Sample Category Title

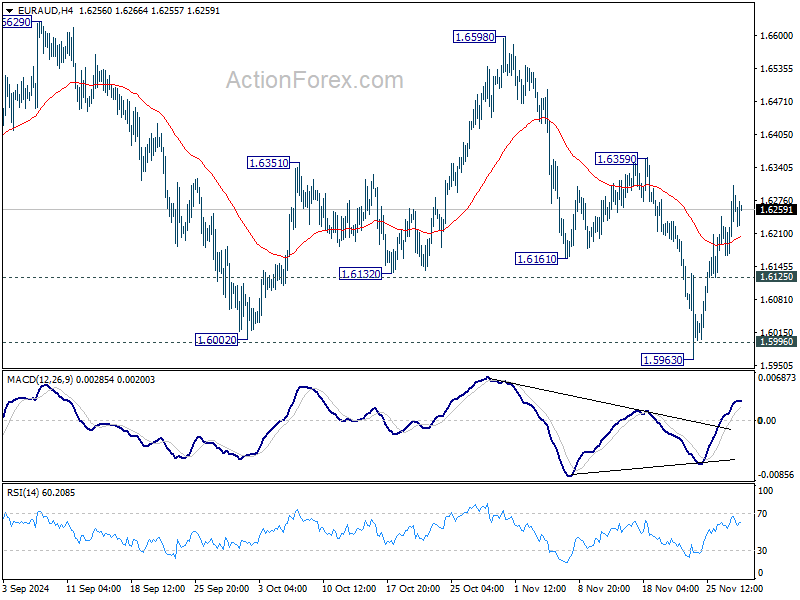

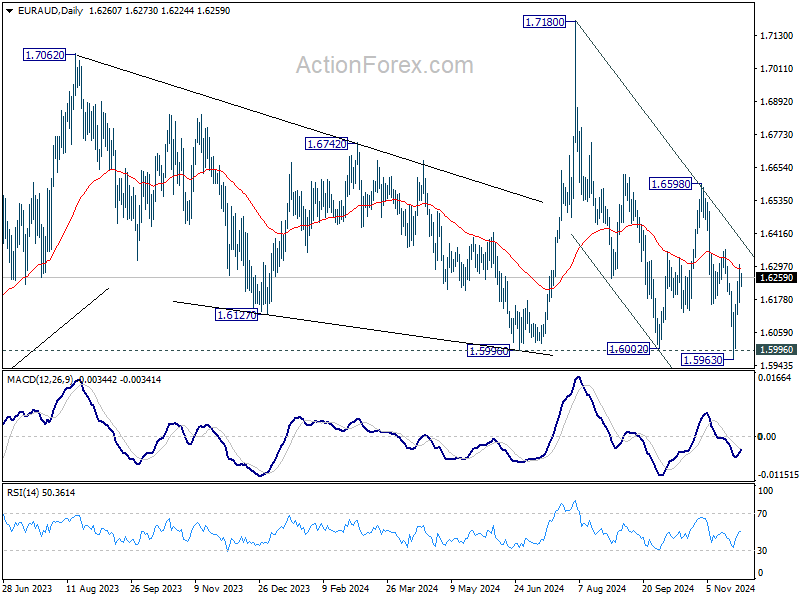

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6187; (P) 1.6247; (R1) 1.6324; More...

Intraday bias in EUR/AUD stays neutral first. On the upside, firm break of 1.6359 resistance will be the first sign of bullish reversal and target 1.6598 resistance for confirmation. On the downside, though, below 1.6125 minor support will bring retest of 1.5963 low.

In the bigger picture, immediate focus is now on 1.5996 key support level. Sustained break there will argue that whole up trend from 1.4281 (2022 low) is already reversing. Deeper decline would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388, even as a correction. Nevertheless, strong rebound from current level, followed by break of 1.6359 resistance, will keep medium term outlook neutral at worst.

