Sample Category Title

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1677; (P) 1.1709; (R1) 1.1764; More….

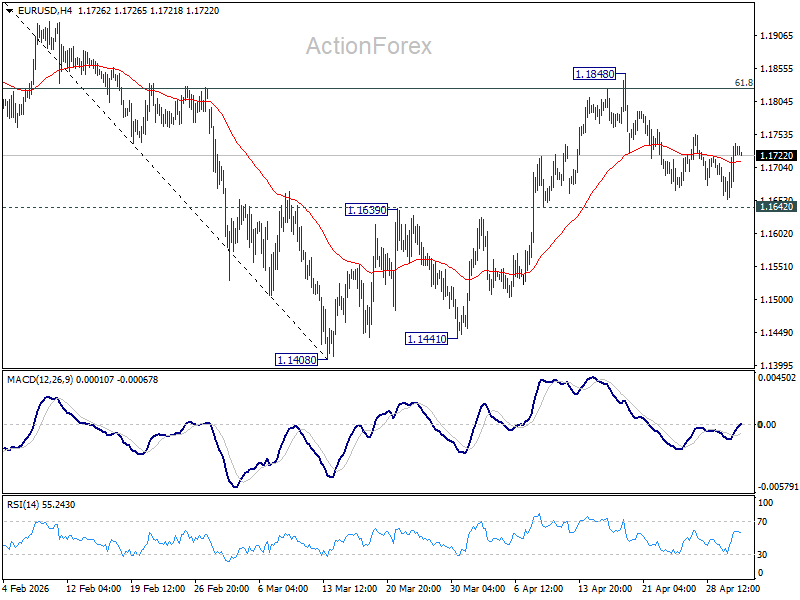

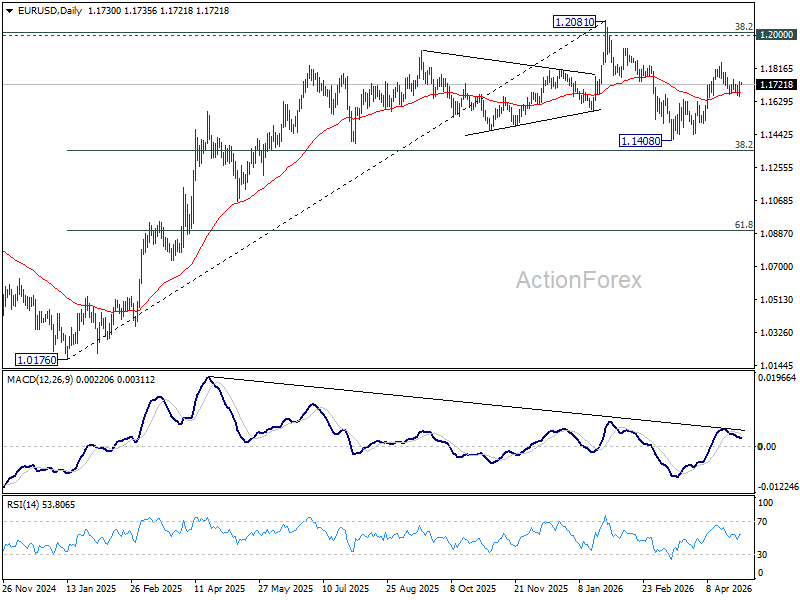

Range trading continues in EUR/USD and intraday bias remains neutral. Further rise will remain in favor as long as 1.1642 support holds. On the upside, sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1642 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1530). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

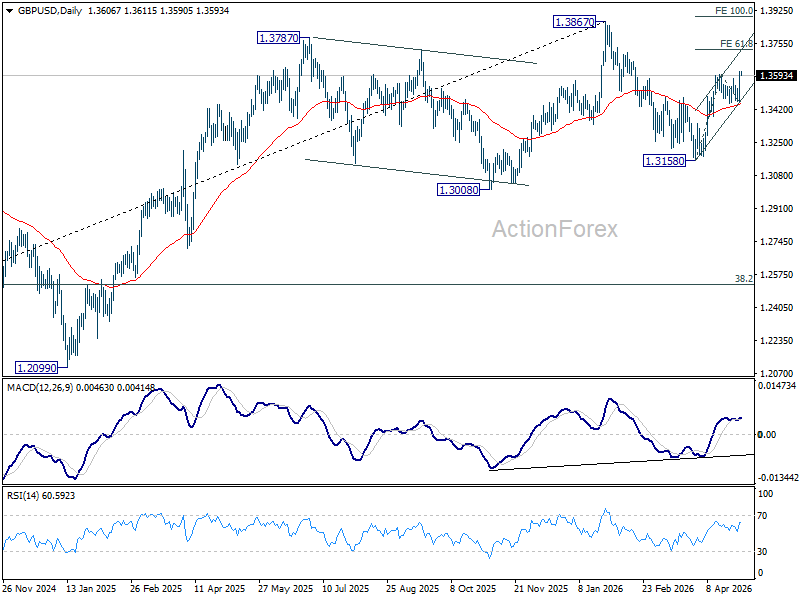

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3502; (P) 1.3557; (R1) 1.3660; More...

