year-over-year. Energy remains the key near‑term upside risk, with the Middle East conflict lingering and physical supply constraints becoming more binding, driving stronger pass‑through into refined products. Food inflation was already firming in March, and higher transport and fertilizer costs should broaden price pressures across food categories in coming months.

While core inflation remains restrained by restrictive real rates, administrative price smoothing and fiscal offsets, particularly in an election year, are adding upside risks to inflation expectations. Median 2026 expectations have risen to 4.9% from 3.9% prior to the US‑Iran war, per the Brazilian Central Bank's (BCB) FOCUS Survey. Against this backdrop, we think the BCB is likely to proceed with a cautious cut at the June meeting, but the outlook beyond that has become increasingly uncertain, with a pause in the easing cycle looking more likely.

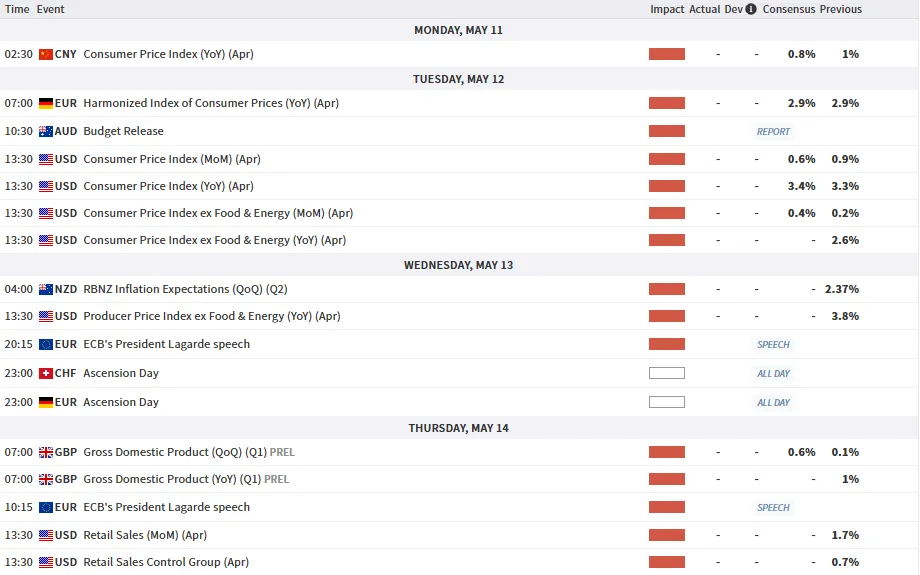

Summary 5/11 – 5/15

Monday, May 11, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 01:30 | CNY | CPI Y/Y Apr | 0.90% | 1.00% |

| 01:30 | CNY | PPI Y/Y Apr | 1.70% | 0.50% |

| 14:00 | USD | Existing Home Sales Apr | 4.05M | 3.98M |

| 01:30 | CNY |

| CPI Y/Y Apr | |

| Consensus | 0.90% |

| Previous | 1.00% |

| 01:30 | CNY |

| PPI Y/Y Apr | |

| Consensus | 1.70% |

| Previous | 0.50% |

| 14:00 | USD |

| Existing Home Sales Apr | |

| Consensus | 4.05M |

| Previous | 3.98M |

Tuesday, May 12, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:30 | JPY | Household Spending Y/Y Mar | -1.50% | -1.80% |

| 23:50 | JPY | BoJ Summary of Opinions | ||

| 01:30 | AUD | NAB Business Conditions Apr | 6 | |

| 01:30 | AUD | NAB Business Confidence Apr | -29 | |

| 05:00 | JPY | Leading Economic Index Mar P | 114.6 | 113.3 |

| 06:00 | EUR | Germany CPI M/M Apr F | 0.60% | 0.60% |

| 06:00 | EUR | Germany CPI Y/Y Apr F | 2.90% | 2.90% |

| 06:30 | CHF | Producer and Import Prices M/M Apr | 0.10% | 0.20% |

| 06:30 | CHF | Producer and Import Prices Y/Y Apr | -2.70% | |

| 09:00 | EUR | Germany ZEW Economic Sentiment May | -20.5 | -17.2 |

| 09:00 | EUR | Germany ZEW Current Situation May | -77.5 | -73.7 |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment May | -20 | -20.4 |

