Sample Category Title

Markets Ignore Geopolitical Risks, Chase AI Rally, and Dump Dollar

Markets spent last week aggressively chasing the AI-driven equity rally while largely ignoring geopolitical tensions in the Middle East. Despite renewed uncertainty over a promised peace deal, stocks surged to new records while Dollar weakened broadly on strong risk appetite. S&P 500 followed NASDAQ to fresh records, while Asia’s major technology-heavy benchmarks exploded higher as well. Japan’s Nikkei, South Korea’s KOSPI, and Taiwan’s TAIEX all surged to new highs as investors doubled down on semiconductor and AI infrastructure themes.

At the same time, the rally underneath the surface was far less broad than headline indices suggested. Traditional industrial and cyclical sectors lagged badly. DOW struggled to break above the 50,000 level, FTSE drifted sideways, and Germany’s DAX actually weakened under the weight of fresh US tariff threats targeting European autos. Investors were not buying “the economy.” They were buying AI.

That distinction is important because it explains the market’s remarkable “geopolitical indifference” throughout the week. Traders appeared willing to ignore Middle East risks unless they directly threatened the AI growth story or caused a full-scale oil shock capable of destabilizing global markets.

Indeed, investors spent much of Thursday and Friday positioning for a potential “peace dividend” after reports suggested Washington and Tehran were discussing a 30-day framework to reopen the Strait of Hormuz. Oil prices fell sharply as traders priced the possibility that commercial shipping could normalize and that Iran might back away from its increasingly aggressive chokepoint strategy.

But reality quickly complicated the optimism. Iranian officials publicly rejected Washington’s timelines for accepting the proposal, while US Central Command confirmed American forces had conducted “self-defense strikes” against Iranian-linked ports after destroyers came under attack in Hormuz.

That disconnect may be the single most important signal from last week. Markets are not reacting to geopolitical instability the way they would earlier in the year. Investors increasingly appear convinced that AI-driven earnings growth and liquidity momentum can absorb almost any macro shock short of outright regional war.

Dollar’s performance captured that shift perfectly. Normally, a week featuring military clashes in Hormuz and a stronger-than-expected US payrolls report would have fueled broad Dollar strength. Instead, the greenback weakened sharply as traders continued rotating into risk-sensitive currencies and equities.

The jobs report itself actually strengthened the bullish macro narrative. April payrolls came in far stronger than expected, confirming that March’s strength was not simply a one-off surprise. At the same time, wage growth remained relatively tame, reinforcing the “Goldilocks” idea that the economy is resilient enough to avoid recession while inflation pressures remain manageable enough for the Federal Reserve to comfortably stay on hold.

That combination effectively removed two major market fears simultaneously: recession panic and hawkish Fed panic. Once those risks faded, investors simply returned to chasing the strongest momentum theme available — AI.

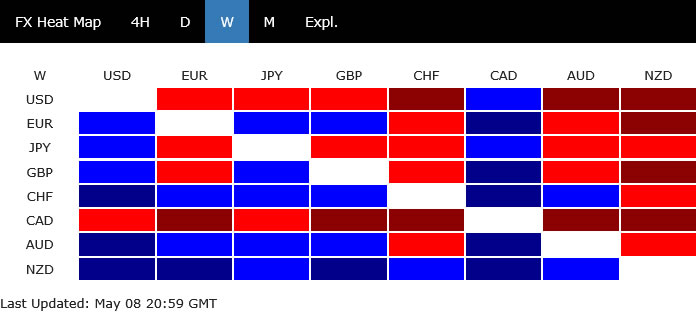

Currency markets reflected that same dynamic. Kiwi and Aussie led gains as Asia’s tech and semiconductor optimism intensified, while Dollar and Yen underperformed amid the broader risk-on environment. Canadian Dollar was hit especially hard as collapsing oil prices and weak domestic labor data undermined the case for Bank of Canada tightening.

The real question now is whether markets have become too comfortable dismissing geopolitical danger altogether. Heading into the weekend, investors are effectively betting that some form of US-Iran agreement will eventually emerge and prevent a full-blown Hormuz catastrophe. For now, traders appear willing to look past the risks and keep chasing the AI-driven rally, leaving Dollar under pressure — at least until those assumptions are proven wrong.

Weekly Currency Performance (May 4 – May 8, 2026)

| Rank | Currency | Performance Driver |

|---|---|---|

| 1 | NZD | Strong risk-on sentiment, AI-led Asia rally |

| 2 | CHF | The odd one out, supported by softer global yields |

| 3 | AUD | Benefited from Asian equity surge and improved risk appetite |

| 4 | EUR | Supported by broad Dollar weakness, capped by tariff concerns |

| 5 | GBP | Neutral performance amid UK political uncertainty |

| 6 | JPY | Intervention effects faded; pressured by risk-on environment |

| 7 | USD | Weakened despite strong NFP as risk appetite dominated |

| 8 | CAD | Hit by oil price decline and weak domestic employment data |

NASDAQ Nears Key Projection as AI Rally Accelerates

NASDAQ’s powerful uptrend extended again last week, bringing the index within striking distance of 61.8% projection of 14,784 to 24,019 from 20,690 at 26,398. The AI-driven rally continues to dominate global equity markets, with momentum remaining firmly bullish for now.

However, technical conditions are becoming stretched. Daily RSI remains in overbought territory, suggesting upside momentum could begin fading after the 26,398 level and especially as NASDAQ approaches the medium-term rising channel ceiling, currently near 27,142. A break below 25495 support would be the first indication of a short-term top and likely trigger a period of consolidation.

Still, there is no confirmed reversal signal yet. If NASDAQ decisively breaks above the channel resistance, the rally could enter another acceleration phase, opening the way toward 100% projection at 29,926.

Nikkei Rally Faces Channel Resistance After Record Run

Japan’s Nikkei also extended its strong uptrend last week and is now pressing against medium-term channel resistance. The rally has been fueled by the global AI boom, semiconductor demand, and renewed foreign inflows into Japanese equities.

Short-term conditions are becoming overbought, as reflected in D RSI readings, suggesting the index could struggle to sustain the same pace of gains near current levels. Some pullback or consolidation would not be surprising as the market tests the upper boundary of the channel.

Nevertheless, outlook remains bullish as long as 58,928 support holds. Firm breakout above channel resistance would signal renewed upside acceleration and could quickly drive Nikkei toward 61.8% projection of 53,590 to 59,332 from 50,558 at 68,196.

Dollar Index Remains Under Pressure Despite Stabilization

Dollar Index gyrated lower last week but managed to stay above the 97.63 support. The broader technical outlook remains unchanged, with the rebound from 95.55 likely completed at 100.64, just below 38.2% retracement of 110.17 to 95.55 at 101.13.

Further downside remains favored while 99.34 resistance caps recovery attempts. Decisive break below 97.63 would pave the way for another test of 95.55 low.

For now, there is still uncertainty over whether the corrective structure from 95.55 could evolve into a more complex consolidation with another rebound leg. However, a firm break below 95.55 would confirm resumption of the broader downtrend from both the 101.17 (2025 high) and the 114.77 (2022 peak).

