Sample Category Title

BoJ Hikes, Microsoft Disappoints, Fed Decides

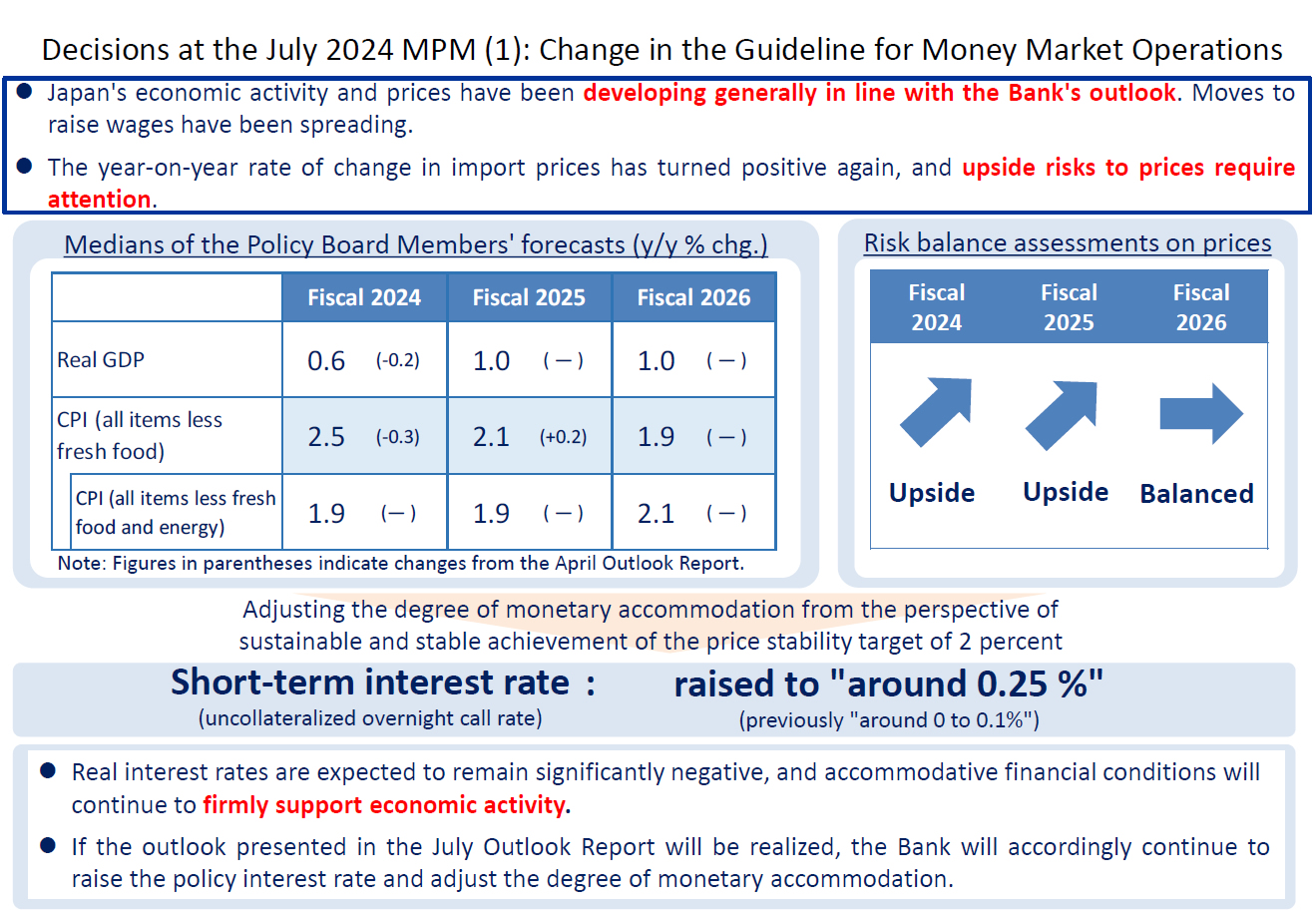

The Bank of Japan (BoJ) raised its rate to 0.25% as cautiously expected and announced that it will reduce the monthly bond purchases in a predictable manner – but allow enough flexibility to support stability in the JGB markets. More importantly, the language in the communique was quite bullish on prices. The BoJ officials said that ‘underlying CPI inflation is expected to increase gradually, since it is projected that the output gap will improve and that medium- to long-term inflation expectations will rise with a virtuous cycle between wages and prices continuing to intensify.’ The latter hinted that today’s rate hike is certainly not the BoJ’s last one. Now, all eyes are on BoJ Governor Ueda for further tips and hints. The 10-year JGP yield is pushing higher after the decision and the yen is in demand. Both the USDJPY and the EURJPY tested their 200-DMA to the downside, the GBPJPY extends and consolidates losses below the 200 mark, and there is reason to believe – with what we heard from the BoJ thus far today – that the policy will become less loose to support the Japanese yen in the medium to long run.

Across the Pacific, the Federal Reserve (Fed) also started its two-day policy meeting and will announce its decision later today. The Fed is not expected to make a change to its rates today, but is widely and wildly expected to hint at a September rate cut. Activity on Fed funds futures doesn’t only hint at a 100% chance for a rate cut to happen in September but it also shows that the doves are getting ahead of themselves with the assessment of a nearly 15% chance that the Fed could cut 50bp or more in September – which will obviously not happen unless there is a big crisis or stress on the financial markets. Therefore, the stretched Fed pricing is a sign that the Fed cut expectations went too far and that we shall see a correction even though the Fed hints strongly at a September cut today – with the risk of hardly upsetting the market if it does not.

The US 2-year yield remains on track for further weakness in the base case scenario of a hint for September cut, while the US 10-year yield consolidates near 4.13%, the US dollar is softer this morning, but the index remains in the bullish trend – above a major Fibonacci support to its ytd positive trend, as the rate cut bets elsewhere rise along with the Fed cut bets. In this context, the EURUSD tipped a toe below the 1.08 yesterday after a surprise slowdown in German growth casted shadow on a better-than-expected EZ GDP number. Inflation figures on the other hand were encouraging in Spain but less so in Germany. The aggregate EZ inflation figures are due later today. A sufficiently soft set of data should keep the European Central Bank (ECB) doves in charge of the market and not let the EURUSD gain too much strength in case we see a dollar rebound after the Fed decision.

