Sample Category Title

German Gfk Consumer Confidence Sinks to Two-Year Low as Inflation and War Fears Hit Sentiment

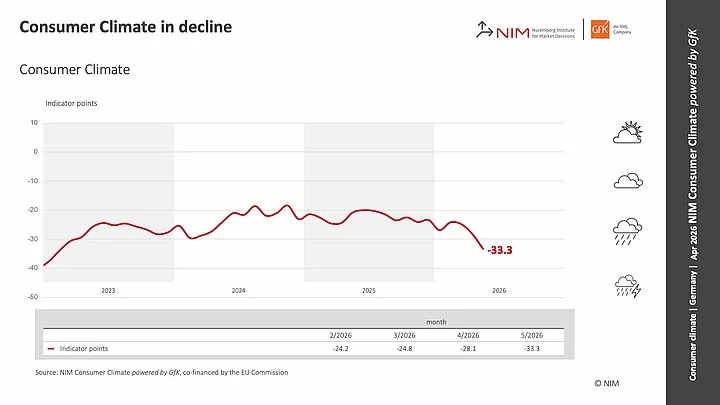

Germany’s GfK Consumer Climate for May fell sharply from -28.1 to -33.3, marking its lowest level since February 2023 and signaling further deterioration in household sentiment. The decline reflects mounting pressure on consumers as inflation expectations surge again, eroding purchasing power and confidence.

Underlying components point to broad-based weakness. Income expectations plunged from -6.3 to -24.4 in April, while willingness to buy slipped from -10.9 to -14.4. Although willingness to save eased slightly from 18.5 to 16.1, it remains elevated, suggesting households are still prioritizing precautionary behavior over consumption.

According to NIM’s Rolf Bürkl, income expectations are “literally collapsing” under the weight of rising inflation, leaving consumers increasingly reluctant to commit to major purchases.

The ongoing conflict involving Iran is weighing on economic expectations, with the outlook for Germany’s economy over the next 12 months deteriorating further from -6.9 to -13.7. The reading is now comparable to levels seen at the start of the Ukraine war in April 2022.

| Indicator | Previous | Latest | Change |

|---|---|---|---|

| GfK Consumer Climate (May) | -28.1 | -33.3 | ↓ -5.2 |

| Income Expectations (Apr) | -6.3 | -24.4 | ↓ -18.1 |

| Willingness to Buy (Apr) | -10.9 | -14.4 | ↓ -3.5 |

| Willingness to Save (Apr) | 18.5 | 16.1 | ↓ -2.4 |

| Economic Expectations (12m) | -6.9 | -13.7 | ↓ -6.8 |

USD/JPY Daily Outlook

Daily Pivots: (S1) 159.13; (P) 159.49; (R1) 159.73; More...

