Sample Category Title

New Zealand’s goods export rises 14% yoy in Jul, imports up 8.5% yoy

New Zealand's goods exports saw a robust increase of 14% yoy in July, reaching NZD 6.1B. Goods imports also rose by 8.5% yoy to NZD 7.1B, leading to a trade deficit of NZD -963m, a stark contrast to the expected surplus of NZD 331m.

Breaking down the export data, the strongest growth came from Australia, with total exports up by 19% (NZD 135m), followed by the EU, where exports surged by 30% (NZD 114m). Exports to China increased by 8.5% (NZD 107m), while exports to the US and Japan rose by 4.7% (NZD 35m) and 5.3% (NZD 17m), respectively.

On the import side, the largest increase was from South Korea, where imports more than doubled, rising by 103% (NZD 480m). Imports from China also saw significant growth, up 18% (NZD 233m). In contrast, imports from the US and the EU declined sharply, with drops of -30% (NZD -255m) and -14% (NZD -147m), respectively. Imports from Australia showed a modest increase of 0.82% (NZD 6.3m).

ECB’s Rehn flags September rate cut amid growing growth risks

ECB Governing Council member Olli Rehn highlighted growing concerns about Eurozone's economic outlook, stating that the "recent increase in negative growth risks" has strengthened the case for a rate cut at the next monetary policy meeting in September, assuming disinflation remains on course.

Rehn acknowledged that while inflation is expected to continue its path towards the 2% target, the journey is likely to be "bumpy" throughout the year. The real challenge, however, lies in the growth outlook.

He pointed out that there are still "no clear signs of a pick-up in the manufacturing sector," despite the fading impact of high energy costs that had previously weighed on the sector.

Rehn further cautioned that if investments in the manufacturing sector fail to recover and growth continues to rely heavily on the services sector, the "projected pick-up in productivity growth may be jeopardized."

He also warned that the slowdown in industrial production "may not be as temporary as assumed," suggesting that Eurozone could face prolonged economic challenges if the manufacturing sector does not regain momentum.

BTCUSD Completes Death Cross

- BTCUSD trades sideways in the past few sessions

- Sentiment deteriorates after multiple rejections at 50-day SMA

- Momentum indicators are skewed to the downside

BTCUSD (Bitcoin) has been losing ground in August, experiencing a strong selloff on the back of a downbeat July NFP report. In contrast to stocks, Bitcoin has failed to recover notable ground as the 50-day simple moving average (SMA) has repeatedly repelled any upside attempts.

Should the recent rangebound movement break to the downside, immediate support could be found at the April bottom of 56,483. A violation of that territory could pave the way for the July low of 53,250. Even lower, the six-month low of 49,450, registered in August, could provide downside protection.

On the flipside, bullish actions could send the price to test the recent rejection region of 61,850, which lies very close to the 50-day SMA. If that barricade fails, there is no prominent resistance until the April hurdle of 67,270. Further advances could then cease around the July peak of 70,015.

In brief, BTCUSD has been trading sideways in the past few sessions, but the death cross between 50- and 200-day SMAs has further deteriorated the already bearish short-term picture. For that to alter, the price needs to jump back above its 200-day SMA.

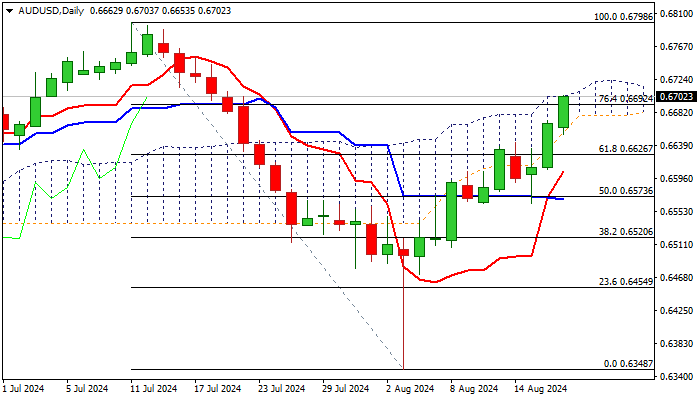

AUD/USD Outlook: Continues to Trend Higher Ahead of FOMC Minutes, Powell’s Speech in Jackson Hole

AUDUSD rose to the highest levels in almost one month on Monday, in extension of almost 0.9% daily advance on Friday and 1.5% gains last week

The pair enters the third consecutive week of strong gains, with the latest acceleration being boosted by revived risk appetite and hopes of September Fed rate cut (with renewed talks about 50 basis points cut).

