Sample Category Title

USD/JPY Mid-Day Outlook

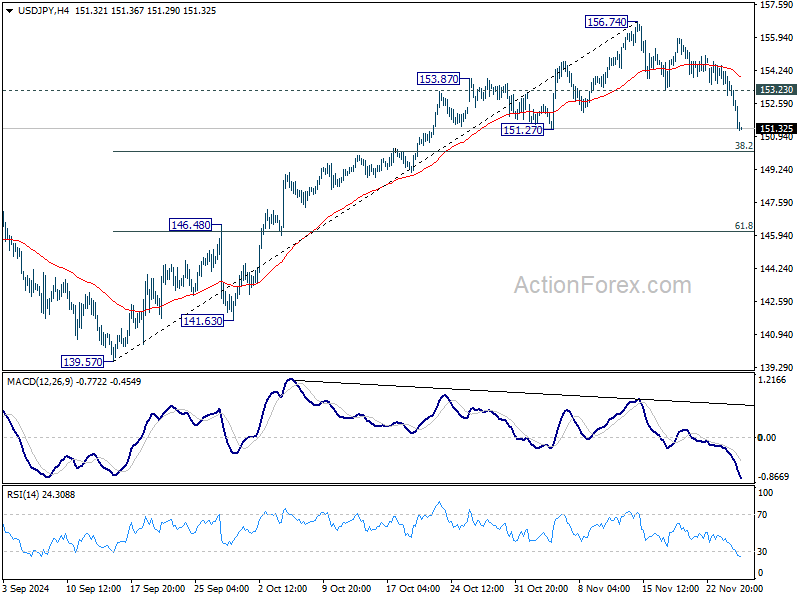

Daily Pivots: (S1) 152.57; (P) 153.53; (R1) 154.07; More...

USD/JPY's corrective fall from 156.74 is extending lower and intraday bias stays on the downside. Deeper fall should be seen to 38.2% retracement of 139.57 to 156.74 at 150.18, but strong support is expected there to bring rebound. On the upside, above 153.23 minor resistance will turn intraday bias back to the upside for retesting 156.74. However, decisive break of 150.18 will argue that whole rise from 139.57 could have completed, and bring deeper fall to 61.8% retracement at 146.12 next.

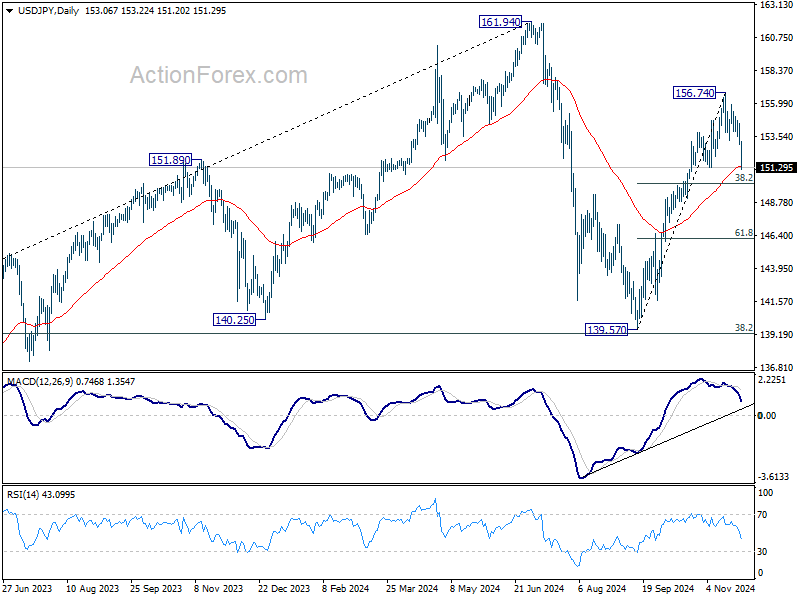

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Yen Leads Markets, Dollar Weakens With Reversal Risks

Yen is asserting dominance in today’s markets, benefiting from notable decline in US and European benchmark treasury yields. US 10-year yield, in particular, is seeing a renewed drop, which is gaining momentum alongside the weakening USD/JPY. This raises the risks that both could be reversing their rallies that began in mid-September. However, with reduced liquidity during the US Thanksgiving holiday, current price actions could be exaggerated, leaving markets to await next week for more definitive trend signals.

