Sample Category Title

EUR/USD Revisits Support While USD/JPY Eyes Bigger Recovery Move

EUR/USD declined from 1.1800 and traded below 1.1750. USD/JPY is rising and might gain pace above 158.00 and 158.80.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- The Euro started a fresh decline after a decent move to 1.1800.

- There was a break below a key bullish trend line with support at 1.1765 on the hourly chart of EUR/USD at FXOpen.

- USD/JPY climbed higher above the 156.40 and 157.10 levels.

- There is a major bullish trend line forming with support at 157.40 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair climbed above the 1.1780 resistance zone before the bears appeared, as discussed in the previous analysis. The Euro started a fresh decline and traded below 1.1765 against the US Dollar.

There was a break below a key bullish trend line with support at 1.1765. The pair declined below 1.1750 and tested 1.1720. A low was formed near 1.1721 and the pair started a consolidation phase.

There was a minor recovery wave above 1.1740 and the 23.6% Fib retracement level of the downward move from the 1.1787 swing high to the 1.1721 low. EUR/USD is still trading below 1.1750 and the 50-hour simple moving average.

On the upside, the pair is now facing hurdles near 1.1745. The next key resistance is 1.1755 and the 50% Fib retracement. The main barrier for the bulls could be 1.1785. A clear move above 1.1785 could send the pair toward 1.1840. An upside break above 1.1840 could set the pace for another increase. In the stated case, the pair might rise toward 1.1920.

If not, the pair might resume its decline. The first major support on the EUR/USD chart is near 1.1720. The next important region for buyers sits at 1.1700. If there is a downside break below 1.1700, the pair could drop toward 1.1675. Any more losses might send the pair toward 1.1640.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a fresh upward move from 155.00. The US Dollar gained bullish momentum above 156.50 against the Japanese Yen.

It even cleared the 50-hour simple moving average and 157.00. The pair climbed above 157.50 and traded as high as 157.78. The pair is now consolidating gains above the 23.6% Fib retracement level of the upward move from the 155.03 swing low to the 157.78 high.

The current price action above 157.40 is positive. Immediate resistance on the USD/JPY chart sits at 157.80. The first key hurdle is near 158.00. If there is a close above 158.00 and the RSI moves above 65, the pair could rise toward 158.80.

The next major stop for the bulls could be 159.50, above which the pair could test 160.00 in the coming days. On the downside, the first major support is 157.40, a bullish trend line, and the 50-hour simple moving average.

The next area of interest for buyers could be 157.10. If there is a close below 157.10, the pair could decline steadily. In the stated case, the pair might drop toward the 50% Fib retracement at 156.40. Any more losses might open the doors for a drop to 155.00.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Chart Alert: Nasdaq 100 Faces Pullback Risk as Semiconductor Rally Shows Signs of Exhaustion

