Sample Category Title

Japan Moves Markets Without Spending a Yen as USD/JPY Reversal Triggers FX Shake-Up

Yen is stealing the spotlight in an otherwise crowded macro day—and it did not take actual intervention to do it. After pushing through the 160 level earlier this week and hitting 160.71, USD/JPY has staged a dramatic reversal, plunging back toward 155 in a move that has caught traders off guard. The speed and scale of the shift point to a powerful repositioning dynamic, driven by a surge in intervention fears, and then amplified by opportunistic buying..

The catalyst was a “final warning” from Finance Minister Satsuki Katayama, who said the timing for “bold steps” is “now nearing.” That phrase, in Japan’s policy language, is widely understood as a direct precursor to intervention. Katayama’s follow-up message—“don’t put your smartphones down”—reinforced the urgency, particularly heading into Golden Week, when thinner liquidity can amplify market moves.

Markets reacted immediately. Short Yen positions were aggressively unwound, triggering a sharp squeeze. At the same time, new longs began to build, with traders betting that authorities will continue to apply pressure until USD/JPY stabilizes at lower levels, potentially closer to 155 or beyond. Whether Japan has intervened or not is almost secondary—the psychological impact alone has been enough to force a major repositioning.

This episode underscores the power of verbal intervention. Without spending a single Yen—at least officially—Japan has managed to engineer a nearly 500-pip move. More importantly, it has broken the one-way momentum that had dominated the currency, restoring uncertainty and two-way risk.

Meanwhile, Oil is providing the other half of today’s volatility story. Brent surged to a four-year high above $126 earlier in the session, reflecting ongoing geopolitical tensions. But the rally proved unstable, with prices reversing sharply back toward $114.

The pullback appears to be driven more by market mechanics than fundamentals. With April 30 marking the expiry of the June Brent contract, position adjustments and rollover flows likely played a role in the sudden reversal. The result is a highly volatile environment where oil is amplifying, rather than stabilizing, broader market dynamics.

In FX, the ripple effects are clear. Yen is by far the strongest performer, while Swiss Franc is benefiting from the unwind of carry trades. As Yen-funded positions are reduced, the Franc gains too.

Dollar, by contrast, is lagging. The retreat in oil prices has undermined its recent strength, and the greenback is largely ignoring macro data releases. Instead, flows are being driven by positioning and cross-market adjustments.

Sterling is finding modest support from a hawkish signal at the Bank of England, where Chief Economist Huw Pill voted for a rate hike. Euro remains steady, with the ECB’s hold offering little surprise and limited market impact.

The bigger picture is that today’s market is being driven less by data and more by positioning and policy signaling. Japan has shown that credible threats alone can move markets. And for now, the Yen’s dramatic comeback is the clearest sign that traders are no longer willing to test authorities without consequence.

