Sample Category Title

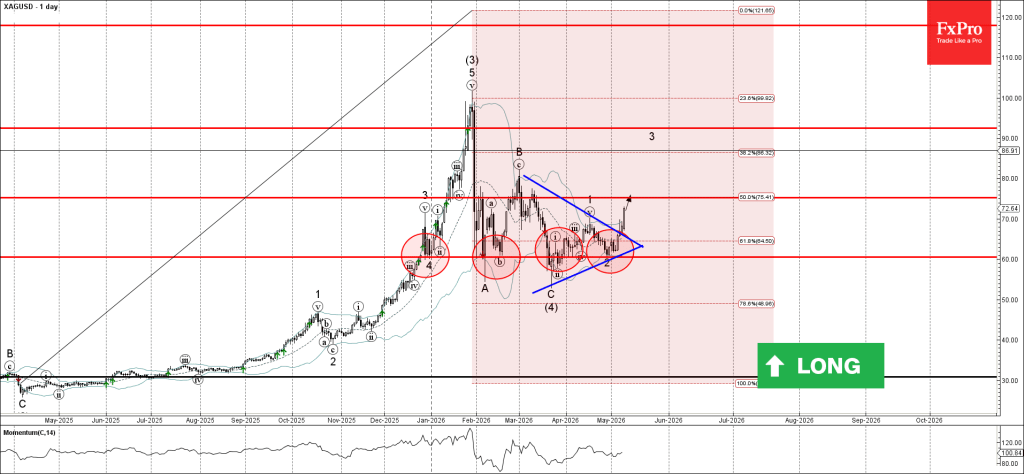

Silver Wave Analysis

Silver: ⬆️ Buy

- Silver broke daily Triangle

- Likely to rise to resistance level 75.30

Silver recently broke through the resistance zone between the resistance level 70.00 and the resistance trendline of the daily Triangle from February.

The breakout of this resistance zone accelerated the active minor impulse 3 – that belongs to the intermediate impulse wave (5) from March.

Silver can be expected to rise further to the next resistance level 75.30 – the breakout of which can lead to further gains toward 80.00.

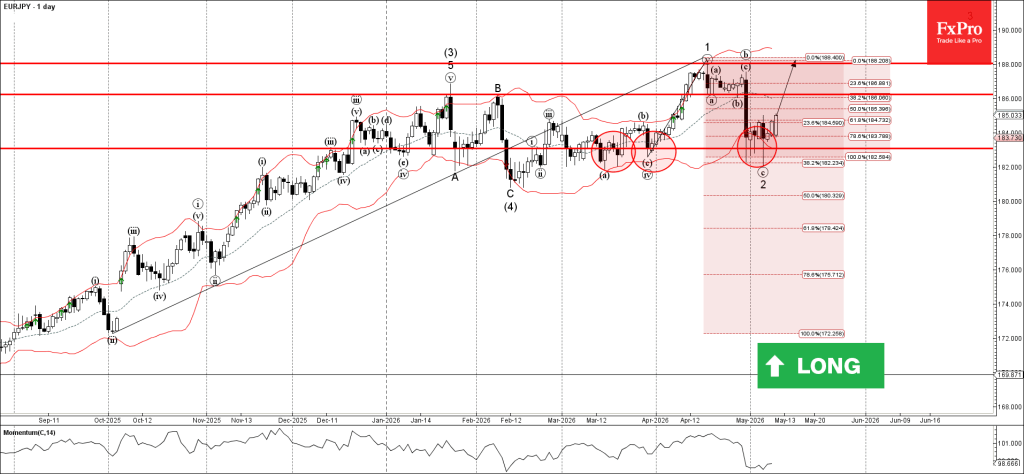

EURJPY Wave Analysis

EURJPY: ⬆️ Buy

- EURJPY reversed from support zone

- Likely to rise to resistance levels 186.00 and 188.00

EURJPY currency pair recently reversed up from the support zone between the strong support level 183.00 (which has been reversing the price from March), lower daily Bollinger Band and the 38.2% Fibonacci correction of the uptrend from October.

The upward reversal from this support zone started the active minor impulse 3 – that belongs to the intermediate impulse wave (5) from February.

Given the clear daily uptrend, EURJPY currency pair can be expected to rise to the next resistance level 186.00 and 188.00.

