Sample Category Title

NZDUSD: Temporary Bounce Rather Than Return to Growth

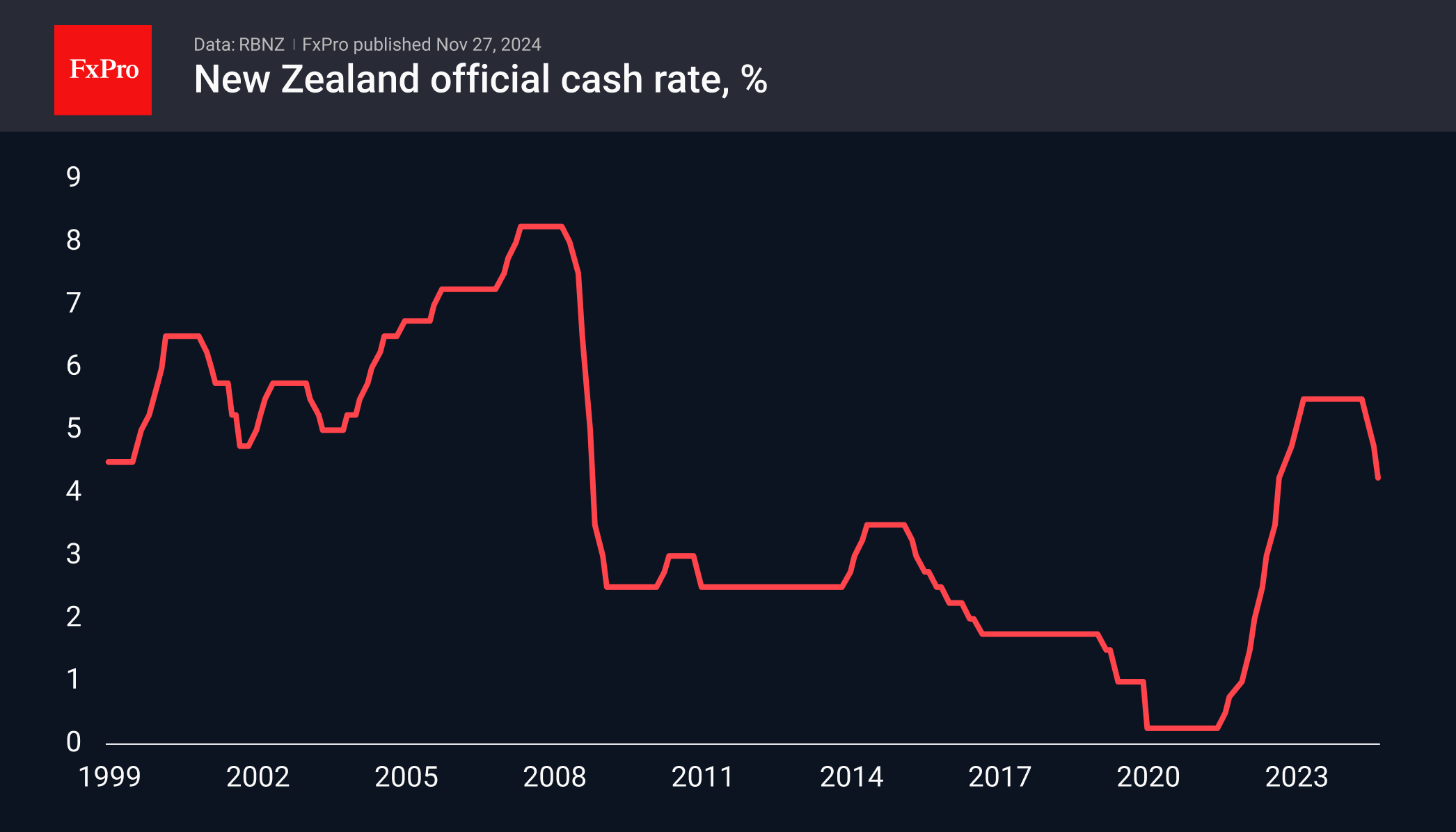

The Reserve Bank of New Zealand (RBNZ) cut its key interest rate by 50 basis points to 4.25%, bringing the total number of cuts in this cycle to 125. The move was in line with average market forecasts, although it represents a higher rate of normalisation than the G10 club of major developed market currencies.

