Sample Category Title

EU Walking the Tariff Talk Against Chinese Electric Vehicles.

Markets

UK gilts underperformed yesterday. Yields with maturities ranging from the 2-yr (+5.1 bps) to the 10-yr (+6.1 bps) all hit five month and post-election highs. The spring Budget, due to be presented later today, is a key moment for the new Labour government and for markets. UK debt sales are expected to rise to the second-highest on record (£300bn) this year, trumped only by the pandemic-stricken years. This time, however, there’s no central bank buying bonds en masse, on the contrary. Labour needs to plug a £40bn hole and wants to invest in infrastructure and public services. With taxes already headed to their highest in decades, cutting expenditures (which usually enjoys little political appetite) and borrowing are the remaining options. By broadening the definition of “debt”, Chancellor Reeves created some £50bn additional borrowing room for future years without breaching the long-term debt reduction targets. Markets are on edge and rightly so. Expansionary fiscal policy may limit the central bank’s ability to cut rates. Sterling welcomes the (front end) interest rate support for now but we doubt whether that’s also going to be the case if rising (credit) risk premia take over at the long end of the curve. EUR/GBP tested 0.83 support yesterday; GBP/USD settled back above 1.30. German rates rose a couple of basis points too, from 3.4-5.7 bps. UST’s parted ways. Yields whipsawed on weaker JOLTS and stronger US consumer confidence before a smooth $44bn 7-yr auction (contrasting with the 2-yr and 5-yr one) settled the debate. Net daily changes varied between -2.8 bps to -4.3 bps. EUR/USD 1.076-1.0778 support lived to fight another day. Strong after-market results from Alphabet and reports of additional Chinese stimulus – likely to be announced at a top meeting next week – failed to inspire Asian trading this morning. Japan is an outlier with recent JPY weakness (USD/JPY 153.4) being the driver of current stock outperformance (+0.5-1%). Q3 GDP growth and inflation features the agenda today. The amount of data may trigger intraday FI and FX volatility but makes directional calls tricky. We expect in any case to see ongoing divergence between the US and Europe with the former growing triple the speed of the latter (2.9% q/q annualized vs 0.2% q/q). The split within the euro area between the ailing core (Germany) and outperforming periphery (Italy, Spain) will most likely deepen. First national CPI prints are due in Germany, Belgium and Spain while the US publishes Q3 PCE deflators. The ADP job report serves as an appetizer for Friday’s payrolls. Both are expected to reflect a significant hurricane-related impact. More tech giants including Microsoft and Meta Platforms report after market.

News & Views

Headline Australian inflation rose by 0.2% Q/Q in the July-September quarter, down from a 1% Q/Q pace in Q2 and printing slightly below consensus (0.3%). Inflation slowed from 3.8% to 2.8% in Y/Y-terms, moving within the Reserve Bank of Australia’s 2-3% inflation target band for the first time since Q1 2021. While prices continued to rise for most goods and services, these increases were offset by large falls for electricity (-17.3%) and automotive fuel prices. (-6.7%). Without rebates (2024-2025 Commonwealth Energy Bill Relief Fund & state-specific discounts) electricity prices would have increased by 0.7% Q/Q. The decline in annual goods inflation from 3.2% Y/Y to 1.4% Y/Y was also down to electricity and gas prices. Annual services inflation rose from 4.5% Y/Y in Q2 to 4.6% Y/Y. Higher prices for rents, insurance and child care were the main contributors. Underlying core measures, like the trimmed mean which filters for the biggest price swings, also point to more stubborn price pressures, keeping the Q2 pace of 0.8% Q/Q in Q3 and only slowing from 3.9% Y/Y to 3.5% Y/Y. Today’s numbers warrant the RBA’s current higher-for-longer approach, suggesting that a first rate cut will effectively only be for Q2 2025. AUD/USD abides by the rules of USD-strength this month, dropping back from 0.69+ end Q3 to 0.6550 currently.

The EU is walking the tariff talk against Chinese electric vehicles. Brussels yesterday announced levies that will come into force today and last for five years. The new duties come on top of an existing 10% tariff on Chinese car imports to the EU. Extra tariffs depend on the manufacturer and range from 7.8% to 35.3%. Earlier this year, the US raised tariffs on Chinese EV’s to more than 100% citing extensive government subsidies. The EU’s decision risks triggering retaliation on goods ranging from dairy over pork and brandy to cars with large engines. The latter could be increased from the current 15% to 25%.

