Sample Category Title

Canada: Retail Sales Rise in February, With Momentum Carrying into March

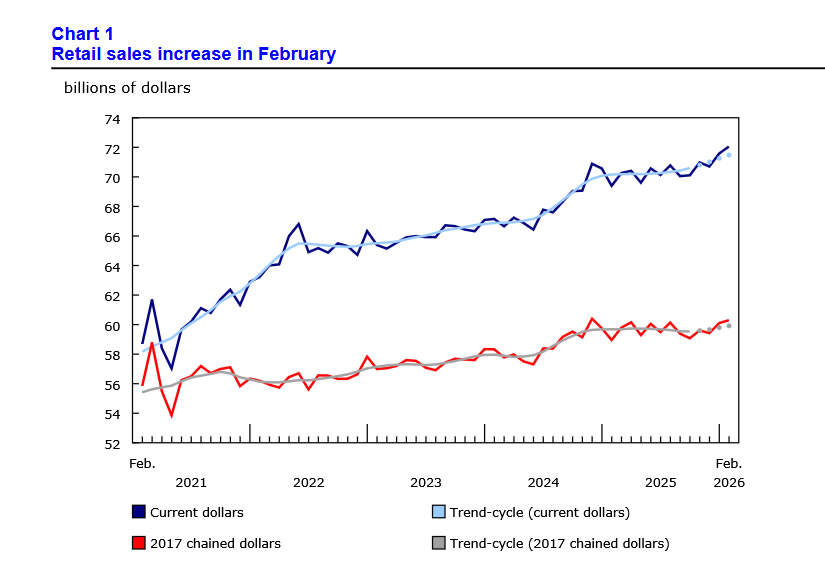

Retail sales rose 0.7% month-on-month (m/m) in February, extending gains into a second month. This was below Statistics Canada’s advance estimate for a 0.9% increase.

In volume terms, activity increased a more modest 0.3% m/m, suggesting the headline gain was largely driven by prices.

Motor vehicle and parts dealers posted a 1.0% m/m increase, driven by higher sales at new car dealers (+0.7% m/m) and a strong rebound in used vehicles (+4.0% m/m).

Receipts at gasoline stations and fuel vendors were flat on the month, though volumes edged up 0.1% m/m, pointing to modest demand.

Core retail sales—excluding motor vehicles and gasoline—also strengthened, rising 0.9% m/m and starting the year on firmer footing.

Core retail sales (excluding autos and gas) rose 0.6% m/m (a second consecutive increase), and were led by general merchandise retailers (+1.2% m/m), food and beverage retailers (+0.9% m/m), and clothing and accessories (+1.1% m/m). Building material and garden equipment dealers fell 0.6%.

Retail e-commerce sales declined 0.6% m/m in February.

Looking ahead, Statistics Canada’s advance estimate points to a further 0.6% m/m increase in March.

Key Implications

Consumers delivered another solid month in February, with early indications pointing to continued strength in March. That said, inflation jumped in March, suggesting some of the momentum is being driven by higher prices rather than broad-based demand growth. Our internal TD Spend data point to some softening in discretionary spending in March.

Higher energy prices will dent purchasing power, but we do not expect this to materially weaken domestic demand beyond what's already embedded in our outlook. Together with the drags from weak population growth and trade-related headwinds the economy is expected to grow at a below-trend pace this year.

