Sample Category Title

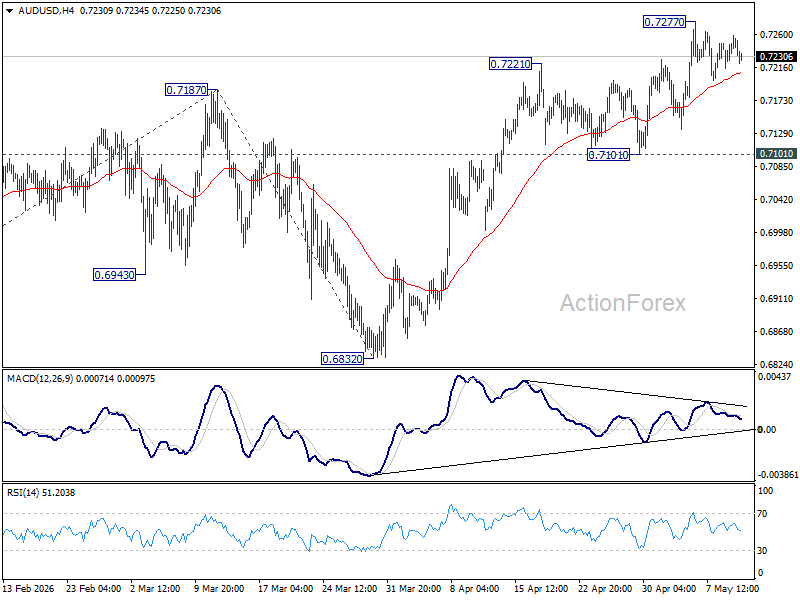

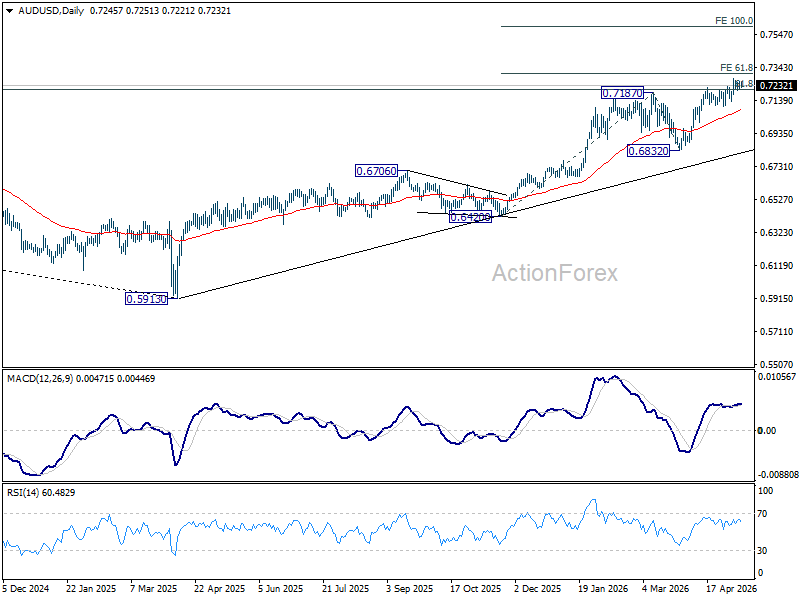

AUD/USD Daily Report

Daily Pivots: (S1) 0.7222; (P) 0.7240; (R1) 0.7266; More...

Range trading continues in AUD/USD below 0.7277 and intraday bias remains neutral. Further rise is expected as long as 0.7101 support holds. On the upside, above 0.7277 will resume larger up trend and target 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.

