Sample Category Title

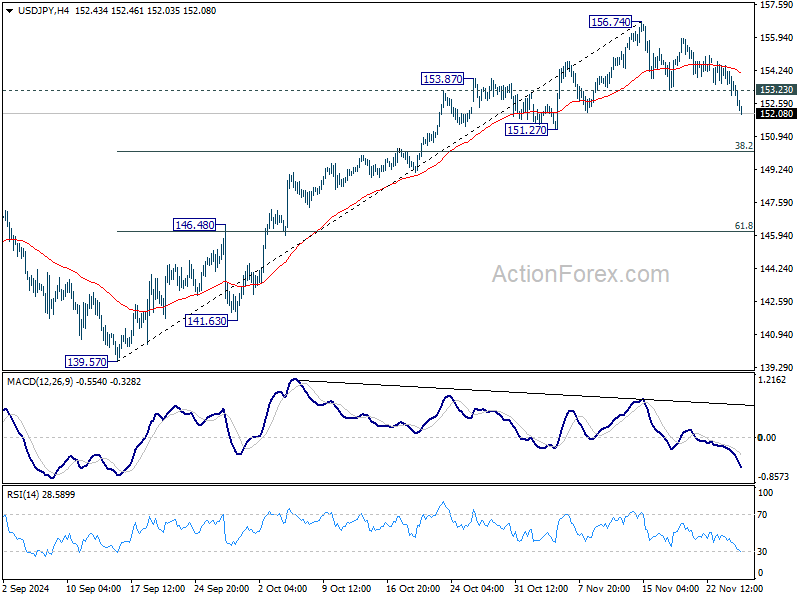

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.57; (P) 153.53; (R1) 154.07; More...

Intraday bias in USD/JPY stays on the downside as corrective fall from 156.74 is in progress. Deeper decline would be seen to 38.2% retracement of 139.57 to 156.74 at 150.18. On the upside, above 153.23 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 156.74 resistance holds, in case of recovery.

