Sample Category Title

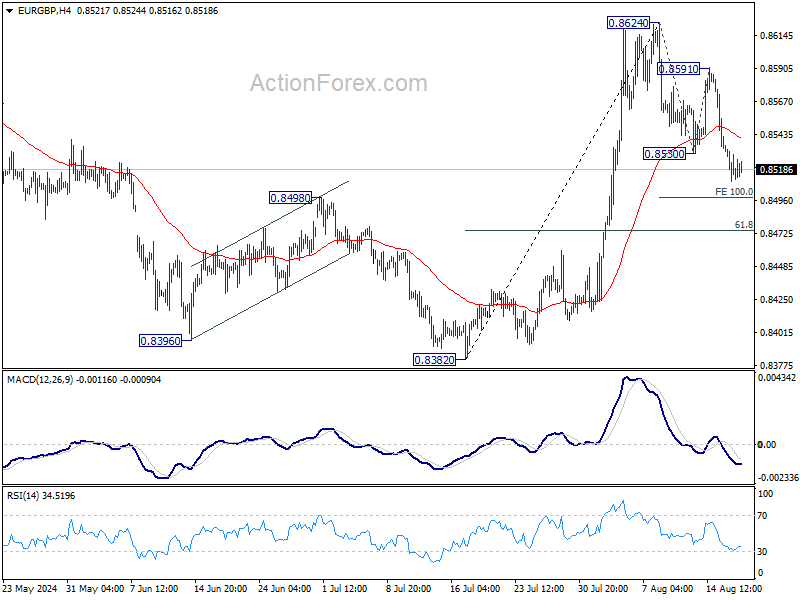

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8507; (P) 0.8523; (R1) 0.8534; More....

Intraday bias in EUR/GBP remains on the downside at this point. Correction from 0.8624 is in progress for 100% projection of 0.8624 to 0.8530 from 0.8591 at 0.8497, which is close to 55 D EMA (now at 0.8494). Strong support should be seen there to bring rebound. But for now, risk will stay on the downside as long as 0.8591 resistance holds, in case of recovery.

In the bigger picture, while the rebound from 0.8382 is strong, there is no confirmation of trend reversal yet. As long as 0.8643 resistance holds, down trend from 0.9267 could still resume through 0.8382 at a later stage. However, firm break of 0.8643 will indicate that such down trend has completed, and turn outlook bullish for 0.8764 resistance next.