Tensions and Franc

Note that the US long-term bonds and the dollar also benefit from some safe haven demand after an explosion in Beirut – following a Hezbollah attack on Israel during the weekend – escalate the geopolitical tensions in the Middle East and directs capital toward safe haven assets. In this context, gold extends gains above the $2400 level and the franc advances. The USDCHF is no longer on track to extend the ytd gains, on the contrary, the pair slipped below a key Fibonacci support back in mid-July, the major 38.2% Fibonacci retracement that stands 0.8885, and is now in the bearish consolidation zone. The tense geopolitical setup and softening Fed expectations explain the U-turn in the USDCHF. However, the global easing vibes will certainly encourage more interest rate cuts from the Swiss National Bank (SNB) this year, and should limit the USDCHF’s downside potential.

Inside tech

Beirut explosion, a swift flight to safety and a renewed selloff across the Big Tech stocks weighed on major US indices yesterday. The S&P500 fell 0.50% while Nasdaq 100 slid around 1.40%. Nvidia tumbled 7% to its 100-DMA. But, Nasdaq futures are in a better shape this morning following a 7.5% rally from AMD after raising its forecast for AI accelerators. Microsoft, on the other hand, didn’t blow anyone’s mind when it reported earnings yesterday. The overall revenue rose by a slightly better-than-expected 15%, but revenue from Azure, its cloud computing platform that’s the main growth engine, grew only 29%, down from 31% in the previous period. About 8 percentage points of that increase was due to AI, up from 7 percentage points, but it was not enough. The market first sent Microsoft shares 9% down, the price than recovered to settle with around 3% loss. Due today after the bell, Meta’s results will be important for those looking for hints that all that massive AI spending is bearing fruits. Meta had said last quarter that it needed to spend more on AI to get to a level of play that will generate revenue. Hopefully, that timeline doesn’t extend at this quarter’s announcement. Zuckerberg knows that investors’ patience is wearing thin as Meta trades some 15% below its July peak.

Bottom?

US crude tumbled to $75pb level yesterday, unable to recover from the negativeness of the sluggish Chinese growth. But the rising geopolitical tensions and a major decline of nearly 4.5-mio-barrels in the US oil inventories last week help to bring the dip buyers in near the $75pb level. I believe that we may have hit a bottom near the $75pb this week. And I also believe that the lower the prices will go the higher the chance of a delay from OPEC to exit its production cut strategy.

Note that I will be on holiday for the next two weeks. See you again in August!

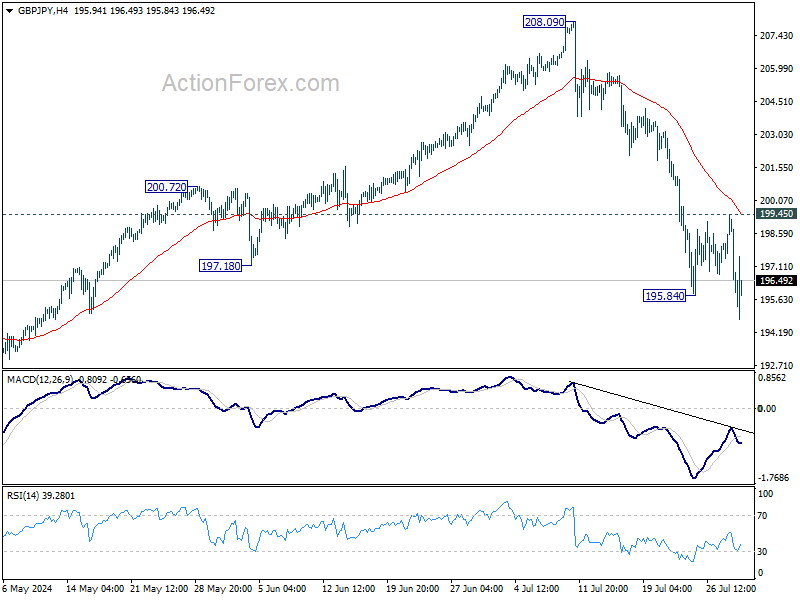

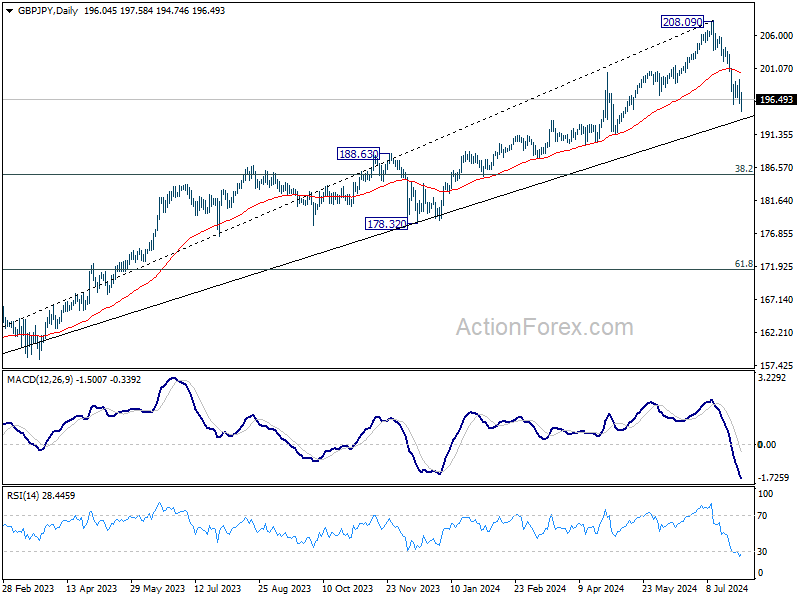

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.86; (P) 197.17; (R1) 198.37; More...

Intraday bias in GBP/JPY is back on the downside with breach of 195.84 temporary low. Fall from 208.09 is probably a larger scale correction and should target 185.49 fibonacci level. Nevertheless, on the upside, firm break of 199.45 resistance will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, considering bearish divergence condition in W MACD, 208.09 might be a medium term top and fall from there could already be correcting whole up trend from 148.93 (2022 low). Risk will now stay on the downside as long as 55 D EMA (now at 200.51) holds. Deeper fall would be seen to 38.2% retracement of 148.93 to 208.09 at 185.49.

