Sample Category Title

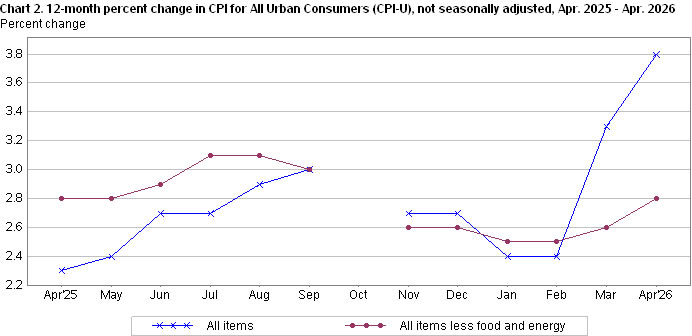

US: Inflation Rises to Three-Year High of 3.8% in April

The Consumer Price Index (CPI) rose by 0.6% month-on-month (m/m) in April, meeting the Bloomberg consensus forecast. On a twelve-month basis, CPI jumped 3.8% – the fastest rate of growth in three-years.

- Another surge in energy costs accounted for roughly half the monthly gain in headline, led by a 5.6% m/m gain in prices at the pump. Food prices (+0.5% m/m) also heated up last month, led by a sharp acceleration in grocery costs (+0.7% m/m).

Excluding food and energy, core inflation rose 0.4% m/m, a tick stronger than consensus and roughly double the rate of increase from the month prior. On a twelve-month basis, core prices were up 2.8% (from 2.6% in March).

Services inflation jumped 0.5% m/m, following a softer 0.2% m/m gain in March. Primary shelter costs were the main driver, rising 0.5% m/m – much stronger than the 0.2% m/m averaged over the prior three months.

- Non-housing services also firmed thanks to another uptick in airfares and personal care services.

Core goods prices were flat, as price gains in apparel and education & communication goods were offset by a pullback in household furnishings and medical goods.

Key Implications

Inflationary pressures heated up in April, as elevated crude oil prices continued to push gas prices higher and lead to some spillover price effects across other categories like food and airfares. That said, some of the uptick in core inflation looks overdone. Primary shelter contributed 0.2 percentage points to April's increase – double its normal monthly contribution – which looks to be related to an unwinding of a government-shutdown survey quirk that occurred in the CPI data late last year. This effect should fall out next month, allowing the shelter component to resume its downward trend.

This morning's numbers reinforce why the Fed needs to remain patient. Even assuming a "more normal" reading on shelter prices last month, core inflation would've still firmed relative to March. With secondary price effects from higher energy prices likely to intensify in the months ahead, we're likely to see core measures of inflation drift a bit higher and hover around 3% through year-end. Treasury yields across the curve were little changed post-release, with Fed futures now shifting back to pricing in a 60% probability of a rate hike by March 2027.