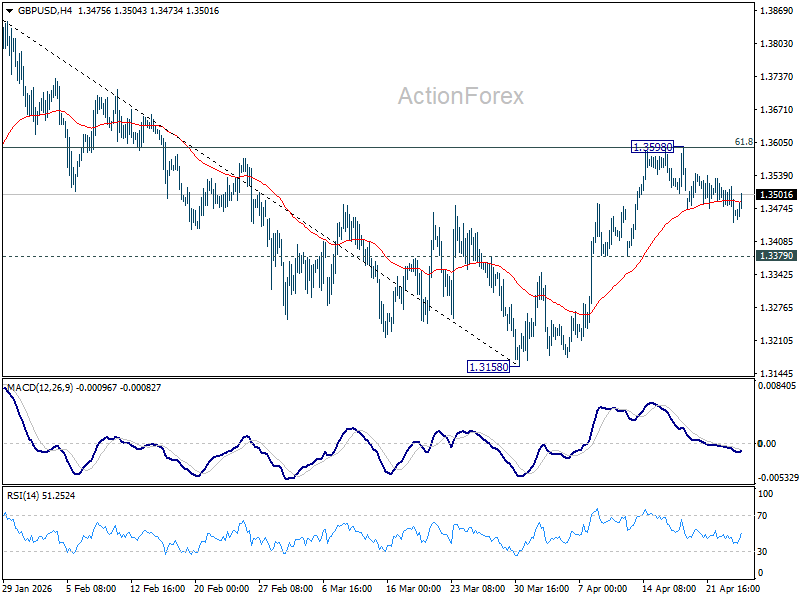

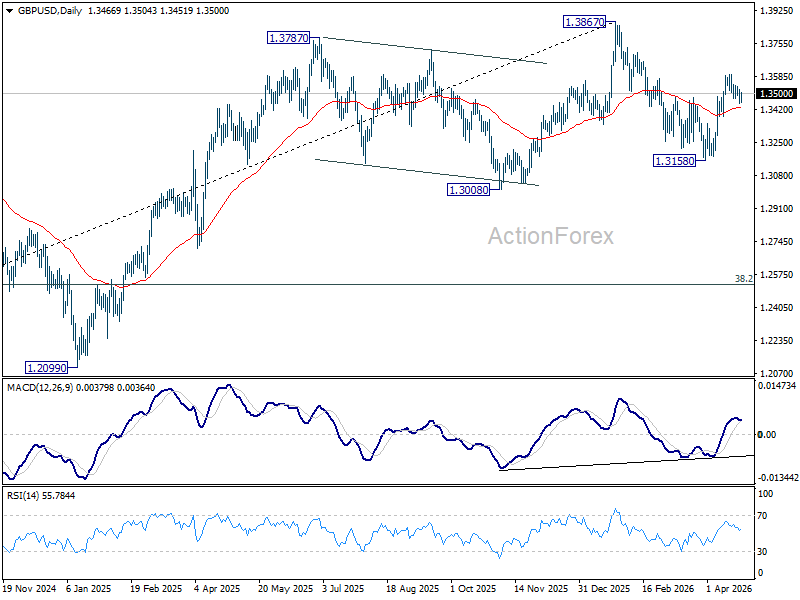

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3435; (P) 1.3477; (R1) 1.3507; More...

GBP/USD is still bounded in consolidations below 1.3598. Intraday bias bias stays neutral first. Further rise is still in favor with 1.3379 support intact. On the upside, sustained break of 61.8% retracement of 1.3867 to 1.3158 at 1.3596 will pave the way to retest 1.3867 high. However, firm break of 1.3379 will bring deeper fall back to 1.3158 low instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

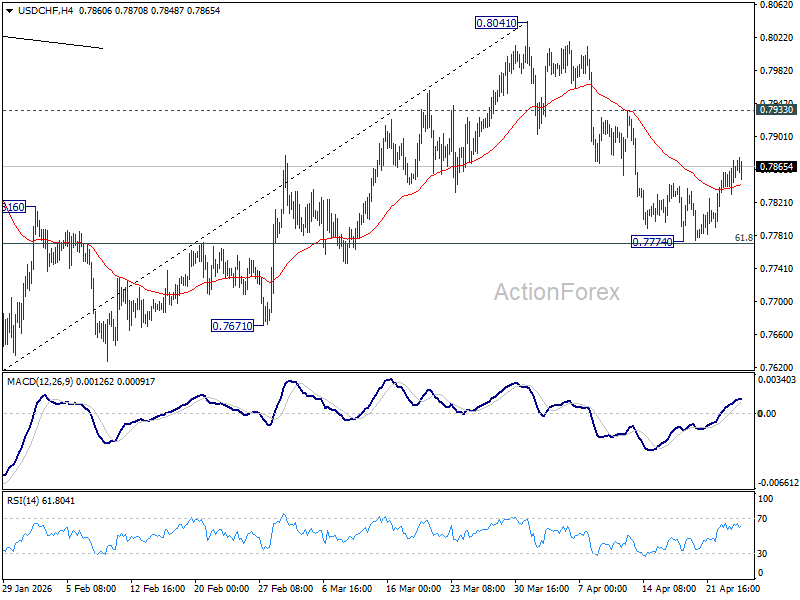

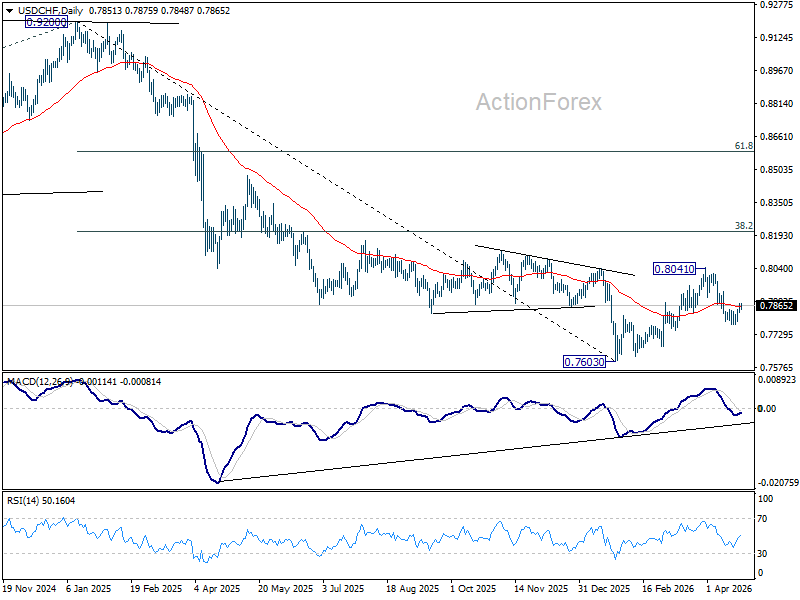

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7838; (P) 0.7856; (R1) 0.7882; More….