Yen Up Slightly After BoJ Hike; Aussie Tumbles on Core Inflation Relief

Yen rose broadly today after the BoJ raised interest rates for the second time this year, and maintained hawkish bias. However, buying momentum has not been decisive. This lack of strong momentum can be attributed to the fact that the rate hike decision was likely well priced in by the markets. Nikkei's rebound following the announce further indicates that BoJ's move was anticipated. Additionally, traders remain cautious ahead of FOMC rate decision later today, where Fed might signal a rate cut in September.

In contrast, Australian Dollar tumbled broadly following release of quarterly CPI data. Markets and economists showed relief as the trimmed mean CPI slowed in Q2, which overshadowed the rise in headline CPI. The continued core disinflation provides RBA with some room to keep interest rates unchanged next week, avoiding the need for another rate hike.

Overall, Dollar is following Aussie as the second weakest currency of the day so far, with Loonie r trailing in third place. Swiss Franc has emerged as the strongest currency, followed by Yen and then Euro. British pound and Kiwi are positioned in the middle of the performance spectrum.

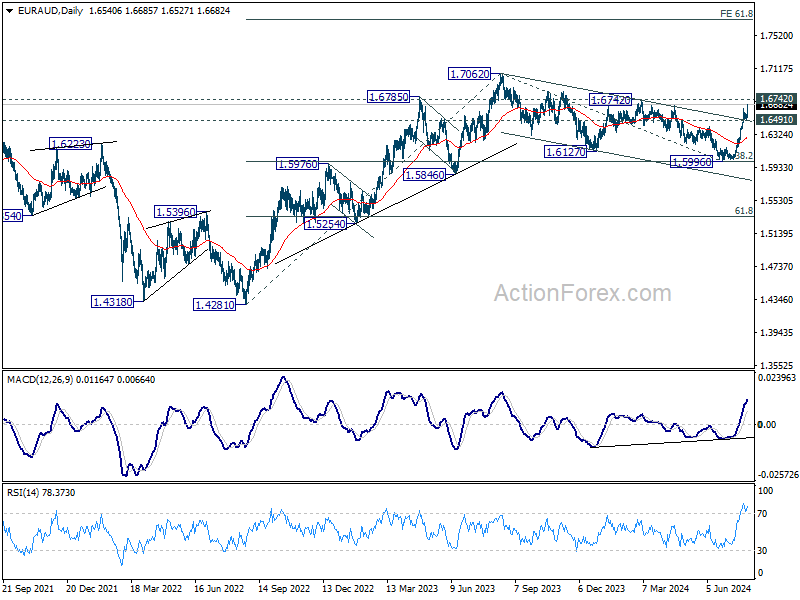

Technically, EUR/AUD's rally from 1.5996 resumed today and hits as high as 1.6685 so far. The bullish view remains intact, and correction from 1.7062 should have completed with three waves down to 1.5996. Further rise is expected as long as 1.6491 support holds. Decisive break of 1.6742 resistance will argue that larger up trend from 1.4281 (2022 low) is ready to resume through 1.7062 high.

In Asia, at the time of writing, Nikkei is up 0.03%. Hong Kong HSI is up 1.90%. China Shanghai SSE is up 1.75%. Singapore Strait Times is up 0.29%. Japan 10-year JGB yield is up 0.0533 at 1.050. Overnight, DOW rose 0.50%. S&P 500 fell -0.50%. NASDAQ fell -1.28%. 10-year yield fell -0.035 to 4.143.

