Sample Category Title

Oil Stalls as ‘Frozen Conflict’ Replaces Escalation Fears in US–Iran Standoff

Despite the cancellation of a second round of US–Iran talks, crude oil prices showed little urgency to push higher, with Brent holding near $106 and WTI anchored around $98. In earlier phases of the conflict, such a diplomatic failure would likely have triggered a sharp rally. This time, the market response was muted, signaling a deeper shift in how geopolitical risk is being priced.

The key transition is from escalation risk to what can best be described as a “frozen conflict.” The dual blockade remains firmly in place—Iran continues to restrict flows through the Strait of Hormuz while the US maintains pressure on Iranian ports—yet neither side is moving toward decisive confrontation. With the indefinite ceasefire still in place, the market is interpreting the conflict as contained rather than expanding.

That distinction matters for oil pricing. The market has repeatedly tested the upside but failed to sustain a break above the 110 zone, reinforcing the view that current conditions represent tension without escalation. Even with significant supply disruptions from the Hormuz chokepoint—responsible for a substantial portion of global oil transit—the absence of further deterioration is capping the risk premium.

There are also tentative signs of diplomatic movement, though far from a breakthrough. US President Donald Trump acknowledged receiving a “much better” proposal from Iran, while reports suggest Tehran has floated a tactical compromise—reopening the Strait in exchange for delaying nuclear negotiations. These incremental steps support a scenario of prolonged negotiation rather than sudden resolution or renewed conflict.

At the same time, traders are showing clear signs of war fatigue. Price spikes are increasingly being faded rather than chased, reflecting a reluctance to commit to directional trades without confirmation of either escalation or de-escalation. Oil is effectively trapped between structural supply constraints and a lack of fresh catalysts.

This leaves the near-term outlook skewed mildly higher, but with limited momentum. Without a clear break in the narrative—either through escalation or a verified diplomatic breakthrough—oil is likely to grind higher rather than surge.

Technically, Brent crude is now testing the ceiling of a near-term falling channel around 109.50. Failure at this level, followed by a break below 102.16, would confirm rejection and resume the corrective move from 119.24 with another leg toward 87.79.

Conversely, a clean break above channel resistance would mark a shift back into escalation pricing, opening the path toward a retest of the 120 key psychological level.

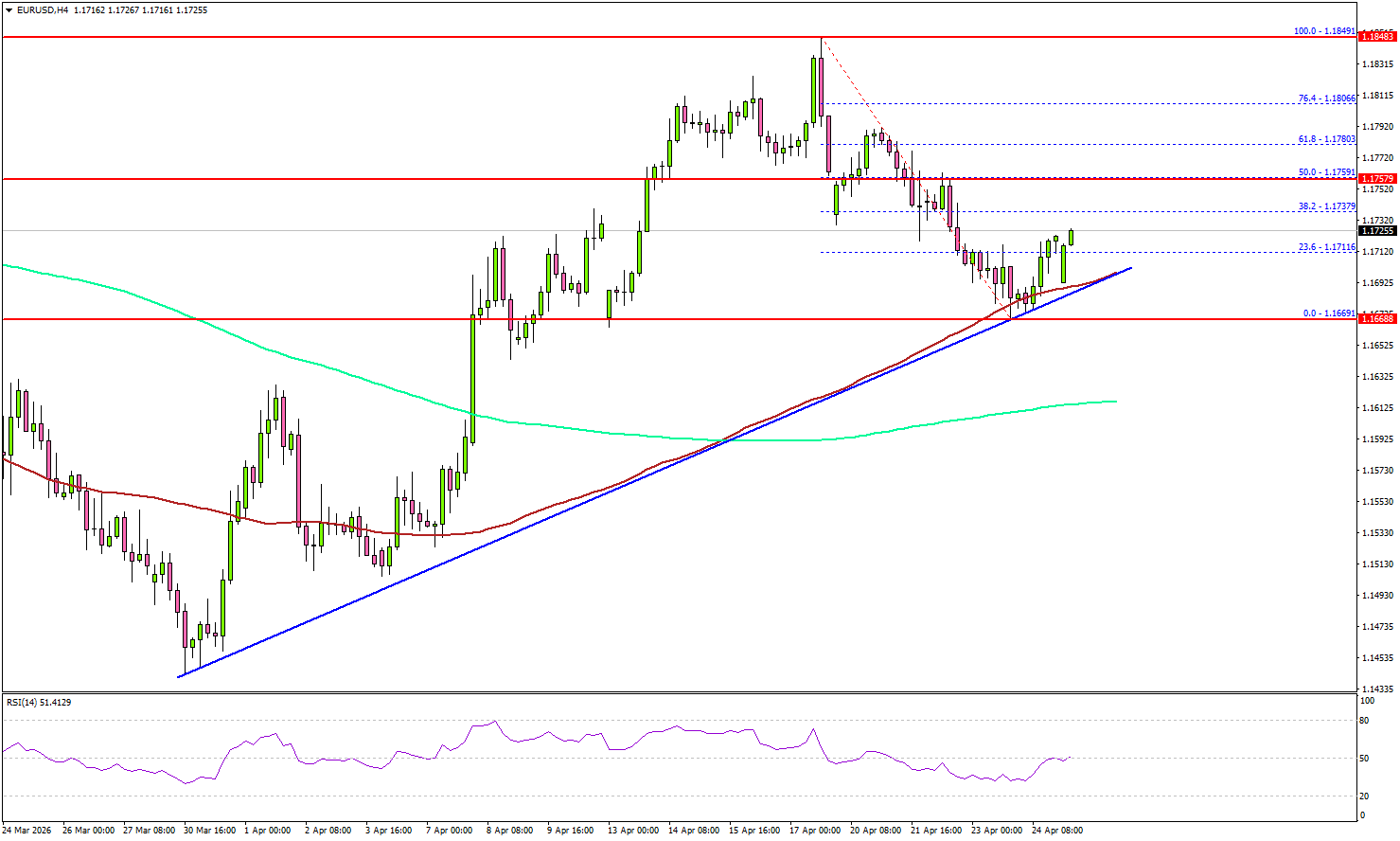

EUR/USD Tests Support—Can It Recover And Resume Upside?