Investors still need more evidence and await release of FOMC July meeting minutes and more significant speech of Fed Chair Powell in Jackson Hole symposium, which will shed more light on Fed’s next steps.

Widely expected dovish stance of the US central bank will further deflate the US dollar, though disappointing comments from Powell cannot be ruled out, and dollar would receive fresh support in such scenario.

Monday’s rally broke above Fibo barrier at 0.6692 (76.4% of 0.6798/0.6348 downtrend) and cracked pivotal resistance at 0.6701 (daily cloud top).

Firm break here to open way for push towards target at 0.6798 (2024 high, posted on July 11).

However, overbought daily studies may slow bulls, with limited dips (ideally to be contained by 55DMA at 0.6638) to provide better buying opportunities.

Res: 0.6714; 0.6750; 0.6798; 0.6839.

Sup: 0.6653; 0.6638; 0.6600; 0.6570.

Sunset Market Commentary

Markets

Markets took a slow start to the new trading week which looks more enticing later on. In the absence of high profile headlines today, softer yields and a weaker dollar initially proved the to be the path of least resistance, even as the momentum of this trade eased as US traders joined. German/EMU yields reversed small declines to currently trade up to 1.5 bps higher. US yields show a similar picture. Still, any sustained rebound in yields looks difficult for now. US inflation, while still well above the 2% target, has softened enough for the Fed to give more weight to growing signs of a cooling of activity and, in particular, a slowdown in job creation. Last week’s US data (retail sales) suggest that the US economy is heading for a soft landing, rather than an outright recession. Still markets see room for the Fed to ‘substantially’ scale back policy tightening in order to prevent an unnecessary slowdown in activity/rise in unemployment. This week, the (US) PMI’s, comments at the Fed Jackson Hole symposium, the minutes of the July Fed meeting and the annual revision of the BLS’ US payrolls data might help markets to make up their mind on the pace of Fed easing. The debate remains open (and that probably remains the case after Jackson Hole), but markets continue to err on the side of the Fed being behind the curve. Fear for a sharp US downturn triggered a wild risk-off correction early August, but stocks in the meantime rebounded on the hope of easier (global) financial conditions. However, with especially US markets having reversed course, the risk rebound is shifting into a lower gear. Europe now outperforms the US (Eurostoxx 50 + 0.5%, S&P 500 +0.1%). Oil (Brent $79.2/b) still struggles to hold the $80/b reference despite ongoing geopolitical tensions in the Middle East region as uncertainty on global demand lingers.

Anticipation of easier financial conditions keep the dollar in the defensive. USD/JPY this morning tested the 145.20 area (compared to a 147.63 close on Friday) but the USD selling gradually eased intraday (146.15 currently). EUR/USD (1.1035) regained the 1.10 barrier. The EMU eco picture remains uninspiring, but high wage growth (Q2 ECB negotiated wages to be published on Thursday) might force the ECB to take a guarded approach on further easing. The December EUR/USD 1.1139 top is within reach with the 2023 top at 1.1276. Sterling initially tried to extend its post-CPI comeback from end last week, but EUR/GBP 0.85 support holds (currently 0.852).

News & Views

Bulgarian president Radev unexpectedly declined to approve a new interim cabinet, adding he will delay snap elections until after October 20. His decision deepens the political turmoil in the country, which will head to the ballot for the seventh time in less than four years. President Radev, whose powers have already been clipped by the government following several unilateral decisions to form governments over the past years, said that interior minister Stoyanov wouldn’t be able to guarantee fair elections if he continues in his role. The current political crisis delays Bulgarian efforts to join the euro. The middle of 2025 target date (already delay from 1/1/2025) is on a slippery slope. Apart from politics, the country has difficulties meeting the price stability criterion for joining EMU with average inflation rates well above the ECB’s June 2024 convergence report reference value (3.3%).