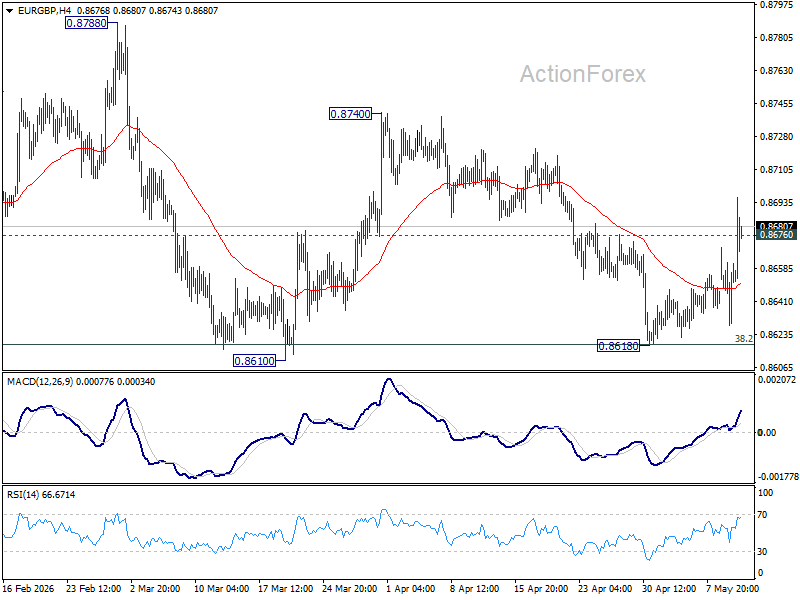

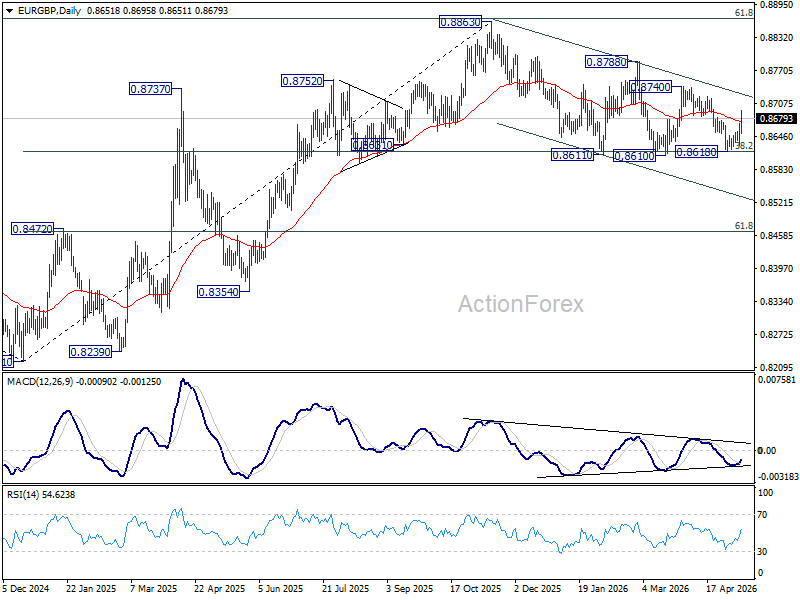

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8632; (P) 0.8651; (R1) 0.8673; More…

EUR/GBP's extended rebound and break of 0.8676 resistance suggests that fall from 0.8740 has completed at 0.8618 already. Intraday bias is back on the upside for 0.8740 first. Firm break there will target 0.8788 resistance next. For now, risk will stay on the upside as long as 0.8618 holds, in case of retreat.

In the bigger picture, focus is back on 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Strong rebound from there will retain medium term bullishness. Rise from 0.8221 should resume through 0.8863 at a later stage. Nevertheless, sustained break of 0.8618 will confirm that whole rise from 0.8221 has completed at 0.8863. Deeper decline should then be seen to 61.8% retracement at 0.8466 at least.

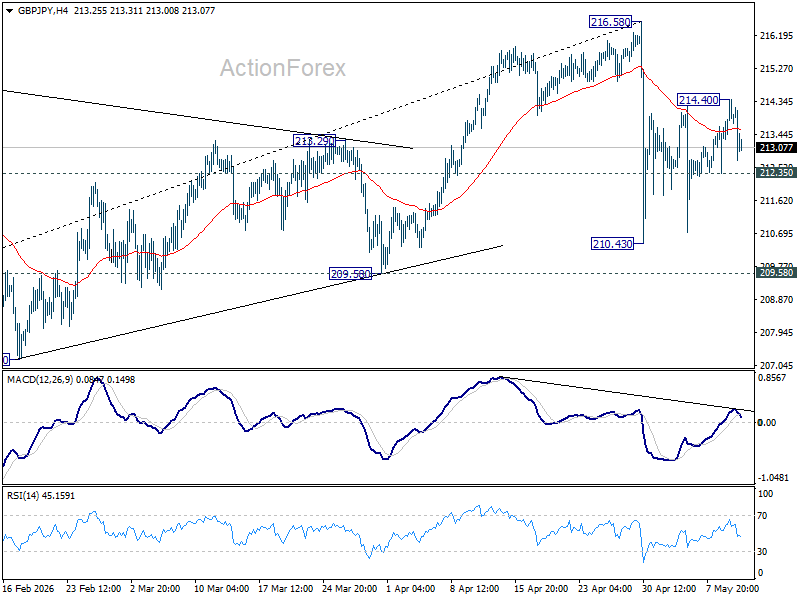

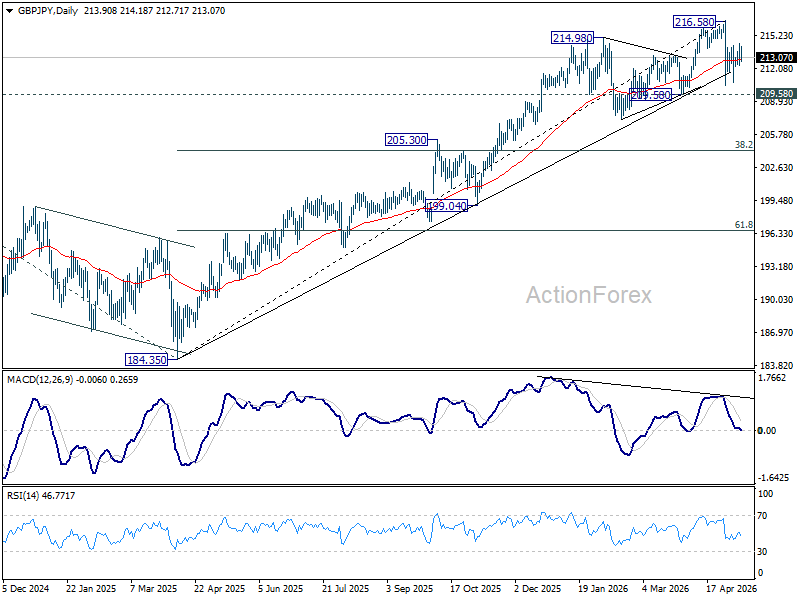

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 212.51; (P) 213.46; (R1) 214.81; More...

Intraday bias in GBP/JPY is turned neutral again with 4H MACD crossed below signal line. On the downside, break of 212.35 minor support will bring deeper fall back to 210.43 support. On the upside, firm break of 214.40 will bring stronger rebound to retest 216.58 high.

In the bigger picture, while the fall from 216.58 is steep, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 205.75) will argue that it's already in medium term down trend for 184.35 support.