Key Highlights

- EUR/USD corrected gains and tested the 1.1665 support.

- A bullish trend line is forming with support at 1.1690 on the 4-hour chart.

- GBP/USD could continue to move higher toward the 1.3620 resistance.

- Gold prices are stuck in a range below the $4,800 resistance.

EUR/USD Technical Analysis

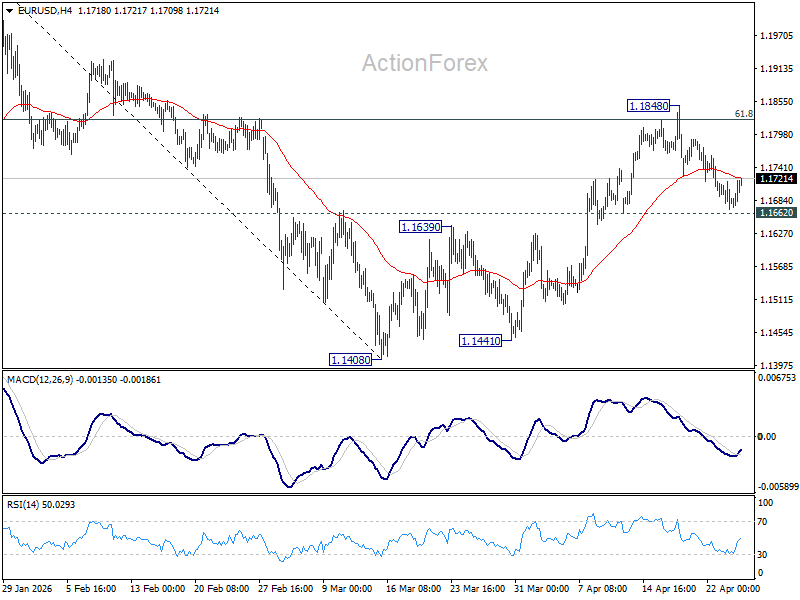

The Euro started a downside correction from 1.1850 against the US Dollar. EUR/USD tested the 1.1665 zone and might start a fresh increase.

Looking at the 4-hour chart, the pair is still above the 1.1665 pivot level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). Besides, there is a bullish trend line forming with support at 1.1690.

On the upside, the pair faces resistance at 1.1760 or the 50% Fib retracement level of the downward move from the 1.1849 swing high to the 1.1669 low.

The first major resistance sits at 1.1800. The main resistance could be 1.1850. A close above 1.1850 could open doors for gains above 1.1920. In the stated case, the bulls could aim for a move to 1.2000.

Immediate support is seen near 1.1690, the 100 simple moving average (red, 4-hour), and the trend line. The next support could be 1.1620 and the 200 simple moving average (green, 4-hour). A close below 1.1620 might push the pair toward 1.1550. Any more losses could initiate a fresh move to 1.1420 in the coming days.

Looking at GBP/USD, the pair is again moving higher and the bulls could aim for a move above the 1.3600 level.

Upcoming Key Economic Events:

- ECB's Schnabel speech.

USD/JPY Nears 160 Again on Strong U.S. Data Ahead of BoJ Meeting

The extension of the two-week Iran ceasefire helped global stock markets continue to rise last week. However, WTI oil prices also moved higher as traders stayed focused on the risk of oil supply disruption. Strong U.S. retail sales and better consumer sentiment data also showed that the U.S. economy remains strong.

Higher oil prices and strong U.S. data pushed long-term U.S. interest rates higher. This helped USD/JPY rise back close to the 160 level. In Japan, Finance Minister Satsuki Katayama said Japan is in close contact with the U.S. about possible action to stop further yen weakness.

U.S. company earnings also supported market sentiment, with around 84% of S&P 500 companies that have reported so far beating expectations. Gold fell as the stronger U.S. dollar encouraged selling. EUR/USD and European stock markets also fell as concerns grew that the Iran conflict could hurt economic growth, especially if oil supply remains disrupted.

Markets This Week

U.S. Stocks

Technology stocks moved to new record highs last week, but the Dow fell slightly despite better-than-expected U.S. economic data. The market remained cautious as the U.S. and Iran have still not reached a clear end to the conflict, while the extended ceasefire has made traders nervous about pushing stocks much higher. The Dow remains in a short-term uptrend, but a break below the 10-day moving average could trigger a fall, especially if WTI oil prices continue to rise. Resistance levels are at 49,600, 50,000, 50,500 and 51,000. Support is seen at 48,500, 48,000, 47,000, 46,000, and 45,000.

Japanese Stocks

The Nikkei index touched 60,000 last week as the extension of the U.S.–Iran ceasefire supported market sentiment and the yen remained weak. The market held above the 10-day moving average several times, confirming the short-term uptrend. However, if resistance around 60,000 holds and prices move below the 10-day moving average, the best short-term trading opportunity this week may be to look for a selling opportunity. Resistance is seen at 60,000, 60,500, 61,000, 61,500 and 62,000, while support is at 57,000, 56,000, 55,000, 54,000, and 52,000.

USD/JPY

Strong U.S. economic data and higher WTI oil prices supported the U.S. dollar last week, helping USD/JPY move back closer to resistance around 160 in quiet trading conditions. However, the risk of intervention by Japanese authorities continues to limit further gains. The Bank of Japan meeting could create volatility, especially if it signals a delay in future interest rate hikes, but for now, range trading between 157.50 and 160 remains the best short-term strategy. Resistance is at 160.00, 160.50, 162, and 165, while support is seen at 158.00, 157.50, 156.50 and 155.00.