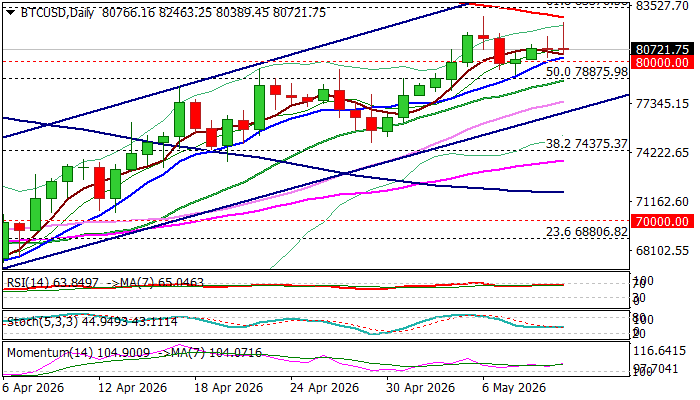

BTCUSD – Bulls Hold Grip Above 80K But 200DMA Barrier Provides Strong Headwinds

Bitcoin continues to trade above 80K mark that keeps near-term action biased higher, with broader uptrend (BTC is moving within a bull-channel off Mar 30 higher low) being fully in play so far.

Fresh recovery leg from 79136 (May 8 correction low) is steady, but gains are gradual and facing increased headwinds from key near-term barriers at 82800 zone (falling 200DMA / May 6 peak – the highest since Jan 31), lacking strength to fully reverse 82821/79136 pullback.

Bullish sentiment is to be supported by expectations for fresh capital inflows and signals that the Fed is likely to hold rates in 2026, with predominantly bullish daily studies contributing to positive near term outlook.

However, bulls need to clear 200DMA and nearby Fibo barrier at 83376 (61.8% retracement of 97946/59805 descend) to signal bullish continuation.

Bull channel upper boundary marks next resistance at 85000 zone, ahead of 88945 (Fibo 76.4%) and 90K (psychological).

Failure at 200DMA, on the other hand, may keep the action in extended consolidation, which should ideally hold above 80K and not exceed recent pullback low, reinforced by rising 20DMA (79000 zone) to keep bulls in play.

Res: 82463; 82777; 83376; 85073

Sup: 80000; 79136; 78875; 76971

Eco Data 5/12/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Household Spending Y/Y Mar | -2.90% | -1.50% | -1.80% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 01:30 | AUD | NAB Business Conditions Apr | 3 | 6 | ||

| 01:30 | AUD | NAB Business Confidence Apr | -24 | -29 | ||

| 05:00 | JPY | Leading Economic Index Mar P | 114.5 | 114.6 | 113.3 | |

| 06:00 | EUR | Germany CPI M/M Apr F | 0.60% | 0.60% | 0.60% | |

| 06:00 | EUR | Germany CPI Y/Y Apr F | 2.90% | 2.90% | 2.90% | |

| 06:30 | CHF | Producer and Import Prices M/M Apr | 0.80% | 0.10% | 0.20% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Apr | -2.00% | -2.70% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment May | -10.2 | -20.5 | -17.2 | |

| 09:00 | EUR | Germany ZEW Current Situation May | -77.8 | -77.5 | -73.7 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment May | -9.1 | -20 | -20.4 | |