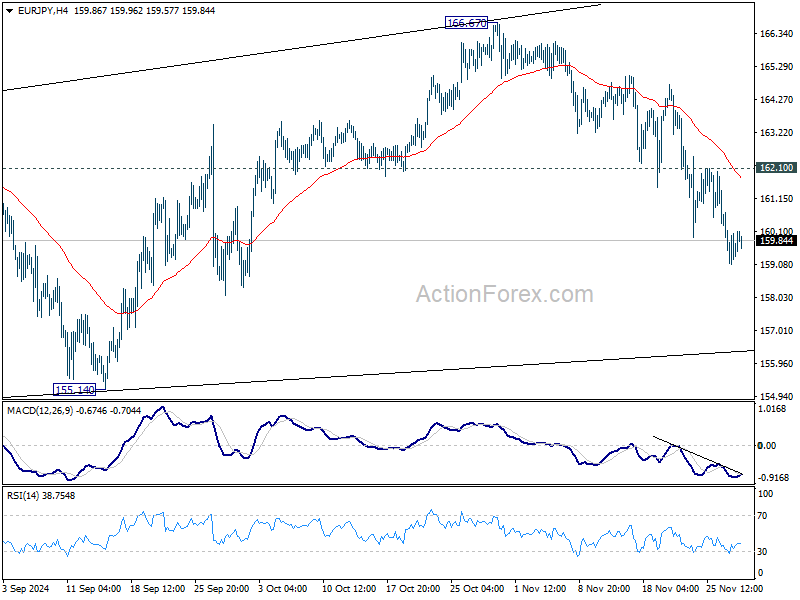

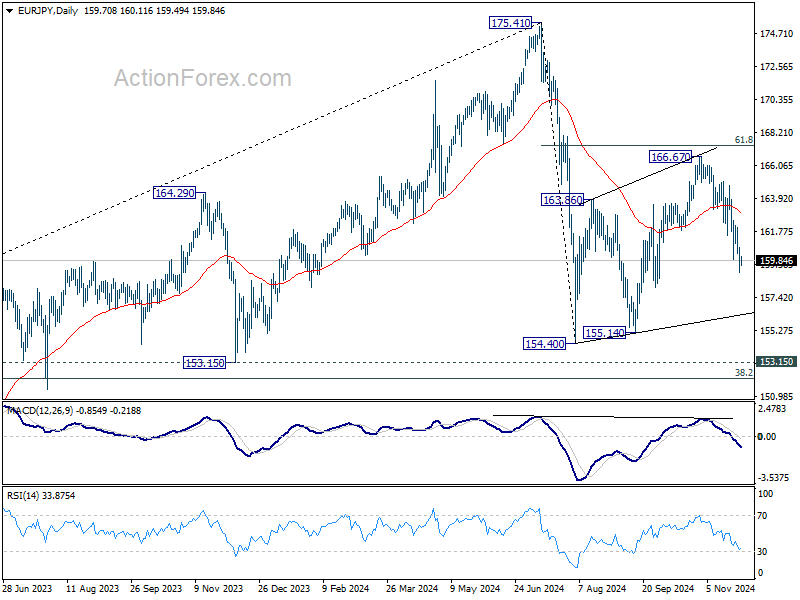

EUR/JPY Daily Outlook

Daily Pivots: (S1) 158.94; (P) 159.82; (R1) 160.56; More....

EUR/JPY's fall from 166.67 is still in progress and intraday bias remains on the downside. As noted before, corrective rebound from 154.40 could have completed with three waves up to 166.67. Deeper decline would be seen to 155.14 support next. On the upside, above 162.10 resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