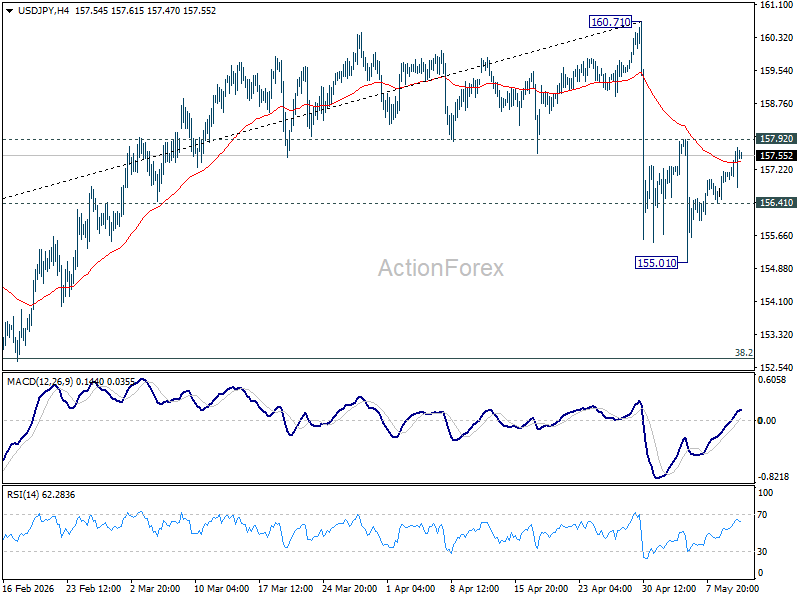

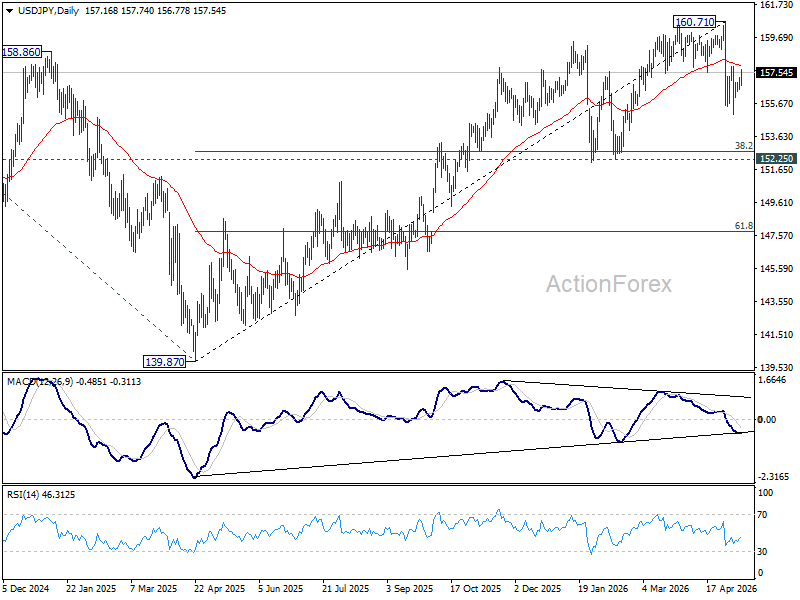

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.63; (P) 156.94; (R1) 157.46; More...

Intraday bias in USD/JPY stays neutral and outlook is unchanged. On the downside, below 156.41 minor support will bring retest of 155.01. Firm break there will resume the fall from 160.71 to 152.25 support next. On the upside, however, firm break of 157.92 will indicate that pullback from 160.71 has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.13) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