| 10:00 | USD | NFIB Business Optimism Index Apr | 95.9 | 96.1 | 95.8 | |

| 12:30 | USD | CPI M/M Apr | 0.60% | 0.60% | 0.90% | |

| 12:30 | USD | CPI Y/Y Apr | 3.80% | 3.70% | 3.30% | |

| 12:30 | USD | CPI Core M/M Apr | 0.40% | 0.30% | 0.20% | |

| 12:30 | USD | CPI Core Y/Y Apr | 2.80% | 2.70% | 2.60% |

| 23:30 | JPY |

| Household Spending Y/Y Mar | |

| Actual | -2.90% |

| Consensus | -1.50% |

| Previous | -1.80% |

| 23:50 | JPY |

| BoJ Summary of Opinions | |

| Actual | |

| Consensus | |

| Previous | |

| 01:30 | AUD |

| NAB Business Conditions Apr | |

| Actual | 3 |

| Consensus | |

| Previous | 6 |

| 01:30 | AUD |

| NAB Business Confidence Apr | |

| Actual | -24 |

| Consensus | |

| Previous | -29 |

| 05:00 | JPY |

| Leading Economic Index Mar P | |

| Actual | 114.5 |

| Consensus | 114.6 |

| Previous | 113.3 |

| 06:00 | EUR |

| Germany CPI M/M Apr F | |

| Actual | 0.60% |

| Consensus | 0.60% |

| Previous | 0.60% |

| 06:00 | EUR |

| Germany CPI Y/Y Apr F | |

| Actual | 2.90% |

| Consensus | 2.90% |

| Previous | 2.90% |

| 06:30 | CHF |

| Producer and Import Prices M/M Apr | |

| Actual | 0.80% |

| Consensus | 0.10% |

| Previous | 0.20% |

| 06:30 | CHF |

| Producer and Import Prices Y/Y Apr | |

| Actual | -2.00% |

| Consensus | |

| Previous | -2.70% |

| 09:00 | EUR |

| Germany ZEW Economic Sentiment May | |

| Actual | -10.2 |

| Consensus | -20.5 |

| Previous | -17.2 |

| 09:00 | EUR |

| Germany ZEW Current Situation May | |

| Actual | -77.8 |

| Consensus | -77.5 |

| Previous | -73.7 |

| 09:00 | EUR |

| Eurozone ZEW Economic Sentiment May | |

| Actual | -9.1 |

| Consensus | -20 |

| Previous | -20.4 |

| 10:00 | USD |

| NFIB Business Optimism Index Apr | |

| Actual | 95.9 |

| Consensus | 96.1 |

| Previous | 95.8 |

| 12:30 | USD |

| CPI M/M Apr | |

| Actual | 0.60% |

| Consensus | 0.60% |

| Previous | 0.90% |

| 12:30 | USD |

| CPI Y/Y Apr | |

| Actual | 3.80% |

| Consensus | 3.70% |

| Previous | 3.30% |

| 12:30 | USD |

| CPI Core M/M Apr | |

| Actual | 0.40% |

| Consensus | 0.30% |

| Previous | 0.20% |

| 12:30 | USD |

| CPI Core Y/Y Apr | |

| Actual | 2.80% |

| Consensus | 2.70% |

| Previous | 2.60% |

Sunset Market Commentary

Markets

President Trump rebuffed Iran’s counterproposal to the US’ 14-point MoU of last week. Calling it “Totally unacceptable” suggests the water between both warring parties remains deep. Trump has threatened to resume a bombing campaign if Iran does not accept a deal but so far he has stopped short of actually doing so, despite the ongoing impasse. Iran meanwhile has deployed submarines in the Strait to act as “invisible guardians”. The Gulf crisis leaves marks on oil prices today, pushing up a barrel of Brent to $104 compared to a Friday close of $101.3. In a sign of the non-linear effects of the Hormuz closure, Saudi Arabia’s state-owned oil company Aramco said that if it continues into June, it will prolong the recovery to 2027. It is warning that the lack of supply will become more apparent from this month on. Bunds and Treasuries lose ground with the former underperforming. German rates add between 2.7-4.9 bps, led by the front end of the curve. Money markets are again erring to the side of three instead of two ECB hikes with a June move priced in for about 85%. US yields recover 3-4.2 bps from the minor declines printed end last week, keeping the 30-yr tenor within striking distance of the psychologically important 5% barrier. Gilts strongly underperform with rates rising 7.7-8.7 bps. Politics are entering the toxic cocktail which already consists of inflation and budgetary risk premia. PM Starmer during a speech today aimed at reviving Labour’s fortunes repeated that he won’t walk away from office. There were no calls for an immediate resignation, at least not from those Labour members who are seen as a viable successor. Starmer lives to fight another day but his political survival is hanging by a thread. The 30-yr UK yield (5.67%), most sensitive to rising risk premia, is closing in on the 1998 high set just last week (5.78%). Sterling shrugs around EUR/GBP 0.865. The dollar has a slight upper hand against most G10 peers but trading is technically insignificant. EUR/USD trades around 1.178, DXY around 98. USD/JPY rises to 157.1, awaiting the arrival of USTS Bessent when taking a detour en route to China together with president Trump later this week. European stock markets lose some ground to the tune of 0.3%. Wall Street opens the new trading week virtually unchanged.

News & Views

Inflation in Norway stayed elevated in April. Headline CPI rose 0.4% M/M and 3.4% Y/Y (from 3.6%). Underlying CPI-ATE inflation (ex-energy and adjusted for tax changes) rose 0.7% M/M and 3.2% Y/Y (from 3%). Food and drinks (+2.9%, potential calendar effect), clothing and footwear (+1.4%) and culture and leisure showed the biggest monthly changes rise. Prices for household equipment (-0.8%), transportation (-0.4%) and communications (-1.0%) eased on a monthly basis. The April 3%+ inflation figures come after the Norges Bank last week raised its policy rate by 25 bps to 4.25%. The NB explained the decision as inflation already being high when the increase in oil and gas prisses due to the conflict in the Middle East can push it even higher. Wage growth also was higher than the NB previously assumed. The NB last week also indicated that recent data/developments didn’t change the assessment from the outlook set out in March that the policy rate might be raised to between 4.25% and 4.5% by the end of the year. Also today’s inflation data probably don’t change this assessment. Markets currently see about a 50% chance of a next 25 bps step in June and a more than fully discounted one in September. At EUR/NOK 10.84, the krone is holding within reach of the strongest levels against the euro since early 2023.