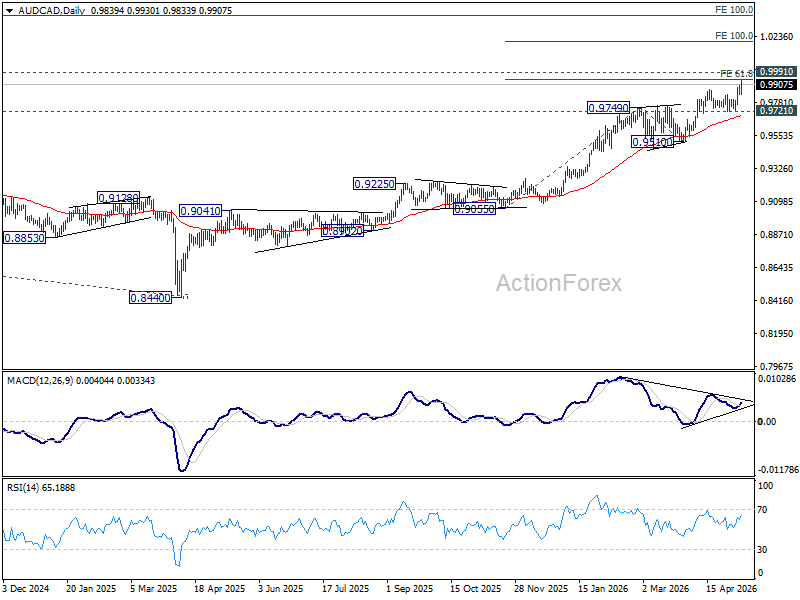

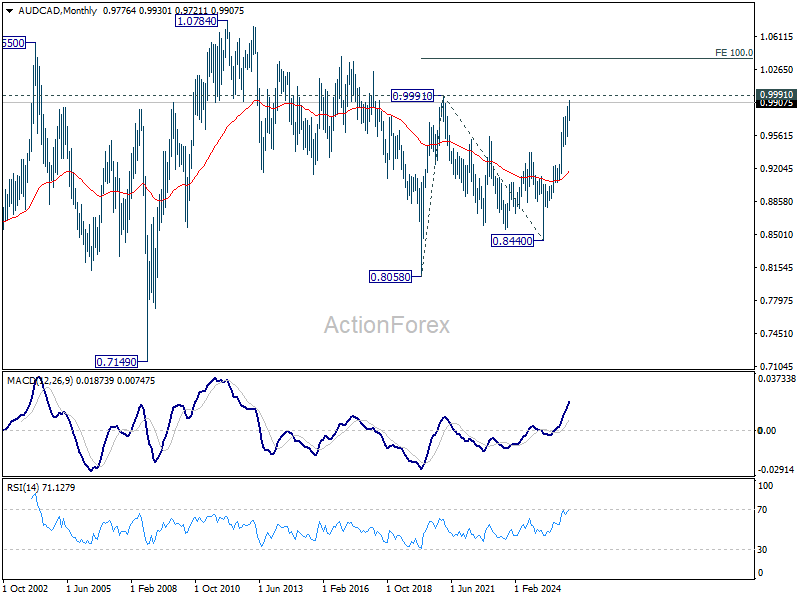

AUD/CAD Targets Parity on RBA-BoC Policy Divergence

Aussie surged strongly last week after RBA delivered another hawkish rate hike to 4.35% and signaled in updated projections that the cash rate could eventually rise toward 4.7%. The guidance reinforced expectations that Australia’s tightening cycle is not yet complete.

In contrast, weak Canadian employment data sharply reduced expectations for any near-term Bank of Canada tightening despite Governor Tiff Macklem’s warnings about inflation risks. Combined with falling oil prices, the softer Canadian outlook added further support to AUD/CAD’s bullish trend.

Technically, AUD/CAD is on track to retest the key 0.9991 resistance (2021 high) with parity coming into view. While some resistance could emerge on the first attempt, a decisive break above parity would likely trigger another wave of upside acceleration toward 100% projection of 0.9055 to 0.9749 from 0.9510 at 1.0204. In any case, near term outlook will stay bullish as long as 0.9721 support holds.

More importantly, sustained break above 0.9991 would confirm resumption of the broader uptrend from the 0.8058 (2020 low). In that scenario, the next medium-term target would come in at 100% projection of 0.8058 to 0.9991 from 0.8440 at 1.0373.

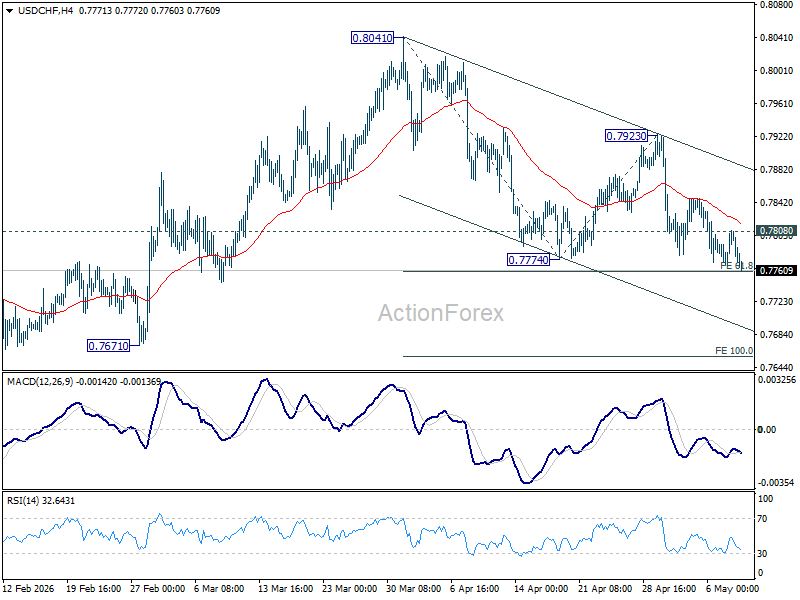

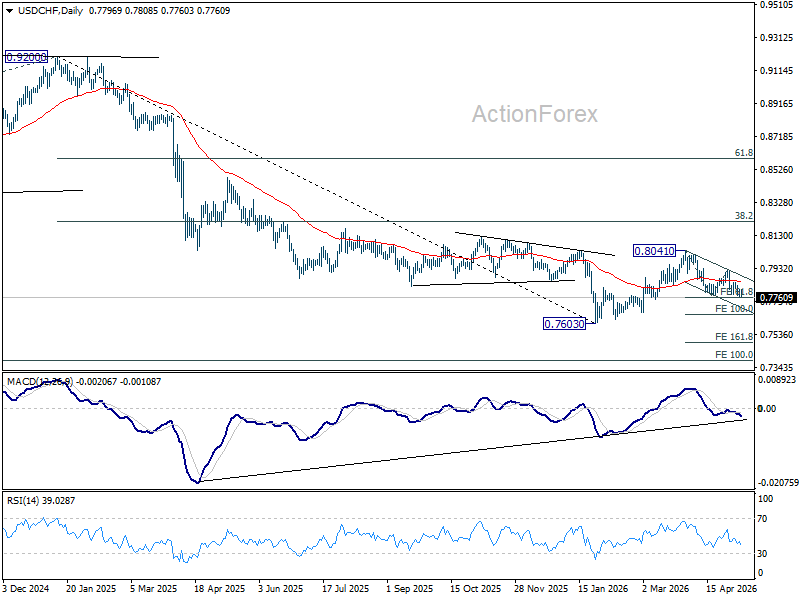

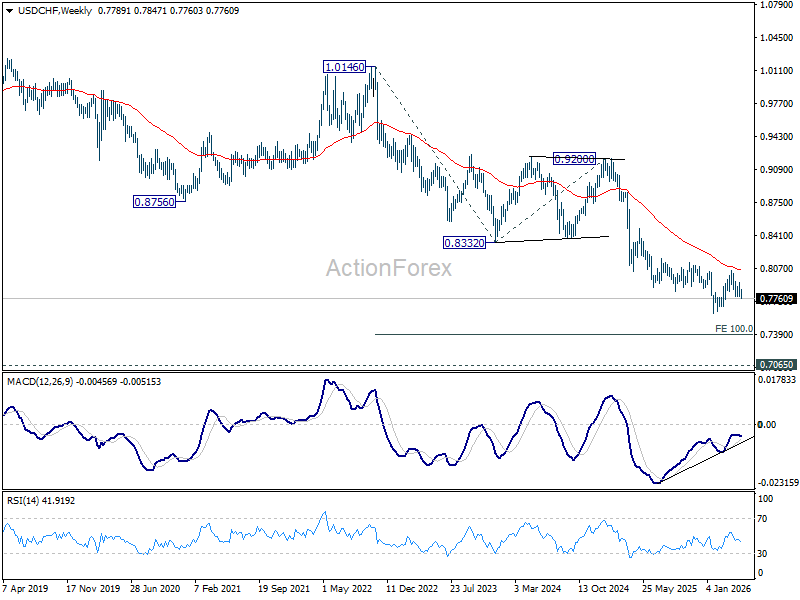

USD/CHF Weekly Outlook

USD/CHF's decline from 0.8041 resumed last week. Initial bias stays on the downside this week. Firm break of 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758 will target 100% projection at 0.7656. On the upside, above 0.7808 minor resistance will turn intraday bias neutral again first.

