Sample Category Title

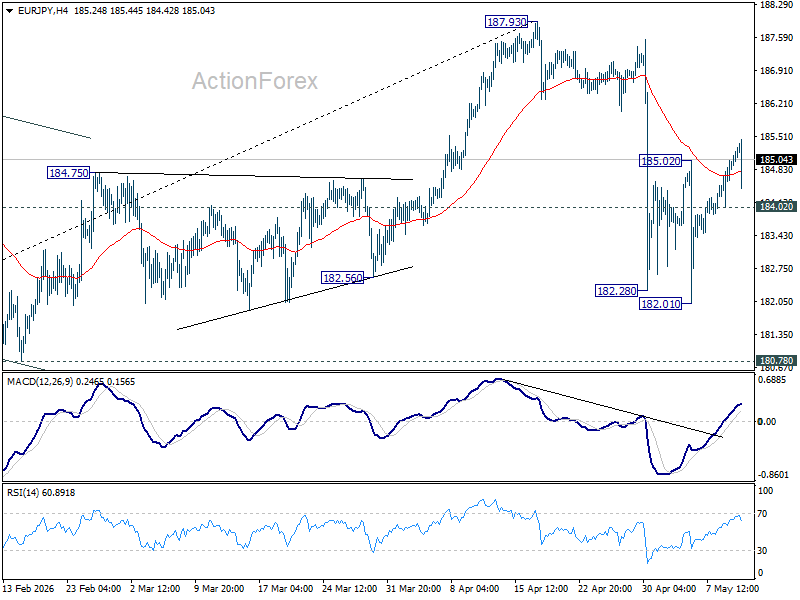

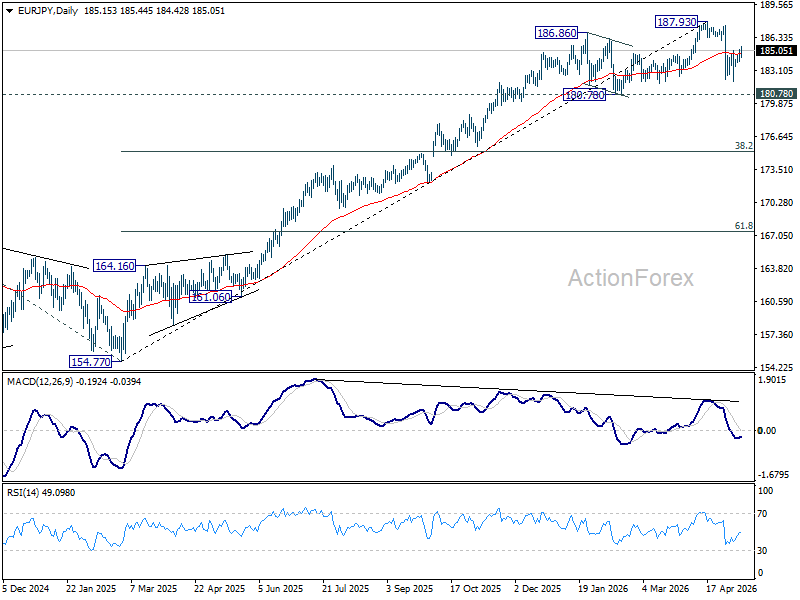

EUR/JPY Daily Outlook

Daily Pivots: (S1) 184.26; (P) 184.75; (R1) 185.65; More...

Intraday bias in EUR/JPY is mildly on the upside with break of 185.02 resistance. Pullback from 187.93 could have completed at 182.01 already. Further rise would be seen back to retest this high. Nevertheless, break of 184.02 minor support will turn bias back to the downside towards 182.01 again.

In the bigger picture, the pullback from 187.93 is steep, there is no sign of reversal yet. Uptrend from 114.42 is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 178.04) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.

