Sample Category Title

Easing Inflation Worries Despite Robust Sales Data

The market mood got a further boost yesterday after the latest data release from he US hinted that the economy is not doing that bad, after all. The retail sales rose 1% in July, more than expected by analysts, the initial jobless claims rose less than expected last week while NY Empire State and Philadelphia Fed manufacturing indices were mixed and didn’t attract much attention. Walmart, on the other hand, gave support to the positive vibes as the retailer did better than the estimates in Q2 and raised its FY revenue forecast on expectation that wealthier households will join the low-income segment in chasing good deals at its stores. The combination of encouraging economic data and robust Walmart earnings gave hope to investors that the US economy won’t collapse, revived the hope of seeing the US economy soft-land, and eased the jumbo rate-hike bets for the Federal Reserve’s (Fed) September meeting. As such, the US 2-year yield rebounded past the 4% mark and the 10-year yield shortly rose to 3.95% but eased back to around 3.90%. The S&P 500 jumped 1.61%, Nasdaq 100 rallied almost 2.50% as did the Russell 2000 index. The US dollar index bounced higher from an almost ytd low and US crude regained the 200-DMA level, near $78pb level, with however little appetite due to the sluggish Chinese growth. The oil refineries’ profits in China fell by over 90% in the first half of the year compared to the same time last year. And even the tense geopolitical situation of the Middle East and the possibility of another escalation between Iran and Israel don’t cheer up oil investors enough to bet for a rise above the $80pb level.

Easing inflation worries despite robust sales data

Even though yesterday’s retail sales data came in strong, and as another proof that the US consumers continue to spend despite high rates, high prices and high credit card debt, there are signs that hint that inflationary pressures are easing. And this brings me back to Walmart. If Walmart thinks that its sales will grow more than they previously forecasted this year, its because the wealthier segments of the market are also looking for deals to counter inflation. Walmart said yesterday that it cut the prices of 7200 products last quarter to maintain its ‘competitive price gaps’ with its rivals. And other retailers like Target, Walgreens, Aldi and Ikea also said to have done the same: cut prices to bring the inflation-squeezed customers back to stores and back to spending. Reportedly, the American cardealers also increased their discounts to the highest levels in three years and restaurants are unfolding meal deals to offer more affordable solutions to boost their customers’ appetite in hope that once they’re in, they will want to spend on non-deal items as well.

The news point that the widespread frustration with inflation is putting downward pressure on prices and could lead to more relaxed monetary policies. And if the monetary easing happens without a severe economic slowdown, Mr. Powell and investors will get the soft-landing that they were dreaming of, which could eventually keep the stock markets in a good shape, although the rotation from the technology stocks to non-technology sectors will likely tame the upside potential in major indices as the past weeks’ selloffs came as a warning that the market is oversaturated, the valuations are high and investors naturally are pickier to jump in at historically high levels without the promise of giant gains. Still, note that the latest earnings season somehow eased worries that the AI investments may not lead to the kind of profits that the companies and investors were looking for.

Too sick to play

Alibaba posted a meagre 4% revenue gain and a 27% plunge in Q2 profit. The cloud business showed a disenchanting 5.9% growth – compared to around 30% growth posted by the cloud segments of the US peers. Alibaba shares were flat in New York and gained 4% in Hong Kong, probably as the share buyback program helped countering the gloomy quarterly results. Its competitor JD.com jumped more than 4%, on the other hand, after its earnings beat expectations. But sales, there, grew just 1.2% in Q2. The numbers look too weak to take the China risks.

More broadly, things are not going well in China as you may have noticed. The fiscal and monetary stimulus measures can’t fuel growth. Investments grew slower than expected in July, the production disappointed while the property crisis continues in full swing: the prices of homes continue to fall. As such, not only the Chinese CSI 300 doesn’t benefit from a rebound in the developed markets, but the country’s biggest steelmaker Baowu Steel Group warned of the worst downturn since 2015. No wonder the iron ore prices continue to melt and Wisdomtree’s industrial metals ETF has given away almost all gains from May to July rebound. Copper futures also see resistance near the 200-DMA. The reflation trade on metals is not appetizing when China is too sick to play.