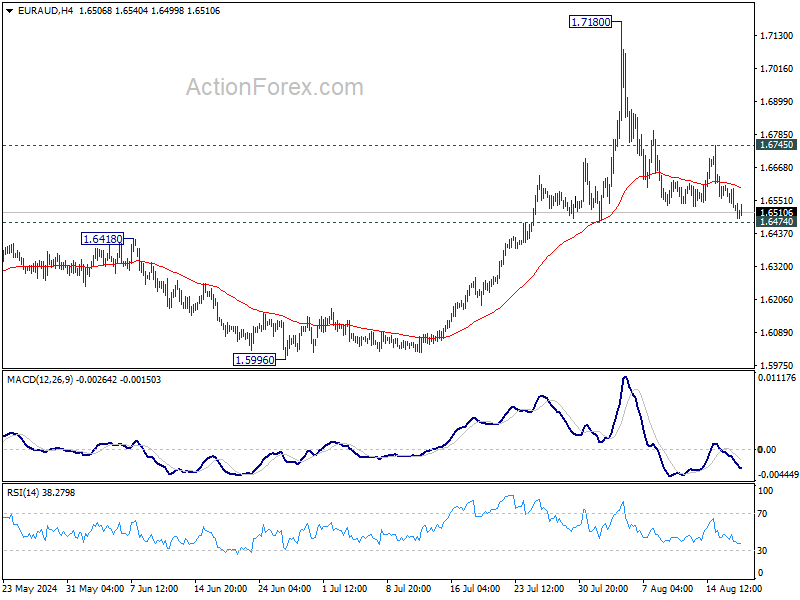

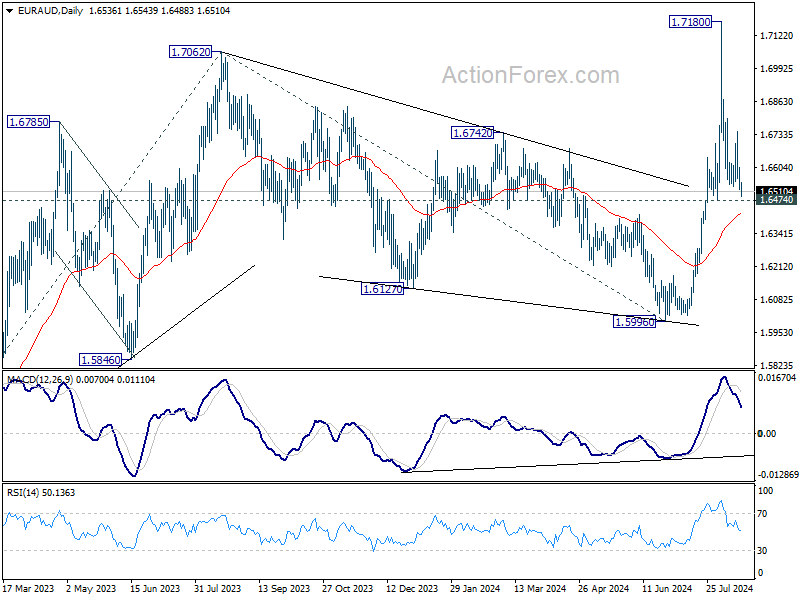

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6499; (P) 1.6553; (R1) 1.6586; More...

Intraday bias in EUR/AUD remains neutral for the moment. Further rally would remain in favor as long as 1.6740 support holds. On the upside, above 1.6745 will argue that the pullback has completed, and turn bias back to the upside for retesting 1.7180. However, firm break of 1.6474 will dampen the bullish view and bring deeper pullback towards 1.5996 support.

In the bigger picture, corrective fall from 1.7062 medium term top should have completed at 1.5996. Larger up trend from 1.4281 (2022 low) is resuming. Next target is 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715. This will now remain the favored case as long as 1.6474 support holds.

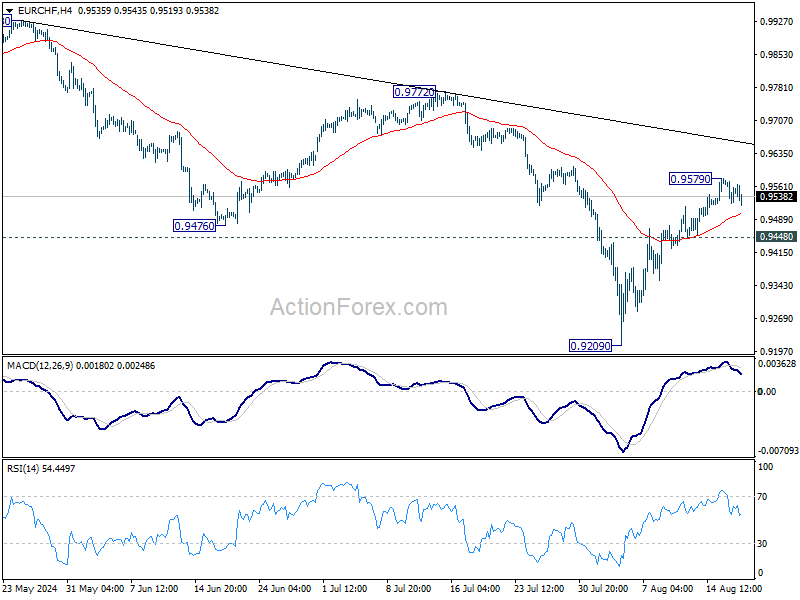

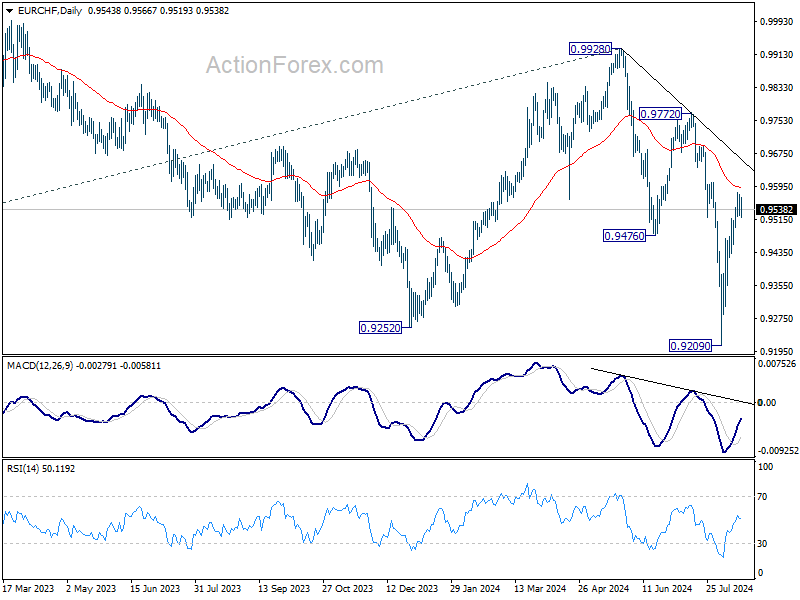

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9525; (P) 0.9552; (R1) 0.9578; More....