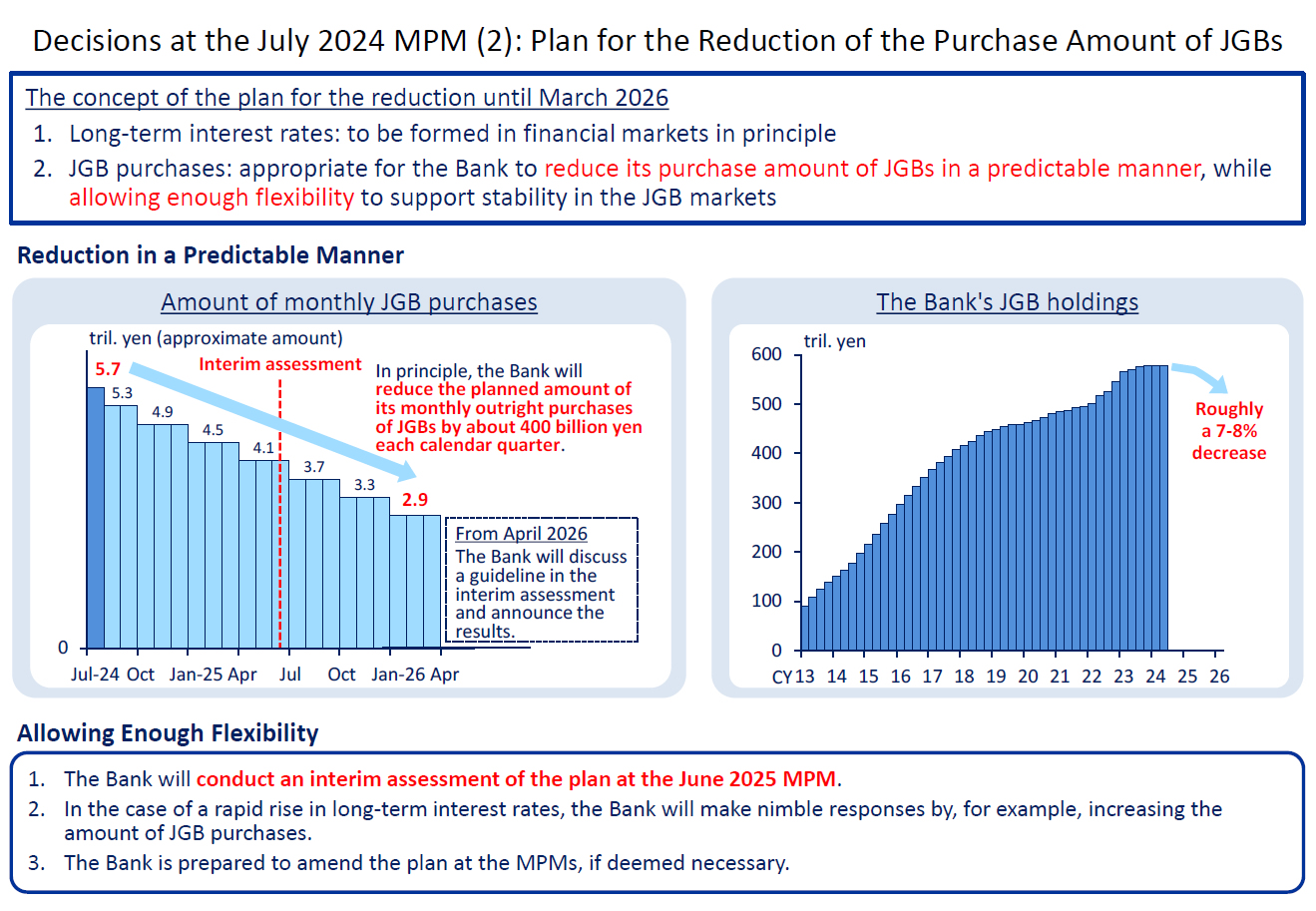

BoJ hikes to 0.25%, signals more increases if outlook realizes

BoJ raised the uncollateralized overnight call rate from 0-0.10% to around 0.25% today. The decision was made by a 7-2 vote, with dissenting votes from Toyoaki Nakamura and Asahi Noguchi, who preferred to gather more information and conduct a careful assessment before adjusting the interest rate.

Regarding JGB purchases, there was a unanimous decision to reduce the amount of monthly outright purchases to about JPY 3T by Q1 2026. The amount will be cut by JPY 400B each calendar quarter.

BoJ stated that economic activity and prices have been "developing generally in line with the Bank's outlook." Moves to raise wages have been spreading, and the annual rate of import price growth has "turned positive again," with upside risks to prices requiring attention.

It also noted if the outlook presented in the July Outlook Report is realized, BoJ will continue to raise the policy interest rate and adjust the degree of monetary accommodation accordingly.

In the new economic projections, the BoJ made several adjustments:

- Fiscal 2024 growth forecast was lowered from 0.8% to 0.6%.

- Fiscal 2025 growth forecast remains unchanged at 1.0%.

- Fiscal 2026 growth forecast remains unchanged at 1.0%.

For inflation projections:

- Fiscal 2024 CPI core forecast was lowered from 2.8% to 2.5%.

- Fiscal 2025 CPI core forecast was raised from 1.9% to 2.1%.

- Fiscal 2026 CPI core forecast remains unchanged at 1.9%.

- Fiscal 2024 CPI core-core forecast remains unchanged at 1.9%.

- Fiscal 2025 CPI core-core forecast remains unchanged at 1.9%.

- Fiscal 2026 CPI core-core forecast remains unchanged at 2.1%.