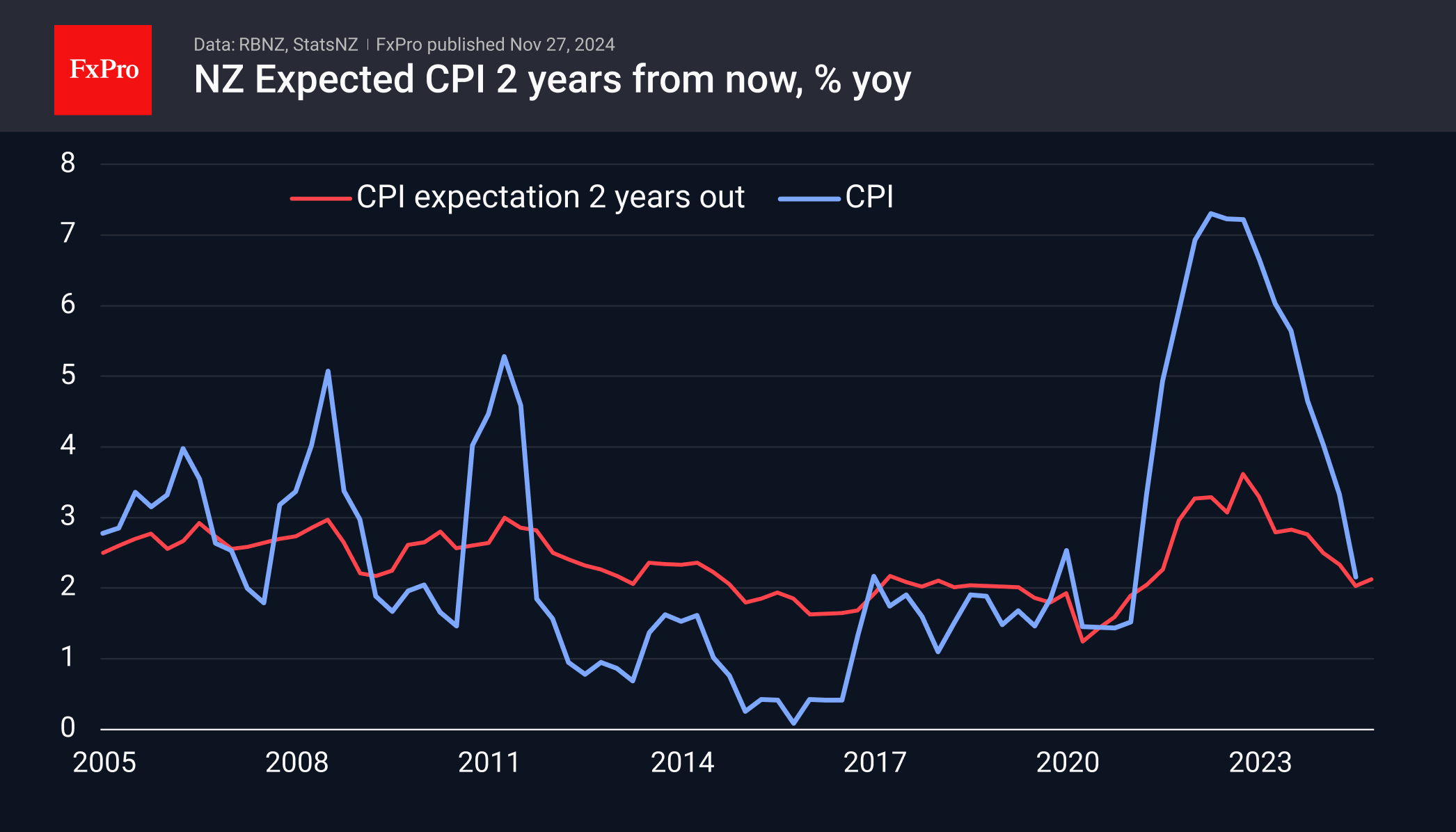

The RBNZ attributed the move to inflation slowing towards the middle of its target range of 1-3% p.a. and inflation expectations stabilising around that level for the next two years. The central bank also indicated its willingness to cut rates next year if there are no inflation surprises.

