Sample Category Title

WTI Crude Oil Signals Breakout, Momentum Points To Fresh Rally

Key Highlights

- WTI Crude Oil started a fresh increase above $98.00 and $100.00.

- It cleared a key bearish trend line with resistance at $99.20 on the 4-hour chart of XTI/USD.

- Gold is struggling to settle above the $4,760 and $4,780 resistance levels.

- EUR/USD failed to gain pace for a move above 1.1800.

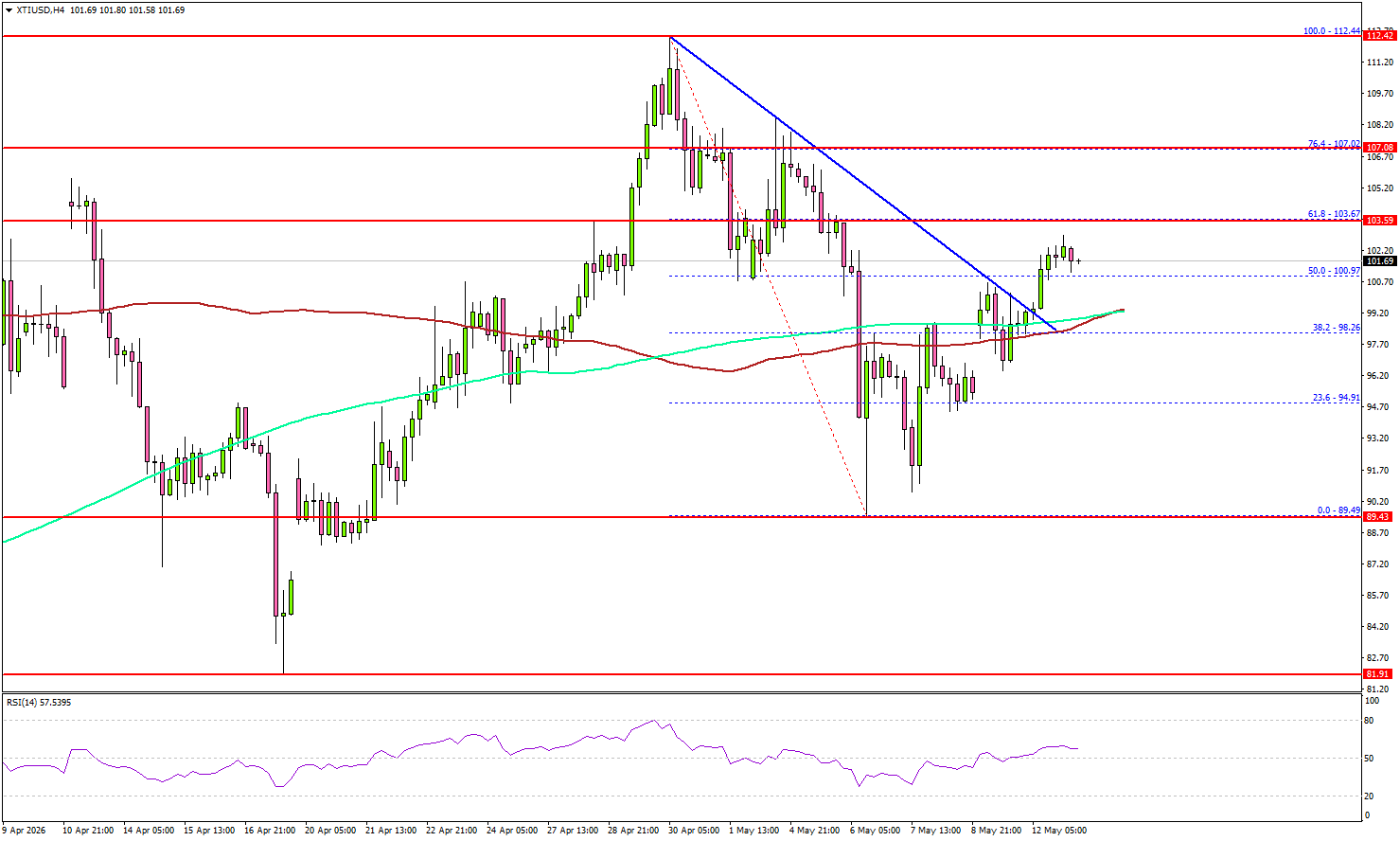

WTI Crude Oil Price Technical Analysis

WTI Crude Oil prices found support near $90.00 against the US Dollar. The price started a steady upward move above the $95.00 and $96.50 levels.

