Sample Category Title

Rate Cut from Riksbank Should be a Done Deal

In focus today

In Sweden, the Riksbank's rate decision, a policy statement and a shorter policy report will be published at 09.30 CET. A press conference follows at 11.00 CET. There will be no new macro forecasts and no new rate path. A 25bp rate cut is - or should be - a done deal. Instead, market focus will be on communication. We expect that they will guide toward two more cuts this year, which is slightly more dovish than in June, though less dovish than market is pricing (three more cuts).

In the euro area, we will get final inflation figures for July. The final HICP data allow us to see how the important domestic inflation indicator ('LIMI') fared in May, see Research Euro Area - The importance of domestic inflation guiding ECB policies, 6 August. The preliminary figures showed that service price pressures eased to around 0.3% m/m, which is still too high, but lower than a couple of months ago.

In Denmark, we get national accounts data for Q2. We expect 1% GDP growth in Q2. GDP declined 1.4% q/q in Q1 on the back of a very strong fourth quarter in 2023. This leaves room for growth in Q2. For more details, see Danish section in Weekly Focus - From fear of inflation to fear of slowdown, 16 August.

In Turkey, the central bank will announce its rate decisions at 13.00 CET. The Central Bank of Turkey has concluded its hiking cycle and is expected to keep the policy rate unchanged at 50%. Since the July meeting, inflation has developed largely in line with their forecasts, as headline inflation in month-on-month terms increased temporarily in July, while the rise in underlying inflation was limited.

Fed's Bostic will be on the wire in the evening at 19.35 CET.

Economic and market news

What happened overnight

Peoples Bank of China (PBOC) left loan prime rates unchanged as expected in the market, after interest rates were lowered in July. More easing is expected later in Q3 as the economy is struggling and PBOC has been waiting for the Fed to start easing before cutting rates (to avoid downward pressure on the renminbi).

What happened yesterday

In the euro area, ECB's Rehn (voting member) spoke about monetary policy. He said that ECB may need to lower interest rates at the September meeting, due to negative growth risks arising, while inflation is on the right track in his eyes. Markets price in a 90% probability of a rate cut in September. We, however, still stick to our call of no cut in September.

Market movements

Equities: Global equities were higher yesterday, and this morning's post might start to sound like a broken record with the MSCI World Index gaining for its eighth consecutive day. Equities were up, volatility was lower (VIX below 15), and cyclicals outperformed defensives. As US stocks rallied into the cash close, all 25 industries finished higher on a day that saw virtually no headline news to drive the market. FOMO is back, and all the fear about a recession among equity investors seems to have gone. Please remember, this is typically how investor behaviour appears when we are very late in the cycle. In the US yesterday, Dow +0.6%, S&P 500 +0.97%, Nasdaq +1.4%, and Russell 2000 +1.2%. This morning, most Asian markets are higher, led by Japanese markets, which are up more than 2%, while Chinese stocks are moving in the opposite direction. Futures in Europe are mixed, while in the US, futures are marginally stronger.

FI: Markets waiting for the important ECB data and Jackson Hole speech later this week resulted in a tight trading range. Markets are also waiting for toda'’s supply with an expected 5y Finland deal and a 10y and long-end German bond tap. 10y Bunds ended virtually unchanged at 2.45%. Key events this week are the EA and US PMIs on Thursday, EA negotiated wage data on Thursday as well as Powel'’s speech in Jackson Hole on Friday. Lane speaks on Saturday.

FX: JPY was the top performer among G10 currencies yesterday, were the USD stay on a weak footing. EUR/SEK declined below 11.50 before the Riksbank rate decision today.