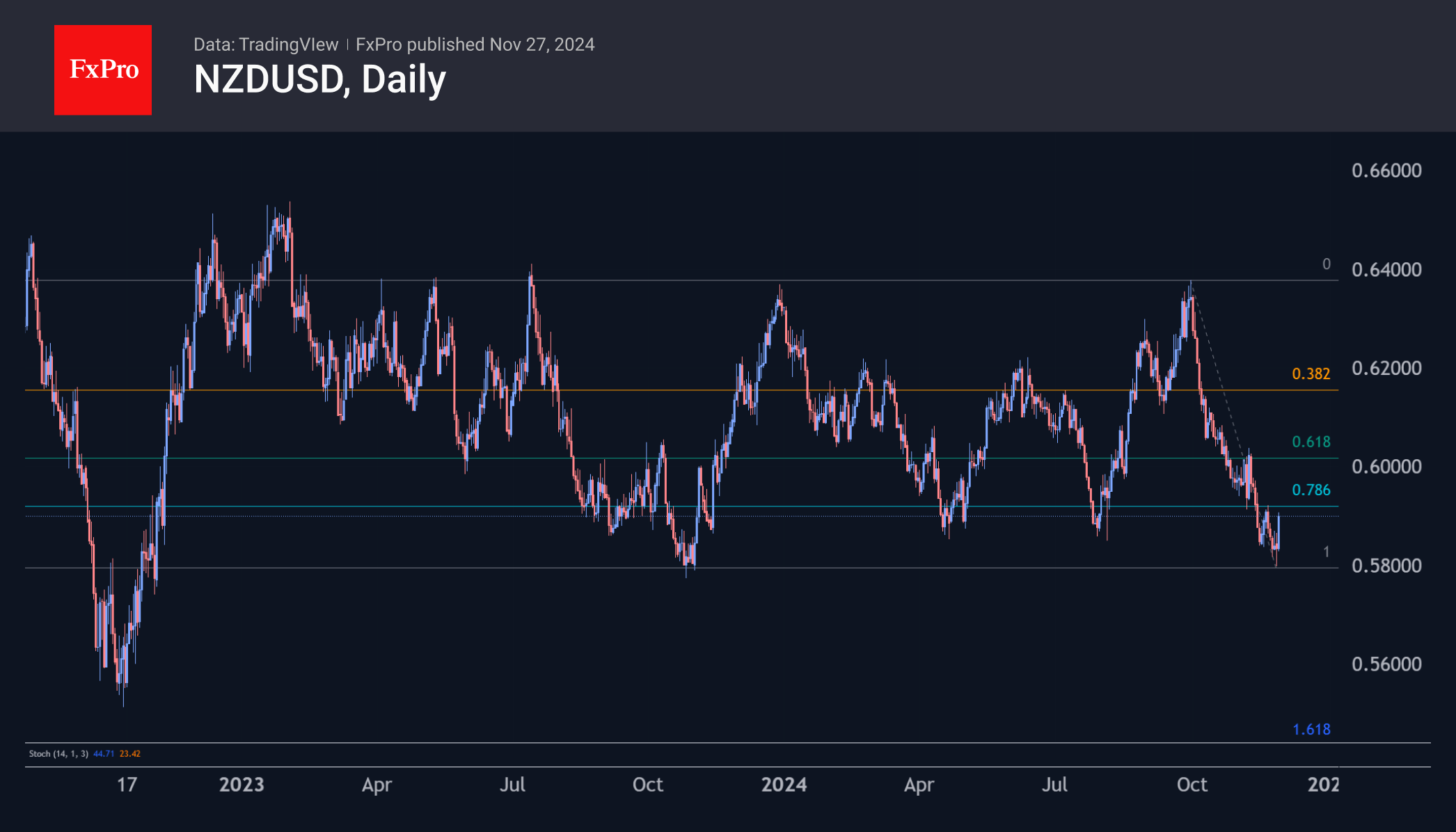

Fundamentally, the increased pace of rate cuts is negative for the currency, but markets have priced it in since early October. In that time, the NZDUSD has lost over 9%.

This has not only been a result of the Kiwi’s weakness but also the dollar’s strength.

However, the currency market’s reaction has been remarkable. The NZDUSD jumped over 1% in response to the release of the rate decision. So far, this looks like a corrective bounce caused by profit-taking after a strong move. The rally could extend to 0.5940, which is 50 pips above the current price. However, a stronger move to just above 0.6000 cannot be ruled out.

