Sample Category Title

AUD/USD Daily Report

Daily Pivots: (S1) 0.7213; (P) 0.7230; (R1) 0.7262; More...

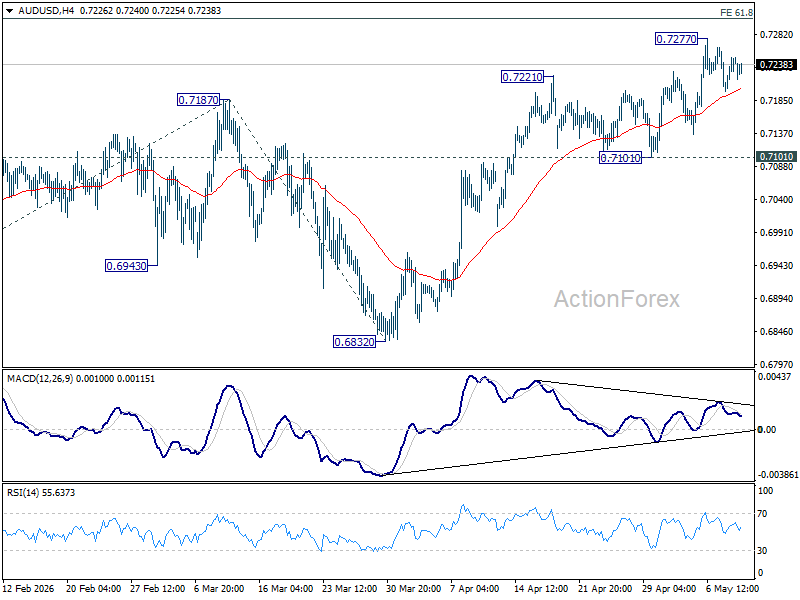

Intraday bias in AUD/USD remains neutral for consolidations below 0.7277. Further rise is expected as long as 0.7101 support holds. On the upside, above 0.7277 will resume larger up trend and target 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306.

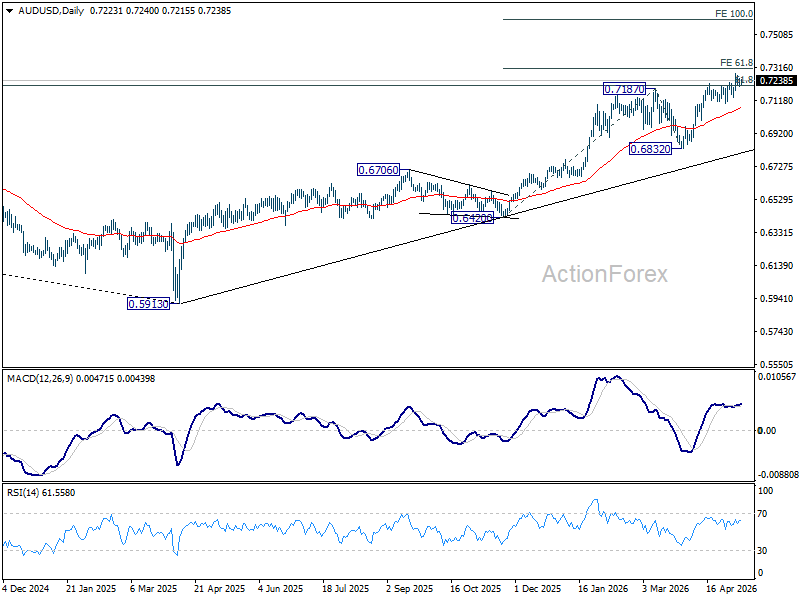

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1740; (P) 1.1764; (R1) 1.1806; More….

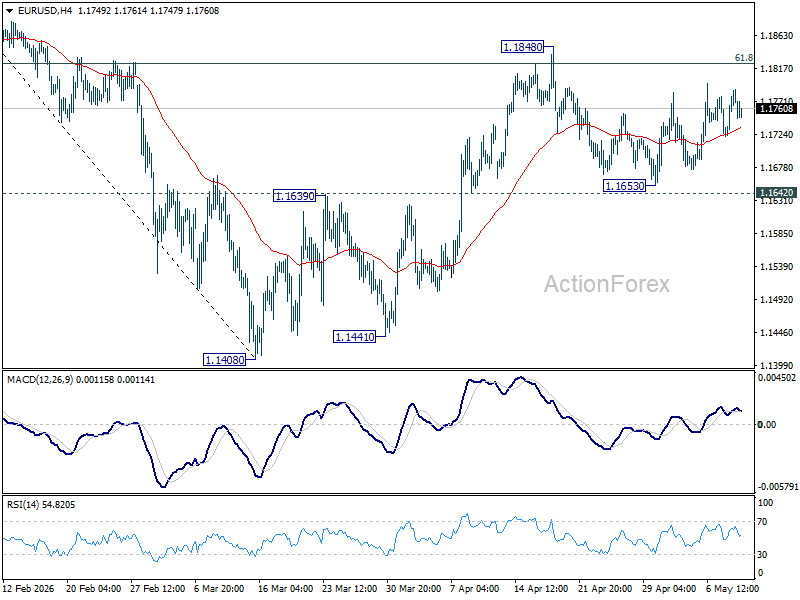

Range trading continues in EUR/USD and intraday bias remains neutral. Further rise is expected with 1.1642 support intact. On the upside, firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