Intraday bias in EUR/CHF remains neutral for consolidations below 0.9579 temporary top. Further rally is expected as long as 0.9448 support holds. Sustained break of 55 D EMA (now at 0.9590) will pave the way back to 0.9972/0.9928 resistance zone. However, decisive break of 0.9448 will suggest rejection by 55 D EMA, and turn bias back to the downside for 0.9209 low.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

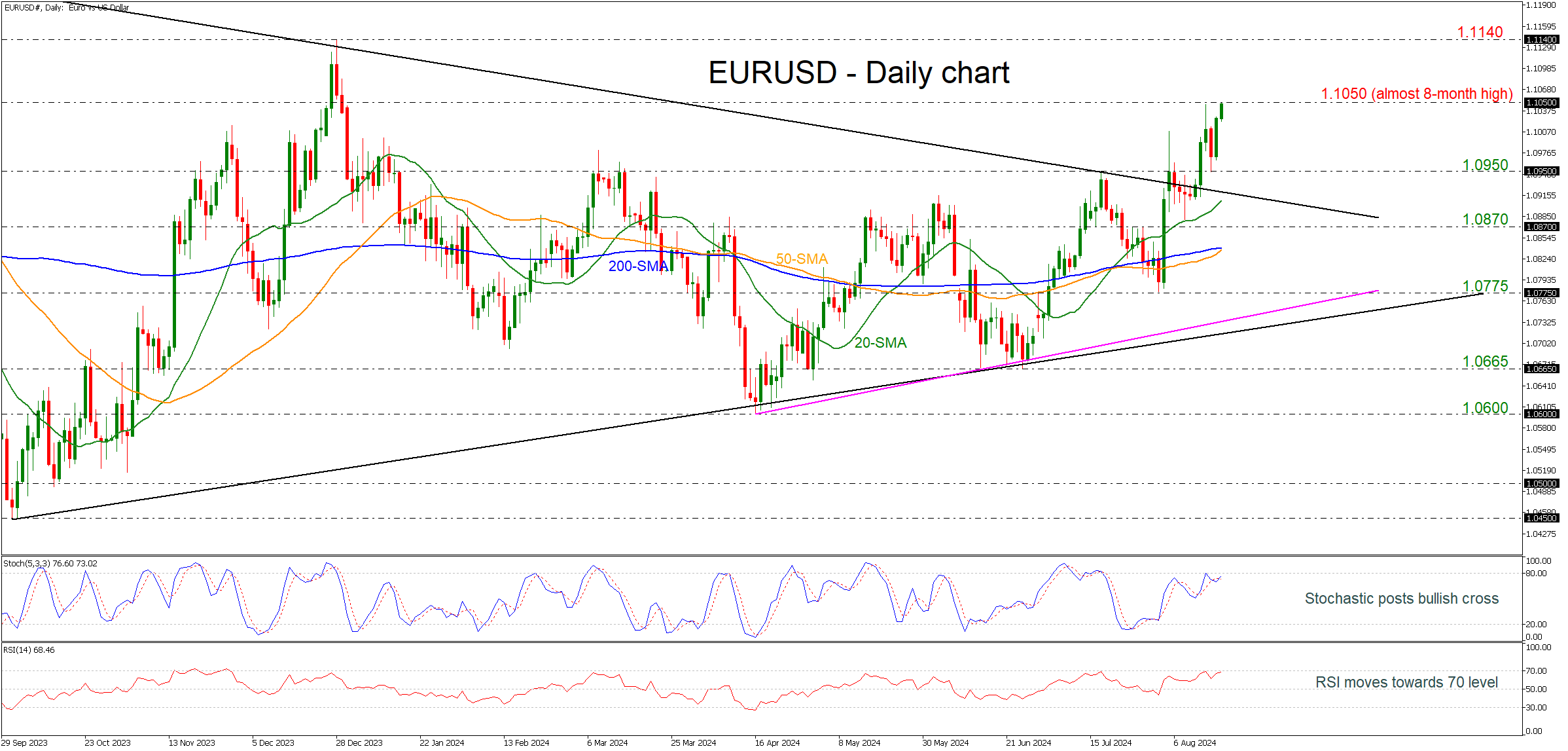

EURUSD Tests 1.1050 Tricky Area

- EURUSD flirts with 8-month high again

- Remains well above the long-term symmetrical triangle

- 50- and 200-day SMAs ready for bullish cross

- Momentum oscillators confirm upside move

EURUSD has been in a bullish move, especially after the rally above the long-term symmetrical triangle last week. The pair is again battling with the almost eight-month high of 1.1050, with the simple moving averages (SMAs) mirroring the current upside movement as they are all ticking higher. Additionally, the 50-day SMA is ready to cross above the 200-day SMA.

According to technical oscillators, the %K and %D lines of the stochastic are posting a bullish crossover, while the RSI is flirting with the 70 level with strong momentum.

If the pair reactivates its uptrend above the previous top, the next target will be the 1.1140 resistance, taken from the peak in December 2023. Even higher, the bulls might head for the 1.1275 number, which was a key resistance area during the second half of 2023.

On the downside, the 1.0950 support has been guarding selling forces over the past two days. Beneath that line, the 20-day SMA around 1.0900 might produce fresh negative volatility, likely squeezing the price towards the 1.0870 barricade. Another defeat there could add more fuel to the bearish wave, bringing the 200-day SMA at 1.0840 immediately under the spotlight.

Overall, EURUSD is sustaining an upward trend as long as it stands above the previous sideways pattern and the 1.1000 psychological mark. To attract new buyers, the pair will need to pierce through the 1.1050 bar.

Attention Shifts to Fed’s Jackson Hole Symposium

Markets

Last week’s US eco data failed to settle the debate on the outcome of the September FOMC meeting. Money markets initially added to 50 bps rate cut bets on slightly below consensus PPI numbers, but later on retraced somewhat after CPI showed continuing disinflation though in line with forecasts. Survey data (Empire Manufacturing), activity figures (retail sales) and labour market data (jobless claims) all helped putting the early August recession scare to bed. Weak US housing data were the odd one out. Attention shifts to the Fed’s Jackson Hole symposium later this week with a keynote speech by Fed Chair Powell on the economic outlook on Friday (4pm CET). In line with guidance at