Sample Category Title

Fed’s Daly advocates for gradual rate cuts to avoid overtightening

San Francisco Fed President Mary Daly indicated in an interview with the Financial Times that the time has come to consider gradually lowering interest rates from their current levels. Daly emphasized the importance of a cautious approach, stating, "Gradualism is not weak, it's not slow, it's not behind, it’s just prudent."

She explained that while Fed aims to reduce the “restrictiveness” of its policy, it intends to maintain a level of restraint necessary to “fully get the job done” on inflation. Daly underscored the Fed's focus on avoiding the risk of "overtightening into a slowing economy."

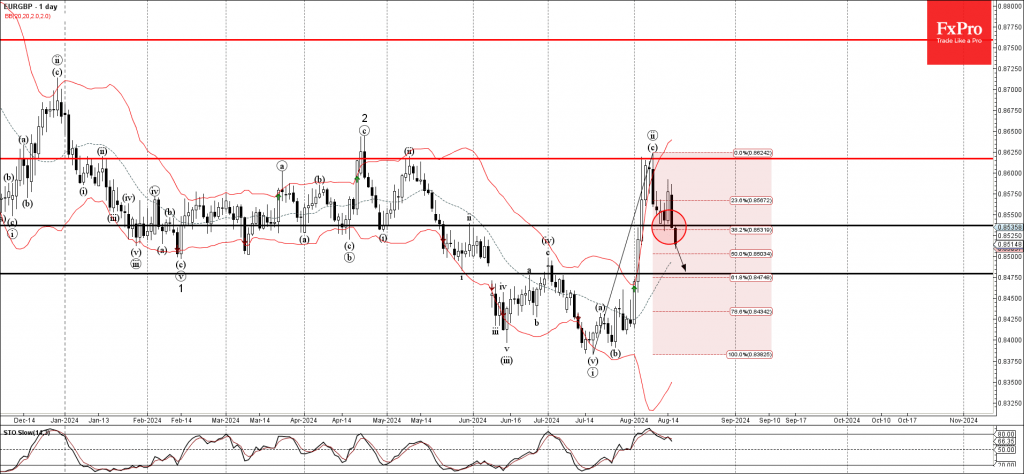

EURGBP Wave Analysis

- EURGBP broke support area

- Likely to fall to support level 0.8475

EURGBP currency pair just broke the support area set between the support level 0.8535 (which reversed the price twice earlier this week) and the 38.2% Fibonacci correction of the earlier sharp upward impulse from July.

The breakout of this support area is aligned with the clear multi-month downtrend seen on the daily EURGBP charts.

Given the strongly bullish sterling sentiment seen across the FX markets today, EURGBP currency pair can be expected to fall further toward the next support level 0.8475.

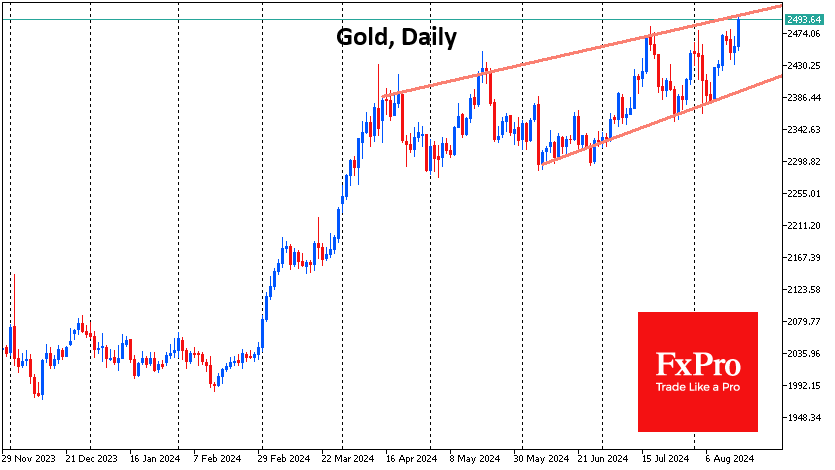

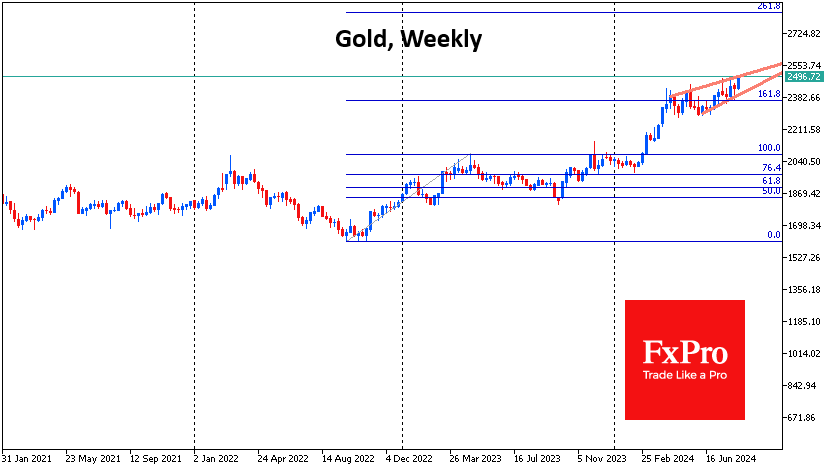

Gold: Third Time Lucky?

Gold has been rising steadily since the end of last week and is attempting to consolidate above $2470 per troy ounce on the spot market for the third time in the last 30 days. Gold has moved in tandem with equities this month, but it is worth noting that it fell less aggressively during the panic and outpaced the rally.

So, gold is riding on a global recovery in demand for risk assets, but it has the fundamental support in its arsenal that has pushed the price to repeated all-time highs since March.

A trend line can be drawn across the local lows of May from which gold rallied in the early days of August. Combined with local resistance at $2475, this forms a bullish triangle with a high probability of a breakout.

The next upside target is $2500. This is the psychologically important round level and the resistance line of the uptrend drawn by the April, May and July highs.

As far as more distant growth targets are concerned, the $2800-2900 area is worth mentioning. The upper boundary of this range is the 261.8% Fibonacci level of growth from the September-October 2022 lows to the April 2023 highs.

The lower boundary of the range is formed by the 161.8% level of the growth impulse from the October lows to the April-May highs. This rally began with the first signs of a shift in the Fed’s monetary policy, supported by tensions in the Middle East and the desire of some central banks to diversify their reserves away from the dollar.

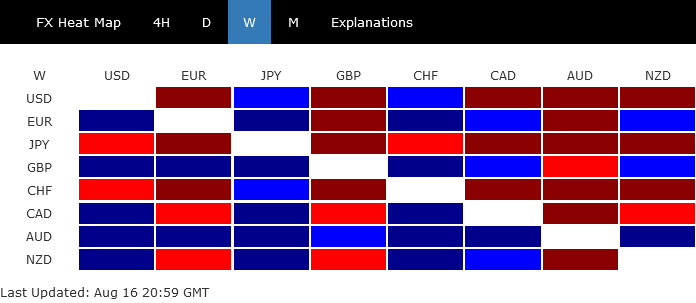

Markets Roar Back as Recession Fears Fade, Safe Havens Crumble

The past few weeks highlighted the volatility of global financial markets and how quickly investor sentiment can shift. The sharp selloff in US markets, driven by fears of an impending recession, now appears significantly overdone in light of last week's robust rebound. Strong retail sales data was a key factor in this turnaround, showing that US consumers remain resilient and continue to drive economic growth, helping to quell recession concerns. While it may be premature to expect major US indexes to resume their record runs that soon, the range for consolidations, even as medium term ones, should have been largely set.