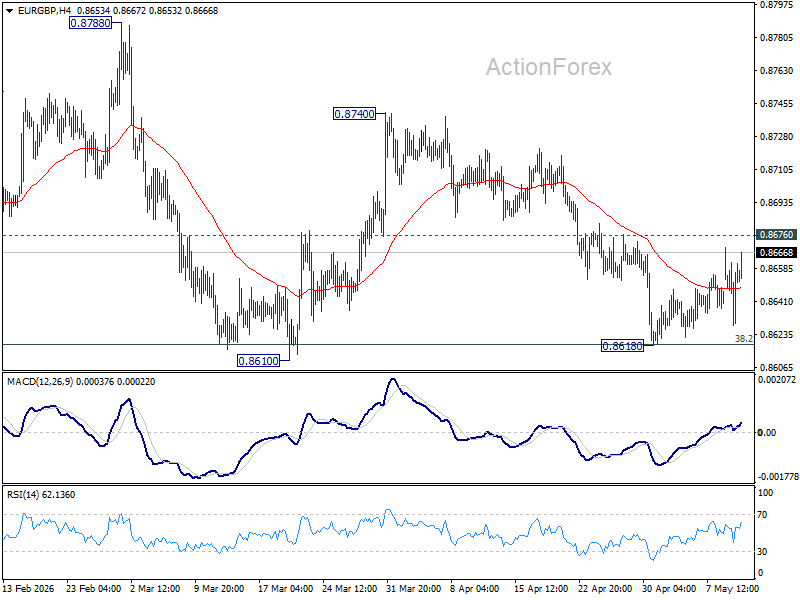

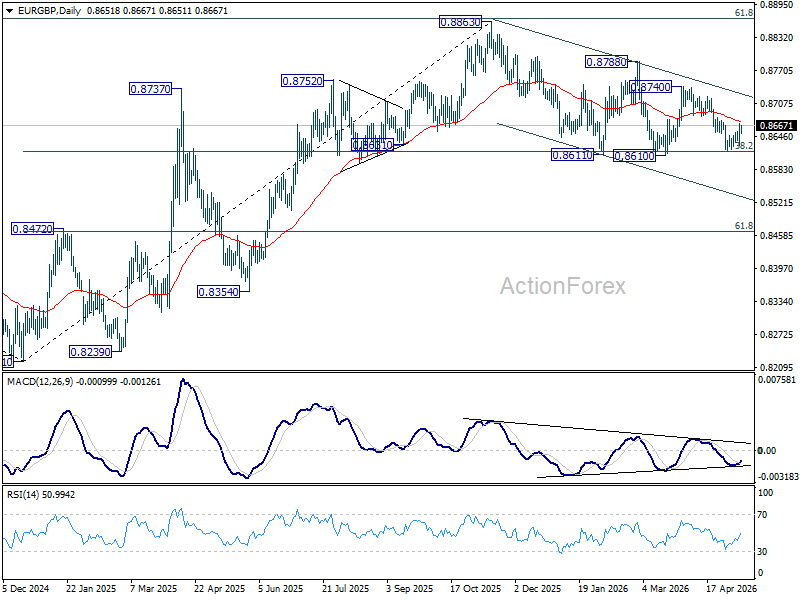

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8632; (P) 0.8651; (R1) 0.8673; More…

EUR/GBP is still bounded in established range above 0.8618 and intraday bias remains neutral. On the downside, firm break of 0.8610 will carry larger bearish implications and pave the way to 0.8466 fibonacci level next. Nevertheless, firm break of 0.8676 will turn bias back to the upside for stronger rebound back to 0.8740 resistance instead.

In the bigger picture, focus is back on 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Sustained break there will confirm that whole rise from 0.8221 has completed at 0.8863. Deeper decline should then be seen to 61.8% retracement at 0.8466 at least. For now, risk will stay mildly on the downside as long as 55 D EMA (now at 0.8677) holds, in case of recovery.