On the other hand, in the minutes of its November meeting released on Tuesday evening, the Fed allowed for a pause in the rate cuts and provided a firmer tone than previously expected.

The tone of monetary policy between the Fed and the RBNZ is diverging in favour of the former. Therefore, it is still difficult to see the NZDUSD’s rise from the lower boundary of the 2-year range as the start of a trend reversal but rather as a temporary bounce unless the fundamental picture changes.

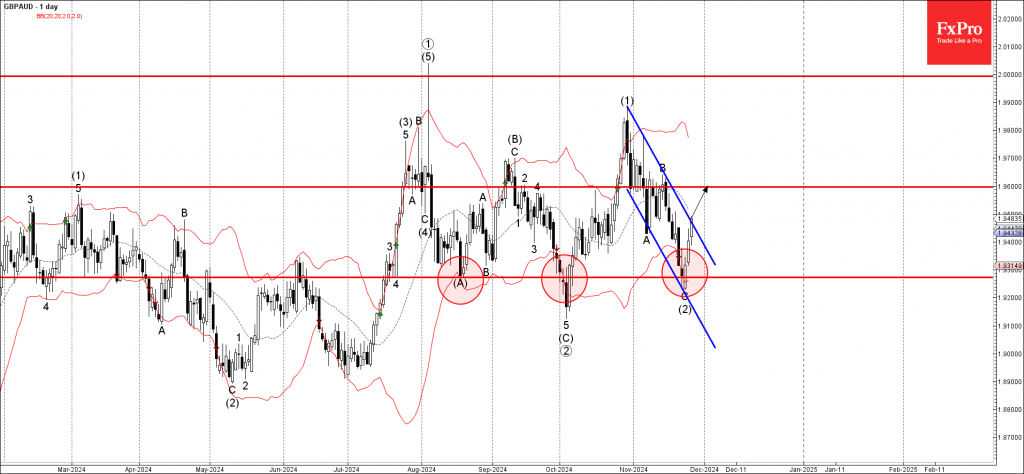

GBPAUD Wave Analysis

- GBPAUD broke daily down channel

- Likely to rise to resistance level 1.9600

GBPAUD currency pair today broke the resistance trendline of the daily down channel from the end of October (which encloses the earlier downward ABC correction (2) – which stopped earlier at the support level 1.9275).

The breakout of this down channel should accelerate the active impulse wave (3) – which belongs to the higher order impulse wave 3 from October.

GBPAUD currency pair can be expected to rise to the next resistance level 1.9600 (former top of wave B of the previous ABC correction (2)).

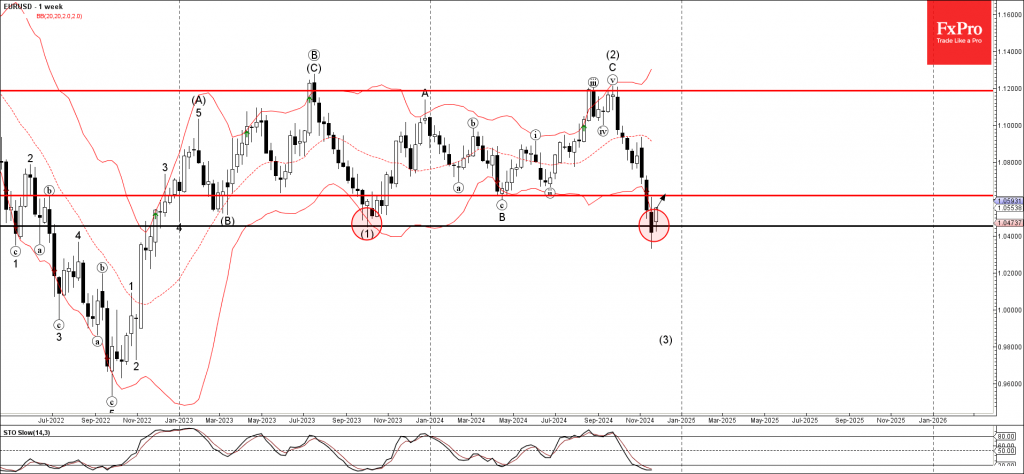

EURUSD Wave Analysis

- EURUSD reversed from support area

- Likely to rise to resistance level 1.0620

EURUSD currency pair recently reversed up from support area located at the intersection of the long-term support level 1.0455 (previous yearly low from 2023) and the lower weekly Bollinger Band.