the July meeting, we think he’ll confirm the likelihood of a September policy rate cut. However, we don’t expect him to echo the market drum of kicking things off with a 50 bps move. SF Fed Daly over the weekend also hailed gradualism as the way to approach the cutting cycle with more signs of inflation being under control and the labour market slowing. She stressed that slowing isn’t the same as being weak. Powell won’t formally close the door on 50 bps neither though with plenty of data (ISM’s, payrolls, CPI) still to be released ahead of the September 18 FOMC meeting. Such scenario will keep the dollar in the defensive while preventing a significant return higher in US bond yields. EUR/USD last week moved above the psychologic 1.10 barrier with the December 2023 top at 1.1139 being the next target. General dollar weakness pulls the trade-weighted greenback to 102 for the first time since early January this morning with USD/JPY losing over two big figures at 145.30. It could add to the bullish comeback of (US) stock markets. The S&P 500 and Nasdaq already completely erased the early August market meltdown. Other things to match this week are, the preliminary benchmark revision to Establishment Survey Data (payrolls, risks to significant downward adjustments to past months data), Minutes of the July Fed meeting (both on Wednesday) ECB Q2 wage data and global PMI’s (both on Thursday), Jackson Hole comments in general (Friday) and the Democratic national convention.

News & Views

Rating agency Fitch confirmed Belgium’s AA- credit rating last Friday, but the outlook remains negative. Strong fundamentals are counterbalanced by fiscal challenge. A very high and rising level of public indebtedness and a political and institutional context complicate fiscal adjustment efforts. The negative outlook reflects insufficient fiscal consolidation to achieve debt stabilization in the medium term. Fitch indicates that rising aging costs, high inflation indexation of expenditure and rising debt service costs make a difficult environment for fiscal consolidation. In its baseline scenario, Fitch expects the fiscal deficit to reach 4.5% in 2026 compared to 4.4% in 2023. The no-policy change scenario of the National bank of Belgium expects a 5.5% deficit in 2026. Fitch in its assessment incorporates modest consolidation efforts from the new government but still sees the debt ratio stuck on an upward trajectory, reaching 109.3% in 2026, from 105.2% in 2023. With respect to economic growth, the rating agency plots GDP growth moderating to 1.1% this year and to stay below the country’s potential (1.2%) at 0.9% in 2025 and 1% in 2026. Inflation is expected to average 4.3% this year as the government is rolling back energy support measures, but is seen falling back to 2.8% and 1.6% in 2025 and 2026.