In the bigger picture, as long as 55 W EMA (now at 0.8051) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

In the long term picture, price action from 0.7065 (2011 low) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). It's uncertain if the fall from 1.0342 is the second leg of the pattern, or resumption of the downtrend. But in either case, outlook will stay bearish as long as 0.8756 support turned resistance holds (2021 low). Retest of 0.7065 should be seen next.

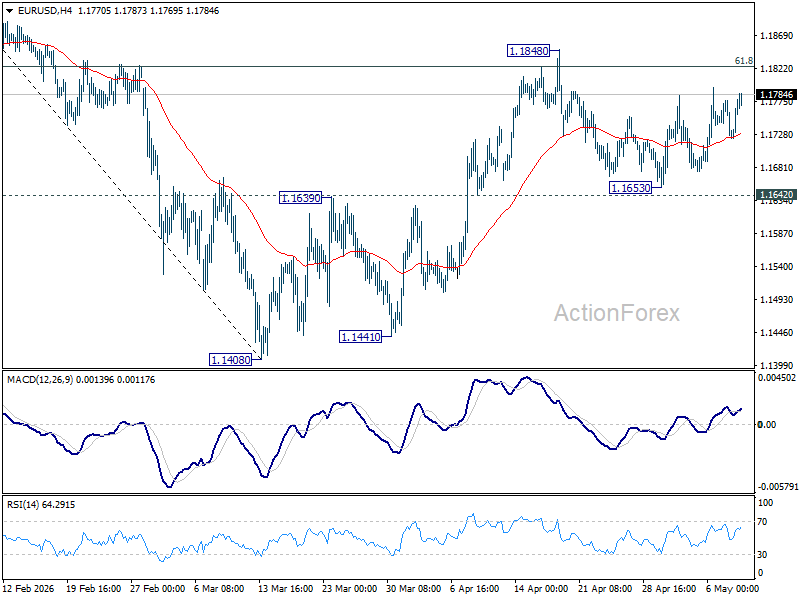

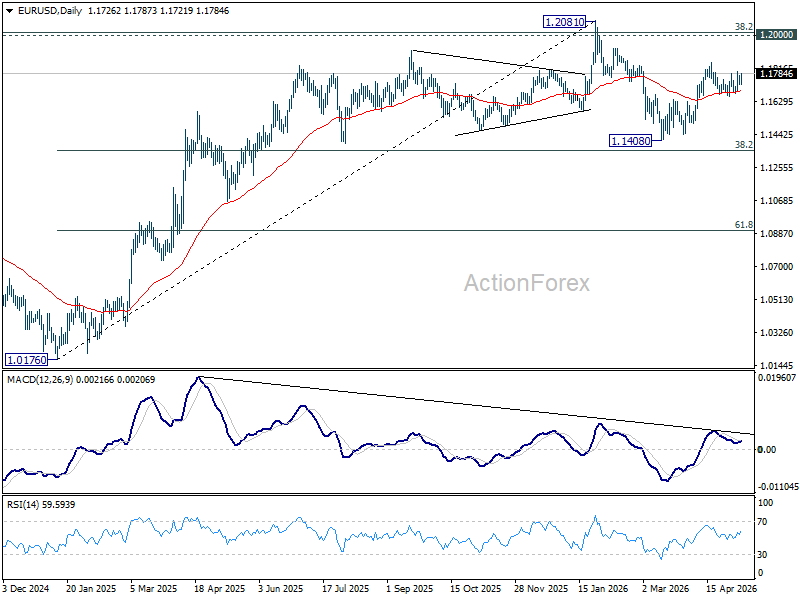

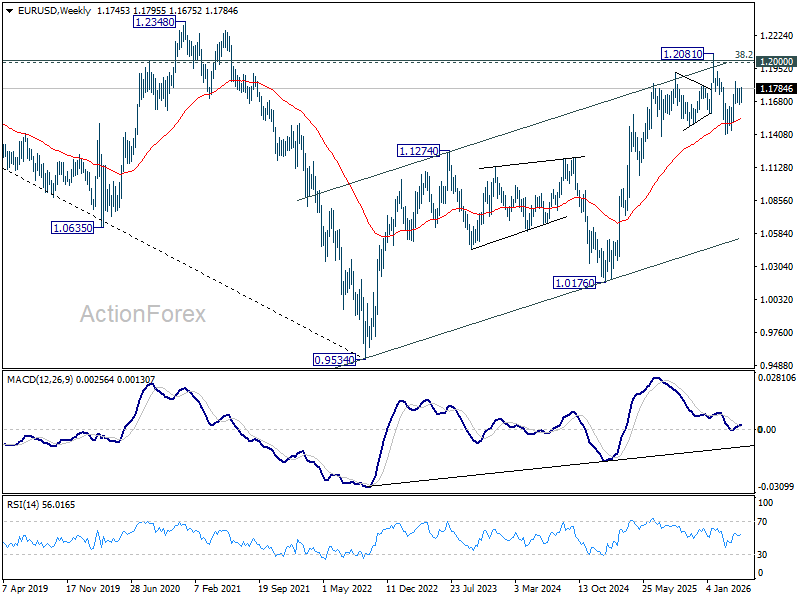

EUR/USD Weekly Outlook

EUR/USD stayed in range below 1.1848 last week and outlook is unchanged. Initial bias remains neutral, and further rise is expected with 1.1642 support intact. On the upside, firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1530). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