Overall in the currency markets, New Zealand Dollar is the second-best performer today after Yen, as investors continue to digest RBNZ's latest rate projections. The central bank’s guidance has left markets divided on whether February will bring another 50bps rate cut or a more modest 25bps adjustment. Meanwhile, Euro ranks third, partly supported by hawkish remarks from a senior ECB official. Despite this, Euro’s movement still appears more like consolidation of its recent losses rather than a clear trend reversal. On the weaker side, Dollar leads the day’s losses, followed by Loonie and Aussie. Both currencies remain under pressure from trade and domestic growth concerns. Sterling and Swiss Franc are holding middle positions.

Technically some attention is now on whether Dollar’s current pullback could evolve into a broader bearish reversal. Key levels to watch include 1.0609 resistance in EUR/USD, 1.2713 resistance in GBP/USD, and 0.8800 support in USD/CHF. A decisive break of these levels across multiple pairs would signal that Dollar’s recent rally is over, paving the way for more sustained downside.

In Europe, at the time of writing, FTSE is down -0.11%. DAX is down -0.37%. CAC is down -0.89%. UK 10-year yield is down -0.0588 at 4.296. Germany 10-year yield is down -0.019 at 2.172. Earlier in Asia, Nikkei fell -0.80%. Hong Kong HSI rose 2.32%. China Shanghai SSE rose 1.53%. Singapore Strait Times fell -0.12%. Japan 10-year JGB yield is up 0.0047 at 1.075.

US initial jobless claims falls to 213k, vs exp 220k

US initial jobless claims fell -2k to 213k in the week ending November 23, below expectation of 220k. Four-week moving average of initial claims fell -1k to 217k.

Continuing claims rose 9k to 1907k in the week ending November 16, highest since November 13, 2021. Four-week moving average of continuing claims rose 13.5k to 1890k, highest since November 27, 2021.

US durable goods orders rises 0.2% mom, ex-transport orders up 0.1% mom

US durable goods orders rose 0.2% mom to USD 286.6B in October, below expectation of 0.4% mom. Ex-transport orders rose 0.1% mom to USD 189.5B, below expectation of 0.2% mom. Ex-defense orders rose 0.4% mom to USD 266.6B. Transportation equipment orders rose 0.5% mom to USD 97.1B.

ECB’s Schnabel advocates gradual approach, cautions against over-easing

ECB Executive Board member Isabel Schnabel stressed the importance of a cautious approach to monetary easing, warning against shifting policy into "accommodative territory."

Speaking to Bloomberg, Schnabel stated that ECB could “gradually move toward neutral” if incoming data continue to align with the bank’s baseline projections. However, she rejected market expectations for accommodative policy, remarking, “From today’s perspective, I do not think that would be appropriate.”

Schnabel also dismissed speculation about larger rate moves, such as half-point cuts, expressing “a strong preference for a gradual approach.”

She cautioned that cutting rates prematurely, even if inflation were to fall short, could be counterproductive if deeper structural issues underlie the economic weakness.

In her view, “the costs of moving into accommodative territory could be higher than the benefits,” particularly as it would deplete policy options needed for future shocks that monetary measures could address more effectively.

Schnabel estimates the neutral interest rate to fall within the 2% to 3% range. With the deposit rate currently at 3.25% after three quarter-point cuts this year, she noted, “we may not be so far” from neutrality now.

Germany’s Gfk consumer sentiment plunges to -23.2, rising concerns over job security

Germany’s GfK Consumer Sentiment Index fell sharply for December, dropping from -18.4 to -23.3, far below expectations of -18.8. This marks the lowest level since May 2024 (-24.0) and reflects a significant deterioration in household confidence as the year ends.

November saw economic expectations decline from 0.2 to -3.6, marking the fourth consecutive drop and the weakest level since February. Income expectations also plunged, falling from 13.7 to -3.5, while willingness to buy slipped further from -4.7 to -6.0. In contrast, willingness to save increased from 7.2 to 11.9, highlighting a defensive shift in household behavior.

“Consumer sentiment in Germany is therefore currently at a level comparable to the end of 2023,” noted Rolf Bürkl, consumer expert at NIM, adding that “consumer uncertainty has increased again recently, as evidenced by the rising willingness to save.” Bürkl highlighted several contributing factors, including rising concerns over job security due to reported job cuts, production relocations, and an uptick in insolvencies.

RBNZ cuts rates by 50bps; projections indicate slower easing ahead

RBNZ delivered a widely expected 50bps cut to its Official Cash Rate, bringing it down to 4.25%. The central bank maintained easing bias, stating that if economic conditions align with projections, “the Committee expects to be able to lower the OCR further early next year.”