In response to this shift in sentiment, the forex markets saw a broad retreat in safe-haven currencies. Yen took the hardest hit, followed closely by Swiss Franc and then Dollar. Conversely, Australian Dollar stood out as the star performer, buoyed not only by the global risk-on sentiment but also by strong domestic job data, which reinforced RBA's stance on to hold off on rate cuts for the foreseeable future.

British Pound also had a strong week, ranking as the second-best performer, as a series mixed economic reports left the market uncertain about timing of BoE's next cut. Euro rounded out the top three, supported by buying interest against Dollar, Yen, and Swiss Franc.

Meanwhile, Canadian and New Zealand Dollars ended the week in the middle of the performance pack. Notably, New Zealand Dollar showed remarkable resilience despite RBNZ's surprise dovish rate cut.

US Markets Soars as Recession Fears Diminish, Dollar Set for Further Weakness

Last week saw a dramatic turnaround in market sentiment in the US, with S&P 500 posting an impressive 3.9% gain, its best weekly performance in 2024. NASDAQ surged even higher, with a 5.2% increase, while DOW rose by 2.9%. This wave of optimism wasn't confined to the US alone—global markets followed suit, with Japan's Nikkei 225 delivering an extraordinary 8.7% gain, closing over 22% higher from its previous week's spike low.

The primary catalyst for this rally was the much stronger-than-expected US retail sales data for July. While the growth was heavily driven by auto sales—a segment known for its volatility—investors interpreted the robust consumer spending as a reassuring sign that the US economy might avoid a recession.

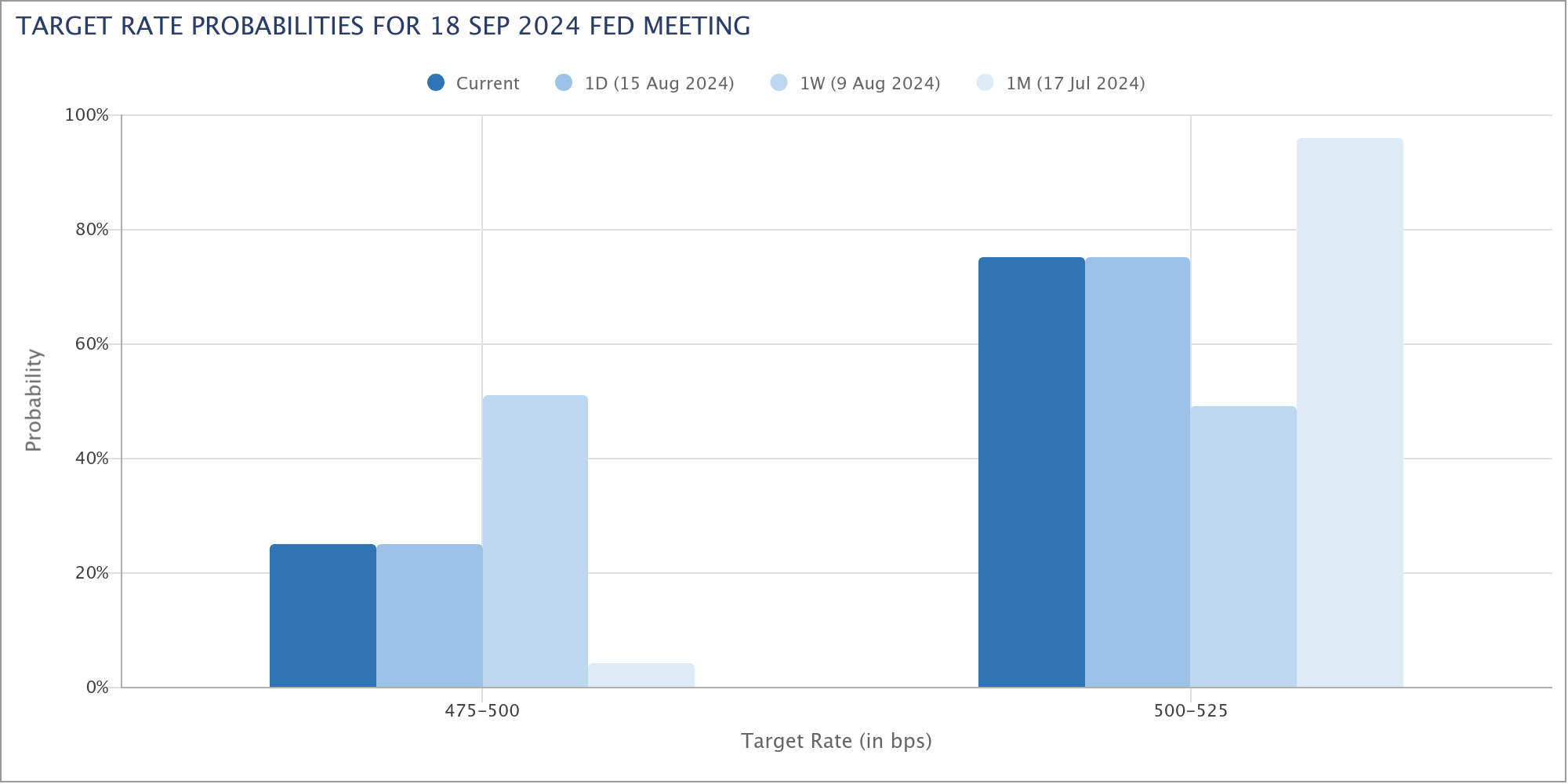

This optimism was further supported by the latest CPI data, which showed continued progress in disinflation. The CPI figures helped solidify Fed's path toward starting monetary easing in September, without the need for an emergency inter-meeting rate cut or a large initial cut. Reflecting this sentiment, fed fund futures now price in only a 25% chance of a 50 basis point cut in September, down from over 55% just a week ago.

However, it's important to remember that the situation remains fluid. There is still one more non-farm payroll report scheduled for September 6, and another CPI report on September 13, both of which could influence the Fed's decision during its September 17-18 meeting.

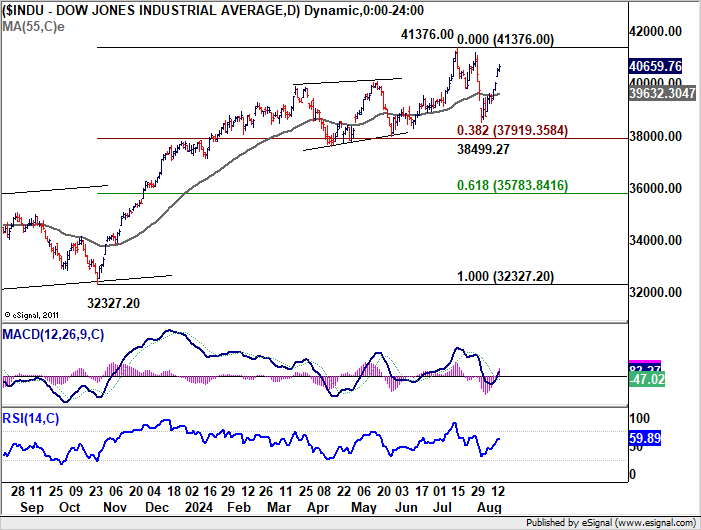

DOW's strong rally confirmed that pullback from 41376.00 has completed at 38499.27. The strong support from 38.2% retracement of 32327.20 to 41376.00 at 37919.35 suggests that price actions from 41376.00 are merely consolidation to rally from 32327.20, not a larger scale correction.

For now, another falling leg could still be seen before the consolidation pattern completes. But downside should be contained by 37919.35 fibonacci support. Another record is envisaged as the up trend resumes at a later stage.