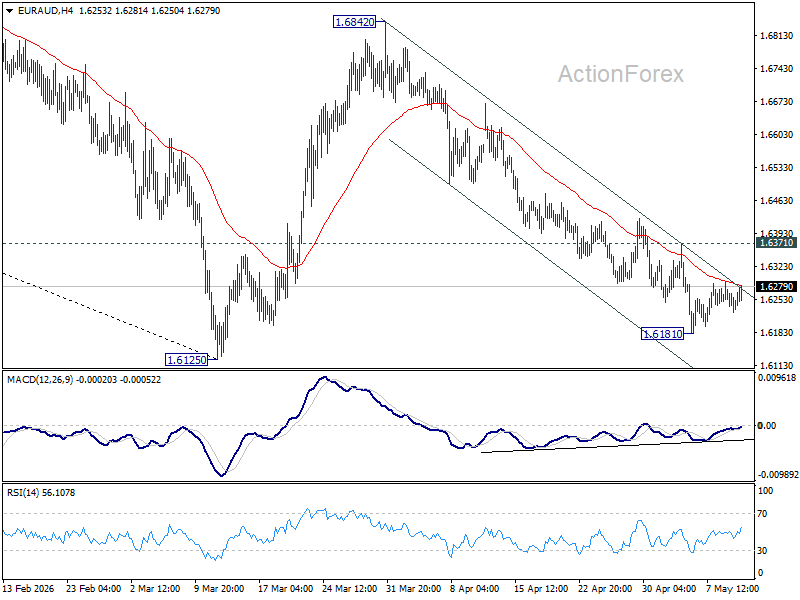

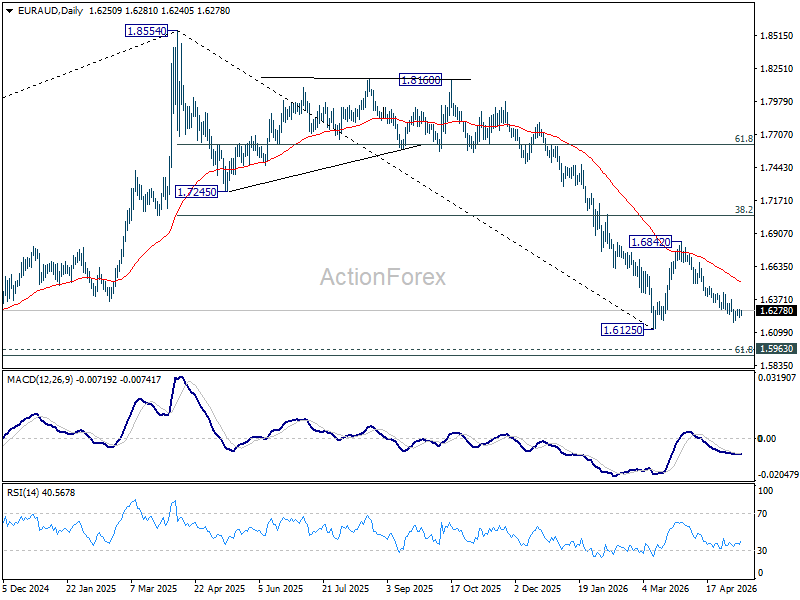

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6220; (P) 1.6254; (R1) 1.6280; More...

Intraday bias in EUR/AUD stays neutral at this point. On the downside, decisive break of 1.6125 will resume larger fall from 1.8554. Nevertheless, break of 1.6371 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound to 55 D EMA (now at 1.6507).

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7039) holds, even in case of strong rebound.

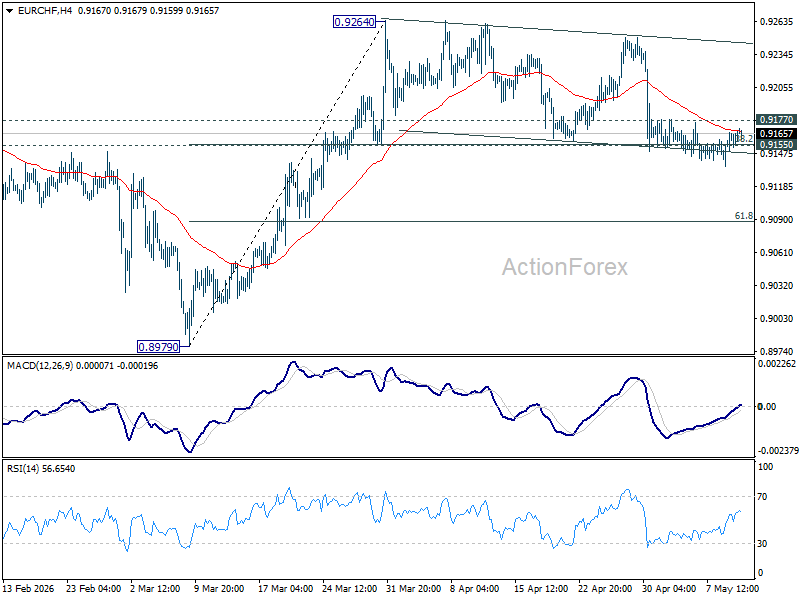

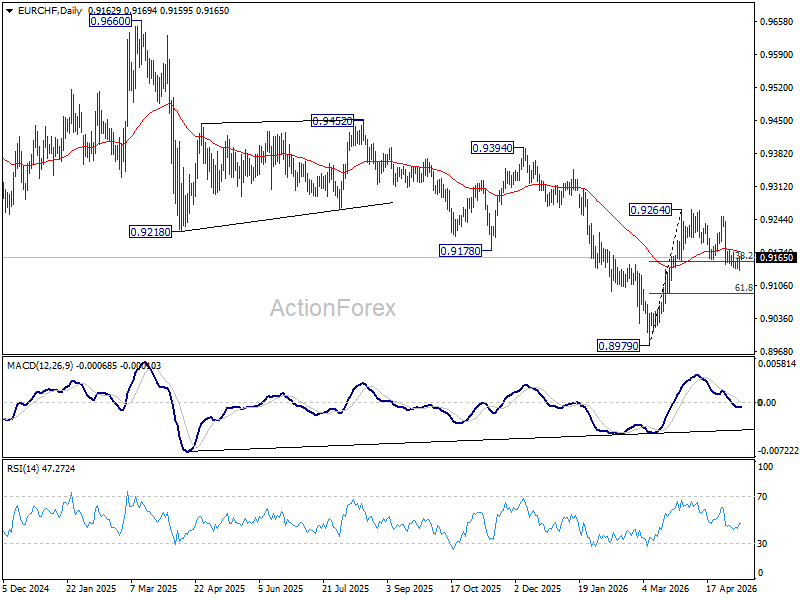

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9138; (P) 0.9152; (R1) 0.9178; More....