Gold

Gold fell slightly last week as the stronger U.S. dollar and rising long-term U.S. interest rates encouraged selling. The market moved below the 10-day moving average, showing weaker short-term momentum. Overall, trading remained quiet as many commodity traders focused more on WTI oil. With the 10-day moving average pointing sideways, range trading is the preferred strategy this week. Resistance is at $4,900, $5,000, and $5,100, while support is at $4,650, $4,600, $4,500, and $4,400.

Crude Oil

WTI rose last week and tested the $100 level again after the two-week ceasefire was extended but negotiations to end the war failed. The Strait of Hormuz remained close to shut, keeping concerns about oil supply deliveries high. The situation in Iran remains unpredictable, so looking to trade against large moves may be the best strategy this week. Resistance is at $100, $110, and $120, while support is at $90, $80, $75, $70, and $67.5.

Bitcoin

Bitcoin tested old resistance around $75,000 last week and held above it as risk sentiment continued to recover. This helped the market move higher and showed that buyers remain active. Upward momentum appears to be growing, so further gains are possible as long as Bitcoin stays above the 10-day moving average. Resistance is at $80,000, $85,000, and $90,000 while support is at $75,000, $65,000, $60,000, and $55,000.

This Week’s Focus

- Monday: None

- Tuesday: Japan BoJ Interest Rate Decision, U.S. CB Consumer Confidence

- Wednesday: Australia CPI, U.S. Durable Goods Orders, Housing Starts and Fed Interest Rate Decision

- Thursday: Japan Industrial Production, E.U. CPI, Unemployment Rate and GDP, U.K. BoE Interest Rate Decision, E.U. ECB Interest Rate Decision, U.S. GDP, Core PCE Price Index and Chicago PMI

- Friday: Japan Tokyo Core CPI, Australia PPI, U.K. S&P Global Manufacturing PMI, U.S. S&P Global Manufacturing PMI

This week, markets will focus on Iran news, oil supply risks, and three major central bank meetings. All three central banks are expected to keep interest rates unchanged, but the Bank of Japan meeting may have the biggest impact. Traders will watch for any comments about possible future rate hikes, especially with Japan’s economy still weak and USD/JPY near 160.

The U.S. Federal Reserve and the European Central Bank will also be important. Traders will focus on inflation, higher oil prices, and whether interest rates could still be cut later this year. Markets are likely to react quickly to WTI oil price moves and new headlines from Iran.

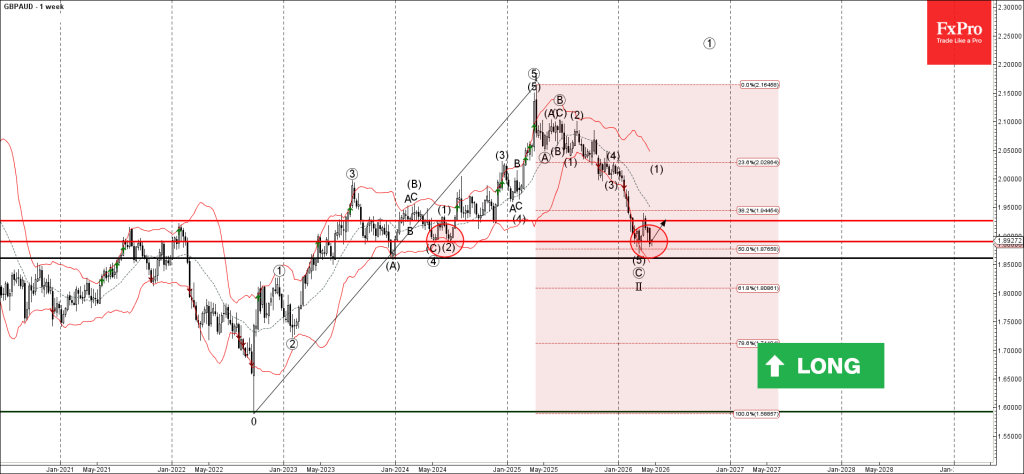

GBPAUD Wave Analysis

GBPAUD: ⬆️ Buy

- GBPAUD reversed from support area

- Likely to rise to resistance level 1.9270

GBPAUD currency pair recently reversed up from the support area between the support level 1.890, lower weekly Bollinger Band and the 50% Fibonacci correction of the sharp upward impulse from May.

The upward reversal from this from the support area continues the active intermediate impulse wave (1).

Given the clear weekly uptrend, GBPAUD currency pair can be expected to rise to the next resistance level 1.9270 (which reversed the price earlier this year).

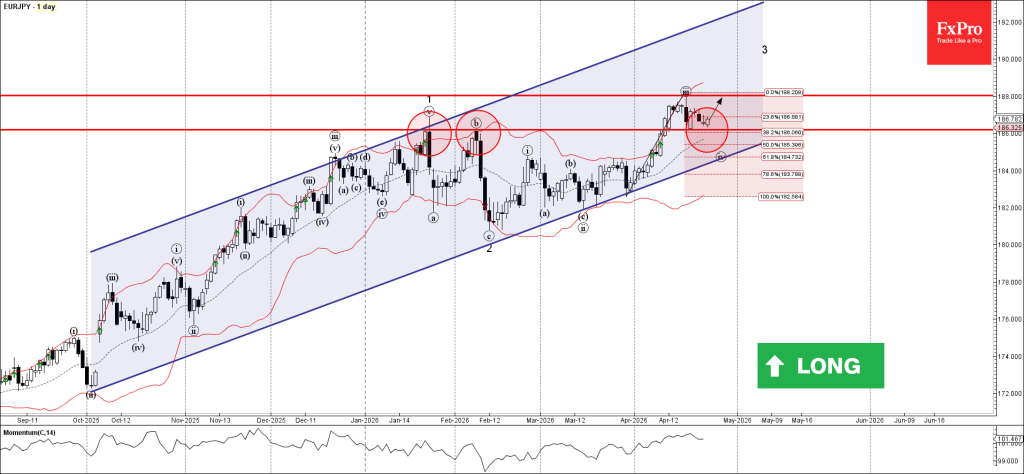

EURJPY Wave Analysis

EURJPY: ⬆️ Buy

- EURJPY reversed from support area

- Likely to rise to resistance level 1.9270

EURJPY currency pair recently reversed up from the support area between the key support level 186.00 (former monthly high from February) and the 38.2% Fibonacci correction of the upward impulse from March.