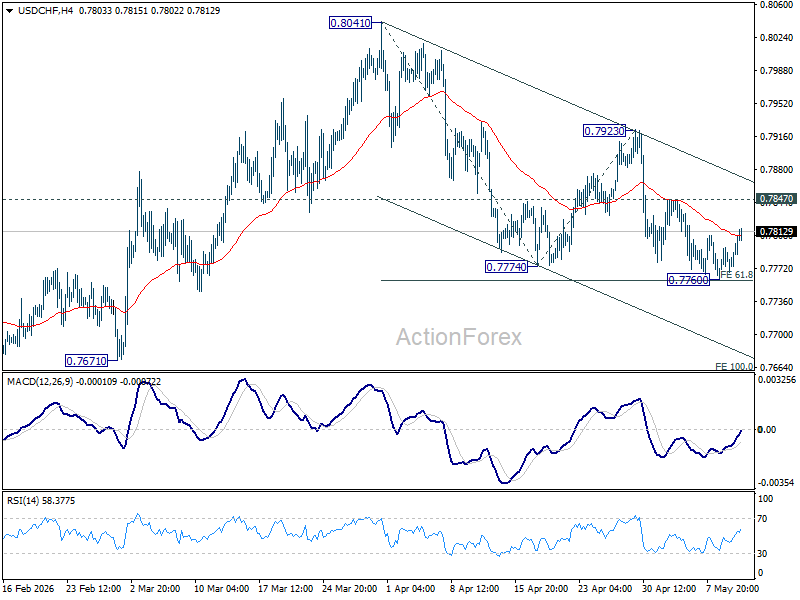

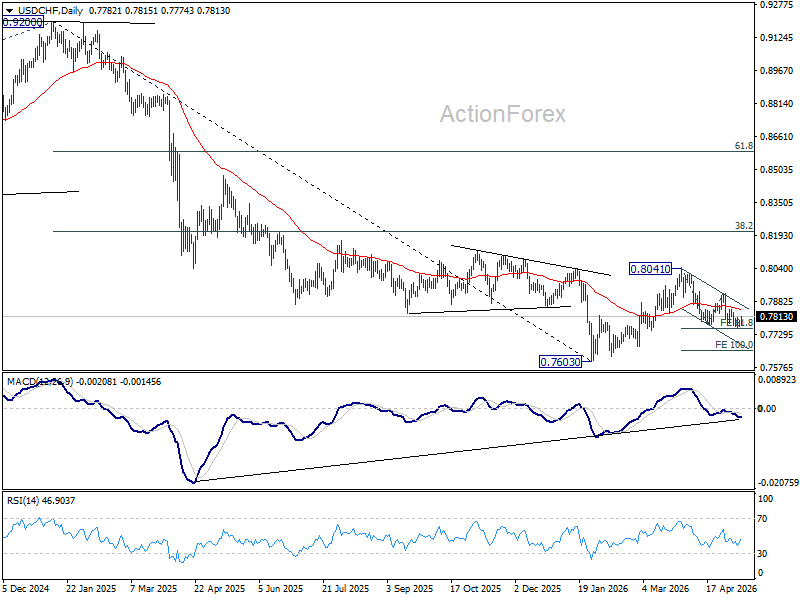

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7759; (P) 0.7776; (R1) 0.7791; More….

USD/CHF's rec continues today but stays below 0.7847 resistance. Intraday bias remains neutral and further decline is expected. On the downside, decisive break of 0.7760 will resume the whole decline form 0.8041, and target 100% projection of 0.8041 to 0.7774 from 0.7923 at 0.7656. However, firm break of 0.7847 resistance will indicate short term bottoming, and bring stronger rebound back to 0.7923 resistance.

In the bigger picture, as long as 55 W EMA (now at 0.8051) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

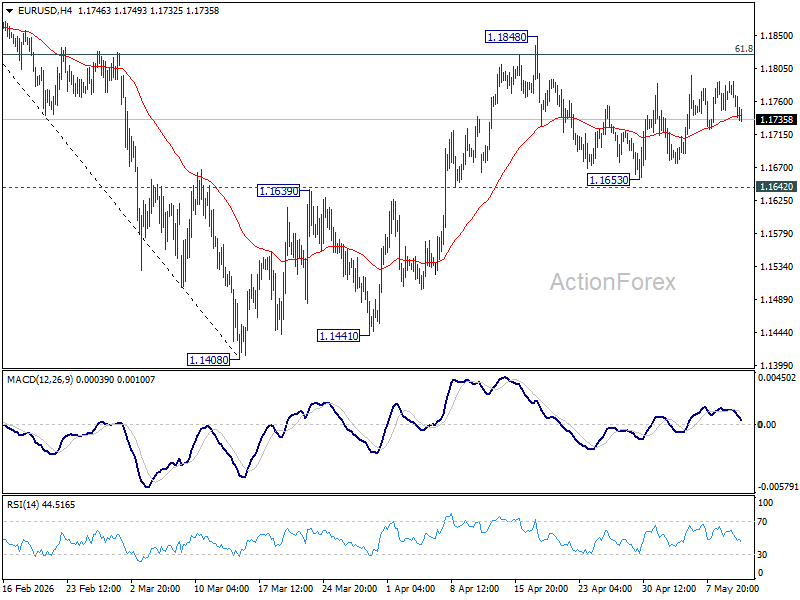

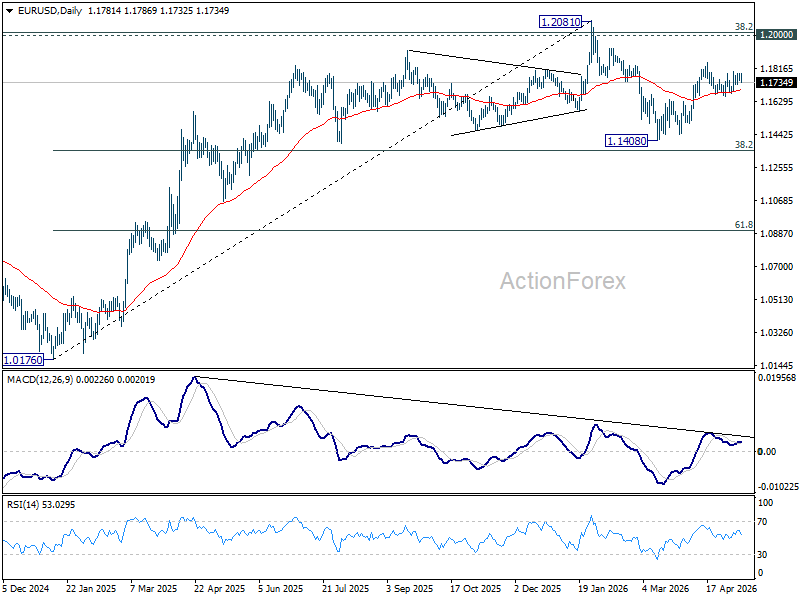

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1752; (P) 1.1769; (R1) 1.1799; More….