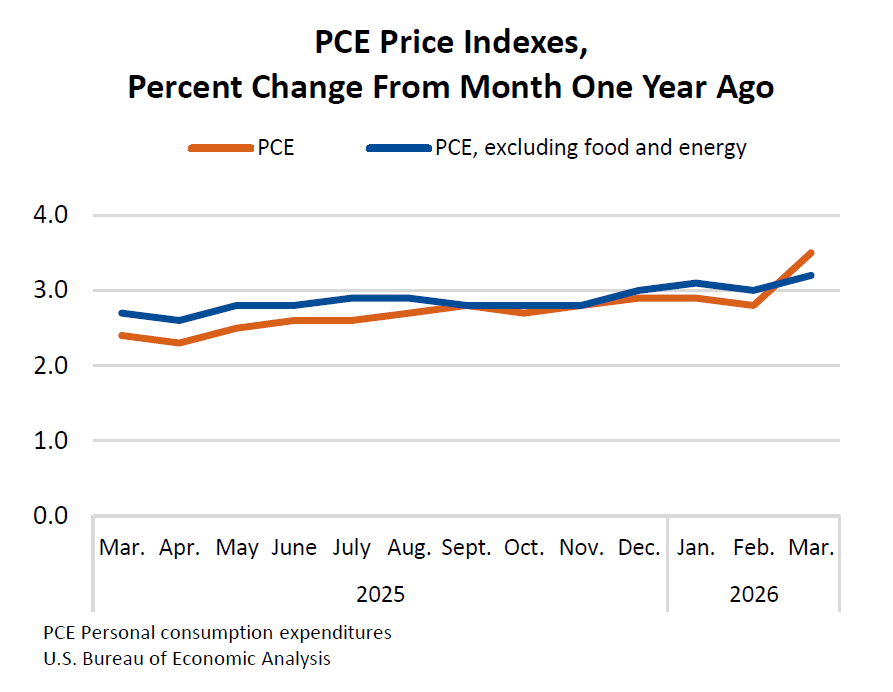

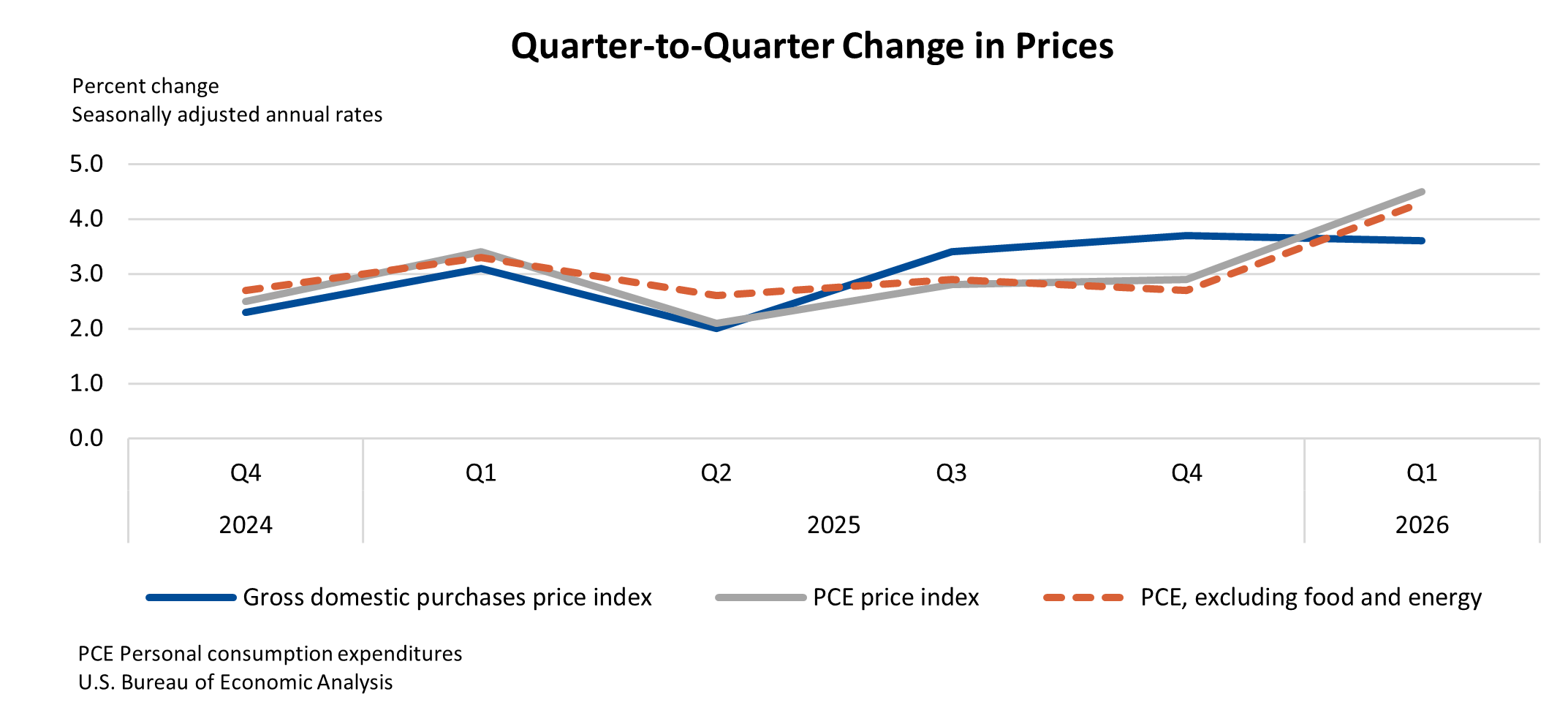

US Personal Income Beats, Spending Solid as PCE Inflation Accelerates to 3.5%

US personal income jumps 0.6% and spending rises 0.9% in March, while PCE inflation accelerates to 3.5%, signaling resurging price pressures. Read More.