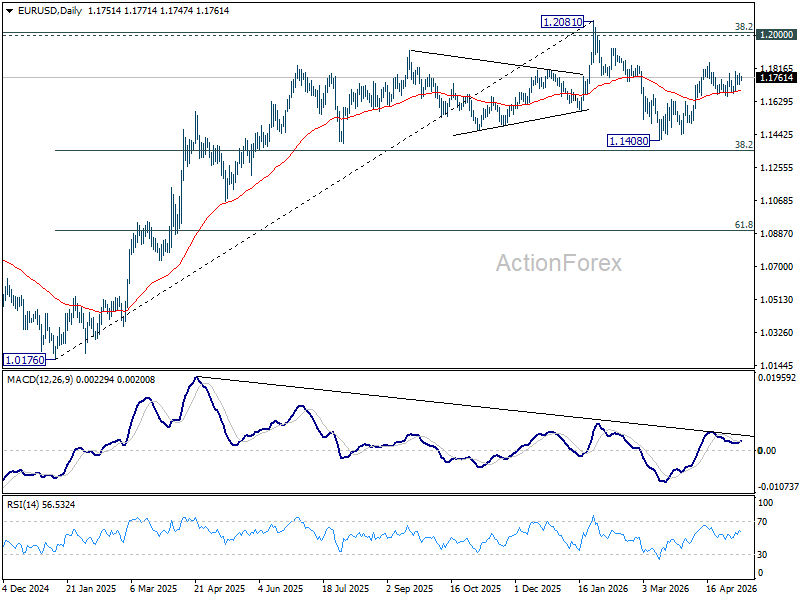

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1539). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

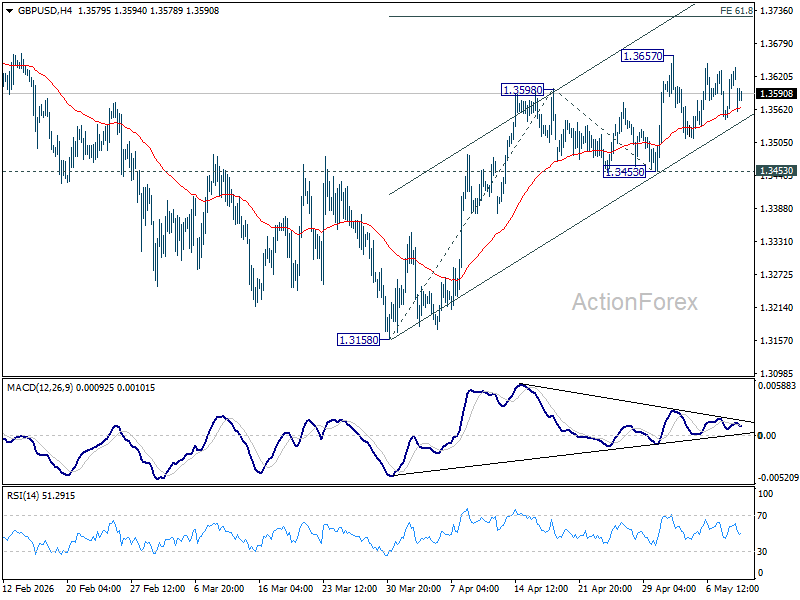

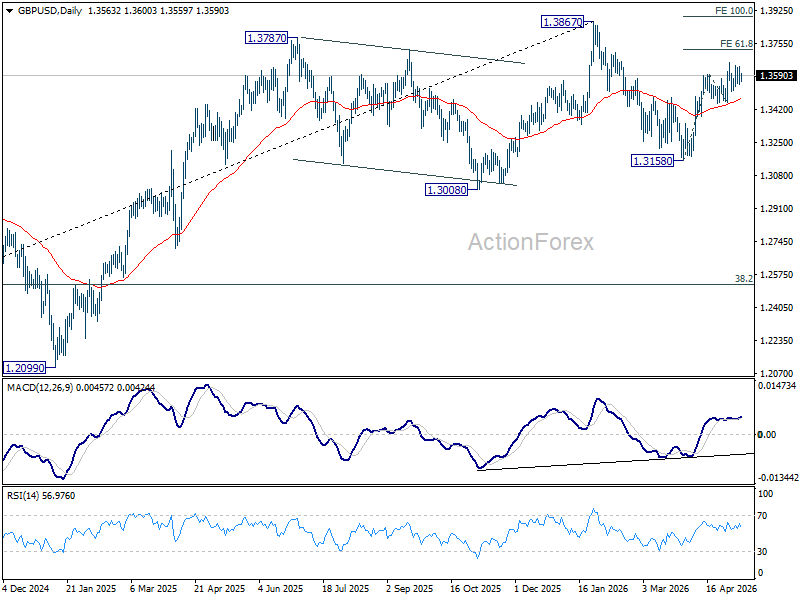

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3568; (P) 1.3602; (R1) 1.3659; More...

Intraday bias in GBP/USD remains neutral as sideway trading continues. Further rise is expected with 1.3453 support intact. On the upside, break of 1.3657 will target 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).