Alphabet Beats, Eyes on UK Budget, US Jobs, Eurozone CPI

Big Tech investors weren’t disappointed on Tuesday, as Alphabet announced better than expected results after the bell. The Google’s parent Alphabet saw its revenue rise 15% from the same time last year, ad revenue grew more than anticipated and more importantly, Google Cloud printed a solid 35% growth compared to the same time last year. The division earned $11.4 billion last quarter, comfortably above the $10.5bn revenue pencilled in by analysts. Google was up by around 1.66% yesterday before the earnings and rallied nearly 6% after the bell. It could have performed better if not for the serious regulatory issues it’s facing, including an antitrust trial questioning its monopolistic position. The trial could require the company to divest major assets like Android, Google Play, or Chrome. Rough. But anyhow, Alphabet’s latest beat serves as a fresh rebuttal to investors who fear a slowdown in AI demand.

And indeed, news at AMD were not enchanting. One of Nvidia’s biggest rivals gave a lacklustre revenue forecast for the current quarter, a message that raised worries about potentially slowing AI sales. Today, it’s Microsoft and Meta’s turn to reveal how well they did last quarter. The earnings announcements will continue with Apple and Amazon on Thursday – and Exxon and Chevron on Friday.

But the latter may be less enthusiastic than the tech peers. BP announced its quarterly results yesterday and they were mixed. The company reported the slowest profit growth in nearly four years due to weak oil prices. That was better than expected and topped with a $1.75billion buyback program. Alas, the company warned that it could change their strategy of buying back $1.75bn worth of shares every three months due to weak oil and gas prices. The shares slumped 5%.

Speaking of oil prices, the barrel of US crude remained under a selling pressure yesterday, and is slightly better bid this morning on the back of a small decline in US oil inventories (API) but trend and momentum indicators remain tilted to the downside and strong resistance is eyed near the $70pb psychological level, which also matches the minor 23.6% Fibonacci retracement on July to September selloff. The fading geopolitical tensions that were supportive of the bulls until this week have left their place to Chinese growth worries and supply/demand discussions – which both are negative for oil prices. In fact, World Bank thinks that global oil supply will exceed demand by 1.2mbpd next year. That makes me wonder whether OPEC might step in to put a floor under a more severe selloff.

Data

On the data front, the first glimpse at the US jobs numbers were soothing for the Federal Reserve (Fed) doves. The JOLTS data released yesterday showed that job openings in the US fell to their lowest levels since 2021, and Atlanta Fed’s GDP Now forecast dived below 3%. As such, the US 2-year yield is now testing the 4% level to the downside, and the US 10-year yield consolidated near 4.25%. The US dollar index eased after hitting a fresh high since summer.

Today, all eyes are on the ADP report. Analysts expect that the US economy may have added around 110K new private jobs in October. A softer-than-expected data could further back the Fed doves and weigh on the US dollar, whereas a strong-looking data will probably do little to erode the rate cut bets until we have more clarity from Thursday’s GDP and core PCE figures and Friday’s official jobs report.

But before, we have a mountain of figures to digest from elsewhere. Earlier today, Australia revealed higher-than-expected inflation in the Q3. But the September figure was lower than pencilled in by analysts and kept the Aussie bears in charge of the market. The AUDUSD continued to advance toward the 65 cents level, pressured by a broadly stronger US dollar and softer iron ore prices on worries that the Chinese stimulus measures won’t be enough to stimulate desired growth and support iron ore prices.

Here in Europe, the major Eurozone countries will be revealing their October preliminary CPI numbers today – expected to show an uptick in headline figures for October. If that’s the case, we could see the euro bears give back field and let the EURUSD rebound after a 4 figure selloff since the end of September. First resistance is eyed at 1.0870, near the minor 23.6% Fibonacci retracement on that selloff and the 200-DMA, and the key resistance sits at 1.0935, the major 38.2% Fibonacci retracement. These resistances could be seriously challenged in case of surprisingly weak jobs data from the US this week.

Elsewhere, Cable is testing the 1.30 level ahead of today’s budget announcement, amid hopes that Rachel Reeves will handle the announcement of the largest tax increase in recent times with enough tact, and the USDJPY is consolidating above 153 ahead of tomorrow’s Bank of Japan (BoJ) decision, which is expected to bring nothing new to the table, if not a pledge of more support for the economy amid rising political uncertainties.