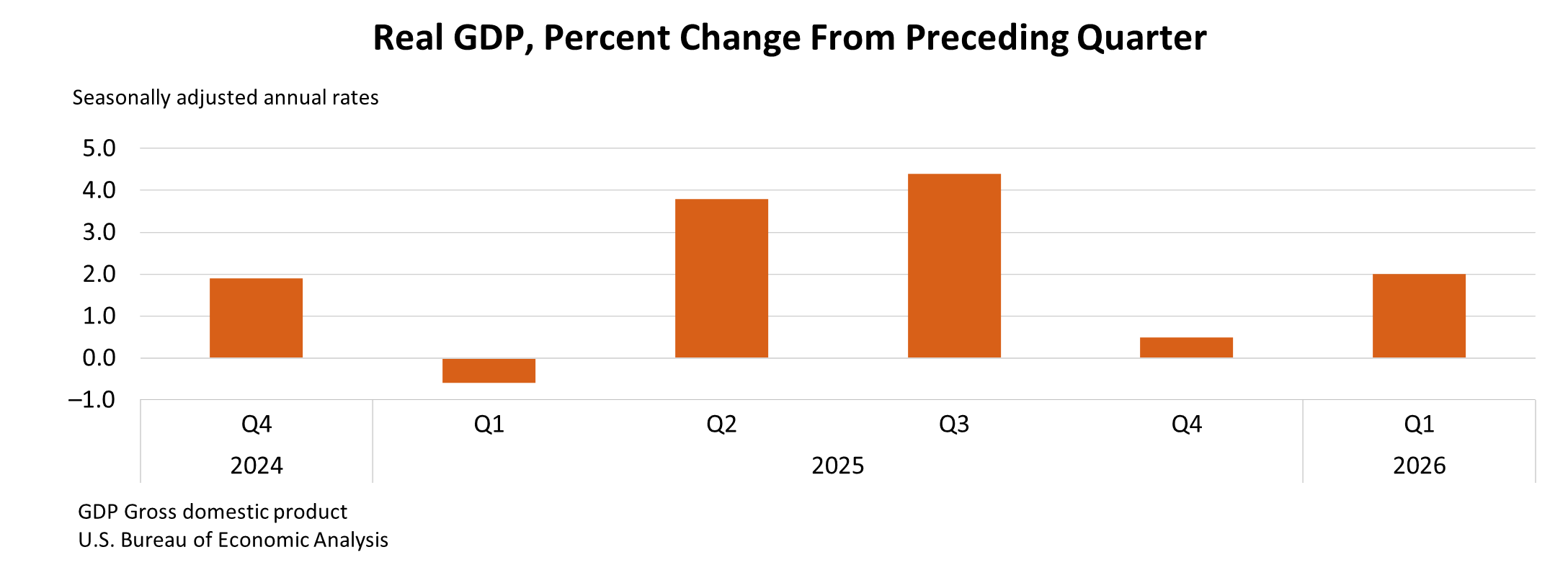

US GDP Growth Picks Up to 2.0% but Misses Expectations as Inflation Surges

US GDP grows 2.0% in Q1, missing expectations, as PCE inflation surges to 4.5%, signaling rising price pressures despite solid demand. Read More.

ECB Holds Deposit Rate at 2.00% as Energy Shock Lifts Inflation Risks

ECB holds rates, but the real message is rising risk. Energy prices are pushing inflation higher while threatening growth. Read More.

BoE Holds at 3.75% as Pill Dissent for Hike on Second-Round Inflation Risks

BoE holds rates, but a hawkish dissent is the real story. Rising energy costs are raising fears of persistent inflation. Read More.

Eurozone Inflation Jumps to 3.0% in April, But Core CPI Ticks Down to 2.2%

Eurozone inflation is rising again—but it’s all about energy. Core pressures are easing, leaving policymakers with a difficult call. Read More.

Eurozone Economic Growth Slows in Q1 as GDP Misses Expectations at 0.1% qoq

Eurozone growth is slowing again. Germany is holding up, but France is stalling and overall momentum remains fragile. Read More.

Japan Industrial Output Falls -0.5% as Petrochemical Weakness Dominates

Japan’s factory output is slipping as energy-linked sectors are hit by supply disruptions, even as retail sales rebound and consumption holds up. Read More.

NZ ANZ Business Confidence Slumps to -10.6, Inflation Expectations Highest Since Feb 2024

Cost pressures are surging in New Zealand, driving inflation expectations higher and pushing business confidence back into negative territory. Read More.

China PMI Signals Modest Growth as Services Slip and Cost Pressures Build

China’s PMI data shows resilient output but growing divergence and rising inflation pressures within the economy. Read More.