EUR/USD is still bounded in established range below 1.1848 and intraday bias remains neutral. Further rise is expected with 1.1642 support intact. On the upside, firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1539). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

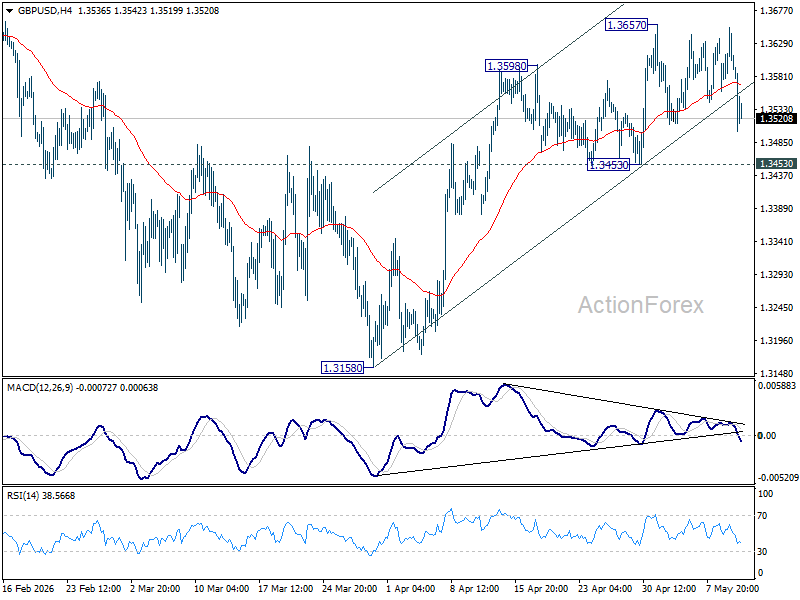

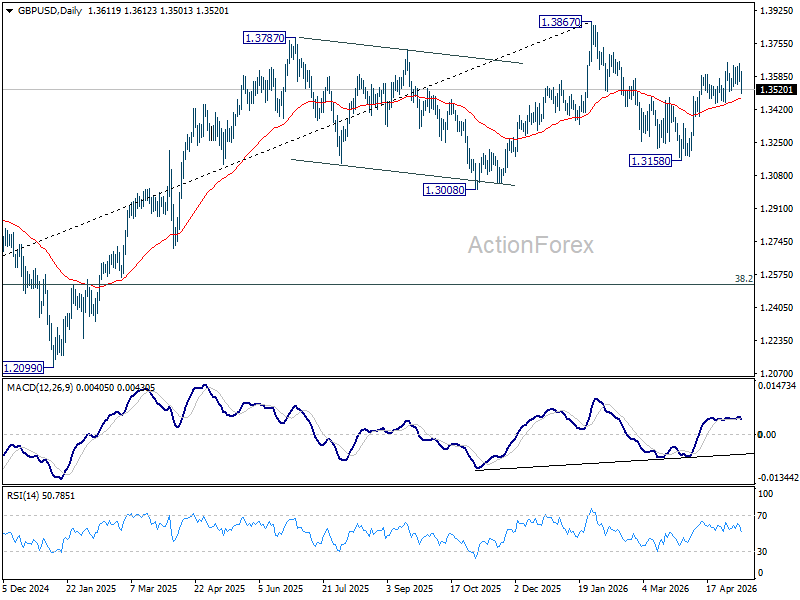

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3555; (P) 1.3603; (R1) 1.3656; More...

GBP/USD falls notably today but stays above 1.3453 support. Intraday bias remains neutral and further rally is in favor. On the upside, firm break of 1.3657 will resume the rally fro 1.3158 to retest 1.3867 high. However, decisive break of 1.3453 will argue that the rebound has already completed, and turn bias to the downside for retesting 1.3158 instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).

Dollar Gains as Oil and CPI Lift Fed Hike Bets, but Risk Appetite Holds Firm

Dollar strengthened broadly today as rising oil prices and firmer-than-expected US inflation data continued pushing markets toward a more hawkish Federal Reserve outlook. However, the overall move remained relatively measured as broader risk sentiment stayed resilient, with investors still reluctant to fully embrace defensive positioning ahead of the Trump-Xi summit later this week.

Oil prices remained a key driver. Brent crude climbed back above %107 while WTI traded above %100 as stalled US-Iran peace negotiations continued sustaining geopolitical risk premium in energy markets. Nevertheless, both benchmarks remain largely trapped within the broad consolidation ranges established after the sharp March spike, suggesting traders still see the Hormuz crisis as unresolved but not yet spiraling into a full-scale crisis. The eventual direction of the Strait of Hormuz situation may depend heavily on the outcome of Thursday’s Trump-Xi summit.

The second major support for Dollar came from US inflation data. April CPI showed headline inflation accelerating from 3.3% yoy to 3.8% yoy, while core CPI rose from 2.6% yoy to 2.8% yoy, both slightly above expectations. The firmer core readings in particular raised concern that energy-driven inflation pressures may now be spreading more broadly into underlying consumer prices. Fed fund futures subsequently pushed further toward pricing no rate cuts this year, while implied odds of a rate hike rose toward 28%.

Still, Dollar’s rally remained restrained overall. US equities held relatively firm, and broader risk appetite continued receiving support from ongoing optimism surrounding AI-related investment themes and semiconductor demand. The market tone suggests investors are pricing higher inflation risk without yet fully shifting toward outright crisis positioning.