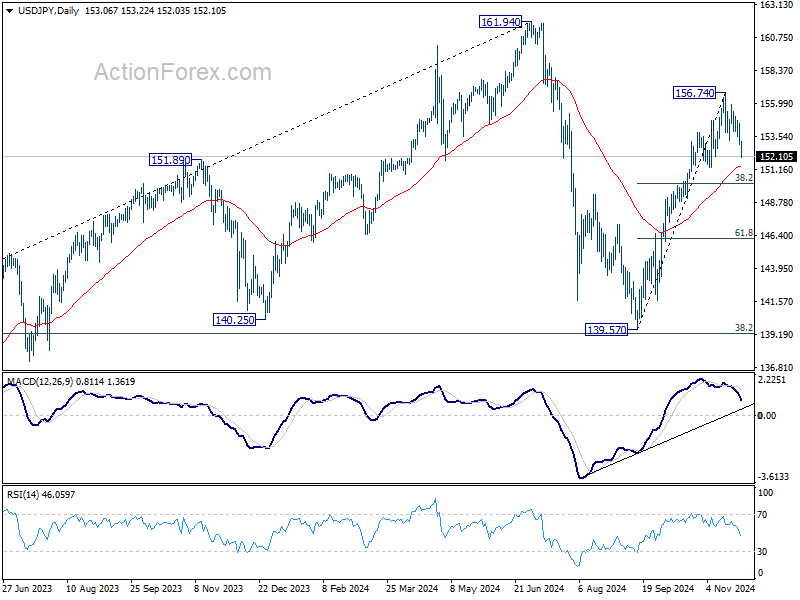

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

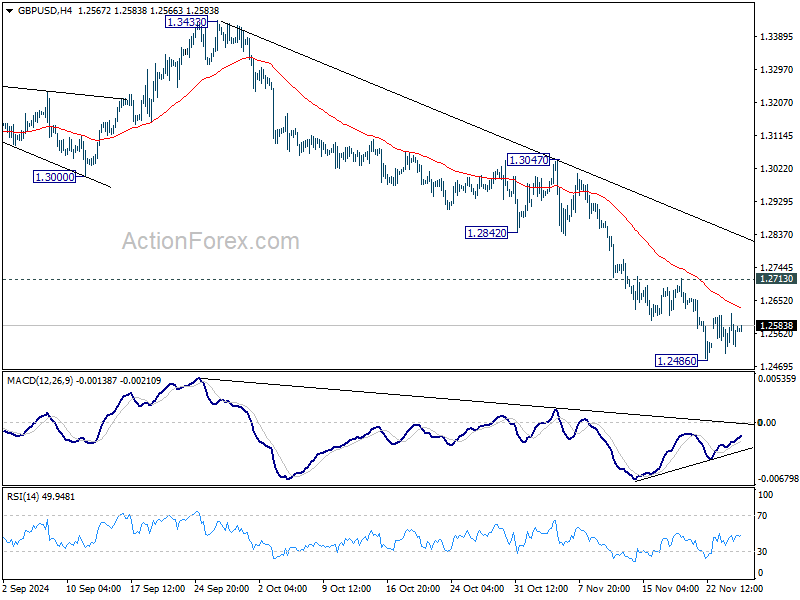

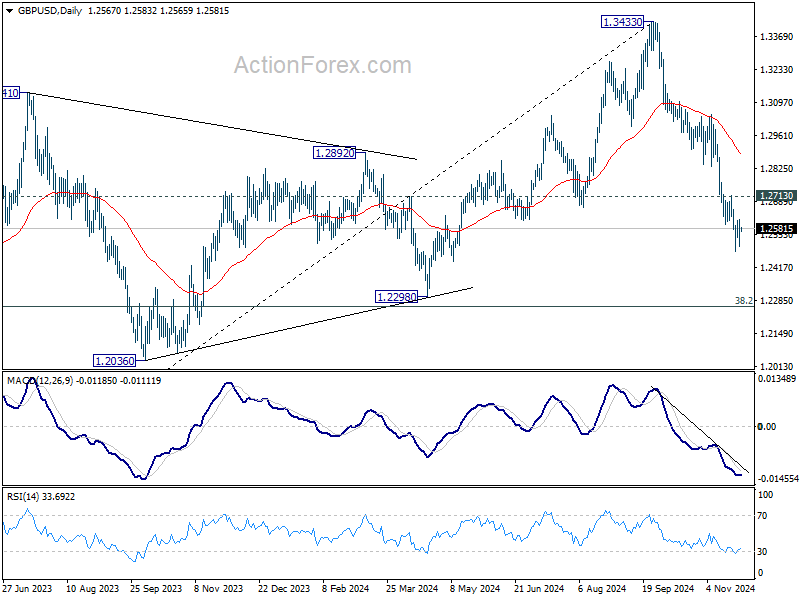

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2511; (P) 1.2564; (R1) 1.2620; More...

GBP/USD is staying in consolidation above 1.2486 and intraday bias remains neutral. Further decline is expected as long as 1.2713 resistance holds. On the downside, break of 1.2486 will resume the fall from 1.3433 to 1.2298 cluster support zone.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2893) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

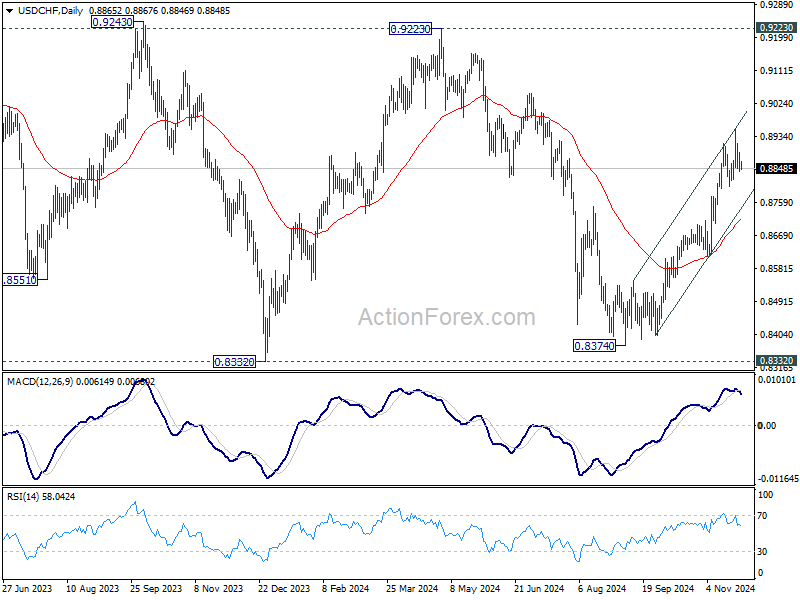

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8840; (P) 0.8868; (R1) 0.8892; More…