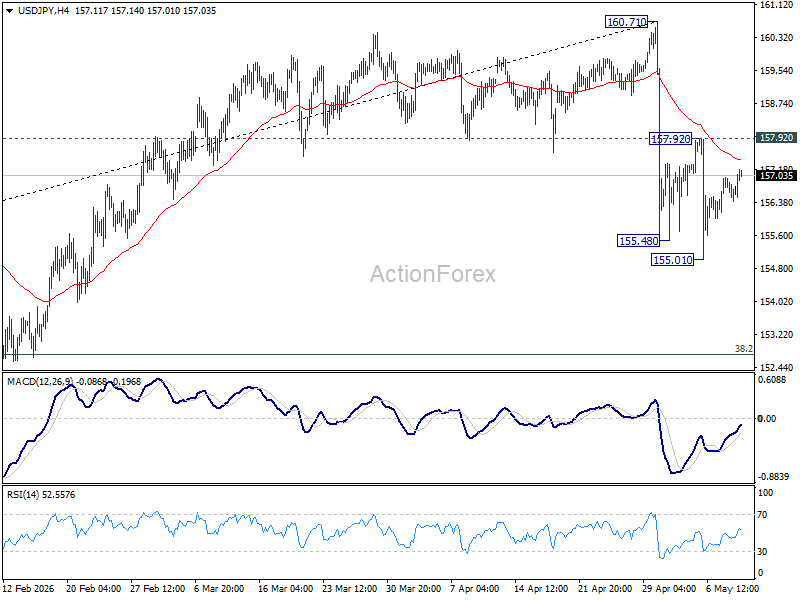

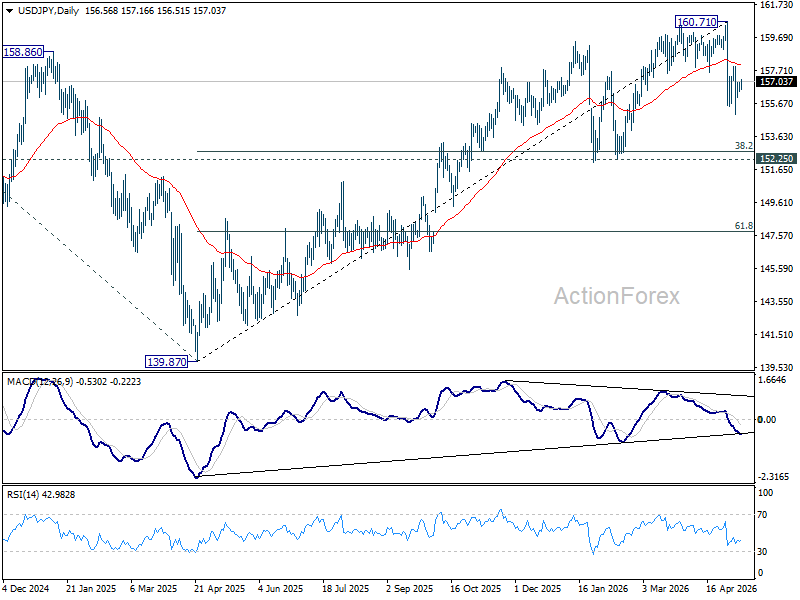

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.41; (P) 156.69; (R1) 156.97; More...

Intraday bias in USD/JPY remains neutral at this point. On the downside, break of 155.01 will resume the fall from 160.71 to 152.25 support next. On the upside, however, firm break of 157.92 will indicate that pullback from 160.71 has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.13) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

Sunrise Market Commentary

Markets

April payrolls in the US were stronger than expected (115k vs 65k) and confirm outgoing Fed chair Powell’s message at the presser of the April policy meeting. He said the labour market is showing “more and more signs of stability” after a year of near-zero job growth. Inflation, by contrast, was “kind of misbehaving”. With upside risks posed by the Iran war looming, there’s no reason to expect any near-term policy easing. Markets price a long rates status quo at least through the end of the year. Treasuries gained ground, outperforming Bunds in the process. US rates lost a couple of basis points, between 2.7 and 3.8 bps. German rates steadied with some minor underperformance at the front end of the curve, where the 2-yr yield added 1.5 bps. Oil prices on Friday weren’t guiding much by flatlining around but above $100. The black gold stayed on the sidelines while awaiting Iran’s response to the latest US proposal to end the war. That finally came over the weekend and received a hard pass from president Trump. "I have just read the response from Iran’s so-called 'Representatives.' I don’t like it — TOTALLY UNACCEPTABLE!” Brent jumps more than 4% at the Asian open today. A barrel currently trades at $105+. Treasury yields erase Friday’s limited gains by adding 3-4.5 bps across the curve. The US dollar recoups some of the losses it incurred end last week. EUR/USD turns lower to 1.175 after having flirted with the 1.18 barrier. The greenback on a trade-weighted basis hovers around 98. USD/JPY finds a short-term equilibrium between 156 and 158 after a series of FX interventions since April 30 by Japanese authorities. Sterling digested Labour’s devastating election blow, which included a historical loss in the Welsh parliament, very well. EUR/GBP depreciated to 0.864. Prime minister Starmer vowed to stay on as prime minister – easing concerns that a change could lead to less fiscal prudence – but he is not out of the woods. He planned a speech today to outline plans to overturn the party’s fate. If deemed insufficient, it might prompt leadership challenges.