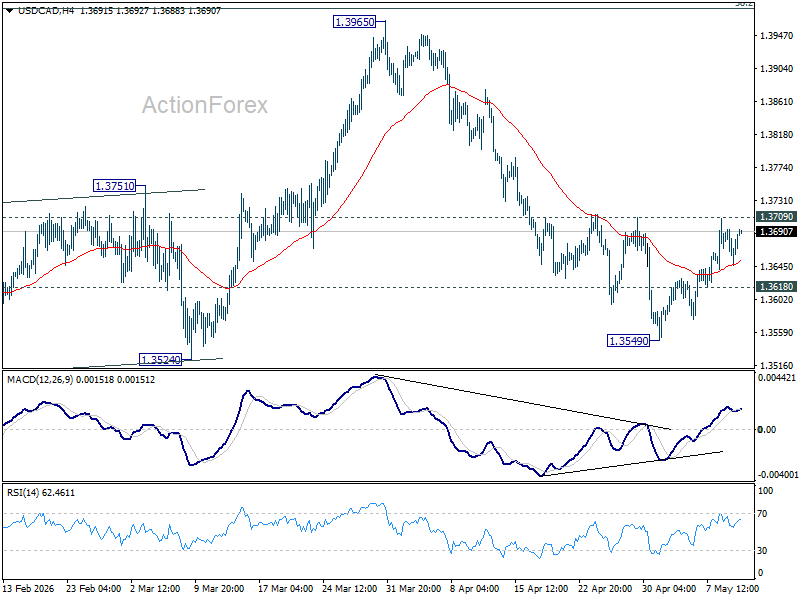

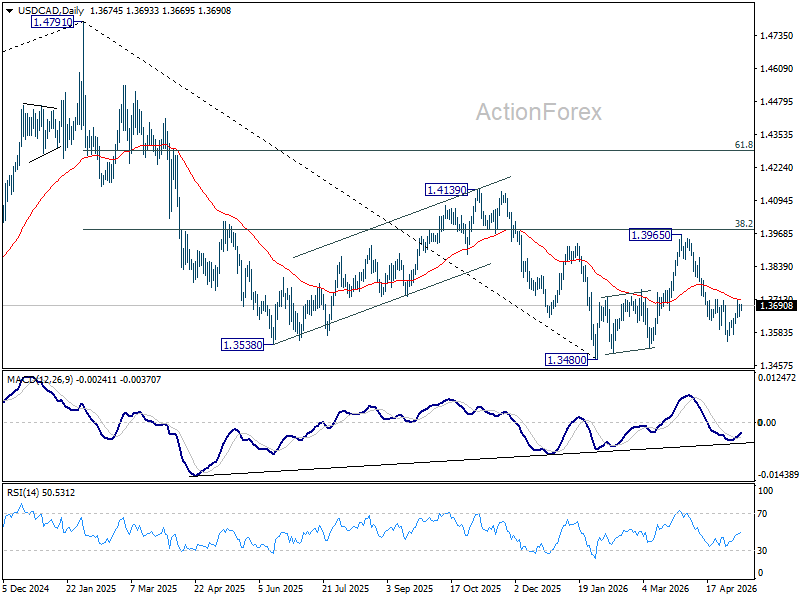

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3650; (P) 1.3672; (R1) 1.3697; More...

Intraday bias in USD/CAD remains neutral for the moment. On the downside, below 1.3618 minor support will suggest that recovery fro 1.3549 has completed, and turn intraday bias back to the downside. Break of 1.3549 will bring retest of 1.3480 low. However, sustained break of 1.3709 will confirm short term bottoming. Intraday bias will be back on the upside for 1.3965 resistance again, as in the third leg of the corrective pattern from 1.3480.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already.

Markets Turn to US CPI as Geopolitical Traders Hold Fire

Markets entered a temporary holding pattern on today as traders largely refrained from making aggressive geopolitical bets ahead of both US inflation data and Thursday’s Trump-Xi summit. Despite hostile rhetoric surrounding the Iran ceasefire, broader market reactions remained restrained, with investors appearing reluctant to commit strongly in either direction until clearer signals emerge later this week.

US President Donald Trump sharply escalated his criticism of Tehran overnight, describing the month-old ceasefire as “unbelievably weak” and effectively “on massive life support” after Iran submitted what he called an “unacceptable” counterproposal to Washington’s latest peace framework. “I would say the ceasefire is on massive life support, where the doctor walks in and says, ‘Sir, your loved one has approximately a 1% chance of living,’” Trump said in the Oval Office. Still, markets showed only measured reactions to the comments.

US equities closed modestly higher overnight, Brent crude stayed capped around the $105 level, and the US 10-year Treasury yield edged up only slightly to around 4.41%. Dollar attempted to extend its recent rebound but remained trapped within familiar trading ranges without decisive follow-through momentum. However, despite the deteriorating rhetoric, markets appear increasingly focused on whether larger geopolitical powers can eventually engineer some form of containment framework.

For now, traders appear unwilling to significantly expand geopolitical positioning before Thursday’s Trump-Xi summit in Beijing. When Pakistan’s mediation stalled last month, it exposed a fundamental wall that Islamabad couldn't climb: Trust and Enforceability. Pakistan has the diplomatic ties, but China has the "checkbook" and the "oil straw" that Iran actually depends on.

China is increasingly viewed as the only party with the leverage to actually reopen the Strait of Hormuz. Recent reports indicate that Iranian officials have been in Beijing specifically to discuss reopening the shipping lanes. Investors likely believe that no matter how much "garbage" (to use Trump's word) is in the current proposal, the real deal will be brokered—or at least green-lit—by Xi and Trump face-to-face.

As a result, markets are temporarily shifting focus back toward more traditional macro catalysts, with today’s US CPI report as the primary near-term volatility trigger. Markets expect headline CPI to rise 0.6% mom in April, lifting the year-on-year rate to 3.7%, which would mark the strongest inflation reading since September 2023. Core CPI is projected to accelerate from 2.6% yoy to 2.7% yoy, partly boosted by a one-time technical adjustment linked to last year’s government shutdown.

The implications for Federal Reserve expectations could be significant. Investors have already been steadily abandoning expectations for rate cuts this year as energy prices rise and inflation risks re-emerge. A hotter-than-expected CPI report could push markets even further toward pricing a prolonged Fed hold — or potentially reopening discussions around additional tightening. The Senate vote on Kevin Warsh’s nomination as Fed Chair is also due today, though markets currently see little chance of surprise around the outcome.

In currency markets, Dollar is currently the strongest major currency for the week so far, followed by Kiwi and Loonie. Yen is the weakest performer, followed by Swiss Franc and Sterling, reinforcing the idea that investors are not yet embracing a full-scale risk-off positioning shift despite lingering geopolitical uncertainty.

In Asia, at the time of writing Nikkei is up 0.42%. Hong Kong HSI is up 0.15%. China Shanghai SSE is down -0.53%. Singapore Strait Times is down -0.08%. Japan 10-year JGB yield is up 0.022 at 2.547. Overnight, DOW rose 0.19%. S&P 500 rose 0.19%. NASDAQ rose 0.10%. 10-year yield rose 0.04 to 4.41.

Silver’s $6 Surge May Be the Start of a FOMO Phase

Silver’s explosive rally may be entering a new phase as investors abandon hopes for a pullback and begin chasing momentum instead. The metal’s breakout above the critical 84.21–84.46 resistance zone, combined with a collapsing Gold-Silver Ratio and persistent global supply deficits, is fueling speculation that the rally could accelerate further toward 92.90. Read More.