Looking at the 4-hour chart of XTI/USD, the price settled above $98, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The price cleared the 50% Fib retracement level of the downward move from the $112.44 swing high to the $89.49 low.

Besides, it cleared a key bearish trend line with resistance at $99.20. On the upside, immediate resistance is near the $103.65 level. The first key hurdle for the bulls could be $107.00 and the 76.4% Fib retracement level of the downward move from the $112.44 swing high to the $89.49 low.

A close above $107.00 might send Oil prices toward $112.00. Any more gains might call for a test of $115.00 in the near term. On the downside, the first major support sits near the $98.50 zone and the 100 simple moving average (red, 4-hour).

The next support could be $96.20, below which the price could dive and test $92.00. A daily close below $92.00 could open the doors for a larger decline. In the stated case, the bears might aim for a drop toward $88.00.

Looking at Gold, the bears are still active below the key resistance at $4,800. The main support sits at $4,600.

Economic Releases to Watch Today

- US Producer Price Index for April 2026 (MoM) – Forecast +0.5%, versus +0.5% previous.

- US Producer Price Index for April 2026 (YoY) – Forecast +4.9%, versus +4.0% previous.

OECD Sees BoJ Raising Rates to 2% by End-2027

The OECD projected on Wednesday that the Bank of Japan will continue steadily normalizing monetary policy, with the short-term policy rate expected to rise from the current 0.75% to 2% by the end of 2027.

In its latest Economic Survey of Japan, the OECD argued that resilient domestic demand, sustained wage growth, and improving inflation dynamics should allow the Japanese economy to absorb external shocks from the Middle East conflict. "Growth is projected to remain above potential in 2026-27."

The report highlighted what it described as “significant developments towards a positive wage-price cycle,” pointing to rising corporate profits, stronger pricing power among firms, and improving inflation expectations. According to the OECD, labor shortages and changing price dynamics are supporting robust nominal wage growth and private investment, helping Japan’s economy remain resilient despite geopolitical volatility and higher energy costs.

The OECD said "policy interest rate should continue to be increased gradually to avoid overshooting" the 2% target, particularly as the output gap closes and wage growth shows signs of becoming more sustainable. The report argued that the current policy rate remains "near the bottom end of the range of the nominal neutral rate."

The OECD expects inflation to "converge towards the 2% target" during 2026-27, reinforcing the case for continued policy normalization and further reduction of the BOJ’s balance sheet over time.

Fed’s Goolsbee: Inflation Is Moving the Wrong Way, Labor Market Is Not

Chicago Fed President Austan Goolsbee warned overnight that US inflation is moving in the “wrong way,” expressing particular concern that price pressures are spreading beyond energy and tariffs into broader service categories. His remarks followed April’s firmer-than-expected CPI report, which showed both headline (3.8%) and core (2.8%) inflation accelerating as rising oil prices increasingly fed through the economy.

Goolsbee said the “unexpectedly disappointing” part of the report was the strength in services inflation, arguing that this category cannot simply be explained away by higher oil prices. “That’s the part that I’m nervous about,” he said, adding that he wants to see services inflation “at least stop growing and hopefully start going back down.”

Goolsbee also emphasized that the labor market remains broadly stable, meaning the Fed is currently not facing a difficult trade-off between inflation and employment. “One side of the mandate is going wrong and the other side is not going,” he added, "So in the short run, I want us to be cognizant of that."

