Sample Category Title

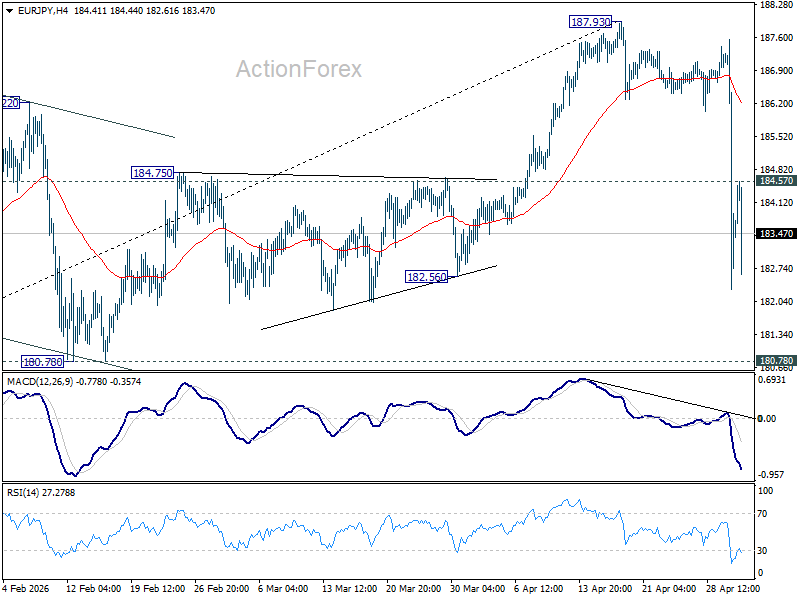

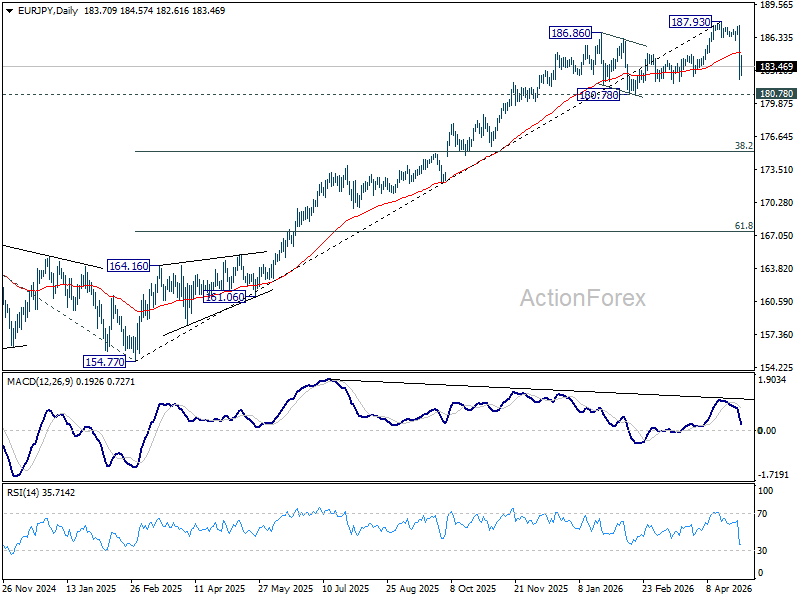

EUR/JPY Daily Outlook

Daily Pivots: (S1) 181.48; (P) 184.53; (R1) 186.77; More...

Intraday bias in EUR/JPY remains on the downside, and fall from 187.93 could extend lower to 180.78 support. But strong support should emerge there to bring rebound, at least on first attempt. On the upside, above 184.57 will turn intraday bias neutral first. However, decisive break of 180.78 will argue that it's already correcting whole five-wave impulse from 154.77. Next target will be 38.2% retracement of 154.77 to 187.93 at 175.26.

In the bigger picture, the pullback from 187.93 is steep, there is no sign of reversal yet. Uptrend from 114.42 is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 177.50) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.