Intraday bias in EUR/CHF stays neutral for the moment. On the upside, break of 0.9177 minor resistance will turn bias back to the upside for 0.9264 resistance. However, sustained trading below 0.9155 cluster support (38.2% retracement of 0.8979 to 0.9264 at 0.9155) will turn bias back to the downside for deeper pullback to 61.8% retracement at 0.9088 and possibly below.

In the bigger picture, considering bullish convergence condition in W MACD, a medium term bottom should be in place at 0.8979. Sustained trading above 55 W EMA (now at 0.9241) will add more credence to this case. Further break of 0.9394 resistance will pave the way to 0.9660 resistance next. However rejection by the 55 W EMA will set up another fall through 0.8979 low at a later stage.

Valuation Vertigo

Major US and European indices resisted well yesterday despite a sharp rise in oil prices after US/Iran peace hopes fell off a cliff. Regardless, the S&P500 and Nasdaq100 printed fresh record highs, while even the industrial-heavy Dow Jones eked out a small gain. Most gains came from tech names, however, with VanEck’s Semiconductor ETF surging another 1.72% to — of course — another record high, while European indices were less enthusiastic, as rising yields in reaction to higher oil prices somehow tamed enthusiasm.

This morning, US crude is consolidating within the $98–100pb range, and futures are in the red.

Now, I’ve trained myself to look at the market through different — and rosier — lenses. Because let’s admit it: stock prices have risen through financial crises, pandemics, wars, energy crises and more. Measures like liquidity injections, QE, lower rates and fiscal spending help, while new tools and technologies increase productivity, new businesses emerge, and the world moves on. But what we see today is that downside corrections are disappearing, leaving no room for the market to readjust. Today, markets rally on good news, and on bad news — on hopes that things will get better tomorrow. And that’s leading to a parabolic rise in some sectors. As much as I love technology and the stocks involved, a chart like the Kospi raises a few questions.

In fact, I collected a few charts and opinions regarding what’s causing the market rally to extend despite the deluge of unfavourable geopolitical headlines and rising energy prices — considering that energy is the building block of every sector out there, from food to tech.

The main explanation being pointed to is strong earnings. According to FactSet, among the 89% of S&P 500 companies that have reported results so far, 84% posted a positive EPS surprise and 80% reported a positive revenue surprise. And earnings expectations were not soft heading into the earnings season. On the contrary, the S&P500 earnings growth was expected to come in around 13.1%–13.2% YoY. Now that we’re entering the final stretch of the season, the verdict is that S&P 500 earnings growth is tracking near 27.7%. If 27.7% is confirmed as the final growth rate for the quarter, it would mark the S&P500’s strongest earnings growth since Q4 2021, when earnings rose 32.0%, according to FactSet. In other words, S&P 500 earnings growth came in at roughly twice the level analysts had expected.

How come? Stronger-than-expected AI-driven growth, resilient demand and surging energy profits led companies to massively outperform expectations. Fine. That also explains why the equity rally has narrowed to a handful of tech and energy stocks. In fact, if you strip tech out of the equation, the implied earnings growth for the rest of the S&P500 was likely in the mid-single digits, roughly around 5–7%.

Tech optimism also pushed chip-heavy Asian indices higher, with the Taiex and Kospi standing out.

But if we broaden the scope beyond the US and tech, and despite rising oil prices and a strong US dollar, EM stocks also extended gains to record highs.

Why? Investors rotated away from expensive US equities into cheaper international and EM valuations, and despite the strong US dollar, global liquidity remained abundant because AI-driven capex and commodity revenues likely continued recycling into financial markets. Copper — a barometer for global economic health — has risen 24% since the end of March!

But something doesn’t add up. First, higher energy prices and a stronger dollar are fundamentally harmful for EM markets, and those that are not tech-heavy will at some point face the reality of energy scarcity.

And it’s not only EM. If the Middle East war doesn’t end quickly, the world — including the G7 economies that have relied on their ample oil reserves — will start facing scarcity. If there’s no resolution to the Middle East conflict and the Strait of Hormuz remains closed, global oil inventories could reach operational stress levels by June. If there’s still no resolution by September, inventories could fall toward operational floor levels — the minimum required to keep pipelines functioning and refineries operating. That risk appears underpriced — if not mostly ignored — overshadowed by the strength of earnings.

But even there, in an X post, Mike Zaccardi highlighted that this year’s global equity rally is almost entirely driven by higher EPS estimates. And that is especially striking for MSCI EM stocks.