BoJ Summary Shows Growing Support for Near-Term Rate Hike

The BOJ’s April meeting summary revealed a noticeably more hawkish debate inside the board, with several policymakers openly discussing the possibility of another rate hike as the Iran-driven oil shock lifts inflation risks. Markets are increasingly pricing a potential move as early as June. Read More.

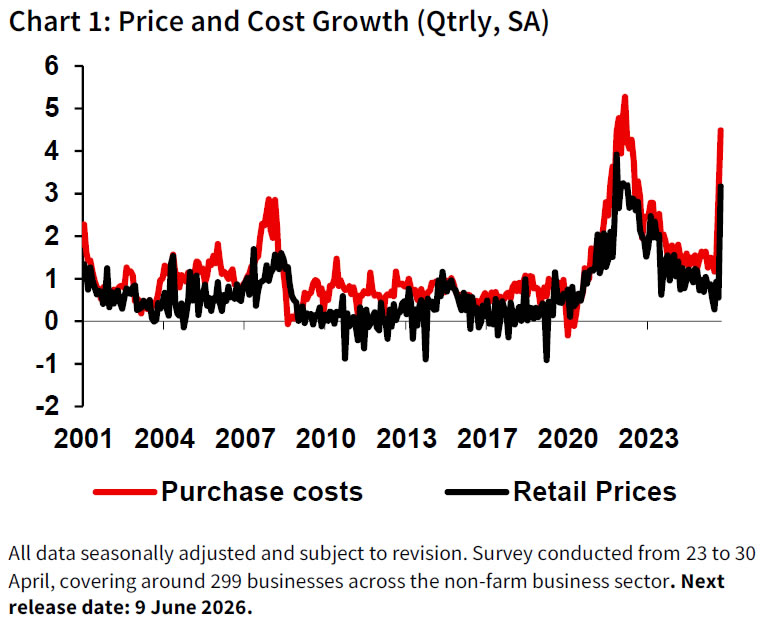

Australia NAB Survey Shows Cost Growth Jumps to 4.5% as Margin Squeeze Intensifies

Australia’s April NAB survey painted an increasingly stagflationary picture as purchase cost growth surged to 4.5% following the Middle East energy shock. While firms continued facing rising input costs, weaker trading, employment, and activity indicators suggested margin pressure is beginning to weigh more heavily on the broader economy. Read More.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3650; (P) 1.3672; (R1) 1.3697; More...

Intraday bias in USD/CAD remains neutral for the moment. On the downside, below 1.3618 minor support will suggest that recovery fro 1.3549 has completed, and turn intraday bias back to the downside. Break of 1.3549 will bring retest of 1.3480 low. However, sustained break of 1.3709 will confirm short term bottoming. Intraday bias will be back on the upside for 1.3965 resistance again, as in the third leg of the corrective pattern from 1.3480.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already.

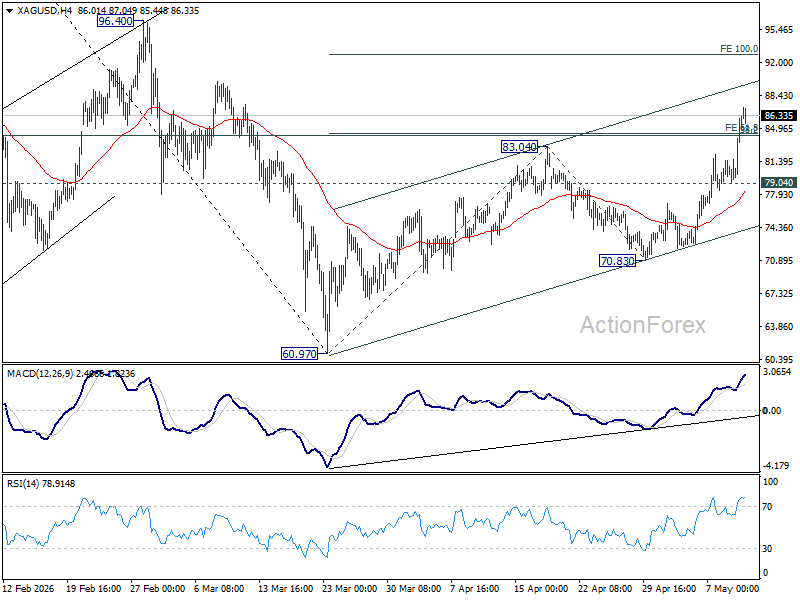

Elliott Wave Outlook: Silver (XAGUSD) Five Wave Advance Signals Bullish Continuation

The short‑term Elliott Wave view in Silver (XAGUSD) indicates a constructive bullish sequence after the break above the April 17 peak at 83.05. That move confirmed a higher‑high structure and reinforced the upward bias. From the April 30 low, the rally has unfolded as a five‑wave impulse, a classic Elliott Wave formation that often signals continuation of strength.

Wave (i) advanced to 76.96, while the corrective pullback in wave (ii) found support at 72.16. Momentum then carried the metal higher in wave (iii), reaching 82.12. A modest retracement in wave (iv) concluded at 78.08, preserving the integrity of the bullish sequence. The structure now points toward one final leg higher to complete wave (v). This move should also finalize wave ((i)) of a larger degree, setting the stage for a corrective phase in wave ((ii)). That correction will balance the cycle from the April 30 low before the broader rally resumes.

Near term, the key pivot rests at 70.95. As long as this level remains intact, pullbacks are expected to attract buyers. Corrective sequences may unfold in three, seven, or eleven swings, each offering potential entry points for continuation of the bullish trend.