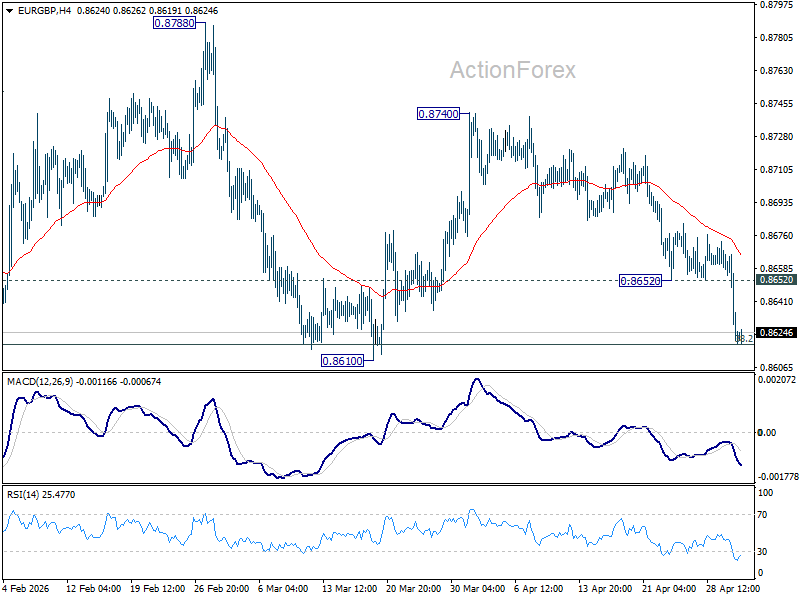

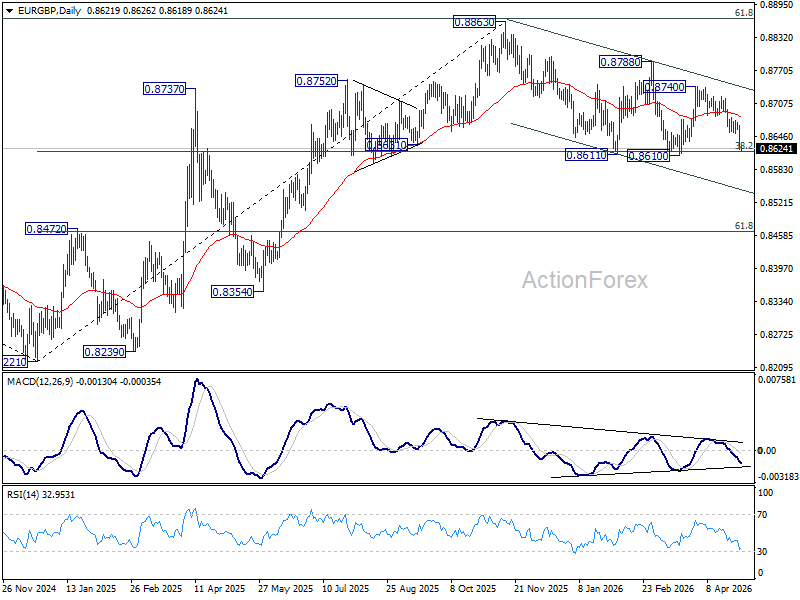

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8608; (P) 0.8639; (R1) 0.8656; More…

EUR/GBP's fall from 0.8740 resumed and accelerated after breaking through 0.8652. Intraday bias is back on the downside fro 0.8610 key support. Decisive break there will carry larger bearish implications and pave the way to 0.8466 fibonacci level next. On the upside, above 0.8652 support turned resistance will turn intraday bias neutral again first.

In the bigger picture, focus is back on 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Sustained break there will confirm that whole rise from 0.8221 has completed at 0.8863. Deeper decline should then be seen to 61.8% retracement at 0.8466 at least. For now, risk will stay mildly on the downside as long as 55 D EMA (now at 0.8682) holds, in case of recovery.