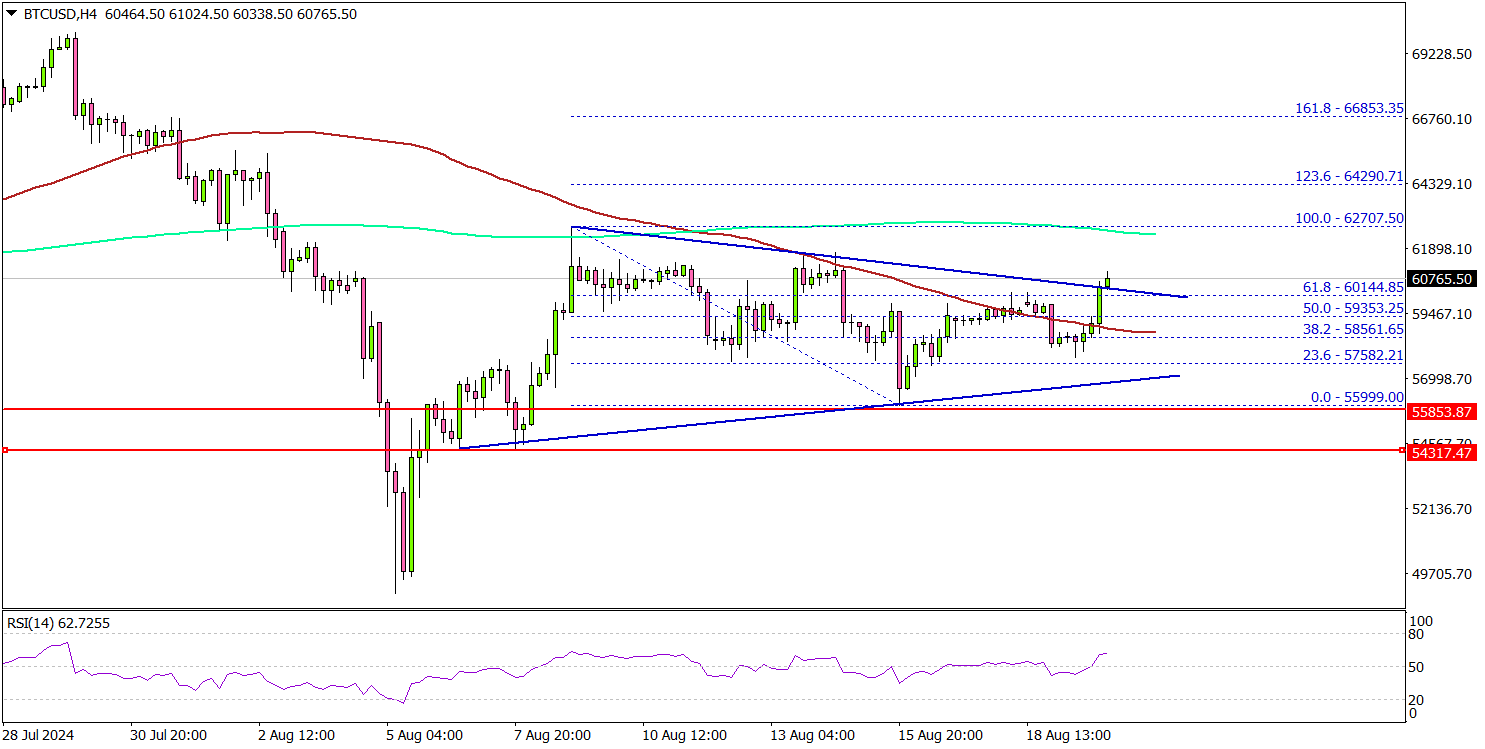

Bitcoin Price Breakout: Could It Lead To Bigger Gains?

Key Highlights

- Bitcoin price is aiming for a decent increase above the $60,000 resistance.

- BTC cleared a key contracting triangle with resistance at $60,800 on the 4-hour chart.

- Gold bulls pushed the price above the $2,500 resistance zone.

- GBP/USD is showing positive signs and aiming for a move above 1.3000.

Bitcoin Price Technical Analysis

Bitcoin price formed a base above the $56,000 level and started a fresh increase. BTC/USD climbed above the $58,000 resistance to start a decent increase.

Looking at the 4-hour chart, the price gained pace for a move above the 50% Fib retracement level of the downward move from the $62,707 swing high to the $55,999 low. It cleared a key contracting triangle with resistance at $60,800.

The price is now trading above the 61.8% Fib retracement level of the downward move from the $62,707 swing high to the $55,999 low, and the 100 simple moving average (red, 4 hours).

On the upside, the price might struggle to clear the $62,500 resistance and the 200 simple moving average (green, 4 hours). A successful close above $62,500 might start another steady increase. In the stated case, the price may perhaps rise toward the $65,000 level.

Immediate support is near the $59,500 level. The next key support sits at $58,500. A downside break below $58,500 might send Bitcoin toward the $55,000 support. Any more losses might send the price toward the $52,500 support zone.