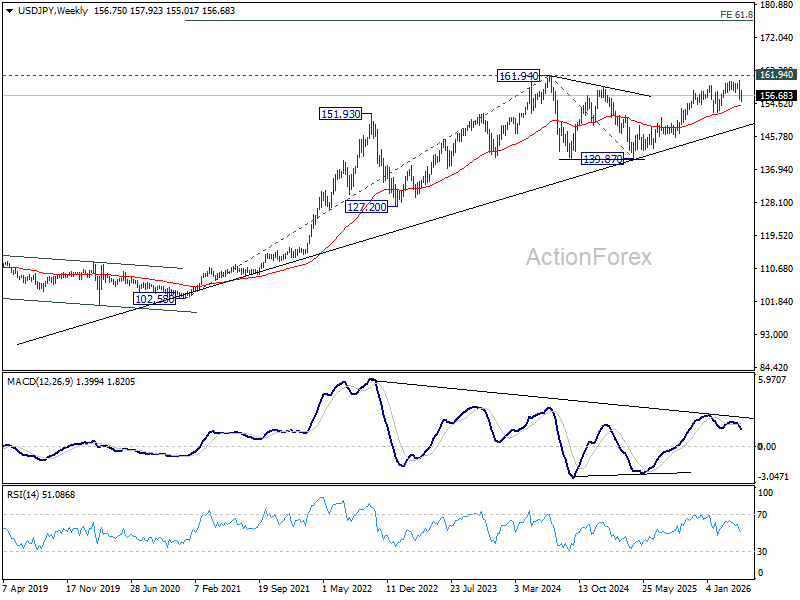

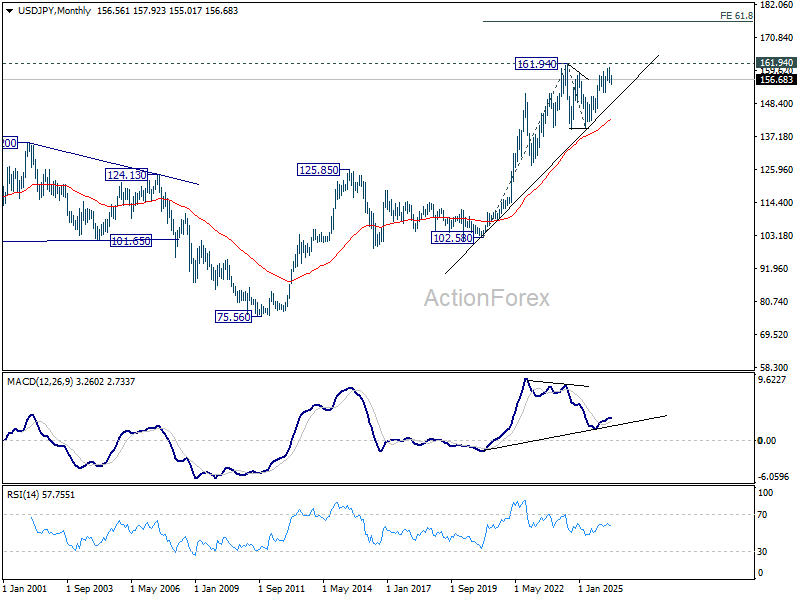

USD/JPY Weekly Outlook

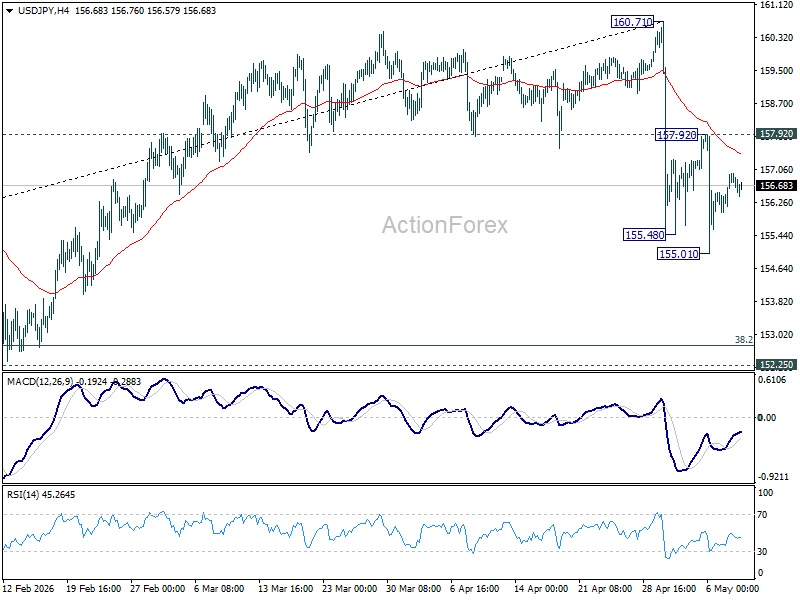

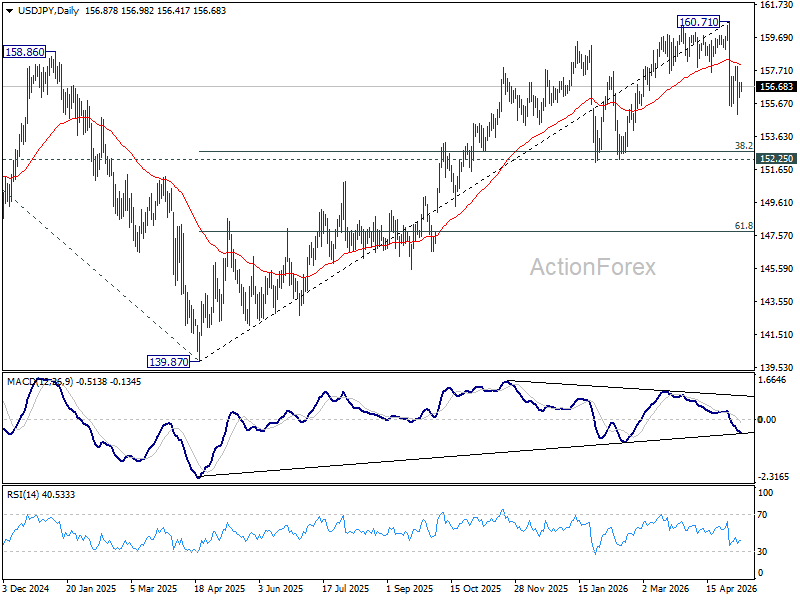

USD/JPY dipped to 155.01 last week but recovered since then. Initial bias stays neutral this week first. On the downside, break of 155.01 will resume the fall from 160.71 to 152.25 support next. On the upside, however, firm break of 157.92 will indicate that pullback from 160.71 has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.02) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

In the long term picture, up trend from 75.56 (2011 low) is still in progress and might be ready to resume. Firm break of 161.94 will target 61.8% projection of 102.58 (2020 low) to 161.94 (2024 high) from 139.87 at 176.55 in the medium term. Long term outlook will stay bullish as long as 139.87 support holds, even in case of deep pullback.