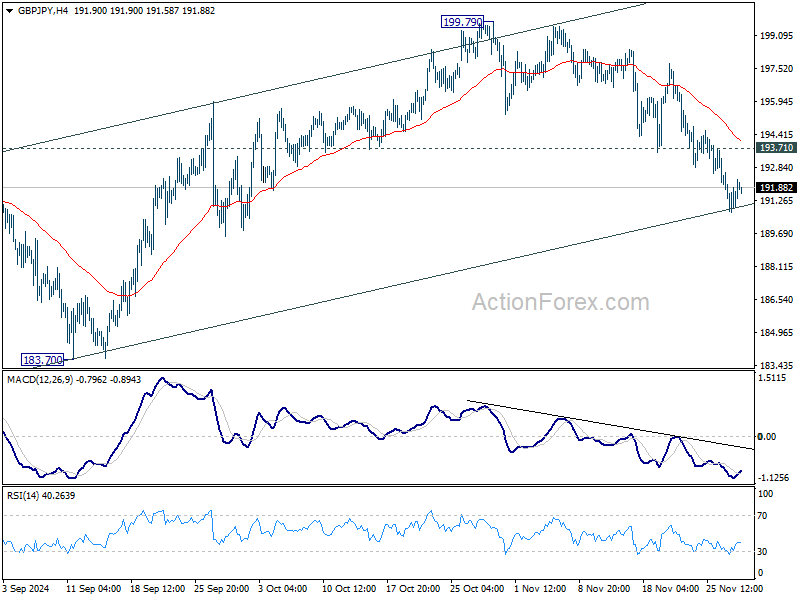

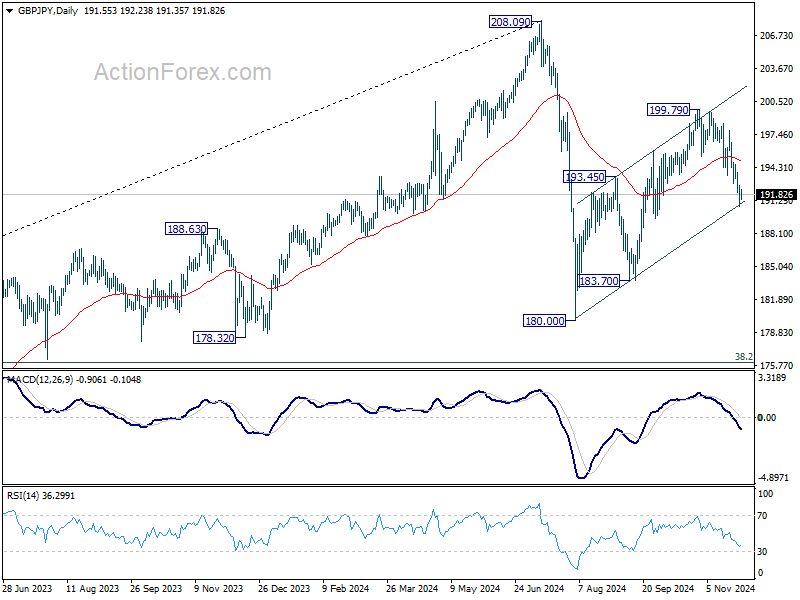

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.66; (P) 191.64; (R1) 192.60; More...

Intraday bias in GBP/JPY remains on the downside as fall from 199.79 is in progress. As noted before, corrective rise from 180.00 could have completed with three waves up to 199.79. Deeper decline would be seen to 183.70 support next. On the upside, above 193.71 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

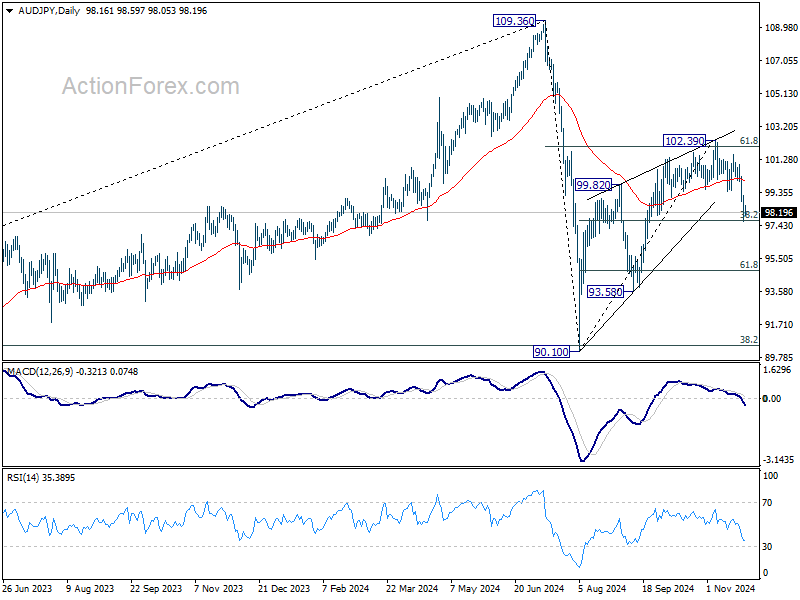

Yen Strength Extends Amid Quiet Forex Markets; AUD/JPY Tests Key Levels

The forex market has turned subdued as the US Thanksgiving holiday curbs activity, but overall trends have held steady. Yen continues to outperform, supported by the ongoing decline in US and European benchmark yields, maintaining its position as the strongest currency this week so far . Euro is the second strongest, showing signs of gaining ground against commodity currencies like the Australian and Canadian Dollars, though it still lacks the momentum needed to decisively advance against Dollar and other European majors.