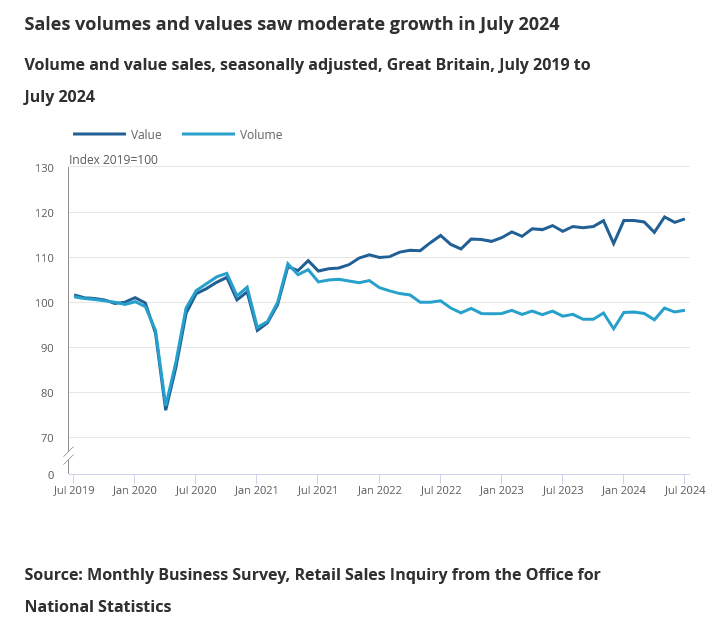

UK retail sales rises 0.5% mom in Jul, vs exp 0.6% mom

UK retail sales volumes rose by 0.5% mom in July, slightly below market expectations of 0.6% increase. On a broader scale, sales volumes in the three months leading up to July saw a 1.1% rise compared to the previous three months ending in April.

Breaking down the data, non-food stores—which include department, clothing, household, and other non-food stores—saw a notable 1.4% increase in sales volumes. Non-store retail sales, which encompass online and other forms of retail not conducted in physical stores, rose by 0.7%, driven primarily by a rebound in retailers other than mail order services. However, the overall growth was tempered by a -1.9% decline in automotive fuel sales volumes.

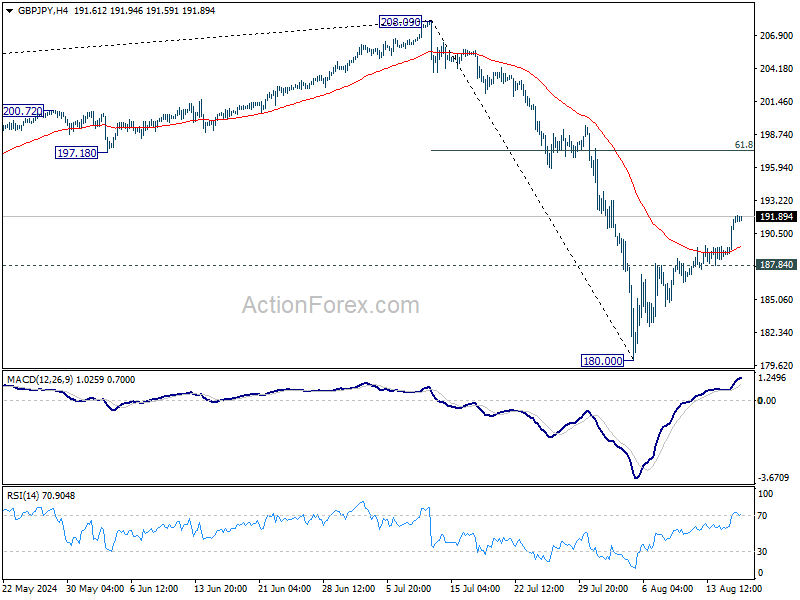

GBP/JPY Daily Outlook

Daily Pivots: (S1) 189.77; (P) 190.89; (R1) 193.02; More...

Intraday bias in GBP/JPY remains on the upside at this point. Fall from 208.09 should have completed at 180.00 already. Rebound from there is seen as the second leg of the corrective pattern from 208.09. Further rally should be seen to 61.8% retracement of 208.09 to 180.00 at 197.35, and possibly above. On the downside, however, break of 187.84 minor support will turn bias back to the downside for retesting 180.00 instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). Current development suggests that the first leg has completed and the range of medium term consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09.