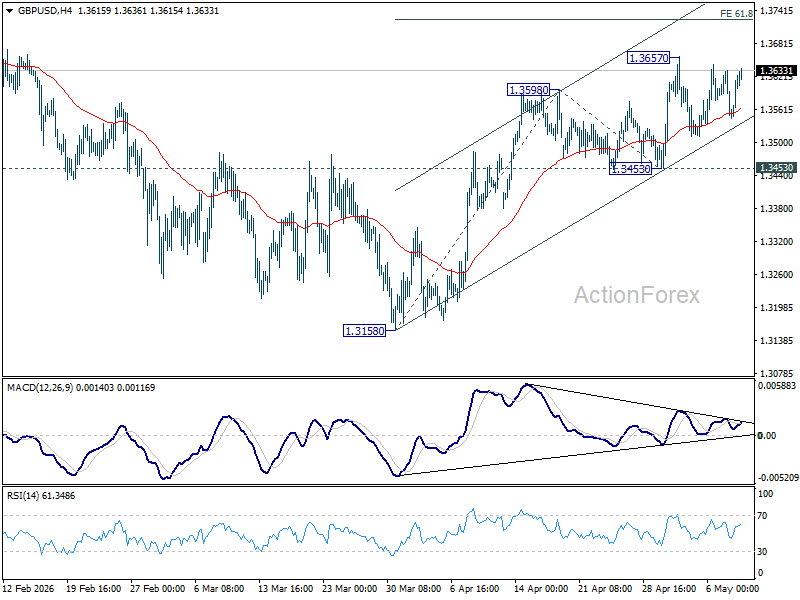

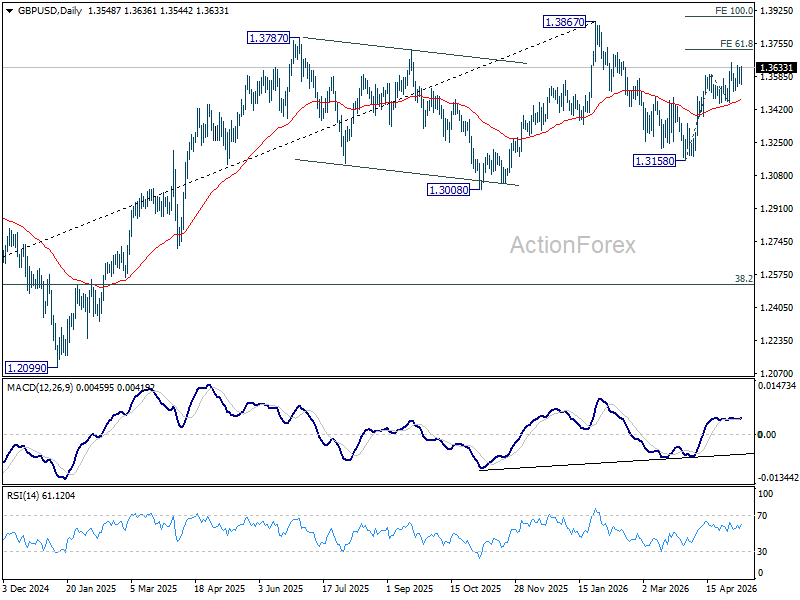

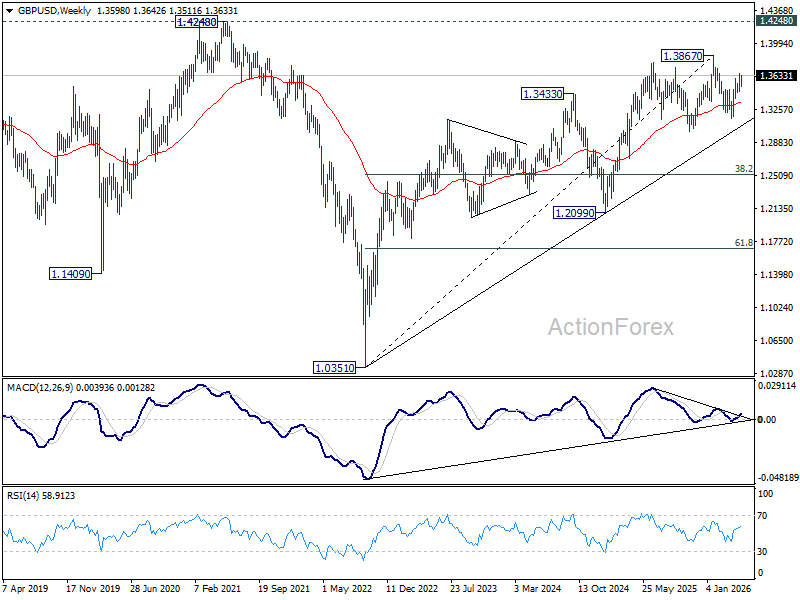

GBP/USD Weekly Outlook

GBP/USD stayed in range trading below 1.3657 last week and outlook is unchanged. Initial bias remains neutral for consolidations, and further rise is expected with 1.3453 support intact. On the upside, break of 1.3657 will target 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).

In the long term picture, as long as 1.4248/4480 resistance zone holds (38.2% retracement of 2.1161 to 1.0351 at 1.4480), the long term outlook will remain bearish. That is, price actions from 1.0351 are seen as a corrective pattern to down trend from 2.1161 (2007 high) only. Nevertheless, decisive break of 1.4248/4480 will be a strong sign of long term bullish reversal.

USD/CHF Weekly Outlook

USD/CHF's decline from 0.8041 resumed last week. Initial bias stays on the downside this week. Firm break of 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758 will target 100% projection at 0.7656. On the upside, above 0.7808 minor resistance will turn intraday bias neutral again first.

In the bigger picture, as long as 55 W EMA (now at 0.8051) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

In the long term picture, price action from 0.7065 (2011 low) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). It's uncertain if the fall from 1.0342 is the second leg of the pattern, or resumption of the downtrend. But in either case, outlook will stay bearish as long as 0.8756 support turned resistance holds (2021 low). Retest of 0.7065 should be seen next.