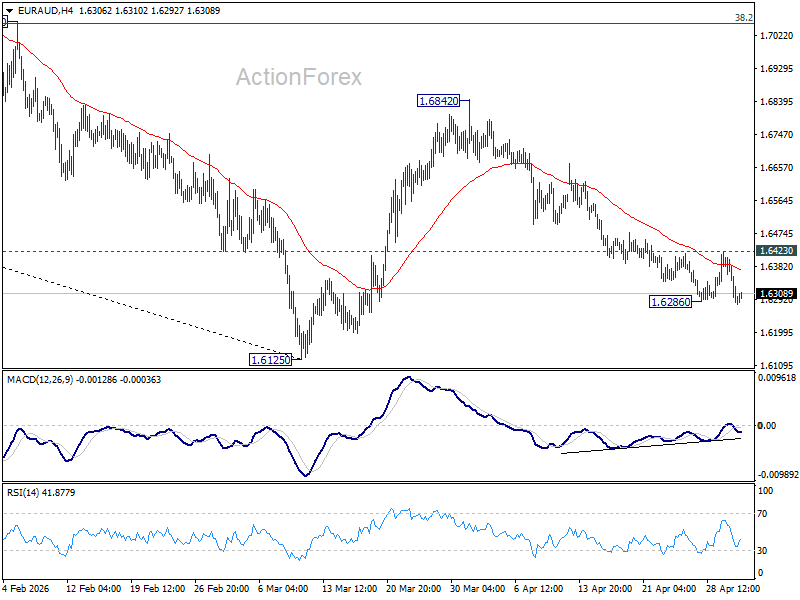

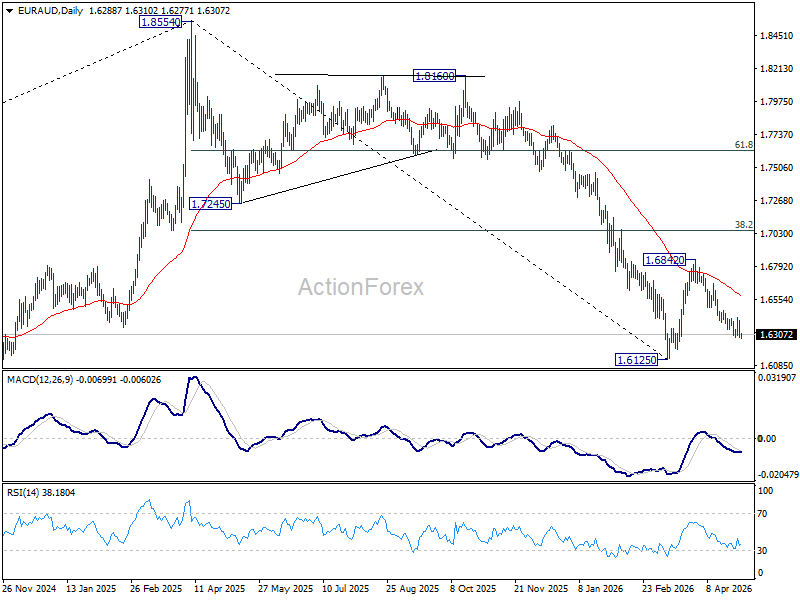

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6245; (P) 1.6334; (R1) 1.6381; More...

EUR/AUD's fall from 1.6482 resumed after brief recovery. Intraday bias is back on the downside for retesting 1.6126 low. Decisive break there will resume larger down trend from 1.8554. On the upside, break of 1.6423 resistance will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7129) holds, even in case of strong rebound.

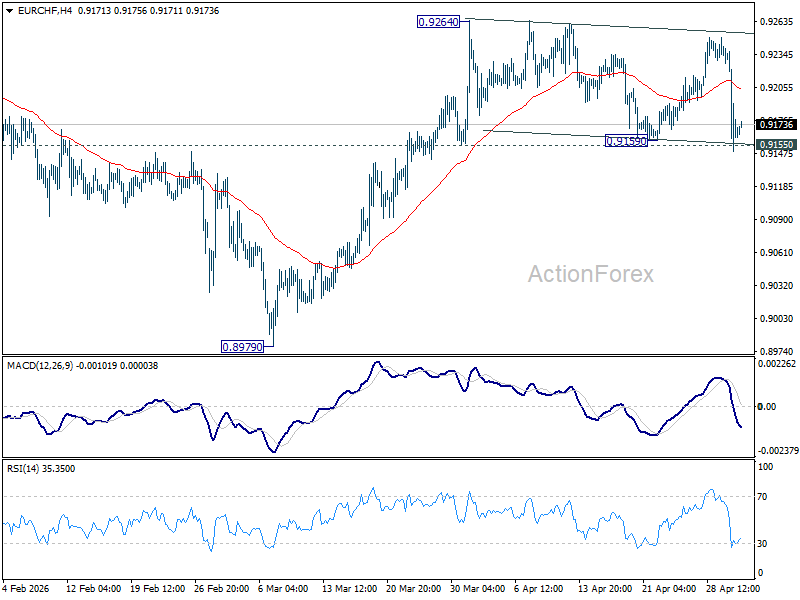

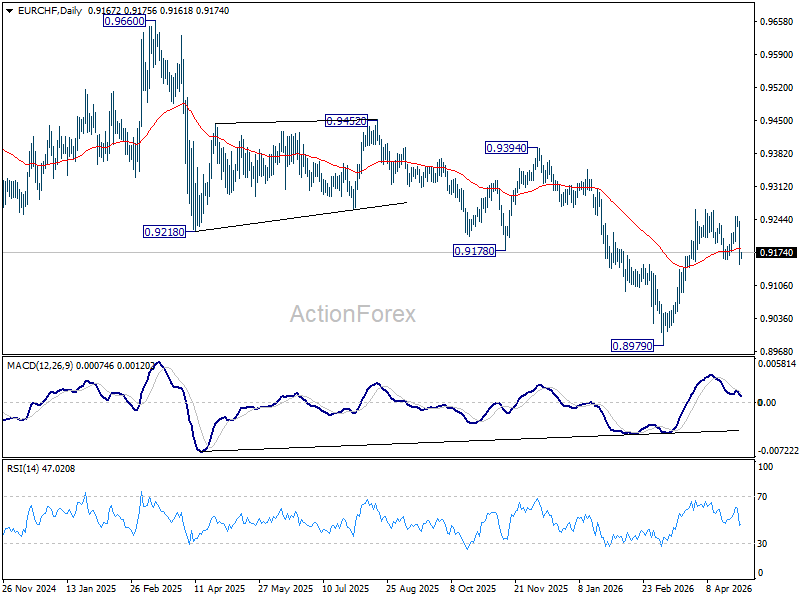

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9131; (P) 0.9188; (R1) 0.9227; More....