Rating agency Fitch this weekend confirmed the Czech Republic’s AA- rating with a stable outlook. It is underpinned by a record of credible macroeconomic and monetary policies, and a robust institutional framework. Fitch has revised down this year's real GDP growth forecast to 0.9%, from 1.2% expected in February, given the weak start to the year and subdued external demand, but puts forward an average 2.4% growth rate in 2025-2026. Headline inflation has been moving close to the central bank's target of 2% and is set to average 2.2% in 2024-2026, allowing the CNB to continue its easing cycle bringing the key rate at 3.75% by end-2024 (in line with our forecast) and 3.5% by end-2025. Fitch expects the budget deficit to narrow to 2.5% of GDP in 2024 and 2.2% in 2025 from 3.5% in 2023. The debt/GDP ratio is set to increase to 43.7% in 2025, from 42.4% in 2023 and to gradually decline to 42.9% in 2028 driven by the narrowing of primary budget deficits and recovering economic growth.

Graphs

DXY (trade-weighted USD index) testing 102 big figure as easing of global financial conditions continues to pressure the dollar

Brent oil struggles to hold the $80/b reference as uncertainty on global demand persists

Eurostoxx 50 reversing early month risk-off repositioning

EUR/SEK holding near 11.50 pivot as Riksbank is expected to further scale back policy restriction.