The upward reversal from this from the support area continues the active short-term impulse wave 3 of the extended impulse wave (3) from last year.

Given the strong daily uptrend and the bullish euro sentiment seen today, EURJPY currency pair can be expected to rise to the next resistance level 188.00 (top of the previous impulse wave iii).

Eco Data 4/27/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 06:00 | EUR | Germany GfK Consumer Confidence May | -33.3 | -30.2 | -28 | -28.1 |

| 06:00 | EUR |

| Germany GfK Consumer Confidence May | |

| Actual | -33.3 |

| Consensus | -30.2 |

| Previous | -28 |

| Revised | -28.1 |

Dual Pressure on Dollar: Fading US–Iran Risks and the Warsh Fed Factor

Dollar’s inability to hold onto last week’s gains is emerging as a key signal that the broader trend may be turning lower again. While the greenback initially found some support on headlines of stalled US–Iran talks, the move quickly lost momentum as markets shifted focus to ceasefire extensions and renewed diplomatic efforts. The reaction suggests that geopolitical developments are no longer delivering sustained support to the Dollar, with traders increasingly fading risk-off spikes rather than chasing them.

At the same time, a second and potentially more durable driver is coming into play: the evolving outlook for US monetary policy. The path toward a leadership transition at the Federal Reserve, combined with growing expectations of a more flexible and potentially dovish policy stance, is weighing on yields and undermining Dollar strength. Together, fading war premium and a shifting Fed narrative are creating a dual headwind for the greenback, opening the door for further downside ahead.

Geopolitical Premium Fades as Markets Look Through Conflict

The market reaction to geopolitical developments last week highlights a clear shift in behavior. Dollar did attempt to strengthen when US–Iran talks were abruptly canceled just ahead of the ceasefire deadline, but the move lacked conviction. The rally was shallow and short-lived, suggesting that traders were no longer willing to aggressively price in escalation risk.

That hesitation became more evident as events unfolded. The announcement of an indefinite US–Iran ceasefire, and then the Israel–Lebanon truce, quickly erased what little upside momentum Dollar had built. Rather than reinforcing safe-haven demand, these developments triggered a reversal.

The final confirmation came with reports of a second round of US–Iran talks in Islamabad. Dollar weakened further on the news, reinforcing the idea that markets are now fading geopolitical risk rather than chasing it. This pattern suggests that the impact of the Iran war on currencies is diminishing, with traders looking through the noise toward more durable macro themes.

Conflict Containment and Oil Signal

A key reason behind this shift is the perception that conflicts are being contained rather than allowed to escalate into a broader regional war. The Israel–Lebanon ceasefire, in particular, signals that the US and its allies are successfully “siloing” tensions, preventing spillover across multiple fronts. This containment reduces the probability of a systemic shock that would justify sustained Dollar strength.

Oil prices provide a clear real-time gauge of this dynamic. While Brent remains elevated, the inability to break decisively above the $110 level suggests that markets are not pricing a full-scale disruption scenario. Instead, current levels reflect ongoing tension without escalation—an important distinction for broader asset pricing.

As long as oil remains below that key threshold, the inflation shock is seen as manageable and the risk environment remains supportive. In this context, any temporary spikes in oil—and the associated risk-off flows—are increasingly viewed as opportunities to fade rather than signals of a lasting regime shift.

Equity Markets Reclaim Narrative

At the same time, equity markets are sending an even stronger signal. Major indices including the S&P 500, NASDAQ, Nikkei, and KOSPI have pushed to new record highs, underscoring a decisive return to risk appetite. Investors are no longer positioning around geopolitical headlines; instead, they are reallocating capital toward structural growth themes.

The dominant narrative is once again the AI trade. Strong earnings momentum, continued investment in infrastructure, and long-term productivity expectations are drawing focus away from short-term geopolitical risks. This shift in attention is critical, as it removes a key pillar of support for the Dollar.

Importantly, this is not just a US phenomenon. The global nature of the rally—from Asia to the US—indicates that investors broadly share the view that the current geopolitical environment, while volatile, does not fundamentally derail growth trajectories tied to technology and innovation.

Political Layer – Trump Strategy

The political backdrop further reinforces this interpretation. President Donald Trump’s decision to implement an indefinite ceasefire suggests a deliberate strategy to avoid full-scale military escalation. Despite earlier rhetoric about striking Iranian infrastructure, the administration appears to be prioritizing negotiation over confrontation.

At the same time, the continued US blockade of Iranian ports and Iran’s seizure of tankers should not be viewed purely as escalation. These actions are better understood as tactical positioning ahead of negotiations—hardline gestures designed to strengthen bargaining leverage rather than signals of imminent conflict expansion.

Another important element is the absence of Vice President JD Vance from the second round of talks. His earlier involvement in negotiations—and past high-profile diplomatic confrontations—raised concerns about potential disruptions. Keeping him out of the process suggests a more controlled and pragmatic approach by the administration.

This creates a dual-track strategy. By maintaining a “hawkish anchor” domestically while pursuing diplomacy abroad, the White House preserves flexibility. It can pivot toward escalation if talks fail, but for now, the bias is clearly toward de-escalation and deal-making.

