Sample Category Title

UK 100 Index Swings to All-Time High

- UK 100 hits record high after the BoE rate decision; up 8% year-to-date

- Next target at 8,500, but fears of an overbought market might delay rally

The UK 100 stock index (cash) has been performing incredibly well over the past four months, staging another exponential rally this week to unlock an all-time high of 8,393 on Thursday.

The index has surpassed a couple of targets, including the 2023 top of 8,045 that temporarily ceased bullish actions on April 12. The spotlight is now on the 8,500 psychological level and the resistance line, which joins the 2022 and 2023 highs. However, given the overbought signals coming from the RSI and the stochastic oscillator, there is some doubt whether the index will rise directly towards that bar.

If sellers take control, support could initially develop near Tuesday’s low of 8,270. Sliding below that floor, the price might again seek protection around the 8,100 pivot area and perhaps test the 20-day simple moving average (SMA) around the same location. Should the decline continue below the 8,045 threshold, the next stop could be somewhere between 7,985 and 7,945. Not far below, the lower band of the broken bullish channel, where the 50-day SMA is positioned, might attract greater attention.

In the event the rally strengthens above 8,500, traders might target the 8,600 number.

All in all, the UK 100 index is waiting for its next bullish catalyst to revisit the resistance line at 8,500. Yet, given this week’s vertical rally, and the overbought signals coming from the technical indicators, upside pressures might cool down soon. A correction below 8,045 would neutralize the broad positive outlook.