Dollar Index struggled in range above 102.16 last week as Fed expectations were counted by risk-on sentiment. But technically, outlook will stay bearish as long as 103.65 support turned resistance holds. Break of 102.16 will resume the fall from 106.13 towards 99.57/100.61 support zone.

More importantly, further decline in Dollar Index would push it through medium term trend line support, which would argue that consolidation from 99.57 (2023 low) has completed with three waves to 106.13. Further break of 100.61 support will suggest that the down trend from 114.77 (2022 high) is ready to resume through 99.57 to 61.8% projection of 114.77 to 99.57 from 106.13 at 96.73.

The bearish scenario for the Dollar Index could gain traction if the risk-on sentiment persists, pushing US stock indexes to new record highs.

Sterling Strengthens as BoE Rate Cut Uncertain After Data

Sterling was the second best performer last week after the slew of economic data left no decisive conclusion about whether BoE would cut interest rate again in September. The uptick in July's UK CPI was less than expected while core CPI continued slowing. However, job data was robust while Q2 GDP growth matched expectations. Retail sales in July showed strong rebound even though it missed expectations slightly.

As a result, markets are currently pricing in less than 50% chance of a rate cut in September, with the decision likely to be as closely contested as the one in August. There is a plausible scenario where the BoE might delay a rate cut until November when new economic forecasts and Q3 data are available. However, with only one more Monetary Policy Committee meeting scheduled in December, this could limit BoE to just a total of 50 bps cut this year.

GBP/USD's strong rally last week suggests that correction from 1.3043 has completed at 1.2664 already. Rise from 1.2298 might be ready to resume through 1.3043 to 61.8% projection of 1.2298 to 1.3043 from 1.2664 at 1.3124, which is close to 1.3141 high.

More importantly, any further upside acceleration would raise the chance that GBP/USD is indeed trying to resume whole up trend 1.0351 (2022 low). That would set the stage to 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364 next.

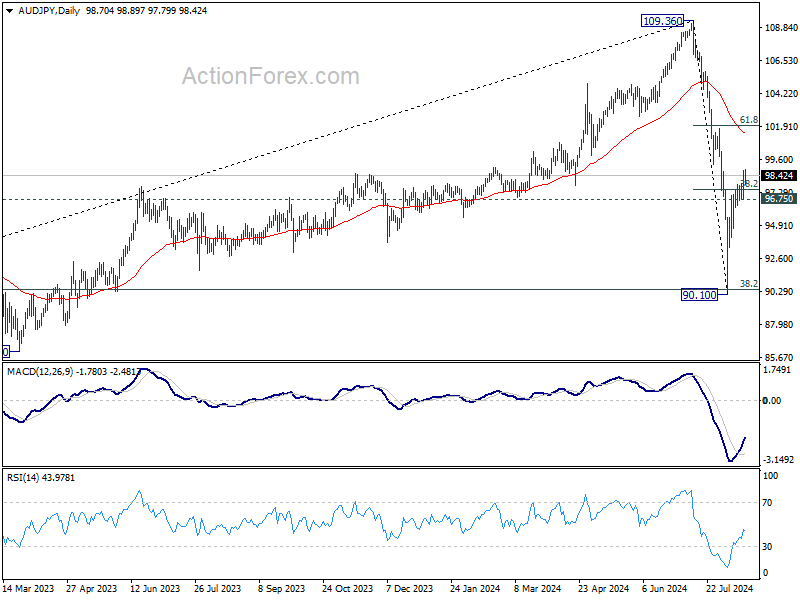

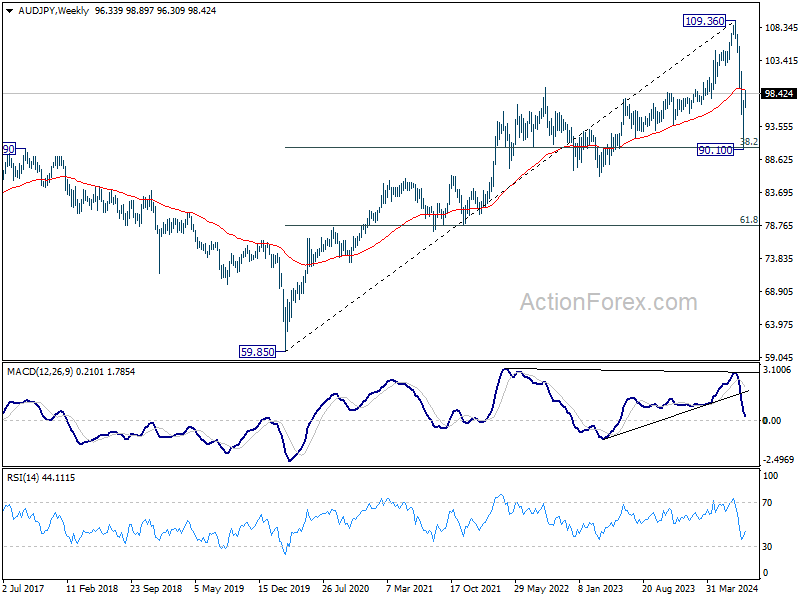

Aussie Leads the Pack as Risk-On Sentiment Boosts Markets, Kiwi Shows Resilience Post-RBNZ Cut

Australian Dollar stood out as the strongest performer in the currency markets last week, driven by a combination of renewed risk-on sentiment and surprisingly robust domestic job data. Additionally, RBA has maintained a clear stance against any imminent rate cuts, which further supported the Aussie's strength. Unless there is an unexpected U-turn similar to the recent surprise from RBNZ, the earliest realistic time for RBA to consider a rate cut is February 2025.

Speaking of New Zealand, Kiwi displayed remarkable resilience despite RBNZ's unexpected rate cut. Although the Kiwi lost ground against the Euro, Sterling, and Aussie, it managed to hold its own against other major currencies. RBNZ's new economic projections were notably dovish, with significant downgrades in Q2 and Q3 growth forecasts, making another rate cut this year almost certain. The key debate now is whether RBNZ will move to cut rates at both of its remaining meetings this year or opt for just one.

Technically, AUD/JPY's extended rebound last week and break of 38.2% retracement of 109.36 to 90.10 at 97.45 suggests that fall from 109.36 has completed at 90.10 already. Further rise is now in favor as long as 96.75 support holds, to 61.8% retracement at 102.22. However, as current rebound is seen as the second leg of the medium term corrective pattern from 109.36, strong resistance could emerge around 102.22 to limit upside.