Governor Adrian Orr did not rule out another large cut in February during the post-meeting press conference. But RBNZ now forecasts the cash rate will drop to around 3.5% by the end of 2024, signaling smaller moves or pauses to assess the impact of prior easing.

On the economic front, RBNZ expects -0.2% contraction in Q3 2024, followed by recovery to 0.3% growth in Q4. Growth is anticipated to strengthen to a steady 0.6% quarterly rate through 2025 and 2026. “Economic growth is expected to recover during 2025, as lower interest rates encourage investment and other spending,” the central bank noted. .

Inflation is projected to slow from 2.2% currently to 2% by early 2025, but RBNZ forecasts show it picking up again and remaining between 2.0% and 2.5% through early 2027.

Australian CPI steady at 2.1% in Oct, underlying inflation shows mixed trends

Australia’s monthly CPI was unchanged at 2.1% yoy in October, below expectations of a rise to 2.5% yoy. This marks the lowest annual inflation rate since July 2021.

Core inflation metrics presented mixed signals, with CPI excluding volatile items and holiday travel slowing from 2.7% yoy to 2.4% yoy. However, trimmed mean CPI, a preferred gauge of underlying inflation, rose from 3.2% yoy to 3.5% yoy, signaling persistent inflationary pressures in certain sectors.

At the group level, notable price increases were observed in Food and non-alcoholic beverages (+3.3%), Recreation and culture (+4.3%), and Alcohol and tobacco (+6.0%). These were partly offset by a sharp decline in Transport prices, which fell -2.8%, driven by lower fuel costs.

Michelle Marquardt, head of prices statistics at the Australian Bureau of Statistics, noted that "the falls in electricity and fuel had a significant impact on the annual CPI measure this month." She highlighted the value of core inflation measures, such as the trimmed mean, in offering deeper insights into inflation trends amid significant price fluctuations.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.57; (P) 153.53; (R1) 154.07; More...

USD/JPY's corrective fall from 156.74 is extending lower and intraday bias stays on the downside. Deeper fall should be seen to 38.2% retracement of 139.57 to 156.74 at 150.18, but strong support is expected there to bring rebound. On the upside, above 153.23 minor resistance will turn intraday bias back to the upside for retesting 156.74. However, decisive break of 150.18 will argue that whole rise from 139.57 could have completed, and bring deeper fall to 61.8% retracement at 146.12 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

US durable goods orders rises 0.2% mom, ex-transport orders up 0.1% mom

US durable goods orders rose 0.2% mom to USD 286.6B in October, below expectation of 0.4% mom. Ex-transport orders rose 0.1% mom to USD 189.5B, below expectation of 0.2% mom. Ex-defense orders rose 0.4% mom to USD 266.6B. Transportation equipment orders rose 0.5% mom to USD 97.1B.

US initial jobless claims falls to 213k, vs exp 220k

US initial jobless claims fell -2k to 213k in the week ending November 23, below expectation of 220k. Four-week moving average of initial claims fell -1k to 217k.

Continuing claims rose 9k to 1907k in the week ending November 16, highest since November 13, 2021. Four-week moving average of continuing claims rose 13.5k to 1890k, highest since November 27, 2021.

USD/JPY Outlook: Bears Gained Traction and Violate Strong Support Zone

USDJPY extends fresh bearish acceleration into second day and fell 1.1% during Asian / European trading on Wednesday.

Increased demand for yen at the end of month as well as end fiscal year was the main driver of the pair, along with dollar bulls pausing for correction.

Fresh weakness broke below pivots at 152.69 (Fibo 23.6% of 139.57/156.74), 151.97 (200DMA) and dented a higher low of larger uptrend at 151.33 (Nov 5), adding to growing negative signals, which will require confirmation on close below these levels.

Daily studies softened as 14-d momentum slid into negative territory and 10/20/30DMA’s turned to bearish setup, contributing to possible scenario of attack at next pivotal supports at 150.15/00 (Fibo 38.2% / psychological.

Alternatively, failure to clearly break 151.33 trigger would ease current strong downside pressure and probably keep the price in prolonged consolidation range, though with bearish bias expected while the action stays below 153.00 zone.

Res: 151.98; 152.69; 153.00; 153.80.

Sup: 151.22; 151.00; 150.18; 150.00.

EUR/USD Steady Ahead of Major US Data Releases

EUR/USD remains stable at around 1.0483 as markets digest the implications of the latest FOMC minutes. The Federal Reserve signalled a potential pause in rate cuts if inflation reaccelerates but also indicated readiness to continue easing if economic indicators weaken.