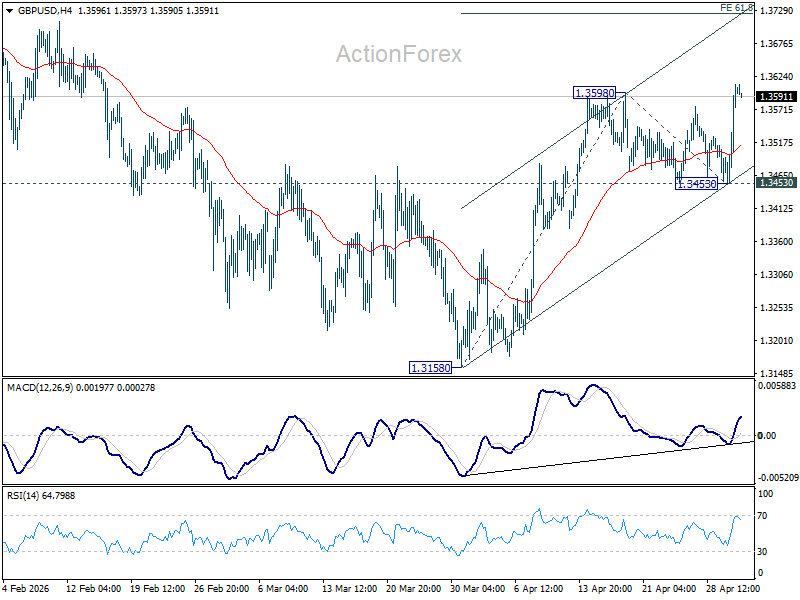

GBP/USD's breach of 1.3598 suggests that rise from 1.3158 is resuming. Intraday bias is back on the upside for 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high. For now, risk will stay on the upside as long as 1.3453 support holds, in case of retreat.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

Dollar Selloff Accelerates as Risk Rally and Yen Surge Take Hold

Dollar is losing ground quickly as markets move into May, caught between a powerful risk rally and a sharp rebound in the Japanese Yen. What stands out is not just the scale of the move, but the shift in market priorities—growth optimism is now outweighing both geopolitical risks and inflation concerns.

The risk-on tone is being driven by a standout earnings season. Alphabet delivered a blockbuster quarter, with its cloud business posting 63% growth—the fastest since 2020—offering clear evidence that the AI boom is translating into real revenue. This has helped push S&P 500 and NASDAQ to fresh record highs, reinforcing confidence that corporate America can sustain growth even in a high-rate environment.

That confidence is not limited to tech. Caterpillar provided strong forward guidance, effectively giving the “all-clear” signal for the industrial sector. Its outlook suggests that infrastructure and energy demand remain robust, and that the broader economy is holding up better than many had feared.

At the same time, markets are showing a remarkable ability to look past geopolitical risks. The surge in oil prices earlier this week and ongoing tensions around Iran have failed to derail sentiment. Instead, investors are treating these developments as background noise, focusing on earnings and growth instead.

Yen, however, is anything but background noise. After sliding past 160 earlier in the week, USD/JPY has reversed sharply, with the Yen staging a powerful rebound. The move has been driven by what traders see as a “final warning” from Japanese authorities, triggering a rapid unwind of short positions.

Japan’s top currency diplomat declined to confirm direct intervention, stating, “I won’t comment on what we’ll do ahead,” while noting that Golden Week holidays have begun. However, the market has largely interpreted recent developments as a “de facto” confirmation of action.

Adding to that perception, Japan’s Nikkei reported, citing government sources, that both the Ministry of Finance and the Bank of Japan had stepped in. In Japan’s communication framework, such reporting is often seen as an unofficial signal, reinforcing the credibility of intervention and amplifying its market impact.

In practice, it may not matter whether Japan has actually intervened. The market has acted as if it has. Short Yen positions have been aggressively covered, and fresh longs are emerging as traders bet that authorities will continue to defend the currency.

The combined effect of risk-on flows and Yen strength has left Dollar under broad pressure. For the week, Yen is the clear outperformer, while Dollar is the weakest. Loonie and Aussie are benefiting from the risk backdrop, while Euro and Kiwi are lagging. Sterling sits in the middle, supported by a mildly hawkish signal from the Bank of England.

In Japan, at the time of writing, Nikkei is up 0.61%. 10-year JGB yield is down -0.019 at 2.506. Hong Kong, China and Singapore are on holiday. Overnight, DOW rose 1.62%. S&P 500 rose 1.02%. NASDAQ rose 0.89%. 10-year yield fell -0.03 to 4.39.