No change in USD/CHF's outlook and intraday bias stays neutral. Further decline is expected as long as 0.7933 resistance holds. On the downside, sustained break 61.8% retracement of 0.7603 to 0.8041 at 0.7770 will resume the decline from 0.8041 to retest 0.7603 low. However, break of 0.7933 will bring retest of 0.8041 high instead.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8059) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

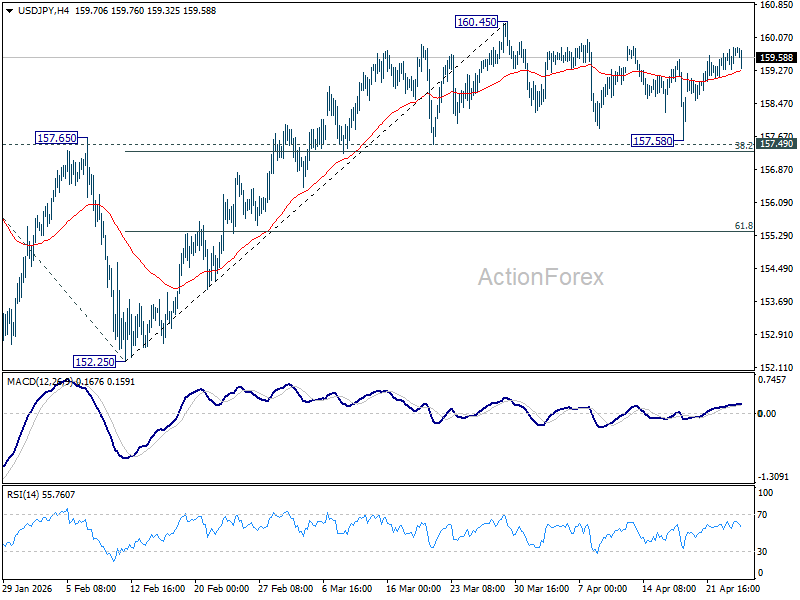

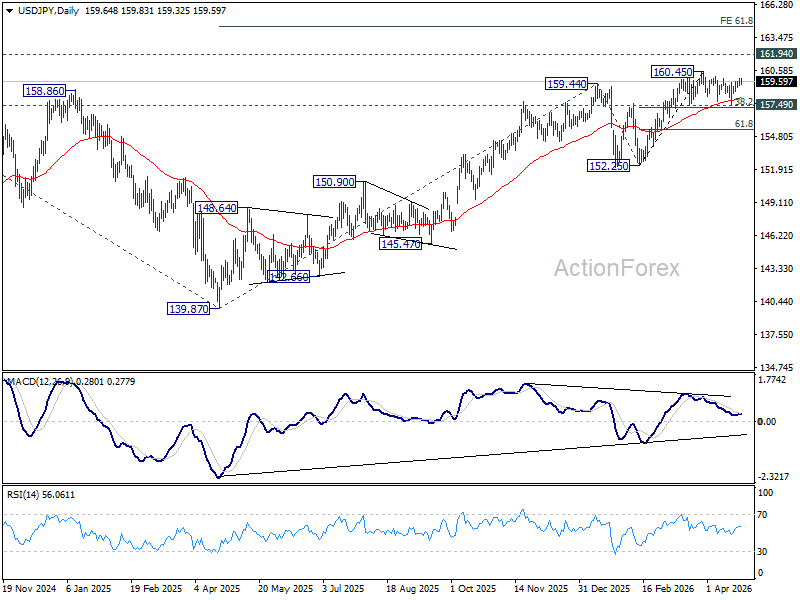

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 159.41; (P) 159.64; (R1) 159.99; More...