Gold (XAU/USD) Rises Slow and Steady: In-Depth Technical Analysis

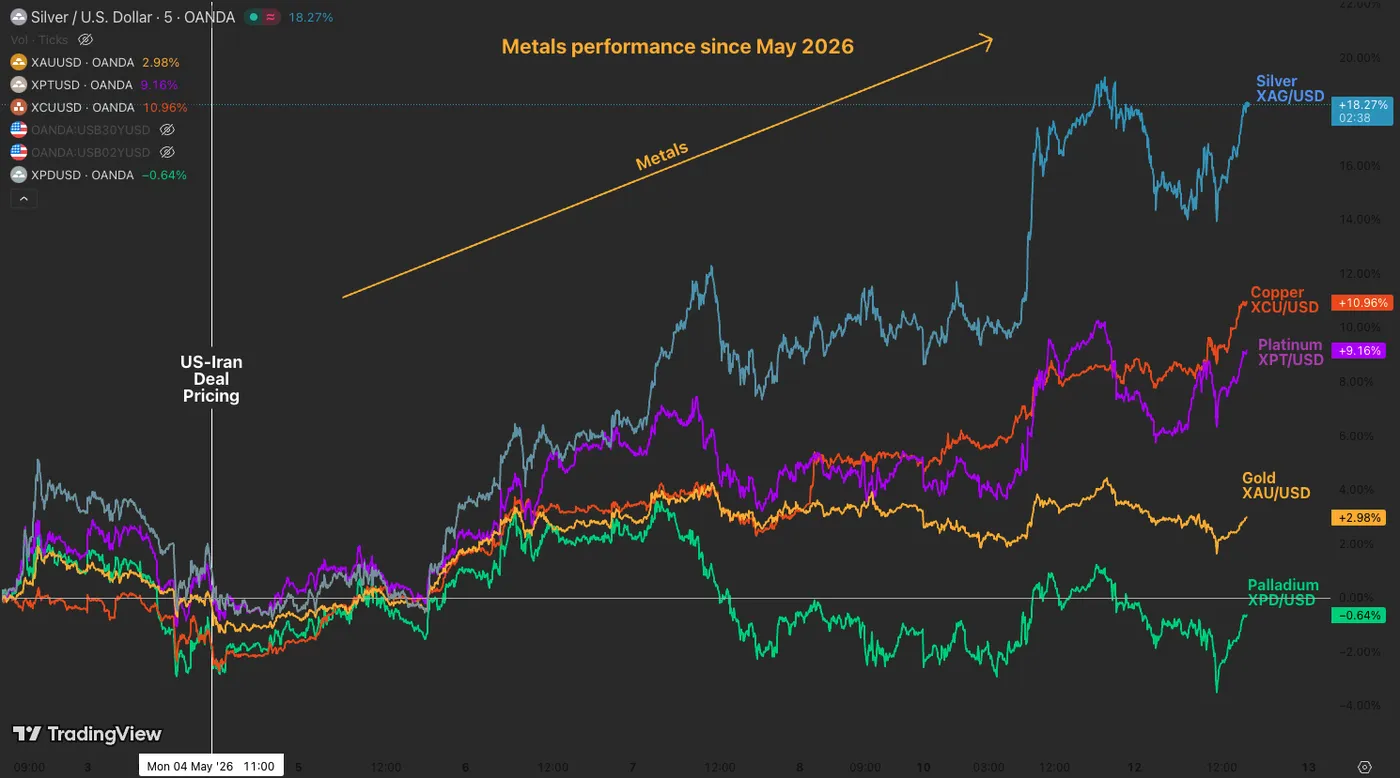

After yesterday's sharp rally in alternative precious metals, with Copper, Platinum, and Silver all surging as Chinese inflation reached a 45-month high, the strong upward momentum has now eased.

However, precious commodities traders were caught off guard by this morning's higher-than-expected US inflation report.

As the US Dollar surged in response to the hawkish CPI data, traditional risk assets and alternative metals pulled back.

Still, the metals complex is holding strong relative to the tech-heavy Nasdaq and the broader cryptocurrency market, which are seeing much sharper declines today.

Metals performance since the beginning of May 2026. Source: TradingView, May 12, 2026.

Broad financial markets are now essentially frozen in a state of suspended animation following the CPI release. Participants' eyes are firmly turning toward the monumental Trump-Xi diplomatic summit scheduled over the next three days.

This high-stakes meeting between the world's two largest economic superpowers is virtually guaranteed to rock global investor appetite and set the directional tone for the remainder of the quarter. Metals will not be isolated from such dynamics.

Despite the current economic and geopolitical uncertainty, Gold has stayed relatively quiet. The metal is consolidating within its wide $4,500 to $4,900 range.

By holding steady and absorbing market volatility, Gold is building a solid technical foundation for a possible longer-term rally.

Importantly, Gold has stayed resilient even with recent hawkish data and the fast-paced rise in crude oil prices. This ongoing relative strength suggests that the fundamental outlook for this safe-haven asset may be changing in the near future.