Tokyo Inflation Cools to Multi-Year Low, but Energy Risks Point to Rebound Ahead

Tokyo inflation is cooling—but not for long. Subsidies are masking price pressures as energy costs threaten a rebound. Read More.

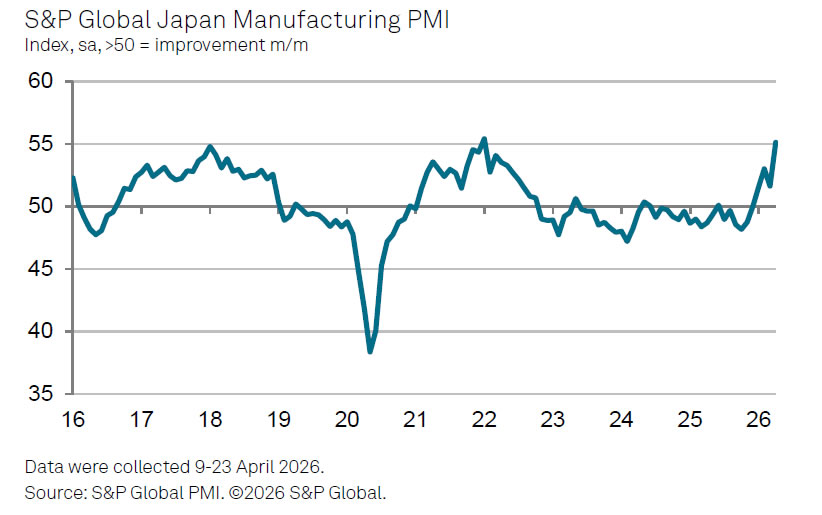

Japan Manufacturing PMI Jumps to 55.1, but Supply Strains Raise Sustainability Concerns

Japan’s factory sector is booming—but cracks are forming. Supply delays and rising costs could quickly reverse the gains. Read More.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3502; (P) 1.3557; (R1) 1.3660; More...

GBP/USD's breach of 1.3598 suggests that rise from 1.3158 is resuming. Intraday bias is back on the upside for 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high. For now, risk will stay on the upside as long as 1.3453 support holds, in case of retreat.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