Despite near the strong volatile, EUR/CHF is still bounded in established range below 0.9264. Intraday bias remains neutral and further rise is expected with 0.9155 support intact. On the upside, firm break of 0.9264 will resume the rise from 0.8979 to 0.9394 resistance next. However, break of 0.9155 will turn bias back to the downside for deeper pullback.

In the bigger picture, considering bullish convergence condition in W MACD, a medium term bottom should be in place at 0.8979. Sustained trading above 55 W EMA (now at 0.9277) will add more credence to this case. Further break of 0.9394 resistance will pave the way to 0.9660 resistance next. However rejection by the 55 W EMA will set up another fall through 0.8979 low at a later stage.

Earnings Outshine War Worries

Another month ended with no light at the end of the tunnel for the Iran war. On the contrary, the US is not willing to lift the naval blockade in the Strait of Hormuz, while Iran says it will not give up its nuclear programme and will not come to the negotiating table unless the US lifts the blockade. We’re repeating the same lines every day.

Meanwhile, the near-closure of the Strait of Hormuz keeps the oil market tight. Trump downplays rising oil prices, arguing that there is plenty of oil – but blocked in the Strait – and that prices will fall like a rock once the issues are resolved. But when will that be? No one knows.

This is the takeaway from this week’s central bank meetings: the Federal Reserve (Fed), the Bank of Canada (BoC), the European Central Bank (ECB) and the Bank of England (BoE) all left rates unchanged, but their policy outlook was more or less aggressive. The ECB decision, for example, initially came across as dovish, until Christine Lagarde said a rate hike was discussed and could come as soon as June, depending on the data. That’s the issue: recent data confirmed that the energy shock slowed European growth to near zero in Q1 while pushing inflation to 3%. The question is whether energy-led inflation will spill over salaries and broader economy. If it does, the ECB must act.

The ECB’s tone brought euro bulls back in. The EURUSD extended its recovery above the 100-DMA, while benchmark EU 10-year yields fell and the Stoxx 600 jumped 1.38%, helped by a sharp correction in oil prices. With no clear trigger, the move likely reflects positioning and the re-emergence of the ‘demand destruction’ narrative as oil approaches $120pb.

This is not a hard ceiling. A prolonged conflict could eventually break above $120pb, but yesterday’s retreat in oil supported equities, alongside earnings.

Strong earnings – especially from banks and energy – boosted the Stoxx 600, mirroring the US.

In the US, major indices hit fresh record highs on AI optimism. The Dow Jones gained 1.62%, led by Caterpillar, which beat estimates with a 22% rise in Q1 revenue, supported by data centre and power infrastructure demand. The company reported a record $63bn backlog, up nearly 80% year-on-year. The AI boom may be displacing some jobs, but it is creating others. Some expect AI spending to reach $1tn next year, with Big Tech alone projected to spend over $700bn this year – potentially rising to $800–900bn.

As we enter May – traditionally a softer month – earnings resilience continues to offset geopolitical and inflation concerns.

US data showed Q1 growth slowing to around 2%, while price pressures eased. This pushed the US 2-year yield lower, with the 10-year falling below 4.40%.

US futures point to a positive open, while many European markets are closed for Labour Day. AI optimism remains the base case unless geopolitics deteriorate.

After the close, Apple reported better-than-expected earnings, with services revenue nearing $31bn. The company authorised a $100bn buyback and raised its dividend by 4%. However, Apple remains absent from the AI model race and relies on external providers: they don’t have to spend on pricey infrastructure, but higher reliance to model providers means margin pressure and reduced control over its ecosystem over time, leaving Apple more exposed to pricing power and innovation cycles dictated by external AI providers than its own decisions.

In FX, the US dollar weakened, driven by a sharp drop in USDJPY after Japanese authorities signalled possible intervention beyond 160. This pattern is now well established: authorities warn near 160 and may step in. Intervention doesn’t reverse the trend but clears speculative positioning. Buying the yen remains unconvincing, but selling USDJPY into 160 – if timed well – can be effective.

ECB and BoE Stay on Hold with Hawkish Hints

In focus today

Today is a holiday in many markets and relatively quiet in terms of data releases. Focus remains on energy markets ahead of the close of the week, following yesterday's volatile oil price movements.

In the US, we receive the April ISM manufacturing index, where markets expect a rise to 53.0 (prior: 52.7).

We also look out for the tier-2 releases of April PMI manufacturing indexes in the UK and US.