The upward reversal from the support level 1.0455 will form the weekly Bullish Engulfing if the pair closes this week near the current levels.

Given the oversold weekly Stochastic and the strength of the support level 1.0455, EURUSD currency pair can be expected to rise to the next resistance level 1.0620 (former support from May).

US personal income surges 0.6% mom in Oct, Core PCE inflation edges higher to 2.8% yoy

U.S. personal income grew by 0.6% mom in October, exceeding market expectations of a 0.3% mom rise, with a total increase of USD 147.4B. Personal spending also climbed, rising 0.4% mom or USD 72.3B, aligning with forecasts. The robust income growth outpacing spending suggests an improved capacity for household savings or future consumption, adding resilience to the economy.

Inflation metrics, reflected in the PCE price indices, showed modest increases. Headline PCE price index rose 0.2% mom, while the core PCE price index, which excludes food and energy, rose 0.3% mom, both in line with expectations. Year-over-year, the headline PCE rose to 2.3% from 2.1%, and the core PCE increased to 2.8% from 2.7%, also meeting expectations.

Goods prices fell by -1.0% yoy, while services prices rose by 3.9% yoy, highlighting inflationary pressures concentrated in the services sector. Food prices saw a slight increase of 1.0% yoy, while energy prices dropped by -5.9% yoy, easing some cost pressures for consumers.

Sunset Market Commentary

Markets

“I would warn against moving too far, that is into accommodative”. ECB Executive Board member Schnabel broke ranks with the dovish current inside the central bank in place since this summer. Given the inflation outlook, Schnabel thinks that the ECB can gradually move toward neutral if incoming data continue to confirm the ECB’s baseline scenario. She believes that neutral is somewhere between 2% and 3% with the current deposit rate (3.25%) being not so far from these levels. The ECB’s October lending survey highlighted that banks no longer think that rates are holding back loan demand while the housing sector seems to be bottoming out. It’s evidence that the impact of the ECB’s restrictive policy is fading visibly. We must add that more dovish governors see neutral more near the lower bound of Schnabel’s estimate. Her strong preference to a gradual approach means ruling out half-point moves, an idea EMU money markets are still contemplating. Schnabel’s argumentation isn’t just about upside inflation risks. She’s confident of reaching the 2% target next year, but warns that the road will be bumpy. Instead, the ECB Board member highlights the discrepancy between survey-data, heavily influenced by uncertainty stemming from political troubles and Europe and Trump’s election victory, and hard data which gives her confidence on a consumption-driven recovery. From a more technical perspective, she doesn’t want to use valuable policy space that will be needed in the future when the economy is facing shocks that monetary policy can deal with more effectively. The front-end of the EMU swap curve slightly underperforms (2y: +2 bps) on Schnabel’s comments, but the impact could have been bigger given the aggressive ECB cuts that money markets are still discounting. For the next three meetings, they count on nearly 100 bps of cumulative rate cuts meaning at least one larger move. The rate bottom end 2025 lays below neutral at 1.75%. Schnabel’s comments nevertheless raise the stakes for tomorrow’s national and Friday’s EMU November CPI inflation numbers. Risks could be asymmetric with the bigger corrective move coming on higher inflation numbers. US Treasuries outperform today with yields correcting 4.5 bps to 7 bps lower, the belly of the curve outperforming the wings.

The single currency managed to put aside some worries (tariff threat, risk of collapsing French government,…), backed by the more hawkish ECB rhetoric. EUR/USD recovered from 1.0480 to 1.0525 in first instance. As US eco data were published, a sniff of USD weakness even propelled the pair to 1.0580. Traders pared some positions going into tomorrow’s US public holiday (Thanksgiving) and thin trading on (Black) Friday. Final revisions to Q3 GDP showed marginally weaker personal consumption (3.5% Q/Qa from 3.7%) and a slightly softer core PCE deflator (2.1% from 2.2%). Mixed durable goods orders (ranging between -0.2% and +0.2% M/M depending on the metric) and weekly jobless claims (stable at 213k) were too close to expectations.