Sterling was among the weakest major currencies earlier in the session as UK political concerns intensified following the first ministerial resignation calling for Prime Minister Keir Starmer to step down. Markets had already become uneasy after Labour’s poor local election results last week, but Miatta Fahnbulleh’s resignation turned the leadership crisis into a more immediate market concern. However, the Pound later stabilized after senior Cabinet ministers rallied behind Starmer following a critical internal meeting where he insisted he would not resign voluntarily without a formal leadership challenge.

Yen also experienced significant intraday volatility. Initially, the currency weakened alongside rising oil prices, continuing the recent pattern where higher energy costs pressure Japan’s import-heavy economy. However, Yen later rebounded strongly after US Treasury Secretary Scott Bessent reaffirmed that both the United States and Japan believe excessive currency volatility is undesirable.

Speaking after meeting Prime Minister Sanae Takaichi, Bessent said Washington remained in close contact with Japanese authorities on exchange rate developments and expressed confidence that BOJ Governor Kazuo Ueda would successfully avoid falling behind the curve on inflation. The remarks were interpreted by markets as broad US support for Japan’s recent Yen-buying intervention efforts. The comments followed similar remarks earlier from Japanese Finance Minister Satsuki Katayama, who confirmed close coordination with Washington on currency market developments.

In the currency markets, Dollar is the strongest one for the day so far, followed by Kiwi, and then Loonie. Sterling is the worst, followed by Swiss Franc, and then Aussie. Euro and Yen are positioning in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.30%. DAX is down -0.95%. CAC is down -0.57%. UK 10-year yield is up 0.105 at 5.11. Germany 10-year yield is up 0.049 at 3.092. Earlier in Asia, Nikkei rose 0.52%. Hong Kong HSI fell -0.22%. China Shanghai SSE fell -0.25%. Singapore Strait Times rose 0.07%. Japan 10-year JGB yield rose 0.019 to 2.544.

US CPI Hits Highest Since 2023, Core Inflation Beats Expectations

April’s US CPI report reinforced the “higher for longer” inflation narrative as both headline and core prices accelerated faster than expected. Rising gasoline, shelter, and food costs suggest inflation pressures are broadening beyond energy alone, further reducing expectations for Fed rate cuts this year. Read More.

EUR/GBP Surges as Markets Price “Zombie Government” Risk as Starmer Crisis Deepens

Sterling came under intense pressure after the first ministerial resignation demanding Keir Starmer’s departure transformed Labour’s political crisis into a broader market concern. With more than 80 MPs reportedly calling for a leadership transition, traders are increasingly pricing “zombie government” risk into UK assets. Read More.

German ZEW Sentiment Rises to -10.2, But Economy Still Burdened by Energy Shock

Germany’s ZEW survey showed investor sentiment recovering modestly in May as markets increasingly hoped for eventual de-escalation in the Iran conflict. However, weak industrial activity, rising energy costs, and deteriorating current conditions continued highlighting the fragile state of Europe’s largest economy. Read More.

BoJ Summary Shows Growing Support for Near-Term Rate Hike

The BOJ’s April meeting summary revealed a noticeably more hawkish debate inside the board, with several policymakers openly discussing the possibility of another rate hike as the Iran-driven oil shock lifts inflation risks. Markets are increasingly pricing a potential move as early as June. Read More.

Australia NAB Survey Shows Cost Growth Jumps to 4.5% as Margin Squeeze Intensifies

Australia’s April NAB survey painted an increasingly stagflationary picture as purchase cost growth surged to 4.5% following the Middle East energy shock. While firms continued facing rising input costs, weaker trading, employment, and activity indicators suggested margin pressure is beginning to weigh more heavily on the broader economy. Read More.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3555; (P) 1.3603; (R1) 1.3656; More...

GBP/USD falls notably today but stays above 1.3453 support. Intraday bias remains neutral and further rally is in favor. On the upside, firm break of 1.3657 will resume the rally fro 1.3158 to retest 1.3867 high. However, decisive break of 1.3453 will argue that the rebound has already completed, and turn bias to the downside for retesting 1.3158 instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).

US CPI Hits Highest Since 2023, Core Inflation Beats Expectations

US inflation accelerated further in April as rising energy and shelter costs kept price pressures elevated. Headline CPI rose 0.6% mom, matching expectations, while core CPI increased 0.4% mom, above the expected 0.3% gain and signaling broader underlying inflation momentum beyond energy alone.

The energy component remained the dominant driver of the monthly increase. The energy index rose 3.8% mom after surging 10.9% in March, accounting for more than 40% of the overall monthly rise in consumer prices. Gasoline prices alone climbed 5.4% during the month and were up 28.4% compared with a year earlier as the Middle East conflict continued disrupting global energy markets. Shelter costs also remained firm, rising 0.6% mom, while food prices increased 0.5% mom.

On an annual basis, headline CPI accelerated from 3.3% yoy to 3.8% yoy, above expectations of 3.7% yoy and marking the highest reading since May 2023. Core CPI also strengthened from 2.6% yoy to 2.8% yoy, exceeding forecasts of 2.7% yoy.