USD/CHF is staying in consolidation below 0.8956 and intraday bias remains neutral. Outlook will continue to stay bullish as long as 0.8800 support holds, in case of retreat. Break of 0.8956 will resume the rally from 0.8374, and target 0.9223 key resistance next.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

Ceasefire Gives Hope, US Data in Focus Before Thanksgiving

Even though Donald Trump’s tariff threats on China, Mexico and Canada didn’t concern Europe, the feeling in Europe was far from being comfortable yesterday. The word tariff gives cold chills especially to the European carmakers that already found themselves in crossfire with China. As such, Stellantis lost more than 5% yesterday while Volkswagen tanked another 2.76%.

Overall, Germany and Slovakia are the most vulnerable countries to any additional tariffs in Europe, because half of Germany’s GDP comes from exports, and cars make up to around 15% of these exports. Slovakia, on the other hand, has the highest per-capita car production globally, with automotive exports forming a significant part of its economy. The economic curse seems unrelenting for Germany. The country didn’t have time to get itself out of the energy crisis that the trade dispute is about to hit. Funny enough, you wouldn’t guess that the German economy is suffering badly when looking at the DAX valuations. The index trades near ATH levels, when the underlying economic fundamentals are telling a different story.

In the US, the market mood was better. Trump’s tariff threat, the rising inflation expectations as a result of them, and the cautious approach for further rate cuts from the latest Federal Reserve (Fed) minutes were outweighed by ceasefire news from the Middle East: Israel and Hezbollah inked a 60-day ceasefire agreement. The S&P500 posted its 52nd record high this year, the Dow Jones also extended its rally to a fresh record. Not everyone was happy, though. GM for example tanked 9% as its supply chain’s heavy reliance on both sides of its borders will explode the production costs and weigh on its profits.

Elsewhere, the energy companies had a slow session as crude oil consolidated and extended losses below the $70pb level on ceasefire news. Note that the news that OPEC+ is considering delaying the oil production restart beyond January has certainly tamed the selling pressure. Key nations at OPEC said that the timing may not be right for pushing 180’000 more barrels in an oversupplied market. The IEA for example predicts an oil surplus of more than 1mbpd next year – mainly due to the faltering Chinese demand. And that number risks being higher with Trump’s ‘drill baby drill’ policy. OPEC will meet at the start of next month and should drop plans to provide more oil in the next few months. And the latter should help throw a floor under the oil selloff, but will hardly reverse the medium-term negative outlook. Only a significant jump in demand, ideally from China, could do that. As such, US crude will likely consolidate below the 50-DMA.

In the FX, the US dollar eased yesterday as investors priced out a part of the geopolitical risks, while appetite in gold remained intact. The US 2-year yield extended a retreat, as the probability of a 25bp cut from the Fed jumped to 65% in the aftermath of the meeting minutes. Today, the US will release a crowded set of data before the Thanksgiving break. On the menu, the weekly jobless claims, the latest GDP update, durable goods orders and the core PCE index – the Fed’s favourite gauge of inflation. Quickly, the US economy is expected to have grown by around 2.8% in Q3 – slightly down from 3% printed previously but sales are expected to print a strong 3% growth (but we already knew that). Price pressures, however, are expected to have tamed in Q3 – which is good news for the Fed doves and the rate cut expectations. Yet, the core PCE index probably ticked higher to 2.8% in October, from 2.7% printed a month earlier. And that’s not great news for the inflation’s trajectory. Even less so as Trump’s tax cuts and tariffs are expected to give a boost to prices in the coming months. As such, a relatively strong growth number and softening price pressures last quarter will be welcome, but strong sales growth and a potential uptick in core PCE demand caution. I still believe that cutting first and seeing what happens is not the best strategy when the economic data remains strong. But I am not the Fed head. If the inflation data doesn’t surprise to the upside, investors will continue to back another 25bp cut in December and the latter could lead to a downside correction in the US dollar, and a rebound in major counterparts.