The eco calendar today is pretty uninspiring, so we’ll mostly be looking for the fall-out of the US disapproval of Iran’s counterproposal. It leaves president Trump with little, if any, progress in the war with Iran before his closely watched encounter with his Chinese counterpart on Thursday and Friday. Key talking points include trade (truce extension), Tehran and Taiwan but there’s not much expected in terms of a breakthrough. Important economic data later this week is limited to tomorrow’s US April CPI and Friday’s retail sales. The country kicks of its mid-month refinancing operations with a $58bn 3-year bond sale today. A 10-yr and 30-yr bond sale (tomorrow and Wednesday) are the ones to follow-up on closely.

News & Views

KMPG and REC’s monthly UK reports on jobs showed permanent placements falling at a quicker rate in April amid greater market uncertainty. The report, compiled by S&P global, also throw rising business costs in the mix. Although conditions remain more favourable than they were through much of 2025, hiring decisions are being referred because of uncertainty stemming from the war in Iran. While slightly rising temp billings offered some counterweight, total demand for workers was still declining (13th consecutive month). The overall availability of workers continued to increase markedly in April. Redundancies and lower demand were key factors for the latest rise in candidate numbers. Starting salaries for permanent workers increased again, but the rate of pay growth remains below the series long-term average.

Chinese producer prices increased at the quickest pace since October 2021 in April. They rose by 1.7% M/M, up from 1% in March and moving the annual PPI pace from 0.5% to 2.8%, the fastest increase since July 2022. The Iran war is the obvious catalyst of rising factory-gate prices. Consumer price inflation rose by 0.3% M/M and from 1% Y/Y to 1.2% on a headline level. Core CPI went from 1.1% Y/Y to 1.2% Y/Y. Apart from transportation and energy costs, there was a price boost from holiday travel demand. Separate details showed consumer goods inflation picking up from 1.3% to 1.4% Y/Y and services inflation moving from 0.8% to 0.9% Y/Y.

Oil Prices Jump on Iran Counterproposal

In focus today

In Norway, April inflation data is due for release. There are usually large fluctuations in the various price components during the Easter months of March and April. This year, Easter was a week earlier than last year, and many of the offers for typical Easter products were more extensive in March than last year. We expect this to result in a solid lift in the annual growth in food prices in April, but that parts of the service sector such as cultural activities and hotels and restaurants will show the opposite development. We expect core inflation to rise from 3.0% y/y to 3.2% y/y in April. This would be in line with both consensus and Norges Bank's estimate from the MPR in March.

In Denmark, April inflation data is also set for release. We expect headline inflation at 1.4% y/y, up from 1.2% y/y in March, driven by higher fuel prices.

In Japan, Q1 GDP data will be released overnight. Both the Tankan business survey and PMIs suggest the economy was on a decent footing in Q1. Since then, the service sector has slowed down but remains in expansionary territory.

The rest of the week brings a light data calendar, with the most important releases being US April CPI on Tuesday and the Riksbank minutes on Wednesday. Developments in the US-Iran war remain a key focus. In addition, Trump will visit Beijing for meetings with President Xi Jinping on Thursday and Friday.

Economic and market news

What happened overnight

In China, April inflation came in higher than expected on the back of higher global energy prices. PPI rose to 2.8% y/y (cons:1.6%, prior: 0.5%), the highest reading since mid‑2022. CPI also beat expectations at 1.2% y/y (cons: 0.9%, prior: 1.0%), with gains concentrated in gasoline and gold jewellery. The move further distances China from the deflation seen over the past years, but the impulse is largely cost‑push rather than demand‑driven. Against a backdrop of weak domestic demand, today's figures are unlikely to prompt a significant policy shift, though they may slightly reduce the urgency for further monetary easing.

What happened over the weekend

In the Middle East conflict, Iran sent its response to a US proposal for peace talks via mediator Pakistan, reportedly focused on ending the war on all fronts. The Iranian counterproposal includes demands for compensation for war damages, recognition of Iranian sovereignty over the Strait of Hormuz, an end to the US naval blockade, guarantees against further attacks and a lifting of sanctions. President Trump deemed the proposal "totally unacceptable" on Truth Social. Brent crude is up around 6% from Friday's close, trading around USD106/bbl this morning. Despite the month‑old ceasefire, security in the Gulf remains fragile, with reports of hostile drones over the weekend, although a Qatari LNG tanker was allowed to transit the strait to Pakistan.

In the US, the April jobs report came in as a mixed bag. Nonfarm payrolls surprised to the topside at 115k (cons: 62k, Danske: 80k), while the unemployment rate held at 4.3%. Cumulative revisions to NFP were -16k. Wage growth was weaker than expected, with average hourly earnings up by only 0.2% m/m SA (cons: 0.3%). The household survey painted a weaker picture, showing a 226k drop in employment and a 92k decline in the labour force, helping explain why the unemployment rate did not tick down despite the strong NFP. We do not expect the print to have a significant lasting impact on the Fed policy outlook.

Also in the US, consumer sentiment weakened further in May, with the preliminary University of Michigan index declining to 48.2 (cons: 49.5, prior: 49.8). At the very least, inflation expectations ticked slightly lower on both the 1‑year and 5‑year horizons, to 4.5% and 3.4%, respectively.