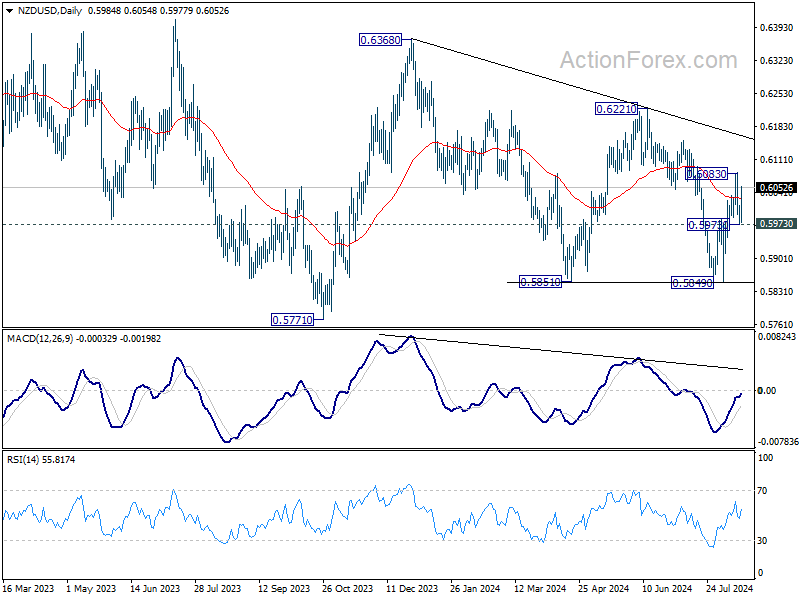

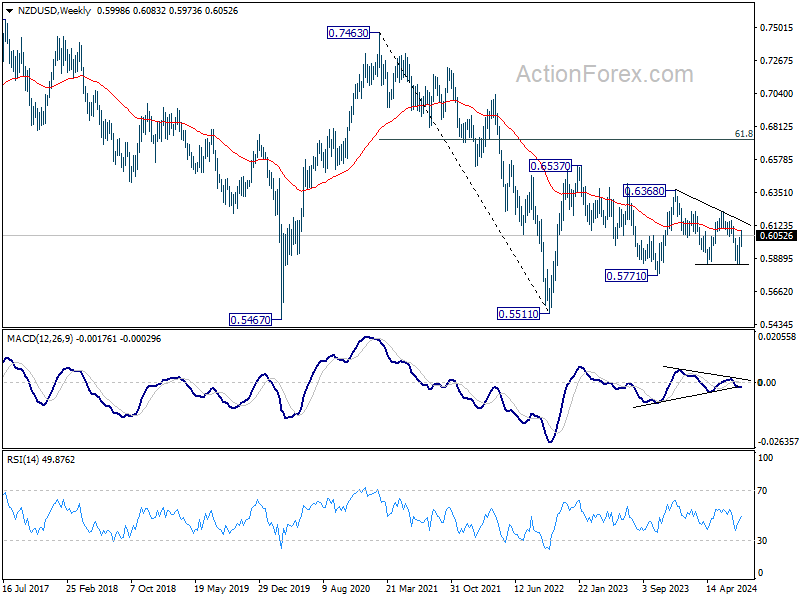

NZD/USD's post RBNZ retreat was rather brief as it quickly rebounded after hitting 0.5973. Further rally is now expected as long as 0.5973 support holds, and break of 0.6083 will target trend line resistance (now at around 0.6164). For now, it's too early to decide whether NZD/USD is ready to breakout from the converging range pattern that started back in 2022 at 0.5511. So, beware of strong resistance from the falling trend line to limit upside.

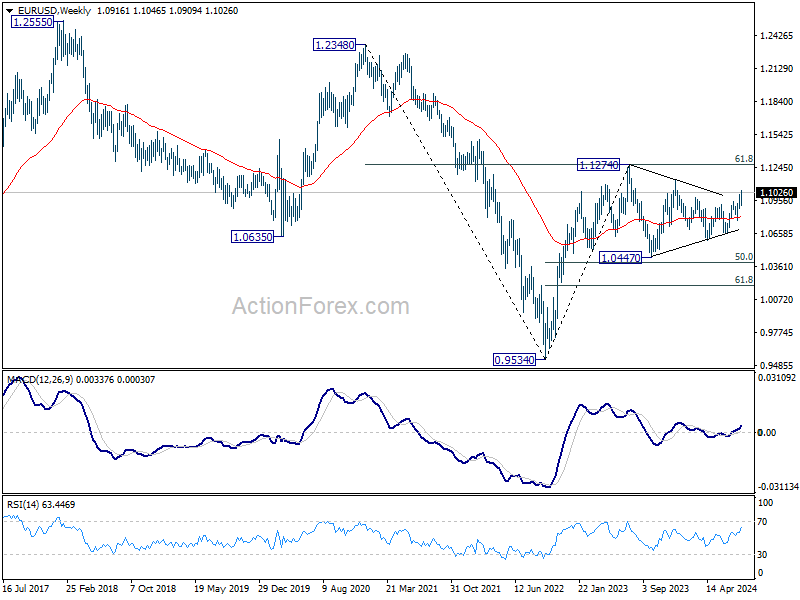

EUR/USD Weekly Outlook

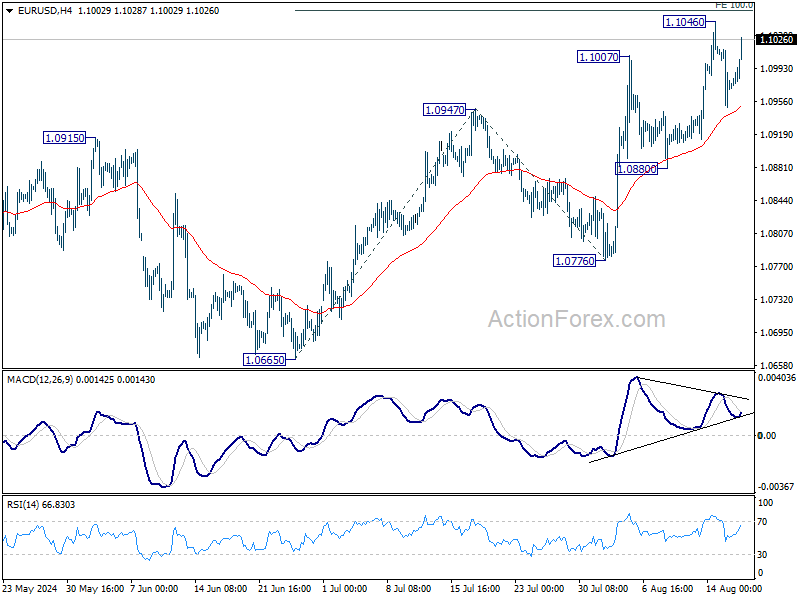

EUR/USD retreated after edging higher to 1.1046 last week but stayed in range above 1.0880 support. Initial bias remains neutral this week for consolidations, and further rally is in favor. On the upside, firm break of 100% projection of 1.0665 to 1.0947 from 1.0776 at 1.1058 could prompt upside acceleration through 1.1138 resistance to 161.8% projection at 1.1232. However, considering bearish divergence condition in 4H MACD, break of 1.0880 will suggest near term reversal and turn bias to the downside for 1.0776 support and below.

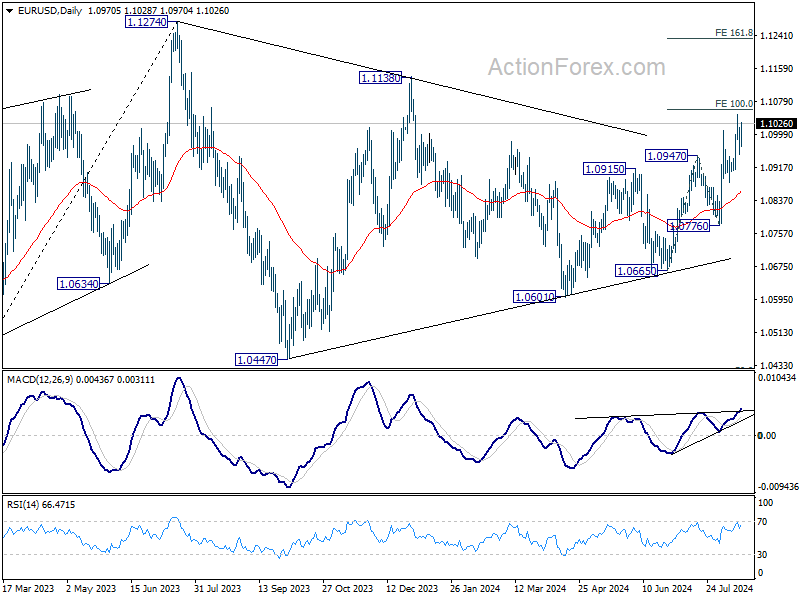

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's could still extend. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0776 support will extend the correction with another falling leg back towards 1.0447 support.