Looking at gold, the price is rising and there could be more upsides above the $2,500 level in the near term.

Today’s Economic Releases

- US Goods and Services Trade Balance for June 2024 - Forecast $-72.4B, versus $-75.1B previous.

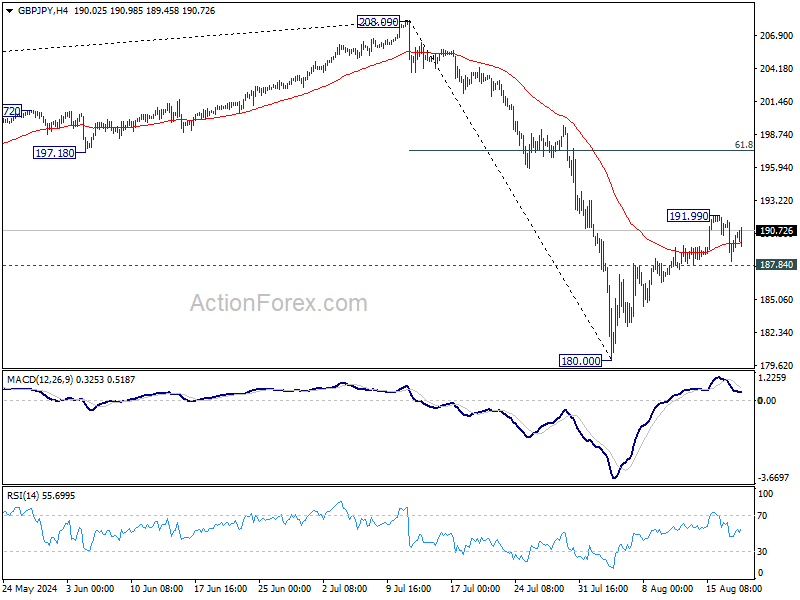

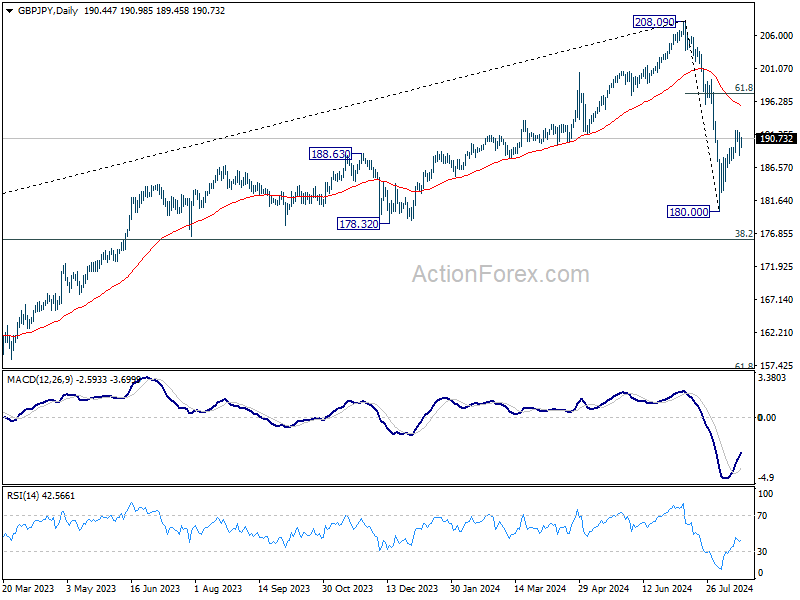

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.58; (P) 190.11; (R1) 191.97; More...

GBP/JPY is staying in range of 187.84/191.99 and intraday bias remains neutral first. On the upside, above 191.99 will target 61.8% retracement of 208.09 to 180.00 at 197.35, as the second leg of the corrective pattern from 208.09. On the downside, however, firm break of 187.84 support will turn bias back to the downside for retesting 180.00 instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). Current development suggests that the first leg has completed and the range of medium term consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09.