British property website Rightmove states that UK property prices declined 1.5% M/M in August to be 0.8% higher compared to the same month last year (from -0.4% M/M and + 0.4% Y/Y in July). Even so, Rightmove indicated that buyer inquiries in August were 19% higher compared to a year ago (from a 11% Y/Y rise in July). In its assessment, Rightmove director Tim Bannister indicated that "While mortgage rates aren't yet substantially lower since the rate cut, the fact that the long-hoped-for first cut has finally arrived, and mortgage rates are heading downwards, is positive for home-mover sentiment".

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June. Stubborn inflation (core, services) make follow-up moves less evident. Markets nevertheless price in two to three more cuts for 2024 as disappointing US and unconvincing EMU activity data rolled in, dragging the long end of the curve down. The move accelerated during the early August market meltdown.

US 10y yield

The Fed in its July meeting paved the way for a first cut in September. It turned attentive to risks to the both sides of its dual mandate as the economy is continuing to move better in to balance. Money markets tend to err in favour of a 50 bps lift-off. The pivot weakened the technical picture in US yields with another batch of weak eco data pushing the 10-yr sub 4%.

EUR/USD

EUR/USD moved above the 1.09 resistance area as the dollar lost interest rate support at stealth pace. US recession risks and bets on fast and large (50 bps) rate cuts trumped traditional safe haven flows into USD. EUR/USD 1.1139 (Dec 2023 high) serves as next technical reference.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually 0on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. Risk-off proved a more important driver of GBP recently, triggering a return from 0.84 towards 0.86.

USD Extends Losses, Yen Gains

The week starts on a mixed note in Asia, after major US indices recorded their best week since last October and boosted appetite in global risk markets. A softer-than-expected CPI read in the US combined with robust retail sales and weekly jobless claims data boosted the expectation that the Fed could eventually achieve a soft landing. Goldman Sachs cut its recession forecast from 25% to 20%. The return of the carry positions in the yen last week also helped boosting appetite in the riskier pockets of the market. As a result, the S&P500 rallied almost 4% last week and is up by more than 8% since the dip we saw at the beginning of the month, Nasdaq 100 rallied more than 5% last week and is up by almost 12% since the August dip, the Dow Jones gained almost 3% last week and 6% since the August dip and the Russell 2000 recovered nearly 3% as well last week and has rebounded by more than 7% since its dip earlier this month. The Stoxx 600 recovered more than 6% since the August dip and the Japanese Nikkei soared almost 22%. In summary, it looks like the mini panic of the beginning of the month has well reversed. The VIX index is back to the pre-panic levels.

What’s next?

The US dollar starts the week downbeat. We don’t have a busy economic calendar this week, but the central bank policies and rate discussions will be on the menu of the week as the annual Jackson Hole meeting will begin on Thursday, Federal Reserve (Fed) Chair Jerome Powell will speak on Friday, and many other central bankers will speak at the event. Although Jackson Hole witnessed important policy pivots in the past and is a place where important twists and tweaks could happen, there is little potential for further dovishness regarding the Fed policy when Powell speaks later this week. There is nothing out there – at least in the data that’s available to us – that suggests that the Fed should announce a jumbo rate cut at the September meeting. We will be looking for a hint of what will happen after the September rate cut.

Price-wise, the US dollar is softer on Monday, the dollar index is testing the August support at the time of writing. The market pricing remains more dovish than what the Fed is set to deliver at the September meeting (with around 30% probability given to a 50bp cut), and also more dovish than what the Fed could deliver for the rest of the year. Therefore a USD rebound is plausible. The EURUSD which pushes higher above the 1.10 level and Cable that is preparing to re-test the 1.30 should have a limited upside potential.