Referring to its April Business survey, IFO reported that 8.1% of companies in Germany see their own survival at risk. In a comment, IFO Survey’s head Klaus Wohlrabe analysis that given the geopolitical uncertainty and insolvency figures are likely to remain a high level in the coming months. Especially the situation in retail is seen as being critical with 17.4% (new high) of the companies considering their survival under threat. 11.6% of all trading companies (wholesale and retail) are said to fear being forced out of business. In a broader perspective, across sectors, IFO sees a lack of orders and weak demand, rising operating and energy costs and burdensome bureaucracy as weighing on activity, with the crisis spreading along supply chains. Among service providers, 7.6% see their survival threatened. In manufacturing, the threat to survival fell slightly to 7.5%.

The Labour Market Failed to Boost the Dollar

- Strong US employment figures were not enough to prevent the dollar from falling.

- Geopolitics and risk appetite remain the key drivers.

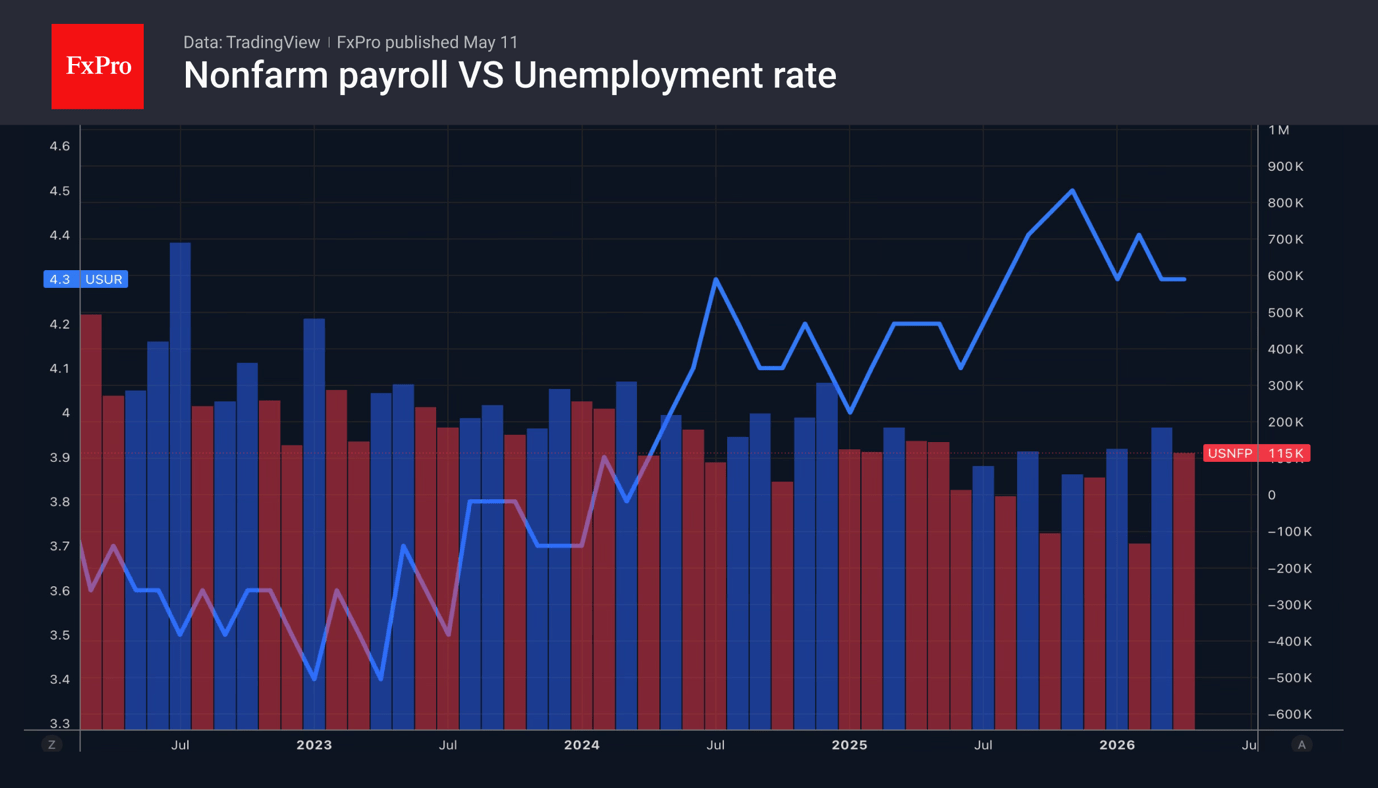

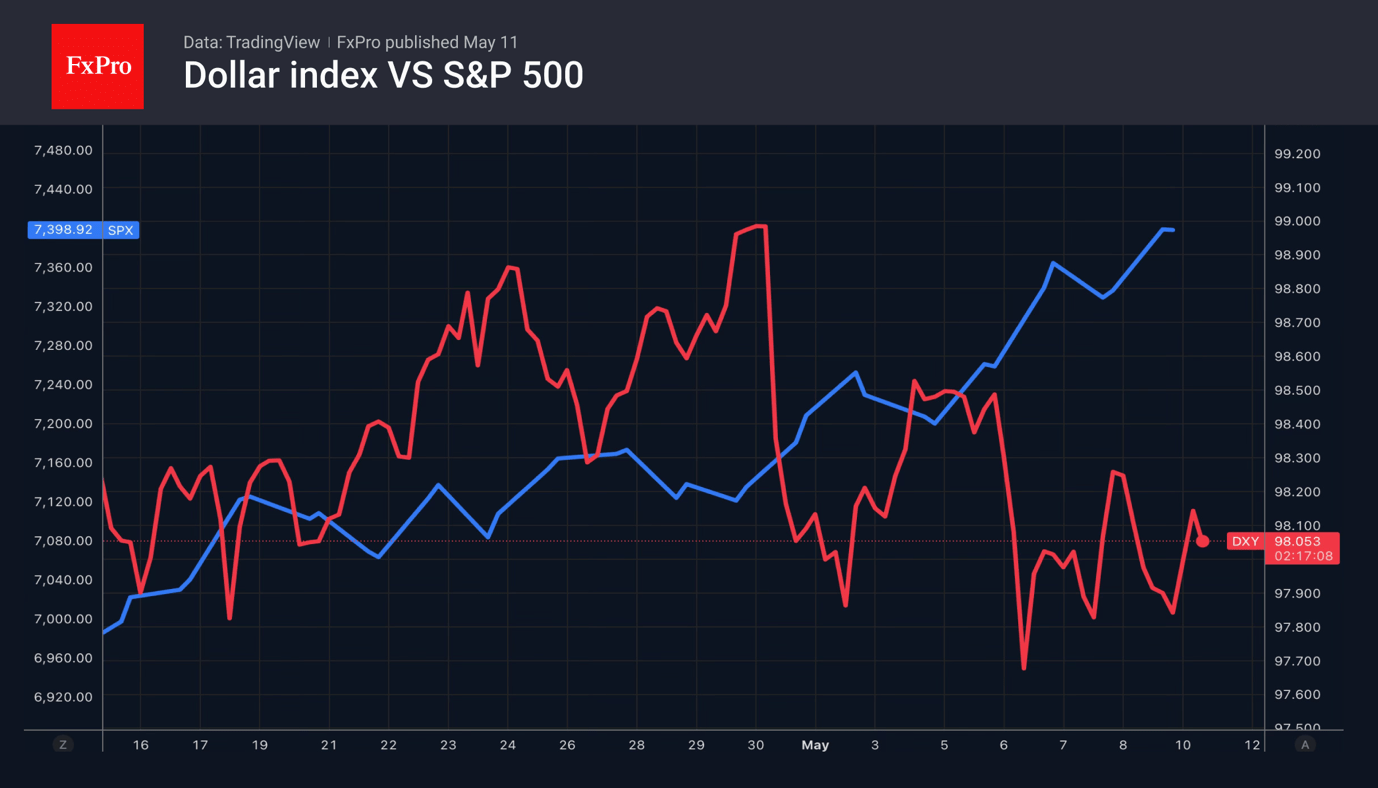

The US dollar came under pressure from sellers on Friday, and a strong labour market report failed to reverse the trend, merely slowing the pace of the decline. Non-farm payrolls rose by 115K in April, almost doubling expectations thanks to strong hiring in the private sector (+123K). Unemployment remained at 4.3%. Although wage growth accelerated from 3.4% y/y to 3.6%, this was below the forecast of 3.8%. The labour market is not showing any signs of distress.

Strong economic data has pushed futures markets to increase the probability of the Fed tightening monetary policy in 2026 from 14% to 21%. Meanwhile, expectations for a rate cut have dropped from 12% to just 6%. Normally, this would support the US dollar, but the market appears to be focused elsewhere.

One reason is the reduced demand for the dollar as a safe-haven asset. Investors continued buying into the S&P 500, boosting demand for US assets and creating a “Goldilocks” style environment, where economic growth slows but remains resilient enough to support risk appetite. At the same time, markets were also closely watching negotiations between Washington and Tehran.

To the markets’ disappointment, Iran rejected the Americans’ proposals and put forward its own conditions. Donald Trump considers them completely unacceptable and intends to resume Operation Inherent Resolve. A week earlier, he provoked Tehran’s anger and an escalation of the geopolitical conflict. History now risks repeating itself. In addition, the escalation of the situation in the Middle East will boost demand for the US dollar as a safe-haven asset.

That said, there is still a glimmer of hope for a peaceful resolution to the conflict. Neither Washington nor Tehran has yet to announce that talks will not take place. Moreover, there is a chance that the meeting between Donald Trump and Xi Jinping will be followed by pressure on Iran—at the very least, psychological pressure.