On the weaker side, Loonie and Aussie remain under pressure, weighed down by US tariff threats targeting Canada and China. Aussie is also being pushed lower by its underperformance against Kiwi, which is benefiting from expectations of a slower rate-cutting cycle in 2025. These expectations were reinforced today by comments from a senior RBNZ official. Dollar is also softer but has yet to confirm a bearish reversal, even against the surging Yen.

Technically, AUD/JPY is now at a critical juncture, pressing against 38.2% retracement of 90.10 to 102.39 at 97.69. Decisive break below this level would strongly suggest that the corrective rebound from 90.10 has completed with three waves up to 102.39.

In a less bearish scenario, fall from 102.39 could represent the second leg of a medium-term corrective pattern originating at 90.10. However, a more bearish interpretation suggests the decline from 102.39 might be the third leg of a larger correction that began at 109.36.

In either case, firm break of 97.69 would open the door for deeper decline to 61.8% retracement at 94.79.

Also, progression in AUD/JPY’s fall could serve as an early indicator for broader Yen strength across other crosses.

In Asia, at the time of writing, Nikkei is up 0.37%. Hong Kong HSI is down -1.17%. China Shanghai SSE is down -0.08%. Singapore Strait Times is up 0.26%. Japan 10-year JGB yield is down -0.0147 at 1.060. Overnight, DOW fell -031%. S&P 500 fell -0.38%. NASDAQ fell -0.60%. 10-year yield fell -0.060 to 4.242.

RBNZ’s Silk signals slower easing path with potential pauses ahead

Assistant Governor Karen Silk indicated that RBNZ is likely to slow the pace of monetary easing and incorporate pauses into its rate cycle after February.

“There could be pauses built in, but it is definitely a slower track after February,” she noted in an interview with Bloomberg. This aligns with the bank’s updated projections released yesteday.

Silk highlighted the importance of maintaining "mildly restrictive" monetary policy to manage inflationary pressures, particularly as inflation is projected to rise to 2.5% next year.

Looking further ahead, Silk noted that RBNZ expects to be "a little closer" to the long-term neutral rate by the end of 2025. However, she emphasized that current projections do not indicate rates falling "below neutral" at any point during the forecast period.

NZ ANZ business confidence eases to 64.9, outlook continues to brighten

New Zealand's ANZ Business Confidence dipped marginally in November, falling from 65.7 to 64.9, but it remains at what ANZ describes as an "impressive high" level. Own Activity Outlook, a key forward indicator, rose to a decade high of 48.0 from 45.9, reinforcing optimism about future economic conditions

Inflation related metrics also showed broad improvement, with cost expectations down from 64.2 to 62.9, wage expectations easing from 77.0 to 75.5, and pricing intentions falling from 44.2 to 42.2, marking the first decline in four months. Notably, inflation expectations dropped significantly from 2.83% to 2.53%.

ANZ attributed the robust activity outlook to the impact of interest rate cuts, which are "changing actual behavior, not just expectations." While the economy remains fragile, ANZ highlighted that "things are starting to turn higher," with improving activity suggesting early signs of recovery.

RBNZ is likely to take comfort in these trends, as "sufficient domestic disinflation pressure" appears to be in the pipeline, even if growth rebounds faster than expected. However, the survey tempered expectations for aggressive rate cuts, indicating that "large emergency cuts" may not be necessary.

Looking ahead

Germany CPI flash and Eurozone M3 money supply will be released in European session. Canada will release current account. US is on holiday.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.66; (P) 191.64; (R1) 192.60; More...

Intraday bias in GBP/JPY remains on the downside as fall from 199.79 is in progress. As noted before, corrective rise from 180.00 could have completed with three waves up to 199.79. Deeper decline would be seen to 183.70 support next. On the upside, above 193.71 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

RBNZ’s Silk signals slower easing path with potential pauses ahead

Assistant Governor Karen Silk indicated that RBNZ is likely to slow the pace of monetary easing and incorporate pauses into its rate cycle after February.

“There could be pauses built in, but it is definitely a slower track after February,” she noted in an interview with Bloomberg. This aligns with the bank’s updated projections released yesteday.