Key Takeaways

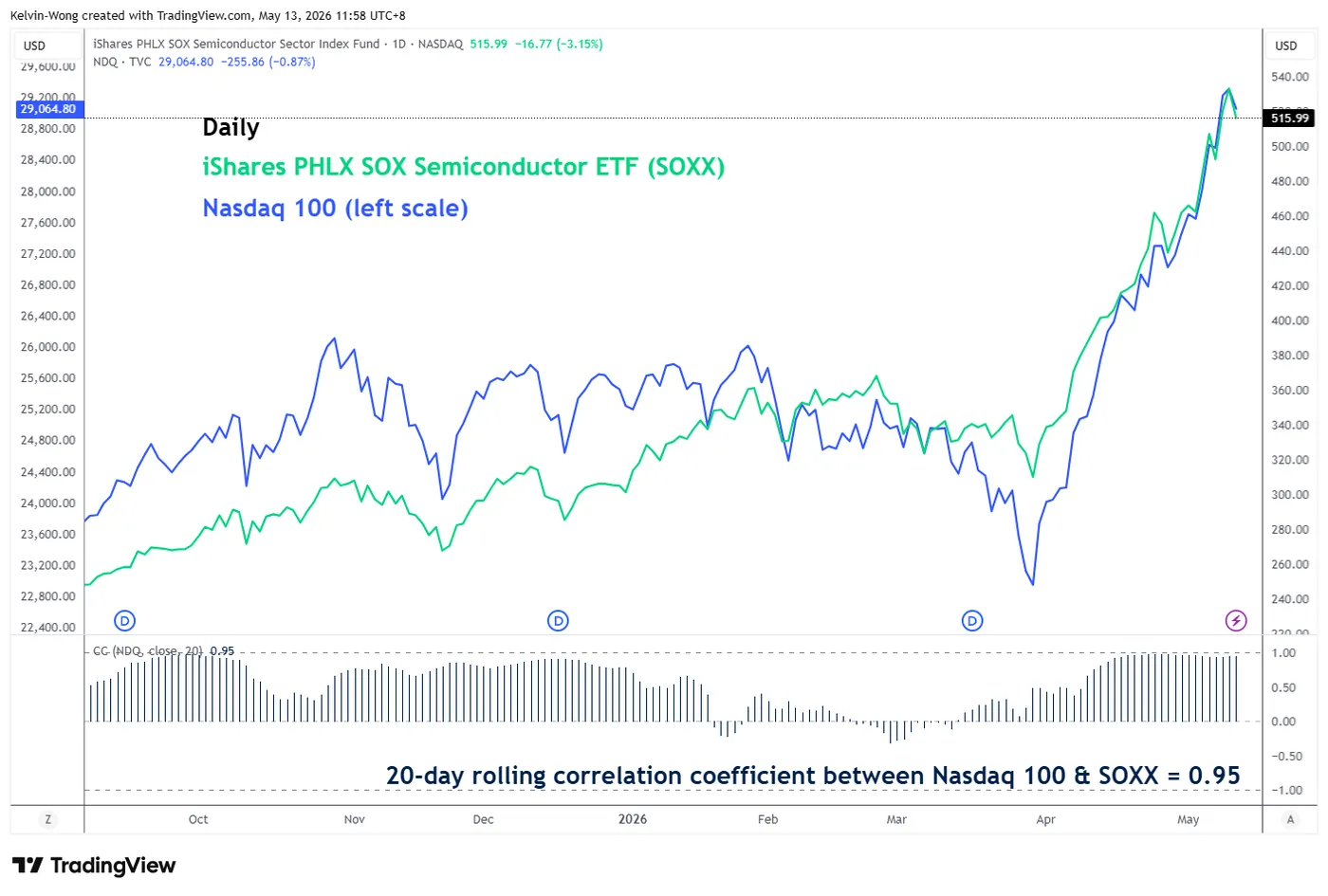

- Nasdaq 100 extended its medium-term bullish trend to a fresh record high of 29,390, supported largely by explosive gains in semiconductor and AI-related stocks such as Intel, Advanced Micro Devices, and SanDisk.

- The strong correlation between the Nasdaq 100 and the iShares Semiconductor ETF suggests that emerging exhaustion signals in semiconductor stocks could trigger a near-term corrective pullback in the broader tech-heavy index.

- Bearish technical indicators, including bearish RSI divergence, overstretched price action above the 20-day moving average, and Bollinger Band exhaustion conditions, point to rising risks of a short-term mean reversion decline below the 29,505/615 resistance zone.

The price actions of the US Nasdaq CFD index, a proxy of the Nasdaq 100 E-mini futures, have surged as expected. It rallied by 3.2% from Friday, 8 May 2026 intraday low of 28,480 to hit a fresh all-time intraday high of 29,390 on Monday, 11 May 2026 in the US session.

Its current medium-term uptrend phase has been in place since the 30 March 2026 low, and a significant contribution of the gains has come from US semiconductor and AI-hardware-related stocks, such as SanDisk, up 151%, Intel, up 150%, and Advanced Micro Devices, up 105%, in the past three months.

US Semiconductors Are Showing Signs of Medium-Term Bullish Exhaustion

Fig. 1: Correlation of iShares PHLX SOX Semiconductor ETF, SOXX, with Nasdaq 100 as of 12 May 2026. Source: TradingView.

Fig. 2: iShares PHLX SOX Semiconductor ETF, SOXX, medium-term trend as of 12 May 2026. Source: TradingView.

The price movement of the Nasdaq 100 and the iShares Philadelphia, PHLX, Semiconductor Sector exchange-traded fund, SOXX, has moved in almost perfect direct lockstep.

The 20-day rolling coefficient between the Nasdaq 100 and SOXX stands at 0.95, which indicates that future movements of US semiconductor stocks, using SOXX as a bellwether, are likely to have a significant influence and impact on the Nasdaq 100.

The prior 6-week consecutive rally of the SOXX has reached an overstretched volatility condition, as seen in the daily Bollinger Bands indicator.

The daily price action of SOXX had a daily close above the upper Bollinger Band, two standard deviations away from the 20-day moving average, on Monday, 11 May 2026, coupled with a bearish divergence condition seen on the daily RSI momentum indicator at its overbought zone.

These observations suggest the bullish impulsive up move of SOXX since the 30 March 2026 low has reached a potential bullish exhaustion condition, where the next movement may be a multi-day corrective decline sequence, in turn triggering a negative feedback loop into the Nasdaq 100.

Let’s now uncover the short-term, 1- to 3-day, trajectory of the Nasdaq 100 from a technical analysis perspective.

Nasdaq 100: At Risk of Minor Mean Reversion Decline Below 29,505/615

Fig. 3: US Nasdaq 100 CFD index minor trend as of 13 May 2026. Source: TradingView.

Trend bias: Minor corrective decline below 29,505/615 key short-term pivotal resistance within medium-term uptrend.

Supports: 28,660, 28,460/280, and 27,850, close to the 20-day moving average.

Next resistances: 29,893/953 and 30,410/417, Fibonacci extension clusters.

Key Elements Supporting the Near-Term Bearish Bias on the Nasdaq 100

- The current all-time intraday high of 29,390 printed on Monday, 11 May 2026, has moved significantly away from its 20-day moving average by almost 6%.