The Japanese yen, on the other hand, is better bid this morning. The USDJPY fell to 146 after the failure to clear the 150 offers last week. The Bank of Japan (BoJ) Governor Ueda will attend a special session in the Japanese parliament this week and will keep an accommodative tone. But the net speculative yen positions turned positive for the first time since March 2021 and big players are increasing bets that the BoJ will continue hiking the rates despite the sharp market reaction. The 150 level could act as a decent resistance to the USDJPY and keep the yen upbeat despite a cautious BoJ.

Elsewhere, the Fed rate cut bets sent gold to a fresh record last week, the yellow metal traded at $2500 per ounce, while oil hardly got a sentiment boost from improved market mood. The non-escalation of tensions in the Middle East and the sluggish Chinese data keep oil in the hands of the bears. US crude is trading near $76pb this morning, while Brent crude kicks off the week below $80pb mark.

Markets Await Powell’s Jackson Hole Speech Later This Week

In focus today

This week starts rather quietly on the data release front. The only event in our calendar is Fed's Waller (voting member) speaking this afternoon.

The Democratic National Convention kicks off today, and Kamala Harris is expected to be elected as the democratic presidential candidate later in the week.

Early Tuesday, China will announce Loan Prime Rates which is part of the policy tool kit. However, since they cut rates last month, we expect rates to stay unchanged for now. However, more easing is expected later in Q3 as the economy is struggling and PBOC has been awaiting that the Fed would start easing before cutting rates (to avoid downward pressure on the renminbi).

Tuesday, we look out for the Riksbank rate decision, where we expect the central bank to deliver its second rate cut in 2024. On Wednesday, minutes of the Fed's July meeting will be published. On Thursday, August flash PMIs are due for release from the euro area, US and UK. On Friday, markets will pay attention to Fed chair Powell's speech at the annual Jackson Hole Economic Policy Symposium. Early on Friday, we will receive Japanese inflation data.

Economic and market news

What happened over night

In the US, Fed's Daly (voting member) said that recent economic data has given her more confidence that inflation is under control, and that it is time to adjust interest rates from the current level. However, she mentioned that she would back a gradual decline, which sounds more like a 25bp rate cut, rather than a 50bp rate cut. Markets are sure that a rate cut will come in September, the only question is if it will be a 25bp or 50bp rate cut. We maintain our expectations for a 25bp rate cut.

At the end of last week Fed's Goolsbee (voting member) spoke about monetary policy and said that "You don't want to tighten any longer than you have to," and "..the reason you'd want to tighten is if you're afraid the economy is overheating, and this is not what an overheating economy looks like to me." Goolsbee did not say if he would push for a rate cut at the September meeting.

What happened on Friday

In the US, consumer sentiment came in slightly higher than expected in August. This speaks into the shift in the narrative about the US economy from last week, with inflation pressures easing, while consumer spending is holding up, compared to early August after the weaker-than-expected jobs report.

Market movements

Equities: Global equities were higher on Friday and have risen for the seventh consecutive day. It is tempting to declare the full-blown equity recovery as complete. The MSCI World Index is nearly back to its peak levels from mid-July, and the VIX has dropped below 15. As previously mentioned, the speed and continuity of this recovery have been surprising for us. The next steps should be much tougher for equities, as an improved growth outlook will be required to push indexes higher from here. In the US on Friday, Dow +0.2%, S&P 500 +0.2%, Nasdaq +0.2%, and Russell 2000 +0.3%. Asian markets are mixed this morning, while both European and US futures are showing gains.

FI: We could be in for a new test of 3.8% level in 10Y US Treasuries as well as the 4% level in the 2Y Treasuries if the PMI data released this week confirms the slowdown and we have dovish comments from the Federal Reserv'’s Jackson Hole conference this week.

FX: The USD faced broad weakness against G10 currencies on Friday, with the NZD emerging as the top performer. Safe-haven currencies, JPY and CHF also strengthened. EUR/USD rose above the 1.10 mark.