| 10:00 | USD | NFIB Business Optimism Index Apr | 96.1 | 95.8 |

| 12:30 | USD | CPI M/M Apr | 0.60% | 0.90% |

| 12:30 | USD | CPI Y/Y Apr | 3.70% | 3.30% |

| 12:30 | USD | CPI Core M/M Apr | 0.30% | 0.20% |

| 12:30 | USD | CPI Core Y/Y Apr | 2.70% | 2.60% |

| 23:30 | JPY |

| Household Spending Y/Y Mar | |

| Consensus | -1.50% |

| Previous | -1.80% |

| 23:50 | JPY |

| BoJ Summary of Opinions | |

| Consensus | |

| Previous | |

| 01:30 | AUD |

| NAB Business Conditions Apr | |

| Consensus | |

| Previous | 6 |

| 01:30 | AUD |

| NAB Business Confidence Apr | |

| Consensus | |

| Previous | -29 |

| 05:00 | JPY |

| Leading Economic Index Mar P | |

| Consensus | 114.6 |

| Previous | 113.3 |

| 06:00 | EUR |

| Germany CPI M/M Apr F | |

| Consensus | 0.60% |

| Previous | 0.60% |

| 06:00 | EUR |

| Germany CPI Y/Y Apr F | |

| Consensus | 2.90% |

| Previous | 2.90% |

| 06:30 | CHF |

| Producer and Import Prices M/M Apr | |

| Consensus | 0.10% |

| Previous | 0.20% |

| 06:30 | CHF |

| Producer and Import Prices Y/Y Apr | |

| Consensus | |

| Previous | -2.70% |

| 09:00 | EUR |

| Germany ZEW Economic Sentiment May | |

| Consensus | -20.5 |

| Previous | -17.2 |

| 09:00 | EUR |

| Germany ZEW Current Situation May | |

| Consensus | -77.5 |

| Previous | -73.7 |

| 09:00 | EUR |

| Eurozone ZEW Economic Sentiment May | |

| Consensus | -20 |

| Previous | -20.4 |

| 10:00 | USD |

| NFIB Business Optimism Index Apr | |

| Consensus | 96.1 |

| Previous | 95.8 |

| 12:30 | USD |

| CPI M/M Apr | |

| Consensus | 0.60% |

| Previous | 0.90% |

| 12:30 | USD |

| CPI Y/Y Apr | |

| Consensus | 3.70% |

| Previous | 3.30% |

| 12:30 | USD |

| CPI Core M/M Apr | |

| Consensus | 0.30% |

| Previous | 0.20% |

| 12:30 | USD |

| CPI Core Y/Y Apr | |

| Consensus | 2.70% |

| Previous | 2.60% |

Wednesday, May 13, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Apr | 4.60% | 4.80% |