And last but not least, Michael Burry — arguably the most famous bear of modern times, whose hedge fund has recently been washed away by the strength of the bullish tide — insists that today’s tech rally resembles the peak of the dot-com bubble. He highlighted that the Nasdaq 100 is trading at around 43 times earnings, above its implied level of 30, because he argues that “Wall Street may be overstating by more than 50% the earnings at our fastest-growing, most highly valued companies”, he said. The same companies that largely helped the S&P500 print that 27.7% earnings growth, versus the 5–7% growth seen outside tech.

But you know what they say “the market can remain irrational longer than you can remain solvent.”

Anyway, today, the US inflation report will be in focus, with inflation expected to have risen due to the Iran-led jump in energy prices. A higher-than-expected reading could revive hawkish Federal Reserve (Fed) expectations, push yields higher and weigh on equity valuations, while a softer-than-expected print would offer relief that energy-led inflation is being contained. In all cases, the US is trying to put several measures together to ease price pressures — including a proposed gas tax holiday and a suspension of tariff-rate quotas on beef imports. But rising energy prices could easily offset those efforts, alongside mounting pressure from Chinese goods prices, which had so far helped keep Western inflation in check. Today, even that pillar may be starting to crack.

US April CPI Set to Test Iran-Related Inflation Worries

In focus today

- In the US, the most important data release of the week will be the April CPI this afternoon. We forecast headline inflation at 0.6% m/m SA (3.7% y/y) and core inflation at 0.3% m/m SA (2.6% y/y), with the latter below consensus. Markets are naturally looking for signs of underlying inflation accelerating due to the war in Iran.

- In the euro area, the German ZEW index is due today, providing financial analysts' view of the current economic situation and expectations for May.

Economic and market news

What happened overnight

In the Middle East conflict, President Trump warned the ceasefire with Iran is "on life support" after Tehran's counterproposal. Brent crude is trading around USD105/bbl this morning, extending gains from yesterday's session. Trump is reportedly meeting his national security team to consider next steps, including a possible resumption of military action and a renewed naval mission in the Strait of Hormuz. The conflict is also likely to be on the agenda when he meets President Xi Jinping this week.

In Japan, the Bank of Japan's April summary showed a clear hawkish tilt, with some policymakers arguing for raising rates soon and one flagging a possible move at the 15-16 June meeting. Three of nine members backed a hike in April, and the Iran-related oil shock, upgraded inflation outlook and second-round effects were central to the debate, pushing 10-year Japanese government bond yields to a 29-year high this morning. We continue to expect a June rate hike, although developments in the Middle East will be important.

Japan and the US reaffirmed close coordination on exchange rates and FX intervention, Finance Minister Katayama said on Tuesday after a meeting in Tokyo with US counterpart Scott Bessent. Katayama said Japan is acting in line with last September's joint statement allowing FX intervention against excessive volatility, reinforcing expectations that recent large yen-buying operations have tacit US backing.

What happened yesterday

In Norway, core inflation rose to 3.2% y/y in April, as expected and in line with Norges Bank's March MPR. Headline inflation eased to 3.4% y/y (prior: 3.6%). The details show a stronger-than-expected rebound in food prices, while lower service inflation excluding rent surprised to the downside, driven mainly by transport services and hotels/restaurants. There are still no signs of second-round effects from higher energy prices, and higher imported inflation is entirely driven by food, while inflation on other imported goods edged lower.

In Denmark, headline inflation increased as expected to 1.4% y/y in April from 1.2% y/y in March. Electricity prices hit a 25-year low, offsetting higher fuel prices. Food prices rose 0.8% m/m after several months of decline, and signals on the food price outlook remain mixed. A key uncertainty is whether a new government will implement the proposed fee cuts on chocolate and coffee, which could lower food prices by 2%. Core inflation edged down to 1.6%, and seasonally adjusted m/m momentum remains weak.

Equities: Global equities ended 0.2% higher following a solid rally during the US hours. S&P500 rose 0.2% with Nasdaq up 0.1% and Russell2000 0.3% higher. The performance was centred around specific names and sectors, with only 43% of the names in the S&P500 ending higher. Energy was the top performer driven by higher oil prices, amid hostile Trump comments, yet it was the tech and specifically the semi-conductor names that secured the overall performance of the index. US futures are modestly lower and Asian equities are mixed.

FI and FX: Yields rose across tenors and regions during yesterday's session as negotiations between Iran and US took a setback. President Trump warned the ceasefire with Iran is "on life support" after Tehran's counterproposal. Brent crude is trading around USD105/bbl this morning, extending gains from yesterday's session. EUR/USD continues to trade just below 1.18 despite the renewed uptick in oil prices. The rebound in oil prices coupled with softer details in the Norwegian inflation print caused the NOK to perform among G10 peers. Today's US April CPI release is a key data point, and we forecast headline inflation close to consensus at 3.7% y/y but expect to see core inflation below consensus at 2.6% y/y, which could lift EUR/USD above 1.18 even amid the geopolitical concerns. If the print undershoots expectations it could act as a trigger for intervention in the USD/JPY cross which has gradually drifted above 157.5 and in such a scenario we expect the cross to drop to 156.0.