Risk-On Sentiment Sweeps Markets, Weighs on Safe Haven Currencies

Yen, Swiss Franc, and to a lesser extent, Dollar are trailing at the bottom of the weekly currency performance chart. Strong risk-on sentiment has swept through the US markets, and the positive momentum continued in Asia. This shift in sentiment was ignited by better-than-expected US retail sales data overnight, which has significantly reduced fears of a US recession, lowering the likelihood that Fed will feel compelled to deliver an aggressive rate cut at its upcoming September meeting.

In contrast, British Pound has emerged as the strongest performer of the week. Recent economic data has reinforced BoE's cautious stance, suggesting that a rate cut at the next meeting is far from certain. Australian Dollar is following closely behind, supported by RBA's consistent messaging that a near-term rate cut is premature. Euro also shows strength, ranking as the third strongest currency this week, while Canadian Dollar and New Zealand Dollar hold the middle ground.

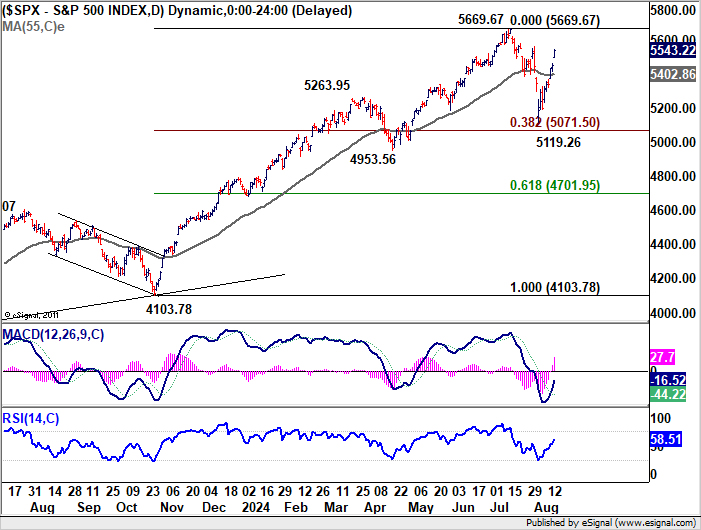

Technically, S&P 500's strong rally this week confirms that pull back from 5669.67 has completed at 5119.26 already. But beware that there might be strong resistance from 5669.67 ahead to limit upside. Consolidation from there could still extend with one more down leg, and through 55 D EMA. But in this bearish case, strong support should be seen from 38.2% retracement of 41.03.78 to 5669.67 at 5071.50 to contain downside to complete the corrective pattern.

In Asia, at the time of writing, Nikkei is up 3.00%. Hong Kong HSI is up 1.77%. China Shanghai SSE is up 0.10%. Singapore Strait Times is up 1.07%. Japan 10-year JGB yield is up 0.0482 at 0.886. Overnight, DOW rose 1.39%. S&P 500 rose 1.61%. NASDAQ rose 2.34%. 10-year yield rose 0.0106 to 3.926.

RBA's Bullock dismisses near-term rate cut expectations

In her remarks to the House of Representatives' economics committee, RBA Governor Michele Bullock emphasized the careful balancing act in managing inflation while minimizing harm to the labor market. Bullock reiterated that the Board believes current monetary policy is "sufficiently restrictive" to bring inflation down over a reasonable timeframe without causing undue damage to employment.

Despite financial markets anticipating a rate cut by the end of the year, Bullock was clear in her message that it is "premature to be thinking about rate cuts" at this stage. She pointed out that inflation remains too high and, in underlying terms, is not expected to fall back within the target range until the end of next year.

While acknowledging that economic circumstances could change, Bullock firmly stated that, based on the current outlook, the Board "does not expect that it will be in a position to cut rates in the near term."

RBNZ confident in inflation outlook, emphasizes measured approach to further rate cuts

In a speech today, RBNZ Governor Adrian Orr expressed a "very strong level of confidence" that forward indicators are pointing to a return to low and stable inflation, within the target range of 1% to 3%. Orr emphasized the importance of keeping inflation expectations and pricing intentions "anchored" as the central bank continues to monitor economic conditions.