| 23:50 | JPY | Current Account (JPY) Mar | 2.93T | 2.71T |

| 01:30 | AUD | Wage Price Index Q/Q Q1 | 0.80% | 0.80% |

| 03:00 | NZD | RBNZ Inflation Expectations Q2 | 2.37% | |

| 05:00 | JPY | Eco Watchers Survey: Current Apr | 41.6 | 42.2 |

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.10% | 0.10% |

| 09:00 | EUR | Eurozone Industrial Production M/M Mar | 0.30% | 0.40% |

| 12:30 | USD | PPI M/M Apr | 0.50% | 0.50% |

| 12:30 | USD | PPI Y/Y Apr | 4.90% | 4.00% |

| 12:30 | USD | PPI Core M/M Apr | 0.30% | 0.10% |

| 12:30 | USD | PPI Core Y/Y Apr | 4.30% | 3.80% |

| 14:30 | USD | Crude Oil Inventories (May 8) | -2.0M | -2.3M |

| 23:50 | JPY |

| Bank Lending Y/Y Apr | |

| Consensus | 4.60% |

| Previous | 4.80% |

| 23:50 | JPY |

| Current Account (JPY) Mar | |

| Consensus | 2.93T |

| Previous | 2.71T |

| 01:30 | AUD |

| Wage Price Index Q/Q Q1 | |

| Consensus | 0.80% |

| Previous | 0.80% |

| 03:00 | NZD |

| RBNZ Inflation Expectations Q2 | |

| Consensus | |

| Previous | 2.37% |

| 05:00 | JPY |

| Eco Watchers Survey: Current Apr | |

| Consensus | 41.6 |

| Previous | 42.2 |

| 09:00 | EUR |

| Eurozone GDP Q/Q Q1 P | |

| Consensus | 0.10% |

| Previous | 0.10% |

| 09:00 | EUR |

| Eurozone Industrial Production M/M Mar | |

| Consensus | 0.30% |

| Previous | 0.40% |

| 12:30 | USD |

| PPI M/M Apr | |

| Consensus | 0.50% |

| Previous | 0.50% |

| 12:30 | USD |

| PPI Y/Y Apr | |

| Consensus | 4.90% |

| Previous | 4.00% |

| 12:30 | USD |

| PPI Core M/M Apr | |

| Consensus | 0.30% |

| Previous | 0.10% |

| 12:30 | USD |

| PPI Core Y/Y Apr | |

| Consensus | 4.30% |

| Previous | 3.80% |

| 14:30 | USD |

| Crude Oil Inventories (May 8) | |

| Consensus | -2.0M |

| Previous | -2.3M |

Thursday, May 14, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance Apr | -25% | -23% |

| 23:50 | JPY | Money Supply M2+CD Y/Y Apr | 2.10% | 2.00% |

| 06:00 | GBP | GDP Q/Q Q1 P | 0.60% | 0.10% |

| 06:00 | GBP | GDP M/M Mar | -0.10% | 0.50% |

| 06:00 | GBP | Goods Trade Balance (GBP) Mar | -20.1B | -18.8B |

| 12:30 | CAD | Wholesale Sales M/M Mar | 1.30% | 2.00% |

| 12:30 | USD | Initial Jobless Claims (May 8) | 205K | 200K |

| 12:30 | USD | Retail Sales M/M Apr | 0.50% | 1.70% |

| 12:30 | USD | Retail Sales ex Autos M/M Apr | 0.60% | 1.90% |

| 12:30 | USD | Import Price Index M/M Apr | 1.10% | 0.80% |

| 14:00 | USD | Business Inventories Mar | 0.30% | 0.40% |

| 14:30 | USD | Natural Gas Storage (May 8) | 86B | 63B |

| 23:01 | GBP |

| RICS Housing Price Balance Apr | |

| Consensus | -25% |

| Previous | -23% |

| 23:50 | JPY |

| Money Supply M2+CD Y/Y Apr | |

| Consensus | 2.10% |

| Previous | 2.00% |

| 06:00 | GBP |

| GDP Q/Q Q1 P | |

| Consensus | 0.60% |

| Previous | 0.10% |

| 06:00 | GBP |

| GDP M/M Mar | |

| Consensus | -0.10% |

| Previous | 0.50% |

| 06:00 | GBP |

| Goods Trade Balance (GBP) Mar | |

| Consensus | -20.1B |

| Previous | -18.8B |

| 12:30 | CAD |

| Wholesale Sales M/M Mar | |

| Consensus | 1.30% |

| Previous | 2.00% |

| 12:30 | USD |

| Initial Jobless Claims (May 8) | |

| Consensus | 205K |

| Previous | 200K |

| 12:30 | USD |

| Retail Sales M/M Apr | |

| Consensus | 0.50% |

| Previous | 1.70% |

| 12:30 | USD |

| Retail Sales ex Autos M/M Apr | |

| Consensus | 0.60% |

| Previous | 1.90% |

| 12:30 | USD |

| Import Price Index M/M Apr | |

| Consensus | 1.10% |

| Previous | 0.80% |

| 14:00 | USD |

| Business Inventories Mar | |

| Consensus | 0.30% |

| Previous | 0.40% |

| 14:30 | USD |

| Natural Gas Storage (May 8) | |

| Consensus | 86B |

| Previous | 63B |

Friday, May 15, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Apr | 53.2 | |