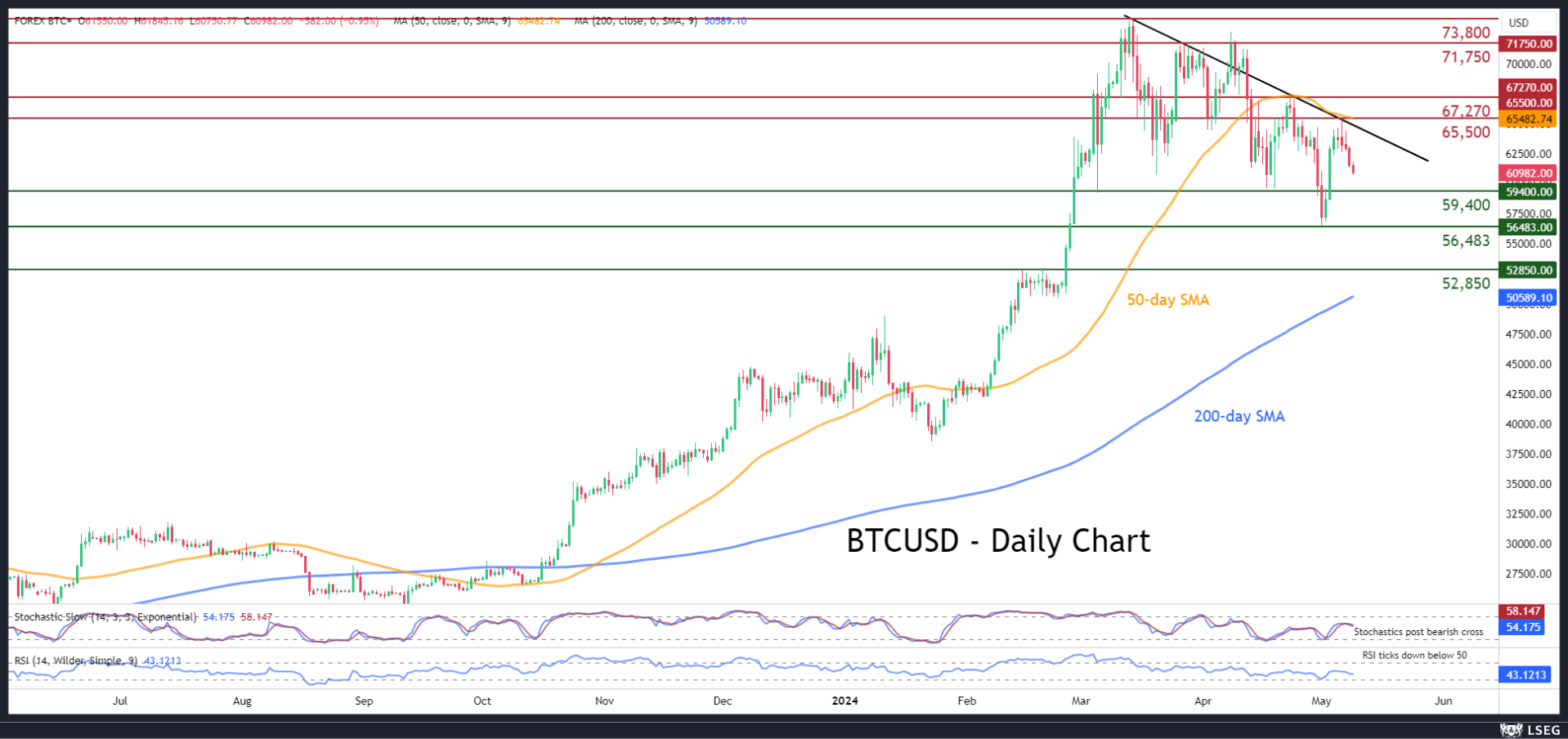

BTCUSD Retreats After Unsuccessful Test of 50-SMA

- BTCUSD drops after failing to claim 50-day SMA

- The price extends its series of lower highs and lows

- Momentum indicators are tilted to the downside

BTCUSD (Bitcoin) had been in a slow but steady recovery since its bounce off the two-month bottom of 56,483. However, the rebound faltered and the price reversed back lower following its second unsuccessful attempt to conquer the 50-day simple moving average (SMA).

Should Bitcoin extend its pullback, the March-April support of 59,400 might curb initial downside attempts. Sliding beneath that floor, the price could challenge the two-month low of 56,483. A violation of that zone may set the stage for the February resistance zone of 52,850.

On the flipside, if buying pressures re-emerge, the price might revisit its recent rejection region of 65,500, which overlaps with the 50-day SMA. Conquering that zone, the bulls could attack the April resistance of 67,270. Even higher, the March resistance of 71,750 might prove to be a tough barrier for the price to overcome.

In brief, BTCUSD has been on the retreat again after its second unsuccessful attempt to claim the 50-day SMA, remaining stuck beneath its downward sloping trendline in place since early March. Hence, for the technical picture to improve, the price needs to decisively break above the restrictive trendline.

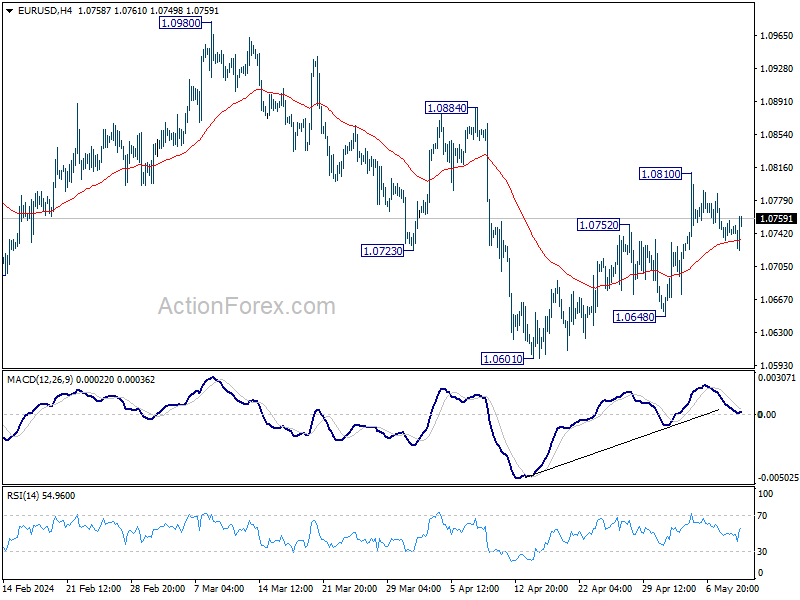

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0736; (P) 1.0747; (R1) 1.0759; More...