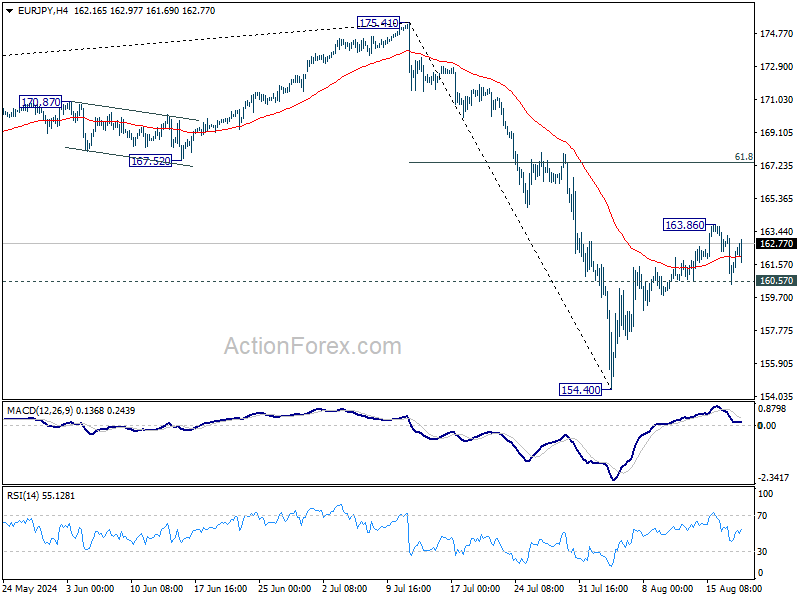

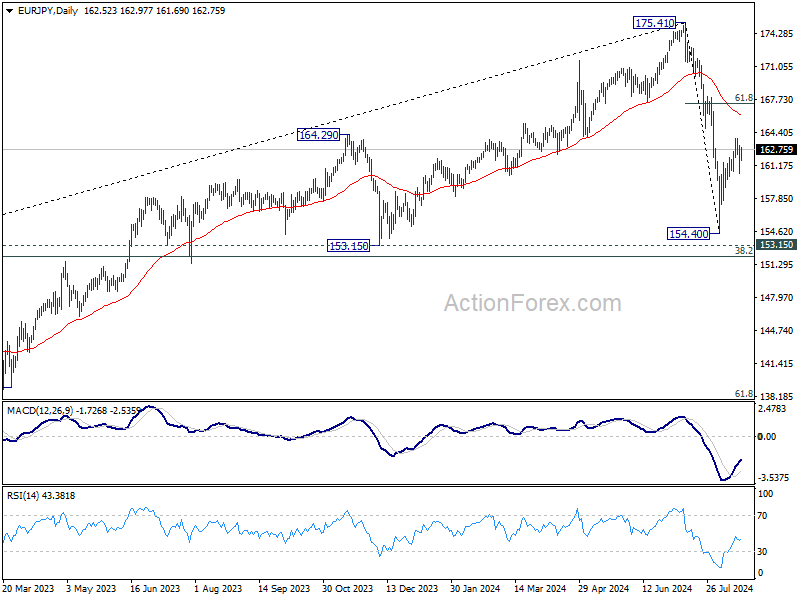

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.88; (P) 162.04; (R1) 163.67; More...

EUR/JPY recovered after drawing support from 160.57, but stays below 163.86 resistance. Intraday bias remains neutral at this point. On the upside, break of 163.86 will target 61.8% retracement of 175.41 to 154.40 at 167.38, as the second leg of the corrective pattern from 175.41. On the downside, however, firm break of 160.57 support will turn bias back to the downside for 154.40 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Current development suggests that the first leg has completed. The range of consolidation should be seen between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high.