News & Views

The Czech National Bank published a concluding statement after the IMF’s article 4 mission to the country. The IMF assesses that the Czech economy is slowly regaining ground after unprecedented shocks with the country transiting from heavily manufacturing-based, export-oriented growth to a more mature and diversified economy. A prudent policy mix has underpinned a return to price stability while preserving fiscal and financial buffers. The IMF expects inflation to converge back towards 2% in 2025. Risks to growth are seen to the downside while risks to inflation appear balanced. The IMF staff sees ground to lower the policy rate further to a neutral level estimated at around 3%. They also suggests the central bank to gradually give way to forecast-based inflation targeting and react less to the latest incoming figures. Simply put, with inflation expectations well anchored, the CNB should no longer be upset by temporary increases in inflation caused by factors outside its control - for example, food or fuel prices. Finally, they also suggested that there is room for the CNB to gradually further reduce the size of its balance sheet, in particular the large currency reserves (+ 40% of GDP) to help limit the risk to the CNB’s financial position.

U.S. Economic Growth Remains Solid in the Third Quarter

The second estimate of third quarter real GDP growth was unchanged at 2.8% quarter-over-quarter (annualized) – in line with the consensus forecast.

Looking under the hood, consumer spending was revised down to 3.5% (from the prior estimate of 3.7%), but this was entirely offset by an upgrade in non-residential fixed investment (3.8% vs. the prior 3.3%) and a smaller drag from inventory accumulation – now estimated to have shaved 0.1 percentage points (pp) from GDP (vs. the prior -0.2 pp).

Government spending expanded by a very healthy 5.0%, largely due to a sharp increase in defense spending (+13.9%). State & local spending rose 2.7%, up from Q2's 2.3%.

Net exports shaved 0.6 percentage points from Q3 growth (unchanged from the prior estimate), as another sizeable gain in imports (+10.2%) more than offset a healthy uptick in exports (+7.5%).

Real Gross Domestic Income (GDI) rose by 2.2% in the third quarter, virtually unchanged from Q2's downwardly revised reading of 2.0% (previously 3.4%). Corporate profits fell 1.1% (annualized) or $10.1 billion after accounting for inventory valuation and capital consumption adjustments. However, corporate profits measured as a share of GDP remains elevated at 13.0% (down from Q2's 13.2%).

- The average of real GDP and GDI, a supplemental estimate of domestic production, rose 2.5% in the third quarter or slightly weaker than the pace of growth suggested by the expenditure GDP data.

Key Implications

Third quarter economic growth remained solid, expanding well above trend, with underlying domestic demand accounting for all of last quarter's gain. Beyond the housing market and some elements of commercial real estate, there are few signs that elevated interest rates are materially weighing on domestic activity.

The U.S. economy will likely end the year on a solid footing, thanks to a resilient consumer and softening (albeit still expanding) business investment. As highlighted in our Quarterly Q&A publication, the outlook for next year has become a little more uncertain. The potential for higher tariffs and large-scale deportations pose notable downside risks to the outlook. But that needs to be weighed against the potential for further tax cuts and a lighter touch on regulation, both of which could lift animal spirits and provide some (if not a complete) growth offset. For now, we've lowered our 2025 GDP forecast by four-tenths to 1.7% but will adjust accordingly as more concrete policies are announced following President-elect Trump's inauguration on January 20th.