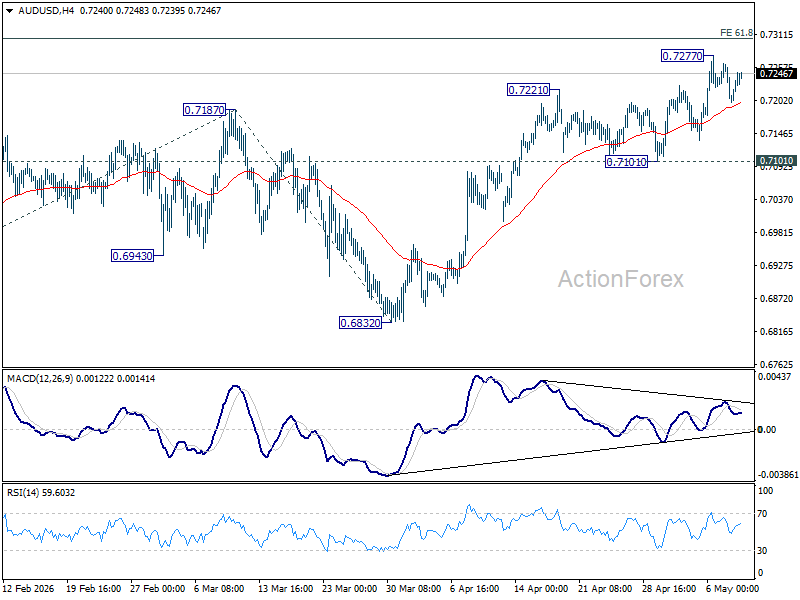

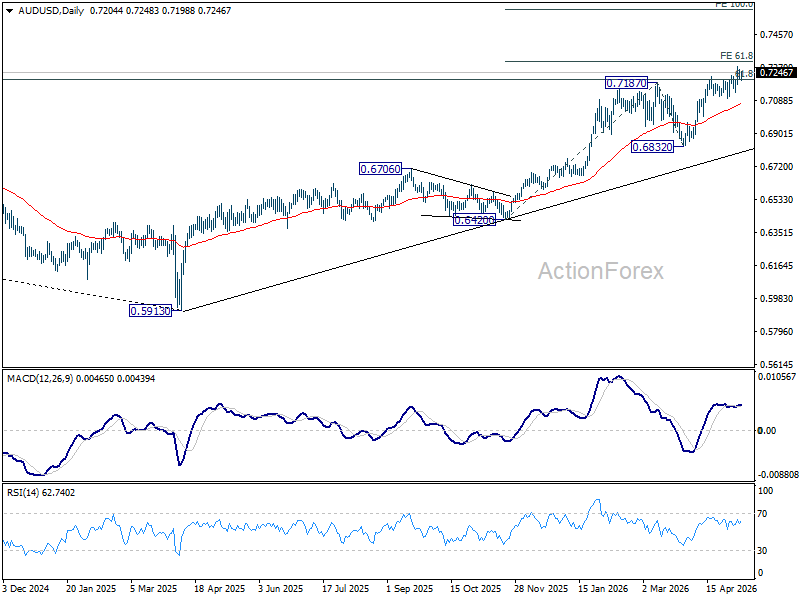

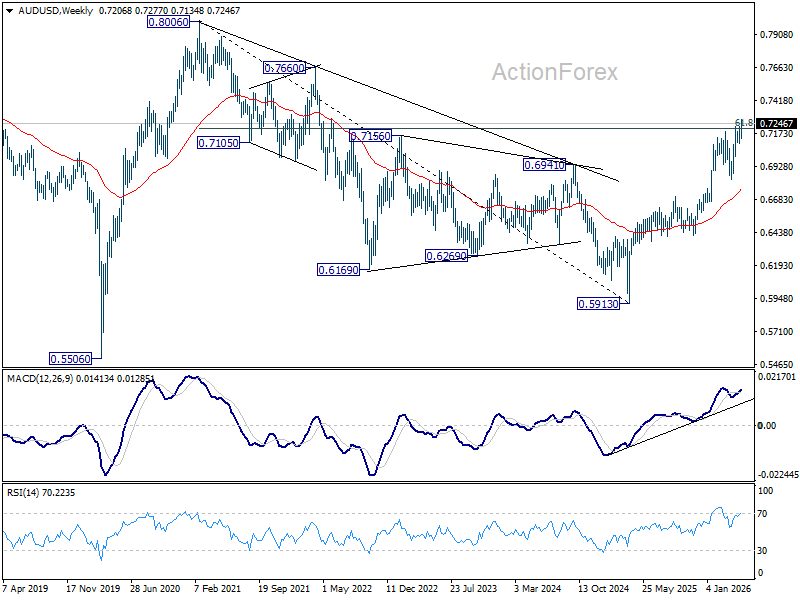

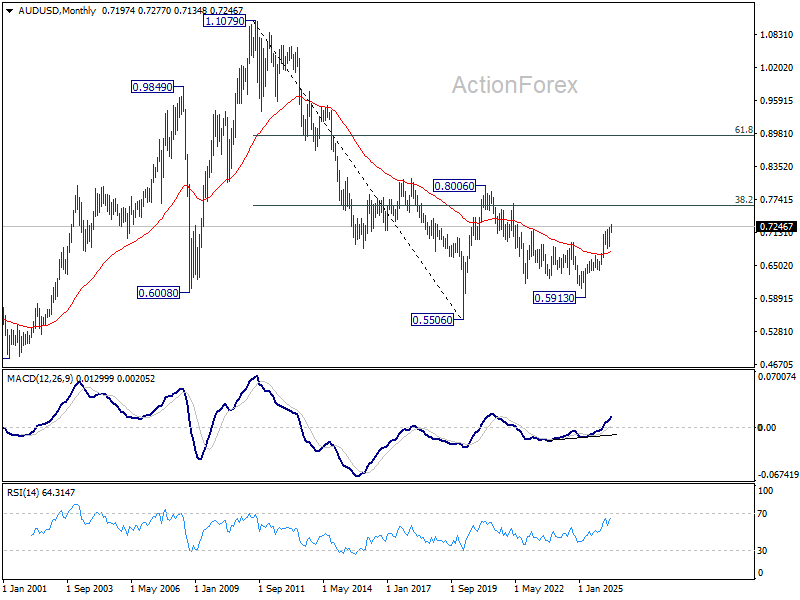

AUD/USD Weekly Report

AUD/USD edged higher to 0.7277 last week as up trend continued, but retreated since then. Initial bias remains neutral this week for consolidations. Further rise is expected as long as 0.7101 support holds. Above 0.7277 will target 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.

In the long term picture, rise from 0.5913 is seen as the third leg of the whole pattern from 0.5506 (2020 low). It's still early to judge if this is an impulsive or corrective pattern. But in either case, further rise should be seen back to 0.8006 and possibly above. This will remain the favored case as long as 55 W EMA (now at 0.6730) holds.