Bitcoin reached the highest levels since March on the back of rising odds for a Trump win – which is also sending Trump’s Media and Technology Group shares skyrocketing since five weeks. The prediction markets assess more than 60% chance for a Trump win at next week’s presidential election, while the latest CNN poll gives 47% chance of winning to both candidates, making the Trump-friendly assets’ gains vulnerable.

US and Euro Area Q3 GDP Releases Today

In focus today

In the US, ADP's October private sector employment report and flash Q3 GDP will be released in the afternoon. ADP's figures could provide some early hints of what to expect from Friday's key non-farm payrolls release. We expect that GDP expanded 2.5% on annualized q/q basis (Q2: 3.0%) largely driven by still solid private consumption.

In the euro area, we receive the preliminary estimate of GDP growth in Q3 of 2024. The German economy likely stagnated or contracted slightly in the third quarter while strong growth in Southern Europe combined with the Olympic Games in France should leave overall euro area growth in positive territory. Hence, we forecast GDP growth of 0.2% q/q like in the first quarter, driven by service providers while the manufacturing sector likely was a drag on activity.

In the UK, Chancellor Rachel Reeves is set to announce the Labour government's first budget in the afternoon. We will likely see a budget more expansionary than previously. The budget is set to be "all about investments". So, expect increase in public investments, and particularly the NHS. The shortfall is likely to be covered by a large increase in taxes with estimates indicating up to GBP 40bn. The BoE will judge the measures at its upcoming meeting on 7 November and to what extent it might alter the inflation outlook.

In Japan, we expect no changes from the BoJ early Thursday. Governor Ueda will probably try to find a less dovish tone at the meeting to avoid adding to the recent yen slide. After all, inflation is on target and consumers' purchasing power is heading in the right direction now.

Economic and market news

What happened overnight

In Australia, CPI was released for Q3 deviating only slightly from consensus with 2.8% y/y (cons: 2.9%, prior: 3.8%).

What happened yesterday

In the US, the JOLTs report for September showed a sharp decline in US job openings with 7.44M (cons: 8.00M, prior: 7.86M). The Fed uses the figure as a proxy for overall labour demand, and thus the decline suggests that labour markets remain on a cooling trend. The overall level of layoffs has been rising gradually, but in a historical context it remains low. The ratio of job openings to unemployed job seekers declined slightly to 1.09. This should allow the Fed to continue cutting rates at the coming meetings.

The Conference Board's October consumer survey showed a notable uptick in optimism both with regards to current economic conditions as well as the future outlook. These somewhat mixed signals released at the same time led to a very muted market reaction.

In Sweden, Q3 GDP growth dropped 0.1% in both q/q (cons: 0.4) and y/y (cons: 0.7). The indicator however should be treated with caution, but the Riksbank's own company survey paints a gloomy picture as well. The survey showed more negative sentiment compared to the latest one in May. Combining these two the overall picture seems a bit more negative than the Riksbank's base scenario, which is that a growth recovery next year will keep inflation close to the 2% target.

In Japan, the head of the opposition Democratic Party for the People (DPP), which would be critical to form a government in Japan, stated on BoJ: "Once there is certainty that real wages will exceed 4% at next year's spring wage negotiations, that's when the BoJ can review monetary policy". This reflects the risk of political resistance to tightening policies that BoJ will meet.

Equities: Global equities were marginally higher yesterday, but notably, most sectors were lower. The overall lift was facilitated by higher tech stocks in the US. In the US, the group of cyclicals was higher, while defensives were lower. In Europe, 21 out of 25 industry groups were lower, but cyclicals still outperformed, and banks were higher. This type of odd rotation is very much linked to reporting, but it is also worth noting that it does not result in higher indices overall despite the cyclical outperformance. For the record, with tech outperformance yesterday, Nasdaq achieved its first record closing since 10-July. In the US yesterday: Dow -0.4%, S&P 500 +0.2%, Nasdaq +0.8%, and Russell 2000 -0.3%. Asian markets are broadly lower this morning, with Japan running its own course, being higher despite only a marginal weakening of the yen this morning. European futures are lower this morning, while US futures are again mixed.

FI: Markets recorded a 3bp Bund-ASW spread tightening to hit a low of 11bp. The German swaps spreads against €STR are all negative now. Front end (ECB pricing) was 4bp higher in the 2025 segment and points to 103bp of cuts next year.