Today promises heightened activity for EUR/USD due to a slew of US economic data releases. It is a significant day as the US will release its initial Q3 GDP estimate. After recording a 2.8% growth in Q2, market participants are keen to see if this momentum carried into the third quarter. Expectations suggest a robust period, potentially boosting the US dollar if the data exceeds forecasts.

Additionally, the US will unveil October's figures for personal income and expenses, durable goods orders, and the core PCE price index. These data points could significantly influence the dollar's trajectory, adding to today's trading volatility.

Technical analysis of EUR/USD

H4 chart: The EUR/USD appears to be challenging the upper boundary of its recent downward trend. Current technical analysis suggest a potential upward move towards 1.0580. After reaching this level, a corrective pullback to 1.0460 may occur before another upward wave targets 1.0700. This bullish scenario is supported by the MACD, which shows a positive divergence as it approaches the zero line from below.

H1 chart: The shorter-term H1 chart indicates that EUR/USD is on an upward trajectory towards 1.0580, with the currency consolidating above 1.0460. A breakout above this consolidation could validate the move towards 1.0580. Subsequently, a retracement to 1.0460 may set the stage for further advances. The Stochastic oscillator signals potential upward momentum, suggesting an increase in buying pressure.

CAD/JPY Technical: Another Falling Domino Yen Cross Rattled by Trump’s Tariffs Threat

- A higher beta CAD/JPY cross pair can be considered as a macro theme play in line with a potential risk-averse environment triggered by Trump’s trade tariffs.

- Technical analysis suggests a potential new medium-term downtrend phase for CAD/JPY.

- Watch the 111.45 key medium-term resistance on the CAD/JPY.

US President-elect Trump’s latest trade tariffs salvo, a cornerstone of his “America First” policy has hit his northern neighbour where he threatened to impose 25% tariffs on all Canada’s exports to the US, in retaliation for illegal migration and drug trafficking into the US via Canada’s borders as alleged by Trump on his latest social media posts on his Truth Social site.

Canada is one of the largest trading partners with the US where its exports t are mostly energy-related. Hence if such tariff measures are followed through by the incoming Trump administration, Canda export revenues are likely to take a significant hit which in turn trigger a negative feedback loop in the Canadian dollar.

A higher beta trade can be expressed or played out using the yen crosses; CAD/JPY as a macro theme play to capture such potential adverse impact on the Canadian dollar where the Bank of Canada (BoC) may be forced to introduce more dovish monetary policy stance in 2025 to offset the “higher costs” of its oil-related exports to the US.