- The hourly RSI momentum indicator flashed a bearish divergence condition on Monday, 11 May 2026.

- The hourly RSI momentum indicator staged a bearish breakdown below its key ascending support on Tuesday, 12 May 2026.

Sunrise Market Commentary

Markets

UK gilts took a heavy blow on a toxic combination of political and fiscal uncertainty while a renewed oil price rise added further fuel to already lingering inflation risks. Prime minister Starmer for now resists growing pressure to leave office in the wake of last week’s historical election defeat. Some 90 Labour lawmakers by now have called on Starmer to resign. Unless at least 81 of them rally behind a single potential successor – automatically triggering a leadership contest – it is up to Starmer to decide. It’s mere perceived control over his own fate, though. Either he stays on as a lame duck bowing to backbencher demands or he eventually resigns. Acknowledging the risks, gilts sold off, pushing yields between 7.4 and 10.3 bps higher across the curve. The 10-yr (5.1%) and 30-yr (5.77%) closed at the highest level since 2008 and 1998 respectively. GBP lost ground but finished off the intraday lows. EUR/GBP traded just shy of 0.87 before paring gains to 0.867. European swap rates added 3.8-6.9 bps, slightly outperforming vs Bunds. Japanese yields continue their ascent, which remained largely below the radar lately even though several tenors are near, at or even above multidecade highs. US yields rose 3.8-5.3 bps with the 2-yr yield retesting the 4% barrier. April CPI numbers topped expectations and added to the intraday rise. The 3.8% headline print (from 3.3%) was not only supported by energy. Price rises were much broader. Services inflation in particular was striking, or as Fed Goolsbee called it: worrying. Even excluding a sharp shelter increase (0.6% m/m), the so-called supercore services gauge quickened to 3.4%, the highest since February 2025. We upgrade our in-house forecast for May to 4.2% for the headline and 2.9% for core. The US dollar strengthened to EUR/USD 1.1739. DXY bounced to north of 98. USD/JPY saw some intraday volatility during USTS Bessent’s visit to Japan. Some attributed it to authorities doing a rate check, the final stage before potential interventions. USD/JPY (157.63) quickly recovered from a drop to as low as 156.78.

There’s little inspiring on the economic agenda today. April US PPI’s are worth mentioning as a gauge for pipeline price pressures that may eventually show up in CPI. ECB’s Lagarde and chief economist Lane are scheduled to speak today, be it after European closing hours. We’ll be watching Lane for giving an update of a closely watched slide in a speech he gave April 14 and in which he plotted the oil forward curve in comparison with the ECB’s base and adverse scenario. Spoiler alert: it’ll have moved further towards the adverse one. Markets (ex. UK) in general may keep a cautious bias, sticking the sidelines going into the high-stakes meeting between the US and Chinese president from Thursday through Friday.

News & Views

Energy lobby groups Eurogas and the International Association of Oil & Gas Producers asked to maximize flexibility when it comes to refilling depleted natural gas inventories. Storage levels dropped below 30% for the first time since 2022 at the end of March/early April compared with an EU goal of reaching 90% ahead of the heating season (with 10 percentage point deviation). In their joint statement, Eurogas and IOGP call for flexibilities to be activated by the EC and member states as soon as possible, early in the storage season. “Initiatives such as demand aggregation or diversification approaches should remain voluntary in nature and must not distort wholesale price signals. Clear and credible price signals are indispensable to attract natural gas, and crude oil supplies in global markets, particularly in a tightening market characterized by intense competition for LNG cargoes, including by Asian buyers.” The timing of the statement coincides with an informal meeting of EU energy ministers later today.

The monthly Business Survey of the Banque de France showed economic activity growing more slowly in industry and construction and stagnating in market services. Industrial production remained relatively strong and even exceeded expectations. The outlook for May points to stagnation or declines in all sectors. Firms are still concerned about rising raw material prices and logistical disruptions. Due to strong competition, companies only partially pass these increases onto customers. Selling prices should continue to rise in industry and construction. In services, they are mainly seen in transport and logistics driven by higher diesel costs.