Rising oil prices and fears of accelerating US inflation in April forced gold to take a step back after several days of gains. As long as consumer prices remain high, central banks, led by the Fed, will continue to consider raising interest rates. In such conditions, the non-interest-bearing precious metal finds itself in an uncomfortable position.

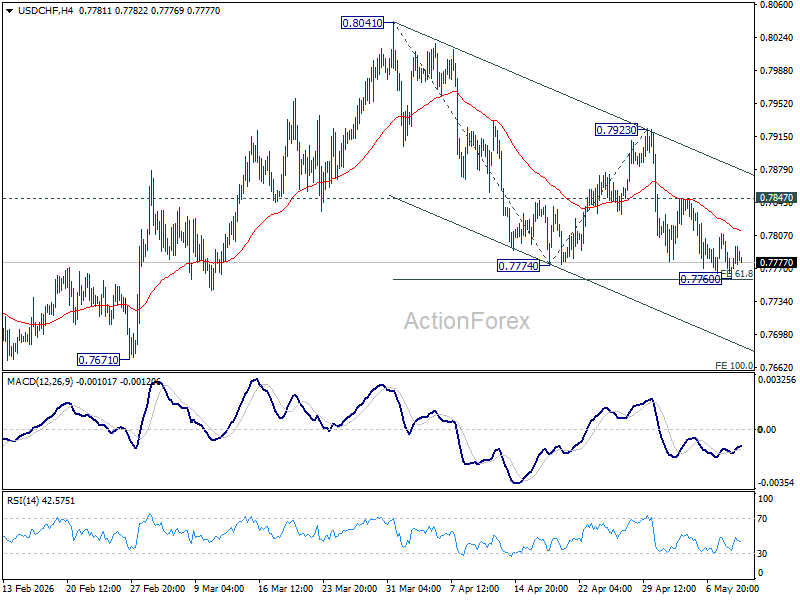

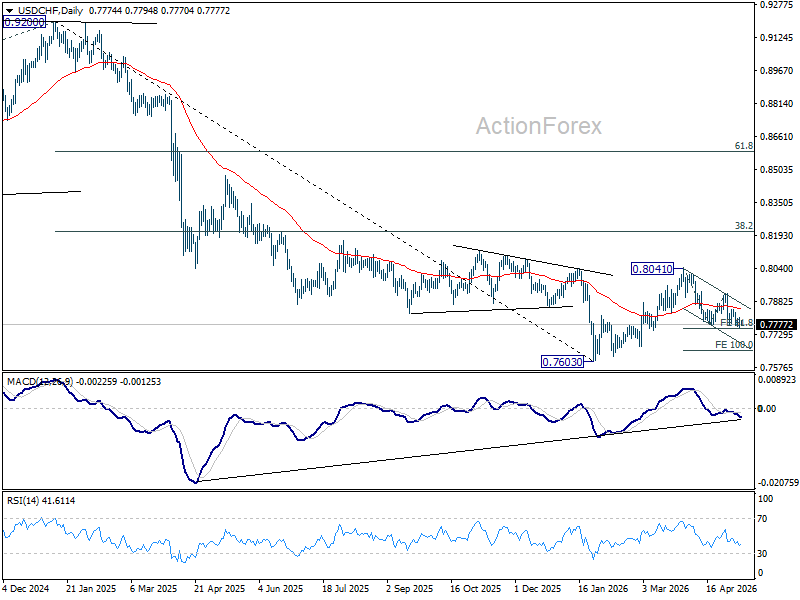

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7746; (P) 0.7777; (R1) 0.7793; More….

Intraday bias in USD/CHF remains neutral for consolidations above 0.7760. On the downside, decisive break of 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758 will resume the whole decline form 0.8041, and target 100% projection at 0.7656. However, firm break of 0.7847 resistance will indicate short term bottoming, and bring stronger rebound back to 0.7923 resistance.

In the bigger picture, as long as 55 W EMA (now at 0.8051) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