The report is likely to further reduce expectations for Fed rate cuts this year and may even revive market discussion around the possibility of additional tightening if energy-driven inflation pressures continue broadening into core categories.

| Indicator | Previous | Latest | Expectation |

|---|---|---|---|

| Headline CPI (MoM) | 0.9% | 0.6% | 0.6% |

| Core CPI (MoM) | 0.2% | 0.4% | 0.3% |

| Headline CPI (YoY) | 3.3% | 3.8% | 3.7% |

| Core CPI (YoY) | 2.6% | 2.8% | 2.7% |

Chart Alert: WTI Crude Is Poised for a Potential Volatility Bullish Breakout Above $102.54/bbl

Key Takeaways

- West Texas Intermediate crude oil remains strongly supported by ongoing geopolitical tensions after hopes for renewed US-Iran peace talks faded, increasing the risk of a prolonged Strait of Hormuz disruption and sustained global energy supply tightness.

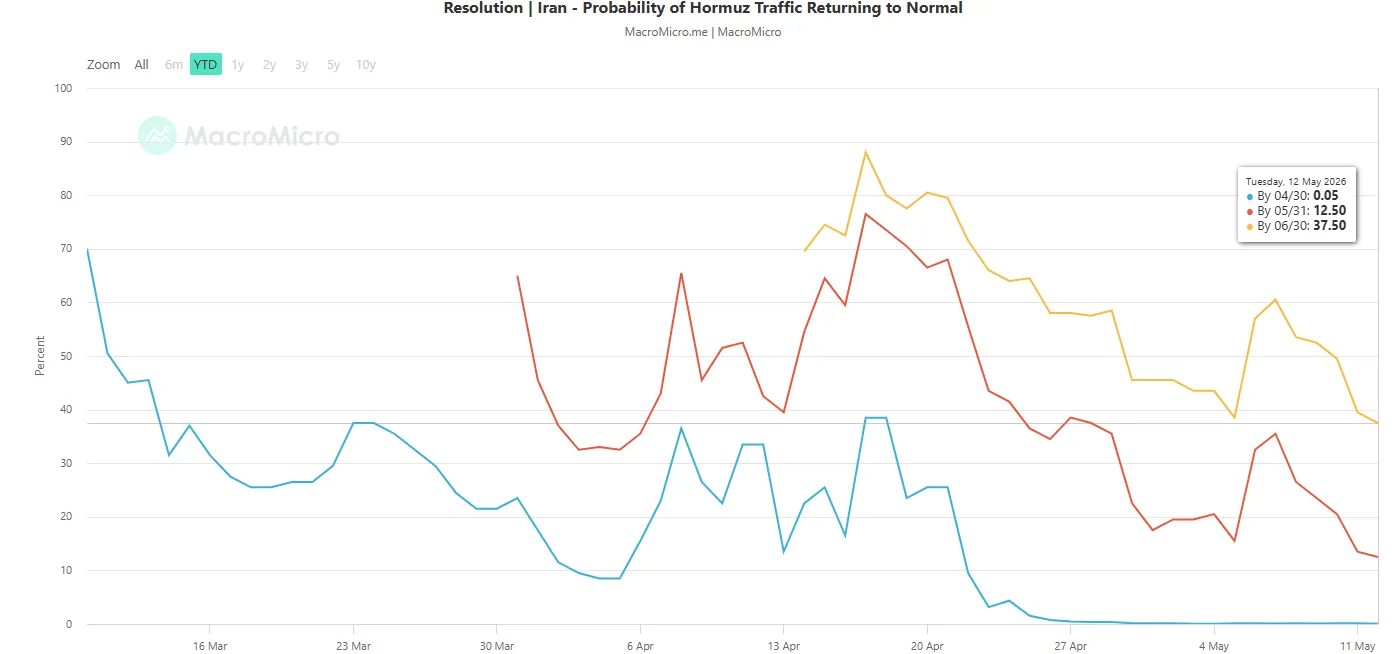

- Prediction market data from Polymarket shows sharply declining probabilities of shipping traffic normalising in the Strait of Hormuz by May and June 2026, reinforcing elevated geopolitical risk premiums in oil markets.

- Technically, WTI crude is showing bullish breakout conditions above its 20-day and 50-day moving averages, supported by bullish candlestick formations and positive RSI momentum, with $102.54 acting as the key breakout resistance level.

The optimism that was being priced in by global markets last week for an imminent second round of US-Iran peace deal talks to take place this week has fizzled out after US President Trump rejected Tehran’s response to the latest US proposal on Sunday.

The key hurdle is the transfer of Iran’s enriched uranium. In a nutshell, without any set dates for peace talks emerging on the near-term horizon, the ongoing two-month-plus closure in the Strait of Hormuz is likely to extend, which may aggravate the global energy and oil crunch as oil flows continue to dwindle.