Outlook in USD/JPY remains unchanged as range trading continues. Intraday bias stays neutral. Further rise is expected with 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) intact. On the upside break of 160.45 will target a retest on 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 153.80) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

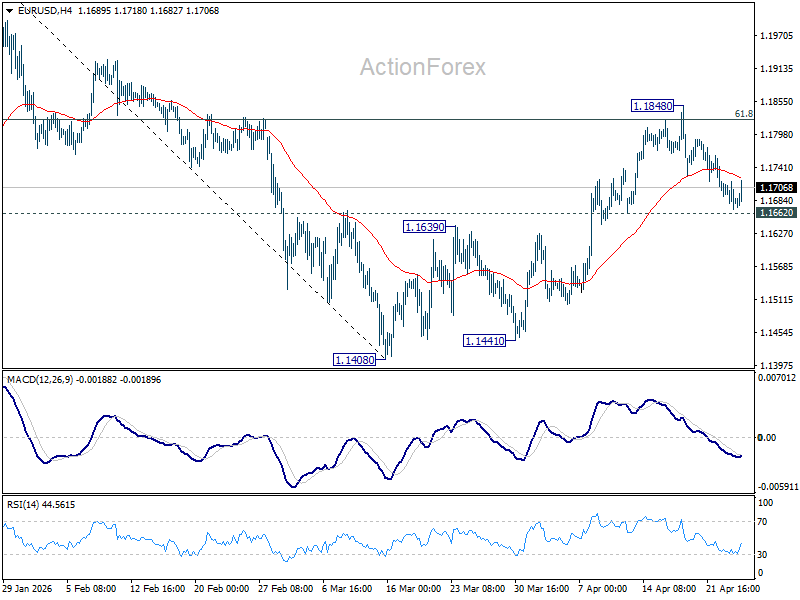

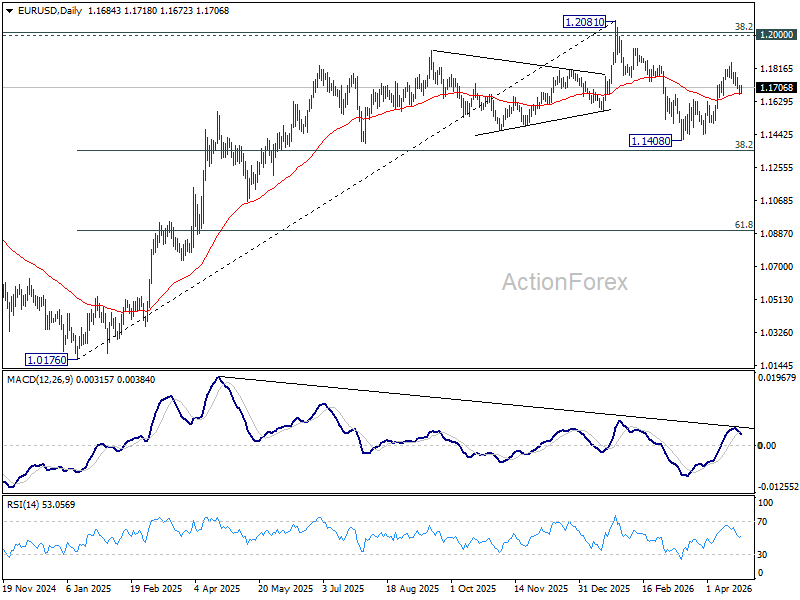

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1663; (P) 1.1691; (R1) 1.1712; More….

EUR/USD recovers ahead of 1.1662 support and intraday bias remains neutral. Further rise is still mildly in favor. On the upside, sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1662 support will indicate the the rebound fro 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1507). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

Dollar Eases as US–Iran Talk Hopes Rise, Markets on Guard for Weekend Risk

Dollar is paring back some of this week’s gains as tentative optimism emerges around a possible revival in US–Iran peace talks. The shift in sentiment is modest but notable, with traders dialing down some defensive positioning built earlier in the week. Oil prices are also reflecting this adjustment, with Brent pulling back to around $105 after briefly touching $108 earlier in the day.

The key catalyst is the report that Iranian Foreign Minister Abbas Araqchi is scheduled to arrive at Islamabad tonight, leading a high-level delegation. This development is being interpreted as a key signal that diplomatic channels are reopening after a week of uncertainty.

Pakistan’s role has been critical. Prime Minister Shehbaz Sharif and his mediation team have been actively working behind the scenes to bridge gaps after the first round of talks failed. The fact that discussions have progressed to the point of a physical meeting suggests that backchannel diplomacy has made tangible progress.

In diplomatic terms, such a visit is not symbolic. A foreign minister does not enter a high-stakes negotiation environment without a pre-negotiated framework or at least a baseline for discussion. Araqchi’s arrival suggests that both sides may have moved beyond the earlier stalemate over the 10-point plan.

His profile also matters. Araqchi is widely seen as a pragmatic negotiator, in contrast to the more hardline stance of the IRGC. His involvement signals that Iran’s leadership may be willing to explore a more flexible position, potentially opening the door for progress.

Equally important is the continued US presence in Islamabad. Reports that logistics and security teams remained on the ground even when talks were “on hold” earlier in the week indicate that Washington never fully disengaged. This suggests that neither side is prepared to let the ceasefire collapse outright.