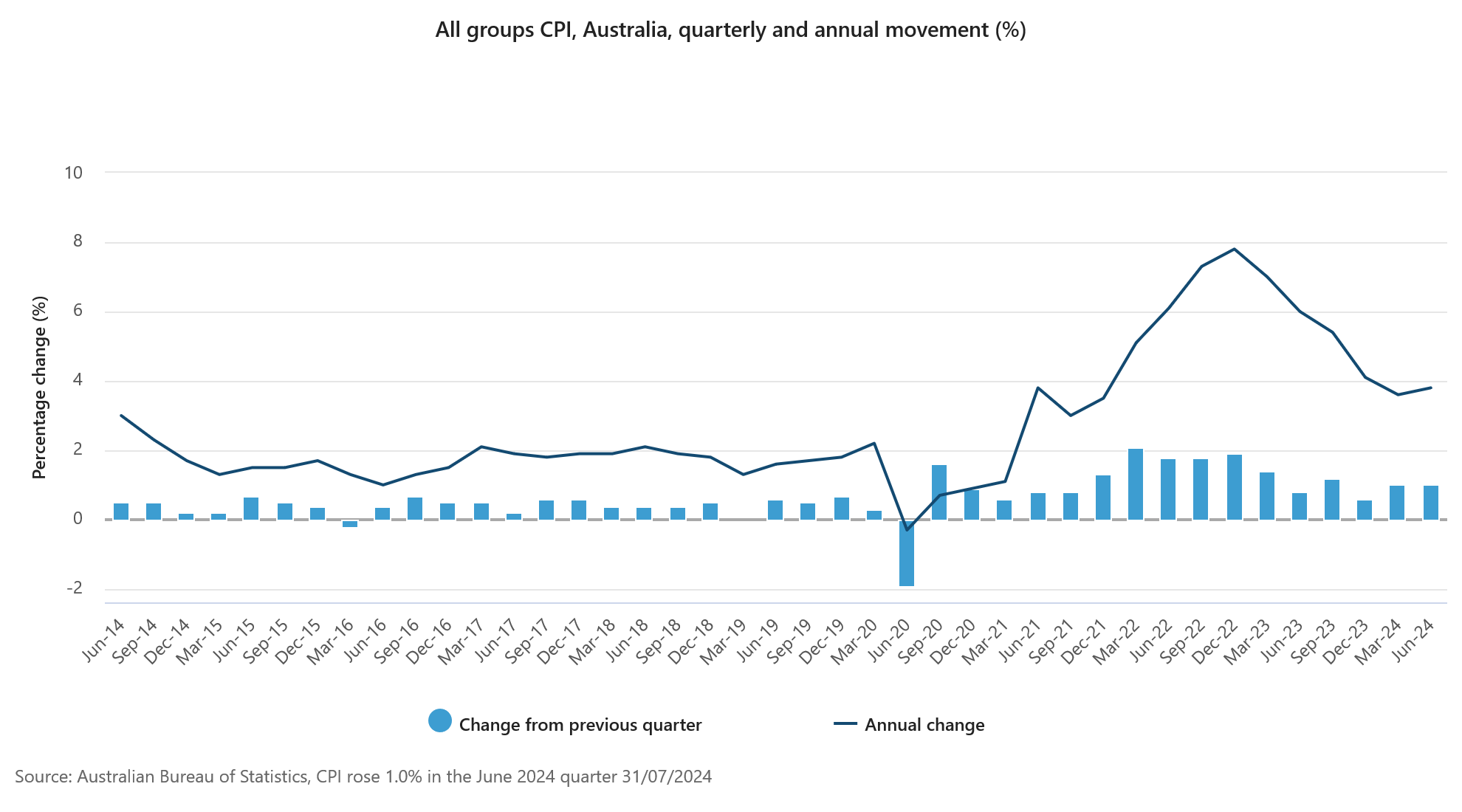

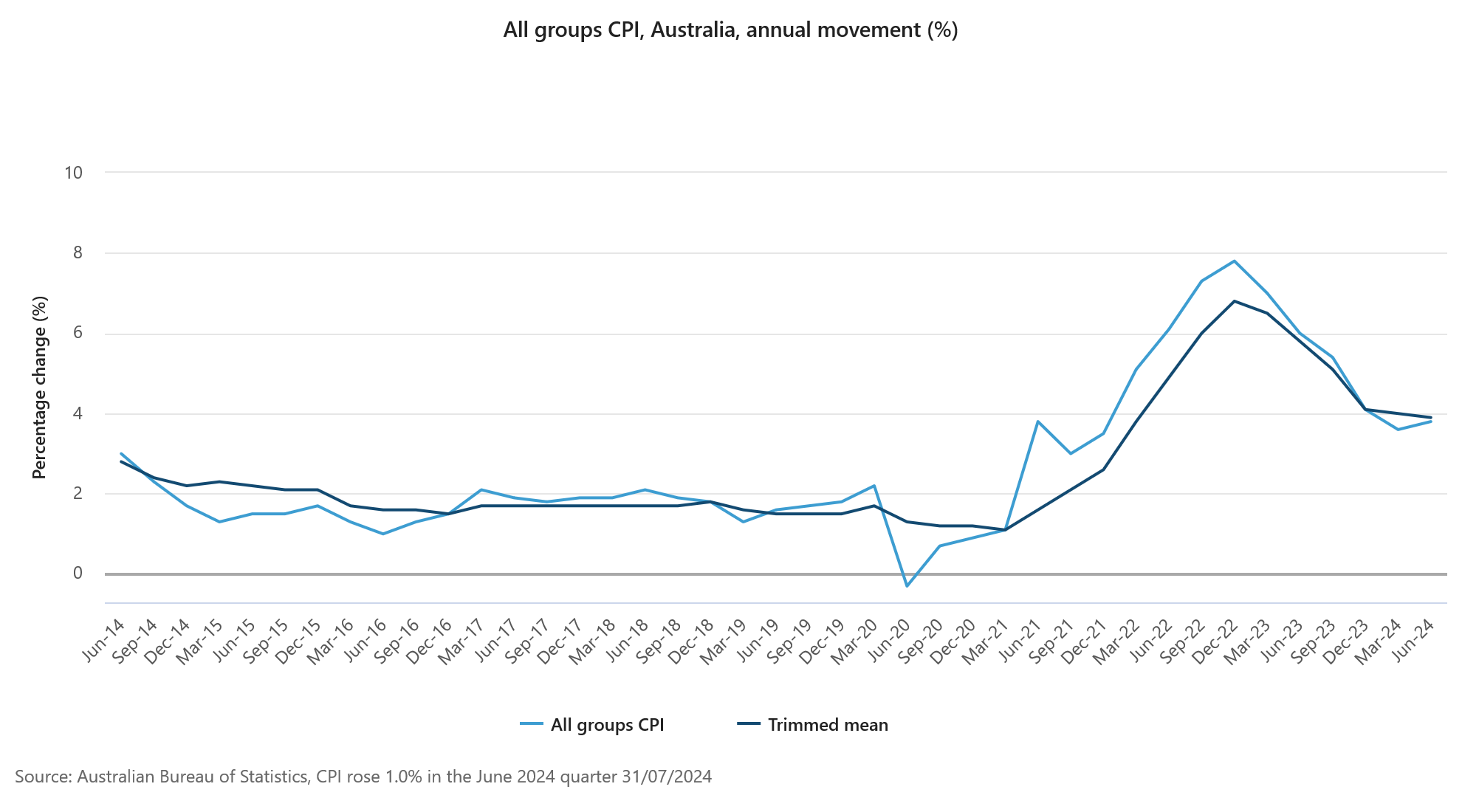

Australia's trimmed mean CPI drops to 3.9%, continuing six-quarter downtrend

In Q2, Australia's CPI rose by 1.0% qoq, matching both expectations and the pace set in Q1. Annual rate increased from 3.6% to 3.8% , also in line with forecasts.

More notably, the core inflation measure marked its sixth consecutive quarter of cooling. Trimmed mean CPI, which is a key indicator of underlying inflation, rose by 0.8% qoq. This represents a slowdown from the prior quarter's 1.0% qoq increase and falls below the expected 0.9% qoq. Annually, trimmed mean CPI slowed from 4.0% yoy to 3.9% yoy, below the expected 4.0% and continuing its downward trend from the peak of 6.8% in the December 2022 quarter.

Additionally, the monthly CPI for June slowed from 4.0% yoy to 3.8% yoy, again matching expectations.

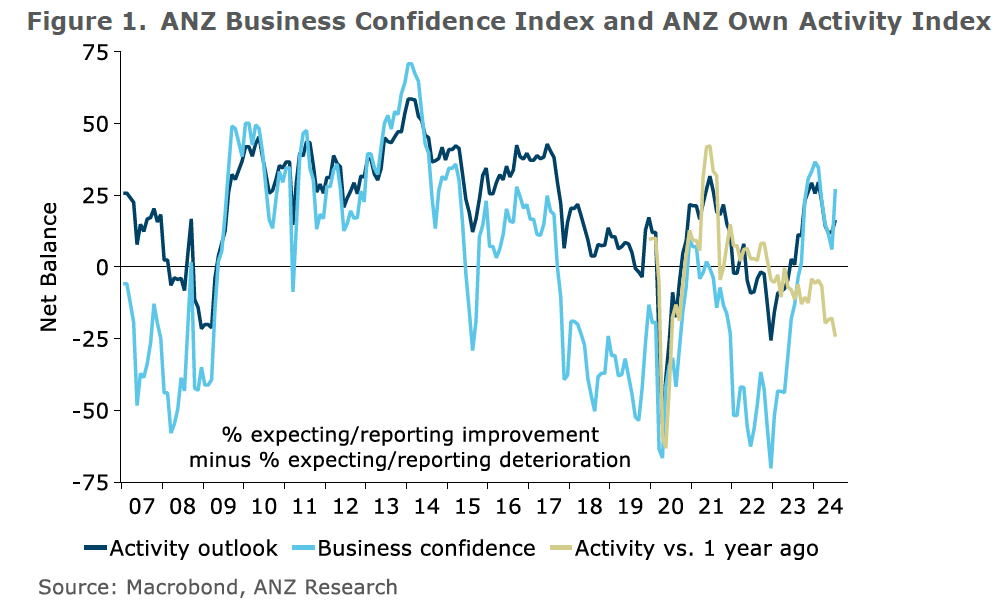

NZ ANZ business confidence jumps to 27.1, inflation expectations fall further

In July, New Zealand's ANZ Business Confidence saw a notable increase, jumping from 6.1 to 27.1. Own Activity Outlook also improved, rising from 12.2 to 16.3. Meanwhile, cost expectations fell slightly from 69.2 to 68.2, and wage expectations edged up from 73.5 to 74.6. Pricing intentions saw an increase from 35.3 to 37.6. Importantly, inflation expectations continued their steady decline, falling from 3.46% to 3.20%.