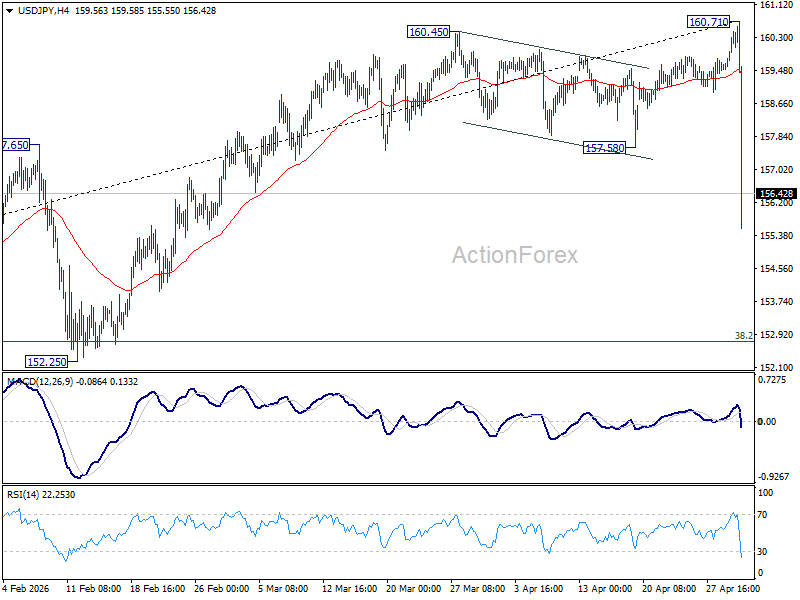

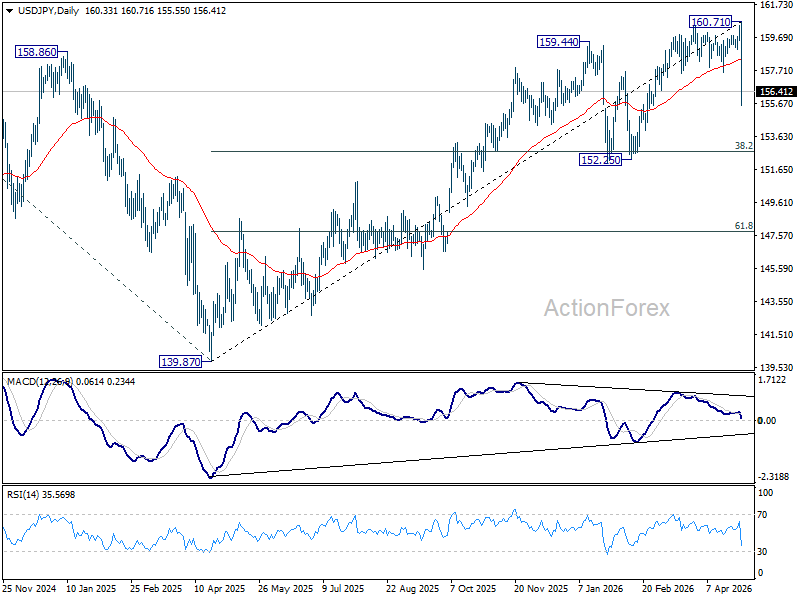

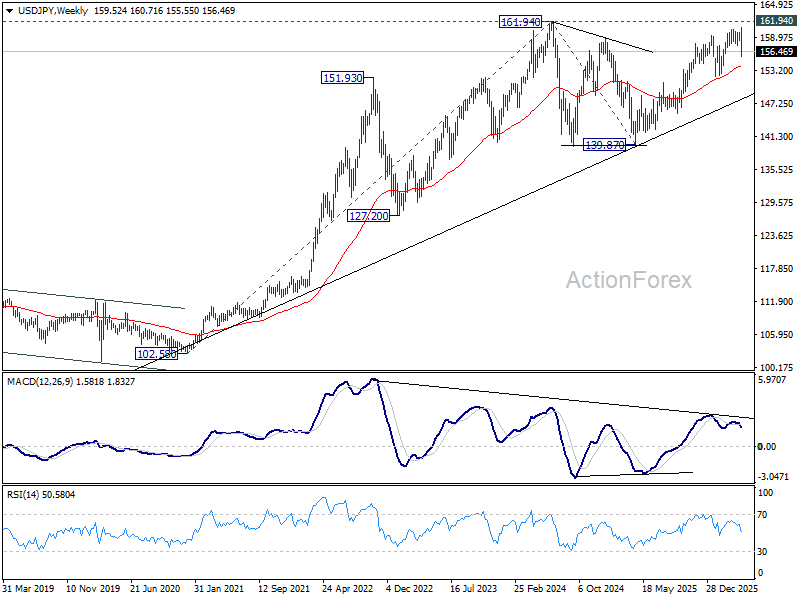

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 159.79; (P) 160.14; (R1) 160.79; More...

USD/JPY steep decline today suggests medium term topping at 160.71, on bearish divergence condition in D MACD. Deeper fall should be seen to 152.25 cluster support (38.2% retracement of 139.87 to 160.71 at 152.74). Strong support should emerge there to bring rebound, at least on first attempt. However, decisive break of 152.25/75 will confirm rejection by 161.94 high. That would pave the way back to 61.8% retracement at 147.83 next.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 153.90) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

US Personal Income Beats, Spending Solid as PCE Inflation Accelerates to 3.5%

US personal income rose 0.6% mom in March, beating expectations of 0.3% mom, signaling stronger household income growth. At the same time, personal consumption expenditures increased 0.9% mom, in line with expectations, indicating that consumer demand remains resilient despite rising price pressures.

The inflation picture, however, showed a clear pickup. The PCE price index rose 0.7% mom, while core PCE increased 0.3% mom, both matching expectations.

On an annual basis, headline PCE accelerated from 2.8% yoy to 3.5% yoy, while core PCE edged up from 3.0% yoy to 3.2% yoy. The data suggests that price pressures are re-intensifying, even as monthly core readings remain relatively contained.

| Indicator | February | March |

|---|---|---|

| PCE Price Index (MoM) | — | 0.7% |

| Core PCE (MoM) | — | 0.3% |

| PCE Price Index (YoY) | 2.8% | 3.5% |

| Core PCE (YoY) | 3.0% | 3.2% |

US GDP Growth Picks Up to 2.0% but Misses Expectations as Inflation Surges

US economy expanded at an annualized pace of 2.0% in Q1, accelerating from 0.5% in Q4 2025 but falling short of expectations for 2.2% growth. The rebound was driven by stronger investment, exports, government spending, and continued consumer activity, although a rise in imports—subtracting from GDP—partly offset the overall gain.

The composition of growth points to a shift in momentum. Investment and exports provided a stronger contribution, while government spending also turned higher. However, consumer spending decelerated compared to the previous quarter, suggesting some moderation in household demand. Still, underlying domestic demand remained firm, with real final sales to private domestic purchasers rising 2.5%, up from 1.8% in Q4.