FX: A relatively calm start to the week without any major G10 FX moves. EUR/USD remains just above the 1.08 mark, while USD/JPY has stabilized above 153 - only four figures below the level where Japanese authorities last intervened in FX markets in early May this year. EUR/GBP faced renewed pressure during yesterday's session, with the cross briefly dipping below the 0.83 mark. NOK saw a slight rebound yesterday, bringing EUR/NOK below 11.85, while EUR/SEK is still hovering just above 11.50.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0783; (P) 1.0804; (R1) 1.0840; More...

Intraday bias in EUR/USD remains neutral as consolidations continues above 1.0760. Further decline is expected as long as 1.0871 resistance holds. Below 1.0760 will target 61.8% retracement of 1.0447 to 1.1213 at 1.0740. Firm break there will target 1.0601 support next. However, considering bullish convergence condition in 4H MACD, break of 1.0871 will indicate short term bottoming, and turn bias back to the upside for 55 D EMA (now at 1.0946).

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

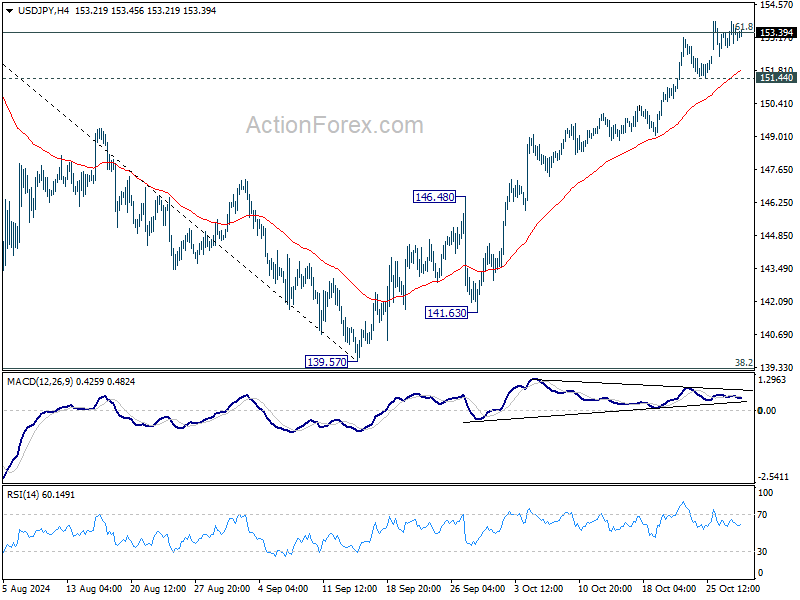

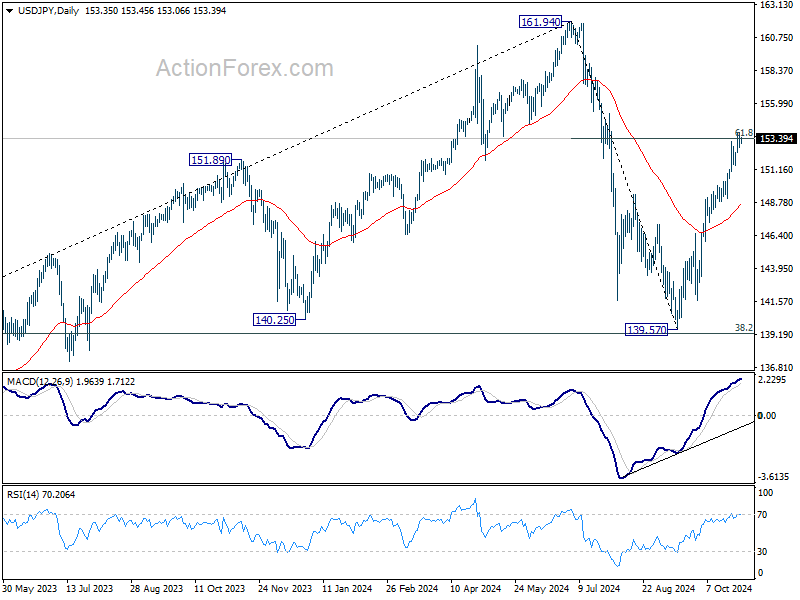

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.80; (P) 153.33; (R1) 153.92; More...