Spot Silver (XAGUSD) 60-Minute Elliott Wave Chart

XAGUSD Elliott Wave Video:

https://www.youtube.com/watch?v=dLrJP4_qXao

Silver’s $6 Surge May Be the Start of a FOMO Phase

Silver bulls may finally be getting the move they have been waiting for — and the rally could now be feeding itself.

On Monday, Silver exploded higher by more than $6 an ounce at its peak, marking its biggest single-day surge since February. But the most important part of the move may not be the size of the rally itself. It is what the rally says about investor psychology. For weeks, traders kept waiting for a meaningful pullback toward the 70–75 area that never came. Now, the market may be shifting from “wait for the dip” to "fear of missing out".

The clearest sign of that transition is how aggressively Silver is outperforming Gold. Normally, periods of geopolitical stress and inflation fears tend to favor Gold as the safer defensive asset. Instead, Silver is taking the lead. That suggests markets are starting to lean toward growth optimism, industrial demand strength, and the broader AI-electrification story.

The “smoking gun” is the Gold-Silver Ratio. Since mid-April, it has collapsed from above 61:1 to 55, signaling increasingly aggressive relative buying of Silver. In macro terms, that ratio compression strongly suggests investors are pricing economic activity and industrial demand rather than simply seeking shelter from uncertainty.

Fundamentally, the setup has been building quietly for a long time. Global Silver demand is projected to exceed supply for a sixth consecutive year in 2026, creating a structural deficit that many traders believed would eventually matter. For months, however, Silver struggled to fully capitalize on that backdrop because Dollar stayed relatively firm on Middle East tensions and many investors doubted the rally’s durability. The market became crowded with traders waiting for weakness that never arrived.

That hesitation may now be turning into forced participation. Once markets realize the expected pullback is not happening, positioning can shift violently. Silver’s rally increasingly has the feel of a market transitioning from skepticism into momentum chasing — and those phases can accelerate quickly.

Technically, the breakout was extremely significant. Silver sliced through the major 84.21–84.46 resistance zone without much difficulty, a clear sign that buying pressure overwhelmed supply. That area included both 100% projection of 60.97 to 83.04 from 70.83 at 84.46 and 38.2% retracement of 121.83 to 60.97 at 84.21.

The next major technical target now sits near 100% projection at 92.90. As long as 79.04 support holds, the near-term outlook remains cautiously bullish.

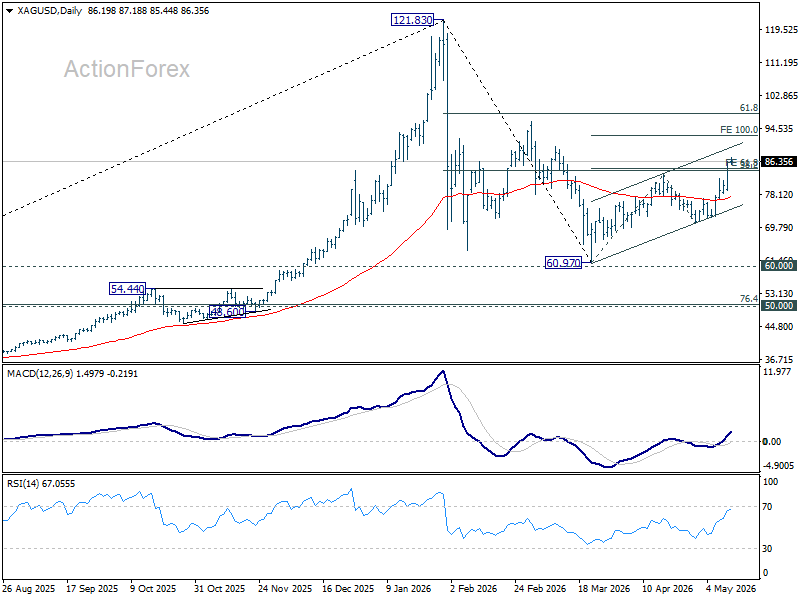

But the bigger long-term question is still unresolved. It remains too early to say whether Silver is truly beginning a new secular breakout through 121.83 record high. The rally from 60.97 could merely be the second leg of the corrective pattern from 121.83.

The answer may depend on what happens next around 92.90. If momentum accelerates further through that level, the psychology of the market could shift again — from FOMO into something much bigger.