Still, uncertainty remains high. The geopolitical backdrop has not fundamentally changed, with maritime tensions and supply risks in the Strait of Hormuz continuing to underpin oil prices. This limits the extent of risk recovery and keeps markets cautious.

In FX markets, the reaction is measured. Canadian Dollar leads the week so far, supported by oil, while Dollar holds firm despite today’s pullback. Euro continues to lag on weak economic fundamentals, and Yen remains under pressure, though intervention risks persist. Aussie and Kiwi are positioned in the middle.

Overall, markets are positioning carefully, aware that any breakthrough—or breakdown—over the weekend could trigger sharp gaps at the next open.

In Europe, at the time of writing, FTSE is down -0.24%. DAX is up 0.28%. CAC is down -0.41%. UK 10-year yield is down -0.205 at 4.992. Germany 10-year yield is up 0.005 at 3.016. Earlier in Asia, Nikkei rose 0.97%. Hong Kong HSI rose 0.24%. China Shanghai SSE fell -0.33%. Singapore Strait Times fell -0.43%. Japan 10-year JGB yield rose 0.014 to 2.441.

Canada Retail Sales Rise 0.7% in February, Miss Expectations Despite Broad Gains

Canada retail sales rose 0.7% in February, missing expectations, while core sales gained 0.6%. Advance estimate points to another 0.6% increase in March. Read More.

Germany Ifo Falls to 84.4 as Iran Crisis Hits Confidence

German business confidence has dropped to pandemic-era lows as the Iran crisis hits sentiment. The outlook is deteriorating fast. Read More.

UK Retail Sales Rise 0.7% as Fuel Stockpiling Drives March Rebound

UK retail sales rose 0.7% in March, beating expectations as fuel buying surged, while underlying demand remained modest with ex-fuel sales up just 0.2%. Read More.

SNB's Schlegel Flags Global Uncertainty from Middle East Conflict, Signals Policy Readiness

Rising energy prices are pushing inflation higher—and central banks are watching closely. SNB signals readiness to act. Read More.

Japan's Core Inflation Rises to 1.8% in March, Core-Core Ticks Down

Japan CPI rises to 1.8% in March but remains below BoJ's target as core-core inflation slips to 2.4%. Rising oil prices and cost pressures pose risks ahead. Read More.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1663; (P) 1.1691; (R1) 1.1712; More….

EUR/USD recovers ahead of 1.1662 support and intraday bias remains neutral. Further rise is still mildly in favor. On the upside, sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1662 support will indicate the the rebound fro 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1507). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

Canada Retail Sales Rise 0.7% in February, Miss Expectations Despite Broad Gains

Canada’s retail sales rose 0.7% mom to CAD 72.1B in February, falling short of expectations for a 0.9% increase but still marking a solid gain after recent softness. The advance was relatively broad-based, with sales increasing in seven of nine subsectors.

The main driver came from motor vehicle and parts dealers, where sales rose 1.0% for a second consecutive month. Core retail sales, which exclude autos and fuel, also showed resilience with a 0.6% increase.

Looking ahead, preliminary estimates from Statistics Canada point to a further 0.6% rise in March.

| Indicator | Feb 2026 |

|---|---|

| Retail Sales (MoM) | +0.7% |

| Retail Sales Value | CAD 72.1B |

| Core Retail Sales (MoM) | +0.6% |

| Motor Vehicle & Parts Sales | +1.0% |

| Subsector Performance | 7 of 9 ↑ |

| Advance Estimate (March MoM) | +0.6% |

Weekly Recap: Dollar, Crude Oil and S&P500 Continues Their Growth

US Dollar

The US dollar has continued its advance amid a reduced likelihood of de-escalation in the Middle East conflict. The US has ruled out military action and intends to deprive Iran of oil revenues by blocking the Strait of Hormuz. This long-term game risks extending the rally in Brent and WTI. This will deal a blow to the eurozone, which is dependent on energy imports. Under these conditions, Germany has halved its 2026 GDP forecast, from 1% to 0.5%, and the EURUSD pair has retreated.

Rising oil prices are weighing on the euro due to deteriorating trade conditions within the currency bloc. However, for most of April, EURUSD rose as investors bought into rumours of productive talks between the US and Iran. As soon as it became clear that the opposing sides had reached a stalemate, the regional currency began to be sold off on the back of the facts.

The euro’s retreat is reinforcing the S&P 500’s rapid rally. The broad stock index has hit a new record high, driven by bargain-hunting by the market crowd amid expectations of strong corporate earnings. The US economy will suffer less from the closure of the Strait of Hormuz and high oil prices than the European economy. As a result, alongside FOMO (the fear of missing out), the theme of American exceptionalism may return to markets. Under such conditions, the USD index and equities will move in the same direction.