In the long term picture, a long term bottom is in place at 0.9534 (2022 low). Sustained break of 55 M EMA (now at 1.1012) will raise the chance of long term reversal. But even in this case, firm break of 1.2348 structural resistance is needed to confirm. Rejection by 55 M EMA will maintain bearishness for extend the down trend from 1.6039 (2008 high) through 0.9534 at a later stage.

EUR/USD Weekly Outlook

EUR/USD retreated after edging higher to 1.1046 last week but stayed in range above 1.0880 support. Initial bias remains neutral this week for consolidations, and further rally is in favor. On the upside, firm break of 100% projection of 1.0665 to 1.0947 from 1.0776 at 1.1058 could prompt upside acceleration through 1.1138 resistance to 161.8% projection at 1.1232. However, considering bearish divergence condition in 4H MACD, break of 1.0880 will suggest near term reversal and turn bias to the downside for 1.0776 support and below.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's could still extend. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0776 support will extend the correction with another falling leg back towards 1.0447 support.

In the long term picture, a long term bottom is in place at 0.9534 (2022 low). Sustained break of 55 M EMA (now at 1.1012) will raise the chance of long term reversal. But even in this case, firm break of 1.2348 structural resistance is needed to confirm. Rejection by 55 M EMA will maintain bearishness for extend the down trend from 1.6039 (2008 high) through 0.9534 at a later stage.

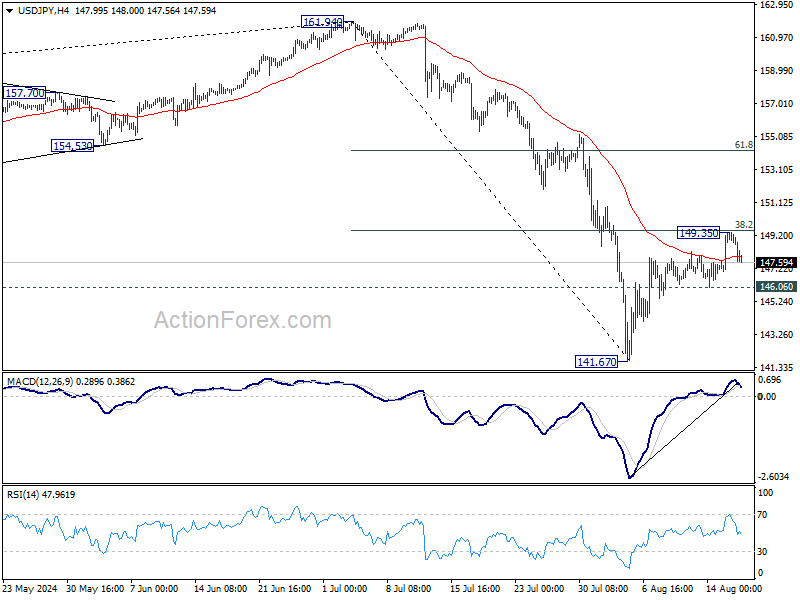

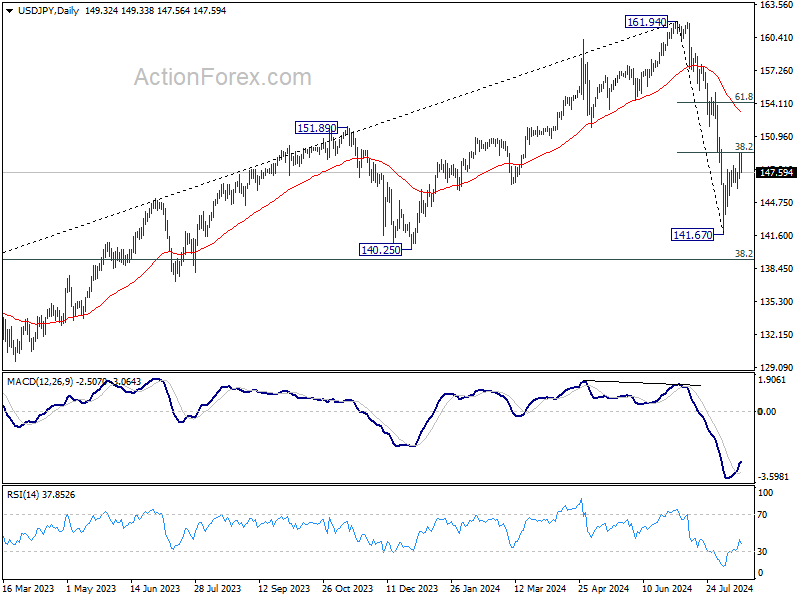

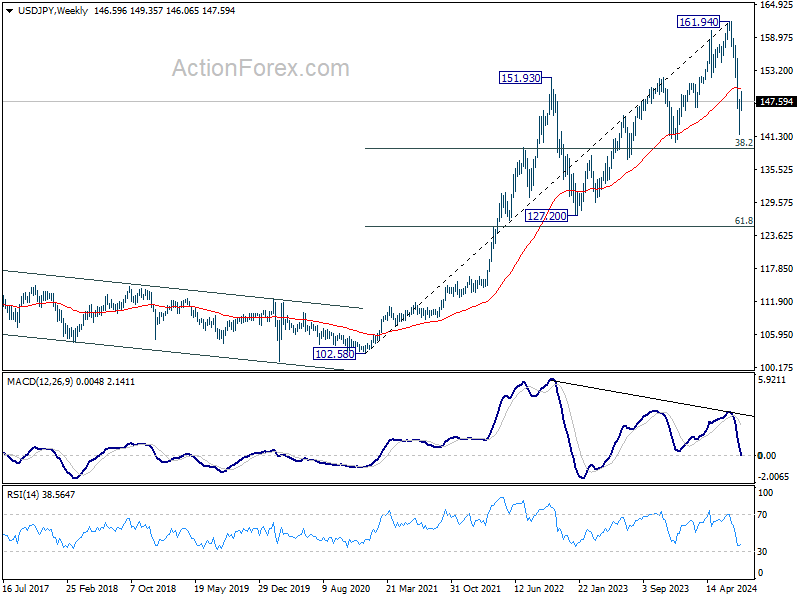

USD/JPY Weekly Outlook

USD/JPY's rebound from 141.67 extended higher last week but failed to break through 38.2% retracement of 161.94 to 141.67 at 149.41 and retreated. Initial bias remains neutral this week first. On the downside, break of 146.06 minor support will suggest rejection by 149.91, and turn intraday bias back to the downside for retesting 141.67 low. On the upside, sustained break of 149.41 will extend the rebound to 61.8% retracement at 154.19, as the second leg of the corrective pattern from 161.94.

In the bigger picture, fall from 161.94 medium term is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.86) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

In the long term picture, it's still early to conclude that up trend from 75.56 (2011 low) has completed. However, a medium term corrective phase should have commenced, with risk of deep correction towards 55 M EMA (now at 132.84).