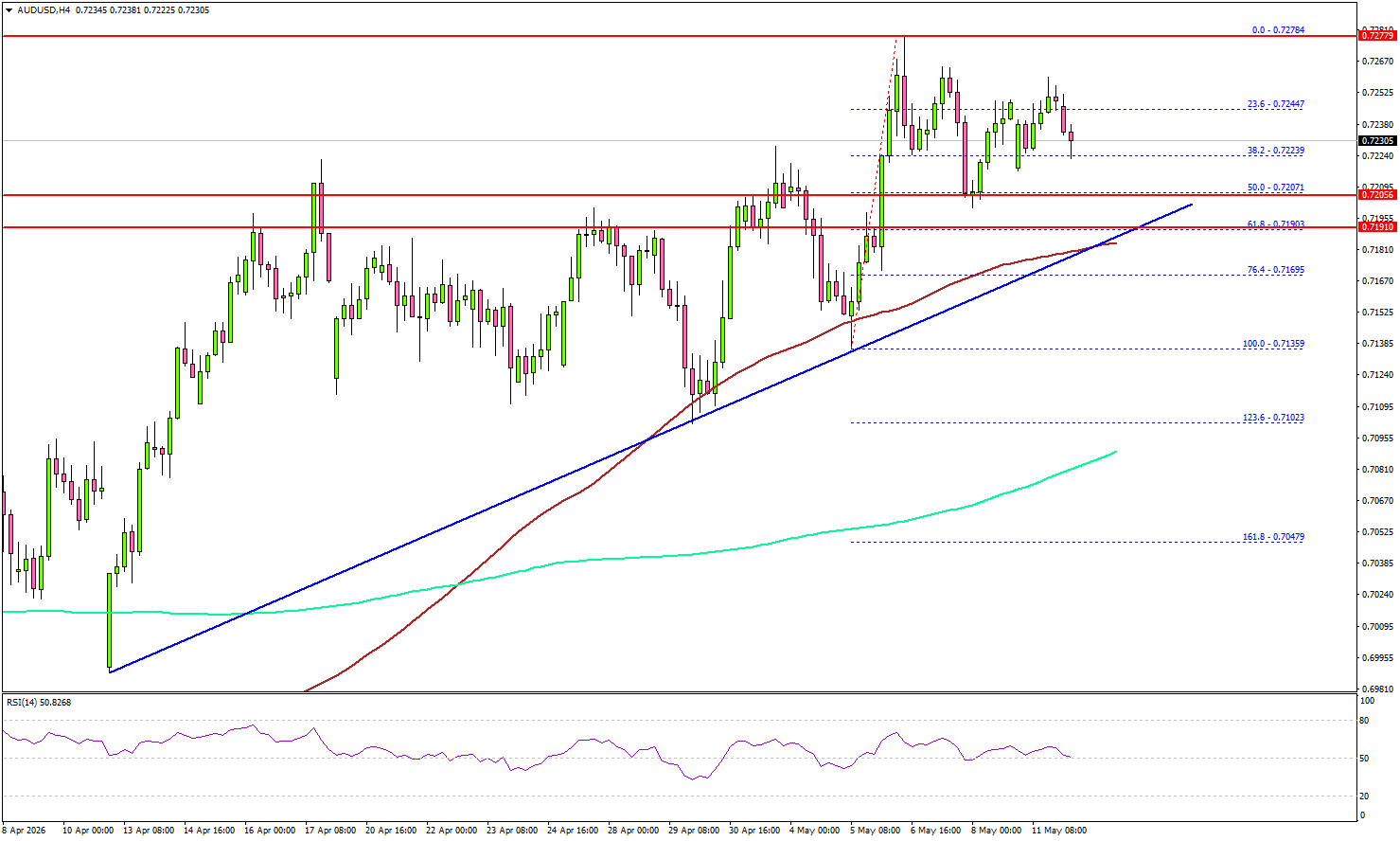

AUD/USD Signals Strength, Major Bullish Break May Be Near

Key Highlights

- AUD/USD started a fresh increase above the 0.7200 pivot zone.

- A bullish trend line is forming with support at 0.7190 on the 4-hour chart.

- EUR/USD could gain strength if it clears 1.1800 and 1.1840.

- USD/JPY started a consolidation phase below the 158.00 resistance.

AUD/USD Technical Analysis

The Aussie Dollar remained supported above 0.7120 against the US Dollar. AUD/USD started a fresh increase above the 0.7180 and 0.7200 resistance levels.

Looking at the 4-hour chart, the pair settled above the 0.7200 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). A high was formed at 0.7278 before there was a pullback.

The pair dipped below 0.7250 and tested the 50% Fib retracement level of the upward move from the 0.7135 swing low to the 0.7278 high. The bulls remained active above 0.7200 and the pair recovered losses.

There is also a bullish trend line forming with support at 0.7190. On the upside, the pair faces resistance at 0.7275. The first major resistance sits at 0.7300. The main resistance could be 0.7320.

A close above 0.7320 could open doors for gains above 0.7365. In the stated case, the bulls could aim for a move to 0.7450. If there is a downside correction, the pair could find support at 0.7220. The next support could be near the trend line or 0.7200.

A close below 0.7190 might push the pair toward 0.7135. Any more losses could initiate a fresh move to 0.7080 and the 200 simple moving average (green, 4-hour).

Looking at EUR/USD, the pair is showing positive signs, and the bulls could aim for a move above the 1.1840 resistance.

Upcoming Key Economic Events:

- US Consumer Price Index for April 2026 (MoM) – Forecast +0.6%, versus +0.9% previous.

- US Consumer Price Index for April 2026 (YoY) – Forecast +3.7%, versus +3.3% previous.

- US Consumer Price Index Ex Food & Energy for April 2026 (YoY) – Forecast +2.7%, versus +2.6% previous.