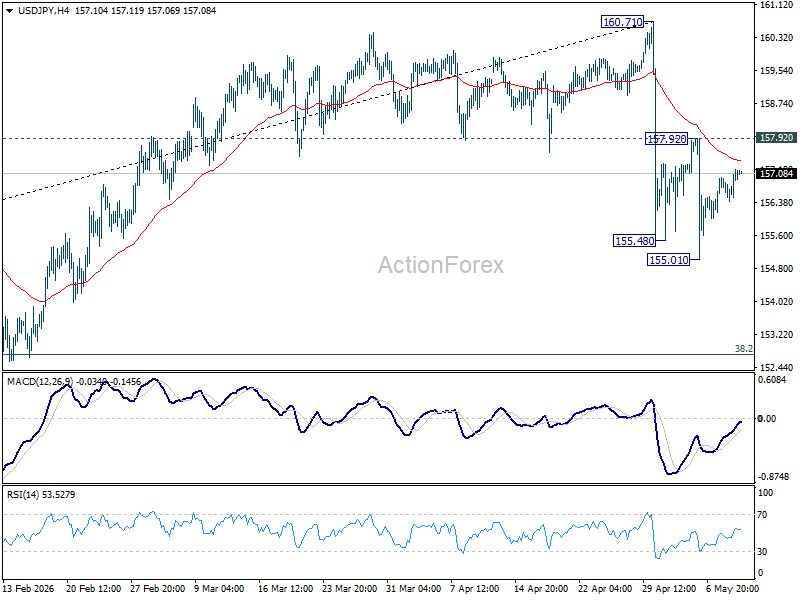

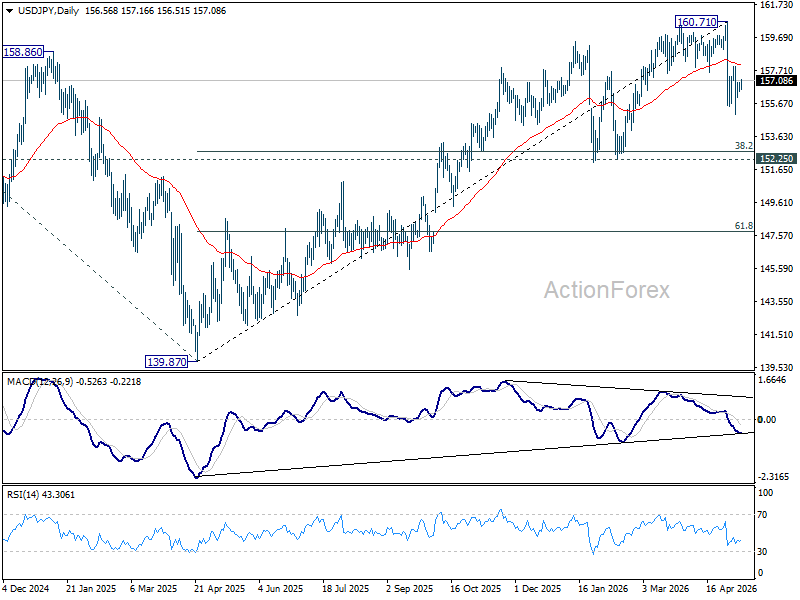

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.41; (P) 156.69; (R1) 156.97; More...

Intraday bias in USD/JPY stays neutral and outlook is unchanged. On the downside, break of 155.01 will resume the fall from 160.71 to 152.25 support next. On the upside, however, firm break of 157.92 will indicate that pullback from 160.71 has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.13) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