GBP/JPY Daily Outlook

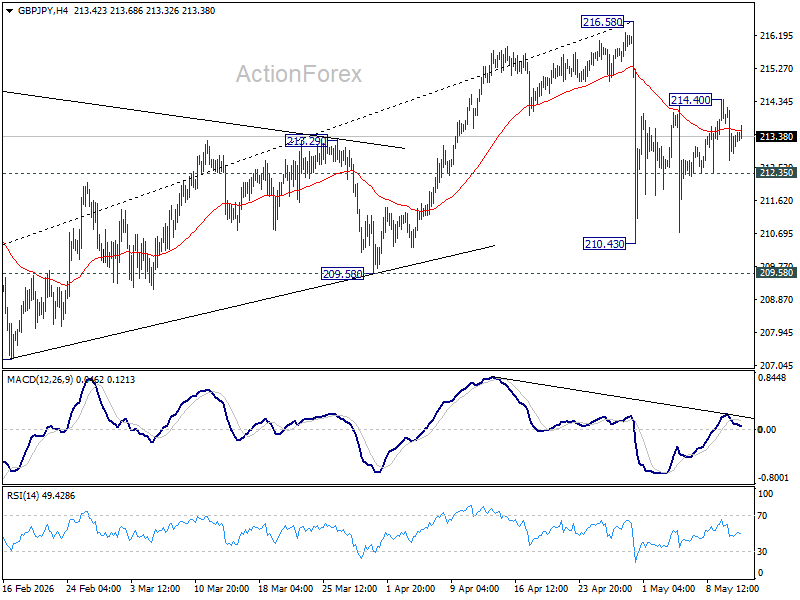

Daily Pivots: (S1) 212.67; (P) 213.43; (R1) 214.13; More...

Intraday bias in GBP/JPY remains neutral for the moment. On the downside, break of 212.35 minor support will bring deeper fall back to 210.43 support. On the upside, firm break of 214.40 will bring stronger rebound to retest 216.58 high.

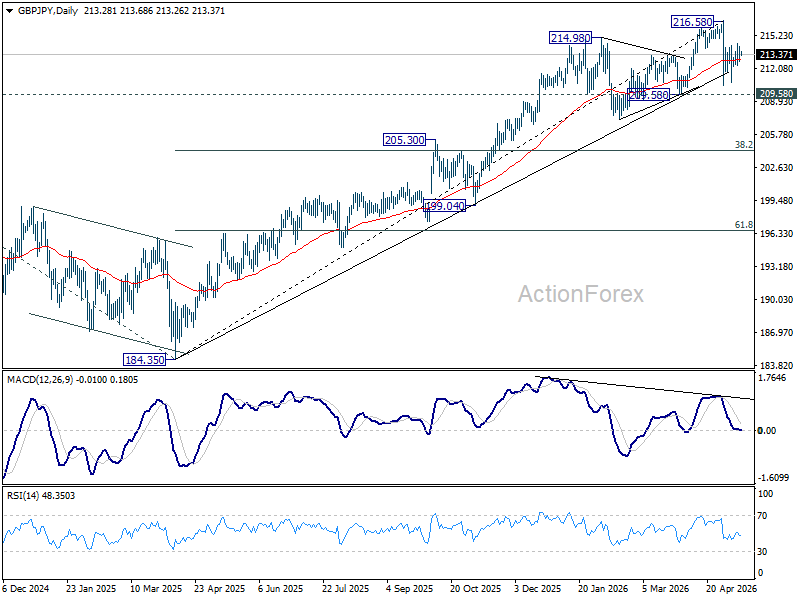

In the bigger picture, while the fall from 216.58 is steep, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 205.75) will argue that it's already in medium term down trend for 184.35 support.