Re-escalation Unlikely, AI Trade Dominates

Taken together, these developments point to a declining probability of near-term re-escalation. Markets are increasingly interpreting both military actions and diplomatic moves as part of a managed process rather than a path toward broader conflict. This perception is critical in shaping asset allocation decisions.

As a result, the underlying risk-on tone is likely to persist. Investors who have already begun rotating back into equities—particularly AI-linked sectors—are unlikely to reverse course unless oil breaks decisively higher or geopolitical dynamics deteriorate sharply.

In this environment, the AI trade is set to remain the dominant market driver. With geopolitical risks fading into the background and policy uncertainty easing, capital is flowing back into long-duration growth assets. This shift not only supports equities but also reinforces downside pressure on the Dollar, as safe-haven demand continues to erode.

Fed Transition and Warsh Outlook Add Downside Pressure on Dollar

A second major force weighing on Dollar is the evolving outlook for Federal Reserve leadership, with the “Warsh factor” rapidly gaining traction in markets. Developments late last week point to a clearer path for Kevin Warsh to succeed Jerome Powell, removing a key layer of uncertainty that had been overhanging policy expectations.

The turning point came with the Department of Justice’s decision on April 24 to drop its investigation into Powell related to the Fed’s headquarters renovation. The probe had become a political flashpoint, effectively blocking Warsh’s nomination from advancing. Its closure clears a critical hurdle, opening the way for a smoother transition ahead of Powell’s term expiry on May 15.

Political Path Opens for Warsh Nomination

This shift has immediate political implications. Senator Thom Tillis, a key member of the Senate Banking Committee, had previously pledged to block any nominee while the investigation remained open. With that obstacle now removed, markets expect Tillis to lift his hold, allowing Warsh’s nomination to proceed to a full Senate vote.

For markets, however, the more important question is not procedural but directional: what kind of Fed Chair Warsh is likely to be. Early signals suggest that investors are interpreting him as more dovish than Powell, or at least more open to policy flexibility.

Policy Signals Point to Softer Inflation Focus

During his confirmation hearing on April 21, Warsh emphasized alternative inflation measures such as Trimmed Mean and Median inflation. These metrics currently paint a softer picture than the standard Core PCE framework used by Powell, leading markets to infer that Warsh may place less weight on persistent inflation pressures.

This distinction matters. By focusing on these “cleaner” measures of inflation, Warsh effectively lowers the perceived urgency for maintaining restrictive policy. It gives markets a rationale to bring forward expectations for rate cuts, particularly if incoming data continues to soften.

“Less Is More” Communication Shift

Warsh also signaled a shift in communication strategy. He criticized the Fed’s current forward guidance approach, arguing that policymakers “talk too much” about future rate paths. Markets interpret this “less is more” doctrine as a willingness to step back from aggressive signaling, potentially allowing policy to ease more quickly without pre-commitment.

The combination of reduced uncertainty, a clearer leadership transition, and a perceived dovish tilt is reinforcing expectations for a more aggressive easing cycle, potentially starting this summer. Together with fading geopolitical support, the Warsh factor is becoming a pillar of the “Dollar fade” narrative, adding a structural layer to the downside risks already emerging in recent price action.

Market Implications: Dual Headwinds Set Stage for Sustained Dollar Weakness

The combined effect of fading geopolitical risk and a shifting Fed outlook is tilting the balance against Dollar. With the war premium eroding and policy expectations turning more accommodative, two of the greenback’s key pillars are weakening simultaneously. This creates a backdrop where rallies are likely to be sold into rather than extended.

At the same time, the broader risk environment is turning more supportive. Equity markets continue to lean into the AI-driven growth narrative, and as long as oil prices remain contained below key escalation levels, inflation concerns are unlikely to trigger a sustained risk-off shift. This reinforces the idea that markets are transitioning back to a growth-focused regime rather than one dominated by geopolitical fear.

In this environment, the path of least resistance for Dollar appears to be lower. While near-term volatility around geopolitical headlines and central bank expectations is likely to persist, the underlying trend favors continued downside. Unless there is a decisive re-escalation that pushes oil sharply higher above $110, the current mix of improving risk sentiment and dovish policy expectations should keep pressure on the greenback.

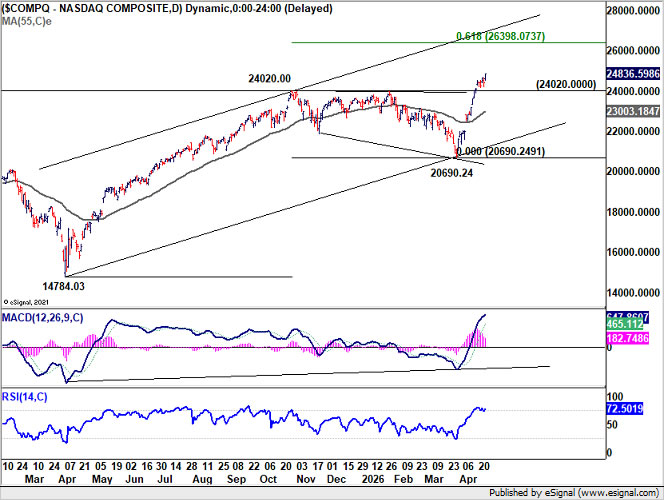

NASDAQ and S&P Hit New Highs as Dollar Fails at 55 D EMA

After some initial hesitation, the uptrend in NASDAQ extended decisively last week, with a strong rally pushing the index to a fresh record close at 24,836.59. Further upside is expected as long as 24,020.00—now turned support—holds. The next target lies at 61.8% projection of 14,784.03 to 24,020.00 from 20,690.24 at 26,398.07. However, strong resistance could emerge ahead of the medium-term channel ceiling near the 27,000 level, potentially capping gains.