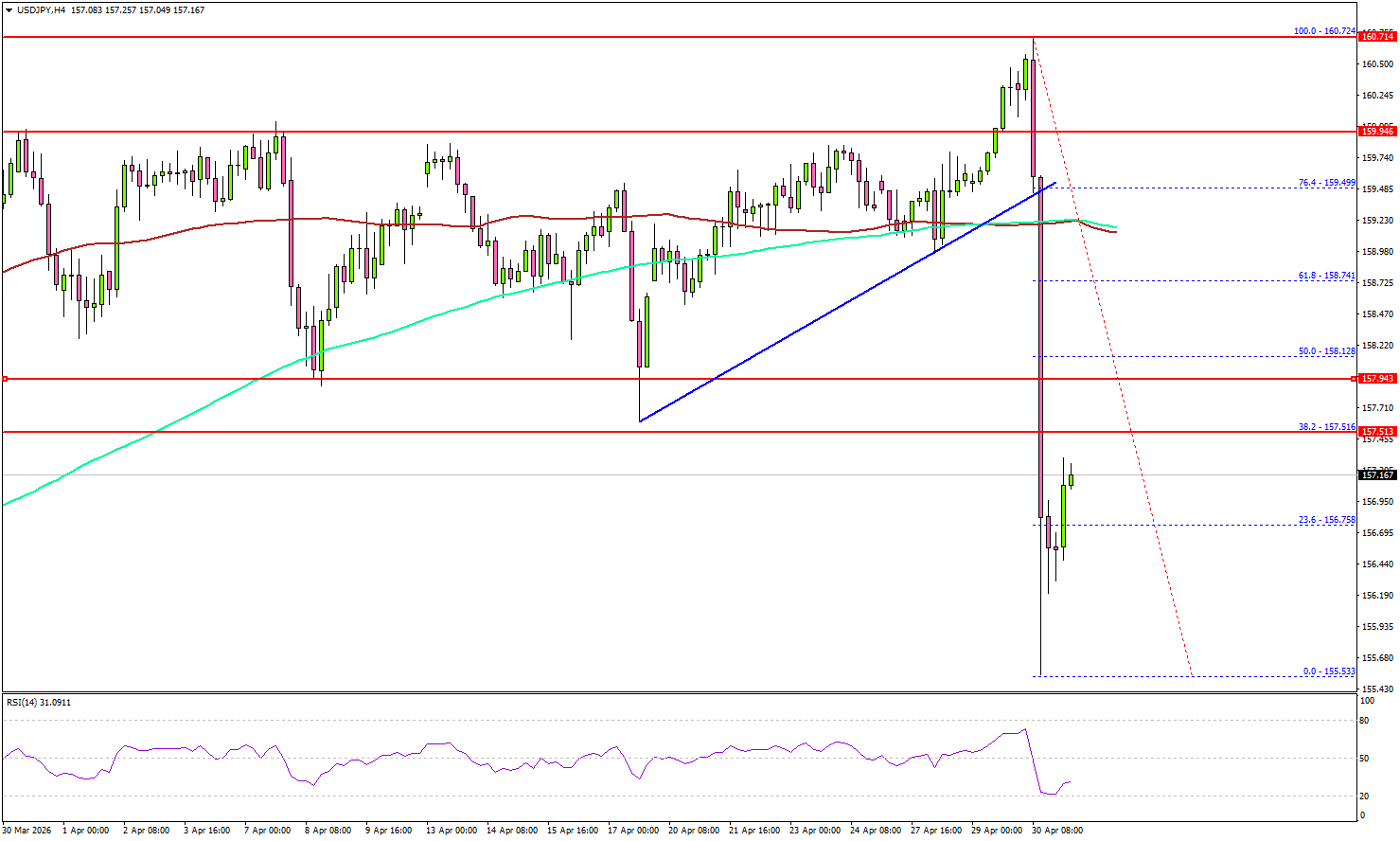

USD/JPY Freefalls, Sellers Trigger Aggressive Downside Move

Key Highlights

- USD/JPY started a sharp decline after it failed to clear 160.80.

- It dived over 500 pips and traded below 156.50 on the 4-hour chart.

- EUR/USD is again moving higher toward the 1.1750 resistance.

- GBP/USD regained traction and rallied above 1.3550.

USD/JPY Technical Analysis

The US Dollar failed to stay above 160.00 against the Japanese Yen. USD/JPY started a major decline below the 158.80 and 158.00 levels.

Looking at the 4-hour chart, the pair traded below a bullish trend line with support at 159.45. There was a close below 158.00, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

The pair even spiked below 156.00. A low was formed at 155.53, and the pair is now correcting some losses. On the upside, the pair faces resistance at 157.50.

The first major resistance sits at 158.00. The main resistance could be 158.75. A close above 158.75 could open doors for gains above 159.20 and the 100 simple moving average (red, 4-hour). In the stated case, the bulls could aim for a move to 160.00.

Immediate support is seen near 156.75. The next support could be 156.20. A close below 156.20 might push the pair toward 155.50. Any more losses could initiate a fresh move to 152.00 in the coming days.

Looking at EUR/USD, the pair is attempting a fresh increase and a close above 1.1750 could trigger steady gains.

Upcoming Key Economic Events:

- US ISM Manufacturing Index for April 2026 – Forecast 53.0, versus 52.7 previous.

Japan Manufacturing PMI Jumps to 55.1, but Supply Strains Raise Sustainability Concerns

Japan’s PMI Manufacturing was finalized at 55.1 in April, up sharply from 51.6 in March and marking the strongest reading since January 2022. The data points to a robust rebound in factory activity, with output expanding at the fastest pace in over a year, supported by a surge in sales and increased production momentum.

The strength in activity, however, is being driven in part by precautionary behavior. According to S&P Global Market Intelligence, manufacturers have been boosting inventories amid growing supply chain disruptions linked to the Middle East conflict. Lead times for inputs deteriorated at the fastest rate in 15 years, while input cost inflation surged to a three-and-a-half-year high, highlighting mounting strain across production networks.

As noted by Annabel Fiddes, the current rebound may prove short-lived. “This suggests the current boost to manufacturing could soon fade unless we see reduced market uncertainty and more stable supply chain conditions,” she said, warning that the pickup in activity is tied to stock-building rather than sustained demand. Without an improvement in supply conditions, rising costs and weaker demand could weigh on the sector in the months ahead.

| Indicator | March | April | Change |

|---|---|---|---|

| PMI Manufacturing | 51.6 | 55.1 | ↑ +3.5 |

| Output Growth | — | Strongest since Jan 2022 | ↑ |

| Sales Growth | — | Fastest since Jan 2022 | ↑ |

Cost & Supply Chain Indicators

| Indicator | Level/Trend |

|---|---|

| Input Cost Inflation | Highest in 3.5 years |

| Supplier Delivery Times | Worst in 15 years |

| Inventory/Stock Building | Increased |

Tokyo Inflation Cools to Multi-Year Low, but Energy Risks Point to Rebound Ahead

Japan's Tokyo core CPI (excluding fresh food) rose 1.5% yoy in April, below expectations of 1.8% yoy and slowing from 1.7% in March. The reading marks the weakest pace since March 2022, suggesting a temporary cooling in inflation momentum. As a leading indicator of nationwide trends, the data points to softer near-term price pressures than markets had anticipated.

The slowdown was largely driven by government subsidies aimed at curbing utility bills and education costs, which have dampened the headline impact of rising prices. Core-core CPI, which excludes both fresh food and energy, also eased from 2.3% yoy to 1.9% yoy, reinforcing the view that underlying inflation has moderated. Headline CPI edged slightly lower to 1.4% yoy, from 1.5% yoy previously.