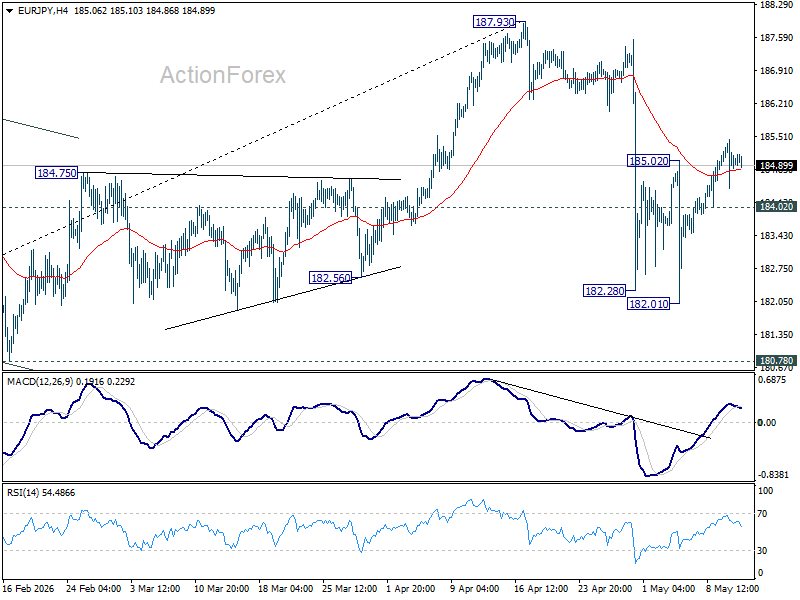

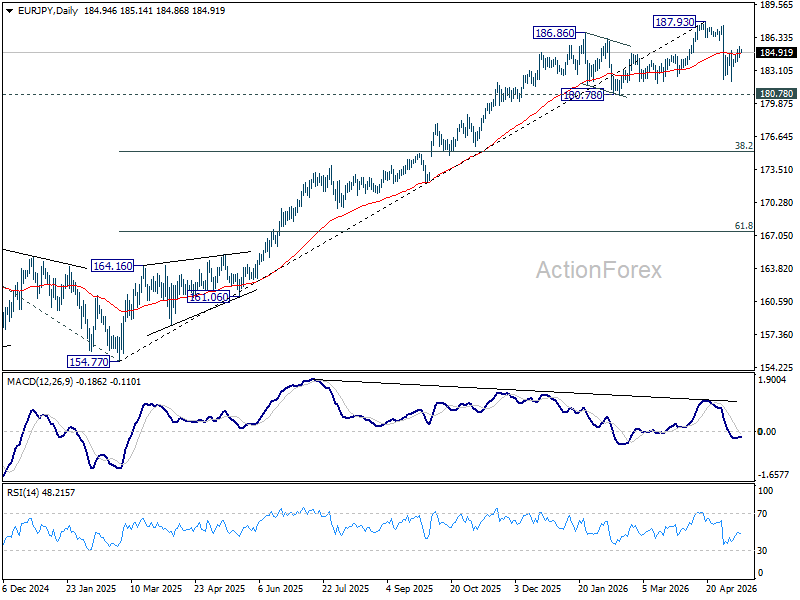

EUR/JPY Daily Outlook

Daily Pivots: (S1) 184.45; (P) 184.95; (R1) 185.47; More...

Intraday bias in EUR/JPY remains mildly on the upside at this point. Pullback from 187.93 could have completed at 182.01 already. Further rise would be seen back to retest this high. Nevertheless, break of 184.02 minor support will turn bias back to the downside towards 182.01 again.

In the bigger picture, the pullback from 187.93 is steep, there is no sign of reversal yet. Uptrend from 114.42 is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 178.04) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.

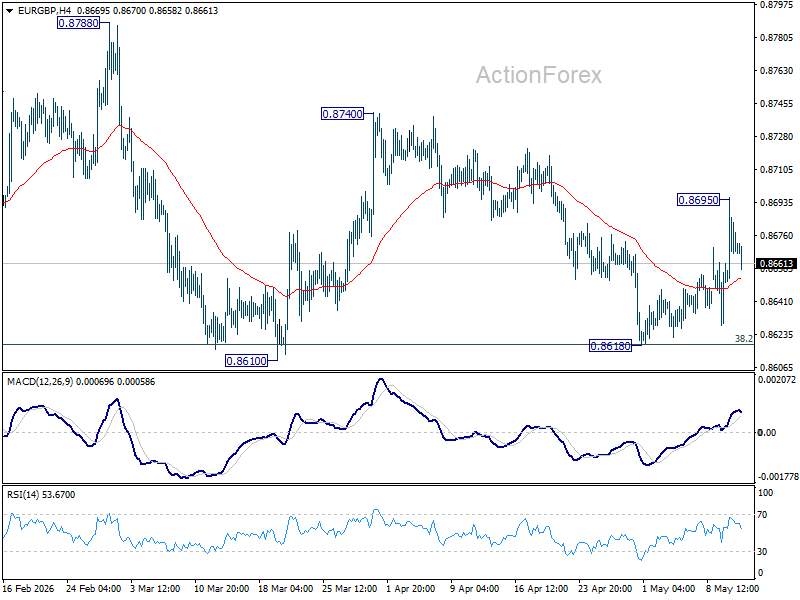

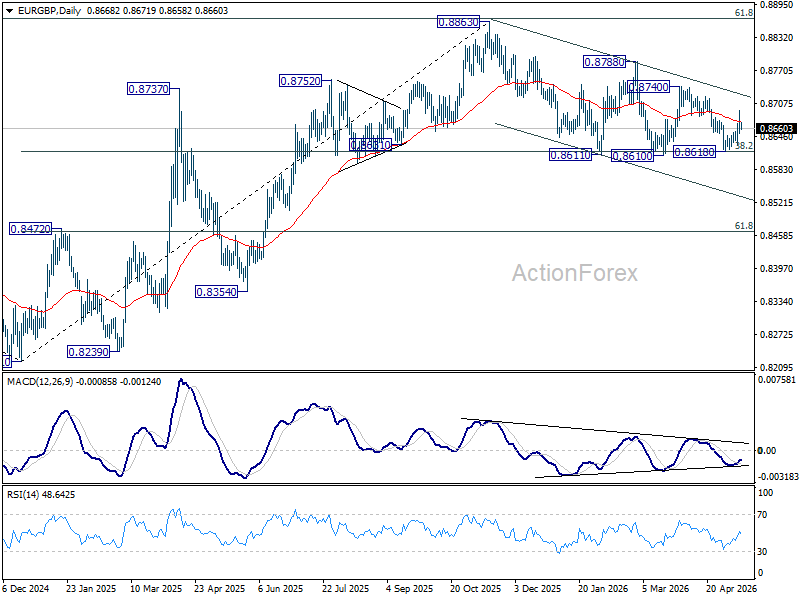

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8641; (P) 0.8669; (R1) 0.8695; More…

EUR/GBP retreated after hitting 0.8695 and intraday bias is turned neutral first. Risk is mildly on the upside as long as 0.8618 support holds. Above 0.8695 will target 0.8740 first. Firm break there will target 0.8788 resistance next.