Assistant Governor Karen Silk, speaking in a separate interview, noted that RBNZ is observing a continued decline in price and wage-setting behaviors. Silk mentioned that if this adjustment occurs more rapidly than anticipated, it could open the door for the central bank to consider a different, potentially faster path for rate cuts.

Earlier this week, RBNZ lowered the OCR by 25 bps to 5.25% and projected that it would fall below 4% by the end of 2025. Silk reiterated that RBNZ is taking a "measured approach" to policy loosening and remains committed to a data-dependent strategy.

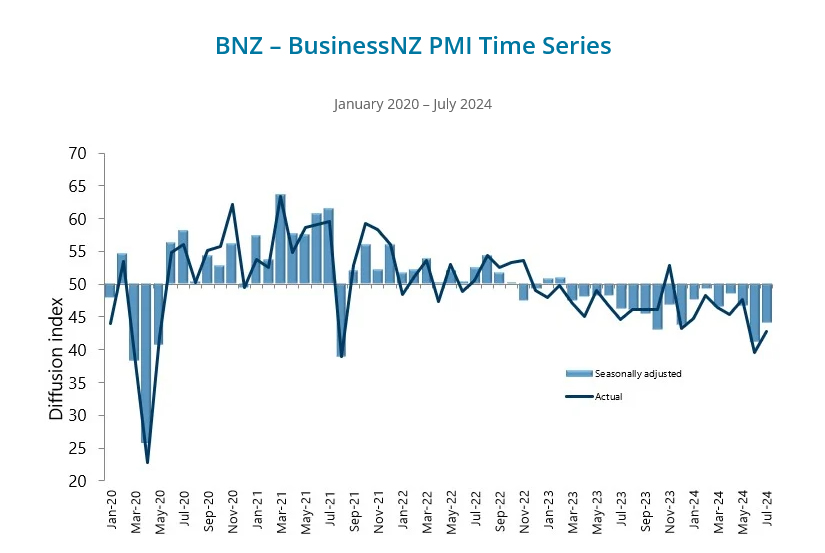

New Zealand BNZ manufacturing rises to 44, 17th month of contraction

New Zealand's manufacturing sector showed a slight improvement in July, with the BusinessNZ Performance of Manufacturing Index rising from 41.2 to 44.0. Despite this rebound, the sector remains deeply entrenched in contraction, marking its 17th consecutive month below the expansion threshold. The current level is still significantly below the long-term average of 52.6.

Breaking down the data, production saw an uptick, increasing from 35.7 to 43.4, while new orders also rose, moving from 39.0 to 42.5. However, employment in the sector continued to decline, slipping from 44.0 to 43.1. Finished stocks decreased from 47.7 to 46.5, and deliveries fell slightly from 44.8 to 44.3.

Despite the relative improvement in activity, the proportion of negative comments from respondents remained high, though it eased slightly to 71.1% in July from 76.3% in June. Businesses cited ongoing issues such as a lack of orders, customers, and sales, which have been persistent concerns in recent months.

BNZ's Senior Economist Doug Steel commented that "manufacturing activity will turn when the broader economy turns." He added that easing monetary conditions, including a lower OCR, could help stimulate a general pick-up in sales, but emphasized that this recovery would take time.

Looking ahead

UK retail sales and Eurozone trade balance are the main features in European session. Later in the day, Canada will release manufacturing sales. US will publish building permits and housing starts, and U of Michigan consumer sentiment.