However, the softer print may prove temporary. Cost-push pressures linked to the Middle East conflict are expected to feed through into energy and broader consumer prices in the coming months.

| Indicator | March | April | Change |

|---|---|---|---|

| Core CPI (ex-fresh food, YoY) | 1.7% | 1.5% | ↓ -0.2 |

| Core-Core CPI (YoY) | 2.3% | 1.9% | ↓ -0.4 |

| Headline CPI (YoY) | 1.5% | 1.4% | ↓ -0.1 |

Cliff Notes: Policy Perspectives from Across the Globe

Key insights from the week that was.

In Australia, the Q1 CPI report provided the first official estimate of the impact on local prices of the Middle East conflict. Headline inflation accelerated sharply to 1.4% (4.1%yr) in Q1 on the back of a 33% surge in auto fuel prices in March alone. Fortunately, a large portion of this spike has since unwound following the fuel excise cut, although fuel prices remain materially above the pre-conflict level.

While there were some signs of price pressures across home-building, vehicle repair and insurance, it is too early to detect, let alone accurately assess, evidence of pass-through. That said, underlying trimmed mean inflation still rose 0.8% in Q1, with annual growth at 3.5%yr, a full percentage point above the mid-point of the target. Notably, March’s data pre-dates the wide range of price increases reported anecdotally for building products and other items which came into effect in April.

Following the CPI release, Chief Economist Luci Ellis reaffirmed our call for the RBA to increase the cash rate by 25bps to 4.35% at the May policy meeting. The combination of an elevated starting point for inflation and imminent risk of pass-through will compel the RBA to act pre-emptively to contain inflation expectations. Next week’s voting split, updated staff forecasts and the tone of communications will be informative on the baseline policy outlook and risks. For now, we retain our base case of another two hikes beyond May, in June and August, taking the cash rate to a peak of 4.85%.

The combination of higher inflation, slower growth and rising unemployment is also fostering a complex macroeconomic backdrop for the 2026/27 Federal Budget, due May 12. A full preview will be published next week, but our preliminary note sets out our central expectation that commodity price windfalls are likely to more than offset spending pressures and result in a net improvement in the budget’s bottom line over the forward estimates.

Offshore, at the beginning of the week the Bank of Japan held its policy rate at 0.75% in a 6-3 vote. Updated forecasts highlight the risk of stagflation, with FY26 growth revised sharply lower to 0.5% (from 1.5%) and core inflation now expected to remain above 2% through to FY28. With Japanese firms increasingly willing to pass on costs, the Middle East conflict risks amplifying domestic inflationary pressures.

The BoJ remains focused on restoring the policy rate as an effective policy lever. Further hikes were signalled, but the timing left open. With policy settings still considered accommodative and a weak yen threatening import inflation, we anticipate the next hike to occur in June, though there is a risk it is delayed to July. The Financial Statements Statistics update due on 1 June will be an important release to gauge firms’ response to the crisis and the implications for both inflation and activity.

In the US, the FOMC then kept the stance of policy unchanged at its April meeting. The tone of the statement was balanced, with a sanguine view on GDP growth and the labour market and inflation simply characterised as “elevated”. The statement also noted that “the Committee is attentive to the risks to both sides of its dual mandate”, while Chair Powell remarked in the press conference that, in his view, policy is in a good place to take time to monitor conditions, being at the “high end of neutral, perhaps mildly restrictive”. Governors Hammack, Kashkari and Logan also showed greater concern over inflation than the labour market at this meeting, wanting to maintain the target range for the federal funds rate and signal that a hike was as likely as a cut on current information.

The Bank of Canada also kept its policy stance unchanged. The conflict in the Middle East and US trade policy were called out as sources of uncertainty for the global economy. But overall, the outlook for Canada’s economy was viewed as little changed from January. Assuming a protracted resolution to the Middle East conflict into 2027, GDP growth is expected to strengthen through 2027-2028 and inflation to turn back towards the 2%yr target from 3%yr in the near term, allowing the Bank of Canada to remain on hold.

Thereafter in Europe, the ECB Governing Council opted to maintain its current policy stance. The ECB acknowledged that “upside risks to inflation and downside risks to growth have intensified” and the merits of a rate hike were discussed, but developments to date were not sufficient to convince the Governing Council to take immediate action – the decision to hold was unanimous. At its previous meeting in March, the ECB presented two downside scenarios alongside its baseline. In the April press conference, President Lagarde was reluctant to discuss the details of those scenarios, noting simply that conditions are diverging from March’s baseline and the upcoming six weeks “will be the right time” to assess the economy “in order to make an informed decision”. Her comments appeared carefully chosen to signal openness to a rate increase in June. Therefore, barring any major changes in the dynamics of the Middle East conflict, we continue to believe that a 25bp policy rate hike is the most probable outcome at the next meeting.