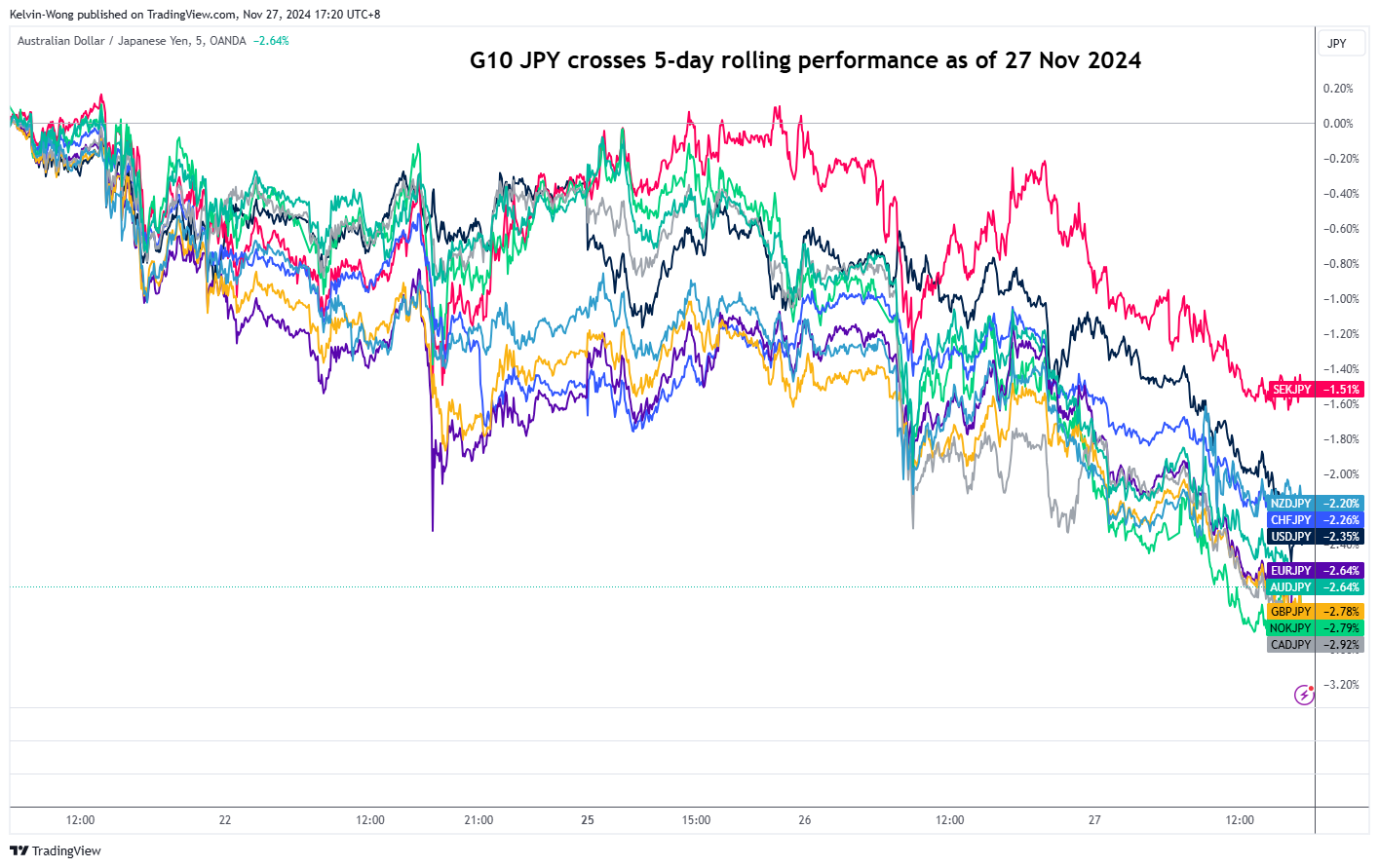

CAD/JPY is the weakest among the G-10 yen cross pairs

Fig 1: G10 JPY cross pairs 5-day rolling performance as of 27 Nov 2024 (Source: TradingView, click to enlarge chart)

The CAD/JPY cross pair has tumbled for two consecutive days with an intraday accumulated loss of 2.1% at this time of the writing and hit a six-week low of 107.82.

Based on a five-day rolling performance basis, the CAD/JPY is now the worst-performing major G-10 JPY cross pair with a loss of -2.9% (see Fig 1).

CAD/JPY at risk of starting a medium-term downtrend

Fig 2: CAD/JPY medium-term & major trends as of 27 Nov 2024 (Source: TradingView, click to enlarge chart)

Key technical analysis elements on the CAD/JPY have suggested an increased risk of a fresh medium-term downtrend phase after it hit a 52-week high of 118.86 on 10 July 2024.

Tuesday, 26 November price action has broken down its 50-day moving average, and the lower boundary of the bearish “Ascending Wedge” configuration.

In addition, the MACD trend indicator has continued to inch toward its zero centreline after a bearish divergence condition flashed out on 14 November 2024.

These observations suggest a potential growing downside momentum factor that may trigger the start of a medium-term downtrend phase for the CAD/JPY.

Watch the 111.45 key medium-term pivotal resistance and a clear break with a daily close below 104.85 exposes the next medium-term supports at 101.80 and 97.55.

On the flip side, a clearance above 111.45 invalidates the bearish scenario for a potential recovery towards the next medium-term resistances of 115.90 and 118.70 in the first step.

NZ Dollar Soars After Central Bank Slashes Rates

The New Zealand dollar has ended a five-day losing streak on Wednesday. In the European session, NZD/USD is trading at 0.5887, up 0.9% on the day.

RBNZ chops rates by 50 basis points

The Reserve Bank of New Zealand lowered its cash rate by 50 basis points today in a widely-expected decision. This brings the cash rate to 4.25%, its lowest level since November 2022. This marked a second straight cut of 50 basis points, as the central bank is showing an aggressive stance to cutting rates.

The rate statement noted that inflation had fallen around the midpoint of the 1%-3% target and if economic conditions evolved as expected, the Bank expected to lower rates early in 2025. Governor Orr echoed this stance in his press conference, as he hinted at another 50-bp rate cut as early as February.

What is suprising is the reaction of the New Zealand dollar, which has surged higher despite the oversized rate cut and the signal of more to come. The RBNZ lowered rates by 50 bp last month and the New Zealand dollar responded with losses of around 1%. This time around, investors may be focusing on the expected positive impact that the rate cut should have on the weak New Zealand economy. As well, some investors had expected a 75-bp cut at today’s meeting and the smaller cut may have boosted the New Zealand dollar.