Traders should expect massive, headline-driven volatility in the very near term across markets and the yellow metal. The ultimate question is which direction this historic consolidation will finally break.

Let's dive right into a multi-timeframe analysis of Gold (XAU/USD) to look at where the action could head for the rest of the week, if not weeks.

Gold (XAU/USD) Multi-Timeframe Technical Analysis

Weekly Chart

Gold weekly chart, May 12, 2026. Source: TradingView.

Gold has been forming the basis for decent support between $4,500 and $4,900, helping the previously bearish momentum turn neutral.

Having failed to push for further downside, bulls are slowly regaining the advantage, with the weekly RSI slowly turning bullish since the beginning of the month.

This week's candle, still forming, is for now looking like a bullish hammer.

4H Chart and Technical Levels

Gold 4H chart, May 12, 2026. Source: TradingView.

After a bearish reaction to the morning US inflation numbers, some mean reversion buying is pushing Gold back above the previous candle, forming a bullish engulfing pattern.

Buyers will want to pursue this bullish momentum to push above the $4,780 weekly highs.

Levels to watch for Gold (XAU/USD) trading:

Resistance Levels:

- Intraday highs: $4,780

- $4,850 to $4,900 key resistance, range highs

- $5,100 pivotal resistance

- Gold all-time high record: $5,602

Support Levels:

- Daily momentum pivot: $4,650 to $4,700

- December 2025 support: $4,500 to $4,550, range lows

- Major support: $4,350 to $4,400

- War lows: $4,101

1H Chart

Gold 1H chart, May 12, 2026. Source: TradingView.

The yellow metal is extending higher towards the end of the session, back above the $4,700 level and the 50-hour MA.

Bulls will need to expand their strength above the intraday level to extend further. Below $4,650, the 200-hour MA, the action may get more bearish towards the bottom of the range.

Safe trades.

Elliott Wave Analysis: Nasdaq Futures (NQ_F) Cycle Ending, Correction Ahead

Short‑term Elliott Wave analysis indicates that the cycle in Nasdaq Futures (NQ) from the March 31, 2026 low is approaching completion as a five‑wave impulse. From that low, wave ((i)) concluded at 24,348.25, followed by a corrective pullback in wave ((ii)) that ended at 23,666. The Index then advanced in wave ((iii)) toward 27,136, while the subsequent dip in wave ((iv)) found support at 26,681.75, as reflected in the one‑hour chart. The final leg, wave ((v)), is now unfolding with internal subdivisions forming another impulse of lesser degree.

From wave ((iv)), wave (i) finished at 27,542.5, and the pullback in wave (ii) ended at 27,009.5. The rally continued with wave (iii) reaching 29,480, before wave (iv) corrected to 28,742. The Index is now progressing in wave (v), which should complete wave ((v)) of 1. This development will also mark the conclusion of the cycle that began on March 31, 2026. Once wave 1 is complete, a corrective phase in wave 2 is expected. That correction should unfold in a larger degree, either as a three‑swing or seven‑swing structure, before the broader trend resumes higher.

In the near term, as long as price remains above 27,012.79, the Index retains scope for one more push upward. However, the cycle has matured considerably, and the risk of chasing the upside has increased. Traders should recognize that while limited extension remains possible, the probability of a corrective pullback is rising. The structure suggests caution, as the market is transitioning from an impulsive phase into a corrective environment.

Nasdaq Futures (NQ_F) 60-Minute Elliott Wave Chart

NQ_F Elliott Wave Video:

https://www.youtube.com/watch?v=fpO8Hih-H68

Eco Data 5/13/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Apr | 5.40% | 4.60% | 4.80% | |

| 23:50 | JPY | Current Account (JPY) Mar | 3.90T | 2.93T | 2.71T | 2.70T |

| 01:30 | AUD | Wage Price Index Q/Q Q1 | 0.80% | 0.80% | 0.80% | |

| 03:00 | NZD | RBNZ Inflation Expectations Q2 | 2.53% | 2.37% | ||

| 05:00 | JPY | Eco Watchers Survey: Current Apr | 40.8 | 41.6 | 42.2 | |

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.10% | 0.10% | 0.10% | |

| 09:00 | EUR | Eurozone Industrial Production M/M Mar | 0.20% | 0.30% | 0.40% | 0.20% |