No change in USD/JPY's outlook and intraday bias stays on the upside. Sustained trading above 61.8% retracement of 161.94 to 139.57 at 153.39 will pave the way to retest 161.94 high. On the downside, below 151.44 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

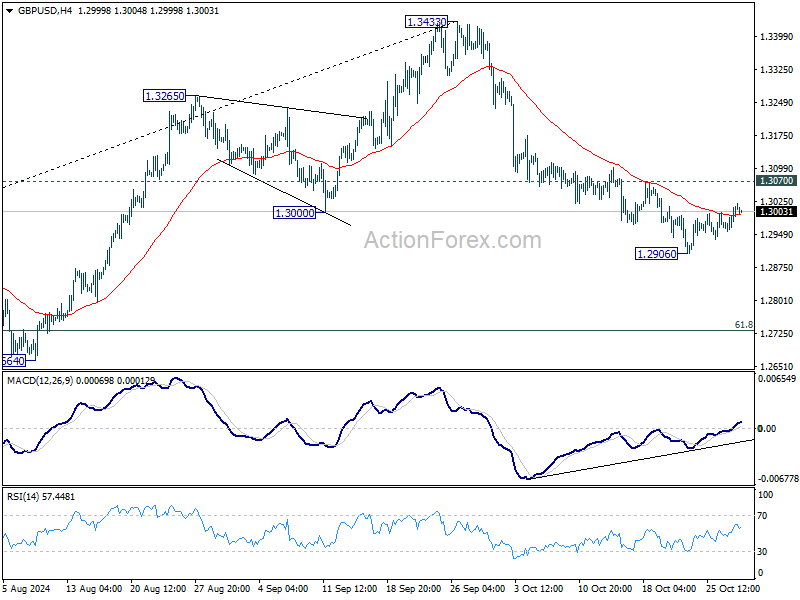

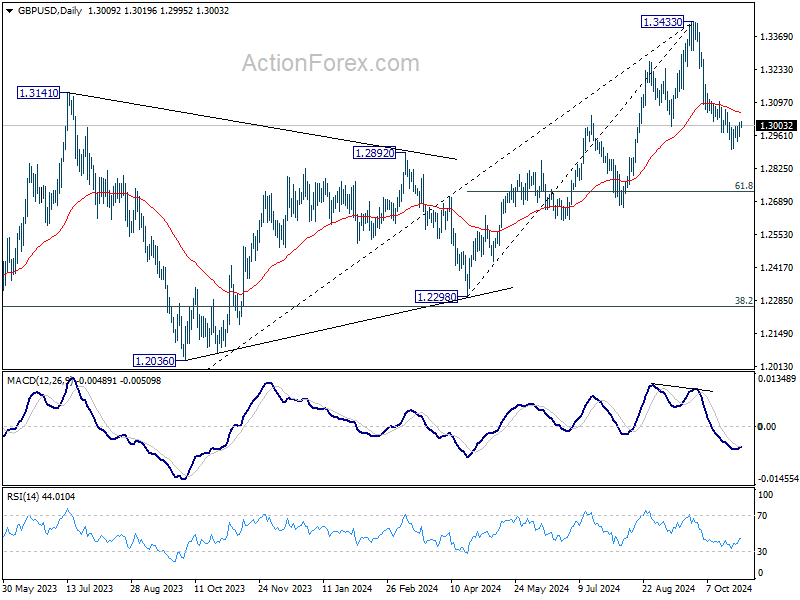

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2976; (P) 1.2996; (R1) 1.3033; More...

Intraday bias in GBP/USD remains neutral as GBP/USD is still extending consolidations above 1.2906. Further decline is expected as long as 1.3070 minor resistance holds. Below 1.2906 will target 61.8% retracement of 1.2298 to 1.3433 at 1.2732. However, considering bearish divergence condition in 4H MACD, firm break 1.3070 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