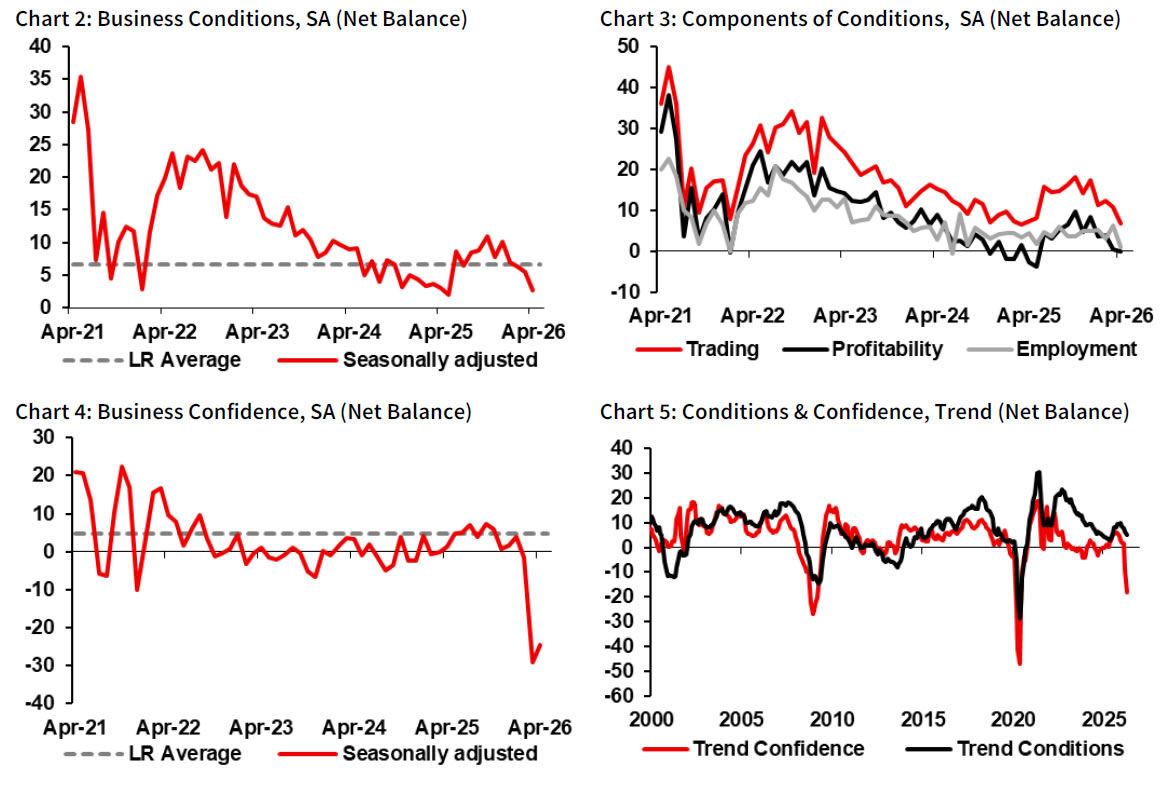

Australia NAB Survey Shows Cost Growth Jumps to 4.5% as Margin Squeeze Intensifies

Australia’s NAB business survey for April painted an increasingly stagflationary picture, with activity indicators weakening further even as cost pressures accelerated sharply. Business confidence improved slightly from -29 to -24, but remained deeply negative, while business conditions fell from 6 to 3, pointing to a significant slowdown in underlying activity momentum.

The deterioration was broad-based. Trading conditions dropped from 11 to 7, employment conditions slumped from 6 to 1, and profitability remained stuck at 0 as firms struggled to absorb surging costs.

Purchase cost growth accelerated sharply from 2.9% to 4.5% in quarterly terms following the Middle East energy shock, while final product price growth rose from 1.1% to 1.8%. The widening gap suggests businesses are facing increasing pressure on margins as rising input costs outpace their ability to pass prices on to consumers.

NAB said the survey highlighted the growing economic strain created by higher energy prices, warning that rising costs and softer demand are beginning to weigh on activity and investment. Forward orders, capex, cashflow, and employment have all fallen noticeably in recent months and are now sitting well below long-run averages.

| Indicator | Previous | Latest |

|---|---|---|

| NAB Business Confidence | -29 | -24 |

| NAB Business Conditions | 6 | 3 |

| Trading Conditions | 11 | 7 |

| Profitability Conditions | 0 | 0 |

| Employment Conditions | 6 | 1 |

| Purchase Cost Growth (Quarterly) | 2.9% | 4.5% |

| Final Product Price Growth (Quarterly) | 1.1% | 1.8% |

BoJ Summary Shows Growing Support for Near-Term Rate Hike

Bank of Japan’s Summary of Opinions from the April meeting revealed a noticeably more hawkish debate inside the board, with several policymakers arguing that another interest rate hike could come sooner rather than later as the Iran war intensifies inflation pressures. One member explicitly said “it is quite possible the BoJ will raise interest rates from the next meeting onward,” even if uncertainty surrounding the Middle East conflict remains unresolved.

The summary showed increasing concern that the oil shock could accelerate underlying inflation and trigger broader second-round price effects. One policymaker warned that “all scenarios point to further upside risks to prices,” while another argued the BoJ should “raise rates soon barring evident signs of an economic slowdown.” Policymakers also highlighted the risk that supply-side constraints linked to the conflict could generate “extremely strong upward pressure on prices.”

The discussion reinforced expectations that the BoJ is gradually shifting toward another normalization step. One member argued the current policy rate remains far below neutral levels and said the central bank should continue raising rates at intervals of a few months, adding tightening should accelerate “without hesitation” if inflation risks intensify further.

At the April 27–28 meeting, the BoJ left its short-term policy rate unchanged at 0.75%, though three of the nine board members voted in favor of an interest-rate hike, a proposal that was ultimately rejected.

Following the release, Japan’s 10-year government bond yield climbed to a fresh 29-year high as markets increased bets on a possible rate hike at the June 15–16 meeting.

Silver (XAG/USD) Is in Breakout Mode, Pushing Above $85: In-Depth Technical Analysis

Silver has officially entered what looks to be a real breakout.

As we noted in our Friday analysis, the metals sector was overdue for a rally, and that move is now underway. Silver has attracted strong buying and has surged past the key $85 level to start the week, up 7% on the session.