| 12:30 | USD | PPI M/M Apr | 1.40% | 0.50% | 0.50% | 0.70% |

| 12:30 | USD | PPI Y/Y Apr | 6.00% | 4.90% | 4.00% | 4.30% |

| 12:30 | USD | PPI Core M/M Apr | 1.00% | 0.30% | 0.10% | 0.20% |

| 12:30 | USD | PPI Core Y/Y Apr | 5.20% | 4.30% | 3.80% | 4.00% |

| 14:30 | USD | Crude Oil Inventories (May 8) | -2.0M | -2.3M |

| 23:50 | JPY |

| Bank Lending Y/Y Apr | |

| Actual | 5.40% |

| Consensus | 4.60% |

| Previous | 4.80% |

| 23:50 | JPY |

| Current Account (JPY) Mar | |

| Actual | 3.90T |

| Consensus | 2.93T |

| Previous | 2.71T |

| Revised | 2.70T |

| 01:30 | AUD |

| Wage Price Index Q/Q Q1 | |

| Actual | 0.80% |

| Consensus | 0.80% |

| Previous | 0.80% |

| 03:00 | NZD |

| RBNZ Inflation Expectations Q2 | |

| Actual | 2.53% |

| Consensus | |

| Previous | 2.37% |

| 05:00 | JPY |

| Eco Watchers Survey: Current Apr | |

| Actual | 40.8 |

| Consensus | 41.6 |

| Previous | 42.2 |

| 09:00 | EUR |

| Eurozone GDP Q/Q Q1 P | |

| Actual | 0.10% |

| Consensus | 0.10% |

| Previous | 0.10% |

| 09:00 | EUR |

| Eurozone Industrial Production M/M Mar | |

| Actual | 0.20% |

| Consensus | 0.30% |

| Previous | 0.40% |

| Revised | 0.20% |

| 12:30 | USD |

| PPI M/M Apr | |

| Actual | 1.40% |

| Consensus | 0.50% |

| Previous | 0.50% |

| Revised | 0.70% |

| 12:30 | USD |

| PPI Y/Y Apr | |

| Actual | 6.00% |

| Consensus | 4.90% |

| Previous | 4.00% |

| Revised | 4.30% |

| 12:30 | USD |

| PPI Core M/M Apr | |

| Actual | 1.00% |

| Consensus | 0.30% |

| Previous | 0.10% |

| Revised | 0.20% |

| 12:30 | USD |

| PPI Core Y/Y Apr | |

| Actual | 5.20% |

| Consensus | 4.30% |

| Previous | 3.80% |

| Revised | 4.00% |

| 14:30 | USD |

| Crude Oil Inventories (May 8) | |

| Actual | |

| Consensus | -2.0M |

| Previous | -2.3M |

US Dollar Rallies Back After CPI: Is the Correction Over? EUR/USD, GBP/USD and Dollar Index Overview

The US Dollar saw a sharp correction after the fragile ceasefire began, but that downward trend has now completely stopped.

With the peace narrative having stalled, it is clear that the FX market is taking a more realistic view of the US-Iran diplomatic talks than stock markets, which remain optimistic despite little real progress.

Foreign exchange markets are focusing on energy prices instead of tech sector excitement, and are adjusting for geopolitical risks.

The petrodollar trade: Oil and US Dollar correlation. Source: TradingView, May 12, 2026.

After gaining against the US Dollar in late March and early April, most major currencies are back to trading in a narrow range.

Today, though, they are quickly reversing as WTI crude oil moves back above $100 with the recently souring narrative.

The ongoing conflict and related economic challenges are supporting the US Dollar. Although new reports suggest Iran may dilute its highly enriched uranium to 3.7% and 20%, overall diplomatic talks have stalled, and the uncertainty continues to disrupt energy supply chains while adding to demand for the US Dollar.