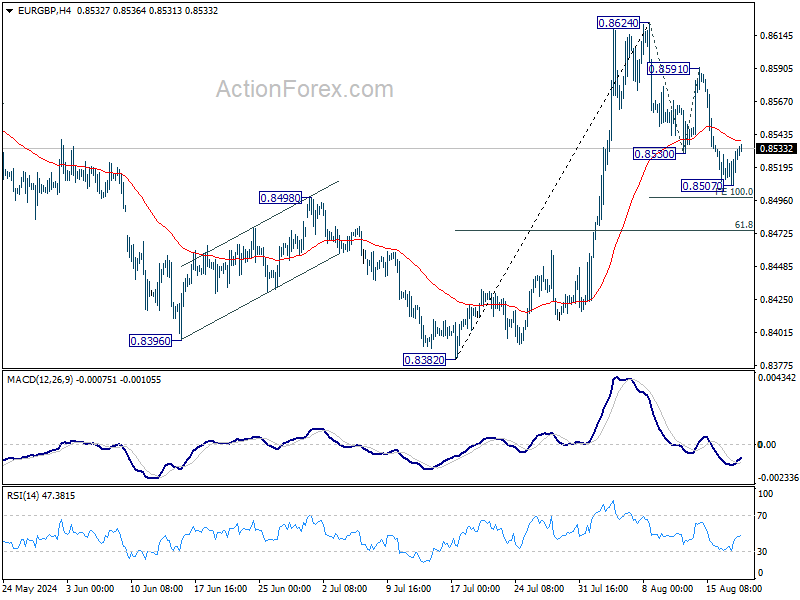

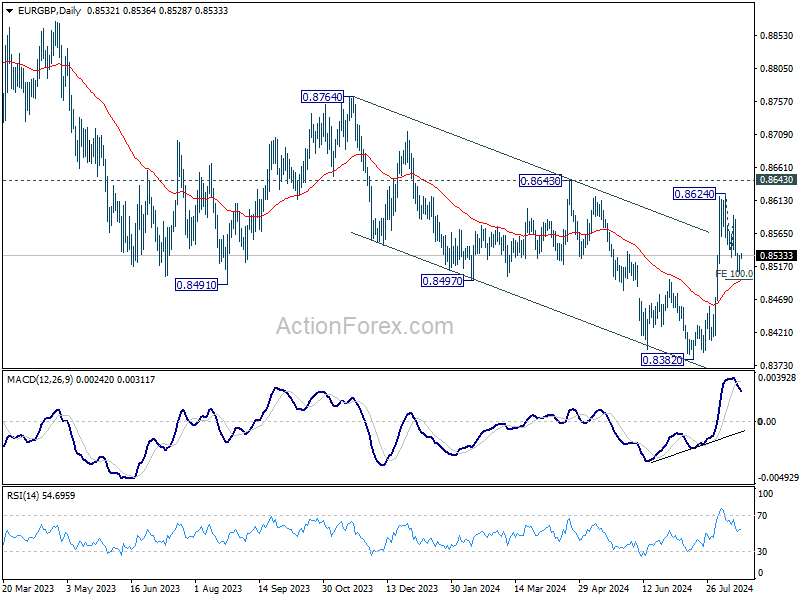

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8517; (P) 0.8525; (R1) 0.8542; More....

Intraday bias in EUR/GBP is turned neutral with current recovery. IN case of another fall, strong support should be seen from 100% projection of 0.8624 to 0.8530 from 0.8591 at 0.8497, which is close to 55 D EMA (now at 0.8494), to complete the correction from 0.8624. Break of 0.8591 resistance will argue that rise from 0.8382 is ready to resume through 0.8624.

In the bigger picture, while the rebound from 0.8382 is strong, there is no confirmation of trend reversal yet. As long as 0.8643 resistance holds, down trend from 0.9267 could still resume through 0.8382 at a later stage. However, firm break of 0.8643 will indicate that such down trend has completed, and turn outlook bullish for 0.8764 resistance next.