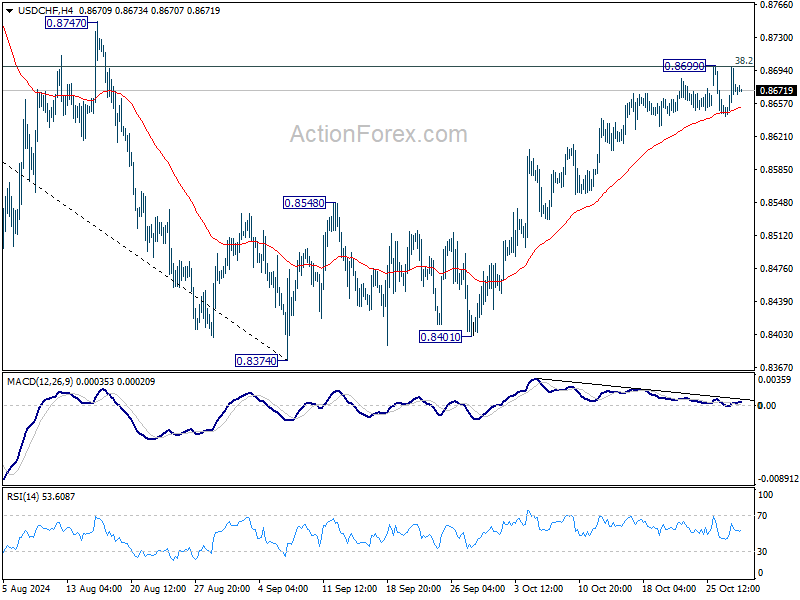

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8646; (P) 0.8672; (R1) 0.8700; More…

Intraday bias in USD/CHF remains neutral and more consolidations could be seen below 0.8699 temporary top. But further rally remains in favor as long as 55 D EMA (now at 0.8608) holds. On the upside, decisive break of 38.2% retracement of 0.9223 to 0.8374 at 0.8698 will argue that fall from 0.9223 has completed after defending 0.8332 low. Further rally should then be seen to 61.8% retracement at 0.8899 next.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

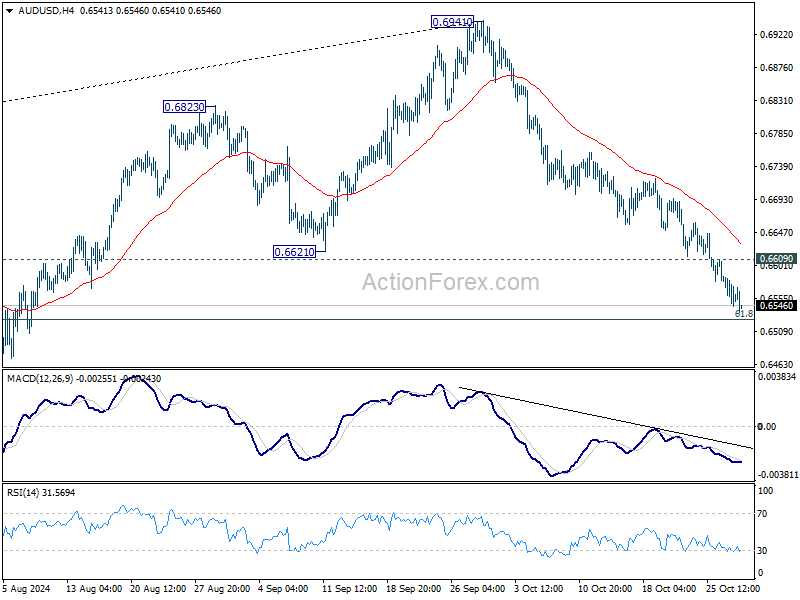

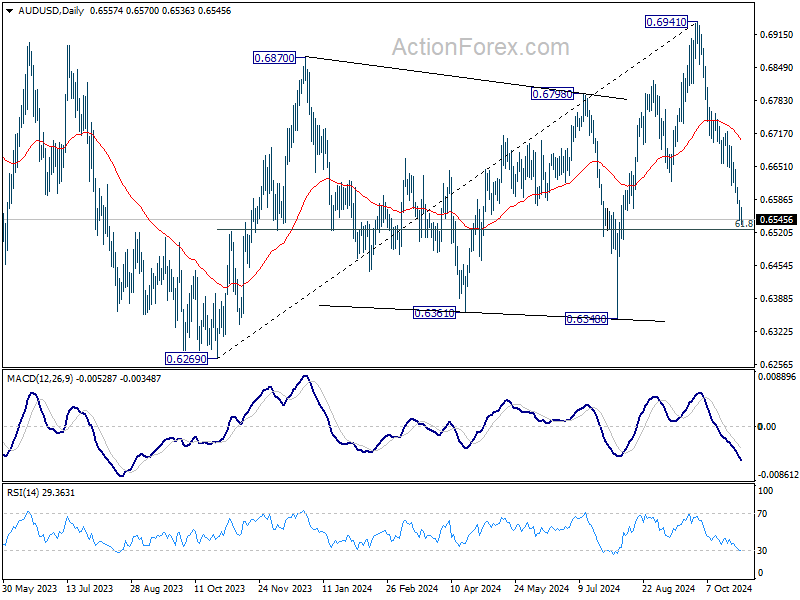

AUD/USD Daily Report

Daily Pivots: (S1) 0.6539; (P) 0.6567; (R1) 0.6589; More...