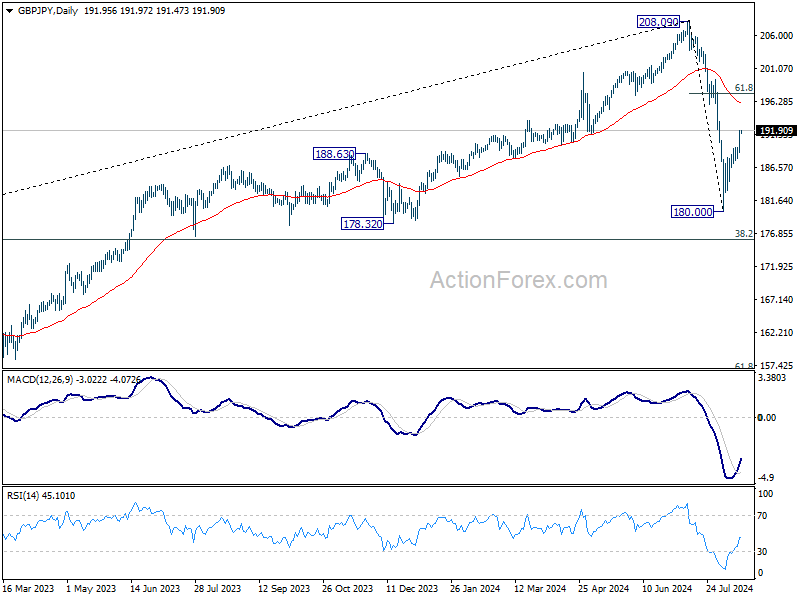

GBP/JPY Daily Outlook

Daily Pivots: (S1) 189.77; (P) 190.89; (R1) 193.02; More...

Intraday bias in GBP/JPY remains on the upside at this point. Fall from 208.09 should have completed at 180.00 already. Rebound from there is seen as the second leg of the corrective pattern from 208.09. Further rally should be seen to 61.8% retracement of 208.09 to 180.00 at 197.35, and possibly above. On the downside, however, break of 187.84 minor support will turn bias back to the downside for retesting 180.00 instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). Current development suggests that the first leg has completed and the range of medium term consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Jul | 44 | 41.1 | 41.2 | |

| 22:45 | NZD | PPI Input Q/Q Q2 | 1.40% | 0.50% | 0.70% | |

| 22:45 | NZD | PPI Output Q/Q Q2 | 1.10% | 0.60% | 0.90% | 0.80% |

| 04:30 | JPY | Tertiary Industry Index M/M Jun | -1.30% | 0.30% | -0.40% | 0.60% |

| 06:00 | GBP | Retail Sales M/M Jul | 0.80% | -1.20% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jun | 14.5B | 12.3B | ||

| 12:15 | CAD | Housing Starts Jul | 245K | 242K | ||

| 12:30 | CAD | Manufacturing Sales M/M Jun | -2.50% | 0.40% | ||

| 12:30 | USD | Building Permits M/M Jul | 1.44M | 1.45M | ||

| 12:30 | USD | Housing Starts M/M Jul | 1.34M | 1.35M | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Aug P | 67.3 | 66.4 |

Cliff Notes: Labour Market Critical to the Medium-Term Outlook

Key insights from the week that was.

In Australia, the week started on a slightly more positive note for consumers, with our Westpac-MI Consumer Sentiment Index showcasing a 2.8% bounce to 85.0 in August. The primary support was a significant improvement in households’ views and expectations around their finances, likely associated with the new financial year’s tax cuts. The sub-indexes tracking ‘family finances vs a year ago’ and ‘family finances next 12 months’ rose 11.7% and 5.1% respectively. These gains are coming off an incredibly weak base however, and given earlier surveys indicated a preference among consumers to rebuild savings buffers from their tax cut, it is understandable we are yet to see a signification improvement in card spending or intentions to ‘buy a major item’.

It is constructive to see that consumers also remain relatively untroubled over the outlook for jobs – a perspective that was certainly supported by July’s labour market data. Growth in employment was far stronger than expected, with nearly 60,000 jobs created in July after a solid run of gains over recent months. However, the main surprise was around labour supply, as evinced by the surge in labour force participation to a cycle high of 67.1%, the highest read in over a century. It was impressive to see businesses absorb such a large portion of this growth via employment; but in the end, the surge in labour supply was enough to see the unemployment rate lift to 4.2%, incrementally adding slack.

Conditions from an income perspective also remain constructive. The wage price index lifted 0.8% (4.1%yr) in Q2. Containing inflation risks, nominal wage growth has undergone a significant moderation on a six-month annualised basis, from 4.7%yr in December to 3.4%yr at June as the labour market moves into balance. Though, with annual inflation having slowed more than wage growth, consumers are slowly beginning to feel the cost of living pressures they have been experiencing let up. In time, this should support a further improvement in family finance expectations and spending.