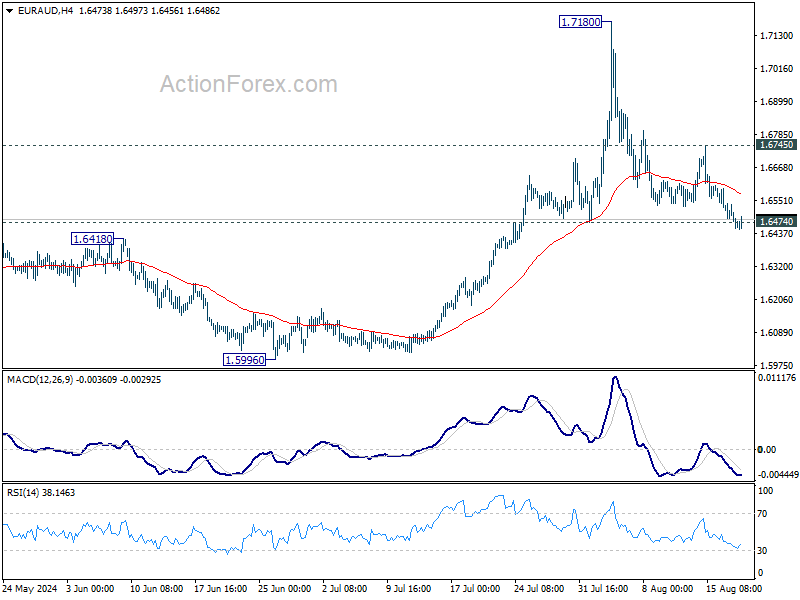

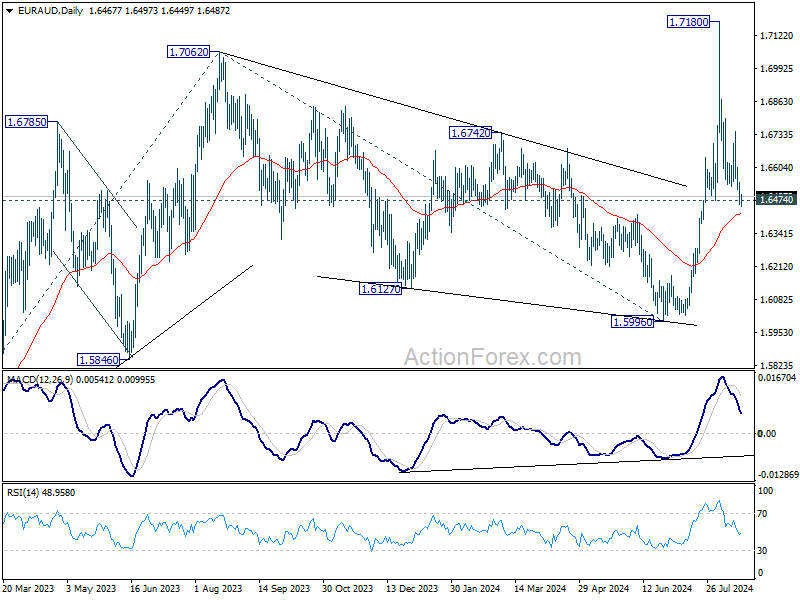

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6417; (P) 1.6506; (R1) 1.6555; More...

Immediate focus is now on 1.6474 support in EUR/AUD. Decisive break there will argue that rise from 1.5996 has completed, and dampen the larger bullish view. Intraday bias will be back on the downside for deeper fall towards 1.5996 in this case. Nevertheless, strong rebound from current level, followed by break of 1.6745 resistance, will retain near term bullishness and bring retest of 1.7180 high.

In the bigger picture, corrective fall from 1.7062 medium term top should have completed at 1.5996. Larger up trend from 1.4281 (2022 low) is resuming. Next target is 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715. This will now remain the favored case as long as 1.6474 support holds. However, decisive break of 1.6474 will argue that EUR/AUD Is still engaging in medium term range trading.

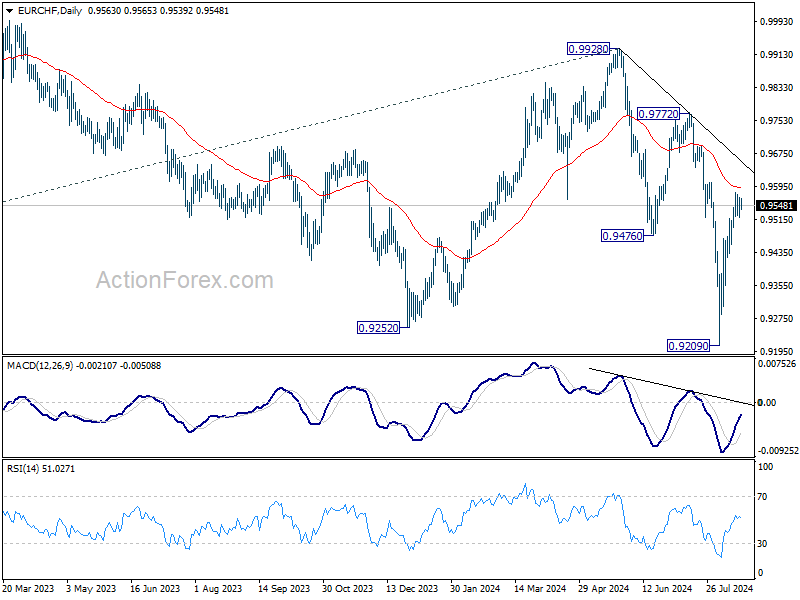

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9535; (P) 0.9552; (R1) 0.9582; More....