Stock indices

The US stock market has concluded that the worst of the conflict in the Middle East is behind us. Oil prices have not skyrocketed, and the rise has not triggered a global recession. Hostilities have given way to a ceasefire, and the parties are moving towards a diplomatic settlement of their disputes. So, it is time to put geopolitics aside and focus on fundamentals. Expectations of strong corporate earnings reports and attractive company valuations have catalysed the S&P 500 rally.

At first glance, the surge in the US stock market was driven by the success of a handful of large-cap companies. When the broad stock index hit a new October high, only 11 S&P companies reached 52-week highs. In the 2021 bull market, around 90% of issuers were trading above their 200-day moving averages. Now, only 60% are.

Nevertheless, the market always follows the leaders. This is likely to manifest as increased trading volumes in US shares. In April, these volumes were 11% below their average levels over the past six months. In March, by contrast, against the backdrop of the escalating conflict in the Middle East, they were 9.5% higher.

Gold

The strengthening of the US dollar is forcing gold into a defensive stance. The precious metal rose in the first half of April on expectations that the conflict’s peak had passed and that de-escalation would lead to lower oil prices. As this has not yet happened, investors have adopted a worrying scenario: that central banks will be forced to tighten monetary policy on a massive scale due to high inflation.

According to the Amundi asset management company, the surge in consumer prices triggered by the energy shock is likely to be temporary rather than permanent. Core inflation will be better contained than in 2022. This will reduce the need for central banks to adopt a more ‘hawkish’ stance, thereby supporting gold.

Central bank bullion sales could put pressure on the price of the precious metal. Since the start of the year, Russia has sold 22 tonnes to finance its budget deficit. As a result, the country’s gold reserves have fallen to 2,304 tonnes.