Economic and market news

What happened yesterday

Oil prices briefly surged to USD 126/bbl, the highest since March 2022, before retreating closer to USD 114/bbl towards the end of the session, which might be linked to the big swing in the Japanese Yen (see separate bullet). As the first oil future contract has moved from delivery in June to July the 'spot price' is now USD 111/bbl at the time of writing while the June contract ended at USD 114/bbl. Prices initially climbed on reports that President Trump was considering military strikes to break the negotiation deadlock with Iran. Iran said it would retaliate on US positions if US renewed attacks, the situation reflecting that efforts to resolve the conflict remain deadlocked. Markets remain sceptical of a near-term resolution to the conflict, with shipping data showing minimal traffic through the Strait of Hormuz and Polymarket investors assigning roughly a 20% probability that traffic in Hormuz strait returns to normal by end of May.

The ECB kept the deposit rate unchanged at 2.00% as widely expected. Lagarde refrained from giving firm guidance of the future rate path and stated that the ECB will have more information in June to take a decision, including new projections and scenarios. By extension, the market reaction was highly contained. We continue to expect the ECB to increase policy rates by 25bp in June and July, respectively. Our call was backed by an ECB sources story later in the afternoon saying that a June hike is very likely and that policymakers were in broad agreement about the need to move. For more details, read our ECB Review - An ocean of uncertainty, 30 April.

The Bank of England (BoE) held the bank rate steady at 3.75% as widely expected, presenting a scenario framework that suggests rate hikes could be appropriate but avoiding any pre-commitment. Markets responded by trading Gilt yields lower, with the June meeting now priced close to a 50-50 chance of a rate hike. The BoE appears cautious, and while risks are tilted towards one or two hikes, we believe the most likely outcome remains no changes. Read more in Bank of England Review - Active hold and no pushback on hawkish pricing, 30 April.

In the US, Q1 flash GDP grew 2.0% q/q AR which was less than expected by consensus (cons: 2.3%, Danske: 1.7%). The growth picture remains similar to last year, with steady but cooling private consumption and AI-related investments in data centres and software driving growth, while residential and non-residential investments remain under pressure. Meanwhile, the Q1 Employment Cost Index rose +0.9% q/q (prior: +0.7%), slightly exceeding expectations, primarily due to an increase in benefits rather than wages.

In the euro area, we received a long list of data. Flash HICP inflation rose to 3.0% y/y in April (prior: 2.6% y/y) in line with consensus, driven by higher energy inflation (10.8% y/y) and the largest monthly increase in food prices since last summer. Core inflation declined as expected to 2.2% y/y (cons: 2.3%, prior: 2.3%), and both services inflation and goods inflation momentum remained broadly in line with recent trends. GDP grew by 0.1% q/q in Q1 2026 (cons: 0.2%, prior: 0.2%), a weaker-than-expected outcome partly driven by volatility in the Irish economy and disappointing French growth. Meanwhile, the unemployment rate fell to 6.2% in March as expected (prior: 6.3%), reflecting a stable labour market. Although unemployment remains low, softer demand for labour, evidenced by declining vacancy ratios and surveys on employment expectations, points to a more balanced labour market compared to 2021/2022.

In Japan, the Ministry of Finance intervened in currency markets on Thursday to support the yen, which surged by up to 3% against the dollar following the move. This marks Japan's first intervention in nearly two years and comes amid mounting speculative pressure on the yen. Finance Minister Katayama hinted at further action, suggesting JPY 160 remains a critical threshold for policymakers.

In Norway, the NAV unemployment rate remained steady at 2.1% in April, slightly above Norges Bank's projection of 2.0%. The marginal rise in gross unemployment reflects a labour market that remains tight and growth near trend. With unemployment levels still low, Norges Bank is likely to maintain its focus on anchoring inflation expectations. Norges Bank also announced that they lift their daily fiscal NOK buying slightly from NOK 50m to NOK 100m in May likely reflecting lower energy prices compared to end-March. This was in line with expectations and should not have any market impact.

Equities: Global equities moved higher yesterday, taking several major indices to fresh all-time highs, including MSCI World, S&P 500, Russell 2000 and Nasdaq.

The move was closely linked to the sharp turnaround in oil yesterday morning. Looking at the oil price over the past 24 hours, the gap between the high and the low has been more than 12%. Importantly, there was no particularly strong trigger behind the massive reversal in oil.

Like yesterday, the key point when analysing market moves is that there are many drivers in play at the same time. Geopolitics, macro data, micro data from one of the busiest earnings days of the season, and central banks. In other words, it is very difficult to separate the individual drivers and assign the exact market reaction to each of them.

One important observation is that yesterday's move to new equity highs was not led by tech. In fact, tech was the only sector lower on the day, with massive underperformance driven by earnings.