In Sweden, household consumption rose by 1.4% m/m in March, in line with the forecast, driven mainly by 'Recreation and culture, goods and services' as well as 'Retail trade, mostly food and beverages'. Private sector production (PVI) increased by 2.2% m/m in services and 6.6% m/m in construction, while industry declined by 2% m/m. New industrial orders declined by 1.4% m/m, although most subsectors still recorded monthly increases.

In the UK, local election results confirmed a major set-back for Labour, with the party suffering the worst municipal losses for a governing party since 1995. Pressure on PM Starmer has increased, with more than 20 Labour lawmakers calling for a timetable for his departure. However, Starmer confirmed that he would not stand down. Former minister West said she would challenge him for the Labour leadership on Monday if no other candidate came forward.

Equities: Global equities closed last week on a strong footing, with risk appetite supported by a mixed but ultimately benign April US jobs report. On Friday, S&P500 rose 0.8%, driven yet again by higher tech. Nasdaq rose 1.7%, Russell2000 rose 0.8%. Global equities posted a 1.8% return seen over last week. The weekend news of US dismissal of the Iranian proposal as "totally unacceptable", has pushed oil prices around 4% higher this morning. That said, Asian markets are having a quiet start to the week with limited reactions to this with the exception of tech impacted indices such as Kospi benefiting from Friday's IT rally. US futures are virtually unchanged.

FI and FX: US President Trump's dismissal of the Iranian response to the US peace proposal as 'totally unacceptable' has sparked renewed concerns that a lasting resolution to the war is still some way out. The UAE, Kuwait and Qatar have all reported incidents involving hostile drones over the weekend, leaving the ceasefire in a fragile state. Brent Crude pushed above USD105/bbl. and EUR/USD declined below 1.1760, reversing some of the gains following last week's April NFP print of +115k. Over the last week apparent willingness from both the US and Iran caused the market to slowly reprice the ECB rate path. Bond yields declined with the 10Y German government bond dropping to 3% after testing 3.10%. 30Y Treasuries tested the 5%-level but have now edged down to 4.97%. If deescalation picks back up, we see this move extending. Going into this week, we eye the war in the Middle East and the Trump-Xi Jinping meeting in Beijing on Thursday and Friday, although we do not anticipate any deals to be made. On the data front, our focus will be on the US April CPI tomorrow and the Norwegian CPI figures this morning. The monthly CPI figures out of Norway have become increasingly important following Norges Bank's more neutral post-hike guidance last week.

Peace Hopes Falter, Tech Unfazed

Congratulations ladies and gentlemen, we just reached the point this Monday where war headlines don’t bother AI investors anymore! Despite waking up to the news that the US rejected Iran’s peace proposal, and that the Strait of Hormuz remains closed, despite the fact that US crude rebounded back above $100pb – a more than 5% jump this morning with no retreat yet – the Korean Kospi index – which had been one of the most sensitive indices to oil prices – is up by more than 4.50% to a fresh ATH at the time of talking. Elsewhere, the Nikkei is struggling to push higher with a 1.71% retreat from an ATH, while the S&P500 and Nasdaq futures are flat, with Stoxx and FTSE futures even pointing to meagre gains.

It’s hard to make sense of the market reaction, it feels like the calm before a storm – higher energy prices will hit the ground sooner rather than later as Middle East tensions prolong and the world’s energy stockpiles dry out.

But that’s something investors are apparently not willing to think about this morning. So let’s talk about more encouraging news.

Friday’s US jobs data came in as good as it possibly could. I noted that the best possible outcome would be higher-than-expected job additions combined with softer-than-expected wage growth – and that’s exactly what the data printed: 115K new nonfarm job additions versus 65K expected, and 3.6% wage growth on a yearly basis, up from 3.4% a month earlier, but softer than the 3.8% expected by analysts.

In simple terms: that’s the sweet spot, the best of both worlds from a market perspective. It means that the US jobs market is weakening, but remains healthy enough to rule out an immediate meltdown, while wage growth remains above the Federal Reserve’s (Fed) 2% inflation target and is still accelerating, but less than pencilled in by analysts. Cherry on top, Michigan’s 1- and 5-year inflation expectations were revised lower, a sign that the Iran war and rising energy prices have not pushed inflation expectations further up. Consumer sentiment and the way people perceive market conditions weakened, but hey, that didn’t necessarily demoralise investors on Friday, especially not when the US 2-year yield eased on relief that the Fed could stay quiet, with no need to intervene to fight inflation… yet.

The US 2-year yield kicked off the week higher – yes, bond investors care more about the jump in oil prices than tech investors do – but the S&P 500 and Nasdaq futures look serene again. The Dow is a bit less comfortable though, with a 0.20% decline at the time of talking.

Anyway, Friday’s sweet jobs data gave another boost to equity markets. The S&P500 and Nasdaq traded at fresh record highs. The Nasdaq rallied 2.35% as AI names led the rally again, and this time despite some less-than-ideal headlines. First, TSMC posted its slowest pace of monthly revenue expansion since October, while CoreWeave – an Nvidia-backed neo-cloud provider – saw its shares drop more than 11% after giving a disappointing outlook. Together, the news revived concerns that torrid AI growth may not be sustainable in the coming years. But again, that didn’t prevent VanEck’s Semiconductor ETF from surging nearly 5% to a fresh ATH level!