The Bank of England’s April meeting also unfolded broadly as expected, the MPC voting 8-1 to keep the policy rate at 3.75%. Chief Economist Hew Pill was the sole dissenter, preferring “a prompt but modest hike in Bank Rate” to contain the risk of second-round inflationary effects. The policy statement maintained a hawkish bias, however, emphasising the potential impact of the energy price shock – its scale and duration – on UK inflation and the committee’s readiness to act to ensure inflation returns to the 2% target. Policy makers also showed concern over economic growth and the labour market, with slack increasing prior to the conflict.

Risks to the economic outlook were illustrated using three alternative scenarios, differentiated by oil and gas price assumptions and the persistence of second-round inflation effects. In the first two scenarios, the Brent oil price averages $108 in Q2 2026 then decreases at different speeds. Both scenarios showed headline inflation peaking above 3.5%yr this year before easing in 2027. Importantly, the Governor emphasised that, if the economy evolves in line with these scenarios, further policy tightening may not be required – the removal of the circa 50bp of easing priced before the conflict potentially sufficient to bring inflation back to the 2% target. The committee judged that the most severe scenario – where Brent averages $127 this quarter and remains above $100 well into 2028 – would likely require “a forceful tightening in monetary policy”, however. The Governor declined to specify what interest rate changes this would entail, but noted the need to act quickly to minimise second-round effects. Bank Rate hikes this year are therefore not guaranteed, but with Brent Oil surging as much as 20% this week to a peak around USD126 (now USD114) as the US and Iran remained at an impasse, conditions may eventually become too close to the BoE’s most severe scenario for the MPC to ignore. We continue to expect a Bank Rate hike at the next policy meeting in June, with further tightening possible, but dependent on evolving circumstances.

Metals Shine Bright After FOMC Meeting – Silver (XAG/USD) & Gold (XAU/USD) Intraday Outlook

- Silver and Gold are bouncing higher again after the Federal Reserve and other Central bank meetings

- With Oil and the US Dollar stumbling on the session, Metals and other risk assets are shining bright

- Intraday timeframe analysis for XAG/USD and XAU/USD

Silver and Gold are bouncing higher in today's session, with the bid taking traction in the wake of the Federal Reserve and a barrage of other global central bank meetings; With both Crude Oil and the US Dollar stumbling during today's session, precious metals and broader risk assets are shining bright again.

For weeks if not months, metals have been trapped in a truly bizarre, choppy range.

Despite numerous attempts, bulls have been completely unable to gather sustained upside momentum – This came along with a lack of real safe-haven demand, and the questioning on whether metals are still valuable at current valuations for flights towards quality.

Yet, every sharp pullback has seen sharp response, preventing any clear technical downtrend.

This erratic, sideways price action points to deep, fundamental confusion among institutional investors.

Gold vs WTI Crude Inverse Correlation – Source: TradingView. April 30, 2026

This widespread Market confusion is quite logical.

The macroeconomic and geopolitical backdrop remains both uncertain and chaotic.

High-stakes US-Iran diplomatic talks are completely stuck in the mud, with President Trump explicitly indicating that he does not mind maintaining the aggressive maritime blockade indefinitely to keep a relentless chokehold on the Iranian economy – Israel and Pakistan are also sending their own conflicting reports.

Meanwhile, global central banks remain highly reluctant to change their defensive policy stances amid this unpredictable environment.

As long as Crude Oil remains structurally elevated (above $80), precious metals—which are highly sensitive to the threat of stickier, energy-driven inflation and the resulting higher for longer rate pricing—will continue to face overhead pressure.

However, it will be incredibly interesting to see how these assets react if the Middle East conflict actually reaches a proper diplomatic resolution.

For now, the intraday rallies in Gold and Silver are almost entirely explicable on the broad-based drop in the US Dollar. If this Greenback weakness gains further structural traction, particularly if the conflict resolves, a clean, aggressive rally could easily follow.

Bulls should have their eyes firmly set on some upside targets for longer-run breakouts, looking at the $4,900 level for Gold and $84 for Silver.

Let's explore the recent shifts in an intraday timeframe analysis of Gold (XAU/USD) and Silver (XAG/USD) to identify where are the key levels to watch for breakouts.

Gold (XAU/USD) 4H Chart and levels

Gold (XAU/USD) 4H Chart, April 30, 2026 – Source: TradingView

After bouncing from its $4,500 Support (near the 2025 December record), the price action is much less bearish but also not so bullish yet. This confirms with the neutral RSI.