Oil was clearly the major trigger for the risk-on move, but with tech lower, defensives outperformed. On top of that, earnings were strong in defensives, not least in US healthcare, which helped lift the defensive sectors.

This morning, Asia is quieter with many markets closed for 1 May. Nikkei is higher despite a stronger yen in the wake of FX intervention.

Many European markets are also closed today, but US futures are trading higher this morning.

FI and FX: Risk sentiment improved over yesterday's session, despite Khamenei's vow to guard Iranian nuclear and ballistic capabilities. Brent Crude pulled back to around USD 114/bbl after breaking above USD 126/bbl at European open. In rates space, EUR swap rates fell back by 5-10bp across the curve and Bund yields declined by 10bp in the medium tenors over the course of the day. In the afternoon, the ECB held policy rates unchanged as widely expected, leaving the deposit rate at 2.00%. Lagarde refrained from providing firm guidance of the future rate path and stated that the ECB will have more information in June to decide, including new projections and scenarios. By extension, the market reaction was highly contained. We continue to expect two hikes in June and July, respectively. EUR/USD jumped higher, breaking above the 1.17 mark. USD/JPY declined sharply by about 2.5% over yesterday's session. Nikkei reported Japanese intervention in the FX market, aligning with the significant price action. The considerable oil price volatility also impacted NOK FX during yesterday's session although the magnitude was relatively contained with EUR/NOK kept within a 9-figure range. Norges Bank's announcement to lift the daily fiscal NOK buying pace by NOK 50m from NOK 50m to NOK 100m also failed to trigger any market response - which we think is fair.

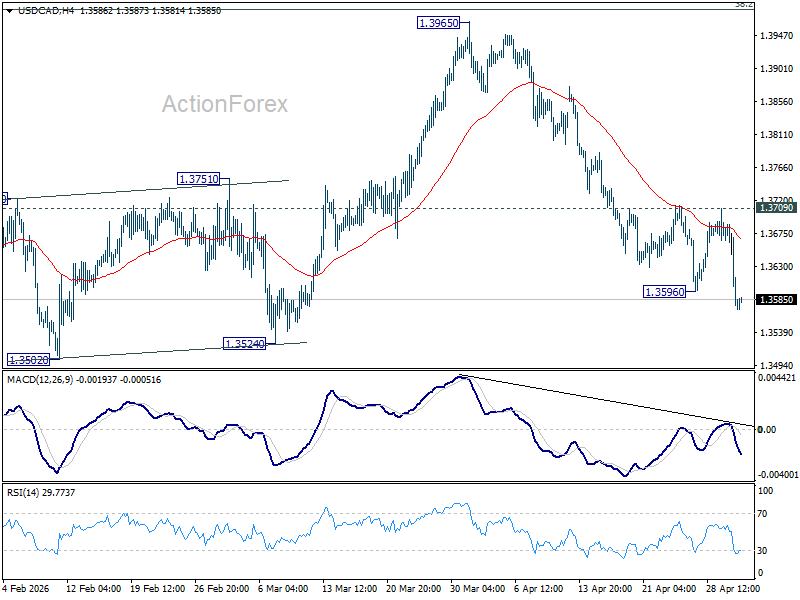

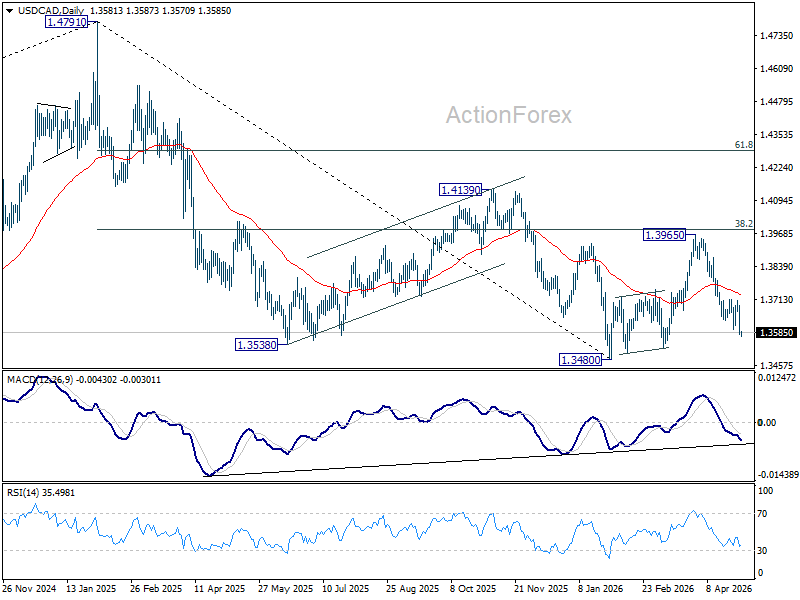

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3543; (P) 1.3619; (R1) 1.3658; More...