In the bigger picture, focus is back on 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Strong rebound from there will retain medium term bullishness. Rise from 0.8221 should resume through 0.8863 at a later stage. Nevertheless, sustained break of 0.8618 will confirm that whole rise from 0.8221 has completed at 0.8863. Deeper decline should then be seen to 61.8% retracement at 0.8466 at least.

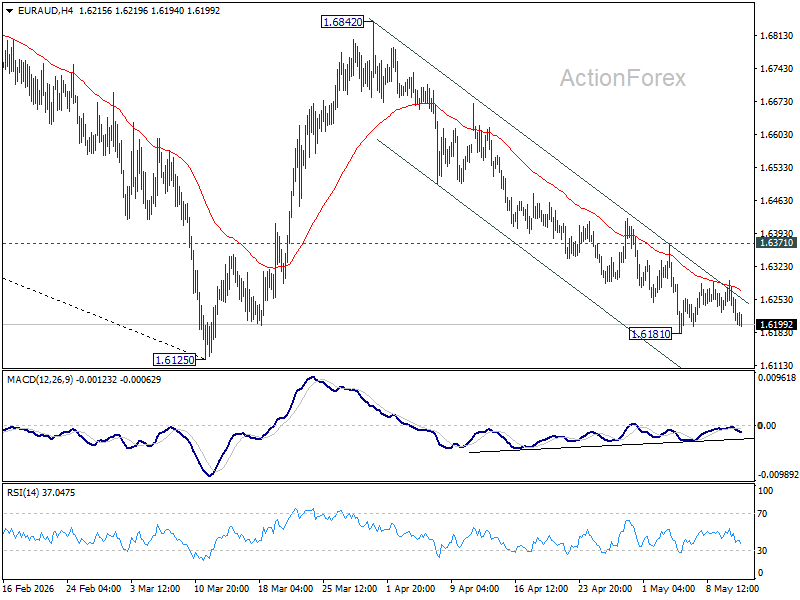

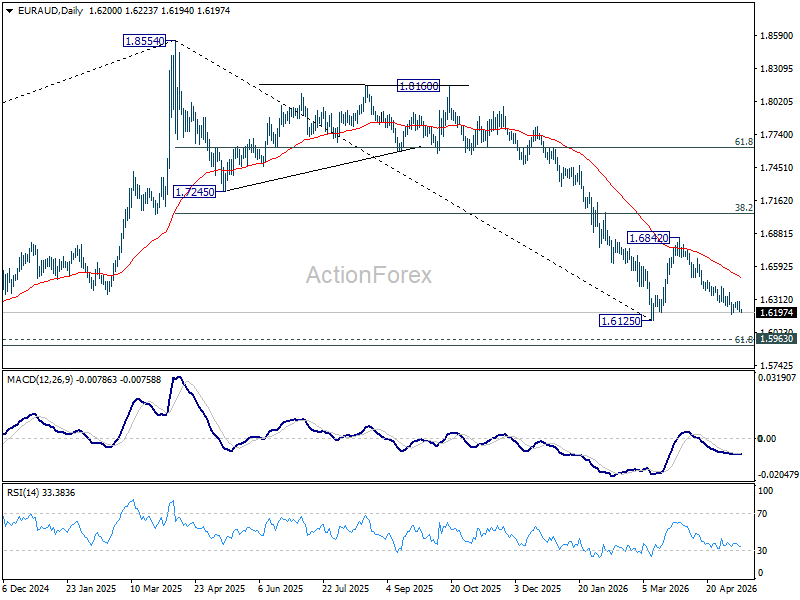

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6169; (P) 1.6231; (R1) 1.6262; More...

Intraday bias in EUR/AUD remains neutral for the moment, and further fall is expected with 1.6371 resistance intact. On the downside, decisive break of 1.6125 will resume larger fall from 1.8554. Nevertheless, break of 1.6371 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound to 55 D EMA (now at 1.6494).

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7039) holds, even in case of strong rebound.