Intraday bias in EUR/USD remains neutral for the moment. Further rally is expected as long as 55 4H EMA (now at 1.0733) holds. On the upside, above 1.0810 will resume the rebound from 1.0601 to 1.0884 resistance next. However, firm break of 55 4H EMA will argue that the rebound has completed, and turn bias to the downside for 1.0648 support instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

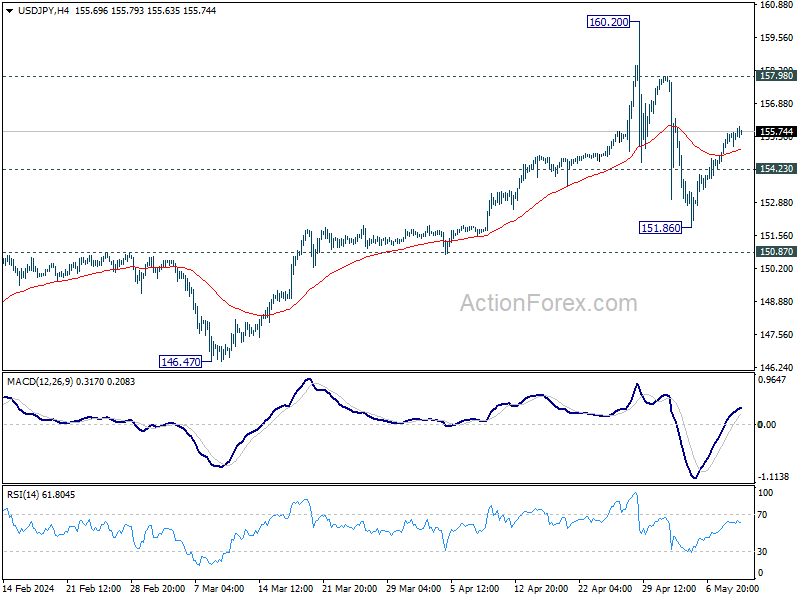

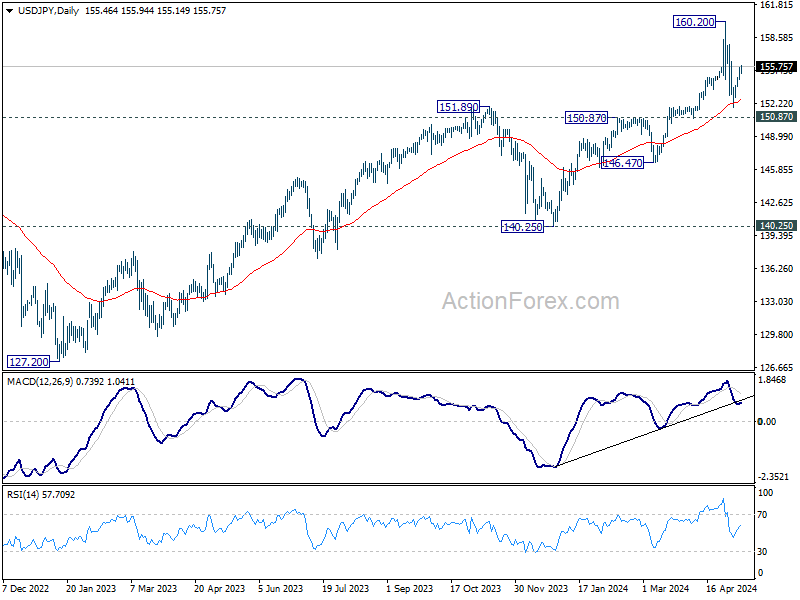

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.76; (P) 155.22; (R1) 155.96; More...