As Westpac Chief Economist Luci Ellis and Senior Economist Pat Bustamante noted earlier this week, one of the more puzzling elements of the RBA’s revised forecasts is the assertion that aggregate supply is lower than previously thought. As above, this week’s labour force update instead highlighted continued strength in labour supply. In today’s essay, Chief Economist Luci Ellis elaborates on what the latest data implies for the RBA’s view on productivity and activity.

First stop offshore this week is New Zealand. There the RBNZ surprised the market by cutting the cash rate 25bps to 5.25%. As detailed by Westpac NZ Economics, the RBNZ also lowered the OCR track significantly, implying another cut will occur at the October Monetary Policy Review and a total of 75bp of cuts will be delivered by end-2024. The RBNZ’s updated profile also suggests the RBNZ still aims to reach neutral OCR levels circa 3% by 2027, but now more quickly. Warranting the revised view on interest rates, the RBNZ’s near-term forecasts for economic growth have been revised down significantly. A wider output gap and looser labour market provides confidence inflation will ultimately fall back to the 2%yr mid-point of the target range, though this is not currently expected until Q2 2026.

The US data flow meanwhile continued to point to a goldilocks economy: benign inflation paired with robust activity growth. Consumer prices gained 0.2% in July, seeing annual inflation edge lower to 2.9%yr and 3.2%yr respectively for headline and core inflation. Food away from home and services ex-shelter were both benign, signalling wage pressures are not a concern and that the discretionary demand pulse is modest. Core goods prices meanwhile exhibited broad-based and persistent weakness. While shelter surprised to the upside in July, with the labour market cooling and households financially constrained, this momentum is highly unlikely to persist; indeed, the BLS' real-time measures of rents point to flat or negative outcomes versus shelter's near-5% annualised pace in July. Earlier in the week, the PPI was also constructive for the inflation outlook, rising 2.2%yr in July, undershooting expectations.

Retail sales subsequently showed strength in July, gaining 1.0% thanks to a strong rebound in autos (sales ex autos were up +0.4%, and the narrower control group +0.3%). In the year-to-date, nominal gains have been modest overall, the control group averaging a monthly gain of 0.3%, but that is a result consistent with real consumption growth modestly below trend, not recession. Of the other US data out this week, the regional Fed manufacturing surveys were weak, but initial claims continued to point to an absence of firing across the economy.

Across the Atlantic, UK data justified the Bank of England continuing with their policy easing, albeit while remaining confident in economic growth’s upturn. The July CPI print surprised to the downside, prices falling 0.2%mth. Base effects saw annual headline inflation edge up from 2.0%yr to 2.2%yr, but annual core inflation slowed from 3.5% to 3.3%. Inflation’s breadth also continued to narrow, with only 54% of the basket now growing in excess of the BoE’s annual inflation target of 2.0%, down from 86% this time last year. Helpfully for the BoE’s risk assessment and messaging, annual services inflation came in well below expectations in July, decelerating from 5.7% to 5.2% (consensus 5.5%yr). Earlier in the week, wages ex. bonus also softened to 5.4%yr in June from 5.7% in May, giving the BoE more confidence to persist with their cutting cycle.

Like in the US, UK activity data remains constructive, GDP growth printing as expected in Q2, at 0.6% (0.9%yr). That said, the detail highlighted a greater degree of downside risks, with private consumption and business investment both weak. Consumption gained just 0.2%, half Q1's 0.4% gain and the Q2 consensus expectation of 0.5%. Investment meanwhile declined 0.1% instead of rising 0.4% as expected. Government spending offset, gaining 1.4% in Q2.

Turning finally to Asia. Japanese GDP surprised to the upside in Q2, the 0.8% gain offsetting Q1's 0.6% decline. Private consumption was the primary support for growth in the quarter, increasing 1.0%. Business investment was similarly robust, up 0.9%. Chinese partial data, in contrast, disappointed again in July. At 5.9%ytd and 3.5%ytd respectively, industrial production and retail sales growth showed no progress from June. And fixed asset investment weakened further, year-to-date growth decelerating to 3.6% from 3.9%, as property investment’s contraction accelerated, from –9.9%ytd to –10.2%ytd, and momentum in the strong sub-sectors of high-tech manufacturing and utilities moderated. Adding further pessimism to the view for housing and consumption, new and existing home prices fell another 0.7% and 0.8% in July. There is clearly need for additional policy support into year-end; to boost sentiment, authorities next steps have to take a more active approach and be immediate for consumers and the property sector.