On the downside, a break below 24,020.00 would signal near-term consolidation, but any pullback should be contained above 55 D EMA (now at 23,003.18) to keep the broader bullish structure intact and set the stage for another leg higher.

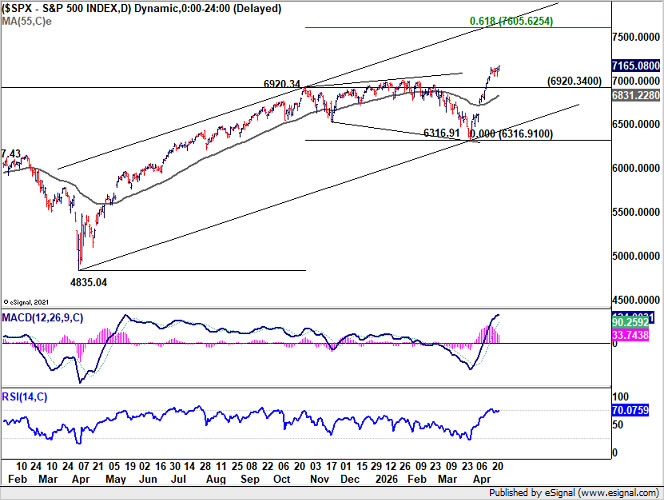

Similarly, the uptrend in S&P 500 extended further, with a new record close at 7,165.08. Further rise is expected as long as 6,920.34—also turned support—holds. The next upside target is 61.8% projection of 4,835.04 to 6,920.34 from 6,316.91 at 7,605.62.

On the downside, a break below 6,920.34 would trigger consolidation, but downside is expected to be contained above 55 D EMA (now at 6831.22), preserving the bullish bias.

Dollar Index showed signs of exhaustion. The recovery from 97.63 extended higher but stalled at 55 Day EMA (now at 98.97). The outlook remains unchanged, with decline from 100.64 seen as reversal of the prior rebound from 95.55. Further downside is expected as long as 99.18 resistance caps. A break below 97.63 would open the way for a retest of the 95.55 low. That said, a firm break above 99.18 would neutralize the immediate bearish outlook and shift focus back toward the 100.64 resistance.

Still, the broader trend remains bearish. With the 38.2% retracement of 110.17 to 95.55 at 101.13 intact, recent price action is viewed as a consolidation phase within a larger downtrend. The prior rejection at 55 Week EMA reinforces this view, suggesting that the broader declines from 110.17 and 114.77 are likely to resume over time.