Silk highlighted the importance of maintaining "mildly restrictive" monetary policy to manage inflationary pressures, particularly as inflation is projected to rise to 2.5% next year.

Looking further ahead, Silk noted that RBNZ expects to be "a little closer" to the long-term neutral rate by the end of 2025. However, she emphasized that current projections do not indicate rates falling "below neutral" at any point during the forecast period.

GBP/USD Eyes Comeback: How Long Can It Hold?

Key Highlights

- GBP/USD started an upside correction from the 1.2500 support.

- It cleared a key contracting triangle with resistance at 1.2600 on the 4-hour chart.

- Bitcoin tested the $91,000 zone before the bulls appeared.

- USD/JPY declined heavily below the 153.50 and 152.00 support levels.

GBP/USD Technical Analysis

The British Pound found support near 1.2500 against the US Dollar. GBP/USD formed a base and recently started a recovery wave above 1.2550.

Looking at the 4-hour chart, the pair cleared a key contracting triangle with resistance at 1.2600. The pair climbed above the 23.6% Fib retracement level of the downward move from the 1.3047 swing high to the 1.2487 low.

However, the pair is still well below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). On the upside, the pair could face resistance near the 1.2700 level.

The first major resistance is near the 1.2750 level or the 50% Fib retracement level of the downward move from the 1.3047 swing high to the 1.2487 low. A close above the 1.2750 level could set the tone for another increase.

The next major resistance could be 1.2835, above which the price could climb higher toward the 1.2950 resistance. Any more gains might send GBP/USD toward 1.3000.

On the downside, immediate support sits near the 1.2600 level. The next key support sits near the 1.2550 level. Any more losses could send the pair toward the 1.2500 level.

Looking at Bitcoin, the price extended its downside correction and tested the $91,000 zone where the bulls emerged.

Upcoming Economic Events:

- German Consumer Price Index for Nov 2024 (YoY) (Prelim) – Forecast +2.2%, versus +2.4% previous.

- German Consumer Price Index for Nov 2024 (MoM) (Prelim) – Forecast -0.2%, versus +0.4% previous.

First Impressions: NZ Business Confidence

Businesses remain very upbeat about the year ahead. There are also some signs that current conditions are gradually improving.

Key results (November 2024)

- Business confidence: 64.9 (Prev: 65.7)

- Expectations for own trading activity: 48.0 (Prev: 45.9)

- Activity vs same month one year ago: -9.7 (Prev: -10.5)

- Inflation expectations: 2.53% (Prev: 2.83%)

- Pricing intentions: 42.2 (Prev: 44.2)

Business confidence remained close a ten-year high in the November survey. General sentiment was slightly lower compared to October, but firms’ own activity expectations – which have tended to correspond more closely with GDP growth – rose another 2 points to 48.

Confidence was stronger this month in the agriculture, retailing and services sectors. This was partly offset by a drop in construction and manufacturing (though the latter was coming off a sharp rise in October).

The surge in confidence in recent months has followed the rapid turnaround in the Reserve Bank’s stance, from warning about the possibility of an interest rate hike in May, to delivering 75bp of OCR cuts (at the time of the survey) with the strong likelihood of more to come.

Firms’ growing confidence about the year ahead is now also being accompanied by signs of a gradual improvement in current conditions. A net 10% of firms reported that their activity was down on the same time last year – still soft, but the gap is closing compared to the net 24% who were behind the pace in July. The agriculture sector in particular is running well ahead of last year, which likely reflects the improvements in meat and dairy prices and the post-cyclone recovery in horticulture.

Meanwhile, the inflation indicators in this month’s survey were fairly benign overall. Expected inflation for the year ahead fell from 2.8% to 2.5% (this month will have captured the full response to the Q3 CPI figures, which were released mid-October). Firms’ own pricing intentions dipped slightly this month, although they remain above their long-run average. Firms continue to see a gradual easing in their own cost pressures, and wage growth expectations have settled at around 2.6% in recent months.

We’re forecasting a 0.2% fall in GDP for the September quarter, followed by a modest 0.3% increase in the December quarter. The RBNZ’s forecasts in yesterday's Monetary Policy Statement were identical to ours. While the business confidence survey has certainly been more ebullient than other high-frequency indicators, it generally supports our view of a return to modest growth in the economy.