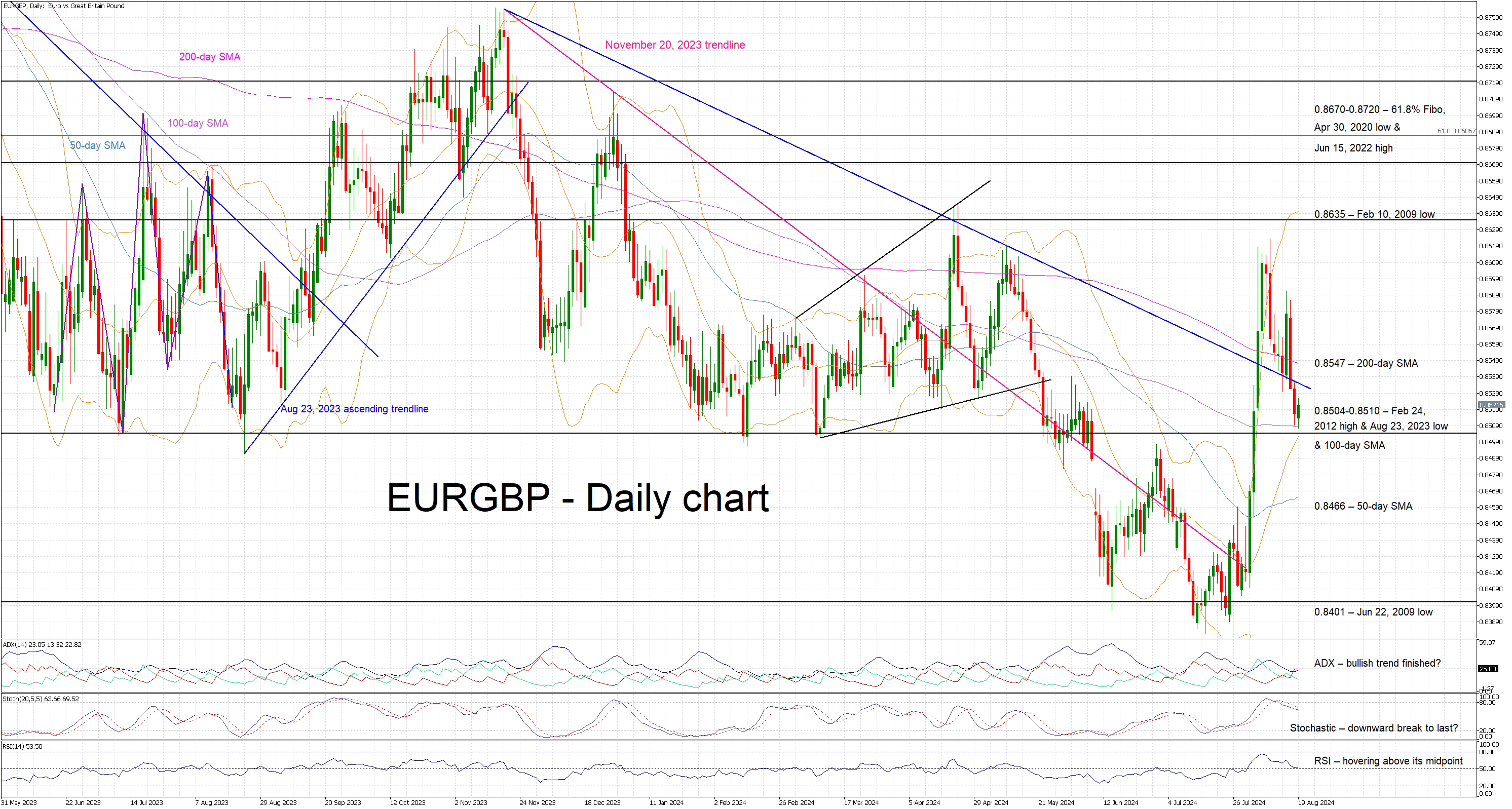

Could Eurozone PMI Surveys Cement September ECB Rate Cut?

- Markets are preparing for the Jackson Hole Symposium

- Eurozone data supports another ECB rate cut

- PMI surveys for the euro area will be published on Thursday

- Euro remains on the back foot against the pound

The Jackson Hole gathering to break the summer lull

Whilst ECB members are probably enjoying their hard-earned holiday break, the countdown to the Jackson Hole Symposium and the crucial September central banks’ meetings has already started. The RBNZ is the latest central bank to ease its monetary policy stance and, interestingly, the first one to openly talk about a recession in the latter part of the year.

Expectations of an imminent recession in the US were the main reason for the recent market rout that scared investors, ignoring the fact that the US data has been relatively satisfactory lately, as portrayed by our custom-made surprise indices. The same cannot be said for eurozone data and especially the German economic releases.

Euro area data remains mixed, rate cut expected

The preliminary GDP prints for the second quarter of 2024 created a sense of optimism in the hawks. Interestingly, the July CPI report for the euro area managed to surprise to the upside with the headline figure printing at 2.6% and the core indicator showing a 2.9% year-on-year increase. In addition, at the July ECB meeting, President Lagarde tried to dent expectations for another rate cut in September.

However, all these are probably not enough to change the current momentum in the ECB council with the market firmly confident that at least 65 bps of extra easing will be announced until year-end on the back of weak economic momentum and the Fed commencing its easing cycle in September.

For the ECB to disappoint the market, two conditions have to be met: (1) the Fed to avoid making a dovish shift at the Jackson Hole Symposium, thus falling shorting from pre-announcing the much talked about rate cut, and (2) the euro area data to show a miraculous improvement.

Euro area PMI surveys in the spotlight this week

Chances of these two events happening simultaneously are rather slim but a strong set of PMI survey prints this week could be a good start. Interestingly, the PMI surveys for the manufacturing and services sectors tell a different story for the eurozone.

The manufacturing PMI surveys for both Germany and France are stuck below 50 for a considerable amount of time. Both countries continue to suffer from the consequences of the Ukraine-Russia conflict, the associated competitiveness loss and the lower demand, both from China and domestically.

On the other hand, the PMI services surveys continue to hover above 50 and thus portray a sector in modest expansion. Services inflation has been a key discussion point in the last ECB meetings, appearing in the official ECB press statement, and thus being as the few reasons that inflation remains elevated.

The market is forecasting another mixed set of PMIs. The manufacturing surveys are expected to edge slightly higher, but remain in contractionary territory, while the PMI services figures could weaken a tad. Such an outcome is unlikely to affect the chances of another ECB rate cut in September.

Euro is losing ground against the pound

Following the late July BoE rate cut, euro/pound managed to rally considerably higher, negating most of the April-July 2024 downward move. However, mostly on the back of the overall negative outlook for the eurozone, the euro has been losing ground against the pound lately.