Intraday bias in USD/JPY remains mildly on the upside as this point. Rebound from 151.86 is seen as the second leg of the corrective pattern from 160.20 high. Further rise would be seen to 157.98 resistance. On the downside, below 154.23 minor support will turn intraday bias neutral.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

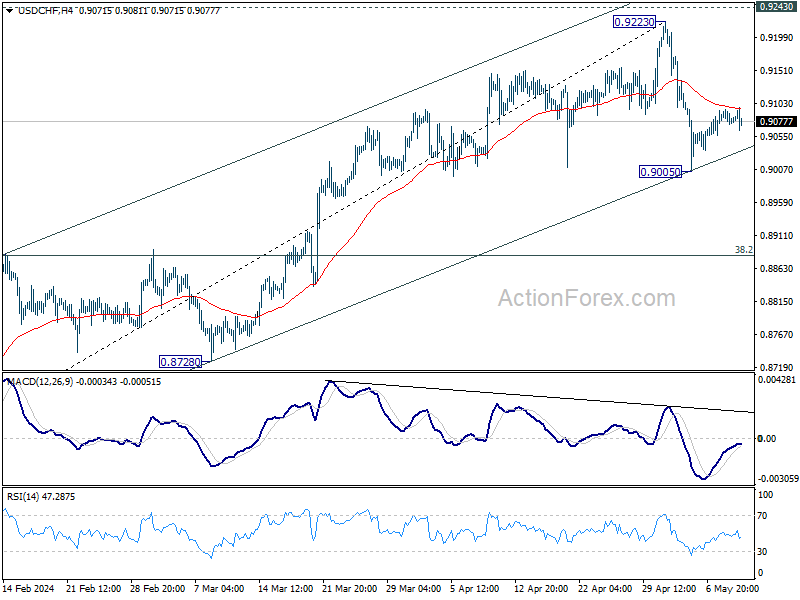

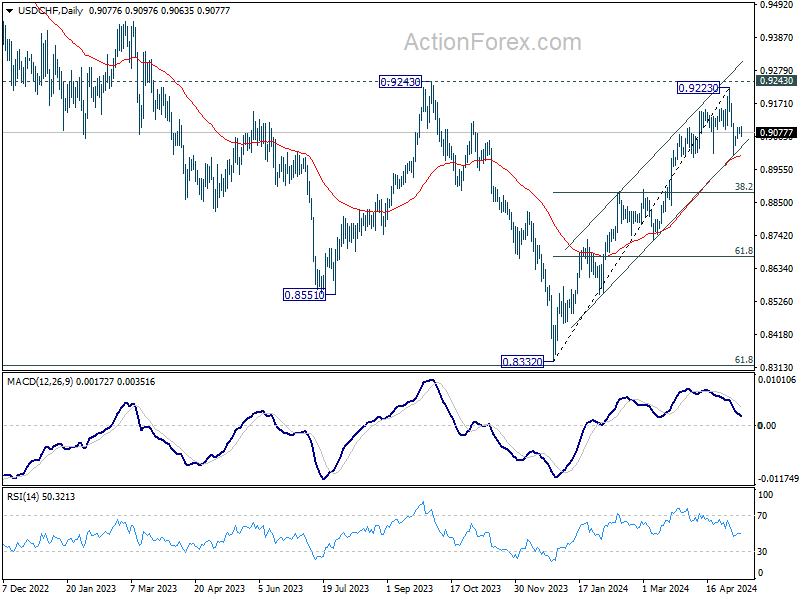

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9071; (P) 0.9083; (R1) 0.9093; More....