| 23:50 | JPY | PPI Y/Y Apr | 3.00% | 2.60% |

| 06:00 | JPY | Machine Tool Orders Y/Y Apr | 28.10% | 28.10% |

| 12:15 | CAD | Housing Starts Y/Y Apr | 245K | 236K |

| 12:30 | CAD | Manufacturing Sales M/M Mar | 3.50% | 3.60% |

| 12:30 | USD | Empire State Manufacturing May | 8.1 | 11 |

| 13:15 | USD | Industrial Production M/M Apr | 0.20% | -0.50% |

| 13:15 | USD | Capacity Utilization Apr | 75.90% | 75.70% |

| 22:30 | NZD |

| Business NZ PMI Apr | |

| Consensus | |

| Previous | 53.2 |

| 23:50 | JPY |

| PPI Y/Y Apr | |

| Consensus | 3.00% |

| Previous | 2.60% |

| 06:00 | JPY |

| Machine Tool Orders Y/Y Apr | |

| Consensus | 28.10% |

| Previous | 28.10% |

| 12:15 | CAD |

| Housing Starts Y/Y Apr | |

| Consensus | 245K |

| Previous | 236K |

| 12:30 | CAD |

| Manufacturing Sales M/M Mar | |

| Consensus | 3.50% |

| Previous | 3.60% |

| 12:30 | USD |

| Empire State Manufacturing May | |

| Consensus | 8.1 |

| Previous | 11 |

| 13:15 | USD |

| Industrial Production M/M Apr | |

| Consensus | 0.20% |

| Previous | -0.50% |

| 13:15 | USD |

| Capacity Utilization Apr | |

| Consensus | 75.90% |

| Previous | 75.70% |

Week Ahead – US Inflation Data Eyed Amid Iran Peace Hopes

- Middle East headlines continue to dominate as hopes of deal grow.

- US CPI and retail sales data to fight for attention as Warsh takes office.

- UK Q1 GDP and BoJ meeting summary also on the agenda.

Markets Cheer Trump’s Peace Push Despite Threats

The late April surge in oil prices wasn’t met with the same risk-off reaction as at the onset of the Iran conflict, as the recharged AI rally eclipsed fears of a deepening energy crisis. Yet, the rise in inflation expectations was notable, and even as some of the worst fears have subsided, key metrics such as the US 10-year breakeven rate are above pre-war levels.

Investors are likely taking heart from the fact that inflation expectations globally remain some distance from the peaks seen immediately after Russia’s invasion of Ukraine. But there’s a danger they’re ignoring the real risk of the current energy crunch becoming the most severe in history. Crucially, the latest relief rally is founded mostly on hope rather than an actual deal between the US and Iran.

Although it’s accurate to say that President Trump’s rhetoric is more indicative of a desire to exit from the conflict than to inflame it, Tehran’s leadership structure has become more “fractured” in the President’s own words. Moreover, the Iranians are known to be tough negotiators, so even if the two sides can agree on a framework for a long-term deal that includes curbs on nuclear enrichment, the risk of re-escalation remains extremely high amid the battle over who controls the Strait of Hormuz and Israel’s repeated violations of its ceasefire with Hezbollah.

Even in the best-case scenario that the Hormuz Strait reopens soon, energy shortages could worsen before they get better, as it would likely take months for oil and gas flows from the Middle East to normalize. However, Iran negotiations are likely to take a backseat next week, as President Trump travels to China for a meeting with President Xi Jinping where trade will be top of the agenda.

Will the US CPI Report Matter?

Nevertheless, investors have scaled back some of their rate hike bets for the major central banks in line with the pullback in oil prices, with expectations for the Federal Reserve once again switching from hikes to cuts. The fluid situation in the Middle East means that the market reaction to the upcoming releases out of the United States, namely Tuesday’s CPI report, will be determined by whether there is any progress in the peace talks, or if Trump has ordered fresh strikes on Iran.

A major flare-up would increase investors’ sensitivity to upside surprises in the inflation data, while positive negotiations would reduce it, as any pickup would be considered temporary.

Headline CPI jumped to 3.3% y/y in March and likely accelerated further in April. The Cleveland Fed’s Nowcast estimate is a rise to 3.6% y/y, while core CPI is seen staying unchanged at 2.6% y/y.

Producer prices for the same month are due the following day on Wednesday. The PPI report quite often tends to negate some of the effects of a CPI surprise if they’re contradictory. But if both sets of figures are hotter-than-expected, risk appetite is likely to be knocked back as Fed rate cut bets would take a hit, with next week’s busy schedule of Treasury auctions potentially exacerbating any spike in US yields.