FOMC minutes: More rate cuts coming

The Federal Reserve released the minutes of the November meeting on Tuesday. At the meeting, FOMC members unanimously voted to cut rates by 25 basis points. The minutes indicated that Fed officials were confident that inflation was falling and the labor market remained strong. Given, this positive outlook, members expected to lower interest rates but no timeline was provided.

NZD/USD Technical

- NZD/USD pushed above resistance at 0.5868 and tested resistance at 0.5901 earlier. The next resistance line is 0.5937

- There is support at 0.5832 and 0.5799

NZD/USD Outlook: New Zealand Dollar Jumps on Disappointment from RBNZ Rate Decision

New Zealand dollar jumps on disappointment from RBNZ rate decision but larger bears remain firmly in play.

Kiwi dollar jumped around 1% against its US counterpart on Wednesday morning after RBNZ’s 50 basis points rate cut disappointed many who expected more aggressive action and cut by 75 basis points.

The Reserve Bank of New Zealand reduced interest rates to 4.25% from 4.75% and signaled further easing, as inflation fell near central bank’s target and the policymakers want to stimulate economy to accelerate the way out of recession.

RBNZ’s statement was dovish and signaled another 50 basis points cut in February, with expectations to reach levels between 2.5% and 3.5%, which is seen as neither restrictive nor accommodative, by the end of 2025.

Although the disappointment from the central bank’s decision prompted some short covering, larger downtrend is unlikely to significantly hurt larger downtrend, as fundamentals are overall negative for Kiwi dollar and technical picture is bearish on daily and weekly chart.

Adding to negative signals was last week’s close below former base at 0.5850 (Apr / July).

Upticks face solid barriers at 0.5910/35 zone (lower top of Nov 20 / 20DMA / Fibo 23.6% of 0.6378/0.5796 downtrend) where recovery should be ideally capped to keep larger bears intact, while sustained break here would signal stronger correction.

Res: 0.5910; 0.5921; 0.5935; 0.5977.

Sup: 0.5900; 0.5816; 0.5796; 0.5773.