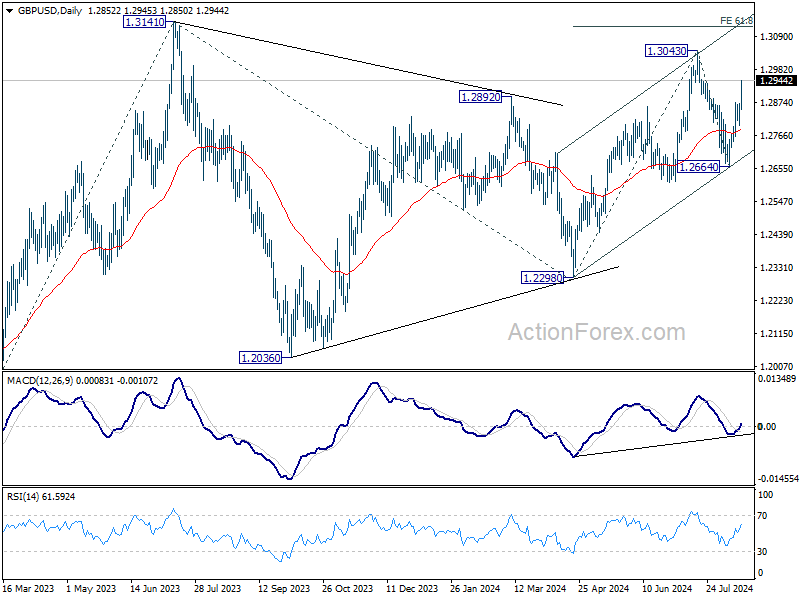

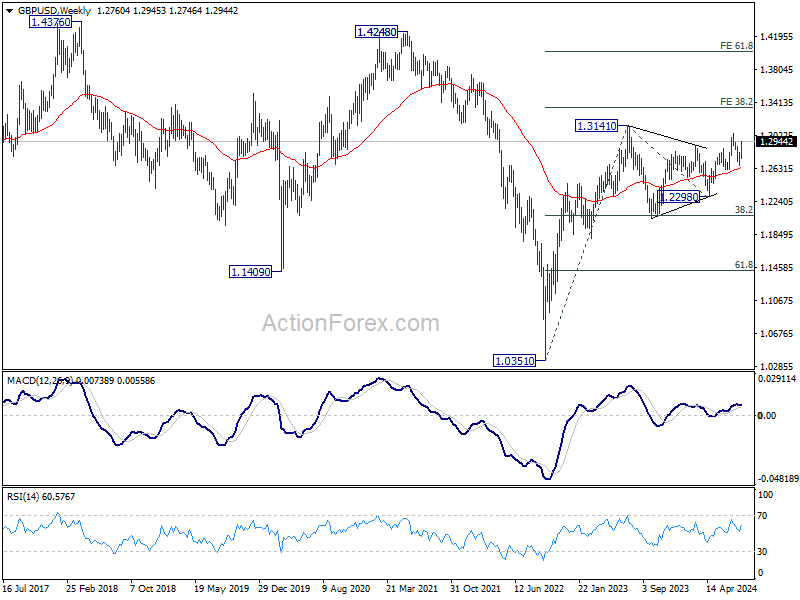

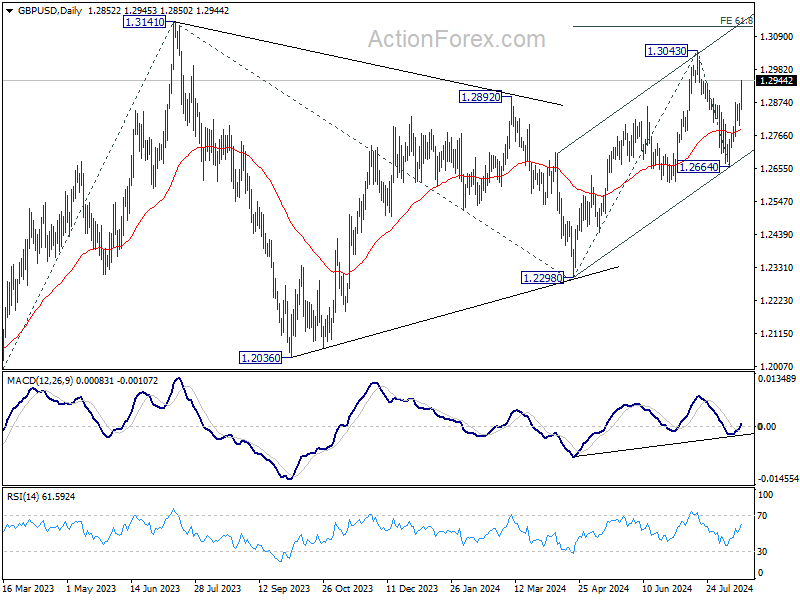

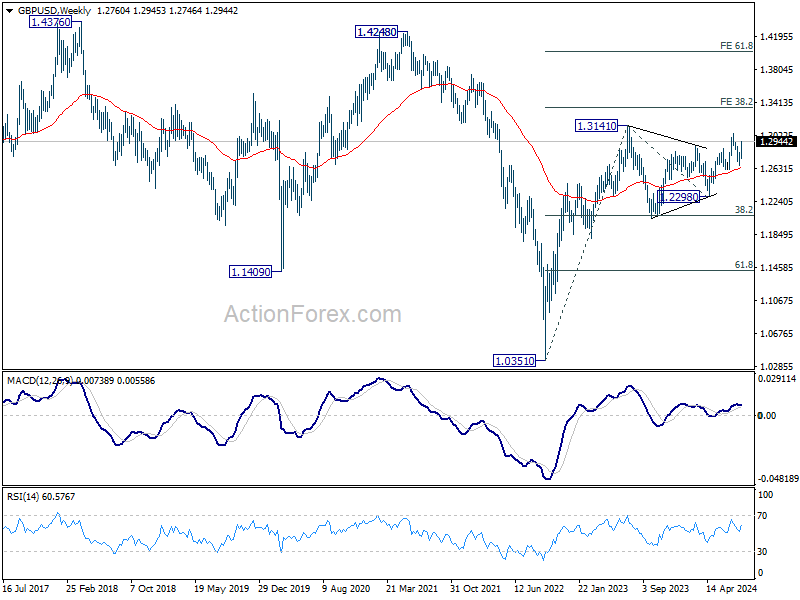

GBP/USD Weekly Outlook

GBP/USD's strong rally last week indicates that correction from 1.3043 has completed at 1.2664 already ahead of 1.2612 support. Initial bias remains on the upside this week for retesting 1.3043. Firm break there will resume whole rise from 1.2998 to 61.8% projection of 1.2298 to 1.3043 from 1.2664 at 1.3124, which is close to 1.3141 high. On the downside, however, break of 1.2798 support will turn bias back to the downside for 1.2664 support instead.

In the bigger picture, corrective pattern from 1.3141 might have completed at 1.2298 already. Rise from there could be resuming the larger up trend from 1.0351 (2022 low). Decisive break of 1.3141 will target 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364 next. However, break of 1.2664 support will delay this bullish case once again and extend the corrective pattern from 1.3141.