ANZ commented that the economic climate remains one where "bad news is good news" for RBNZ. With mounting evidence that monetary policy has been effective, perhaps overly so, there is now a broad expectation that RBNZ will start easing the Official Cash Rate this year.

ANZ noted that "evidence is mounting that the inflation dragon is on its last legs," which positions the New Zealand economy for a more robust recovery compared to a scenario where inflation control efforts were only partially successful.

China's NBS PMI manufacturing falls to 49.4 in amid weak demand and extreme weather

China's official NBS PMI Manufacturing index fell slightly from 49.5 to 49.4 in July, just above the expected 49.3. This index has remained below the 50-mark, which separates growth from contraction, for all but three months since April 2023.

NBS analyst Zhao Qinghe attributed the decline in manufacturing activity to the typical off-season for production in July, insufficient market demand, and extreme weather conditions such as high temperatures and floods in some areas.

PMI Non-Manufacturing index also fell, dropping from 50.5 to 50.2, in line with expectations, but still indicating expansion for the 19th consecutive month. Within this category, construction subindex decreased from 52.3 to 51.2, while services subindex slipped from 50.2 to 50e.

Overall, the official PMI Composite, which combines both manufacturing and non-manufacturing sectors, declined from 50.5 to 50.2.

Looking ahead

Eurozone CPI flash is the main focus in European sesion today while German import prices and eunemployment, as well as Swiss UB economic expectations will be released.

Later in the day, Canada GDP would be a focus while US will release ADP employment, Chicago PMI and pending sales. But the main event is definitely FOMC rate decision.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.86; (P) 197.17; (R1) 198.37; More...

Intraday bias in GBP/JPY is back on the downside with breach of 195.84 temporary low. Fall from 208.09 is probably a larger scale correction and should target 185.49 fibonacci level. Nevertheless, on the upside, firm break of 199.45 resistance will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, considering bearish divergence condition in W MACD, 208.09 might be a medium term top and fall from there could already be correcting whole up trend from 148.93 (2022 low). Risk will now stay on the downside as long as 55 D EMA (now at 200.51) holds. Deeper fall would be seen to 38.2% retracement of 148.93 to 208.09 at 185.49.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Jun | -13.80% | -1.70% | -1.90% | |

| 23:50 | JPY | Industrial Production M/M Jun P | -3.60% | -4.20% | 3.60% | |

| 23:50 | JPY | Retail Trade Y/Y Jun | 3.70% | 3.30% | 2.80% | |

| 01:00 | NZD | ANZ Business Confidence Jul | 27.1 | 6.1 | ||

| 01:30 | AUD | Monthly CPI Y/Y Jun | 3.80% | 3.80% | 4.00% | |

| 01:30 | AUD | CPI Q/Q Q2 | 1.00% | 1.00% | 1.00% | |

| 01:30 | AUD | CPI Y/Y Q2 | 3.80% | 3.80% | 3.60% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q2 | 0.80% | 0.90% | 1.00% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q2 | 3.90% | 4.00% | 4.00% | |

| 01:30 | AUD | Retail Sales M/M Jun | 0.50% | 0.30% | 0.60% | |

| 01:30 | AUD | Private Sector Credit M/M Jun | 0.60% | 0.40% | ||

| 01:30 | CNY | NBS Manufacturing PMI Jul | 49.4 | 49.3 | 49.5 | |

| 01:30 | CNY | NBS Non-Manufacturing PMI Jul | 50.2 | 50.2 | 50.5 | |

| 03:57 | JPY | BoJ Interest Rate Decision | 0.25% | 0.25% | 0.10% | |

| 05:00 | JPY | Housing Starts Y/Y Jun | -6.70% | -2.00% | -5.30% | |

| 05:00 | JPY | Consumer Confidence Jul | 36.7 | 36.5 | 36.4 | |

| 06:00 | EUR | Germany Import Price Index M/M Jun | 0.10% | 0.00% | ||

| 07:55 | EUR | Germany Unemployment Change Jul | 16K | 19K | ||

| 07:55 | EUR | Germany Unemployment Rate Jul | 6.00% | 6.00% | ||

| 08:00 | CHF | UBS Economic Expectations Jul | 17.5 | |||

| 09:00 | EUR | Eurozone CPI Y/Y Jul P | 2.40% | 2.50% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul P | 2.80% | 2.90% | ||

| 12:15 | USD | ADP Employment Change Jul | 166K | 150K | ||

| 12:30 | USD | Employment Cost Index Q2 | 1.00% | 1.20% | ||

| 12:30 | CAD | GDP M/M May | 0.10% | 0.30% | ||

| 13:45 | USD | Chicago PMI Jul | 44.1 | 47.4 | ||

| 14:00 | USD | Pending Home Sales M/M Jun | 1.60% | -2.10% | ||

| 14:30 | USD | Crude Oil Inventories | -1.6M | -3.7M | ||

| 18:00 | USD | Fed Interest Rate Decision | 5.50% | 5.50% | ||

| 18:30 | USD | FOMC Press Conference |

Inflation Decline On Track, RBA Can Soon Relax

Inflation in the June quarter was in line with our expectations, and a shade below on some key measures. With the disinflation on track, we affirm our view that rates are on hold until November and likely to decline from then.

Inflation in the June quarter was broadly in line with our expectations, and a shade below them on some crucial underlying measures. Headline CPI inflation was as expected at 1% in the quarter, while the key trimmed mean measure of trend inflation was a bit below at 0.8% versus our expectation of 0.9%. On a year-ended basis, this represents a small increase in headline inflation (from 3.6% to 3.8%), albeit one that was in line with the RBA’s own forecasts. The RBA will look through the base effects driving this and will note that there are no signs of upward momentum in the trimmed mean or monthly outcomes.