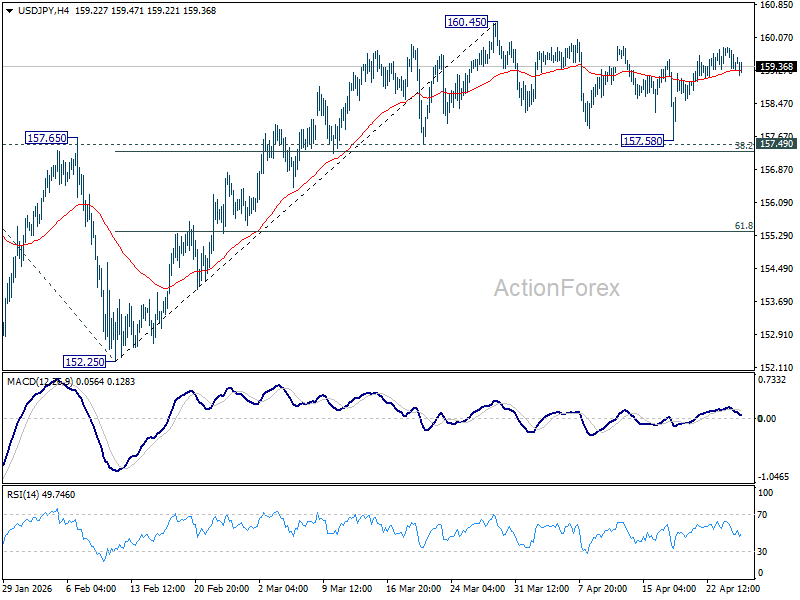

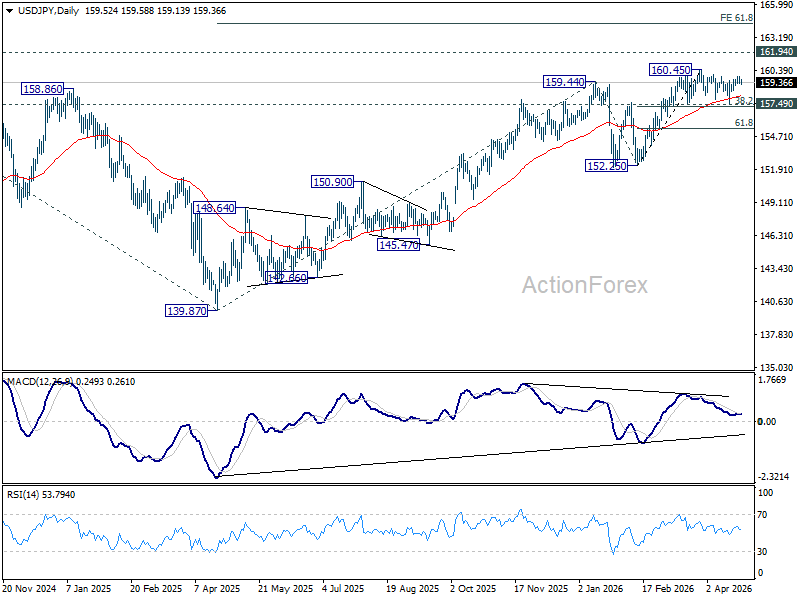

Range trading continues in USD/JPY and intraday bias remains neutral for the moment. Further rise is expected with 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) intact. On the upside break of 160.45 will target a retest on 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 153.81) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

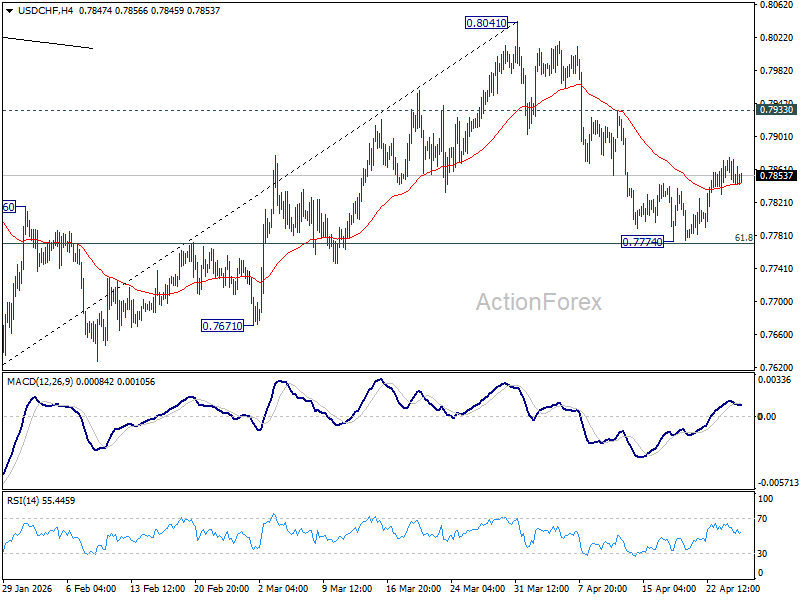

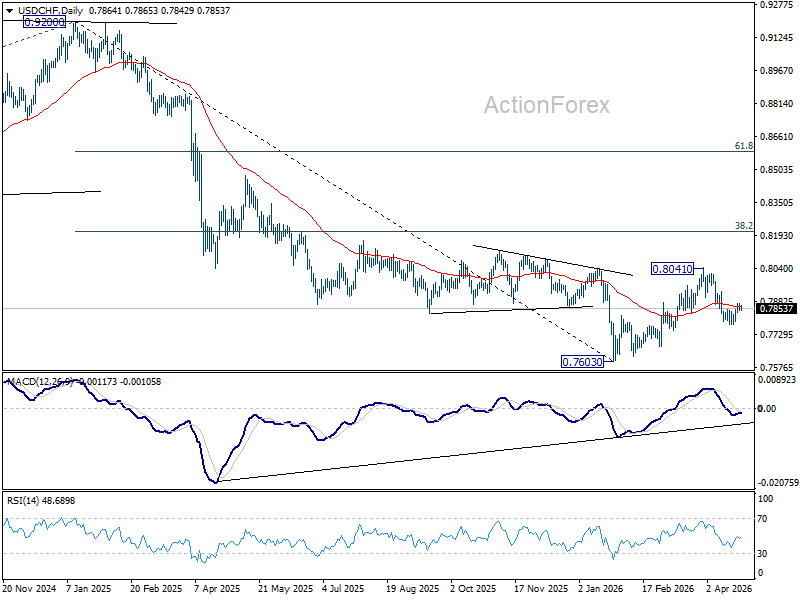

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7837; (P) 0.7858; (R1) 0.7870; More….

Intraday bias in USD/CHF remains neutral for the moment. Further decline is expected as long as 0.7933 resistance holds. On the downside, sustained break of 61.8% retracement of 0.7603 to 0.8041 at 0.7770 will pave the way to retest 0.7603 low. However, break of 0.7933 resistance will bring stronger rise back to retest 0.8041 high.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8053) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