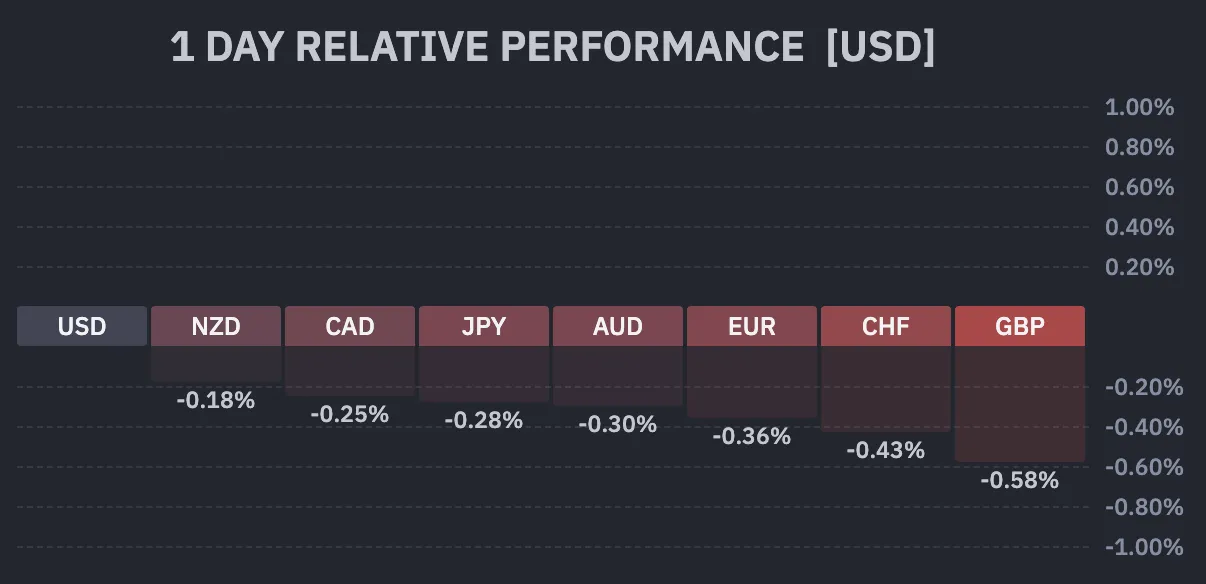

Current session's FX performance. Source: Finviz, May 12, 2026.

Along with the ongoing geopolitical uncertainty, a higher-than-expected inflation report has strengthened the US Dollar, with another inflation report due tomorrow in the form of PPI.

Today’s CPI showed headline inflation at 3.8%, compared with 3.7% expected, and core CPI at 2.8%, versus a 2.6% forecast. That was a large rise, though not too surprising considering the explosion in gas prices.

The strong inflation reading keeps suggesting that the Fed will keep rates unchanged, if not hike, putting pressure on other major currencies.

US morning data. Source: MarketPulse Economic Calendar.

We will look at the Dollar Index, EUR/USD, and GBP/USD to assess the current state of the FX market and where to look next.

Dollar Index 4H Chart

Dollar Index daily chart, May 12, 2026. Source: TradingView.

The US Dollar is breaking out of its end-March downward channel after forming a triple bottom right around the 97.50 level.

With the recent lows coinciding with the mid-zone of the larger 96.00 to 100.00 range, the consolidation could be tightening further between 98.00 and 100.00 as long as the peace process does not move forward.

Expect more US Dollar rallies if the index breaches 98.50.

Levels of interest for the Dollar Index:

Resistance Levels

- 98.50 to 98.70 war pivot

- 98.78 4H 200-period MA

- 99.40 to 99.50 resistance

- Initial war spike 99.68

- 100.00 to 100.50 main resistance zone

- War highs 100.544

Support Levels

- 98.00 2025 support, testing and bearish below

- Support 97.40 to 97.60, triple bottom

- 2025 lows 96.40 to 96.80 support

- Range lows at early 2022 consolidation just below 96.00

GBP/USD 4H Chart and Technical Levels

GBP/USD 4H chart, May 12, 2026. Source: TradingView.

GBP/USD is still trading between 1.3410 and 1.36 but is now rejecting its resistance zone, heading back to support.

Add ongoing outflows and political turmoil in the UK, with Keir Starmer's ministers resigning, and the outlook for the Pound looks bearish.

While still far, watch whether the 1.34170, 2024 top, level holds.

Levels of interest for GBP/USD:

Resistance Levels

- December resistance 1.36, range highs

- Pre-FOMC highs 1.36010

- Resistance 1.37 zone

- 2025 resistance around 1.38

Support Levels

- Key pivot 1.3410 to 1.3440

- 1.34170, 2024 top level

- Pivotal support 1.3250 to 1.33

- 1.32 war support

EUR/USD 4H Chart and Technical Levels

EUR/USD 4H chart, May 12, 2026. Source: TradingView.