Warsh Confirmation Awaited

Also guiding the Fed policy direction next week will be possible comments by Fed chair nominee Kevin Warsh, who looks set to be finally confirmed by the US Senate on Monday, just days before outgoing chair Jerome Powell’s term is set to expire on May 15.

Investors have largely welcomed Warsh’s nomination, as he’s likely to make the case for the need to cut rates further. But any explicit hints about the types of reforms he has in mind could spook markets.

Thursday’s retail sales numbers for April will also be vital, amid some worries about whether US consumer spending will hold up against a backdrop of rising gasoline prices. Other data will include existing home sales on Monday, and the Empire State manufacturing index and industrial production on Friday.

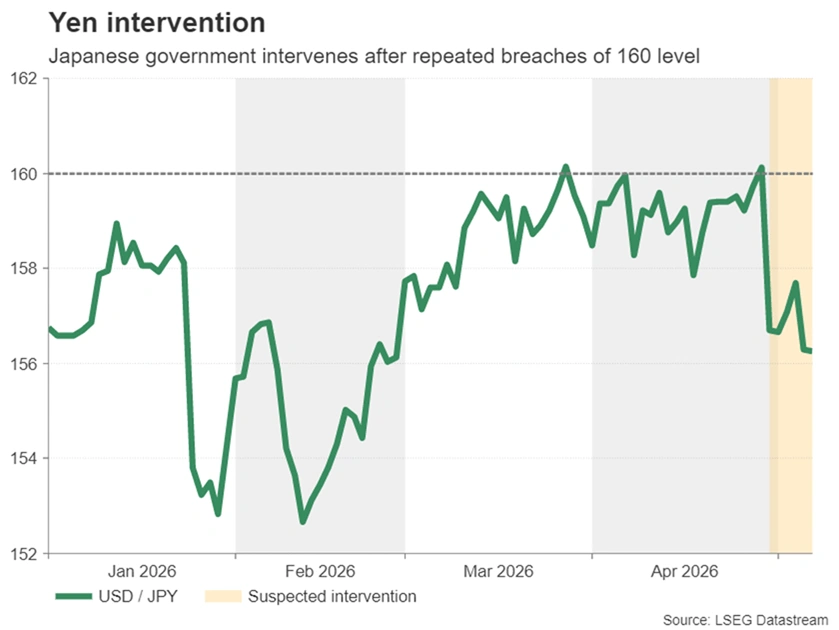

Dollar’s Resilience Tested by Yen Intervention

The US dollar’s losses on the back of the optimism of an end to the Iran conflict have been relatively modest and would have been even less if it wasn’t for the intervention in the yen by Japan’s government. But despite Fed rate hike bets diminishing, a resumption of the dollar’s 2026 uptrend isn’t on the cards either, as Japanese authorities are suspected to have remained active in the FX market following the April 30 intervention.

The yen’s best prospect in the short term is to attempt a dash toward the 152-per dollar area, which twice acted as resistance earlier this year. Such a boost could come from the Bank of Japan’s Summary of Opinions of the April meeting due to be published on Tuesday.

There were three dissents at the meeting, as the hawkish voices grew louder. If the summary reveals that other board members could soon join the calls for an imminent rate hike, the yen could enjoy improved demand other than from central bank buying.