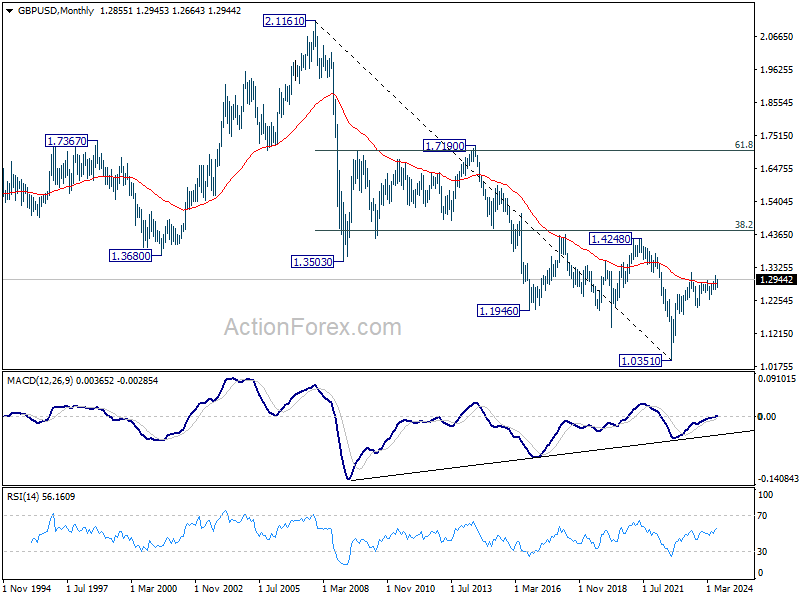

In the long term picture, as long as 1.2298 support holds, rise from 1.0351 long term bottom is expected to continue. But still, firm break of 1.4248 structural resistance is needed to indicate bullish trend reversal. Otherwise, price actions from 1.0351 are tentatively seen as a consolidation pattern only.

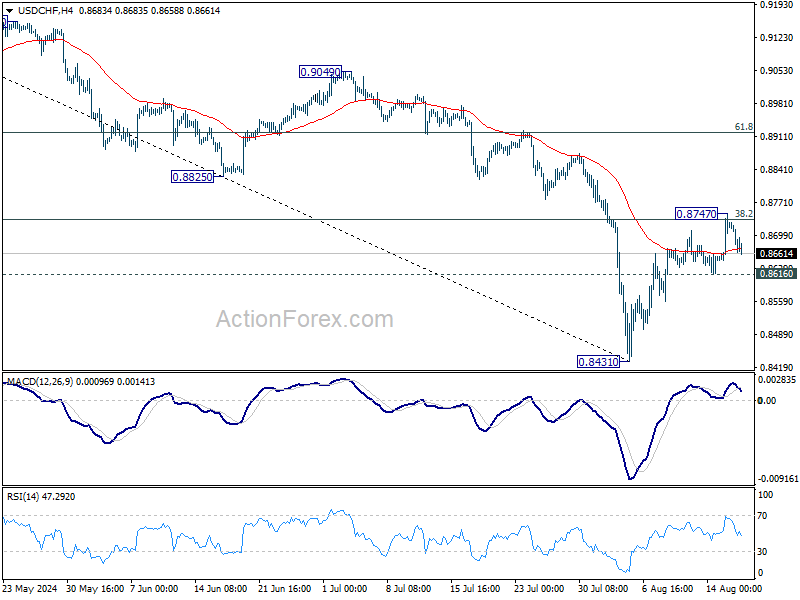

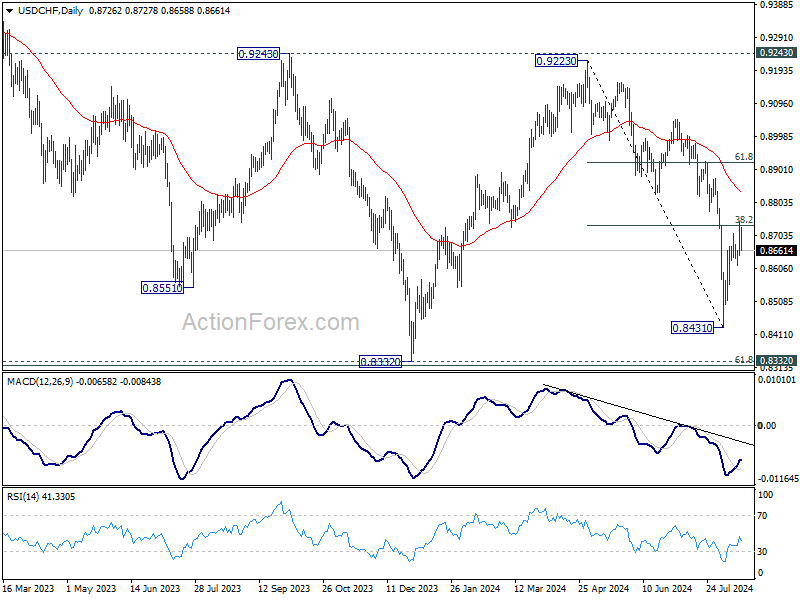

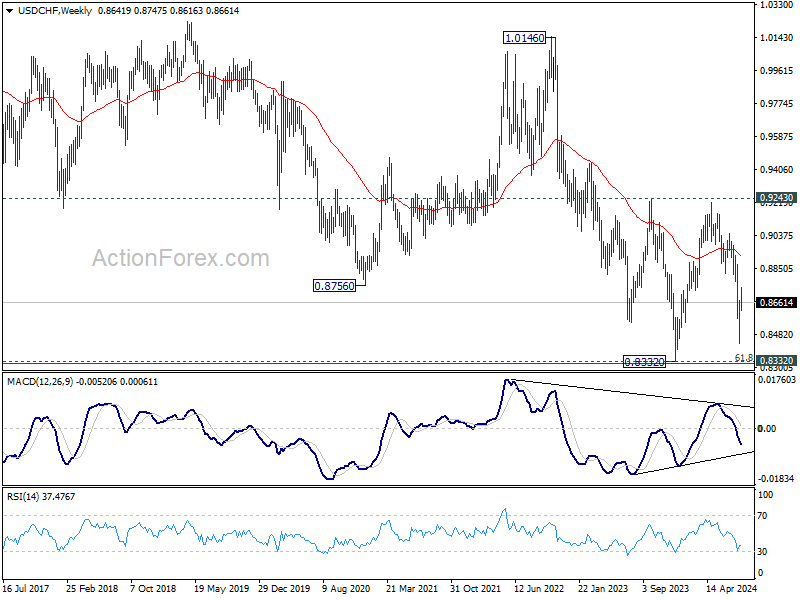

USD/CHF Weekly Outlook

USD/CHF's rebound from 0.8431 extended to 0.8747 last week, but failed to sustain above 38.2% retracement of 0.9223 to 0.8431 at 0.8734 and retreated. Initial bias remains neutral this week first. On the upside, sustained break of 0.8734 will extend to 61.8% retracement at 0.8920, even as a corrective move. On the downside, break of 0.8616 support will indicate rejection by 0.8734, and turn bias back to the downside for retesting 0.8431 low.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

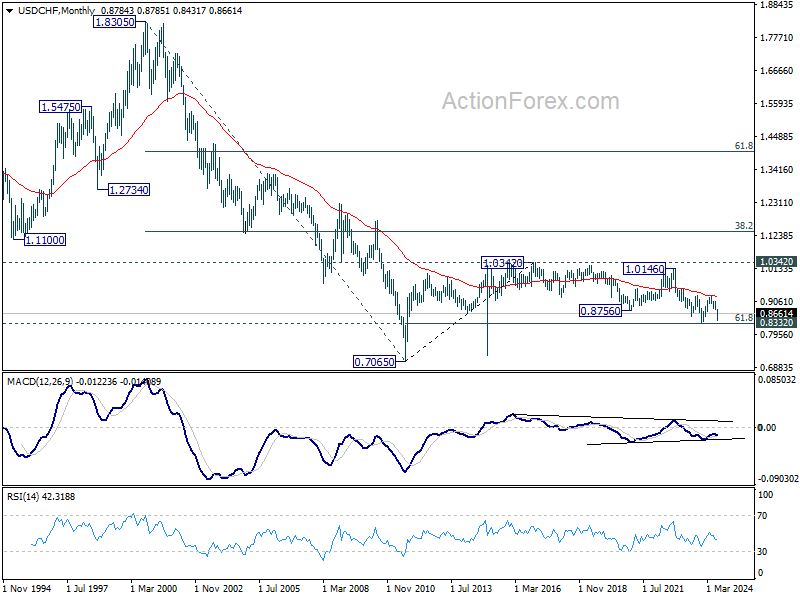

In the long term picture, price action from 0.7065 (2011 low ) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). Fall from 1.0342 (2016 high) is seen as the second leg. Rejection by 55 M EMA suggest that this fall is in progress. Break of 61.8% retracement of 0.7065 to 1.0342 at 0.8317 will pave the way back to 0.7065.