Prolonged Strait of Hormuz Closure May Sustain Elevated Oil Prices

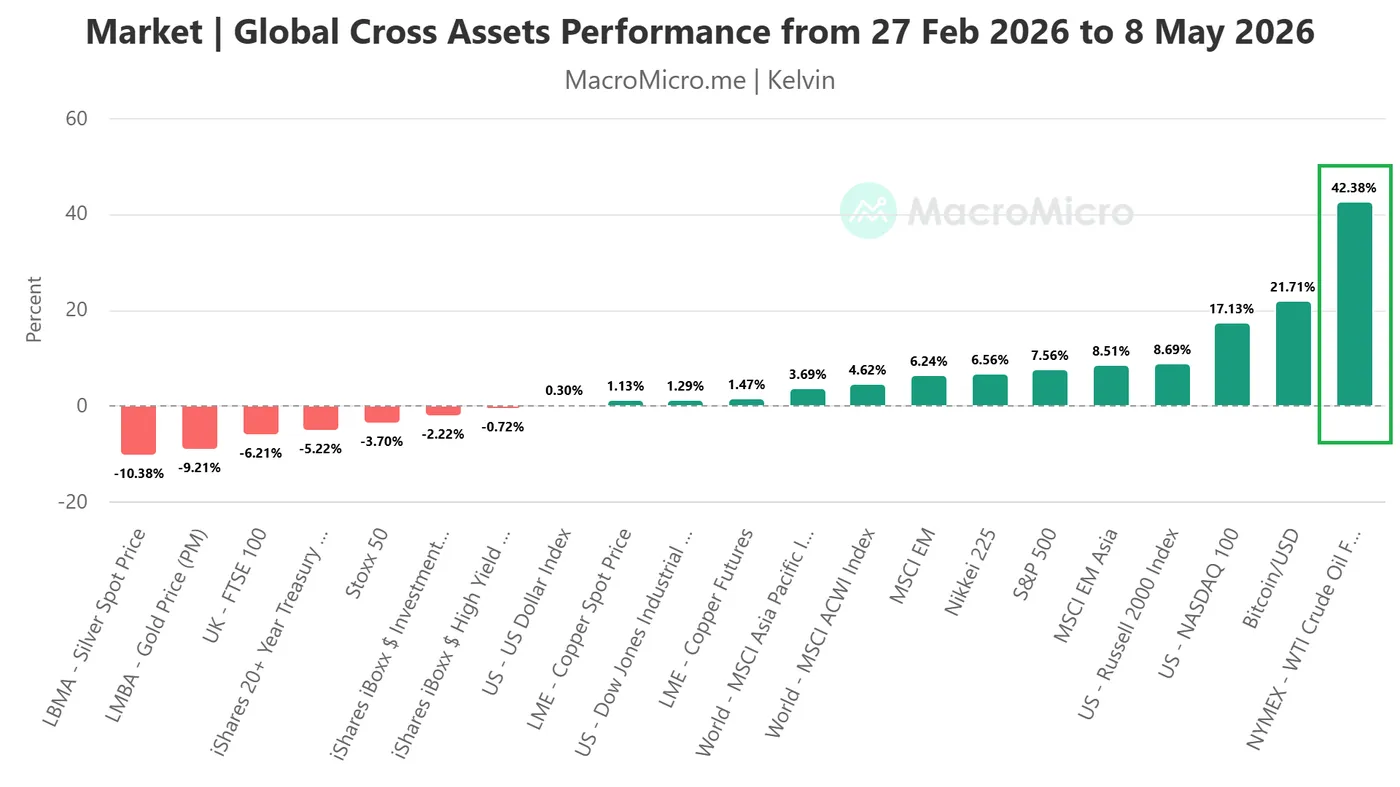

Fig. 1: WTI crude oil futures and other cross-asset performances from 27 February 2026 to 8 May 2026. Source: MacroMicro.

Fig. 2: Polymarket probability of Strait of Hormuz traffic returning to normal as of 12 May 2026. Source: MacroMicro.

Despite the fragile US-Iran ceasefire that has remained in place since 8 April 2026, oil continues to be the top-performing asset class.

From the pre-war baseline of 27 February 2026 through Friday, 8 May 2026, WTI crude oil futures surged by 42%, underscoring persistent supply disruption concerns and elevated geopolitical risk premiums in the energy market.

Betting data from Polymarket, a major prediction market platform, suggests a low probability of a return to normal shipping traffic in the Strait of Hormuz.

The probability of Hormuz traffic returning to normal by the end of May 2026 has been reduced to 12.5% as of 12 May 2026 from 35.5% printed on 7 May 2026.

A similar trend is evident for the end of June 2026, where the probability has fallen sharply to 37.5% from 60.5% over the same period.

Let’s now focus on the 1- to 3-day trajectory of WTI crude oil from a technical analysis perspective.

WTI Crude: Bullish Expansion Above 20-Day and 50-Day MAs

Fig. 3: West Texas oil CFD as of 12 May 2026. Source: TradingView.

Trend bias: Rebound towards the March/April 2026 medium-term range top with 95.00 as key short-term pivotal support.

Resistances: 102.54, 108.20, and 112.84.

Next supports: 90.50, 86.58, and 82.89.

Key Elements Supporting the Near-Term Bullish Bias on WTI Crude

- The price actions of the West Texas oil CFD, a proxy for WTI crude oil futures, have started to accelerate higher above their 20-day and 50-day moving averages following a brief period of subdued volatility observed on Friday, 8 May, and Monday, 11 May.

- The current daily candlestick on Tuesday, 12 May, has transformed into an impending “Bullish Marubozu” pattern after a prior daily bullish “Hammer” seen on 7 May, coupled with a retest of its key 50-day moving average. This is a sign of positive follow-through that may lead to higher prices.

- The hourly RSI momentum indicator continues to exhibit bullish momentum conditions as it remains supported by an ascending trendline.