Elsewhere, the kiwi rallied against the greenback today following a widely expected 50bp cut from the Reserve Bank of New Zealand (RBNZ). Today’s cut marked the second consecutive 50bp cut, bringing total rate reductions to 125bp in just over three months, making the RBNZ the most aggressive rate cutter of the year. But the RBNZ predicted that the average cash rate falling to 3.83% by the middle of next year, suggesting that the policymakers, there, will move to a more gradual rate-cutting path moving forward. The latter could open the door for dipbuying opportunities after the kiwi dropped to the lowest levels in more than a year against the greenback. For those who are not willing to take the risk of a further dollar appreciation, shorting the euro against kiwi could be an alternative play provided the rising odds for more aggressive European Central Bank (ECB) cuts under Trump.

No Surprises in FOMC Minutes

In focus today

From the US, October PCE data is due for release. PCE inflation is expected to remain close to past month's pace in both headline and core terms, in line with the CPI data released earlier. October durable goods orders and revised Q3 GDP data will be released at the same time.

In Sweden, the monthly financial markets statistics for October will be presented. The report contains interesting data such as lending data and average mortgage rates. Deputy Governor of the Riksbank, Per Jansson, will talk about current monetary policy and the economic situation at 8:30 CET.

Economic and market news

What happened overnight

In New Zealand, the Reserve Bank (RBNZ) lowered the interest rate from 4.75% to 4.25% in line with consensus expectations. Before the meeting there were some uncertainties about the size of the rate cut, with some participants expecting a very aggressive 75bp rate cut. Furthermore, Governor Orr signalled that more monetary loosening would come and did not rule out a further 50bp cut at the February meeting. Orr said that RBNZ expect cash rate to reach a neutral level between 2.5% and 3.5% by the end of 2025. NZD/USD rose above 0.5860 following this morning's decision, and we expect the cross to trade close to its current level with 12m forecast of 0.58.

In the Middle East, Israel and Hezbollah agreed to a ceasefire. The ceasefire promises to end the conflict in across the border between Israel and Lebanon, which escalated after the Gaza war started last year. To repeat from yesterday's DMM we wrote that President-elect Donald Trump previously communicated to Israeli Prime Minister Netanyahu that he wants the wars in Lebanon and Gaza to end before he enters office. Netanyahu's willingness to sign a deal with Hezbollah could be part of his effort to please Trump and ensure he can still have US backing for his residual activities in Gaza, and possibly for targeting Iran.

What happened yesterday

In the US, the FOMC minutes released last night was in line with the signals provided by Chair Powell at the press conference, offering no significant surprises. The minutes reiterated that monetary policy is not on a pre-set course and underscored the importance of data dependency. Members, though, are particularly mindful of recent data volatility and the importance of focusing on the underlying tendencies. The minutes presented a positive view on inflation among members, with labour market data, inflation expectations, and pricing power indications reinforcing the disinflation narrative. We agree with these arguments and expect the FOMC to proceed with rate cuts at the next meetings.

US consumer confidence increased slightly more than expected in November to 111.7 (consensus: 111.3) against a revised-up October figure of 109.6. Labour market sub-indices gave somewhat mixed signals, as both "Jobs Plentiful" and "Jobs Hard to Get"-indices declined at the same time. Consumers still see their employment prospects as weaker than before the pandemic though. Plans for big ticket purchases declined a bit, but overall, nothing very surprising in the report.

In the euro area, the EU Commission approved French draft budget for now - but uncertainty remained. EU Commission said French draft budget met the requirements of the fiscal framework of being on a credible fiscal path. The only country that did not meet this requirement was the Netherlands. For 2025, the French budget's net expenditure growth path was also assessed to be in line with the recommendation. The Netherlands was assessed not to be in line with the recommendation. Hence, the Commission had so-far approved the French budget, but the budget has not been passed in the French parliament yet. Marine Le Pen said that she could not support the budget in its current form, so French PM Barnier still risked losing a no-confidence vote on the budget if he did not change it. At the same time, he had to balance the risks of the budget then not being approved by the EU Commission. Hence, risks remained on French government finances until a budget was passed in Parliament even with today's announcement from the EU.