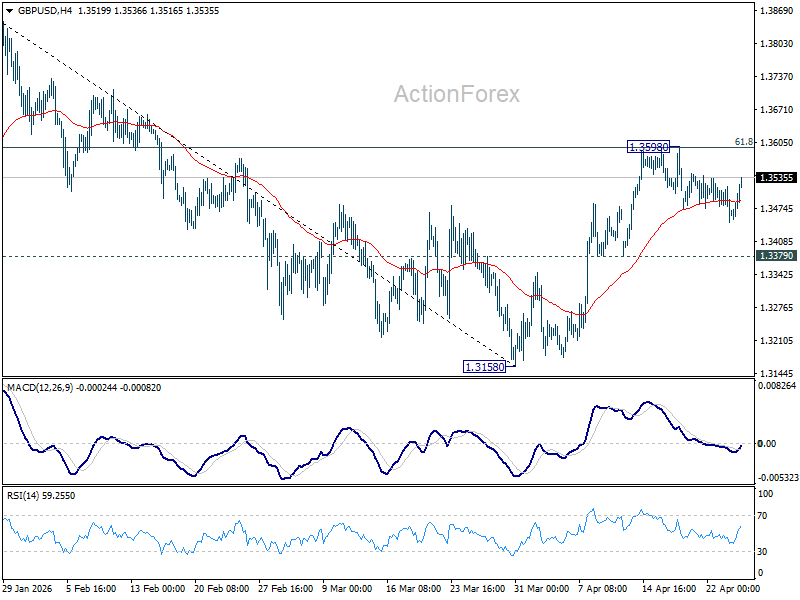

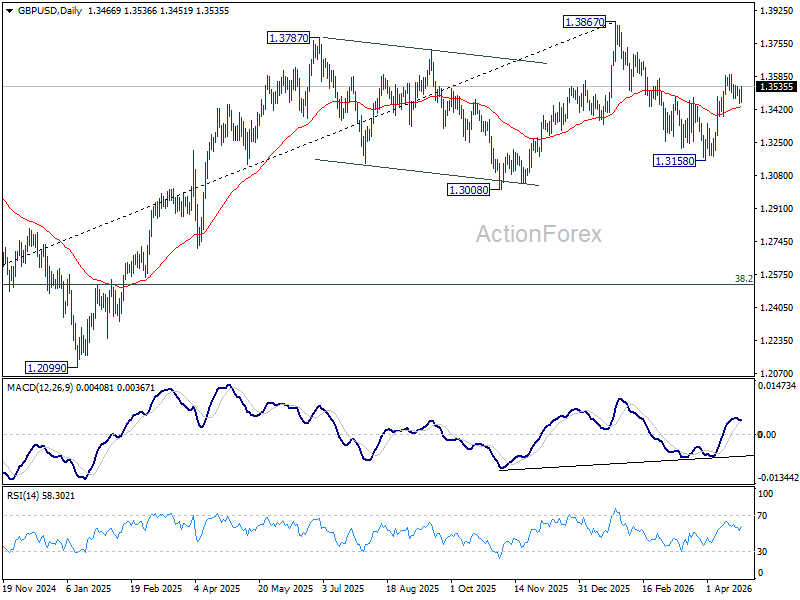

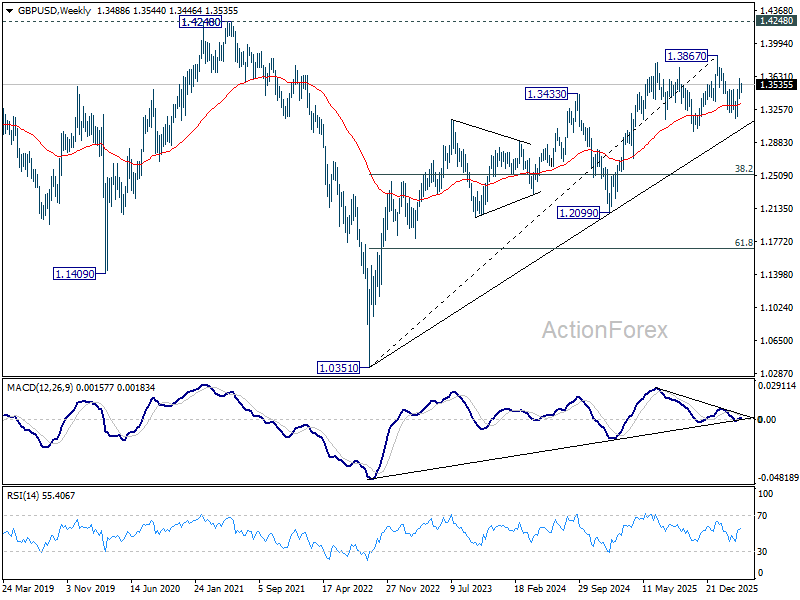

GBP/USD Weekly Outlook

GBP/USD turned into consolidations last week and outlook is unchanged. Initial bias remains neutral this week first. On the upside, firm break of 61.8% retracement of 1.3867 to 1.3158 at 1.3596 will pave the way to retest 1.3867 high. However, break of 1.3379 will bring deeper fall back to 1.3158 low instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

In the long term picture, as long as 1.4248/4480 resistance zone holds (38.2% retracement of 2.1161 to 1.0351 at 1.4480), the long term outlook will remain bearish. That is, price actions from 1.0351 are seen as a corrective pattern to down trend from 2.1161 (2007 high) only. Nevertheless, decisive break of 1.4248/4480 will be a strong sign of long term bullish reversal.

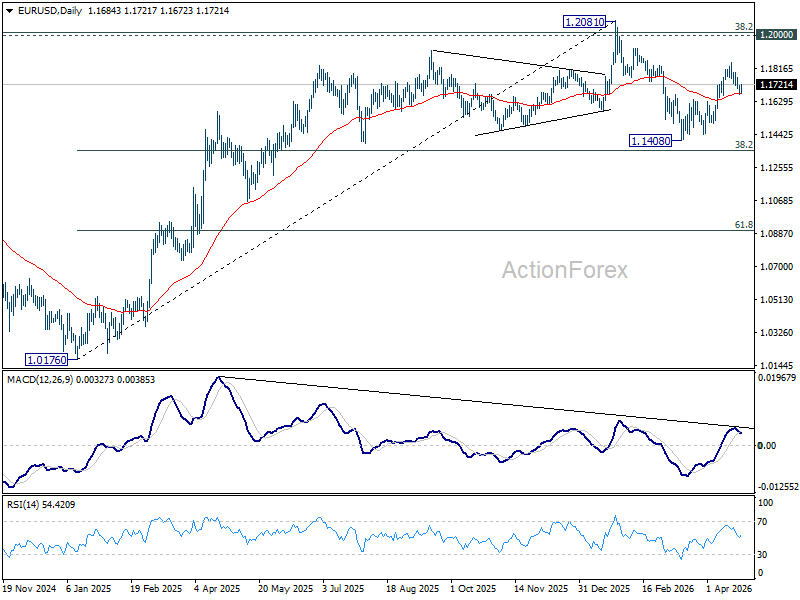

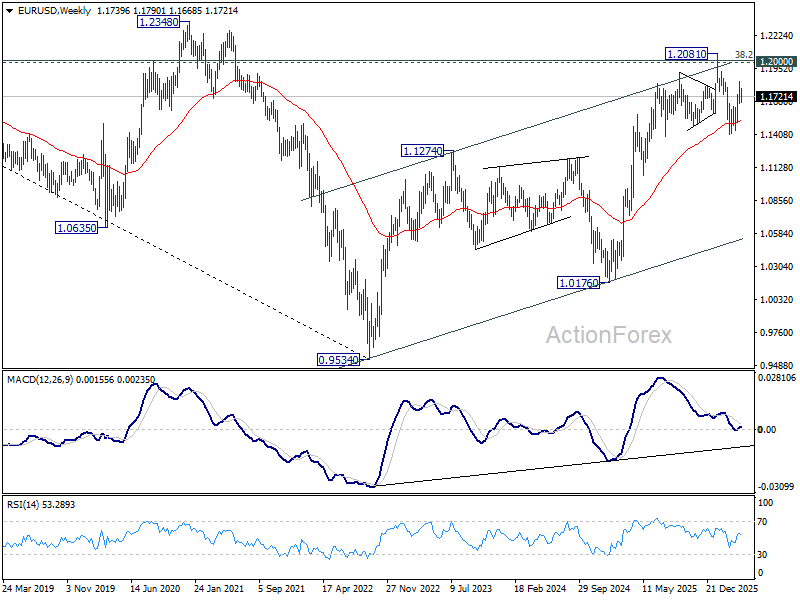

EUR/USD Weekly Outlook

EUR/USD's gyrated lower last week but recovered ahead of 1.1662 support. Initial bias remains neutral this week first, and further rise is in favor. On the upside, sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1662 support will indicate the the rebound fro 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1523). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