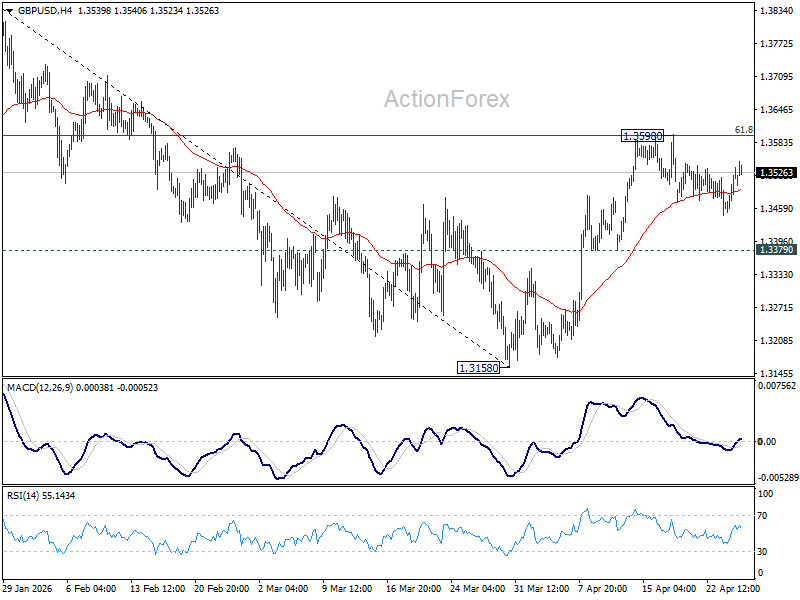

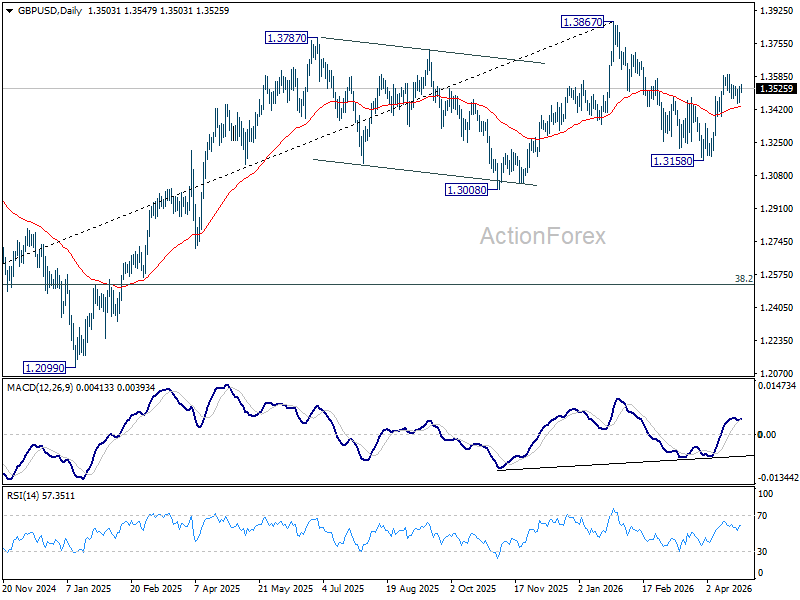

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3477; (P) 1.3508; (R1) 1.3563; More...

Intraday bias in GBP/USD stays neutral and more consolidations could be seen. Though, with 1.3379 support intact, further rally is expected. On the upside, firm break of 61.8% retracement of 1.3867 to 1.3158 at 1.3596 will pave the way to retest 1.3867 high. However, break of 1.3379 will bring deeper fall back to 1.3158 low instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

To Hike or Not to Hike? That’s the Question This Week

Markets

To meet or not to meet? That was the question last Friday. Conflicting messages appeared every hour, but in the end the US didn’t send its top negotiators on the 18h flight to Islamabad. Axios reports this morning that Iran has given a new proposal to the US. Addressing the US’s nuclear concerns would be postponed to a later stage, with the early focus on reopening Hormuz and ending the war. US President Trump is expected to hold a situation room meeting on Iran later today, discussing the current stalemate and potential options for the next steps in the war. Markets learned the hard way frontrunning an end to the conflict including sea traffic through Hormuz. Friday and this morning, there’s no relief rally in the likes of the oil price. Brent crude (June contract) trades at $107/b. Oil prices above $100 over the past two months tended to weigh on risk sentiment, cause bear flattening of core yield curves and support the dollar.

To hike or not to hike? That’s the question this week. Big central banks meet for a second time since the start of the fighting in the Middle East. At the March meeting, the likes of the ECB and BoE signaled a different reaction function compared with the energy supply shock of four years ago. The >2% inflation starting point poses greater risks of de-anchoring valuable inflation expectations. Earlier this month, the used public appearances to further exploit on possible reaction functions. Especially BoE governor Bailey pushed back against aggressive BoE rate hike bets. More in general, they used the initial two-week cease-fire and temporary decrease in oil prices to buy time. They’re looking for evidence in the data of inflation having a broader price impact (beyond energy). Last week’s April PMI’s offered a first clue with details showing a larger upward price effect than a downward growth effect. Especially input, but also output prices picked up tremendous pace. ECB President Lagarde said at the central bank’s end of March Watchers Conference that the optimal policy response to “a large though not-too-persistent overshoot of the inflation target” is some measured adjustment of policy. That’s the way markets have approached this from the very start of the conflict. The timing of a first hike has been variable, varying from April to June while the amount of rate hikes this year has swung between two and four. Going into this week’s meetings, June and 2-3 are on the scorecard for both the ECB and the BoE. The situation is slightly different for the Bank of Japan and the Fed. The BoJ was already looking in the direction of a new rate hike ahead of the war, but used downside economic risks as a reason to delay pulling the trigger. No action is expected tomorrow, but new quarterly forecasts could be the backbone of a move to 1% in June as well. Energy dependence sheltered the US from the oil shock. Fed Chair Powell will hold a steady course as the curtain falls on his tenure as Chair. If any (40% probability by year-end), US money markets err on the side of a cut as the next move as the central bank transitions to leadership under Kevin Warsh.