Inflation pressures, however, intensified sharply. The PCE price index jumped to 4.5% from 2.9%, while core PCE rose to 4.3% from 2.7%, signaling a significant pickup in underlying price pressures. Although the broader price index for domestic purchases eased slightly to 3.6%, the surge in PCE inflation underscores a challenging backdrop for policymakers, where growth remains resilient but inflation risks are rising again.

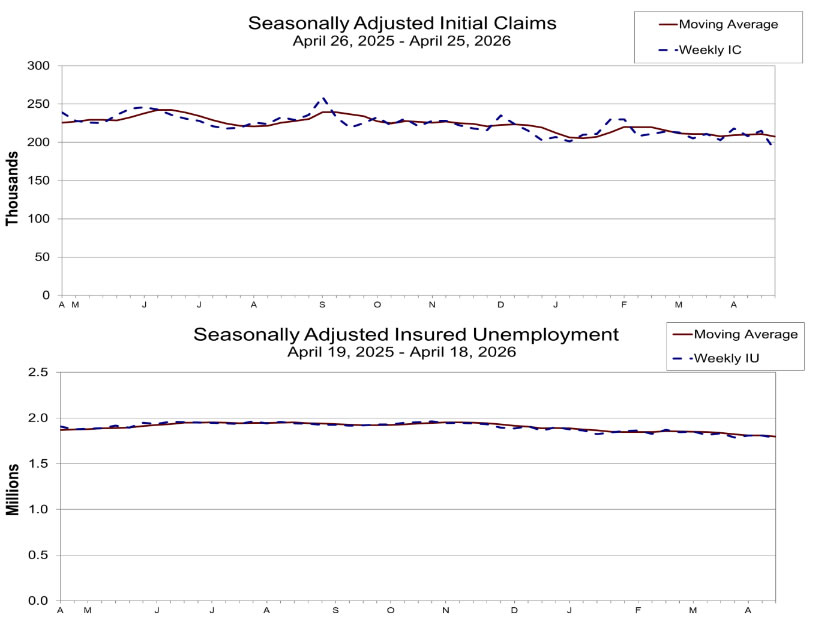

US Initial Unemployment Claims Fall to 189k vs Exp. 212k

US initial jobless claims fell -26k to 189k in the week ending April 25, below expectation of 212k. Four-week moving average of initial claims fell -3.5k to 207.5k.

Continuing claims fell -23k to 1.785m in the week ending April 18. Four-week moving average of continuing claims fell -11.75k to 1.808m.

ECB Holds Deposit Rate at 2.00% as Energy Shock Lifts Inflation Risks

European Central Bank kept its deposit rate unchanged at 2.00%, as widely expected, but the statement highlighted a more complex risk environment. Policymakers acknowledged that “the upside risks to inflation and the downside risks to growth have intensified,” signaling that the balance of risks has shifted as the energy shock deepens.

At the center of the ECB’s assessment is the impact of the Middle East conflict on energy markets. The Governing Council noted that the war has “led to a sharp increase in energy prices, pushing up inflation and weighing on economic sentiment.” The key uncertainty now lies in how persistent this shock proves to be. “The longer the war continues and the longer energy prices remain high, the stronger is the likely impact on broader inflation and the economy,” the statement warned.

Despite the near-term pressure, the ECB emphasized that underlying conditions remain relatively stable. The Eurozone entered this period “with inflation at around the 2% target,” and the economy has shown resilience in recent quarters. Importantly, “longer-term inflation expectations remain well anchored,” even as short-term expectations have moved up significantly, reflecting the immediate impact of energy costs.

Looking ahead, the ECB maintained a flexible stance, reiterating that it will follow a “data-dependent and meeting-by-meeting approach” and is “not pre-committing to a particular rate path.” This keeps all options open, with policy decisions hinging on incoming data, the evolution of inflation risks, and the strength of monetary transmission. While the ECB stopped short of signaling a near-term move, the tone suggests that rising inflation risks will remain firmly in focus.

(ECB) Monetary policy decisions

30 April 2026

The Governing Council today decided to keep the three key ECB interest rates unchanged. While the incoming information has been broadly consistent with the Governing Council’s previous assessment of the inflation outlook, the upside risks to inflation and the downside risks to growth have intensified. The Governing Council is committed to setting monetary policy to ensure that inflation stabilises at the 2% target in the medium term.

The war in the Middle East has led to a sharp increase in energy prices, pushing up inflation and weighing on economic sentiment. The implications of the war for medium-term inflation and economic activity will depend on the intensity and duration of the energy price shock and the scale of its indirect and second-round effects. The longer the war continues and the longer energy prices remain high, the stronger is the likely impact on broader inflation and the economy.

The Governing Council remains well positioned to navigate the current uncertainty. The euro area entered this period of surging energy prices with inflation at around the 2% target, and the economy has shown resilience over recent quarters. Longer-term inflation expectations remain well anchored, although inflation expectations over shorter horizons have moved up significantly.

The Governing Council will closely monitor the situation and follow a data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance. In particular, its interest rate decisions will be based on its assessment of the inflation outlook and the risks surrounding it, in light of the incoming economic and financial data, as well as the dynamics of underlying inflation and the strength of monetary policy transmission. The Governing Council is not pre-committing to a particular rate path.