Monetary policy decisions are not determined by a single number. As Deputy Governor Hauser pointed out recently, labour market, retail sales, building approvals and other key data have all been released in the lead-up to next week’s RBA Board meeting. None of these provided much of a fresh signal, however, rendering the CPI release pivotal.

The below-consensus result cements our expectation that the RBA Board can remain on hold for the time being. As we have previously flagged, another quarter of inflation data should be enough to convince the RBA Board that disinflation is on track and that inflation will be back into the target range on the desired timetable. That would lead the Board to the conclusion that monetary policy does not need to be as tight as it currently is for much longer.

Recall that the RBA regards the current stance of monetary policy as tight. If the cash rate remained where it is indefinitely, inflation would ultimately decline below the 2–3% target range. Monetary policy operates with a lag, so rate cuts need to start ahead of inflation reaching target. If the Board waits too long, it will risk undershooting the target for no benefit. So rate cuts are likely in the near future, provided inflation continues to traverse the trajectory that the RBA Board is seeking to achieve.

We also note the recent comforting inflation experience of other countries. And, as we have argued previously, it is hard to point to anything that would cause Australia to have a qualitatively different disinflation experience. This is not 2016, when the RBA and Federal Reserve were moving in opposite directions. Back then, the US economy was benefiting from the end of the post-GFC headwinds; by contrast, Australia was navigating the unwind of the mining investment boom. The forces driving economic outcomes were completely different across the two economies.

This time around, Australia and peer economies are all facing a more-or-less common shock. Domestic demand growth is weak, and disinflation has been especially pronounced in discretionary spending categories. There are bumps along the way, including the one seen earlier in the year. And there are some home-grown issues in the housing complex, with inflation in both rents and construction costs likely to remain elevated for some time. Fundamentally though, Australia and its peer economies are seeing the pandemic-era, supply-driven inflation surge unwind, and this is running its course.

Given the sub-consensus inflation outcome and the run of other data confirming that domestic demand growth is soft, we affirm our November call for the first rate cut, with more conviction than previously. We note, however, that the Board is not in a hurry to cut given lingering inflation risks. It is plausible that the Board will retain the ‘not ruling anything in or out’ language in its post-meeting communication. We also anticipate that rates will decline only gradually; we currently project that the RBA cash rate target will fall to 3.1% by end-2025, and this is likely to be the trough. In 2026 and beyond, a period of above-average growth can be anticipated, so interest rates are unlikely to fall further from there.

BoJ hikes to 0.25%, signals more increases if outlook realizes

BoJ raised the uncollateralized overnight call rate from 0-0.10% to around 0.25% today. The decision was made by a 7-2 vote, with dissenting votes from Toyoaki Nakamura and Asahi Noguchi, who preferred to gather more information and conduct a careful assessment before adjusting the interest rate.

Regarding JGB purchases, there was a unanimous decision to reduce the amount of monthly outright purchases to about JPY 3T by Q1 2026. The amount will be cut by JPY 400B each calendar quarter.

BoJ stated that economic activity and prices have been "developing generally in line with the Bank's outlook." Moves to raise wages have been spreading, and the annual rate of import price growth has "turned positive again," with upside risks to prices requiring attention.

It also noted if the outlook presented in the July Outlook Report is realized, BoJ will continue to raise the policy interest rate and adjust the degree of monetary accommodation accordingly.

In the new economic projections, the BoJ made several adjustments:

- Fiscal 2024 growth forecast was lowered from 0.8% to 0.6%.

- Fiscal 2025 growth forecast remains unchanged at 1.0%.

- Fiscal 2026 growth forecast remains unchanged at 1.0%.

For inflation projections:

- Fiscal 2024 CPI core forecast was lowered from 2.8% to 2.5%.

- Fiscal 2025 CPI core forecast was raised from 1.9% to 2.1%.

- Fiscal 2026 CPI core forecast remains unchanged at 1.9%.

- Fiscal 2024 CPI core-core forecast remains unchanged at 1.9%.

- Fiscal 2025 CPI core-core forecast remains unchanged at 1.9%.

- Fiscal 2026 CPI core-core forecast remains unchanged at 2.1%.

China’s NBS PMI manufacturing falls to 49.4 in amid weak demand and extreme weather

China's official NBS PMI Manufacturing index fell slightly from 49.5 to 49.4 in July, just above the expected 49.3. This index has remained below the 50-mark, which separates growth from contraction, for all but three months since April 2023.

NBS analyst Zhao Qinghe attributed the decline in manufacturing activity to the typical off-season for production in July, insufficient market demand, and extreme weather conditions such as high temperatures and floods in some areas.

PMI Non-Manufacturing index also fell, dropping from 50.5 to 50.2, in line with expectations, but still indicating expansion for the 19th consecutive month. Within this category, construction subindex decreased from 52.3 to 51.2, while services subindex slipped from 50.2 to 50e.

Overall, the official PMI Composite, which combines both manufacturing and non-manufacturing sectors, declined from 50.5 to 50.2.

Australia’s trimmed mean CPI drops to 3.9%, continuing six-quarter downtrend

In Q2, Australia's CPI rose by 1.0% qoq, matching both expectations and the pace set in Q1. Annual rate increased from 3.6% to 3.8% , also in line with forecasts.

More notably, the core inflation measure marked its sixth consecutive quarter of cooling. Trimmed mean CPI, which is a key indicator of underlying inflation, rose by 0.8% qoq. This represents a slowdown from the prior quarter's 1.0% qoq increase and falls below the expected 0.9% qoq. Annually, trimmed mean CPI slowed from 4.0% yoy to 3.9% yoy, below the expected 4.0% and continuing its downward trend from the peak of 6.8% in the December 2022 quarter.

Additionally, the monthly CPI for June slowed from 4.0% yoy to 3.8% yoy, again matching expectations.

NZ ANZ business confidence jumps to 27.1, inflation expectations fall further

In July, New Zealand's ANZ Business Confidence saw a notable increase, jumping from 6.1 to 27.1. Own Activity Outlook also improved, rising from 12.2 to 16.3. Meanwhile, cost expectations fell slightly from 69.2 to 68.2, and wage expectations edged up from 73.5 to 74.6. Pricing intentions saw an increase from 35.3 to 37.6. Importantly, inflation expectations continued their steady decline, falling from 3.46% to 3.20%.