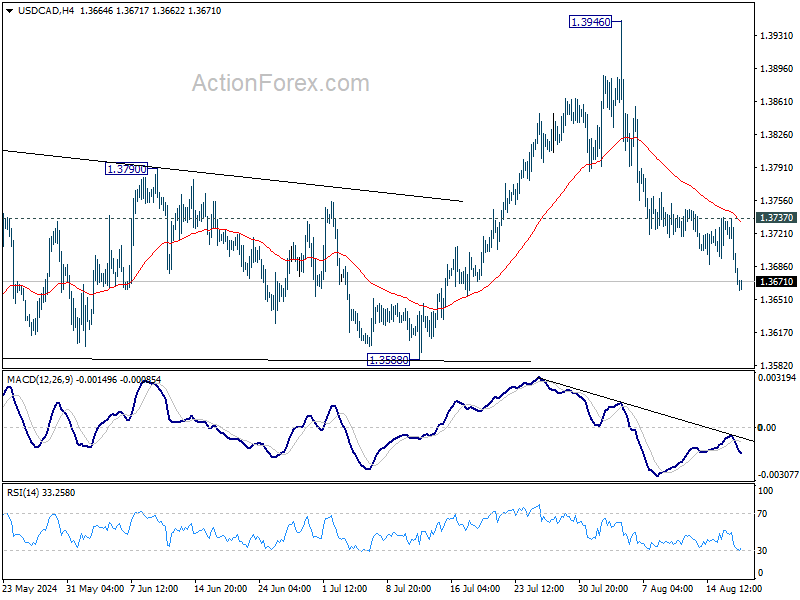

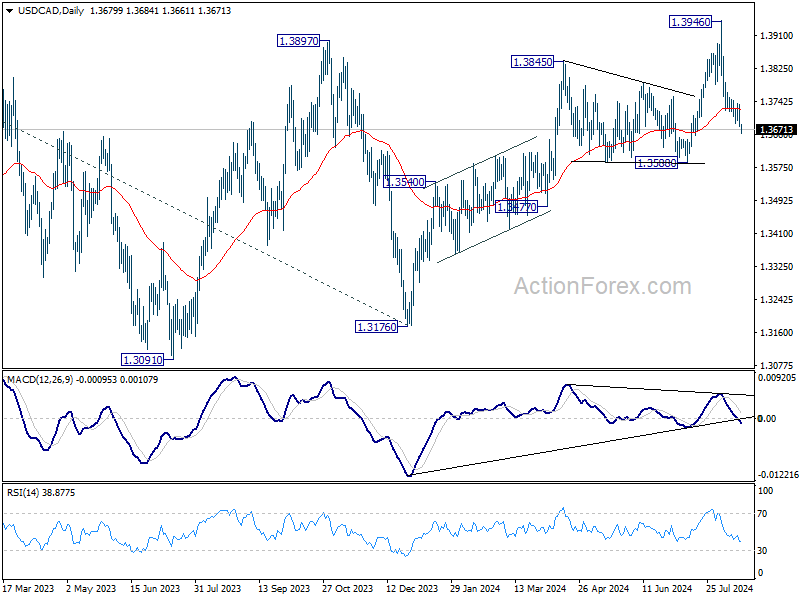

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3658; (P) 1.3698; (R1) 1.3717; More...

USD/CAD's decline from 1.3946 continues today and intraday bias stays on the downside for 1.3588 support. On the upside, above 1.3737 minor resistance will turn intraday bias back to the upside for stronger recovery.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern, that might have completed at 1.3176 (2023 low) already. Firm break of 1.3976 will confirm resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149. This will be the favored case as long as 1.3588 support holds, in case of pullback.

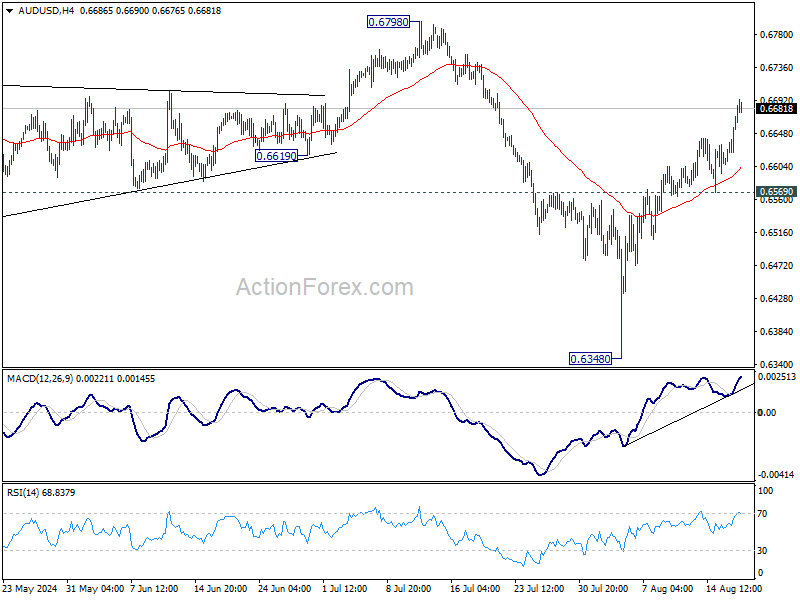

AUD/USD Daily Report

Daily Pivots: (S1) 0.6628; (P) 0.6650; (R1) 0.6691; More...