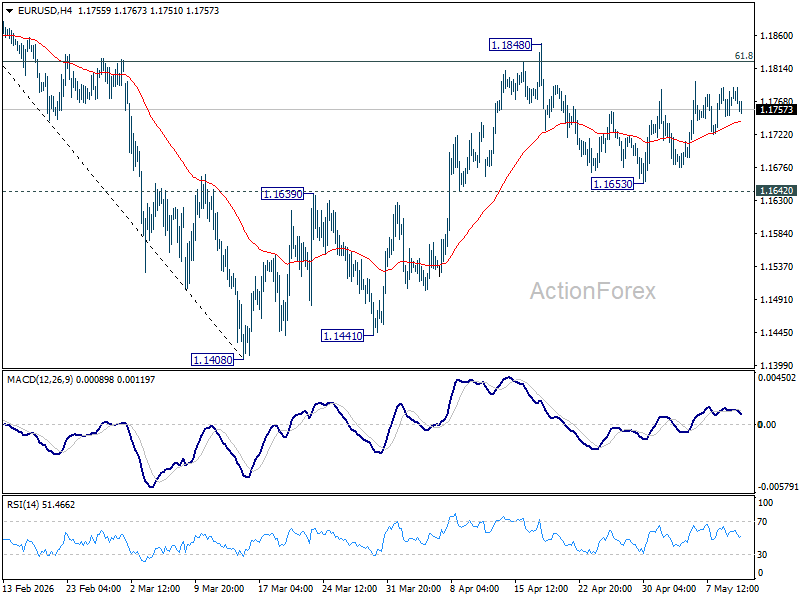

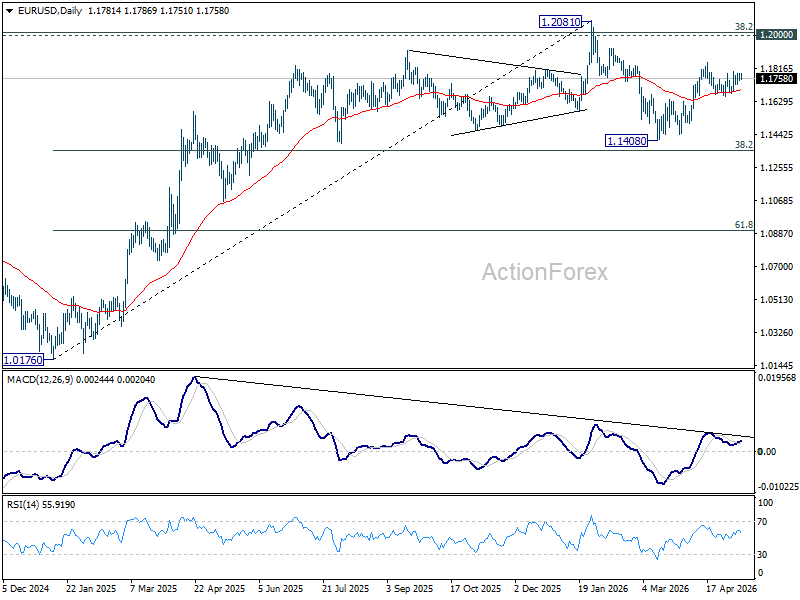

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1752; (P) 1.1769; (R1) 1.1799; More….

Intraday bias in EUR/USD remains neutral and outlook is unchanged. Further rise is expected with 1.1642 support intact. On the upside, firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1539). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