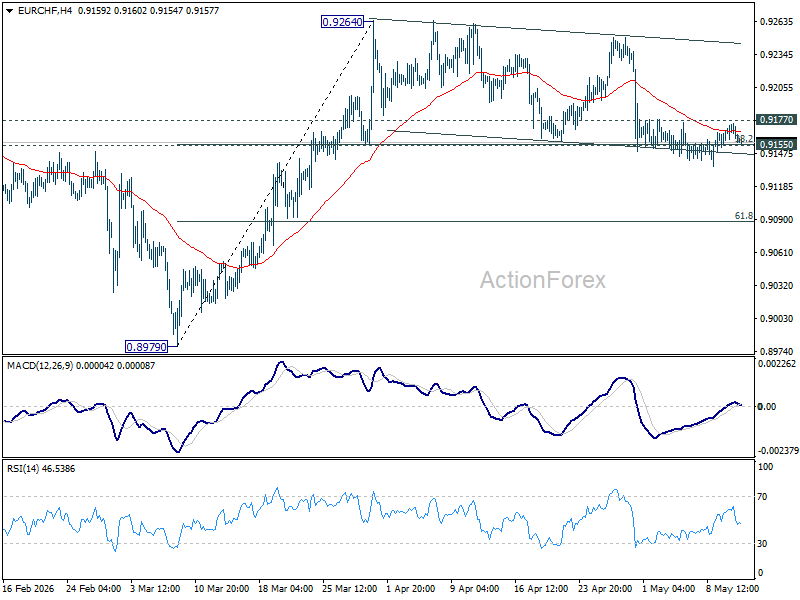

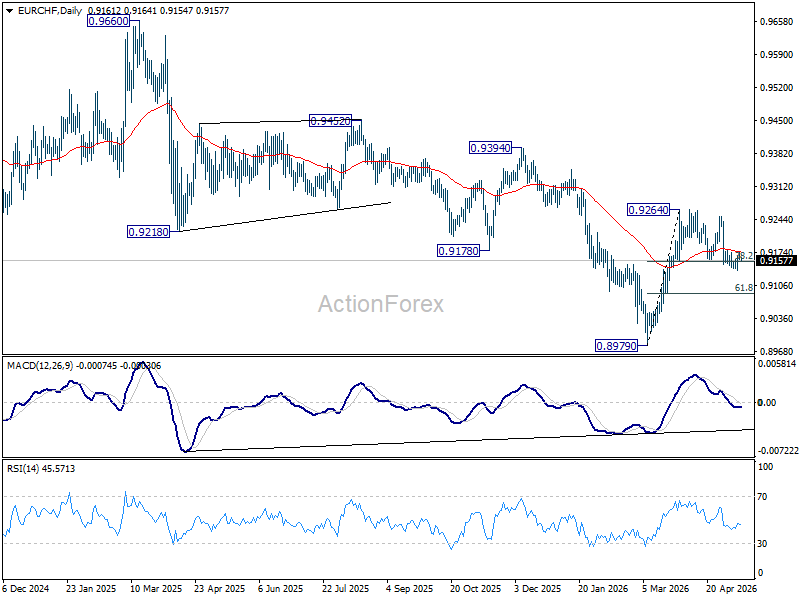

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9151; (P) 0.9162; (R1) 0.9173; More....

Intraday bias in EUR/CHF remains neutral at this point. On the upside, break of 0.9177 minor resistance will turn bias back to the upside for 0.9264 resistance. However, sustained trading below 0.9155 cluster support (38.2% retracement of 0.8979 to 0.9264 at 0.9155) will turn bias back to the downside for deeper pullback to 61.8% retracement at 0.9088 and possibly below.

In the bigger picture, considering bullish convergence condition in W MACD, a medium term bottom should be in place at 0.8979. Sustained trading above 55 W EMA (now at 0.9241) will add more credence to this case. Further break of 0.9394 resistance will pave the way to 0.9660 resistance next. However rejection by the 55 W EMA will set up another fall through 0.8979 low at a later stage.