News & Views

Rating agency S&P has lowered Belgium’s rating from AA to AA- with a stable outlook. Moody’s last week cut Belgium into single A-category, voicing the same concerns as S&P did. The downgrade reflects persistent imbalances in public finances with budgetary consolidation to large structural budget deficits only being gradual, politically sensitive and subject to execution risks. The 2025 budget measures were insufficient to offset rising spending on age-related items and defense and interest payments, it said. The deficit has widened to about 5.2% in 2025 from 4.4% in 2024. S&P expects government measures taken in 2026 will only contain, not reduce the deficit for this year (5.2%). Shortfalls could still amount to 4.5% by 2029. Debt would therefore reach 109% by 2029 from 103% in 2025 with interest payments rising to 2.8% from 2.4%. Economic growth is seen slowing down to 0.9% this year from 1% but risks from prolonged trade disruptions and sustained higher energy prices loom. Inflation may decelerate to 2.4% from 3% in 2025.

Poland is pushing for new European tools to finance defense spending as its own budget is ballooning to unsustainable levels. Polish deficits soared to 7.3% of GDP last year. The country’s finance minister Domanski said defense spending is and will remain Poland’s top priority but the sheer amount of some 5% of GDP is weighing on public finances. Poland is making extensive use of the EU’s €150bn SAFE programme, which Domanski said is a “step in the right direction” but simultaneously calling for additional instruments because it falls short of actual needs. In a related note, Polish prime minister Tusk last week said that Brussels is contemplating to change the accounting rules so that spending via the SAFE initiative does not impact reported deficits.

Peace Hopes Lift Sentiment into Busy Week

Mood is slightly better this morning than it was into the weekend, as Iran reportedly offered the US a proposal to reopen the Strait of Hormuz — a move that could pave the way for the continuation of peace talks between the two parties. The result? Asian equities are higher this morning, with the Nikkei and Kospi rallying to fresh all-time highs. Most US and European futures point to a positive open, except for the UK’s FTSE futures, which are flat as the slight retreat in energy prices weighs on appetite there. US crude is currently trading near $98.60 per barrel, and losses could accelerate if peace hopes improve — you know the music.

Peace hopes — along with resilient earnings — are keeping major markets in a bullish mood. The AAII survey showed that bullish sentiment improved among investors despite rising inflation expectations and early signs of deterioration in economic data. Sentiment indicators on Main Street tell a completely different story, however. Data on Friday confirmed that US consumer sentiment fell to its lowest level on record in April, driven by the spike in energy prices, inflation worries and affordability concerns.

How long can equity markets and underlying economic health diverge? Potentially for a while, as deteriorating fundamentals can also be seen as “good news” for markets: a weakening economy could encourage the central banks to ease policy (or not tighten much), which tends to support valuations.

Take Procter & Gamble, for example. The company jumped before giving back part of its gains despite announcing a Q1 earnings beat. It also said that Brent at around $100 per barrel would cost roughly $1bn after tax compared to pre-war levels. The company highlighted rising transportation and raw material costs, as well as ongoing supply chain disruptions.

These pressures help explain why investors are rotating back into tech stocks, which appear less exposed to supply chain constraints. After Amazon, Google announced plans to invest $10bn in Anthropic — with potentially up to $30bn more — to remain competitive in the AI race. In return, Anthropic is reportedly set to spend heavily on securing compute capacity, including multi-gigawatt agreements with cloud providers, supporting both Amazon’s and Google’s cloud revenues. What a world.

On the policy front, the DoJ suddenly dropped its investigation into Federal Reserve (Fed) Chair Jerome Powell on the renovation of the Fed’s HQ to clear the way for Kevin Warsh, yes, because Kevin Warsh is willing to cut the interest rates – though he said he would behave as a grown-up and not be a ‘sock puppet’, but the idea of lower rates appeal to him, and the White House is loving it. Warsh has also expressed openness to reducing the Fed’s balance sheet — a process that could prove challenging given softer demand for US Treasuries, but potentially manageable if regulatory changes allow banks to operate with lower excess reserves. In short: deregulation remains part of the narrative.

The combination of softer economic data and policy-related headlines pushed US 2-year yields lower on Friday, helping lift the S&P500 to fresh highs, alongside optimism around earnings. The week ahead looks promising, with potential peace developments and a heavy earnings calendar. Around 180 companies in the S&P500 are due to report this week, including major names such as Microsoft, Meta Platforms, Alphabet, Amazon, Qualcomm, Coca-Cola and Verizon, as well as energy giants ExxonMobil and Chevron.