Equities: Global equities were higher yesterday, which was particularly interesting as it marked the first full trading day following Trump's post-election tariff comments. Consequently, it was no surprise to see the US significantly outperforming Europe, with European markets declining in response to Trump's remarks. The surprise (if any) being that global equities were higher despite Trumps tariff threat.

There are two key takeaways here: Firstly, Trump's messages do not provide much clarity on the potential outcome of trade war 2.0. Secondly, while Trump may believe his negotiation tactics are intelligent, they are damaging to the markets as they create uncertainty. In the US yesterday: Dow +0.3%, S&P 500 +0.6%, Nasdaq +0.6%, and Russell 2000 -0.7%. Asian markets are mostly lower this morning, except for Chinese markets, which are higher. Both European and US futures are mixed this morning, with core Europe underperforming.

FI: The divergence between US and German yields continued through yesterday's session. US rates moved higher following the stronger than expected US consumer confidence data, while German bonds rose due to renewed political uncertainty in France. The OAT-Bund spread widened by 5bp to 127bp, the highest level since 2012, through following reports from Le Parisien that President Macron has lost confidence in PM Barnier and the government.

FX: NZD has been the outperformer over the last 24 hours amid this morning's RBNZ meeting proving to be a slight hawkish surprise. EUR/USD has so far done little this week while the NOK has come under renewed pressure. SEK had a strong last week which in combination to the turn in NOK has brought NOK/SEK back to the 0.9840-mark - only two days after the cross tested the parity level. EUR/GBP remains in the last weeks' trading range while USD/JPY continues its latest descent approaching new lows in November.