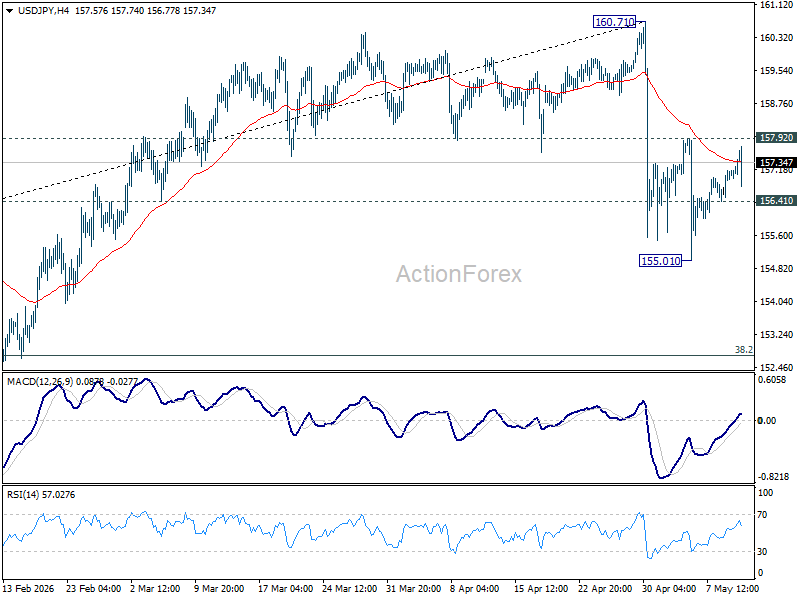

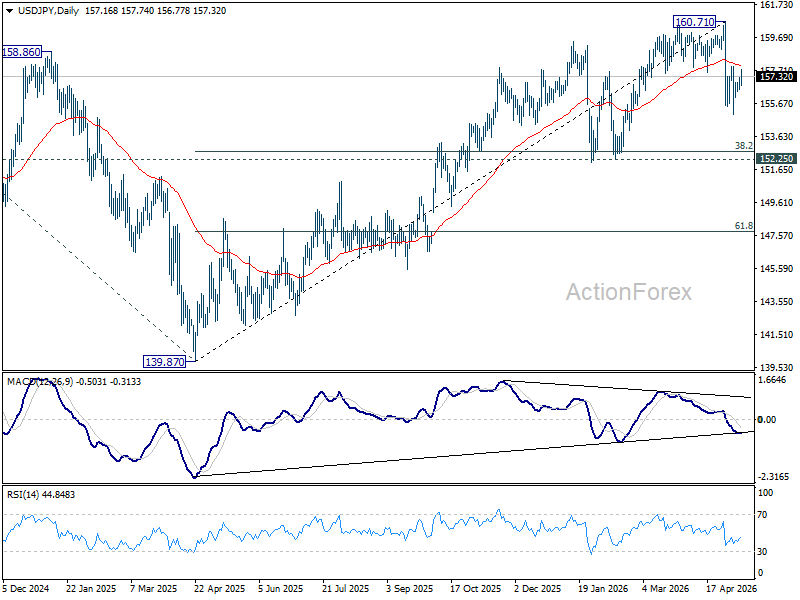

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.63; (P) 156.94; (R1) 157.46; More...

Intraday bias in USD/JPY stays neutral for the moment. On the downside, below 156.41 minor support will bring retest of 155.01. Firm break there will resume the fall from 160.71 to 152.25 support next. On the upside, however, firm break of 157.92 will indicate that pullback from 160.71 has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.13) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