ANZ commented that the economic climate remains one where "bad news is good news" for RBNZ. With mounting evidence that monetary policy has been effective, perhaps overly so, there is now a broad expectation that RBNZ will start easing the Official Cash Rate this year.

ANZ noted that "evidence is mounting that the inflation dragon is on its last legs," which positions the New Zealand economy for a more robust recovery compared to a scenario where inflation control efforts were only partially successful.

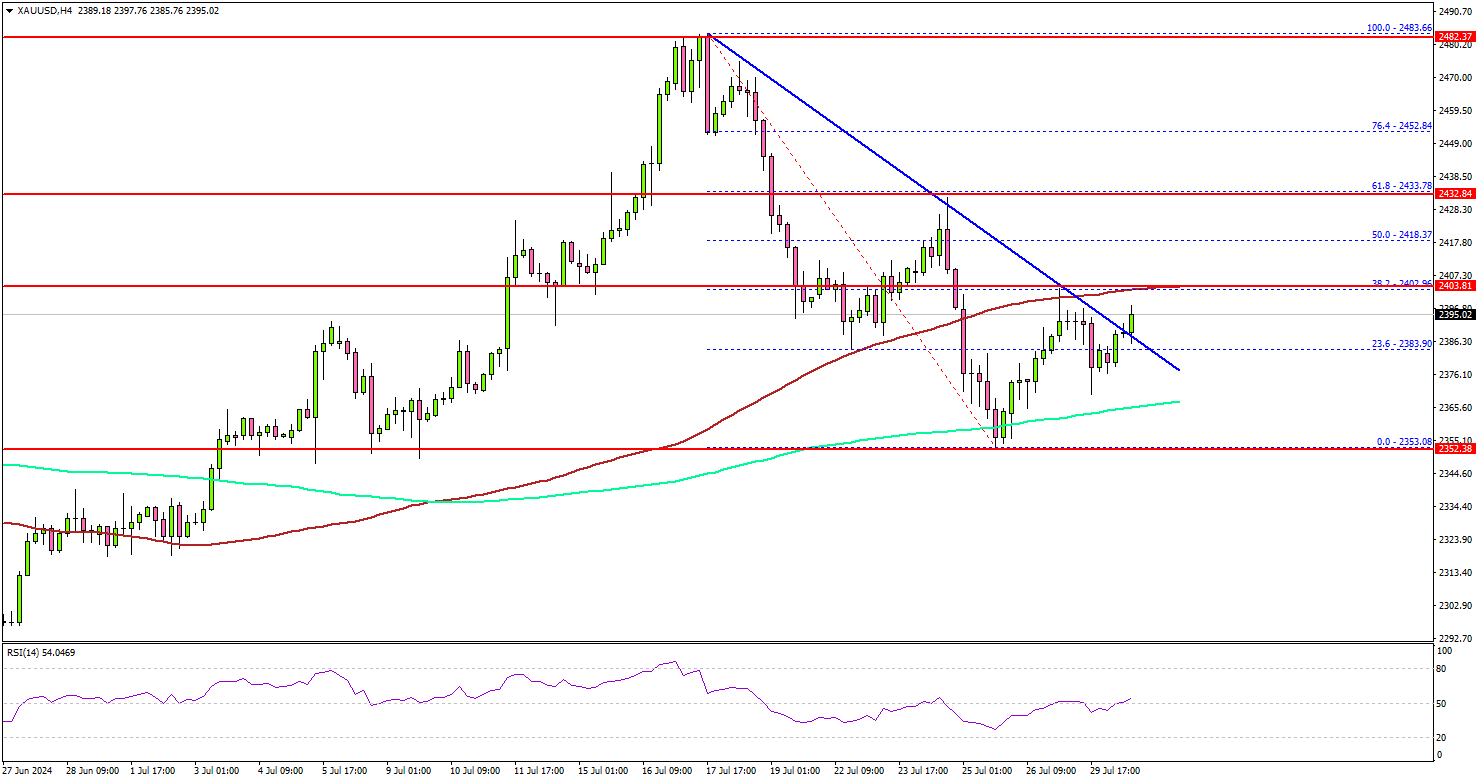

Gold Eyes New Gains: Will It Sparkle Again?

Key Highlights

- Gold is attempting a fresh increase from the $2,350 support zone.

- It cleared a connecting bearish trend line with resistance at $2,388 on the 4-hour chart.

- Oil prices extended losses and traded below $75.50.

- The US ADP employment could change by 150K in July 2024.

Gold Price Technical Analysis

Gold prices found support near the $2,352 level against the US Dollar. The price formed a base and recently started a recovery wave above $2,365.

The 4-hour chart of XAU/USD indicates that the price settled above the $2,380 level and the 200 Simple Moving Average (green, 4 hours). It cleared a connecting bearish trend line with resistance at $2,388.

The price surpassed the 23.6% Fib retracement level of the downward move from the $2,483 swing high to the $2,353 low. The price is now facing resistance near the $2,400 zone and the 100 Simple Moving Average (red, 4 hours).

The next major resistance sits near the $2,420 level and the 50% Fib retracement level of the downward move from the $2,483 swing high to the $2,353 low.

A clear move above the $2,420 resistance could open the doors for more upsides. The next major resistance could be near $2,432, above which the price could accelerate higher toward the $2,445 level. Any more gains might send Gold toward the $2,450 resistance.

On the downside, there is a key support forming near the $2,365 level and the 200 Simple Moving Average (green, 4 hours). A downside break below the $2,365 support might call for more downsides. The next major support is near the $2,352 level. Any more losses might send gold prices toward $2,340.

Looking at Oil, the bears remained in action and they might soon aim for more downsides below the $75.00 support region.

Economic Releases to Watch Today

- US ADP Employment Change for July 2024 - Forecast 150K, versus 150K previous.

- US Pending Home Sales for June 2024 (YoY) - Forecast +1.1%, versus -6.6% previous.

NZDUSD Wave Analysis

- NZDUSD reversed from support level 0.5860

- Likely to rise to resistance level 0.5920

NZDUSD currency pair recently reversed up from the pivotal support level 0.5860 (which reversed the price twice in April), standing close to the lower daily Bollinger Band.

The upward reversal from the support level 0.5860 stopped the c-wave of the previous minor ABC correction 2.

Given the strength of the support level 0.5860, bullish NZD sentiment and the oversold daily Stochastic, NZDUSD currency pair can be expected to rise further to the next resistance level 0.5920.