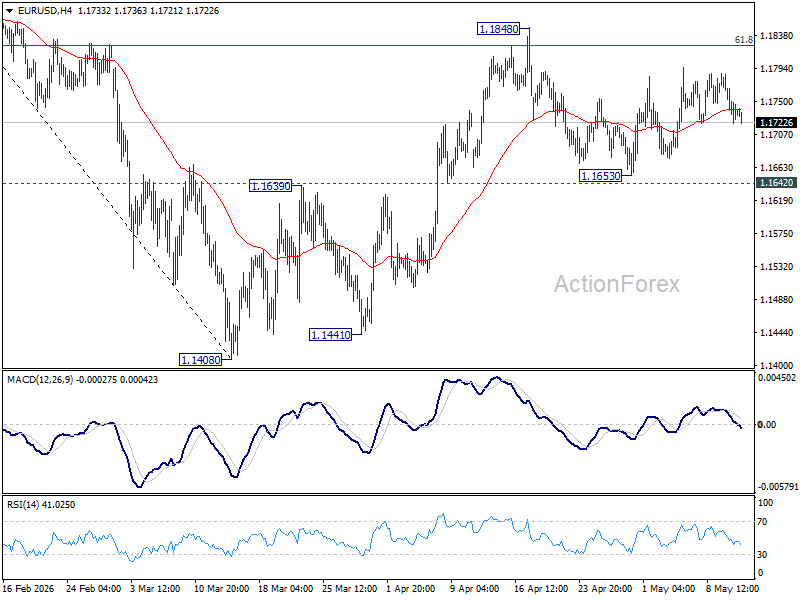

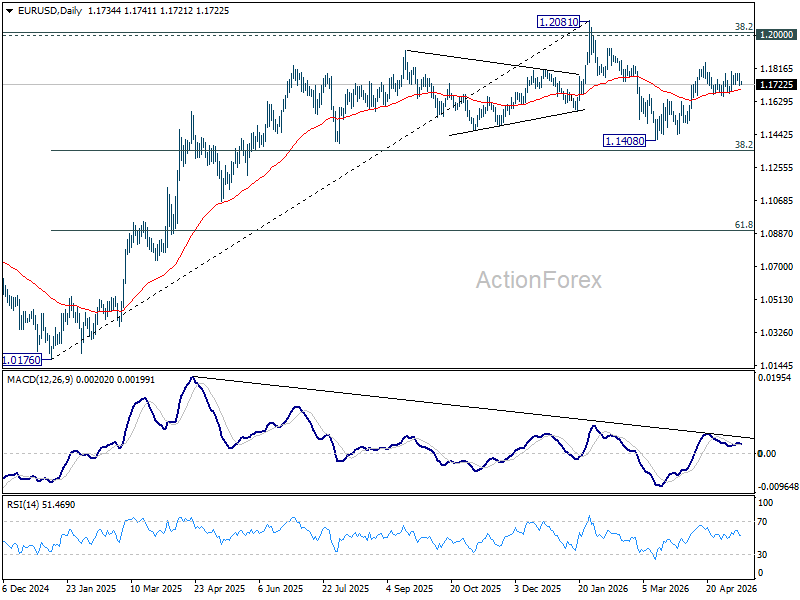

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1709; (P) 1.1748; (R1) 1.1775; More….

Range trading continues in EUR/USD and intraday bias stays neutral. Further rise is expected with 1.1642 support intact. On the upside, firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1539). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

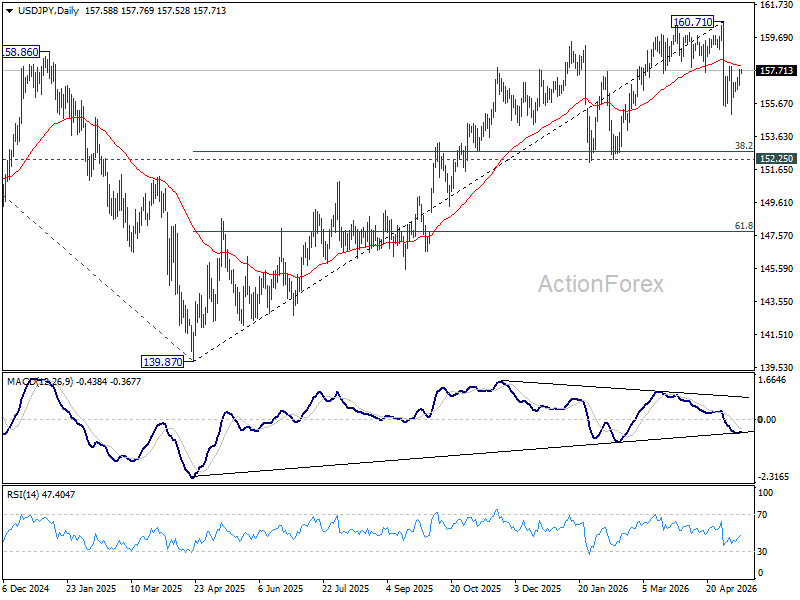

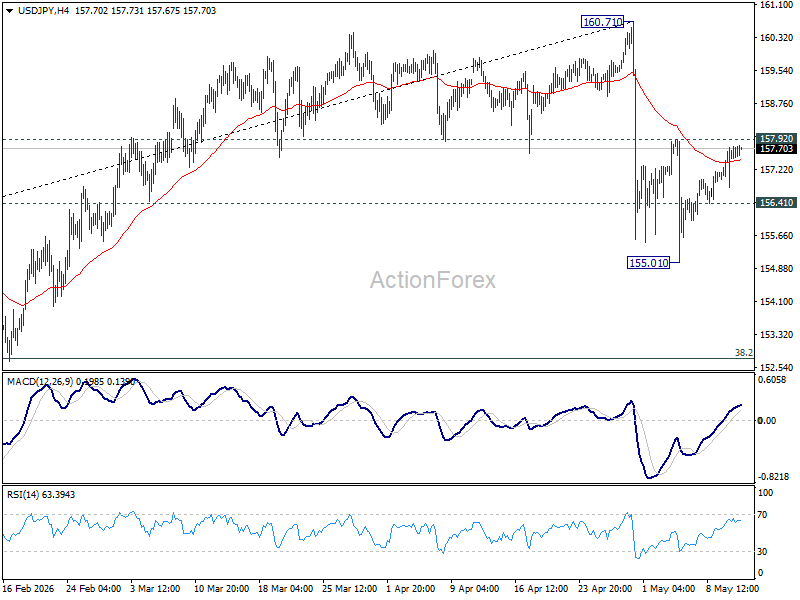

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.96; (P) 157.36; (R1) 157.99; More...

Intraday bias in USD/JPY stays neutral at this point. On the downside, below 156.41 minor support will bring retest of 155.01. Firm break there will resume the fall from 160.71 to 152.25 support next. On the upside, however, firm break of 157.92 will indicate that pullback from 160.71 has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.13) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.