So far, around 28% of S&P500 companies have reported results. Of those, 84% delivered a positive EPS surprise and 81% beat on revenues. The blended earnings growth rate stands at 15.1%. If confirmed, this would mark the sixth consecutive quarter of double-digit year-on-year earnings growth, according to FactSet — not bad at all given the political and geopolitical backdrop.

In Europe, attention will focus on banks, carmakers, LVMH and TotalEnergies. The picture is more mixed, with luxury and autos facing pressure from geopolitical tensions, trade frictions and Chinese EV competition. Given Europe’s relatively limited exposure to tech — which has once again taken the lead — European equities could lag their US peers as earnings season unfolds.

On the monetary policy front, the week is also busy for central banks. The Fed, the BoJ (Bank of Japan), the European Central Bank (ECB), the Bank of England (BoE) and the Bank of Canada (BoC) are all expected to keep policy unchanged at their respective meetings, although uncertainty remains high due to geopolitical risks, elevated energy prices and slowing growth. Most have turned less hawkish in recent weeks, hoping the energy shock proves temporary. Evidence of demand destruction would likely reinforce a “wait-and-see” approach.

The US dollar is sharply lower this morning, and its recent depreciation helps ease inflationary pressures globally. The EURUSD is holding above its 200-day moving average (near 1.1675), while the USDJPY is pushing toward the 160 level — a zone where intervention risks from Japanese authorities tend to increase.

Central Bank Rate Decisions Take Centre Stage This Week

In focus today

Today, the ECB releases its survey on the access to finance of enterprises (SAFE) which among other things will give insight into firms' selling price expectations, wage costs, and inflation expectations.

We expect Bank of Japan to maintain rates unchanged overnight. We believe most conditions for a rate hike are in place, and expect the next hike likely in June, which markets currently price at close to 50-50. The situation in the Middle East will play a significant role in shaping the timing of any policy changes.

This week, monetary policy decisions will be the primary market movers. The key rate announcements include the Fed's decision late Wednesday and the ECB's on Thursday, where we expect both central banks to hold rates steady. Additionally, rate decisions from the Bank of England and the Bank of Canada are scheduled, and we expect all to keep their policy rates unchanged. On the data front, we look out for euro area flash April inflation and Q1 GDP from both the euro area and the US, all on Thursday.

Economic and market news

What happened since Friday

In the Middle East, hopes for peace faded as President Trump cancelled planned US-Iran talks in Islamabad, keeping US envoys in the US and stating Iran's offer was inadequate. Tehran has demanded the removal of the US maritime blockade before entering negotiations, while Iranian Foreign Minister Abbas Araqchi continues diplomatic efforts with mediators in Pakistan and Oman. Oil prices continued their upward trajectory as markets opened, with Brent crude rising 1.2% to USD 106.6/bbl at the time of writing. According to Reuters, only one oil products tanker entered the Gulf on Sunday, sustaining worries of prolonged constraints.

In the US, a shooting incident at the White House Correspondents' dinner likely targeted President Trump and his administration, with the suspect apprehended after firing at a Secret Service agent. The attack, the third assassination attempt on Trump since 2024, has reignited concerns over the security of top officials in light of heightened political tensions in the US.

Also in the US, Republican Senator Thom Tillis announced that he would allow Kevin Warsh's nomination as the next Federal Reserve Chair to advance, following the Justice Department's decision to close its investigation into current Chair Jerome Powell. Tillis had previously blocked the confirmation process, citing concerns over the central bank's political independence. Warsh's confirmation is now expected to proceed before Powell's term ends on 15 May, which means this week's meeting will be Powell's last as the Fed chair.

In China, industrial profit growth accelerated in March, rising 15.8% y/y, the fastest pace since September, underscoring the uneven nature of the economic recovery. While AI-related industries such as semiconductors remain strong, consumer-facing sectors continue to struggle due to weak domestic demand. The impact of the Middle East war is likely yet to be reflected in the data, with rising energy prices expected to increase input costs for manufacturers. This could either erode margins or result in higher prices for consumers.

In Germany, the Ifo indicator declined more than expected in April, with the assessment of current conditions falling to 85.4 and expectations dropping to 83.3, the lowest level since late 2023. The rise in energy prices has significantly worsened the outlook for the German economy, which remains highly exposed due to its large industrial sector. On Wednesday, the German government cut its 2026 GDP growth forecast to 0.5% y/y from 1.0%, highlighting fiscal policy as the sole expected growth driver this year.

In Sweden, producer prices rebounded in March, rising 2% y/y after five months of declines, driven by a sharp 15.8% surge in energy prices. Excluding energy-related products, producer prices fell 0.5% y/y. On a monthly basis, producer prices rose 0.6%, with domestic and import prices both up 3.7%, led by higher costs for crude oil and refined petroleum products.

Equities: Equity markets rose on Friday and over the course of last week, but we are now moving into a much more divergent market environment than the one we have seen over the past several weeks. Until recently, markets have largely traded in a broad risk-on or risk-off fashion, depending on developments around the war in Iran. Last week was different.