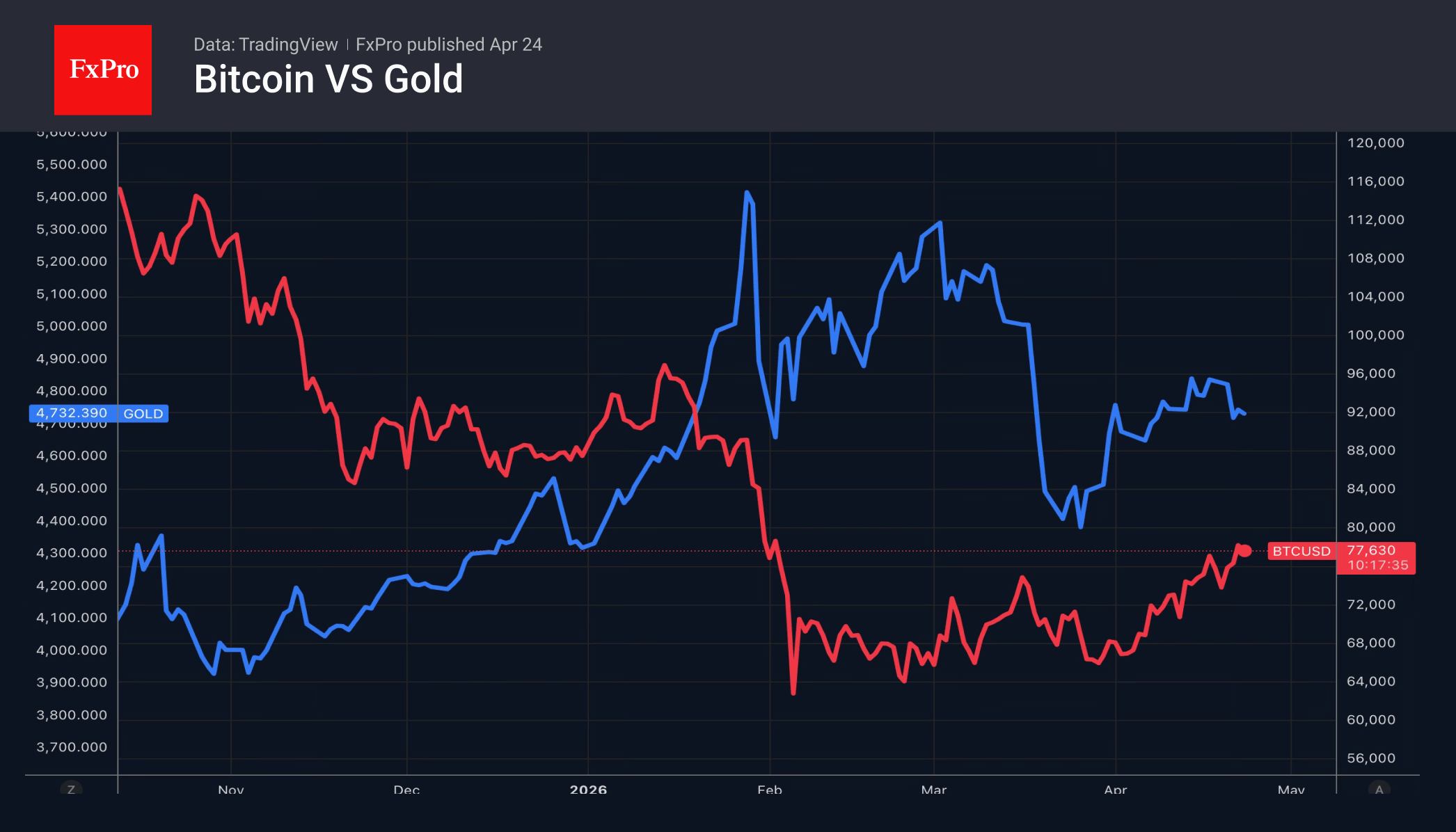

Cryptocurrency

Improved global risk appetite and new record highs for US stock indices have breathed new life into Bitcoin. Prices have reached their highest levels since late January, and the upward momentum stands a good chance of continuing following Donald Trump’s announcement of an indefinite extension of the ceasefire. Investors have concluded that the peak of the conflict escalation has passed and have begun buying risky assets.

Geopolitics has helped Bitcoin outperform gold. The precious metal has lost around 10% of its value since the start of the bombing of Iran, whereas the cryptocurrency has risen by 15%. In recent days, Bitcoin has frequently ignored the bad news and focused solely on the good. This points to ‘bullish’ sentiment in the market.

The most steadfast Bitcoin supporters have come out on top. For instance, Michael Saylor’s Strategy has been to buy up tokens despite the price decline. By the end of the week on the 19th of April, it had acquired $2.54 billion worth of digital assets. This is the largest purchase since November 2024.

What next?

Markets are tired of geopolitics and will be keen to see how central banks respond to the first signs of rising inflation caused by the conflict in the Middle East and high oil prices. Japan, Canada, the UK and the eurozone will announce their interest rate decisions. Although no changes to monetary policy are expected, investors will be watching closely for ‘hawkish’ signals.

Central banks face a difficult choice. Accelerating inflation requires them to raise rates, whilst slowing economic growth calls for a loosening of monetary policy. Most likely, the ECB and other regulators will keep the door open to monetary tightening and continue to monitor developments in the Middle East.

In the meantime, Donald Trump never tires of talking about negotiations. If investors once again believe the US president, the fall in EURUSD risks coming to a halt.

Markets will not overlook the story of Congress’s consideration of Kevin Warsh’s nomination for the post of Fed Chair. The new central bank chief’s appointment may be delayed due to opposition from some Republicans.

Dollar Gaining Ground, Mirroring the 2022 Pattern

- The US dollar is gaining amid persistent inflationary risks.

- Traders are betting on the ECB’s 2022 playbook, selling the euro.

The US dollar has strengthened over five of the last six sessions, driven by increased demand for safe-haven assets and investor confidence that the US economy will fare better than the rest of the world. Purchasing Managers’ Indexes showed clear signs of stagflation, with price indices rising, while overall business activity is slowing. Meanwhile, the European PMI fell to a 17-month low.

According to Joachim Nagel, Donald Trump’s attacks on the Fed are fuelling mistrust in American institutions and a flight from US assets and the dollar. He cited a 2025 Bundesbank study that found that the president’s pressure on the central bank led to rising inflation expectations, lower Treasury bond yields, and a weaker dollar.

Unsurprisingly, Donald Trump’s threats to sack Jerome Powell if he remained in the FOMC after his term as chair expired put pressure on the greenback. However, the growing risks of a renewed escalation of the conflict in the Middle East triggered the opposite process. Instead of fleeing the US, investors are actively buying up American assets. They believe that the US economy will fare better than the rest of the world.

Traders are following the 2022 pattern, when Europe, weighed down by the energy crisis, was unable to offer any resistance to the US, and the EURUSD fell below parity. Not least, this was a consequence of the ECB’s slower response to rising inflation. The Fed began raising rates in March, while the European Central Bank only followed suit in July.

This time, Christine Lagarde and her team intend to act decisively. Bloomberg experts do not expect the ECB to tighten monetary policy in April. However, at the upcoming meeting, the Governing Council is certain to signal its readiness to raise rates.

Meanwhile, the USDJPY’s approach to the psychologically significant 160 mark has triggered a fresh wave of verbal interventions. Finance Minister Satsuki Katayama stated that officials are in close contact with their American counterparts around the clock to counter speculators weakening the yen. The authorities have sufficient funds to counter them.

Gold Falls Nearly 3.0% Over the Week Amid Geopolitical Pressure

On Friday, the price of gold remained below 4,700 USD per ounce. For the week, the price is expected to decline by approximately 3.0%, as escalating tensions between the US and Iran over the Strait of Hormuz support rising energy prices and heighten concerns about inflation.