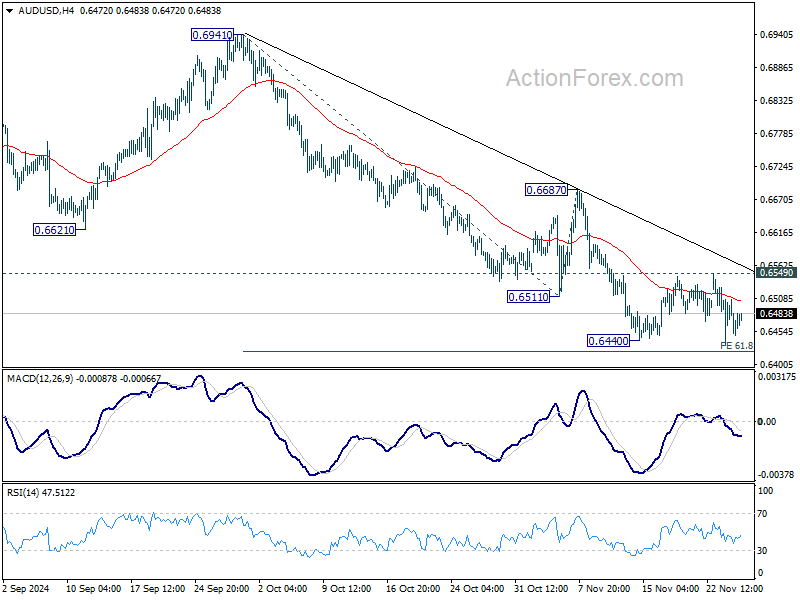

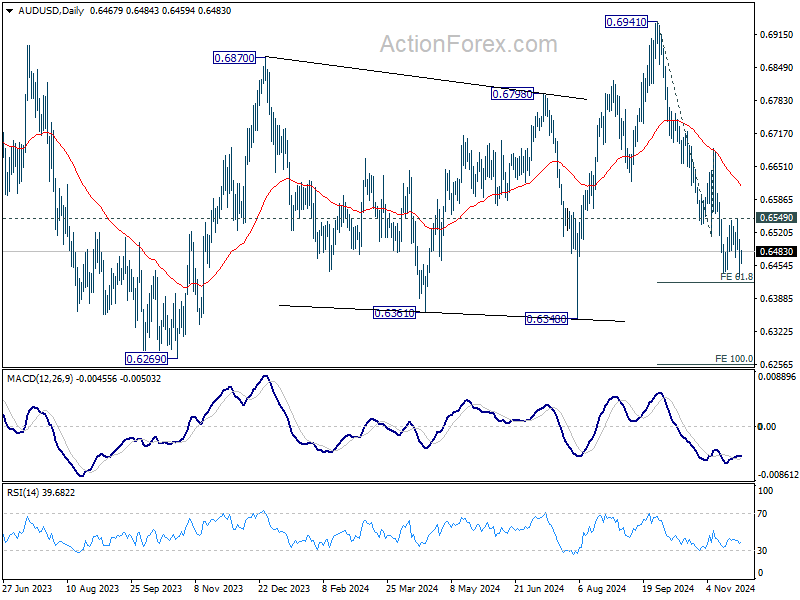

AUD/USD Daily Report

Daily Pivots: (S1) 0.6437; (P) 0.6472; (R1) 0.6511; More...

Intraday bias in AUD/USD remains neutral and more sideway consolidations could be seen. Further decline is expected as long as 0.6687 resistance holds. On the downside, decisive break of 61.8% projection of 0.6941 to 0.6511 from 0.6687 at 0.6421 will resume the fall from 0.6941 to 100% projection at 0.6257 next.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

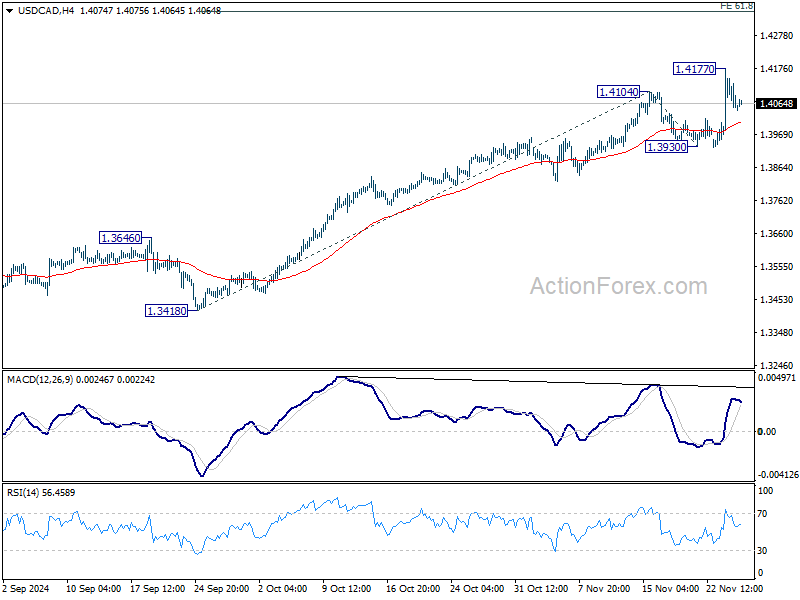

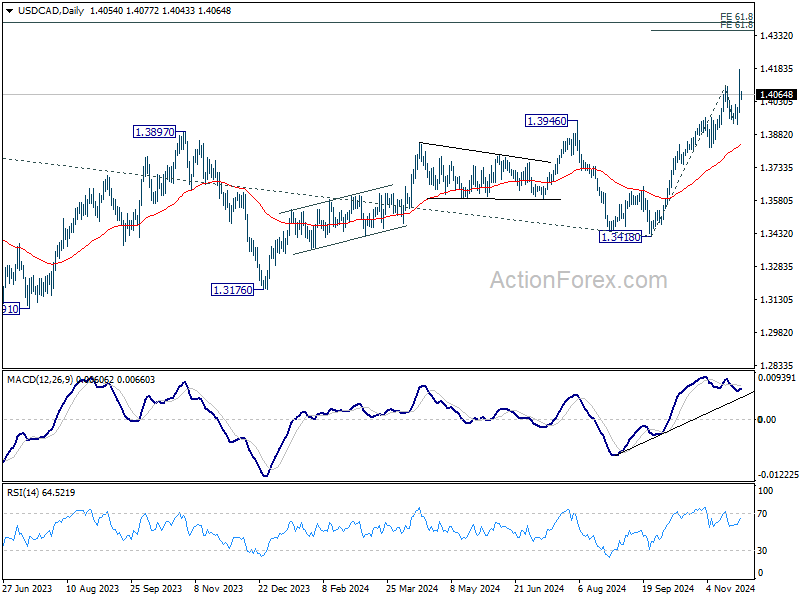

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3958; (P) 1.4068; (R1) 1.4165; More...