USD/CAD's fall from 1.3965 resumed after brief recovery and intraday bias is back on the downside. Next target is a retest on 1.3480 low. For now, risk will remain on the downside as long as 1.3709 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already. Further break of 1.4139 will confirm and bring retest of 1.4791 high.

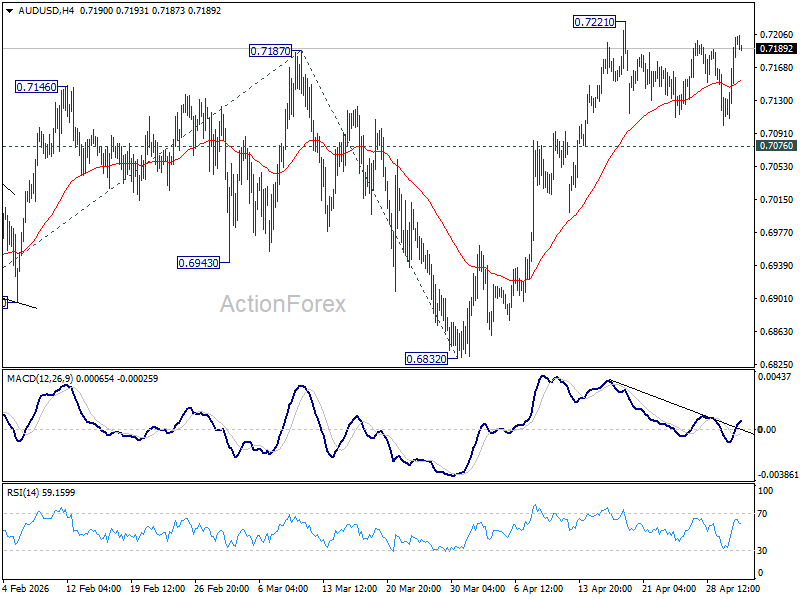

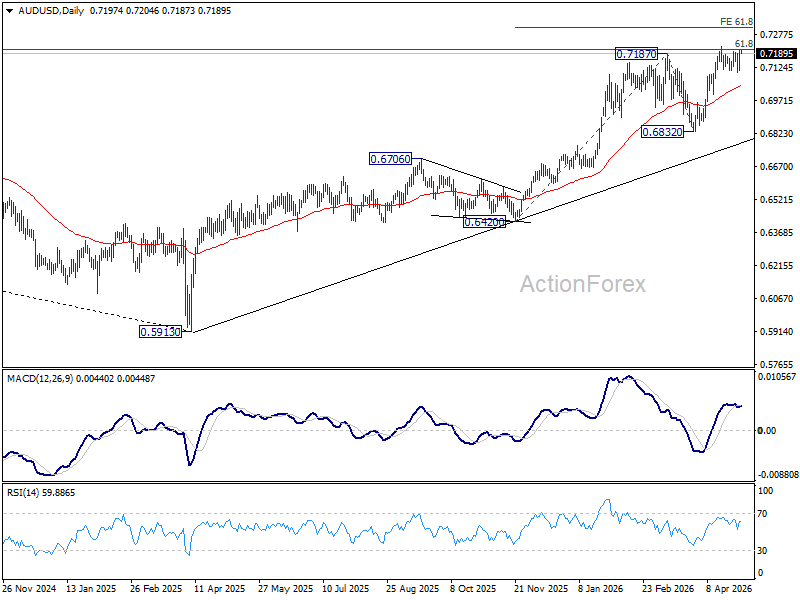

AUD/USD Daily Report

Daily Pivots: (S1) 0.7140; (P) 0.7172; (R1) 0.7234; More...

AUD/USD is still bounded in consolidations below 0.7221 and intraday bias stays neutral. Further rise is expected as long as 0.7076 support holds. On the upside, firm break of 0.7221 will extend larger up trend to 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306. On the downside, break of 0.7076 minor support will turn bias back to the downside for deeper pullback.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.