We saw both a strong earnings impulse, with technology performing particularly well, and at the same time an energy sector that outperformed on the back of higher oil prices. When technology and energy lead, the US benefits the most. Europe, in contrast, continued to lag and traded roughly sideways. This is also consistent with the recent macro data, which increasingly suggest that Europe is suffering materially more from the war in Iran than the US.

It is worth noting that both the S&P 500 and Nasdaq reached new all-time highs on Friday, while the Nikkei 225 is making a new all-time high this morning. On rotations, the divergence continues to increase. Even though energy performed well last week, the technology sector has outperformed energy by around 20% over the past month.

With the US close on Friday, semiconductors had risen for 18 consecutive trading days in the US(!). That illustrates very clearly the powerful underlying technology story that continues to unfold despite the war.

This morning, Asian markets are higher once again, led by South Korea and Taiwan, which are up roughly 60% and 35% year-to-date, respectively. We have said this many times before, and you know one of our key fundamental allocation points: sector allocation is crucial for how to think about regional allocation. If that was not obvious before, it certainly is this year.

European futures are also higher this morning. Tech-heavy Nasdaq futures are trading higher, while Dow Jones futures are slightly lower.

FI and FX: An important central bank week awaits with meetings (in order) from the BoJ, BoC, FOMC, BoE and the ECB. With the conflict in the Middle East entering its 9th week, the central bankers are forced to give their assessment on the experienced impact and their expectations going forward. The week starts light on macro releases but later this week we will get EA HICP and US Q1 flash GDP as wells as important data from Norway and Sweden. Markets in Asia open the week with a constructive risk-on sentiment despite oil prices remaining at the elevated levels from last Friday (June Brent Oil contract at USD106.6 this morning).

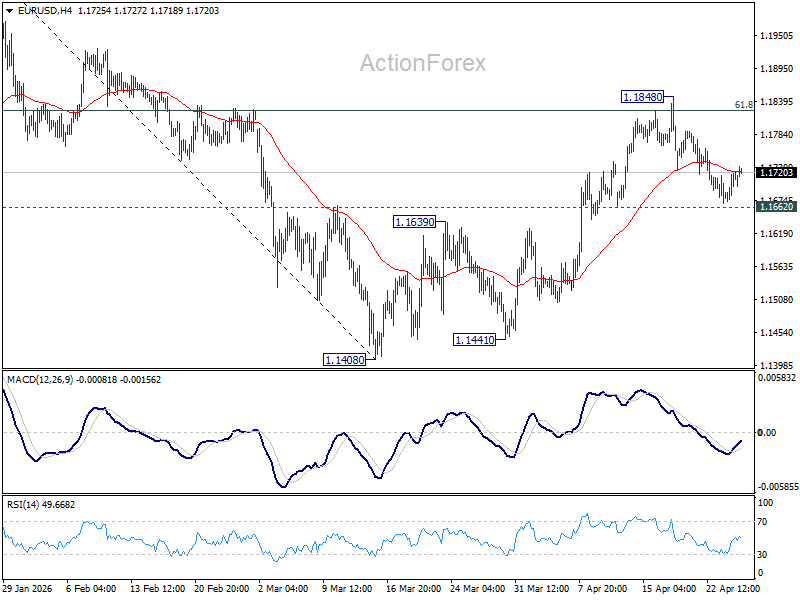

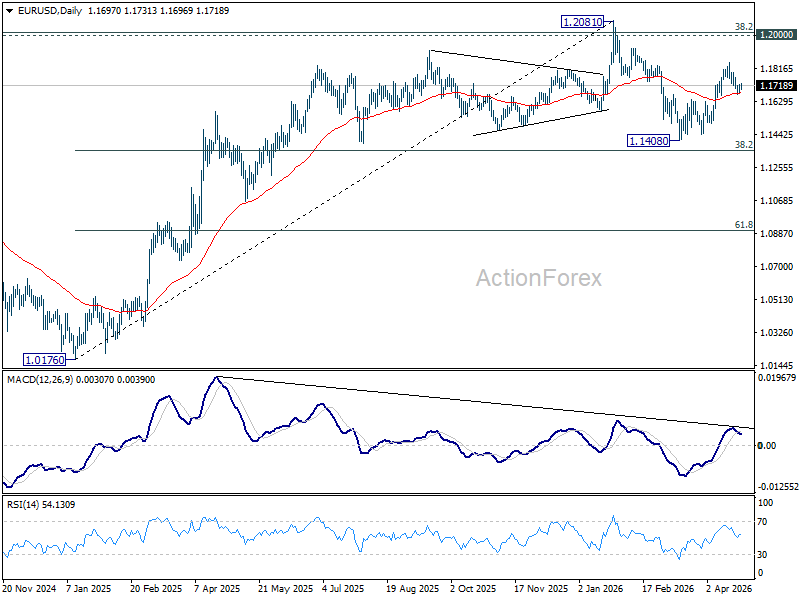

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1688; (P) 1.1706; (R1) 1.1741; More….