Intraday bias in USD/CAD is turned neutral first with current retreat. Further rally is expected as long as 1.3930 support holds. On the upside, break of 1.4177 temporary top will resume larger up trend to 61.8% projection of 1.3418 to 1.4104 from 1.3930 at 1.4354 next.

In the bigger picture, up trend from 1.2005 (2021) is resuming with break of 1.3976 key resistance (2022 high). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

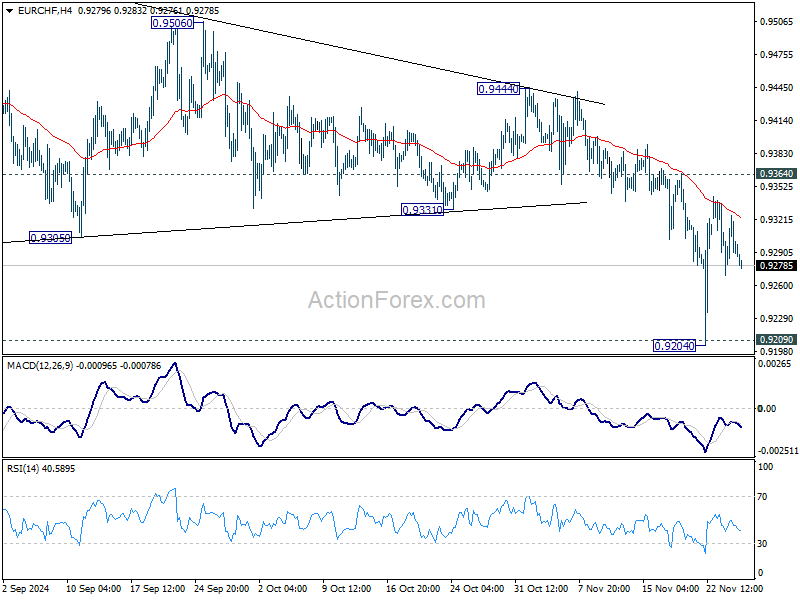

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9281; (P) 0.9313; (R1) 0.9334; More....

Intraday bias in EUR/CHF stays mildly on the downside for the moment. Deeper fall would be seen to retest 0.9204/9 support zone. Decisive break there will indicate larger down trend resumption. For now, outlook will stay bearish as long as 0.9364 resistance holds.

In the bigger picture, outlook will now stay bearish as long as 0.9444 resistance holds. Decisive break of 0.9209 low will resumed long term down trend to 61.8% projection of 0.9772 to 0.9209 from 0.9444 at 0.9096 next.

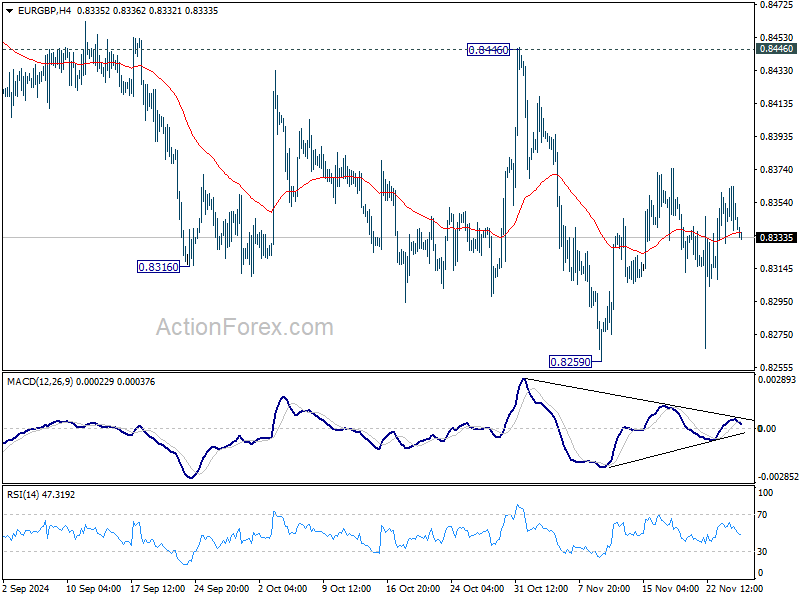

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8330; (P) 0.8347; (R1) 0.8364; More...