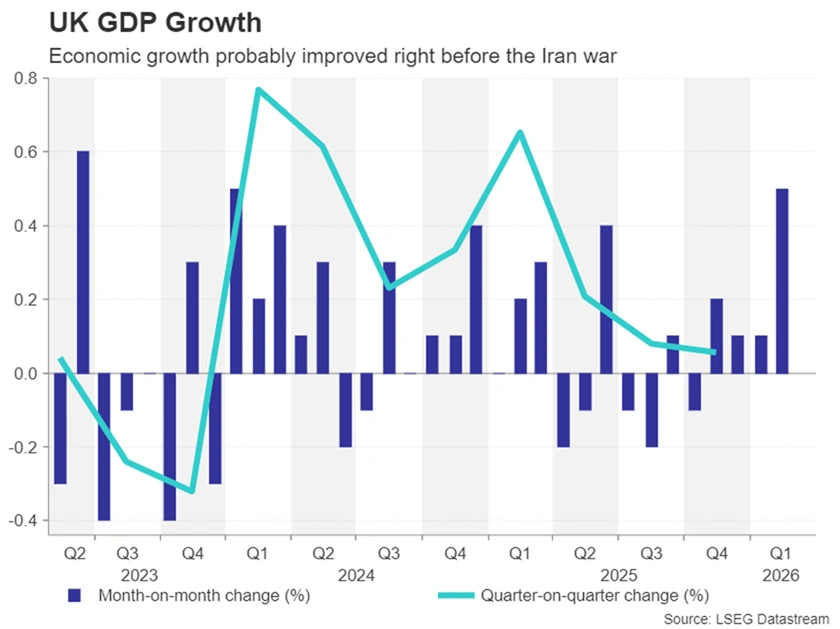

Pound Bulls Tread Carefully

For the pound, whose own rebound against the dollar has been constrained by stagflation risks even as the Bank of England lays the ground for a summer rate increase, the geopolitical developments are being watched closely for the timing and scale of any tightening.

Next week’s initial estimate of Q1 GDP growth will probably play second fiddle to the Iran headlines, but will be important nonetheless, particularly the monthly print for March, to gauge what impact the start of the Iran war had on the British economy.

The data is due on Thursday, along with a breakdown of sectoral growth for the full quarter and March.

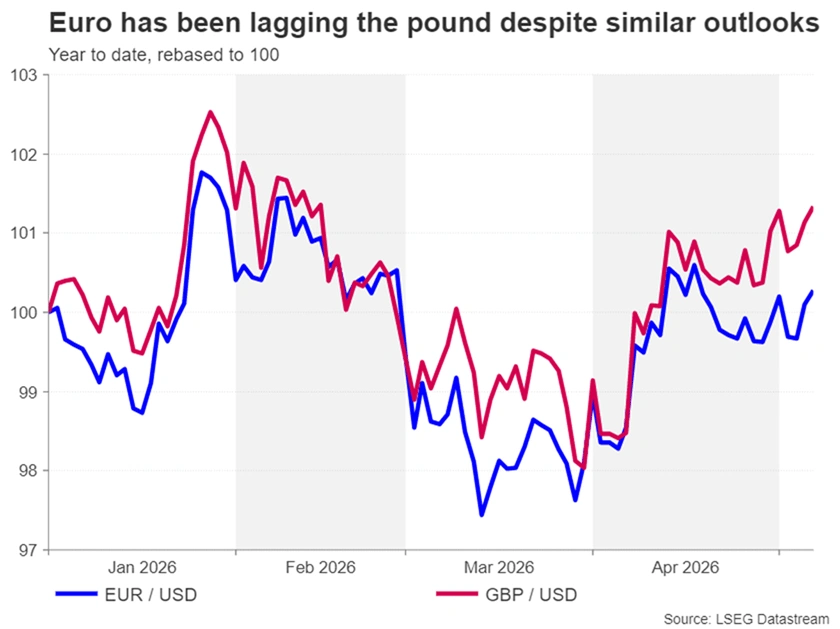

Kiwi Shines While Euro Lags

It’s a very similar story for the euro, whose recovery has been even slower than the pound’s and remains below its mid-April peak. The pricing out of an almost full 25-bps rate hike from year-end ECB expectations following the easing of tensions in the Middle East is probably behind the euro’s underperformance.

Quarterly employment figures and the second estimate of Q1 GDP growth, both on Wednesday, and Germany’s ZEW economic sentiment gauge on Tuesday are the highlights of the European agenda, though they’re unlikely to sway the euro much.

Elsewhere, China is expected to report a jump in both its CPI and PPI measures on Monday as higher energy prices took hold in April. On Wednesday, quarterly wage growth data will be watched in Australia for clues as on the likelihood of a fourth rate increase by the Reserve Bank of Australia. Meanwhile, in New Zealand, the RBNZ’s survey of quarterly inflation expectations could aid the New Zealand dollar’s impressive one-month-long rally against the greenback if they show an uptick.

Mixed Feelings After the April Non-Farm Payrolls Beat and Consumer Sentiment Miss

Markets have shown their fair acts of stoicism in recent days, not reacting the slightest to bad and relatively hawkish news.

Yesterday, Iran reported US strikes on its capital and a few key energy-producing regions (including Bandar Abbas and Sirik – close to Hormuz), which came as a direct response to the Iranian firing on Gulf countries at the beginning of the week.