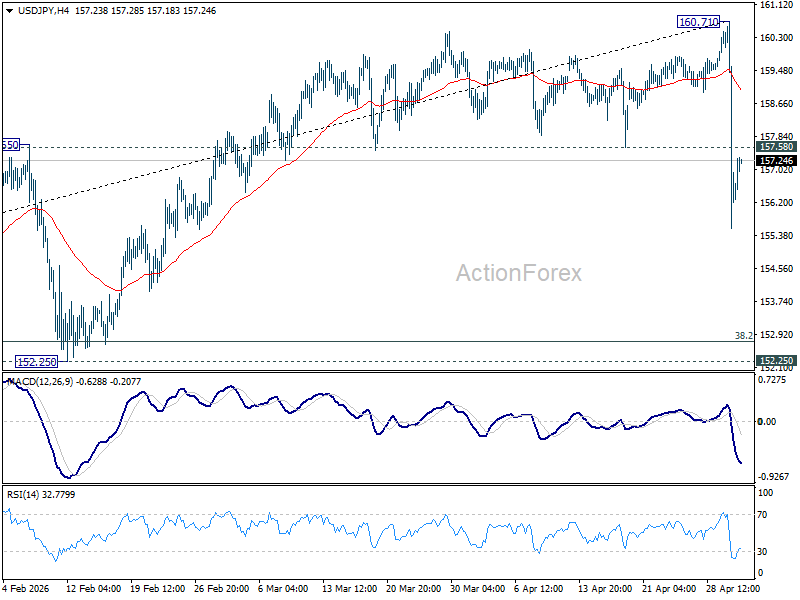

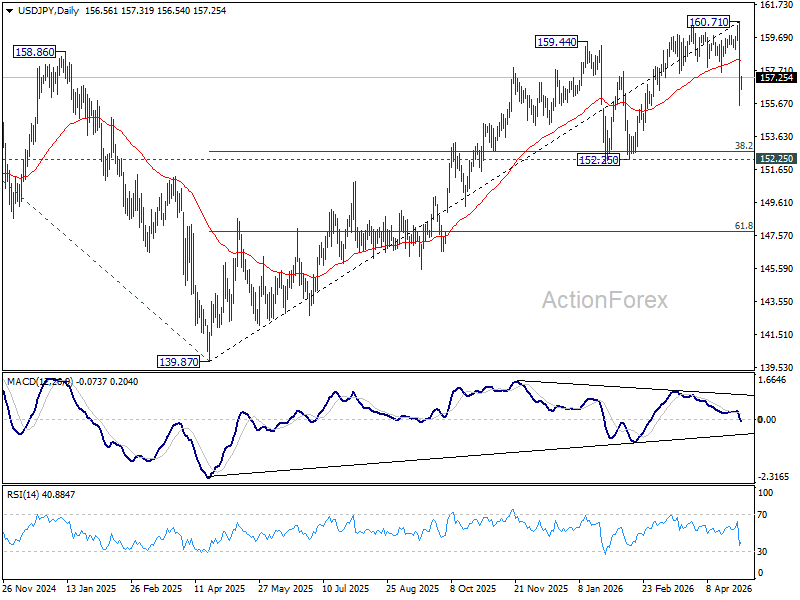

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.55; (P) 157.63; (R1) 159.71; More...

Intraday bias in USD/JPY remains on the downside at this point. Fall from 160.71 would extend lower towards 152.25 cluster support (38.2% retracement of 139.87 to 160.71 at 152.74). Strong support should emerge there to bring rebound, at least on first attempt. On the upside, above 157.58 support turned resistance will turn intraday bias neutral first.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 153.90) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

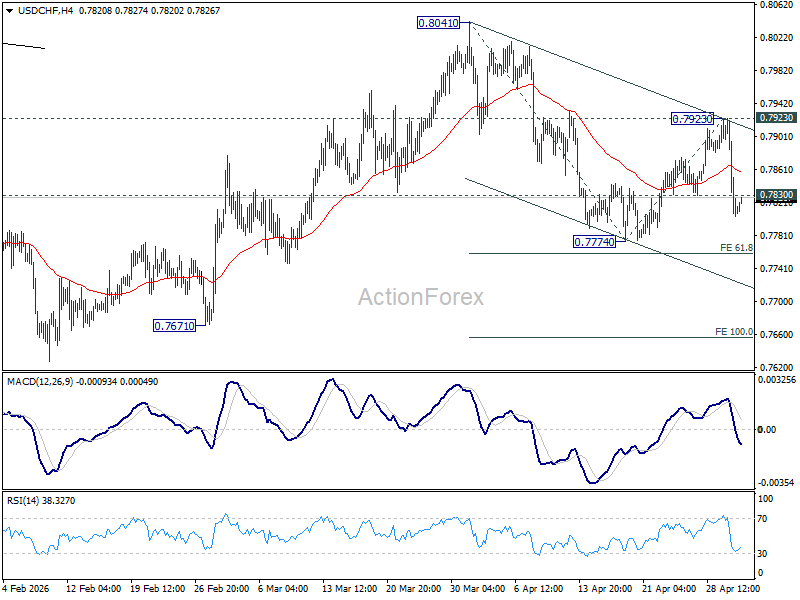

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7773; (P) 0.7848; (R1) 0.7891; More….

USD/CHF's break of 0.7830 support suggests that rebound from 0.7774 has completed at 0.7923 already. Intraday bias is back on the downside for 0.7774 and then 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758. Firm break there will target 100% projection at 0.7656. For now, risk will stay on the downside as long as 0.7923 resistance holds, in case of recovery.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8053) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).