Intraday bias in EUR/USD remains neutral for the moment, and more consolidations could be seen. But further rally is expected with 1.1662 support intact. On the upside, sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1662 support will indicate the the rebound fro 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1530). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

Markets Shrug Off Geopolitics as AI Rally Drives Record Highs Ahead of Central Bank Super Week

Asian equities surged to fresh record highs, with KOSPI jumping more than 2.5% and Nikkei advancing over 1.5%, extending what has become a powerful rally. The strength of the move signals more than just optimism—it reflects a market that is increasingly comfortable ignoring geopolitical noise and focusing on growth narratives.

The shift has been building since the announcement of the indefinite US–Iran ceasefire last week. While negotiations have stalled, the absence of escalation has been enough to anchor sentiment. With no escalation and no resolution, markets are treating geopolitics as background noise rather than a trading driver. Risk appetite has stabilized, and capital is rotating back into equities, particularly those linked to the AI theme.

Also, the focus now shifts decisively to monetary policy, with a dense lineup of central bank decisions scheduled for week.

The Bank of Japan kicks things off on Tuesday, and what was once a straightforward hold has turned into a genuinely “live” meeting. The base case is for no change at 0.75%, but rising and broadening inflation has reopened the door to a surprise hike toward 1.00%. Even if the BoJ stays on hold, the risk for markets lies in the messaging. Without a clear signal toward tightening, Yen weakness could intensify, especially with markets already pricing a strong probability of a June move. In that sense, a passive BoJ may be as market-moving as an active one.

Wednesday brings the Federal Reserve, where the outcome is far less uncertain but no less important. Rates are expected to be held at 3.50%–3.75% in what is likely to be Jerome Powell’s final meeting as Chair before the transition to Kevin Warsh. The decision itself may be uneventful, but the tone will not be. Markets will be watching for how the Fed frames oil-driven inflation risks and whether there are any signals around the pace or endgame of balance sheet reduction.

The Bank of Canada, also meeting on Wednesday, faces a different challenge. A hold is expected, but the focus will be on updated projections as policymakers weigh weak growth—GDP expanding just 0.7% in Q4—against rising fuel costs. The key question is whether the BoC chooses to look through the oil shock or signals concern about second-round inflation effects.

Thursday brings two major European decisions. The Bank of England is widely expected to hold at 3.75%, but its “Super Thursday” projections will be the real driver. With services inflation still persistent, any upward revision to medium-term inflation forecasts could shift expectations back toward tightening, even if rates remain unchanged for now. The risk is not in the decision, but in the signal.

The European Central Bank is also expected to stand pat, with the deposit rate held at 2.00%. The focus will be on President Christine Lagarde’s guidance, particularly whether she offers any clarity on the conditions required for a hike in June. For now, the ECB is firmly data-dependent, but markets are sensitive to any hint of timing or thresholds that could anchor expectations for the next step.

The macro calendar is equally demanding. US GDP, ISM manufacturing, and PCE inflation will provide key insights into the strength of the US economy and inflation trends. In addition, Eurozone GDP and CPI flash estimates, Canada GDP, and Australia CPI will all feed into global policy expectations, ensuring that markets remain highly reactive to incoming data.

In FX markets, the risk-on backdrop is clearly visible. Aussie is leading gains, supported by expectations of strong inflation data. Kiwi and Euro are also firm, while Dollar is under pressure. Swiss Franc and Sterling are lagging, while Yen and Loonie are holding in the middle.

In Asia, at the time of writing, Nikkei is up 1.47%. Hong Kong HSI is down -0.33%. China Shanghai SSE is up 0.09%. Singapore Strait Times is down -0.53%. Japan 10-year JGB yield is up 0.026 at 2.467.

Oil Stalls as ‘Frozen Conflict’ Replaces Escalation Fears in US–Iran Standoff

Oil trades in a tight range as US–Iran tensions enter a “frozen conflict” phase. With Brent testing key near term channel resistance and traders reluctant to chase headlines, the next directional move will depend on a break above $110 or rejection lower. Read More.

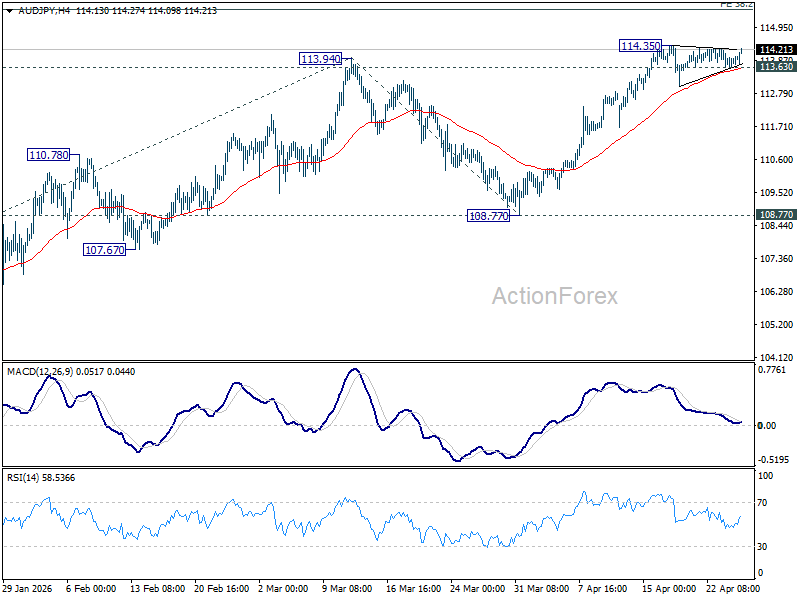

AUD/JPY Eyes Breakout Toward 120 as BoJ Decision and Australia CPI Set Up High-Stakes Week