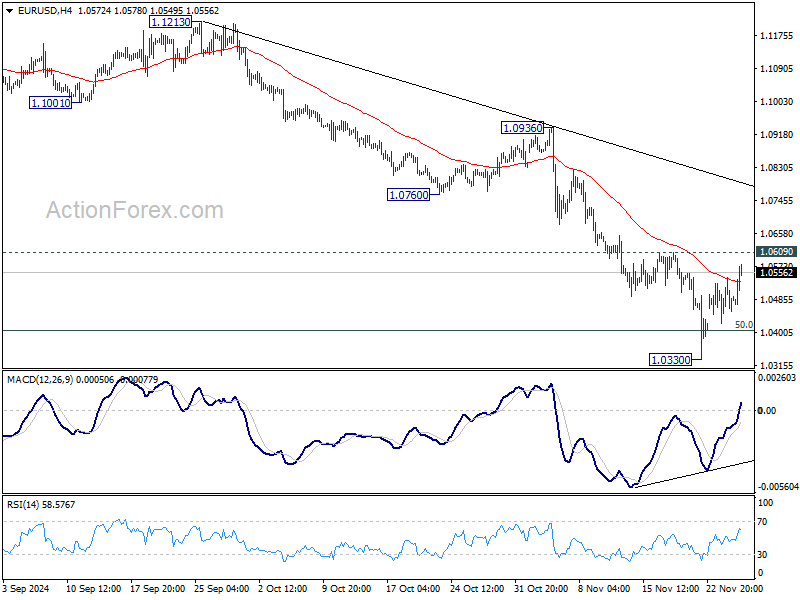

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0428; (P) 1.0486; (R1) 1.0548; More...

EUR/USD's recovery extends higher today but stays below 1.0609 resistance. Intraday bias remains neutral and further decline is still in favor. On the downside, break of 1.0330 will resume the fall from 1.1213. Also, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication. Nevertheless, firm break of 1.0609 will confirm short term bottoming, and turn bias back to the upside for 1.0760 support turned resistance first.

In the bigger picture, immediate focus is now on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

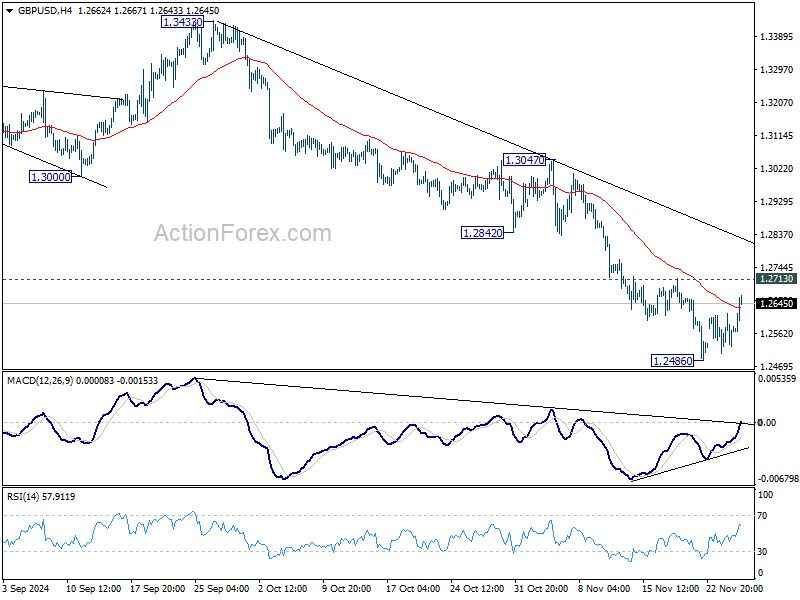

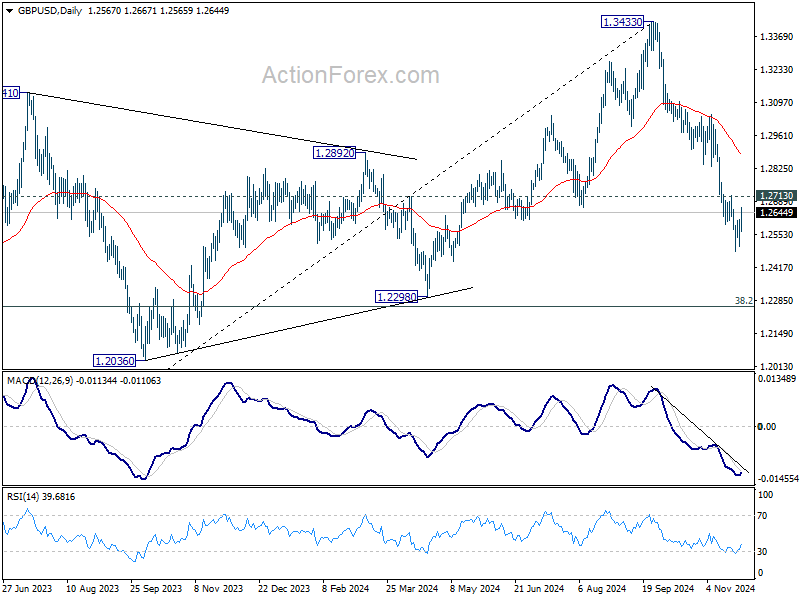

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2511; (P) 1.2564; (R1) 1.2620; More...