Intraday bias in AUD/USD remains on the upside as rise from 0.6348 is in progress. Further rally would be seen to retest 0.6798 resistance next. On the downside, below 0.6569 minor support will turn bias to the downside for retreat.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern. Rise from 0.6340 is likely developing into another rising leg. Firm break of 0.6798/6870 resistance zone will target 0.7156 resistance. In case of another fall, strong support should be seen from 0.6169/6361 to bring rebound.

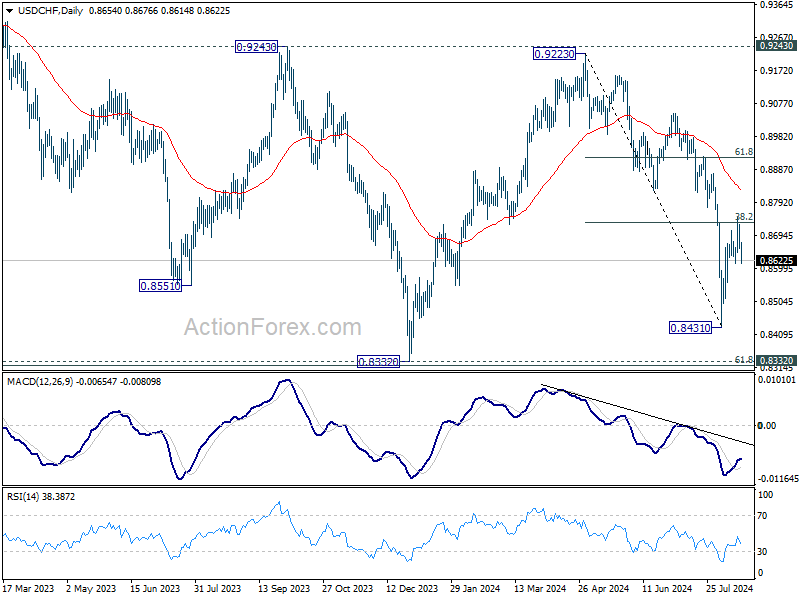

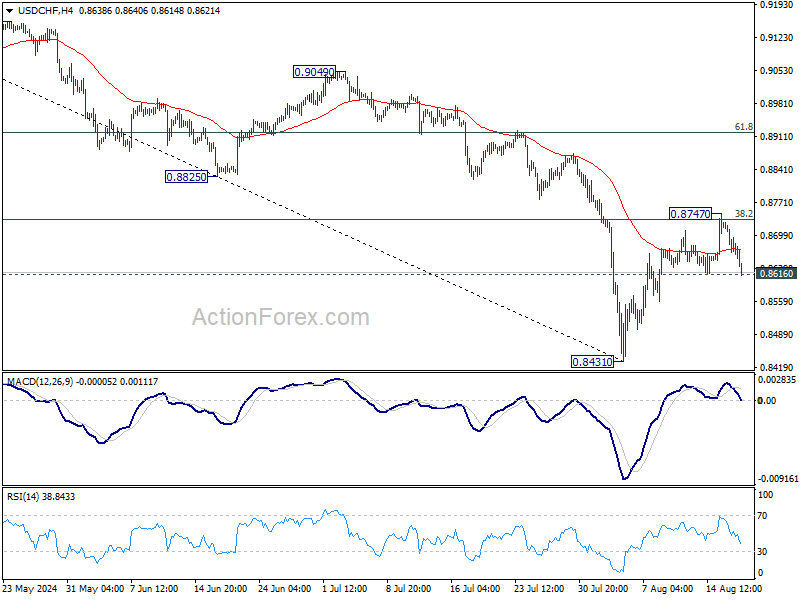

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8636; (P) 0.8685; (R1) 0.8710; More…..

Intraday bias in USD/CHF remains neutral for the moment. On the downside, break of 0.8616 support will indicate rejection by 38.2% retracement of 0.9223 to 0.8431 at 0.8734, and turn bias back to the downside for retesting 0.8431 low. On the upside, sustained break of 0.8734 will extend the rebound from 0.8431 to 61.8% retracement at 0.8920, even as a corrective move.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).