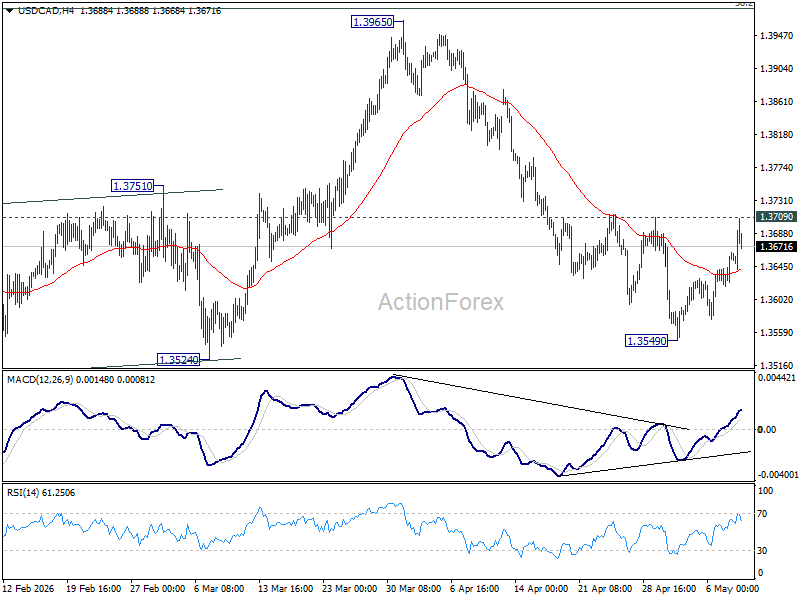

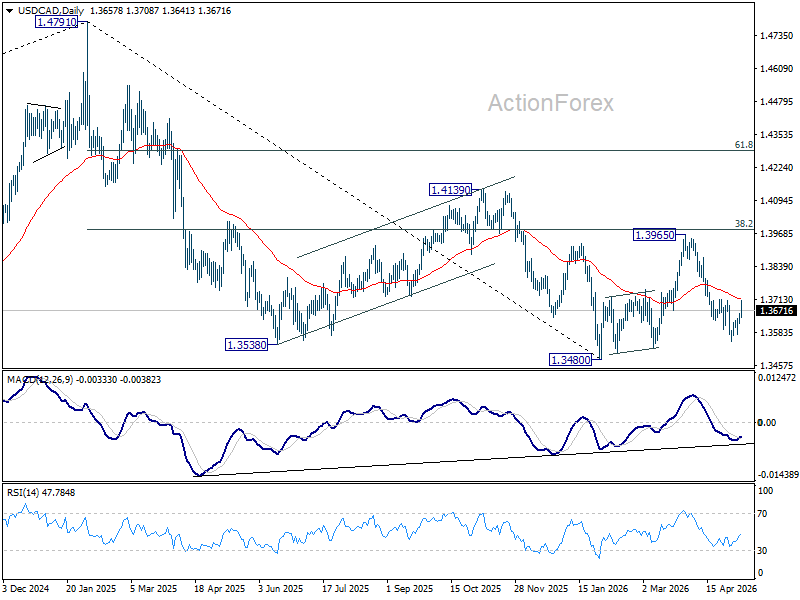

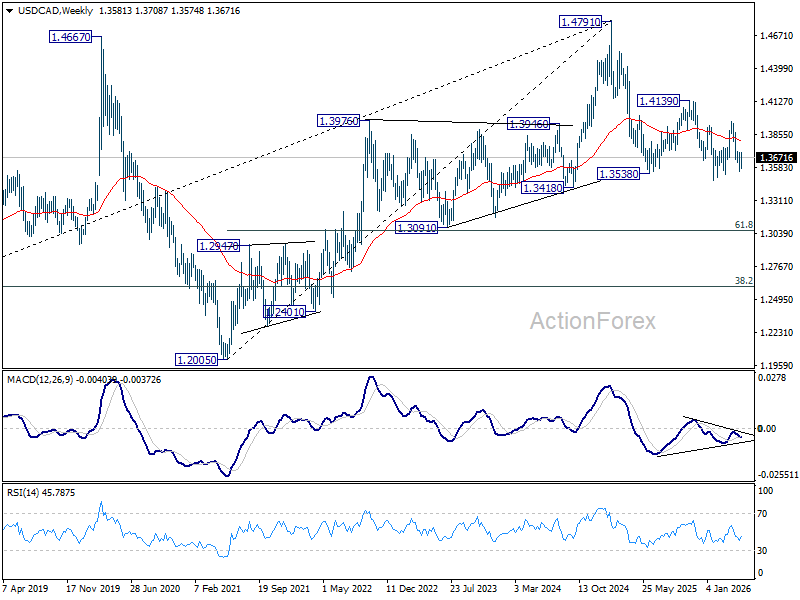

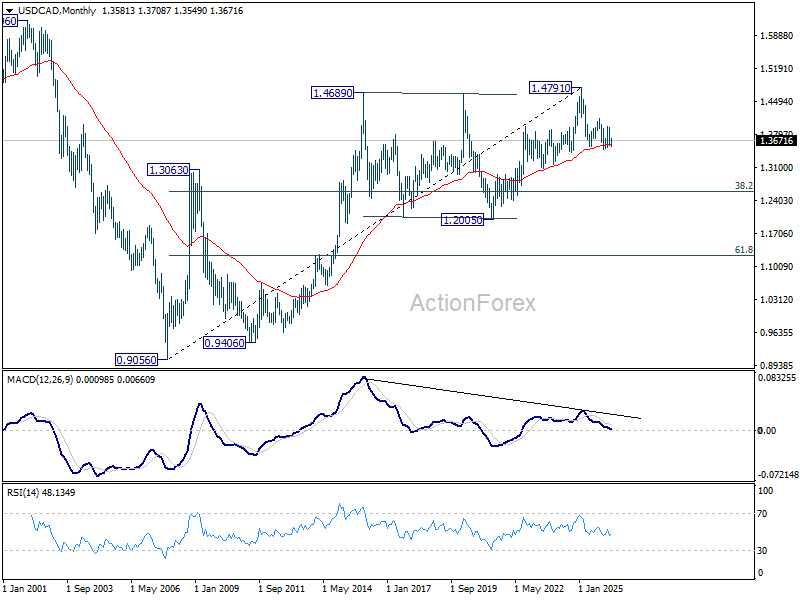

USD/CAD Weekly Outlook

USD/CAD recovered last week but upside is capped by 1.3709 resistance. Initial bias remains neutral this week first. On the downside, below 1.3549 will extend the fall from 1.3965 to retest 1.3480 low. Decisive break there will resume whole down trend from 1.4791. However, sustained break of 1.3709 will confirm short term bottoming, and turn bias back to the upside for 1.3965 resistance again.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already.

In the long term picture, rising 55 M EMA (now at 1.3581) remains intact. Thus, up trend from 0.9056 (2007 low) could still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.

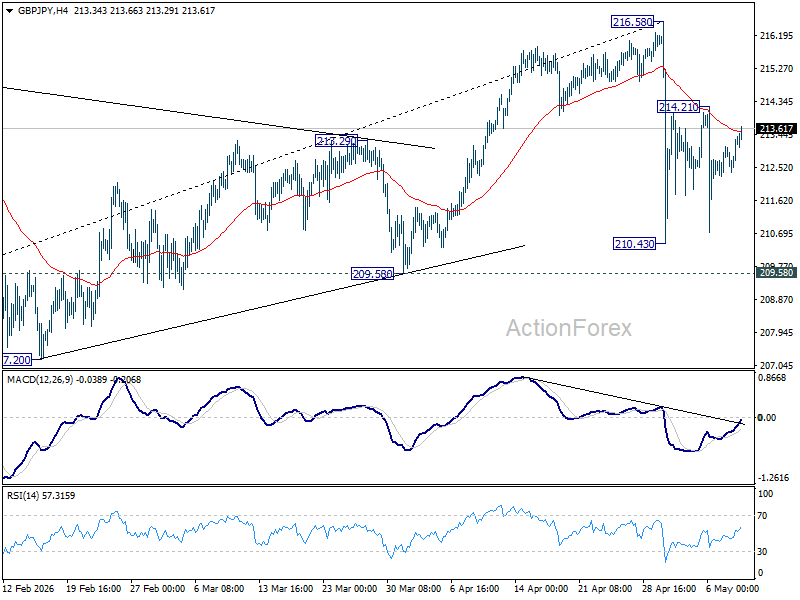

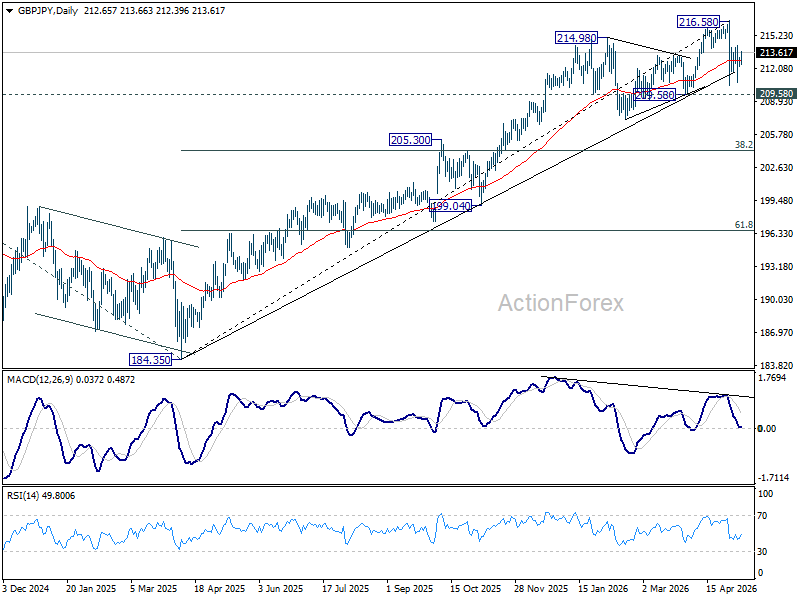

GBP/JPY Weekly Outlook

GBP/JPY stayed in range of 210.43/214.21 last week and outlook is unchanged. Initial bias remains neutral this week first. Below 210.43 will extend the fall from 216.58 to 209.58 support first. However, firm break of 214.21 will argue that the pullback from 216.58 has completed, and turn bias back to the upside for retesting this high.

In the bigger picture, while the fall from 216.58 is steep, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 205.46) will argue that it's already in medium term down trend for 184.35 support.

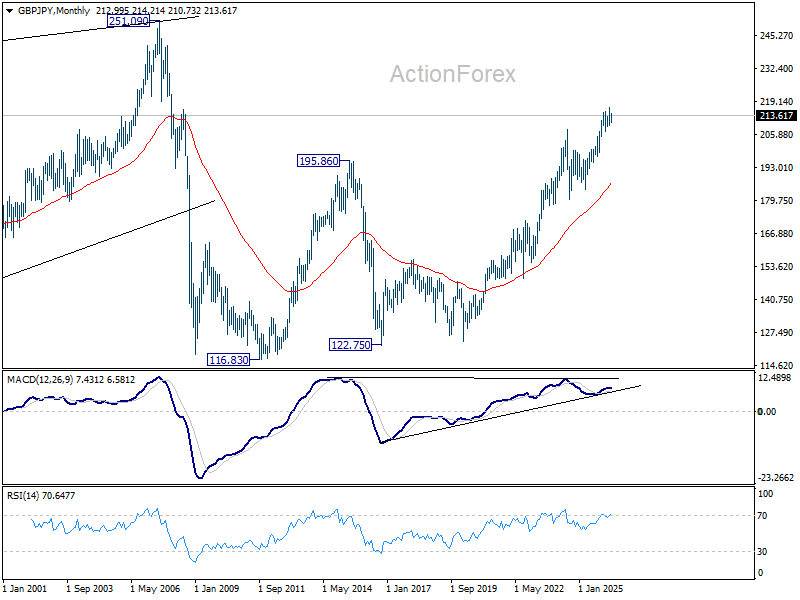

In the long term picture, up trend from 116.83 (2011 low) is in progress. Next target is 251.09 (2007 high). This will remain the favored case as long as 55 M EMA (now at 186.82) holds.