Participants believe this will not escalate into something worse; The cold-truce remains, albeit being quite fragile.

To enlighten the mood however, Non-Farm Payrolls offered a very decent beat (+115K vs 62K exp) in this morning's release, allowing Investor mood to remain calm ahead of the weekend action.

The Unemployment Rate shows unchanged while the unrounded figures show a slight increase – But nothing too alarming.

Morning US Data – MarketPulse Economic Calendar

Canada is still showing an unstable employment picture with ups and downs virtually every month – The Canadian economy is cyclical and amid extreme doubts all around the globe, these labor numbers can only depict this truth.

The preliminary University of Michigan Consumer Sentiment also just released and came with a miss, with many consumers still signalling fears for higher inflation (logical with prices at the pump at the highest since 2022).

We will provide a quick outlook on the Market before diving into WTI (US) Oil Charts to get ready for what could be another volatile weekend.

A Mixed Market Picture

Stock and Energy Product Futures – Courtesy of Finviz

Except for the Tech-heavy index quickly restarting its path higher after a quick stopover, Energy and more traditional equities are scratching their heads in search for a concrete direction.

True directional moves may only be found next week, with traders preparing for the Trump-Xi meeting in China (May 14).

Metals Trade Higher, Particularly Silver and Copper

Metals weekly performance – May 8, 2026 – Source: TradingView

Silver and Copper are leading a path higher in the entire asset class, with Gold starting to pick up some momentum.

WTI (US) Oil Forms a New Range Between $93 and $98

WTI Daily Chart – May 8, 2026 – Source: TradingView

Oil is unable to form a concrete breakout, rejecting its up and down spikes at every attempt.

As traders await for further news, Crude is stabilizing between $93 and $98, the two boundaries to keep in check for any clear break (watch for a 4H close above or below for higher breakout odds).

Keep a close eye on sentiment and Middle East news throughout the weekend.

Safe Trades!

Weekly Focus – Higher Hopes of Hormuz Harmony

This week has been light on the data front so developments in the US-Iran war have shaped markets. The spot oil price declined from USD 115/bbl to around USD 100/bbl following reports of a US one-page memo to the Islamic Republic with suggestions on how to formally end the war while setting up a 30-day period for detailed talks. The deal would involve Iran committing to a moratorium on nuclear enrichment, US lifting sanctions and releasing frozen assets, and both sides lifting the blockage of the Strait of Hormuz (SOH). We are awaiting the Iranian response to the proposal that should come later today. The two-sides remain divided on the issue on Iran's enriched uranium stockpile and on who controls SOH, so the risk of reescalation is high. Even if there was an initial deal, the limbo would continue until there is a more permanent agreement, as talks could collapse and warfare resume anytime. It would be very positive if the SOH would at least gradually reopen but full normalisation would take months.

In terms of data releases, we have received a string of labour market data from the US pointing to broadly steady conditions, which was slightly better than expected. ADP hiring showed steady employment growth, the JOLTs job openings-to-unemployed ratio remaining at 0.95, while continuing jobless claims reached their lowest level since early 2024. Hence, job market data has been slightly better than expected ahead of the US Jobs Report which will be released later this afternoon. In other news, ISM Services delivered mixed signals, with unchanged prices, weaker new orders, and improved business activity and employment indices.

Data releases from the eurozone were light this week. The final PMIs confirmed the flash release for manufacturing while the services index was marginally higher. The Sentix sentiment index rose slightly but remains at the lowest level since April last year. And finally, retail sales for March were broadly similar to February with no clear impact of the war outside of fuel spending, where consumers spend more on fuels but bought a smaller quantity compared to February. Finally, the ECB's wage tracker continues pointing to lower wage growth in 2026 compared to 2025.

From Asia we received PMI data for April where the manufacturing PMI rose in both China, Taiwan, and South Korea, thereby signalling continued growth in the sector as they remain above 50. The global manufacturing sector thus seems to have continued growing in April despite the rise in energy prices as we also saw decent manufacturing PMIs in the eurozone and US last week.

We will not publish the Weekly Focus next week so focus the coming two weeks is on US April CPI on 12 May, flash PMIs for US, eurozone, and UK on Thursday 21 May, and finally euro area negotiated wages and Japanese inflation on 22 May.