GBP/USD recovers further today but stays below 1.2713 resistance. Intraday bias stays neutral and further decline remains in favor. On the downside, break of 1.2486 will resume the fall from 1.3433 to 1.2298 cluster support zone. However, firm break of 1.2713 will indicate short term bottoming, and turn bias back to the upside for 55 D EMA (now at 1.2882).

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2893) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

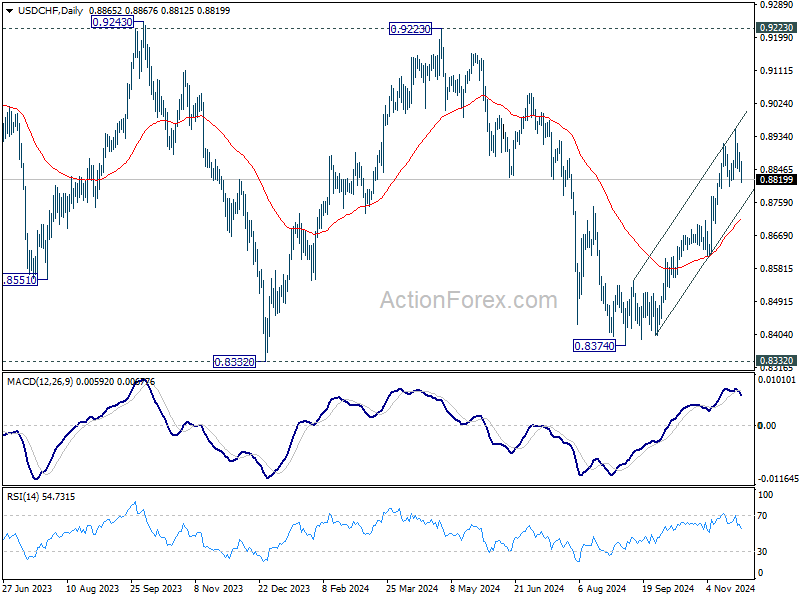

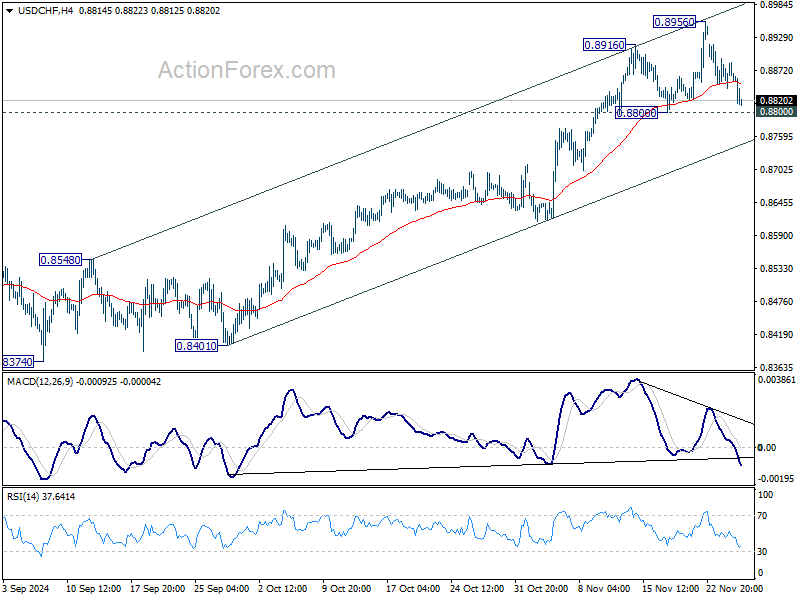

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8840; (P) 0.8868; (R1) 0.8892; More…

USD/CHF dips lower today but stays above 0.8800 support so far. Intraday bias remains neutral and further rise is in favor. Break of 0.8956 will resume the rally from 0.8374, and target 0.9223 key resistance next. However, firm break of 0.8800 will confirm short term topping and turn bias back to the downside for 55 D EMA (now at 0.8713).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.