RBA’s Bullock dismisses near-term rate cut expectations

In her remarks to the House of Representatives' economics committee, RBA Governor Michele Bullock emphasized the careful balancing act in managing inflation while minimizing harm to the labor market. Bullock reiterated that the Board believes current monetary policy is "sufficiently restrictive" to bring inflation down over a reasonable timeframe without causing undue damage to employment.

Despite financial markets anticipating a rate cut by the end of the year, Bullock was clear in her message that it is "premature to be thinking about rate cuts" at this stage. She pointed out that inflation remains too high and, in underlying terms, is not expected to fall back within the target range until the end of next year.

While acknowledging that economic circumstances could change, Bullock firmly stated that, based on the current outlook, the Board "does not expect that it will be in a position to cut rates in the near term."

RBNZ confident in inflation outlook, emphasizes measured approach to further rate cuts

In a speech today, RBNZ Governor Adrian Orr expressed a "very strong level of confidence" that forward indicators are pointing to a return to low and stable inflation, within the target range of 1% to 3%. Orr emphasized the importance of keeping inflation expectations and pricing intentions "anchored" as the central bank continues to monitor economic conditions.

Assistant Governor Karen Silk, speaking in a separate interview, noted that RBNZ is observing a continued decline in price and wage-setting behaviors. Silk mentioned that if this adjustment occurs more rapidly than anticipated, it could open the door for the central bank to consider a different, potentially faster path for rate cuts.

Earlier this week, RBNZ lowered the OCR by 25 bps to 5.25% and projected that it would fall below 4% by the end of 2025. Silk reiterated that RBNZ is taking a "measured approach" to policy loosening and remains committed to a data-dependent strategy.

New Zealand BNZ manufacturing rises to 44, 17th month of contraction

New Zealand's manufacturing sector showed a slight improvement in July, with the BusinessNZ Performance of Manufacturing Index rising from 41.2 to 44.0. Despite this rebound, the sector remains deeply entrenched in contraction, marking its 17th consecutive month below the expansion threshold. The current level is still significantly below the long-term average of 52.6.

Breaking down the data, production saw an uptick, increasing from 35.7 to 43.4, while new orders also rose, moving from 39.0 to 42.5. However, employment in the sector continued to decline, slipping from 44.0 to 43.1. Finished stocks decreased from 47.7 to 46.5, and deliveries fell slightly from 44.8 to 44.3.

Despite the relative improvement in activity, the proportion of negative comments from respondents remained high, though it eased slightly to 71.1% in July from 76.3% in June. Businesses cited ongoing issues such as a lack of orders, customers, and sales, which have been persistent concerns in recent months.

BNZ's Senior Economist Doug Steel commented that "manufacturing activity will turn when the broader economy turns." He added that easing monetary conditions, including a lower OCR, could help stimulate a general pick-up in sales, but emphasized that this recovery would take time.

Skating to Where the Puck Used to Be

Data revisions have partly undercut the RBA's narrative of lower aggregate supply than expected. The RBA will need to skate to where the labour market is going to go, not where it used to be.

Recent events have not materially changed our view about the outlook for the Australian economy. Recent communication from the RBA has, however, changed our minds about how the RBA is seeing things and how it will respond to the data. While it is still possible that the RBA Board will change its mind, RBNZ-style, and pivot sooner than our current base-case expectation, we suspect that fast backflips are not in the RBA’s breakdancing repertoire.

Recall our earlier observation that the RBA had concluded that the labour market was tighter than it had previously thought, even though all bar one of the indicators in its labour market dashboard eased between May and August.