Key ECB interest rates

The interest rates on the deposit facility, the main refinancing operations and the marginal lending facility will remain unchanged at 2.00%, 2.15% and 2.40% respectively.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The APP and PEPP portfolios are declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

***

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation stabilises at its 2% target in the medium term and to preserve the smooth functioning of monetary policy transmission. Moreover, the Transmission Protection Instrument is available to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across all euro area countries, thus allowing the Governing Council to more effectively deliver on its price stability mandate.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:45 CET today.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 159.79; (P) 160.14; (R1) 160.79; More...

USD/JPY steep decline today suggests medium term topping at 160.71, on bearish divergence condition in D MACD. Deeper fall should be seen to 152.25 cluster support (38.2% retracement of 139.87 to 160.71 at 152.74). Strong support should emerge there to bring rebound, at least on first attempt. However, decisive break of 152.25/75 will confirm rejection by 161.94 high. That would pave the way back to 61.8% retracement at 147.83 next.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 153.90) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

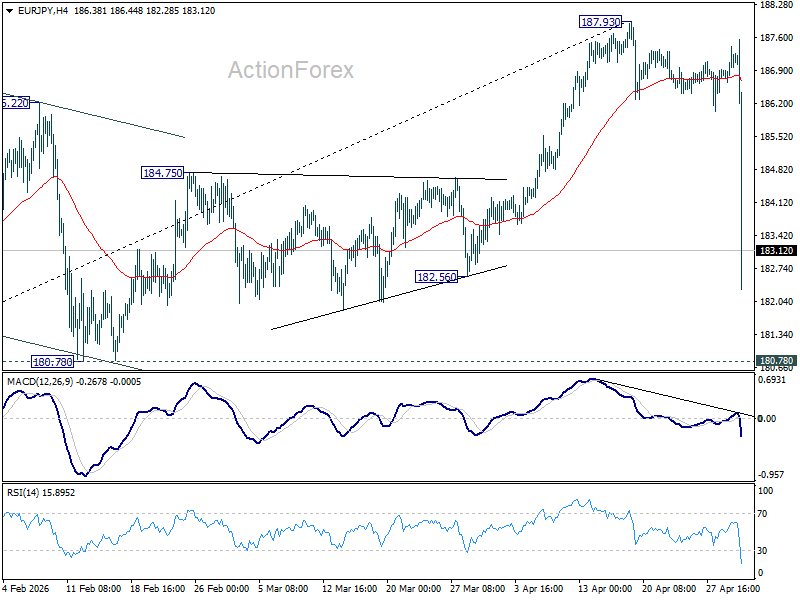

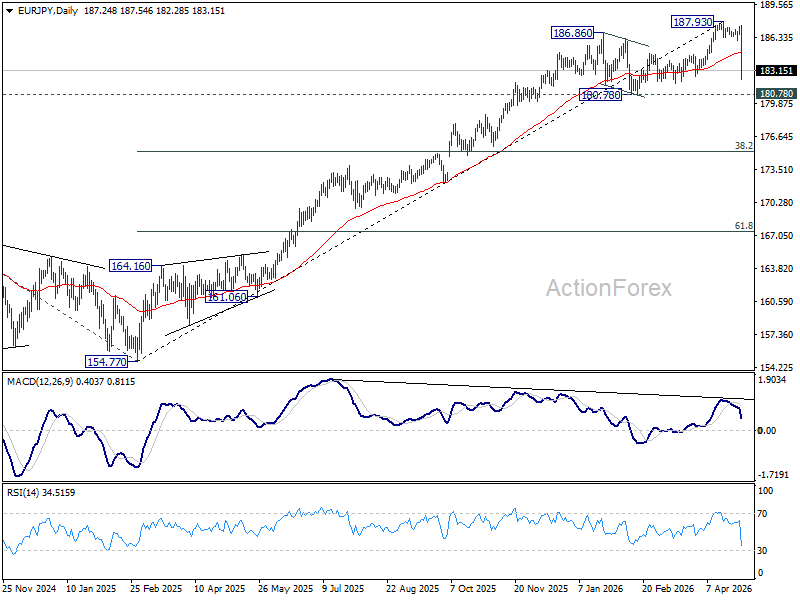

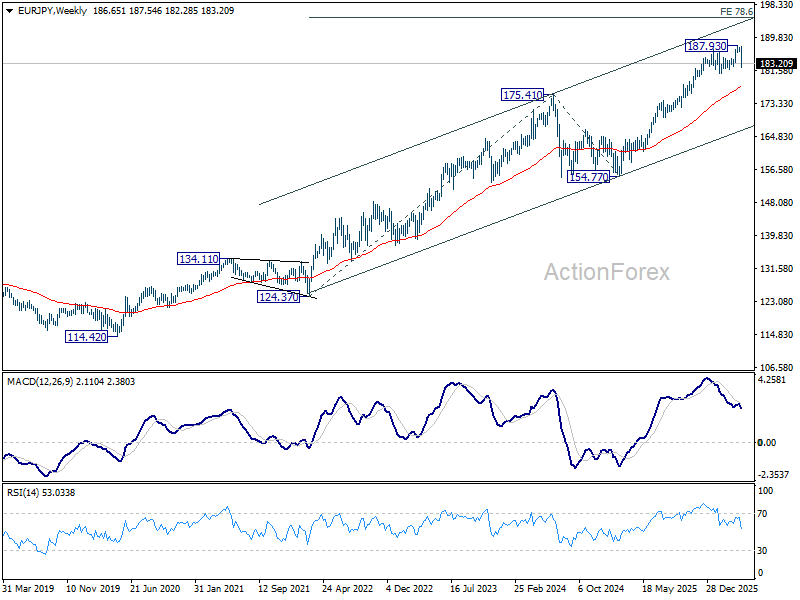

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 186.82; (P) 187.15; (R1) 187.64; More...