Market expectations for aggressive ECB easing are unlikely to be dented by a strong set of PMI surveys but the euro could benefit by climbing above the 200-day simple moving average at 0.8547. On the flip side, weak PMI survey figures are unlikely to prove significantly market-moving as the market is preparing for the all-important Jackson Hole Symposium.

News of the Week (August 19— August 23): GBPCAD Detailed Analysis

Keep your eyes on GBPCAD—new trading prospects are emerging!

The GBPCAD currency pair, representing the exchange rate between the British pound and the Canadian dollar, is the most critical indicator of economic interaction between the UK and Canada. The Canadian dollar is heavily influenced by fluctuations in commodity prices, particularly oil, due to Canada's status as a major exporter. Economic policy decisions and indicators such as employment levels, GDP growth, and trade balance are also important. On the other hand, the British Pound is influenced by factors such as changes in UK monetary policy, as well as economic reports such as inflation, employment, and consumer spending data.

Canada Consumer Price Index (CPI) MoM, Aug 20, 14:30 (GMT+2)

Canada's Consumer Price Index (CPI) is forecast to rise by 0.2%, recovering from a previous decline of -0.1%. If the CPI exceeds this forecast, indicating an increase in inflationary pressures, this could cause the Bank of Canada to consider tightening monetary policy. This would likely lead to a stronger Canadian Dollar and a decline in the GBPCAD pair. Conversely, the Canadian Dollar could weaken if the CPI exceeds the expected 0.2%, indicating less inflationary pressure than expected. This would potentially lead to a rise in the GBPCAD pair, reflecting lower confidence in the strength of the Canadian economy.

Last time on April 16, 2024, Canadian CPI came in below expectations, causing GBPCAD to surge!

UK Manufacturing Purchasing Managers Index (PMI), Aug 22, 10:30 (GMT+2)

The UK manufacturing PMI is forecast to decline slightly to 51.5 from 52.1. If the PMI beats expectations, demonstrating the resilience of the manufacturing sector, this could boost investor confidence in the UK economy and strengthen the Pound. A stronger Pound is likely to lead to a higher GBPCAD exchange rate. On the other hand, if the PMI falls short of expectations, indicating a weakening manufacturing sector, this could undermine confidence in the Pound. Such a scenario will likely lead to a fall in the GBPCAD pair, as the pound will lose ground.

In the Daily timeframe, GBPCAD, in a long-term uptrend, formed a rising channel pattern. The price bounced off the trend line and is consolidating near 161.8 Fibonacci, creating two possible scenarios.

- If the bulls push the price above 1.7630, the target will be 1.7820. However, if the price bounces off the resistance, it could fall to the trend line and then rally upwards;

- Otherwise, if GBPCAD breaks the trend line and falls below 1.7560, it will reach the support at 1.7450;

New Zealand Dollar Extends Gains as Services Index Rises

The New Zealand dollar wrapped up a fourth consecutive winning week and is in positive territory on Monday. NZD/USD is trading at 0.6076, up 0.37% in the European session at the time of writing.

New Zealand PSI pace of contraction eases

The New Zealand Performance of Services Index rose to 44.6 in July, up sharply from 40.7 in June. The index remained in contraction mode (below 50) for a fifth straight month and all industries reported contraction, which is a sign of concern. The services sector makes up about two-thirds of New Zealand’s GDP and the continuing contraction points to a weak economy.

The Reserve Bank of New Zealand delivered an initial rate cut last week and forecast that GDP will decline 0.5% in the second quarter and 0.2% in Q4.This would mark a technical recession, with two consecutive quarters of negative growth.

In the US, last week’s data was solid, as retail sales jumped 1% and inflation ticked lower 2.9%, down from 3%. On Friday, UoM consumer sentiment rose in July and beat expectation, while inflation expectations were unchanged at 2.9%, in line with expectations. The markets melted down after a weak US employment report earlier this month but strong US numbers last week led to improved risk appetite which has hurt the US dollar.