At this point, I am really wondering what will cause this rally to retrace, because at some point, we will see a correction. The S&P500 is up by nearly 17% since the beginning of April and has been trading in overbought territory since mid-April. Earnings beats surely explain the enthusiasm and strong appetite seen over the past two weeks, but the fact that the sharp rise in energy prices doesn’t bother anyone is curious. Really curious.

This week, attention will shift to inflation figures. While European inflation is expected to confirm heating price pressures in April due to higher energy prices – likely coupled with softer growth readings – expectations for US CPI are rather balanced. According to estimates, US headline inflation may have even slowed on a monthly basis in April. On a yearly basis, however, we could see a rise from 3.3% to 3.7%. That’s because the Iran war-related jump had already started creeping into last month’s inflation figures, making the monthly figure look less threatening than the yearly one. But inflation within the 3–4% range remains well above the Fed’s 2% target – let’s remember that – and will continue to keep Fed hawks alert.

It is however worth noting that current levels remain below the painful 5–7% inflation range seen after Covid and during the Ukraine war-led energy crisis. So to me, a reasonable inflation print could keep investors in a sweet mood if doves outweigh hawks on the idea that there is no need for a Fed rate hike this year, unlike European peers that are expected to raise rates – for some, like the European Central Bank (ECB), as soon as the June policy meeting.

That dovish divergence, if confirmed this week, should continue to weigh on the US dollar outlook in the medium run. In the short run, however, the dollar’s direction will continue to be driven by oil prices. Higher oil prices should support the dollar, while lower oil prices would let it soften. That’s why we are seeing a rebound in the US dollar index this morning. Though I must admit that even the dollar’s rebound looks soft compared to the gravity of the headlines. For longer-term traders, geopolitically driven, oil-led US dollar rallies remain interesting opportunities to sell the tops against major peers, though with a great deal of volatility to manage as headlines rapidly change.

This week, besides the war headlines, investors will also closely watch the US President’s first visit to China since 2017. Talks will likely be tense. Trump needs major headlines to divert attention from Iran, but China today is becoming more powerful than ever thanks to its technological catch-up, EVs, and other energy-transition industries. China’s trade surplus jumped 65% in April in USD terms, despite a 25% rise in imports, likely due to higher oil prices. Inflation in China also accelerated in April because of rising energy prices, but China has been fighting deflation since post-Covid and therefore has more room to withstand price pressures than many Asian and Western peers.

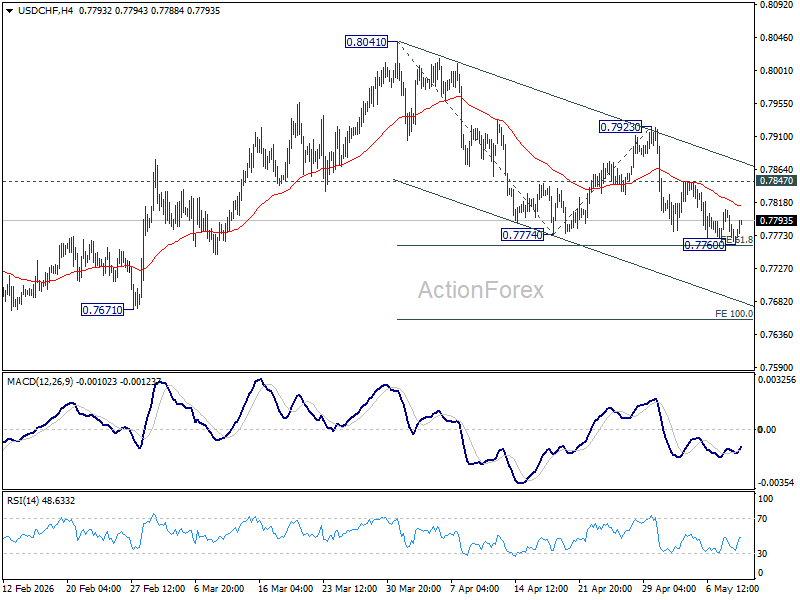

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7746; (P) 0.7777; (R1) 0.7793; More….

Intraday bias in USD/CHF is turned neutral again with current recovery. On the downside, decisive break of 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758 will resume the whole decline form 0.8041, and target 100% projection at 0.7656. However, firm break of 0.7847 resistance will indicate short term bottoming, and bring stronger rebound back to 0.7923 resistance.

In the bigger picture, as long as 55 W EMA (now at 0.8051) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

Dollar Recovers as Iran Talks Stall, Focus Turns to Trump-Xi Summit

The market narrative is becoming more complicated. Dollar and oil are rising again as Iran negotiations stall, yet semiconductor-driven equity rallies continue pushing Asian tech markets higher, highlighting how AI momentum is still partially insulating risk assets from geopolitical stress.

Markets entered the weekend expecting at least some form of diplomatic breakthrough between Washington and Tehran. Instead, they woke up Monday facing another reminder that the Middle East crisis may be drifting into something much longer and more dangerous than a simple “deal or war” scenario. Oil prices jumped sharply, Dollar rebounded broadly, and traders began rebuilding geopolitical risk premium after the highly anticipated US-Iran agreement failed to materialize.