Deputy Governor Hauser’s speech earlier in the week addressed this to some extent. The upshot of the speech is that, because inflation has recently overshot the RBA’s earlier forecasts, it must be that demand is stronger than it thought, or supply is weaker, or a combination of the two. As Westpac Economics colleague Senior Economist Pat Bustamante and I noted earlier this week (PDF 427KB), though, the net surprise on the June quarter 2024 trimmed mean inflation forecasts since the RBA’s November forecast round was in fact roughly zero. In some respects, the RBA is seeking to explain the forecast miss for the September quarter 2023. We are now halfway through the September quarter 2024.

We are reminded of the famous quote from ice hockey legend Wayne Gretsky, to ‘skate to where the puck is going, not to where it has been’. Inferring a lower level of aggregate supply currently from a forecast miss that mainly happened a year ago feels a bit like skating to where the puck used to be quite a while ago.

Yesterday’s labour force results highlighted how quickly that puck can move. As Westpac Economics colleague Economist Ryan Wells reported, the labour force participation rate in July was the highest recorded in more than a century. This represents a significant boost to labour supply.

In addition, following up on a key point of Pat’s and my note, the re-benchmarking of quarterly hours worked reported in the July labour force release also works against the RBA’s thesis of weak productivity dragging on supply. Recall that the RBA revised down its forecast for year-ended productivity growth in the June quarter by a full percentage point between its May and August forecast rounds. As far as we can tell, this was largely because of an outsized reading for June quarter hours worked.

The re-benchmarking changed the story considerably. Growth in total hours worked was previously reported as 0.4% over the year to the June quarter (0.2% for non-farm hours, which is more relevant to the measure of productivity in the RBA forecasts). Each of the quarters in that year has been revised down at least a little. Hours worked are now reported to have been essentially flat compared with a year previously (and –0.2% for non-farm).

This 0.4 percentage point revision in hours worked over the year eliminates a considerable fraction of the rationale for the RBA’s downward revision to its forecast for productivity growth. Even a small upside surprise on June quarter GDP growth, or revisions to recent history, would close the gap further.

Flat hours worked in the face of a strong rise in the number of people participating in the workforce does look a lot like growth in labour supply outstripping labour demand and building up some spare capacity.

It is no surprise that labour supply has been so strong. With the cost of living having risen so much, people need the extra work to earn more money. A separate (and more lagged) ABS release, the Labour Accounts, shows that the share of people with a second job has risen to new highs. This is an example of what economists call an ‘income effect’, where labour supply rises when real hourly wages fall. It stands in contrast to the ‘substitution effect’ of people working more when their hourly wage rises, because working is then more attractive relative to leisure.

If strong labour supply does indeed reflect people seeking more income, we might also see unusual labour market dynamics as this effect unwinds. Normally when labour demand softens, we see some combination of higher unemployment and higher underemployment. Over recent decades, the underemployment adjustment has become stronger relative to that in unemployment. Employers are increasingly using the ‘hours margin’ to adjust their labour demand, rather than laying people off entirely. The RBA knows this, and indeed the key paper describing this effect was co-authored by the newly appointed head of the RBA’s Economic Analysis department.

If the income effect has been the dominant driver of the recent rise in labour supply, then as inflation subsides and real incomes recover, we may see an ongoing softening in hours worked, with neither unemployment nor underemployment rising very much. If people no longer need the extra hours or the second job, they will not report themselves as seeking more hours, and so underemployed.

The implication is that it will be all too easy to misinterpret an easing labour market as still tight. In principle, the RBA’s full employment checklist should help guard against such misinterpretation. But seeing how one quarterly outcome for hours worked seems to have changed the RBA’s view on supply capacity, and so the inflation outlook, it is hard to be confident of this.

The RBA will need to skate to where the labour market is going to go, not where it used to be.

EURJPY Wave Analysis

- EURJPY broke resistance area

- Likely to rise to resistance level 164.90

EURJPY currency pair just broke the resistance area located between the resistance level 162.50 and the 61.8% Fibonacci correction of the earlier sharp downward impulse (c) from the end of July.

The breakout of this resistance area is aligned with the clear multi-month uptrend visible on the weekly EURJPY charts.

Given the strengthening of the bearish yen sentiment, EURJPY currency pair can be expected to rise further toward the next resistance level 164.90 (former low of wave (a) from the end of July).