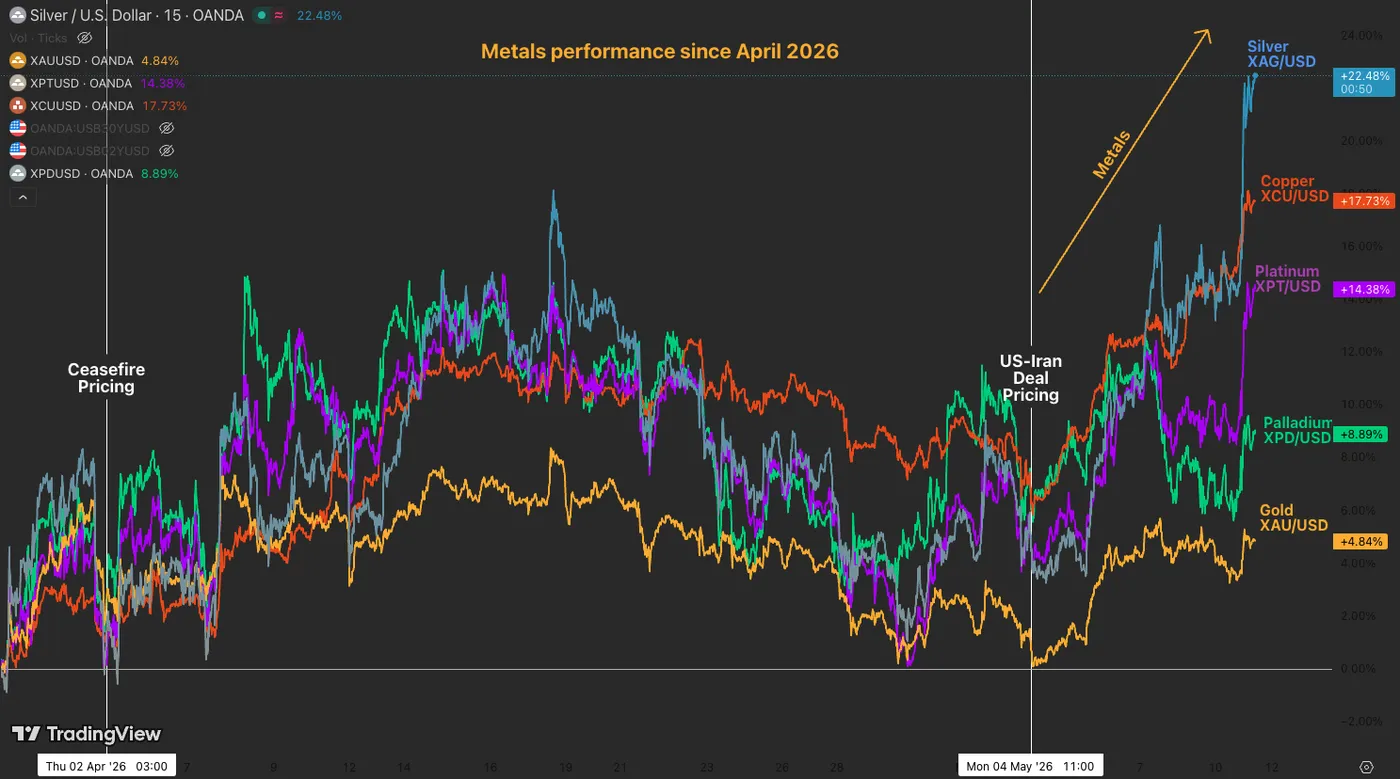

Daily Metal Performance, May 11, 2026. Source: Finviz.

The macroeconomic environment is changing. In recent weeks, if not months now, geopolitical headlines have stopped driving daily moves in most risk assets, and precious commodities were not isolated.

Metals were hit hard at first by conflict and rate-hike fears, but while that link has not disappeared, it is fading.

Energy is now the only asset class still reacting to news coming from the Middle East, mostly because of supply issues in Hormuz and the lack of a ceasefire agreement.

One of the most interesting parts of this breakout is the fact that Silver is moving higher without help from gold, which usually sets the direction for the alternative asset class.

Normally, silver follows Gold’s moves, but this time, the strong bounce suggests there is real demand and strong buying interest focused on alternative metals instead.

Traders could also be responding to China’s higher inflation report from yesterday, which suggests its inflation, a shortcut for economic activity after deflationary trends, is starting to recover.

Silver and Copper are not just precious metals; they are mainly industrial metals.

When China, the world’s largest industrial producer, shows stronger economic activity, it usually means demand for these metals is rising.

Metals performance since April 2026. Source: TradingView, May 11, 2026.

We will dive into a Silver two-timeframe intraday analysis to prepare for the heavy action unfolding in front of our eyes. Is this a breakout?

Let's get right into it.

Silver (XAG/USD) Intraday Timeframe Technical Analysis

4H Chart and Technical Levels

Silver 4H Chart, May 11, 2026. Source: TradingView.

After forming a bullish weekly divergence, the action is now turning much more bullish, and this translated into a break of the prior $83 to $84.50 resistance, now acting as a key momentum pivot.

Evolving into a steep bull channel, the move should trigger high volatility in the coming days.

Without many resistance levels until then, bulls should remain in control until $90, a level to be closely monitored.

Levels to watch for Silver (XAG) trading:

Resistance Levels:

- March range resistance: $90 to $92

- March high resistance: $95 to $97

- Key psychological resistance: $100 to $104

- All-time highs: $121

Support Levels:

- Major resistance now pivot: $83 to $84.50

- Pivot highs: $80 to $81.50

- Pivot lows: $74.50 to $75

- $61.10 war lows

1H Chart

Silver 1H Chart, May 11, 2026. Source: TradingView.

Looking at the 1H candle points to clearer action ahead, with the morning extension now pointing to a slowing in the buying due to the overbought RSI.

The fact that the action did not pull back, however, translates into buyers not giving up their freshly gained advantage.

Check out reactions to the channel top, around $86.50.

For late bulls, watch out for overbought conditions. To do so, either wait for a continued explosion with a buy stop above $87 or a pullback to $81.50 to $82.