EUR/USD is also rejecting its 1.18 resistance and quickly falling towards the 1.17 momentum pivot, with bearish acceleration expected as the RSI falls below neutral.

Sellers are also breaching the 4H 50-period MA, which could weigh on price action. While momentum is still lacking, traders will want to confirm the move with strong bearish candles and volume around 1.1720.

Levels to place on your EUR/USD charts:

Resistance Levels

- 1.17380 4H 50-period MA

- Resistance zone around 1.18, +/- 150 pips

- 1.1830 June 2025 highs

- 1.1850 to 1.1860 recent test

- September 2021 highs, resistance 1.19 to 1.1950 zone

Support Levels

- 1.17 to 1.1720 March pivot

- Rebound highs 1.17200, bearish below

- Major pivot 1.16250 to 1.16350

- 1.1540 to 1.1570 war support

- 1.1475 to 1.15 November support

- War lows 1.1410

Safe trades and keep a close eye on ceasefire news.

US-China – Xi-Trump Meeting Preview: We Expect No Game Changers

We do not expect the Trump-Xi meeting on May 14-15 to lead to major breakthroughs in US-China relations. We expect near-term financial market impact to remain limited.

Trump does not have the incentives nor the means to ramp up the pressure on China with focus remaining on the war in Iran and earlier court ruling still constraining his tariff weapon. For China, keeping relations on a stable track is the main priority, especially when it comes to Taiwan.

The countries could agree on China increasing purchases of US agricultural goods, an extended tariff truce and establishment of mutual trade and investment 'boards', though these should be seen as largely symbolical. Change in the wording of US policy on Taiwan would be a major victory for China.

Sunset Market Commentary

Markets

Risk premia were back in vogue from the start of trading this morning. Evidently, the stalemate in the process of reaching a solution to the US-Iran conflict, via higher oil prices (Brent currently $107.5 p/b), again tilted markets to a more risk-averse approach. However, country-specific issues obviously are also at work. UK markets were the main case in point. Since last week’s huge defeat of Keir Starmer’s Labour party in regional and local elections, (internal) pressure within his party is building for the PM to resign. However, the PM after a Cabinet meeting today reiterated he intends to continue governing at least as no formal leadership contest is being triggered along the party rules. Even so, from a market point of view, whether the UK PM stays in place and adapts policy or whether he finally quits, fiscal policy/sustainability might again be at risk if policy were to shift to a more pro-spending course. UK yields in nervous trading add 9 bps (2-y) to 12 bps (10-y). After holding ‘remarkably’ stable in a first reaction to the election outcome, sterling this time also lost ground. EUR/GBP just missed a test of the 0.87 barrier (currently 0.8675). On Japanese markets, some tensions are also lingering. Yields on Japanese government bonds add between 1 bp (2-y) and 4.8 bps (30-y). This might not look that spectacular. However at 2.56% the Japanese 10-y yield is touching levels last seen in 1997. At 3.83%, the 30-y JGB yield is also closing in on last year’s multiyear top. Higher Japanese risk premia also suggest fiscal sustainability issues. Admittedly, a good 10-y bond auction to some extent mitigated pressure. Even so, FX policy also plays on the background. US Treasury secretary Bessent and Japan Fin Min Katayama indicated to stay in close contact to address undesirable FX volatility. This suggests the US supports Japan’s FX interventions to prevent further yen weakness. However, at some point, it also might put additional pressure on the BOJ to take ‘more fundamental’ action (rate hikes) to provide yield support to the ailing currency. This remains a factor of uncertainty for Japanese yield markets too. The yen intraday briefly spiked from the 157.7 area to near 156.8, but can’t hold on to the gains (currently 157.6). In current context of higher risk/inflation premia, German bond yields add between 6 bps (2-y) and 4.5 bps (30-y). The Eurostoxx 50 cedes about 1%.