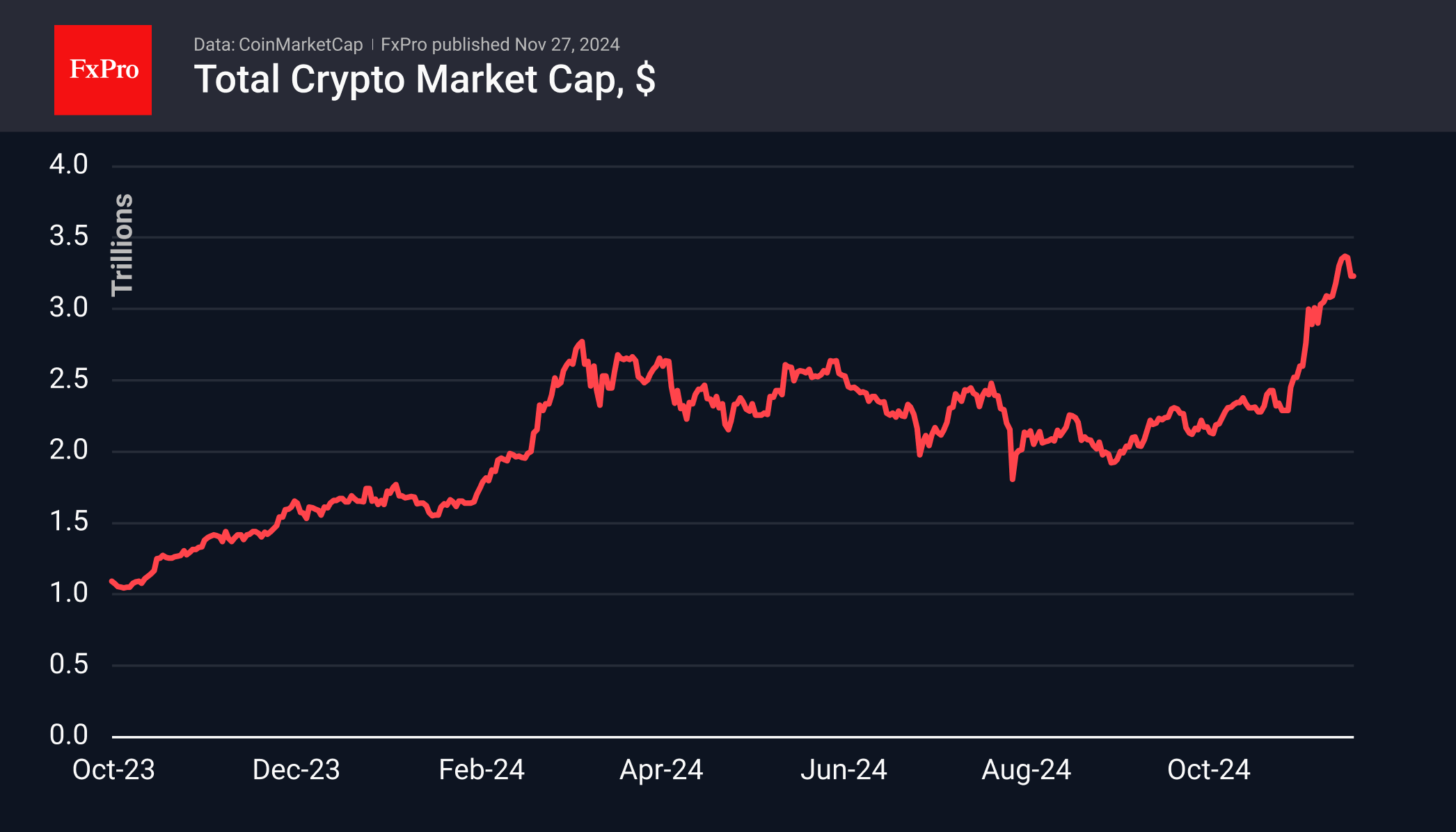

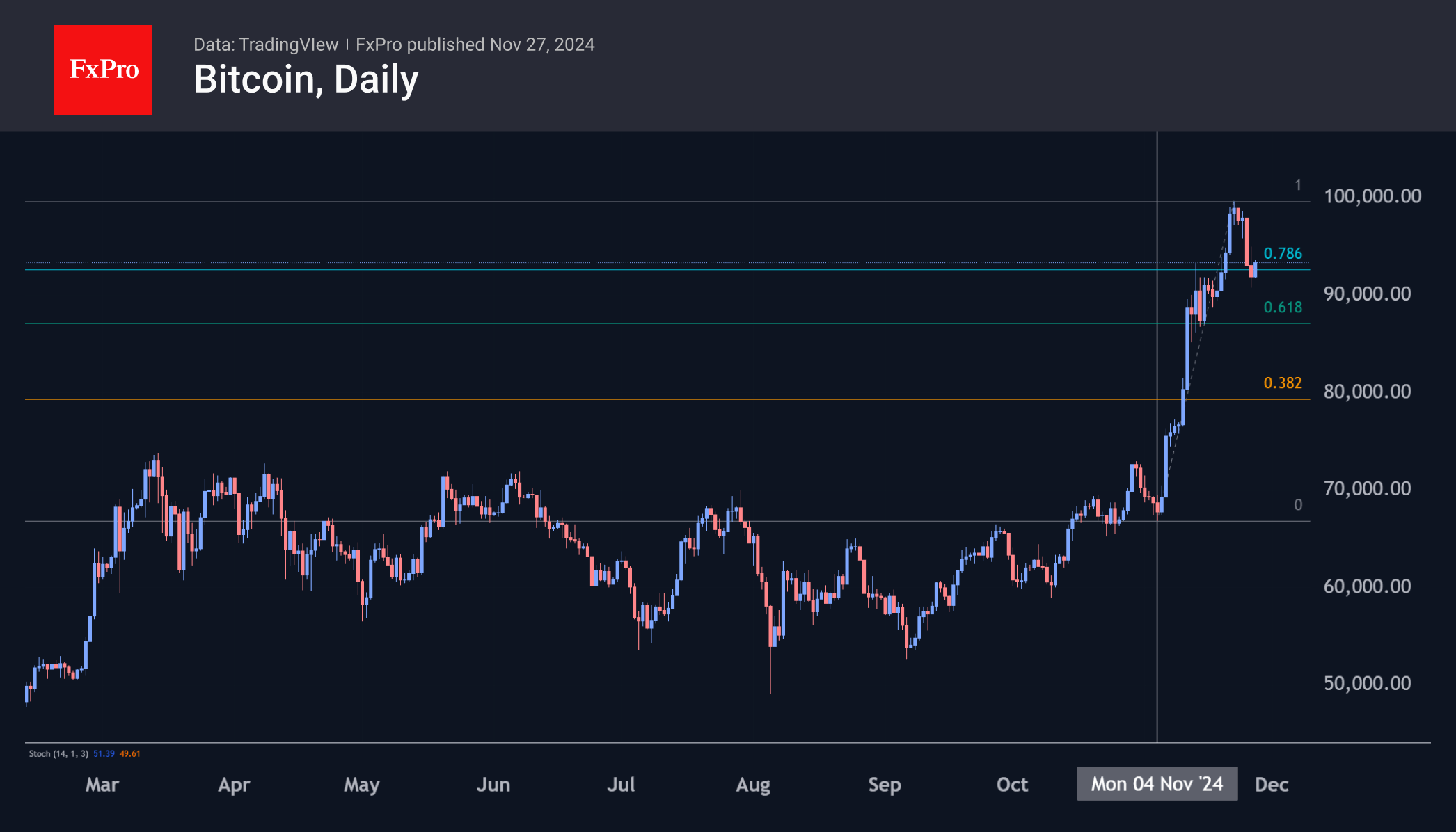

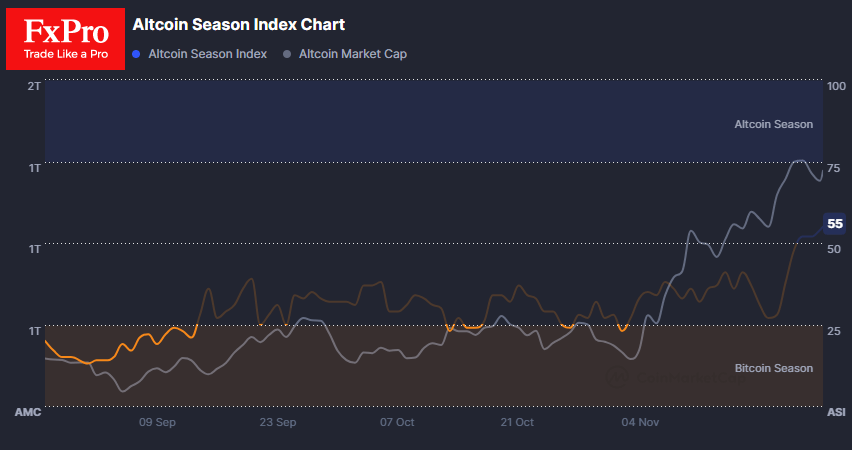

BTC Correction Shifts Attention to Altcoins

Market Picture

The crypto market dipped to a total cap of $3.15 trillion on Tuesday. However, on Wednesday morning, buying prevailed, pushing the capitalisation back above $3.22 trillion, around the same level as the previous day. The return of buyers is boosting hopes of an end to the correction, fuelled by the overwhelmingly positive momentum in equity markets.

A major driver of the recent correction was Bitcoin, which lost almost 9% from peak to trough. Both profit-taking and the cautious sentiment in global markets drove it down. The impact of both factors may be waning at the 76.4% retracement of the rally from the November lows, a strong level in strong bull markets.

Bitcoin’s recent pullback gave altcoins a chance to catch up. The Altcoin Season Index has risen to 54, a new high for the year and an impressive rise from 27 in the last six days. This is an indirect confirmation that Bitcoin’s recent correction is due to a search for more profitable alternatives rather than a fundamental change in sentiment. As such, we expect the crypto market to return to historic highs soon, with altcoins being the driving force. However, this does not negate the renewal of the highs of the first cryptocurrency.

News Background

Bitcoin’s path to the psychological level of $100K has “stalled” against the backdrop of the liquidation of longs for $430 million and increased concerns about the publication of the Federal Reserve meeting minutes and inflation data, notes CryptoQuant. The situation could be exacerbated by the upcoming US Thanksgiving holiday on 28 November.

According to DeFi Llama, Ethereum has regained dominance of the USDT stablecoin offering after TRON took the lead in August 2022. The ETH blockchain has issued $60.3 billion worth of tokens, compared to nearly $58 billion on its rival’s network.

In November, trading volume on the decentralised exchanges (DEX) on the Solana network reached a record $109.8bn, almost twice as high as Ethereum’s. The previous monthly record was set in March 2023. In both cases, such high levels can be attributed to the hype surrounding meme coins.

Tron founder Justin Sun has become the largest investor in World Liberty Financial, the crypto platform linked to Donald Trump’s family. He bought 2 billion WLFI tokens worth $30 million.

Maya Parbho, a presidential candidate for Suriname, the South American republic, has announced plans to recognise Bitcoin as legal tender and move the country’s financial infrastructure to blockchain.