AUD/JPY is approaching a breakout point as BoJ policy and Australia CPI set the tone for the week. With yen weakness risks rising and inflation expected to accelerate, the pair could push toward 120 if key catalysts align. Read More.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1688; (P) 1.1706; (R1) 1.1741; More….

Intraday bias in EUR/USD remains neutral for the moment, and more consolidations could be seen. But further rally is expected with 1.1662 support intact. On the upside, sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1662 support will indicate the the rebound fro 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1530). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

AUD/JPY Eyes Breakout Toward 120 as BoJ Decision and Australia CPI Set Up High-Stakes Week

AUD/JPY is setting up for a potential upside breakout toward 120 psychological level, with the next move likely to be decided by a high-stakes combination of BoJ policy and Australian inflation data. Today's bounce suggests the cross may be preparing to resume its longer-term uptrend, but confirmation now hinges on how these two key catalysts unfold.

The Bank of Japan is at the center of the near-term risk. Once seen as a straightforward hold, the decision has evolved into a "knife-edge" call as inflation broadens across the economy. While the base case remains unchanged at 0.75%, the risk of a surprise hike has crept back into the conversation, particularly ahead of the updated Quarterly Outlook Report, which is expected to show higher inflation projections for FY2026.

However, the more powerful market reaction may come from inaction rather than action. With Yen weakness already a dominant theme, a BoJ hold that lacks conviction or forward guidance could trigger renewed selling pressure. Markets are already pricing a strong chance of a June hike, but without a clear signal, expectations could be pushed further out, leaving the Yen vulnerable.

At the same time, the Australian side of the equation is turning more supportive. Inflation is expected to reaccelerate sharply, with quarterly CPI rising from 3.6% yoy to above 4.0% yoy, and monthly CPI jumping from 3.7% yoy to 4.8% yoy as the oil shock feeds through. If trimmed mean measures also surprise to the upside, it would effectively lock in a May RBA hike and raise the prospect of additional tightening.

This sets up a classic divergence trade. A hesitant BoJ combined with a more hawkish RBA outlook creates asymmetric upside risk for AUD/JPY. In this environment, even a neutral BoJ outcome could be interpreted as bearish for the Yen, while strong Australian data would provide the fuel for a sustained move higher.

There is also a risk that markets move ahead of confirmation. A BoJ hold alone could trigger a breakout attempt, as traders position for continued Yen weakness. But the durability and strength of any rally will likely depend on Australia’s CPI print, which could determine whether the move extends into a broader trend acceleration.

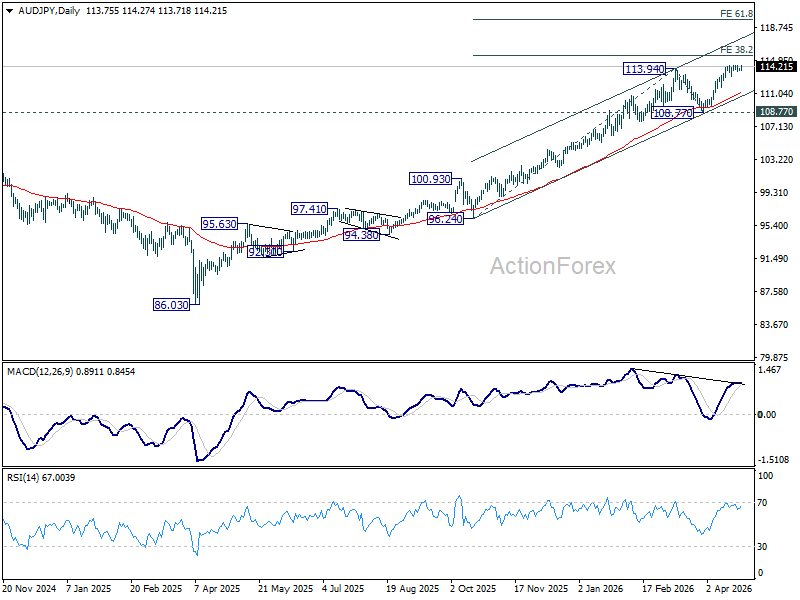

Technically, the setup is approaching a trigger point. AUD/JPY is testing 114.35 resistance, and a break would open the path toward 38.2% projection of 96.24 to 113.94 from 108.77 at 115.53 initially. Decisive break there would likely prompt upside acceleration to 61.8% projection at 119.70, which is close to 120 psychological level.

Failure to break higher, however, would not invalidate the broader bullish structure. A drop below 113.63 would simply extend the consolidation from 114.35 with another falling leg, potentially setting up a stronger base before the next leg higher.