With the market focus mainly on risk premia outside the US, April US CPI inflation also deserved attention. At 0.6% M/M and 3.8% Y/Y for headline (from 3.3%) and 0.4% M/M and 2.8% (from 2.6%) for the core reading, the report was slightly higher than expected. Evidently, the rise in energy/gasoline prices were responsible for the rise in prices. However, the move was more broad-based with amongst others food prices (0.5% M/M) and broader services prices ex energy (0.5% M/M, including shelter 0.6% M/M) adding to price rises. With recent labour and other US activity data holding up well, today’s data justify the call of those FOMC members objecting the easing bias in the statement. Even so, the reaction on US yield markets 2-y +3 bps; 30-y +2 bps) remains modest. US equity indices are correcting 0.5%-0.75% lower.

News & Views

The Belgian debt agency launched a new 5-yr benchmark (OLO 108 3.1% Aug2031) via syndication. The bond was priced to yield MS + 19 bps compared to guidance in the MS +21 bps area. Books were in excess of €45bn, allowing the debt agency to print €8bn. Thanks to today’s sale, the BDA now raised €32bn in OLO funding YtD compared with a €51.6bn target (62%). The remainder is expected to be collected through regular OLO auctions given that today’s deal was this year’s third and final (according to funding plan) syndication. In January the BDA launched its traditional new 10-yr OLO benchmark (3.4% Jun2036). In February, they launched a 30-yr OLO (4.35% Jun2056).

CME Group, the world's leading derivatives marketplace, and Silicon Data, the industry leader in GPU market intelligence and benchmarking, announced they will launch a first-in-class compute futures market later this year, pending regulatory review. The new futures contracts will allow traders, financial institutions, AI builders and cloud-service providers to manage volatility and price risk associated with the multi-trillion-dollar compute market. The products will be based on Silicon Data's indices, the world's first daily GPU benchmarks for on-demand rental rates. The CEO of global trading firm DRW, which backs the initiative argues that compute will become the largest commodity in the world. "The exponential growth in spending on data centers as we move towards that reality has been hampered by the lack of a hedging vehicle. The launch of a compute futures market is an important solution to that problem that can help market participants manage price volatility and plan with greater certainty.”

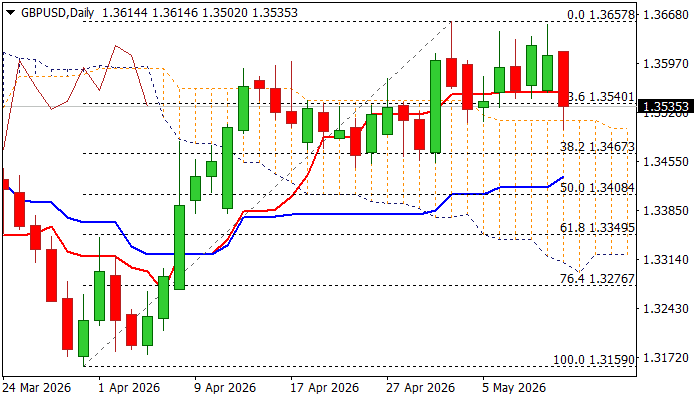

Sterling Falls on Deepening Political Crisis in UK

Cable fell around 0.8% on Tuesday on deepening political crisis, following calls from a number of lawmakers to PM Starmer to step down after his Labour Party suffered heavy losses in recent local elections.

Fresh weakness of sterling and shares, as well as rise of UK long-dated borrowing costs to the highest in three decades, came because of a change of investors’ sentiment towards potential scenario of change of leadership.

Although Starmer opposed calls to resign in today’s cabinet meeting and said he would get on governing, sterling is expected to remain under pressure on growing political uncertainty, as well as threats of deepening economic crisis, as the world starts to feel the full impact of the US – Iran war.

Technical studies on daily chart were weaker on Tuesday, but overall structure is still bullish, although dented with today’s drop.

Fresh bears faced headwinds from daily cloud top (1.3514), but the cloud is narrowing and about to twist in two weeks that could attract bears.

Penetration of cloud would generate initial bearish signal, which will look for confirmation on extension below pivotal supports at 1.3467/50 (Fibo 38.2% of 1.3159/1.3657 / late Apr higher base) break of which to signal reversal and open way for deeper drop.

Daily indicators turned south, although still holding in positive territory, with a batch on converged DMAs at 1.3480/20 zone (100 / 55 / 200) still in bullish configuration and marking significant supports.

Res: 1.3555; 1.3614; 1.3658; 1.3700

Sup: 1.3514; 1.3480; 1.3450; 1.3420