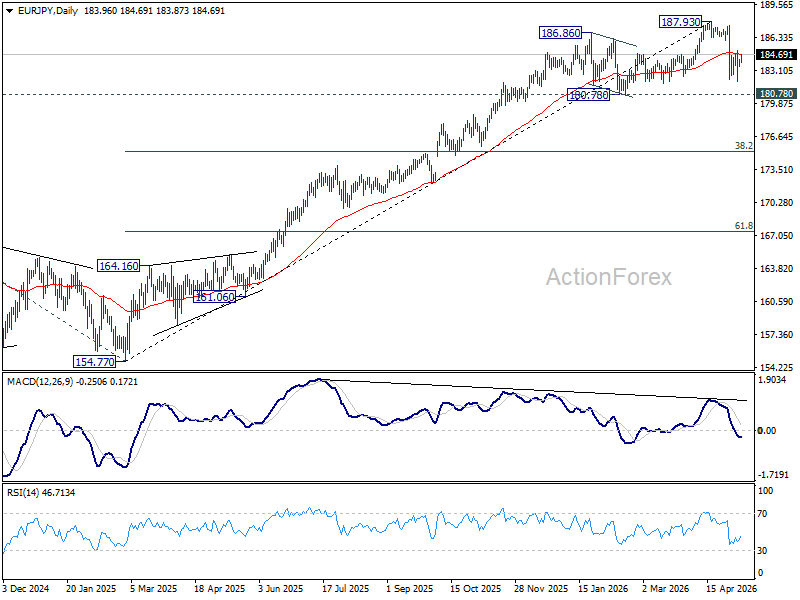

EUR/JPY Weekly Outlook

EUR/JPY edged lower to 182.01 last week but rebounded since then. Initial bias remains neutral this week first. Break of 182.01 will extend the fall from 187.93 to 180.78 support. Nevertheless, firm break of 185.02 will suggest that pullback from 187.93 has completed, and turn bias back to the upside for retesting this high.

In the bigger picture, the pullback from 187.93 is steep, there is no sign of reversal yet. Uptrend from 114.42 is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 177.79) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long 55 W EMA (now at 177.79) holds.

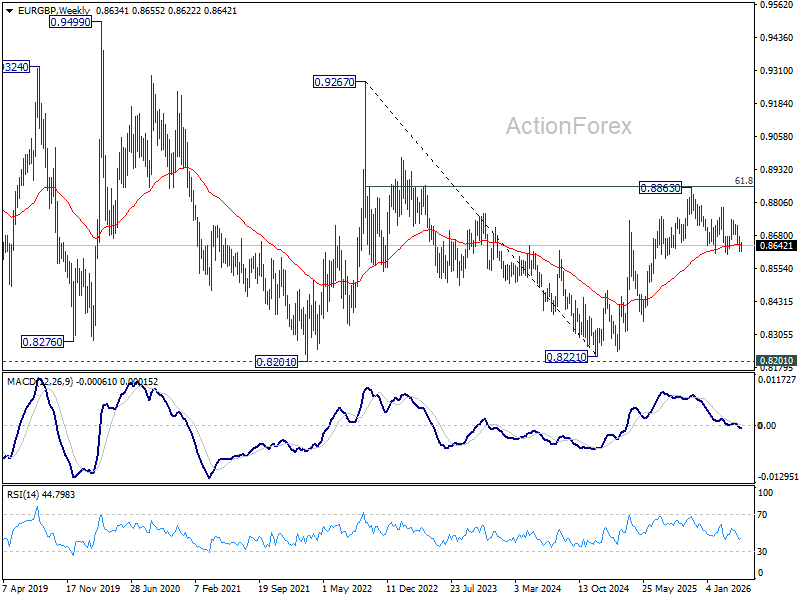

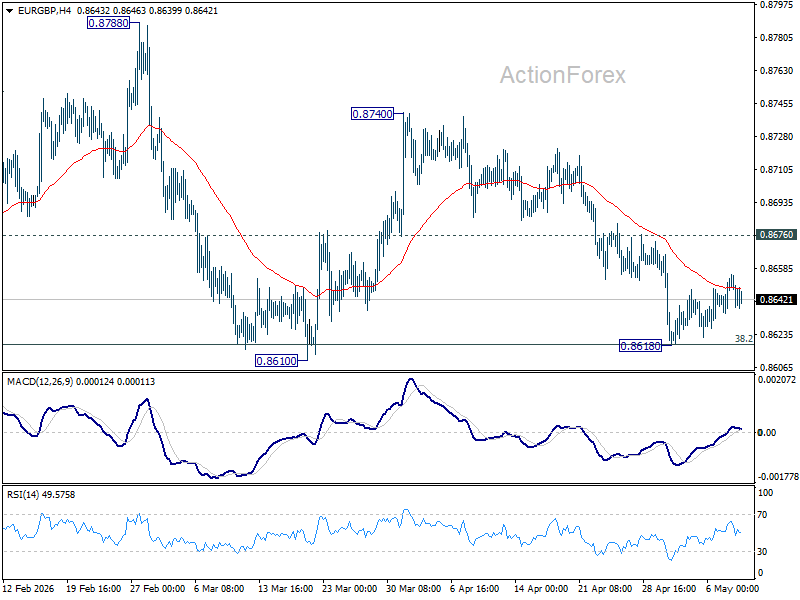

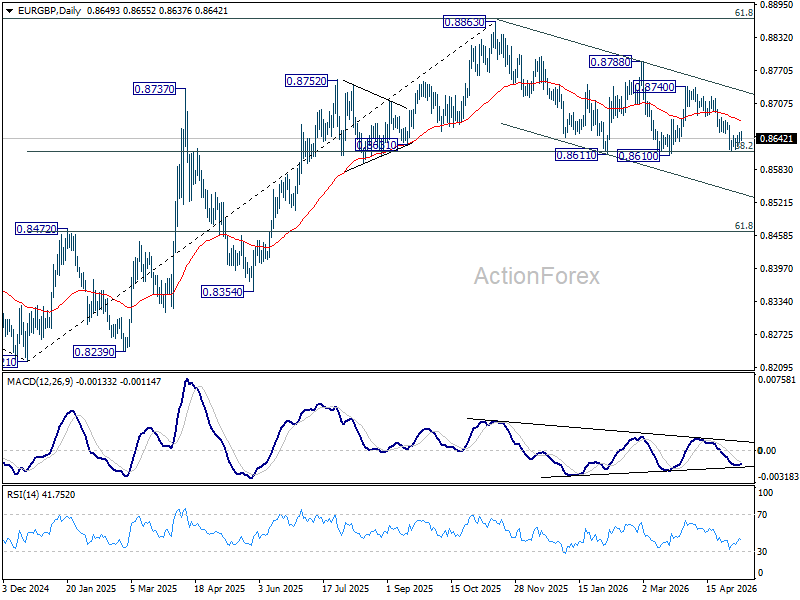

EUR/GBP Weekly Outlook

EUR/GBP recovered last week as it failed to break through 0.8610 support. Initial bias stays neutral this week first. On the downside, firm break of 0.8610 will carry larger bearish implications and pave the way to 0.8466 fibonacci level next. Nevertheless, firm break of 0.8676 will turn bias back to the upside for stronger rebound back to 0.8740 resistance instead.

In the bigger picture, focus is back on 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Sustained break there will confirm that whole rise from 0.8221 has completed at 0.8863. Deeper decline should then be seen to 61.8% retracement at 0.8466 at least. For now, risk will stay mildly on the downside as long as 55 D EMA (now at 0.8677) holds, in case of recovery.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.