Both sides are maintaining their blockades of this strategically vital waterway, with peace talks showing little progress.

US President Donald Trump said on social media on Thursday that he had ordered the US Navy to target and destroy any vessels laying mines in the strait. US troops also boarded a supertanker carrying Iranian oil in the Indian Ocean.

Meanwhile, the truce between the US and Iran has been extended indefinitely, as Washington awaits a new formal proposal from Tehran. The truce between Israel and Lebanon has also been prolonged for three weeks.

High energy prices are reinforcing inflation risks and strengthening expectations of potential interest rate hikes by central banks. Collectively, these factors are weighing on gold, reducing its appeal as a non-yielding asset.

Technical Analysis

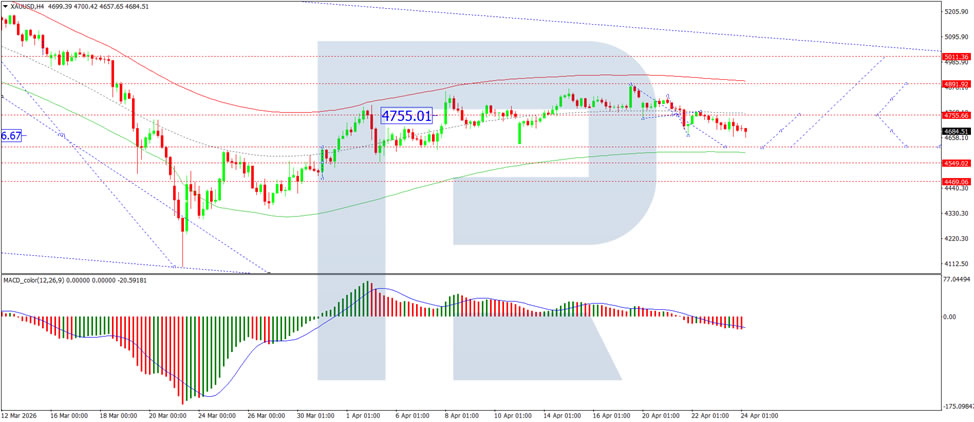

On the H4 XAU/USD chart, gold is trading within a consolidation range around the 4,685 USD level. An upside breakout could push prices towards 4,755 USD, while a downside break could lead to a decline towards 4,616 USD. The MACD indicator confirms the current downside momentum, with its signal line below the centre line and pointing firmly downwards.

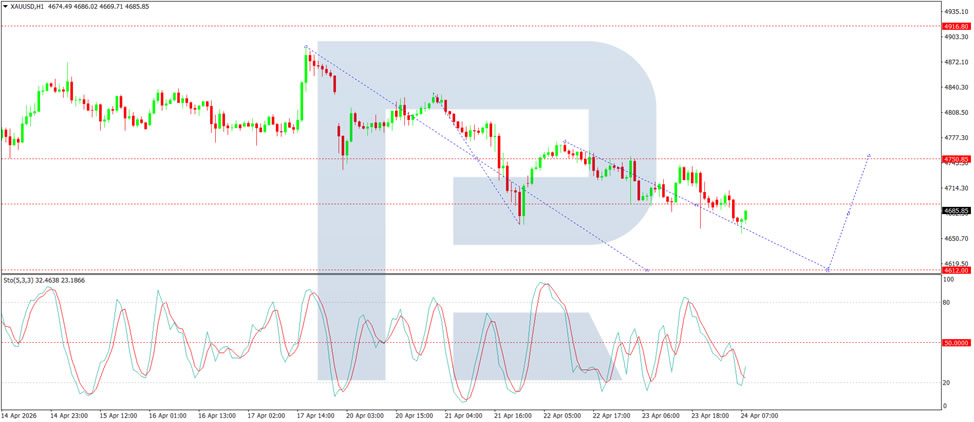

On the H1 chart, gold has broken below the 4,693 USD level and continues to move lower towards 4,616 USD. A corrective rebound towards 4,750 USD (testing from below) is likely, followed by a possible decline to 4,690 USD. The Stochastic oscillator supports this scenario, with its signal line below 50 and pointing firmly downwards towards 20.

Conclusion

Gold is poised to close the week nearly 3.0% lower amid ongoing geopolitical tensions between the US and Iran, which continue to dominate market sentiment. Both sides maintain their blockades of the Strait of Hormuz, while peace talks show little progress. President Trump's stance, ordering the Navy to destroy mines and board an Iranian oil tanker, has kept energy prices elevated and inflation concerns firmly in focus. Although truces with Iran and Lebanon have been prolonged, the lack of meaningful progress towards a resolution continues to weigh on gold. With central banks potentially leaning towards rate hikes amid persistent inflation, the non-yielding metal faces a challenging environment. Technical indicators suggest further downside towards 4,616 USD in the near term.