NZ ANZ business confidence eases to 64.9, outlook continues to brighten

New Zealand's ANZ Business Confidence dipped marginally in November, falling from 65.7 to 64.9, but it remains at what ANZ describes as an "impressive high" level. Own Activity Outlook, a key forward indicator, rose to a decade high of 48.0 from 45.9, reinforcing optimism about future economic conditions

Inflation related metrics also showed broad improvement, with cost expectations down from 64.2 to 62.9, wage expectations easing from 77.0 to 75.5, and pricing intentions falling from 44.2 to 42.2, marking the first decline in four months. Notably, inflation expectations dropped significantly from 2.83% to 2.53%.

ANZ attributed the robust activity outlook to the impact of interest rate cuts, which are "changing actual behavior, not just expectations." While the economy remains fragile, ANZ highlighted that "things are starting to turn higher," with improving activity suggesting early signs of recovery.

RBNZ is likely to take comfort in these trends, as "sufficient domestic disinflation pressure" appears to be in the pipeline, even if growth rebounds faster than expected. However, the survey tempered expectations for aggressive rate cuts, indicating that "large emergency cuts" may not be necessary.

Weekly Economic & Financial Commentary: And So It Begins

Summary

United States: Data Came in Like a Butterball

- Anyone who has ever gobbled until they wobbled can tell you it can be challenging to digest too much at one time. In the financial world, you know it's Thanksgiving when you get a full slate of economic data stuffed into one day. Nobody is relegated to the kids table as we break down what all this data mean for the outlook.

- Next week: ISM Manufacturing Index (Mon.), ISM Services Index (Wed.), Employment (Fri.)

International: Reserve Bank of New Zealand Eases Into Summer; German Business Sentiment Shivers

- It was a relatively light week for international economic data and events. The Reserve Bank of New Zealand delivered its second consecutive 50 bps rate cut to reach a policy rate of 4.25%, and Governor Adrian Orr signaled the possibility for another move of the same size in Q1 if the outlook evolves as expected. Australia monthly CPI data were somewhat mixed though showed stickiness in underlying price pressures, and German Business Sentiment data were somewhat disappointing.

- Next week: China PMIs (Sat.), Australia GDP (Wed.), Reserve Bank of India Policy Rate (Fri.)

Credit Market Insights: Credit Demand Rises Alongside Application Rejection Rates

- Consumer credit demand broadly rose compared to the start of 2024. At the same time, rejection rates for applicants across consumer credit products have remained elevated, demonstrating that consumers cannot rely on credit to sustain their spending patterns to the same degree they have been able to in prior cycles.

Topic of the Week: And So It Begins

- President-elect Donald Trump proposed a 25% tariff on all imported goods from Mexico and Canada and an additional 10% levy on all products from China this week. President Claudia Sheinbaum has signaled that Mexico is prepared to respond with retaliatory tariffs. How important are Canada and Mexico to U.S. imports?

BTCUSD Ends Bearish Correction Near the 90,600 Zone

- Bitcoin rebounds after hitting support near 90,600

- This could mean that the bearish correction is over

- A break above 100,000 could signal uptrend continuation

- For the picture to turn bearish, a dip below 66,700 may be needed

BTCUSD rebounded on Wednesday, after hitting support near the 90,600 zone on Tuesday. Although the crypto king corrected lower after nearly touching the psychological round figure of 100,000, the broader picture continues to point to a healthy longer-term uptrend, and today’s rebound may be the beginning of the next impulsive wave.

The RSI exited its above-70 zone, but it turned north again today, suggesting that it could re-enter that extreme zone and perhaps stay there for a while longer. This would indicate extremely bullish momentum rather than overbought conditions. The MACD, although below its trigger line, remains at extremely positive levels and has started showing signs of bottoming.

If the bulls are strong enough to stay in charge, they may decide to retest the 100,000 zone, the break of which would confirm a higher high and perhaps set the stage for a new record around the next psychological zone of 105,000.

On the downside, a dip below 90,600 could signal a deeper bearish correction, perhaps towards the 84,500 area, but the uptrend would still be intact, supported by the trendline drawn from the low of September 7, as well as the 100- and 200-day EMAs. For a bearish reversal to start being discussed, a dip below the key pivot zone of 66,700 may be needed.

To sum up, Bitcoin rebounded today, suggesting that the bulls may be in the mood to extend the prevailing uptrend. A breach of the 100,000 figure will take the price into uncharted territory and corroborate the bullish case.