The markets expect a rate cut at the Federal Reserve’s next meeting on September 18, with a quarter-point cut being the most likely decision. On Friday, Minneapolis Fed President Neel Kashkari said that a rate cut discussion at the September meeting was “appropriate” as inflation had eased, but expressed concern about the deteriorating labor market.

.

NZD/USD Technical

- NZD/USD tested resistance earlier at 0.6080. Next, there is resistance at 0.6107

- 0.6030 and 0.6003 are providing support

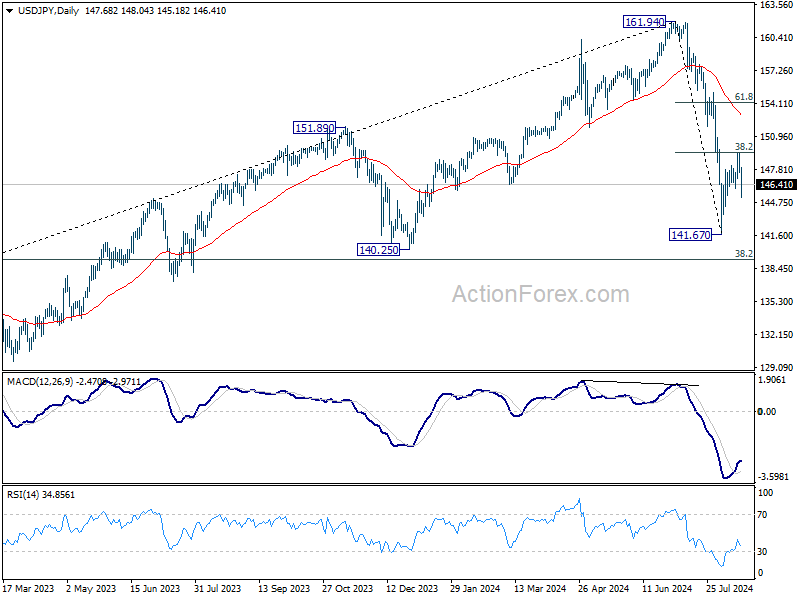

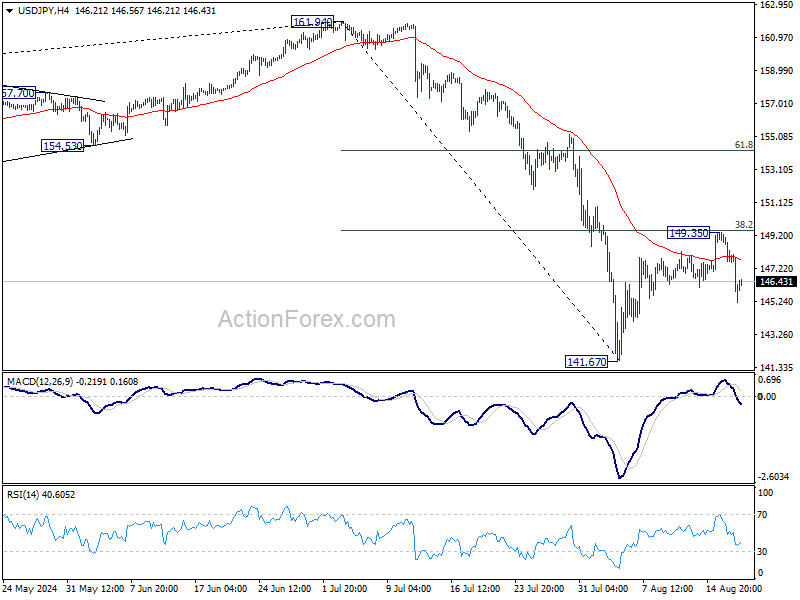

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.00; (P) 148.20; (R1) 148.83; More...

USD/JPY's rebound from 141.67 could have completed after rejection by 38.2% retracement of 161.94 to 141.67 at 149.41. Intraday bias remains on the downside for retesting 141.67 low. Firm break there will resume the whole fall from 161.94 to 139.26 fibonacci level next. For now, risk will stay on the downside as long as 149.35 resistance holds, in case of recovery.

In the bigger picture, fall from 161.94 medium term is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.63) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.