EUR/JPY's steep decline and strong break of 55 D EMA suggests medium term topping at 187.93, on bearish divergence condition in D MACD. Deeper fall could be seen to 180.78. But strong support should emerge there to bring rebound, at least on first attempt. However, decisive break of 180.78 will argue that it's already correcting whole five-wave impulse from 154.77. Next target will be 38.2% retracement of 154.77 to 187.93 at 175.26.

In the bigger picture, while today's fall is steep, there is no sign of reversal yet. Up trend from 114.42 is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 177.50) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.

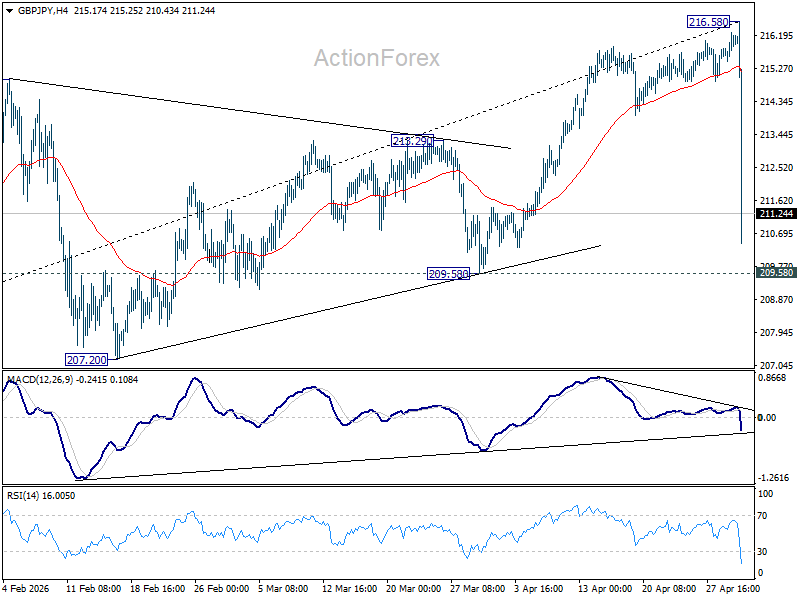

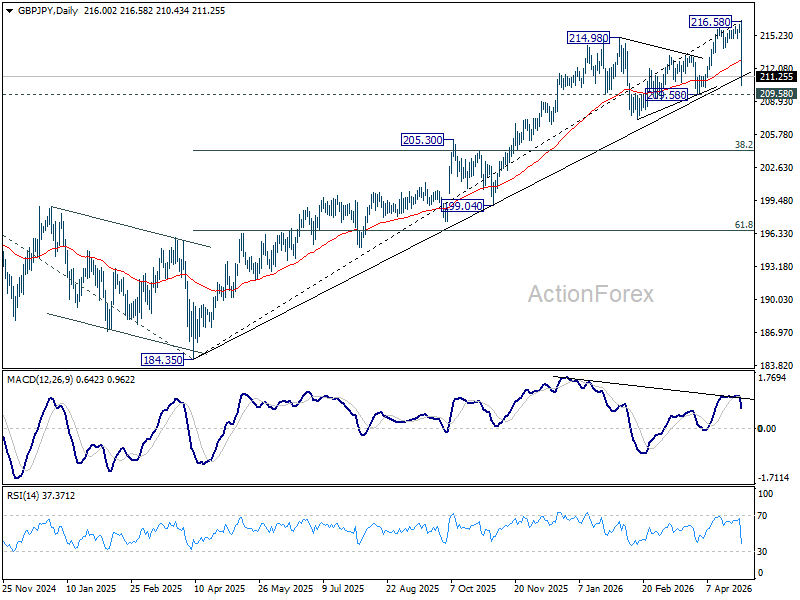

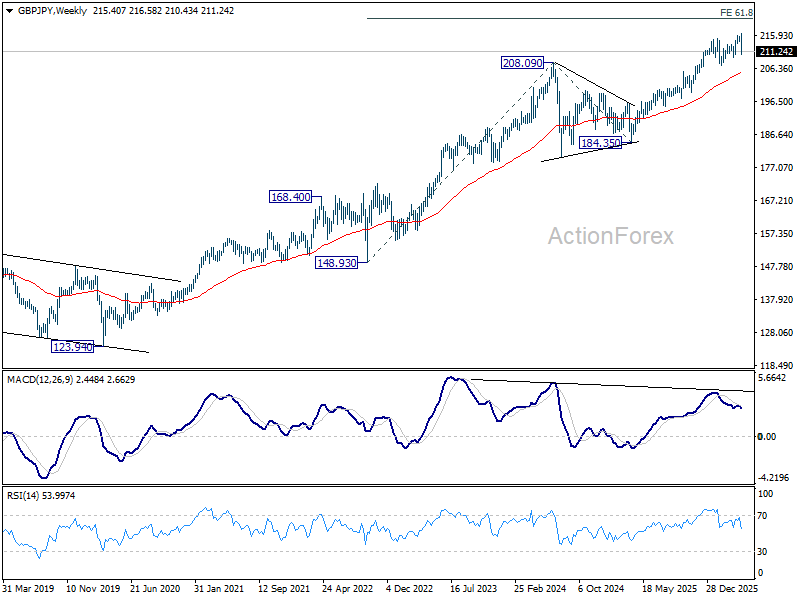

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 215.64; (P) 215.97; (R1) 216.52; More...

GBP/JPY's steep decline and strong break of 55 D EMA today suggests that a medium term top was already formed at 216.58, on bearish divergence condition in D MACD. While deeper fall cannot be ruled out, strong support should emerge from 209.58 to bring rebound, at least on first attempt. However, firm break of 209.58 will solidify the case that it's already correcting the whole five-wave rally from 184.35. In this case, 38.2% retracement of 184.35 to 216.58 at 204.28 will be the next target.

In the bigger picture, while the fall from 216.58 is steep, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 205.09) will argue that it's already in medium term down trend for 184.35 support.

Bitcoin’s (BTC/USD) Price Outlook: Struggling Against Resistance in a High-Stakes Consolidation Phase

- Bitcoin (BTC/USD) is in a high-stakes consolidation phase

- On the H4 chart, BTC is trading below the 50-MA and the 100-MA.

- Key Levels to Watch - Resistance: 77480, 78197, 80000 Support: 75880, 75000, 74250

Bitcoin has enjoyed a period of relative strength, yet as we move into the latter half of the week, the alpha-crypto is facing a cluster of technical hurdles.

Price action suggests a tug-of-war between bulls attempting to maintain the medium-term recovery and bears looking to capitalize on a descending trendline that has capped gains since the recent highs.

H4 Chart: The Macro Battleground

On the H4 timeframe, the broad structure remains somewhat confined. The most notable feature is the descending trendline (black) originating from the 79200 peak. Recent price action shows BTC struggling to make a clean break above this resistance.