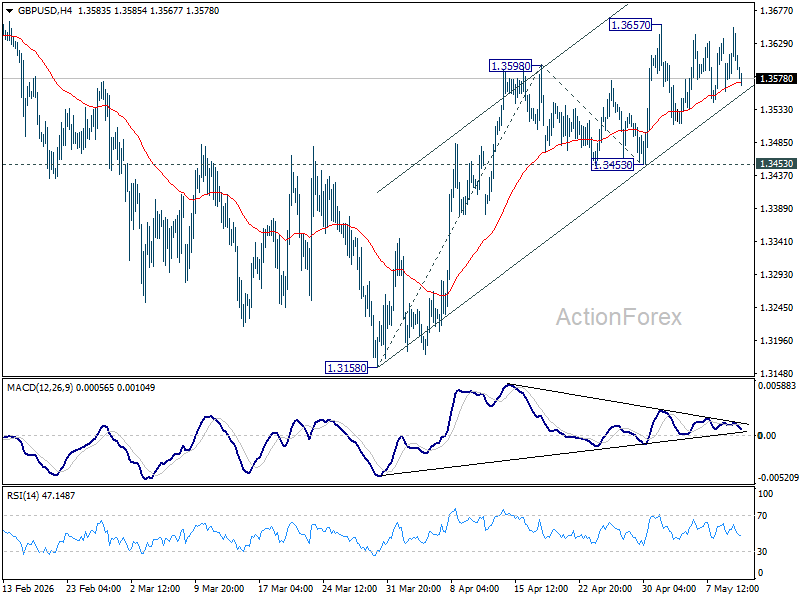

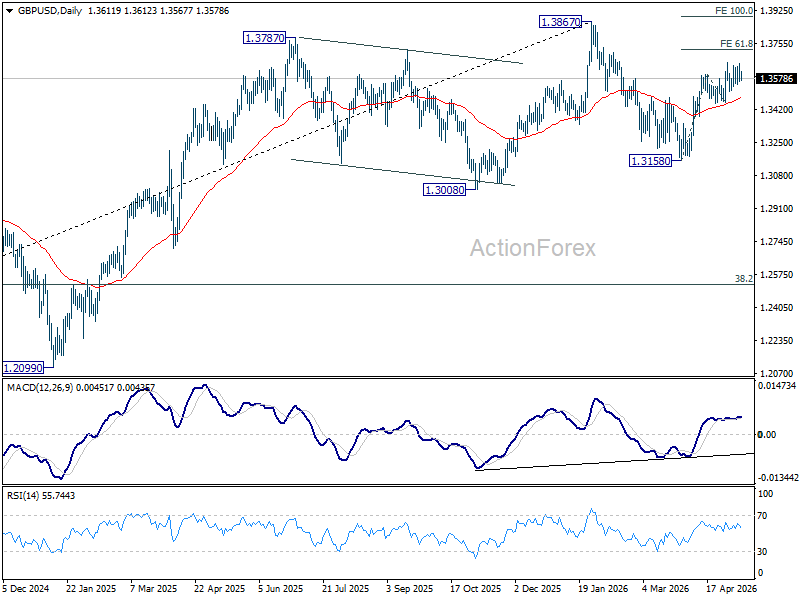

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3555; (P) 1.3603; (R1) 1.3656; More...

Intraday bias in GBP/USD remains neutral and more consolidations could be seen. With 1.3453 support intact, further rise is expected. On the upside, break of 1.3657 will target 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).

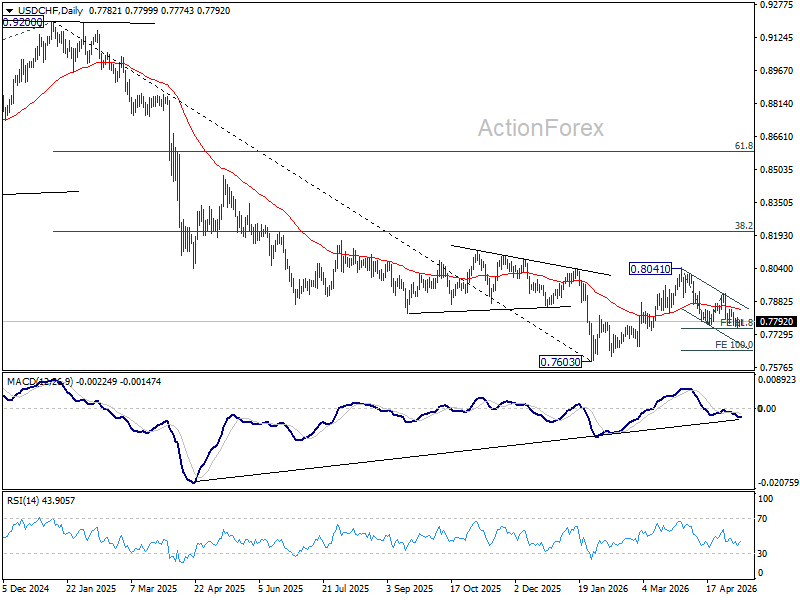

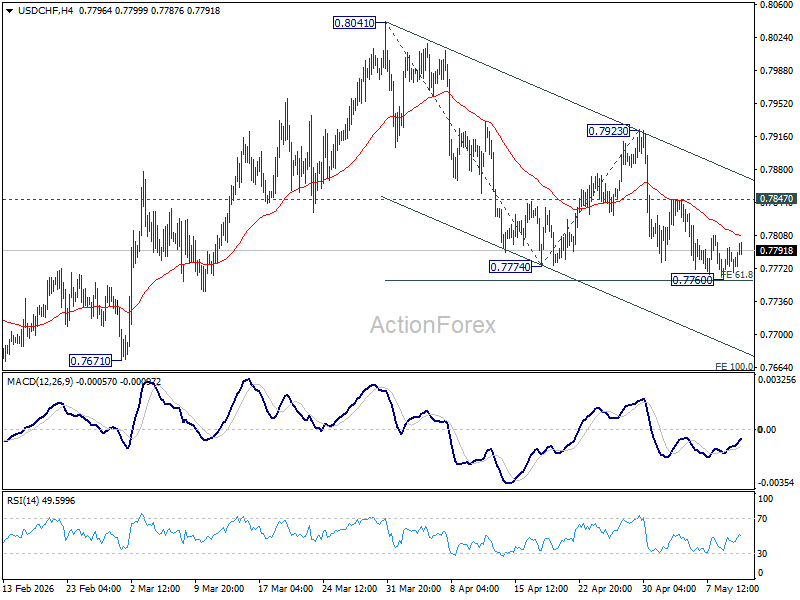

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7759; (P) 0.7776; (R1) 0.7791; More….

Intraday bias in USD/CHF remains neutral and some more consolidations could be seen. Further fall is expected with 0.7847 resistance intact. On the downside, decisive break of 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758 will resume the whole decline form 0.8041, and target 100% projection at 0.7656. However, firm break of 0.7847 resistance will indicate short term bottoming, and bring stronger rebound back to 0.7923 resistance.

In the bigger picture, as long as 55 W EMA (now at 0.8051) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.