Safe trades.

Stocks Hit New Highs on AI Optimism as US-Iran Ceasefire Hangs by a Thread

Key Takeaways

- Global equity markets, led by Nasdaq 100, S&P 500, Nikkei 225, and KOSPI, climbed to fresh record highs as AI-driven optimism continued to overpower geopolitical concerns surrounding the fragile US-Iran ceasefire.

- Rising oil prices, stronger inflation expectations, and hawkish Federal Reserve rhetoric reinforced the “higher-for-longer” interest rate narrative, pushing US Treasury yields higher and supporting broad US dollar strength.

- Chart of the day: The Hang Seng Index maintained a constructive bullish structure after rebounding from its 20-day moving average, with momentum indicators suggesting potential upside continuation above the 26,210/100 support zone.

Top Macro Headlines

- US-Iran ceasefire 'on life support': US President Donald Trump stated the ceasefire with Iran is fading, dashing hopes for an imminent peace deal after rejecting Iran's recent proposal as "unacceptable" over the weekend.

- Global stocks reach record highs: Major indices, including the S&P 500, Nasdaq 100, Nikkei 225, and KOSPI, powered to new record highs as the "artificial intelligence fever" vastly outweighed concerns over Middle East supply shocks.

- Alphabet and Amazon tap overseas debt: Tech giants are issuing debt in lower-yielding currencies like the Japanese yen and Swiss francs to fund massive AI infrastructure buildouts without draining cash reserves.

- Trump heads to China for crucial summit: President Trump and Chinese President Xi Jinping are set for comprehensive talks spanning Iran, nuclear issues, trade, and AI, accompanied by a large entourage of US corporate titans from companies like Tesla, Apple, and BlackRock.

- US CPI data looms: Markets brace for Tuesday's crucial April CPI report, with headline inflation expected to jump to 3.7% y/y from 3.3%, primarily due to the energy price shock caused by the ongoing Strait of Hormuz closure.

Key Macro Themes

- AI fever overpowers geopolitics: Record US equity prices are coexisting with elevated oil and rising yields. According to BlackRock, markets are comfortably pricing in both AI-driven growth and the impact of the Middle East supply shock, remaining heavily "pro-risk" despite the chaos.

- Extreme market concentration: Top-heavy indices have become a global feature. The top 10 US stocks now account for 33% of the overall market value. Meanwhile, single tech champions like Samsung and TSMC make up roughly 20% and 40% of their respective national indices.

- Inflation and hawkish Fed risks: With inflation metrics heating up and oil surging, Chicago Fed President Austan Goolsbee warned that the future of monetary policy could actually include interest rate increases, fundamentally challenging recent rate-cut hopes.

Global Market Impact: Last 24 Hours

Equities: The S&P 500 and Nasdaq closed at new record highs. The tech sector gained 1%, and energy rallied 2.6%, while the Philadelphia semiconductor index reached a new peak, rising 2.6%.

Fixed Income: US Treasury yields climbed, with a 6 basis point rise at the short end bear steepening the curve as a 3-year auction drew weak demand.

FX: The US Dollar inched higher, with the Japanese Yen serving as the biggest G10 decliner. Emerging market currencies like the Indian Rupee and South Korean Won dropped sharply on dollar strength and high energy costs.

Commodities: Oil surged 3%, jumping $3/barrel, as the Strait of Hormuz remains largely closed. Silver rallied 7% to hit a 2-month high at $86.10/oz, outperforming Gold, which recorded only a modest gain of 0.4% due to a rebound in US Treasury yields.

Asia Pacific Impact

- Stock markets: Regional markets broadly surged. The Nikkei, KOSPI, and MSCI Asia ex-Japan indices all hit new record highs. China's A-share market reached an 11-year high following a positive data dump showing surging export growth.

- Currencies: The region experienced broad weakness against the USD. The Yen fell 0.3%, while the Won dropped 1%, despite the massive regional equity rally.

- Economic outlook: China's latest trade data showed a widening trade surplus and rising price pressures in April, suggesting the economy is moving out of disinflation, though unemployment ticked up.

Top 3 Data/Events to Watch Today

- AU NAB Business Confidence (Apr) - 9.30 am SGT Impact: AUD/USD, AUD crosses, ASX 200

- Eurozone ZEW Economic Sentiment (May) - 5.00 pm SGT; consensus: -20, Apr: -20 Impact: EUR/USD, EUR crosses, DAX

- US Core Inflation (Apr) - 8.30 pm SGT; consensus: 2.7% y/y, Mar: 2.6% y/y Impact: All asset classes

Chart of the Day: Hang Seng Index Rebounded from 20-Day MA

Fig. 1: Hong Kong 33 CFD index minor trend as of 12 May 2026. Source: TradingView.

The price actions of the Hong Kong 33, a proxy of the Hang Seng Index futures, have managed a minor bullish reversal right above its 20-day moving average after a 1.7% decline from the 7 May 2026 intraday high of 26,634.

The overall price structure remains bullish as it continues to oscillate within a medium-term ascending channel in place since the 30 March 2026 low.

In addition, the hourly RSI momentum indicator has exhibited bullish momentum conditions as it continues to be supported by an ascending trendline above the 50 level and has not reached its overbought zone above the 70 level.

Watch the 26,210/100 key short-term pivotal support to maintain a potential bullish bias. A clearance above 26,723 sees the next intermediate resistance coming in at 27,100, also a Fibonacci extension.

On the other hand, failure to hold and an hourly close below 26,100 jeopardizes the bullish tone for a slide to retest the next intermediate support at 25,930, also the key 200-day moving average.