EUR/CHF is extending consolidations below 0.9579 temporary top and intraday bias remains neutral. Further rally is expected as long as 0.9448 support holds. Sustained break of 55 D EMA (now at 0.9589) will pave the way back to 0.9972/0.9928 resistance zone. However, decisive break of 0.9448 will suggest rejection by 55 D EMA, and turn bias back to the downside for 0.9209 low.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

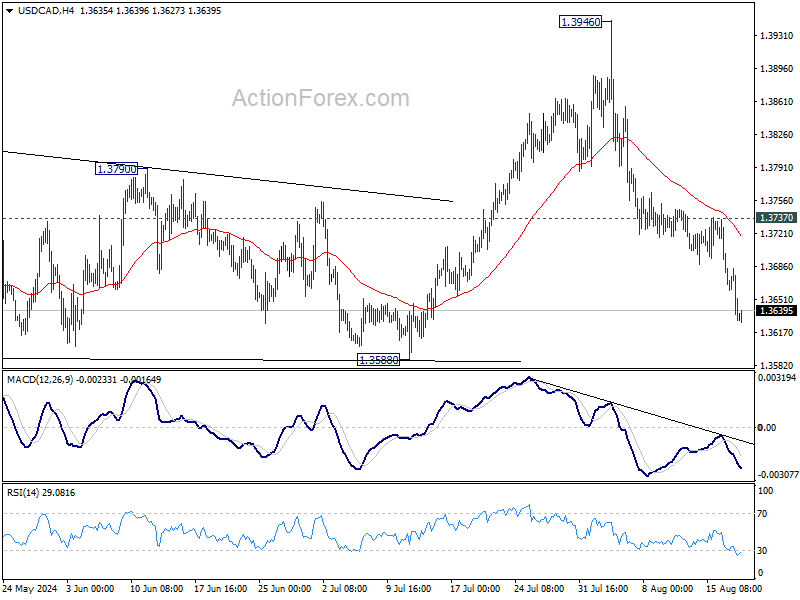

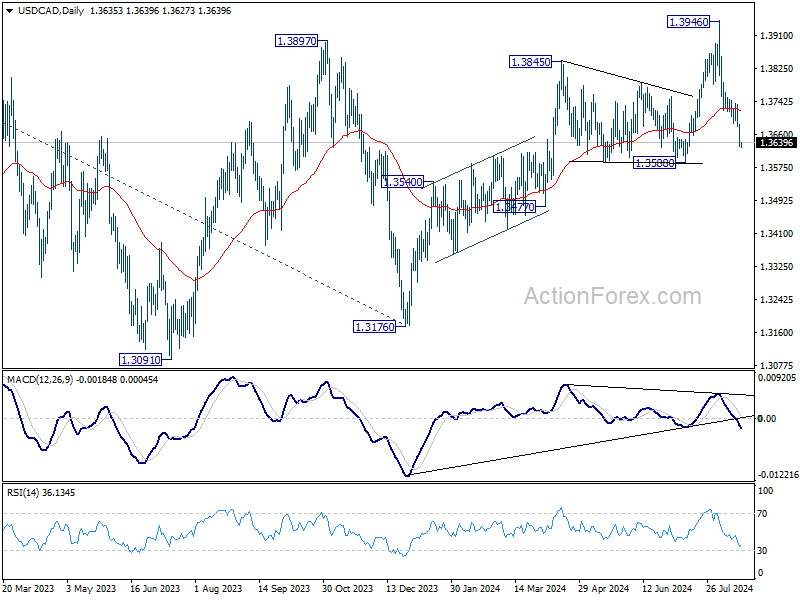

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3614; (P) 1.3650; (R1) 1.3670; More...

Intraday bias in USD/CAD remains on the downside as fall from 1.3946 is extending towards 1.3588 structural support. Strong support could be seen from there to bring reversal. However, for now, risk will stay on the downside as long as 1.3737 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern, that might have completed at 1.3176 (2023 low) already. Firm break of 1.3976 will confirm resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149. This will be the favored case as long as 1.3588 support holds, in case of pullback.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6677; (P) 0.6706; (R1) 0.6761; More...