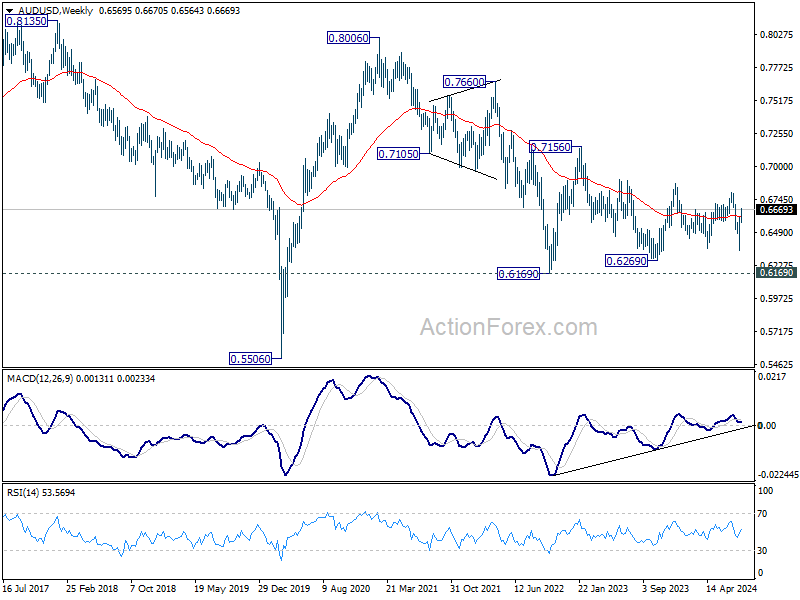

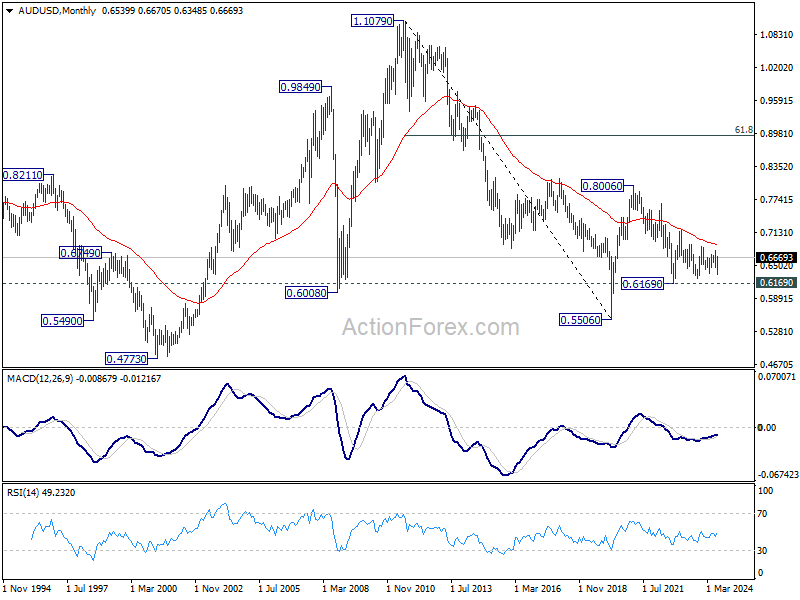

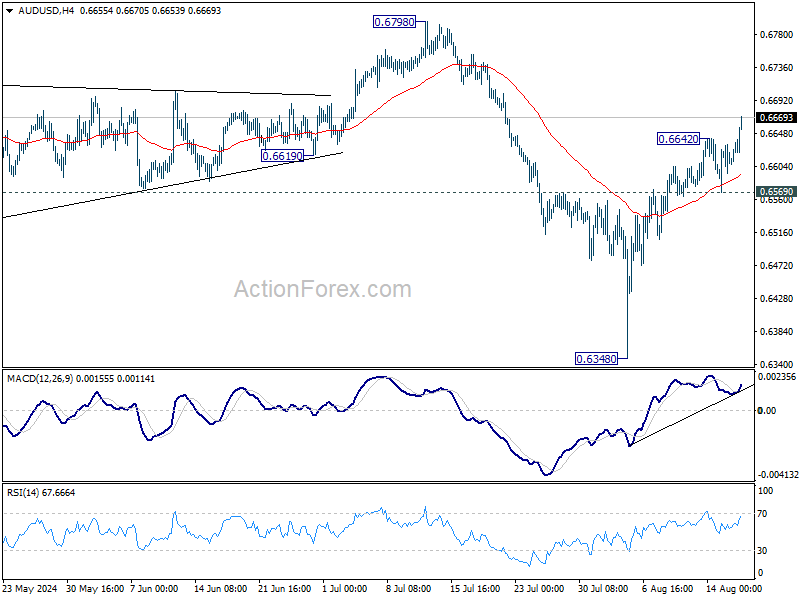

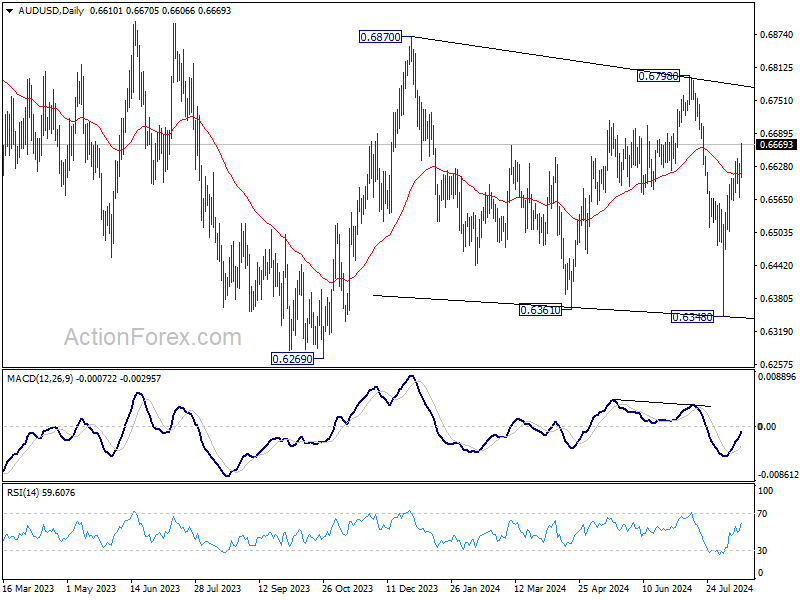

AUD/USD Weekly Report

AUD/USD's rally from 0.6348 extended higher last week and with late break of 0.6642 temporary top, initial bias is back on the upside this week. Further rise should be seen to 0.6798 resistance next. On the downside, below 0.6569 minor support will turn bias to the downside for retreat.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern. Rise from 0.6340 is likely developing into another rising leg. Firm break of 0.6798/6870 resistance zone will target 0.7156 resistance. In case of another fall, strong support should be seen from 0.6169/6361 to bring rebound.

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen as the second leg of the pattern. Hence, in case of deeper decline, strong support should emerge above 0.5506 to bring reversal.