Brent crude surged back above $105 after Iran rejected the Trump administration’s hardline 14-point memorandum of understanding. Tehran responded with its own counterproposal, reportedly demanding immediate sanctions relief, a broader regional military halt, and a phased long-term approach toward nuclear restrictions. US President Donald Trump responded late Sunday with a series of Truth Social posts calling the proposal “TOTALLY UNACCEPTABLE,” signaling that negotiations remain deeply deadlocked.

Yet the broader market reaction was far from classic panic. Gold softened and slipped back below $4700, while Asian technology stocks continued powering higher. South Korea’s KOSPI exploded another 4.5% to fresh record highs as semiconductor names extended their AI-fueled rally. Strong leads from US technology stocks again overwhelmed regional geopolitical concerns. Japan’s Nikkei also briefly touched fresh record highs before pulling back modestly.

The divergence across asset classes was striking. Oil and Dollar traded like geopolitical stress mattered again. Equities, particularly semiconductors, continued trading as though the AI cycle remained the dominant force in global markets. That split may continue to be the defining theme for the week ahead.

Attention is now shifting toward Trump’s upcoming state visit to China from May 13–15, the first trip by a US president to Beijing in nearly nine years. Trump and Xi Jinping are expected to discuss trade, Taiwan, artificial intelligence competition, rare earth export restrictions, and perhaps most critically, the Iran conflict and Hormuz security situation.

There is also a growing theory circulating across markets that Iran may intentionally be delaying negotiations until after the Trump-Xi summit. That could be referred to as the “Dragon Factor” — the belief that Tehran hopes China could negotiate some form of energy-security arrangement or oil corridor that weakens US leverage over Hormuz and sanctions enforcement. Whether realistic or not, the theory highlights how deeply interconnected geopolitics, trade, and energy markets have become.

Before the summit itself, Chinese Vice Premier He Lifeng and US Treasury Secretary Scott Bessent are expected to meet in South Korea on Wednesday for preliminary trade discussions. Any signs of coordination between Washington and Beijing regarding energy stability could quickly become the single most important driver for oil markets.

Meanwhile, this week also carries major monetary policy implications. On Tuesday, the US Senate is expected to approve Kevin Warsh as the next Federal Reserve Chair ahead of Jerome Powell’s departure later this week. Inflation data will follow closely behind, with April CPI forecast to rise to 3.7% yoy while Core CPI could accelerate to 2.9%. If energy-driven inflation begins spilling further into core prices, markets may have to reassess whether the current “Fed on hold” consensus can survive a prolonged oil shock.

Other major releases include the BoC Summary of Deliberations, which is expected to reinforce a cautious hold stance despite mounting oil-driven inflation pressure. German ZEW sentiment is likely to deteriorate further as industrial weakness deepens, while UK GDP later this week may show the first meaningful “war drag” from higher energy cost

In currency markets today, Dollar is currently the strongest performer, followed by Loonie and Euro. Kiwi is the weakest, followed by Swiss Franc and Sterling. Aussie and Yen are trading more mixed.

In Asia, at the time of writing, Nikkei is down -0.37%. Hong Kong HSI is down -0.36%. China Shanghai SSE is down -0.31%. China Shanghai SSE is up 0.64%. Singapore Strait Times is up 0.35%. Japan 10-year JGB yield is up 0.033 at 2.510.

| Event | Timing | Market Focus |

|---|---|---|

| Trump-Xi Summit | May 13–15 | Trade, AI, Taiwan, rare earths, Iran/Hormuz |

| He Lifeng–Bessent Meeting | May 13 | Pre-summit US-China economic and trade discussions |

| Fed Chair Transition Vote | May 12 | Senate vote on Kevin Warsh replacing Powell |

| US CPI | May 12 | Headline CPI expected at 3.7% yoy. Core at 2.9%. |

| BoC Summary of Deliberations | May 13 | Oil shock vs rate hold debate |

| German ZEW Sentiment | May 12 | Weak industrial outlook and trade deterioration |

| UK GDP | May 14 | Economic impact of energy shock |

US-Iran Peace Deal Failed — Brent Oil’s Triangle Pattern Warns Bigger Shock Ahead

Markets spent last week betting the US-Iran conflict was moving toward controlled de-escalation. That assumption is now under pressure after Trump rejected Tehran’s counterproposal and Brent oil surged back toward $105. More importantly, crude’s tightening triangle pattern suggests the market may be “storing energy” for a much larger move ahead. Read More.

China Inflation Heats Up as PPI Hits 45-Month High

China’s inflation rebound accelerated sharply in April, with producer prices hitting a 45-month high and consumer inflation also beating expectations. Rising fuel costs helped drive the move, but core inflation data suggested price pressures are now spreading more broadly across the economy. The data strengthens the view that China’s long deflation cycle may finally be ending. Read More.