AUD/USD's rally from 0.6348 is in progress and intraday bias stays on the upside for 0.6798 resistance. Firm break there will argue that larger rise from 0.6269 is ready to resume through 0.6870 resistance. On the downside, below 0.6676 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern. Rise from 0.6340 is likely developing into another rising leg. Firm break of 0.6798/6870 resistance zone will target 0.7156 resistance. In case of another fall, strong support should be seen from 0.6169/6361 to bring rebound.

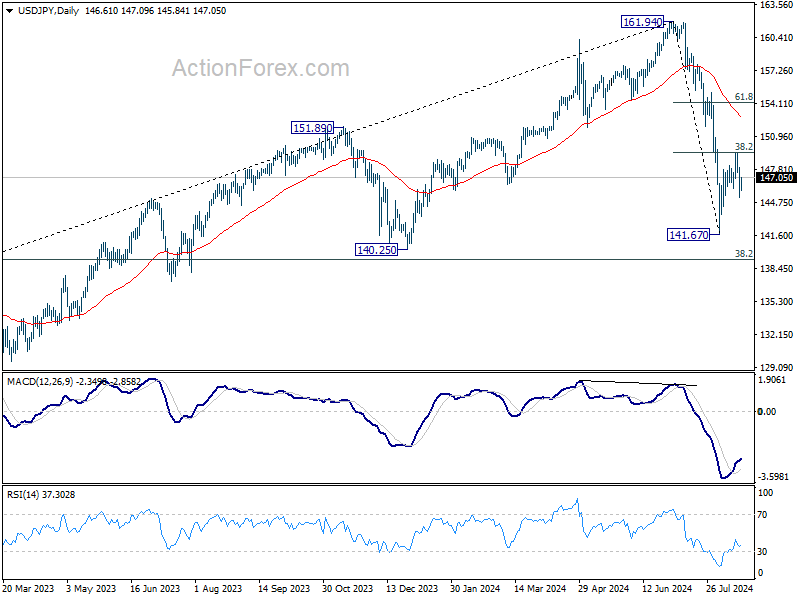

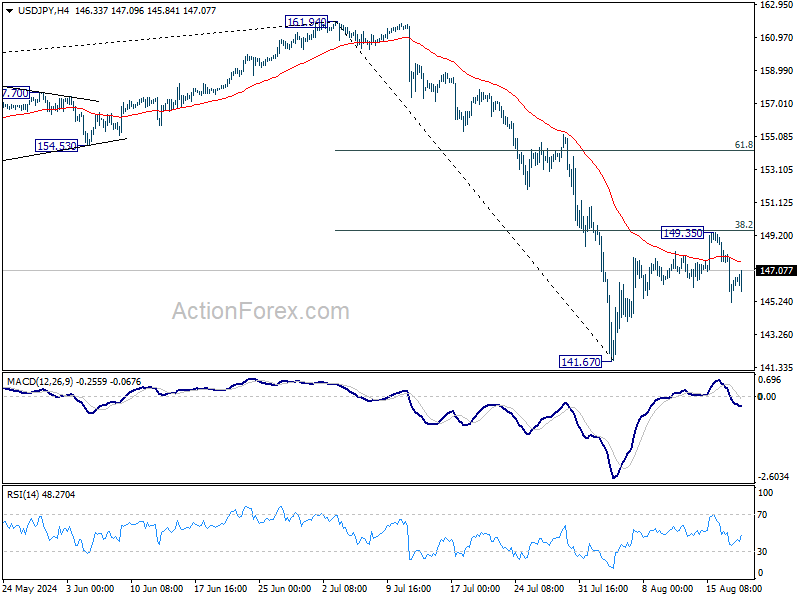

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.17; (P) 146.62; (R1) 148.04; More...

Intraday bias in USD/JPY remains mildly on the downside at this point. Rebound from 141.67 could have completed at 149.35 after rejection by 38.2% retracement of 161.94 to 141.67 at 149.41. Deeper fall would be seen to retest 141.67 low. Firm break there will resume the whole fall from 161.94 to 139.26 fibonacci level next. For now, risk will stay on the downside as long as 149.35 resistance holds, in case of recovery.

In the bigger picture, fall from 161.94 medium term is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.63) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.