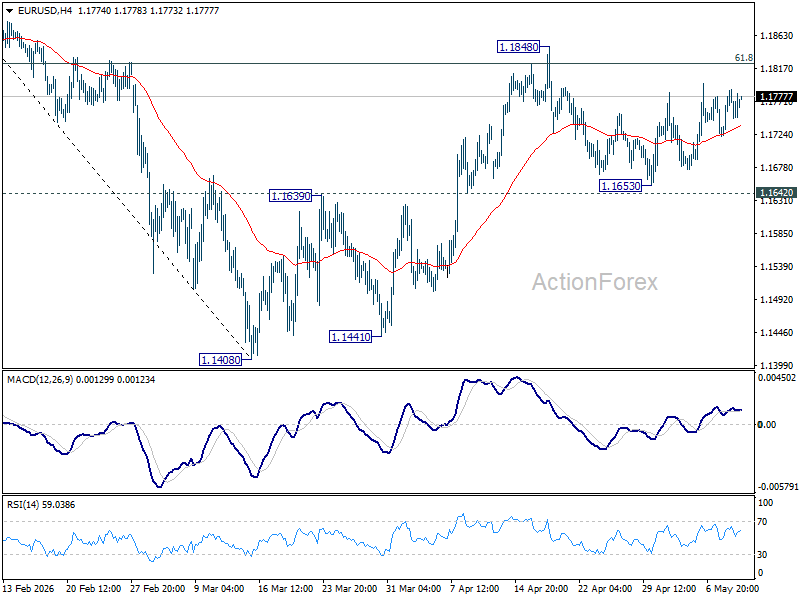

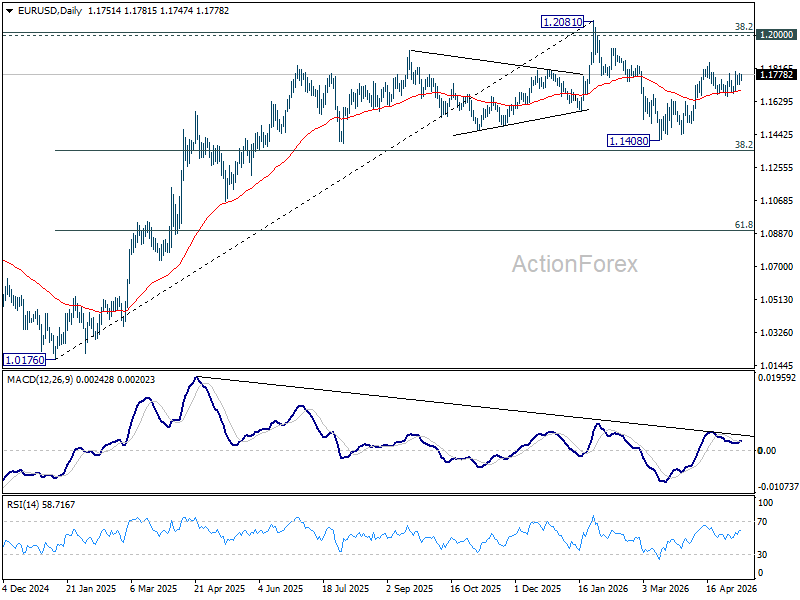

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1740; (P) 1.1764; (R1) 1.1806; More….

Intraday bias in EUR/USD stays neutral as sideway trading continues. Further rise is expected with 1.1642 support intact. On the upside, firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1539). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

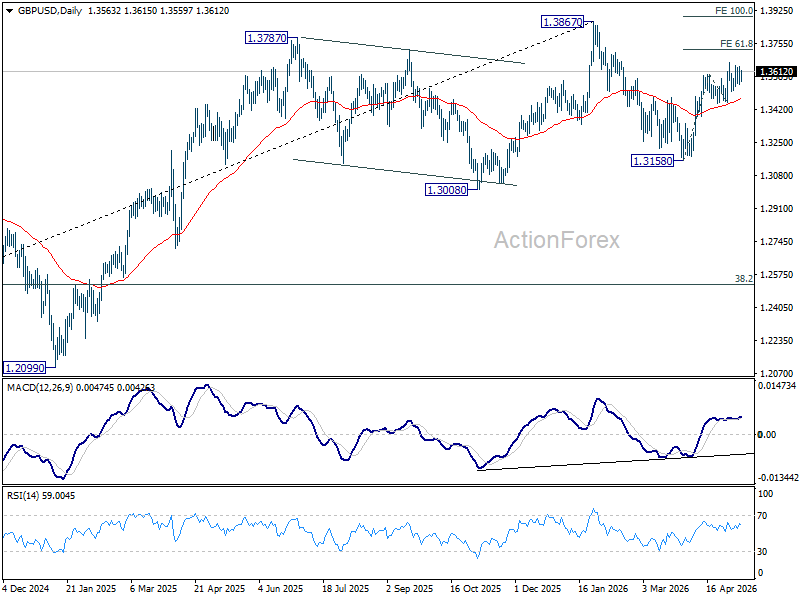

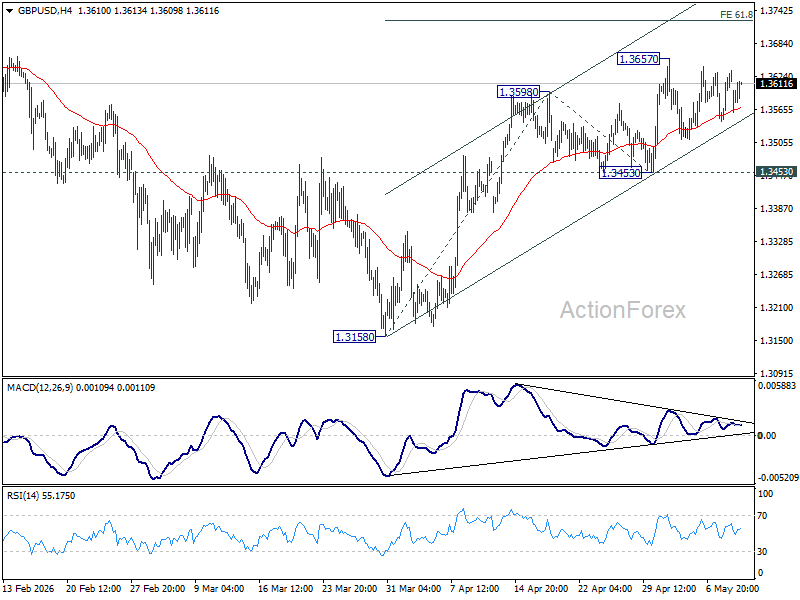

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3568; (P) 1.3602; (R1) 1.3659; More...

Range trading continues in GBP/USD and intraday bias stays neutral for the moment. With 1.3453 support intact, further rise is expected. On the upside, break of 1.3657 will target 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).