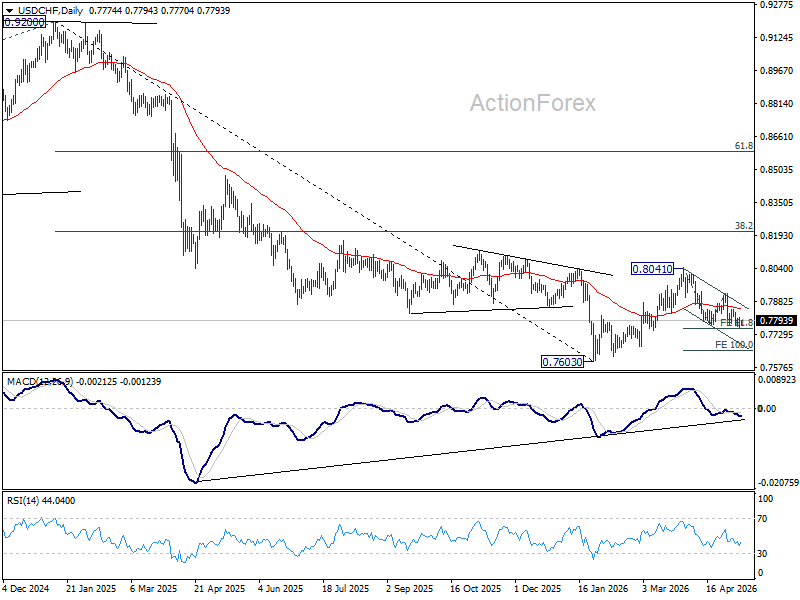

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7746; (P) 0.7777; (R1) 0.7793; More….

Intraday bias in USD/CHF is turned neutral again with current recovery. On the downside, decisive break of 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758 will resume the whole decline form 0.8041, and target 100% projection at 0.7656. However, firm break of 0.7847 resistance will indicate short term bottoming, and bring stronger rebound back to 0.7923 resistance.

In the bigger picture, as long as 55 W EMA (now at 0.8051) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

China Plays to Its Comparative Advantage

In trade, investment and, with time, via financial flows, China has a considerable long-term advantage that is set to grow their real economy and national wealth.

This week, President Xi and President Trump are due to meet and discuss China/US relations, developments in the global economy and, barring a resolution before, likely the conflict in the Middle East. This meeting will not materially change the status quo, being one of a number of in-person meetings planned for this year. But it will guide on the opportunities and risks ahead. Available data points to a stark difference in perspective and each nation’s outlook.

As the US continues to focus on controlling trade across its borders in pursuit of greater domestic investment and production, China has instead enticed investment at home by encouraging foreign trade. To date in 2026, China’s trade surplus has averaged US$88bn per month after holding around US$99bn in 2025, both outcomes roughly three times the 2018-19 average of US$32bn.

The US trade position has, in contrast, deteriorated from an average deficit of US$47bn per month in 2018-19 to US$73bn in 2025-26. This US data admittedly pre-dates the surge in energy exports seen through April and May, but China has also temporarily pulled back on their supply of energy goods to other nations, reducing export revenue.

With future export opportunities remaining the focus, Chinese fixed asset investment continues to grow after rapidly scaling through 2020-2025. Of particular note, transport and storage-related infrastructure spending surged in early-2026, and utilities investment has continued to compound around 9%ytd.

Within the manufacturing sector, stronger demand for green technology goods and refined energy products is likely to elicit a sustained upturn in capital expenditure through 2026, with the key investment sub-categories of electrical machinery, automobiles (EVs) and chemicals all showing evidence of stabilisation in Q1, and global demand receiving strong support from elevated energy prices and open-ended uncertainty over Middle East supply.

In contrast, in the US, investment remains highly concentrated in AI-related infrastructure and conversely is weak in areas related to trade and the domestic real economy. Lingering uncertainty related to tariffs and elevated long-term yields are also at play, in addition to businesses’ focus on technology – US for-profit entities need greater surety over expected returns than China’s state-owned and state-linked entities.

An additional element to consider is the benefit China may receive from the US’ souring relationship with other nations, particularly Europe. This month, President Trump has continued to spar with European leaders, threatening to pull US troops from Germany and other major nations in the region. He then threatened a 10 percentage point increase in the US tariff rate for European cars and trucks, purportedly because the EU had failed to live up to their side of the agreed trade deal.

The EU labelled the US as an “unreliable” trading partner and vowed to respond. Ahead of this development, Chinese authorities were acting to strengthen ties with European leaders, publicly via a number of high-profile visits from European leaders, and behind the scenes by encouraging Chinese firms to invest in Europe and vice versa. There is strong evidence of an integrated, mutually-beneficial trade relationship taking shape between China and Europe.

As we have highlighted frequently, Chinese investment is not concentrated in one jurisdiction, however. It has also spread widely across Asia, Latin America and Africa, targeting not only the production of finished goods, but also the production of supply inputs – from raw materials to high-tech components.

While not their initial intent, over time this project will justify a material increase in the use of the Renminbi in trade, and will also strengthen demand for real and financial investment within China.

These trends will see greater depth and liquidity for China’s onshore financial markets, as well as scope to offer global investments to Chinese investors through the issuance of Renminbi denominated debt and equity instruments. The larger these flows become, the greater the opportunity for Chinese banks and financial entities to facilitate flows, provide capital and manage risk, both on and, more importantly, offshore.

Overall then, in trade, investment and, with time, via financial flows, China has a considerable long-term competitive advantage that is set to benefit their real economy and national wealth.

This analysis initially appeared in Westpac Economics’ May Market Outlook.