In such price action, it is favorable for traders to let prices form the trades:

- For bulls, wait for an extension above $4,700, breaking above the 50 and 200 Moving Averages (stop orders could be valid)

- Bears will want to see a reversal around current levels or rejecting the 50 MA ($4,685) with further acceleration below $4,485 (wait for a rejection of the MA before entering)

Intraday Timeframe Levels to watch for Gold (XAU/USD):

Resistance Levels:

- $4,685 - 4,700 4H 50 & 200 MA

- $4,850 to $4,900 Major Resistance (bullish above)

- $5,100 Pivotal Resistance

- $5,400 mini-resistance

Support Levels:

- December 2025 Support $4,500 to $4,550 (bearish below)

- Pivotal Support $4,325 – $4,400

- Main Channel Lows Support $4,100

- Next Support $3,880 to $4,000

Silver (XAG/USD) 4H Chart and levels

Silver (XAG/USD) 4H Chart, April 30, 2026 – Source: TradingView

Silver bulls have found strong support just above $70 and are testing the upper bound of the bear-channel.

Not far above, the action will meet the 4H 200-period MA ($74.80).

- Extending above should relaunch odds of a continued bounce towards $84.

- Above $84, the action is back to in much more bullish territory.

- Rejecting between here and the 200-MA (~$74), bears will regain the upper hand and add to their chances to create a more meaningful correction in the metal.

- Breaking $61 should see heavy continuation to the downside.

Higher Timeframe Levels to watch for Silver (XAG/USD):

Resistance Levels:

- Pivot lows $74.50 - $75 (4H 200-period MA – bullish above)

- Pivot highs $79 - $79.50

- $84 Major level

- Key Range Resistance $90 to $92

- $96.47 March highs (higher odds of All-time highs if break above)

- Current Record $121.67

Support Levels:

- $70 - $72 Minor Support (recent bounce – Bearish below)

- December FOMC Minor Support $64 to $66

- $61.10 Past Session lows

- $50 to $55 October Resistance now Major Support

- Silver's 2011 All-time highs $49.81

Safe Trades and good luck for next month!

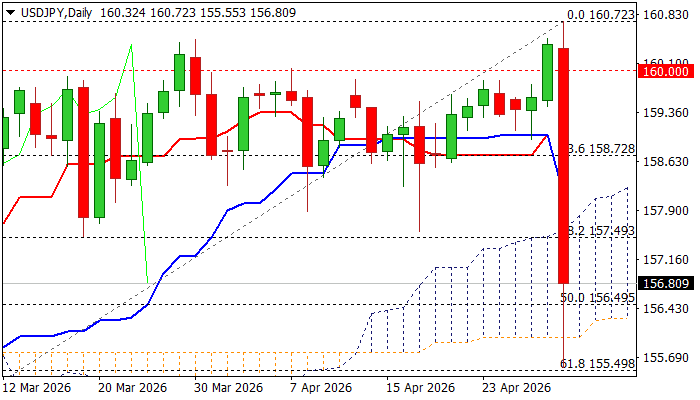

Japanese Yen Surges on Likely Intervention of Japan’s Authorities

Japanese yen surged across the board on Tuesday, gaining around 3% vs its major counterparts, in the biggest daily gain since late 2022.

The rally was sparked by comments from Japan’s FinMin who said that timing to take decisive action in the market was nearing, while some reports, citing government and the central bank, said that Japanese authorities intervened today to support yen, which hit the lowest levels since mid-2024, when the last intervention have occurred.

Today’s action follows the recent narrative that signaled readiness of authorities to intervene when USDJPY breaks resistance at 160 zone

Fresh acceleration hit the levels last traded in late February and marked retracement of near 61.8% of 152.39/160.72 rally, with significant bearish signal seen on surge through ascending and thickening daily Ichimoku cloud (spanned between 157.59 and 155.99).

Daily technical studies weakened after today’s action (steep falling momentum broke into negative territory / MAs turned mainly to bearish setup) although close below daily cloud will be required to signal that bears gained full control.

In such scenario, break of 155.50 (Fibo 61.8%) would expose targets at 153.97 (200DMA) and 153.61 (trendline support).

Near term bias, however, is expected to remain with bears while the price stays within the cloud (top lays at 157.59).