Intraday bias in AUD/USD remains on the downside, as decline from 0.6941 is in progress for 61.8% retracement of 0.6269 to 0.6941 at 0.6526. Sustained break there will target 0.6348 support next. On the upside, above 0.6609 minor resistance will turn intraday bias neutral and bring consolidations first.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3885; (P) 1.3908; (R1) 1.3938; More...

Intraday bias in USD/CAD remains on the upside as rally from 1.3418 is in progress for retesting 1.3946/76 resistance zone. Decisive break there will confirm larger up trend resumption. On the downside, below 1.3875 minor support will turn intraday bias and bring consolidations first.

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage. Decisive break of 1.3976 will target 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391.

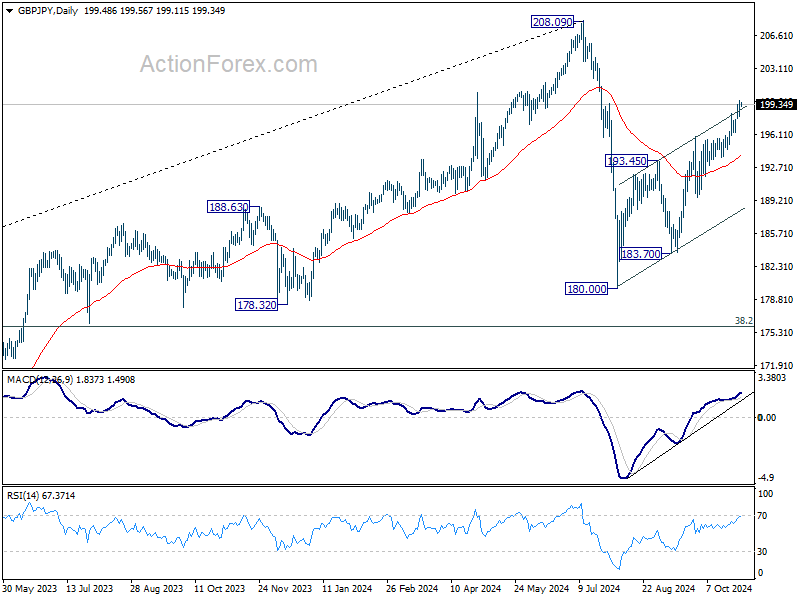

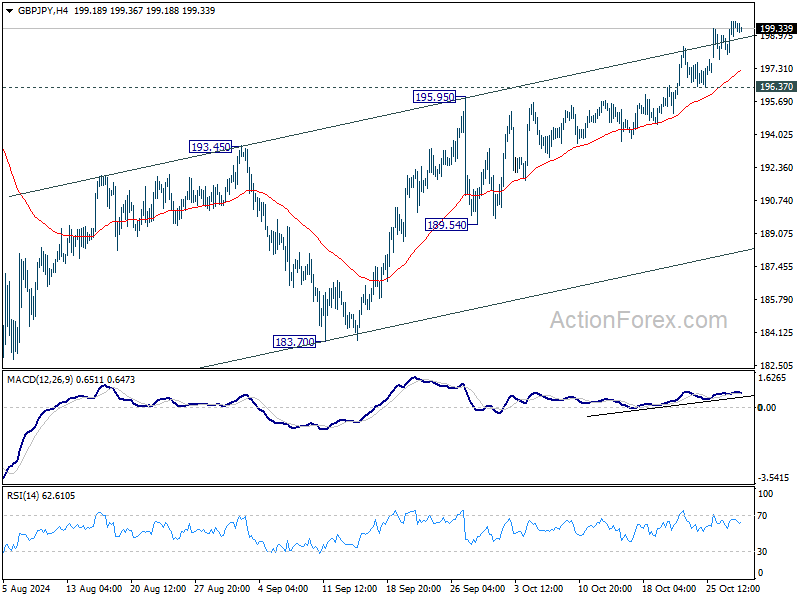

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.52; (P) 199.12; (R1) 200.20; More...

GBP/JPY's rally from 180.00 is in progress and intraday bias stays on the upside. Next target is a retest on 208.09 high. On the downside, below 196.37 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.