The $78,197 level (purple line) remains the "line in the sand" for bulls. While we saw a spike above this earlier in the week, it was short-lived, resulting in a swing high that was quickly sold off. Currently, BTC is trading between the 50-SMA (blue) and the 100-SMA (orange). A sustained move back above the 50-SMA (around $77,452) is required to shift the H4 sentiment back to a clear bullish bias. Conversely, the 75000 level remains the primary psychological support that must hold to prevent a deeper correction.

Bitcoin (BTC/USD) Four-Hour Chart, April 30, 2026

Source: TradingView.com (click to enlarge)

H1 Chart: Consolidation and MA Squeeze

Moving down to the H1 chart, we can see a more granular view of the recent volatility. The price is currently below the Moving Averages. The 50-MA (blue) is acting as immediate dynamic resistance near 76334, while the 100 and 200-MAs are converging above the price.

The RSI (Relative Strength Index) on this timeframe is hovering around the 50 mark, suggesting a lack of clear directional momentum. This "squeeze" typically precedes a volatile breakout. Watch for a candle close above the H1 50-MA to signal a run toward the 78197 resistance zone.

Bitcoin (BTC/USD) One-Hour Chart, April 30, 2026

Source: TradingView.com (click to enlarge)

M15 Chart: Intraday Scenarios for Upcoming Sessions

The M15 chart highlights the immediate intraday battle. We see a series of "Bull" and "Pivot" signals on the RSI Divergence indicator, suggesting that buyers are stepping in at the 75500 - 75800 range.

The Bullish Scenario: For the bulls to take control in the upcoming sessions, we need to see a decisive break above the intraday descending trendline currently sitting near 76500. If price can clear this and flip the H4 50-MA into support, the path opens for a retest of the 78197 resistance. A breach of 78197 would then put the psychological 80000 mark back in focus.

The Bearish Scenario: On the flip side, the inability to break the current intraday trendline suggests exhaustion. If BTC fails to hold the 50-MA on the M15 (currently around 75888), we could see a quick slide back toward the 75000 support level. A break below 75000 would be significant, likely triggering a cascade of sell orders and potentially opening the door for a move toward the 73500 region.

Key Levels to Watch:

- Resistance: 77480, 78197, 80000

- Support: 75880, 75000, 74250

Bitcoin (BTC/USD) M15 Chart, April 30, 2026

Source: TradingView.com (click to enlarge)

Bitcoin is at a crossroads. While the underlying trend has shown resilience, the technicals suggest we are in a consolidation phase. Traders should keep a close eye on the 75000 support and the 78197 resistance; a break of either side will likely define the trend for the remainder of the week.