Range trading continues in EUR/GBP and intraday bias remains neutral at this point. Outlook stays bearish with 0.8446 resistance intact. On the downside, decisive break of 0.8259 will resume larger down trend to 0.8201 key support.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

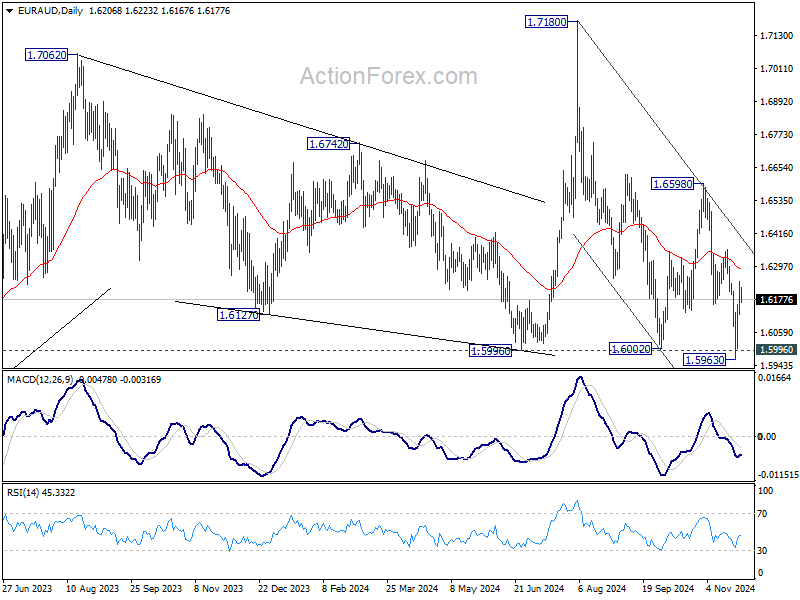

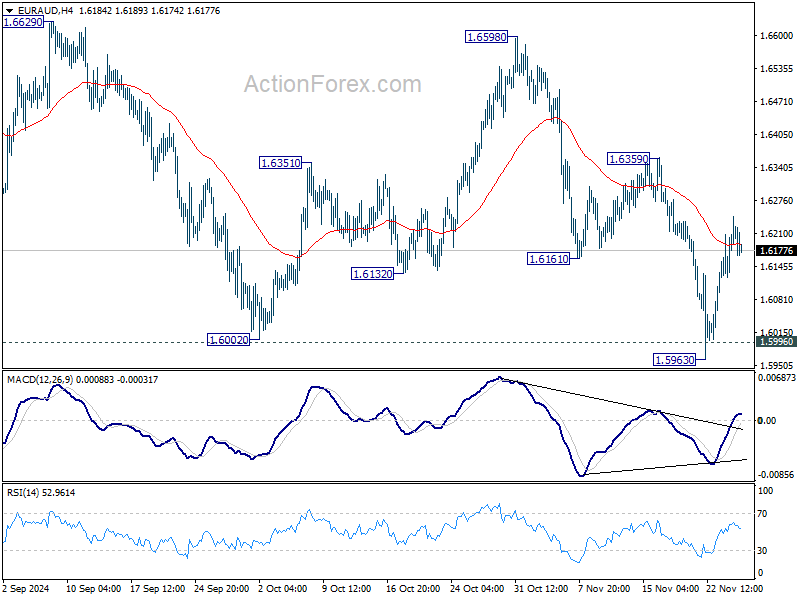

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6137; (P) 1.6191; (R1) 1.6256; More...

Intraday bias in EUR/AUD remains neutral for the moment. Another decline is in favor as long as 1.6359 resistance holds. Sustained break of 1.5996 key support will carry larger bearish implications. However, break of 1.6359 will be the first sign of bullish reversal and target 1.6598 resistance for confirmation.

In the bigger picture, immediate focus is now on 1.5996 key support level. Sustained break there will argue that whole up trend from 1.4281 (2022 low) is already reversing. Deeper decline would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388, even as a correction. Nevertheless, strong rebound from current level, followed by break of 1.6359 resistance, will keep medium term outlook neutral at worst.