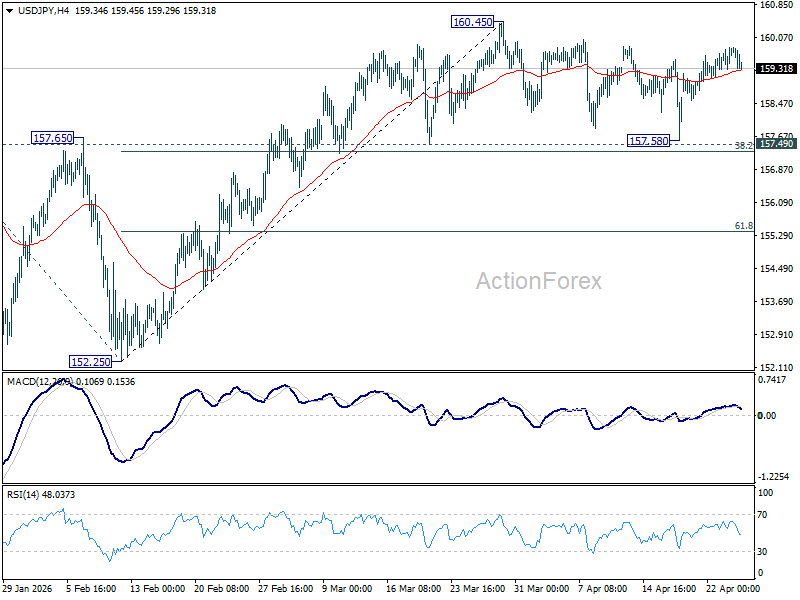

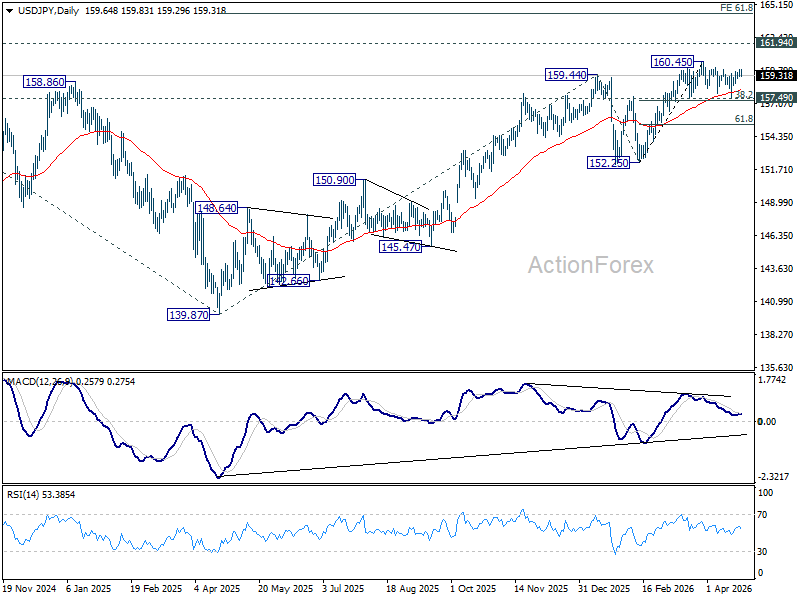

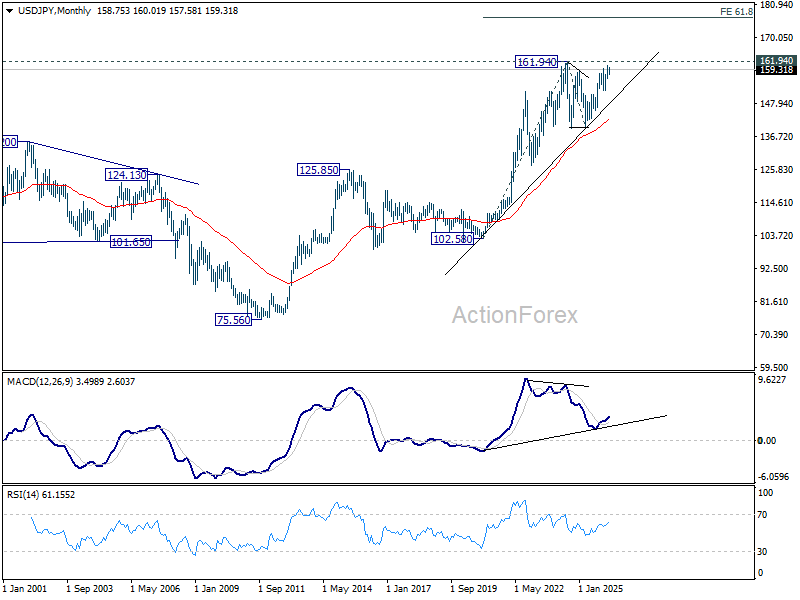

USD/JPY Weekly Outlook

USD/JPY extended consolidations below 160.45 last week and outlook is unchanged. Initial bias remains neutral this week. Further rise is expected with 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) intact. On the upside break of 160.45 will target a retest on 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 153.61) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

In the long term picture, up trend from 75.56 (2011 low) is still in progress and might be ready to resume. Firm break of 161.94 will target 61.8% projection of 102.58 (2020 low) to 161.94 (2024 high) from 139.87 at 176.55 in the medium term. Long term outlook will stay bullish as long as 139.87 support holds, even in case of deep pullback.

GBP/USD Weekly Outlook

GBP/USD turned into consolidations last week and outlook is unchanged. Initial bias remains neutral this week first. On the upside, firm break of 61.8% retracement of 1.3867 to 1.3158 at 1.3596 will pave the way to retest 1.3867 high. However, break of 1.3379 will bring deeper fall back to 1.3158 low instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

In the long term picture, as long as 1.4248/4480 resistance zone holds (38.2% retracement of 2.1161 to 1.0351 at 1.4480), the long term outlook will remain bearish. That is, price actions from 1.0351 are seen as a corrective pattern to down trend from 2.1161 (2007 high) only. Nevertheless, decisive break of 1.4248/4480 will be a strong sign of long term bullish reversal.