Res: 157.24; 157.59; 158.09; 158.72

Sup: 156.50; 155.99; 155.50; 154.26

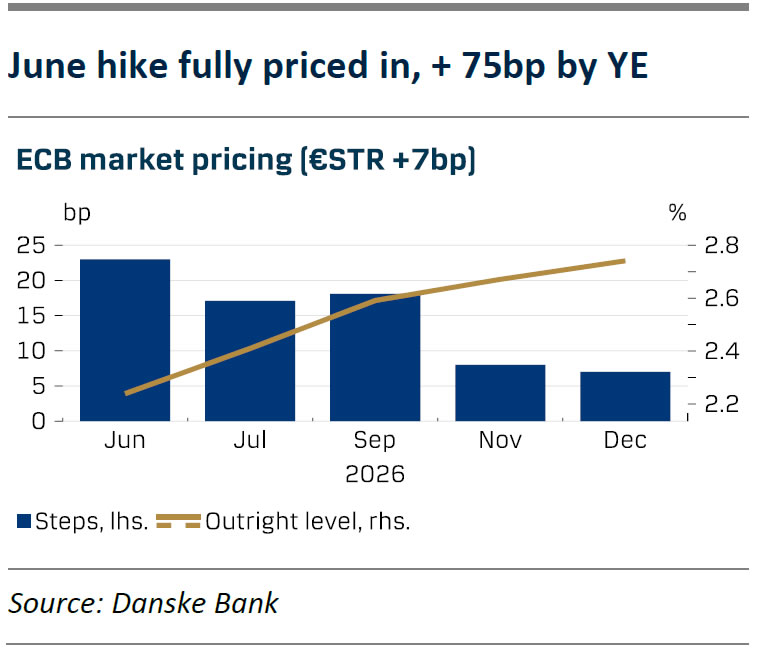

ECB Review: An Ocean of Uncertainty

- The ECB held policy rates unchanged as widely expected with the deposit rate at 2.00% on Thursday 30 April.

- Lagarde refrained from giving firm guidance of the future rate path and stated that the ECB will have more information in June to take a decision, including new projections and scenarios. By extension, the market reaction was highly contained.

- We continue to expect the ECB to increase policy rates by 25bp in June and July, respectively.

The ECB decided to keep the three key policy rates unchanged at the April meeting as widely expected by both consensus and markets, keeping the deposit rate at 2.00%. The ECB stated that both the upside risks to inflation and downside risks to growth have intensified. Yet, the GC remains “well positioned” to navigate the uncertainty and they asses long-term inflation expectations are “well anchored”. ECB highlights that the implications of the Iran war depend on the intensity and duration, so they are not drawing firm conclusions yet but remain in “wait and see” mode.

During the press conference Lagarde refrained from giving firm guidance on the future path of interest rates. She highlighted the deteriorating growth prospects and that she was “certainly not seeing second-round effects”. Lagarde noted that it was a unanimous decision within the GC to keep rates unchanged, but they debated various options including a rate hike, which was a view held by some members of the GC. The ECB will have more information in June where their staff both updates the baseline projections and the economic scenarios. Until then, the ECB is faced with an “ocean of uncertainty”. As a consequence, the market reaction was highly contained with European rates remaining in a tight range, ending the press conference 1-2bp lower with EUR/USD breaking slightly below the 1.17 mark.

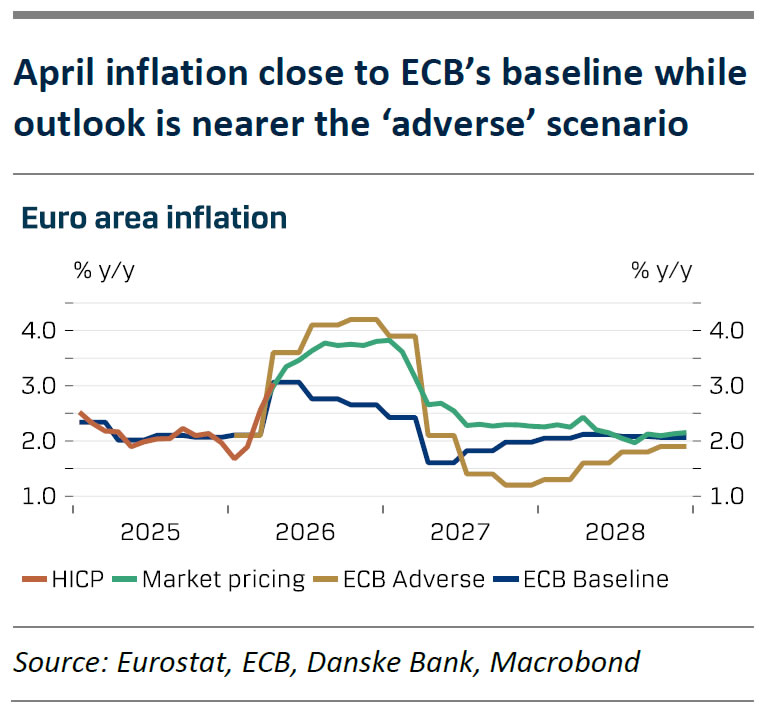

Lagarde stressed that the economy is clearly moving away from the baseline scenario, which aligns with our thinking. Inflation in April rose as expected to 3.0% y/y, similar to the ECB’s March baseline forecast but the outlook is closer to the “adverse” scenario when looking at market pricing (see chart) and seller price expectations rose significantly in the EC’s survey. At the same time Q1 GDP growth was weaker than expected and both consumer confidence, services PMIs, and employment expectations took large hits in April. Since ECB must balance higher inflation with lower growth, we expect two hikes is enough to keep inflation expectations anchored. We therefore keep our call of expecting the ECB to hike policy rates by 25 bp in June and July, bringing the deposit rate to 2.50%. We see risks to the call as tilted to the downside.