Intraday bias in USD/CHF stays neutral and outlook is unchanged. Further decline is in favor as long as 55 4H EMA (now at 0.9096) holds. On the downside, break of 0.9005 and sustained trading below 55 D EMA (now at 0.9000) will bring deeper fall to 38.2% retracement of 0.8332 to 0.9223 at 0.8883. However, firm break of 55 4H EMA will suggest that the pull back has completed, and bring stronger rebound to retest 0.9223 high.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

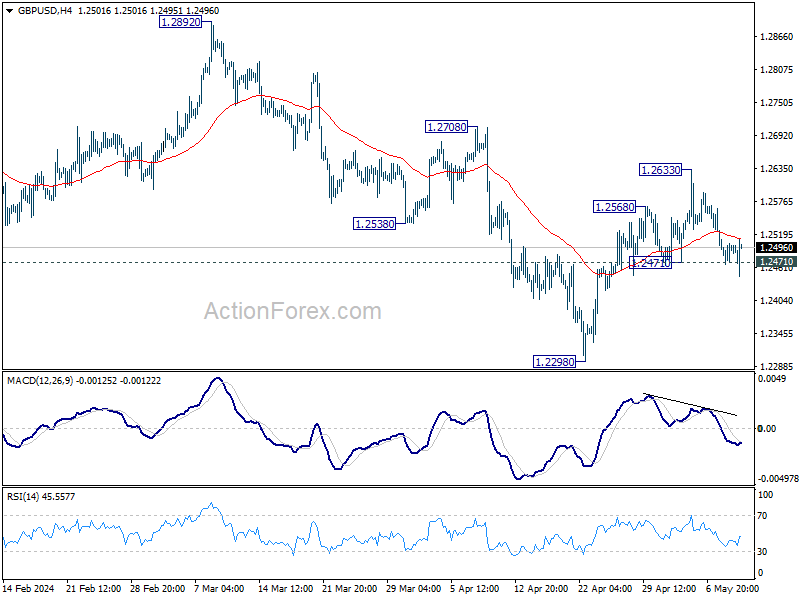

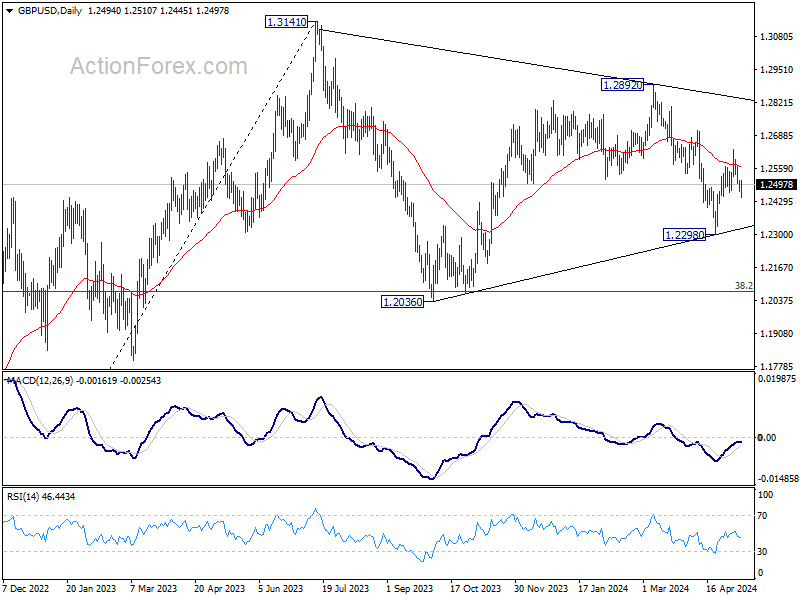

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2468; (P) 1.2497; (R1) 1.2525; More...

GBP/USD breached 1.2471 support briefly but quickly recovered. Intraday bias stays neutral first. Strong bounce from current level will retain near term bullishness. Further break of 1.2633 will resume the rebound from 1.2298 to 1.2708 resistance next. However, firm break of firm break of 1.2471 will indicate that this rebound has completed, and revive near term bearishness. Retest of 1.2298 should then be seen in this case.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

Sterling Weathers Dovish BoE Impact; Dollar Slips on Poor Jobless Claims

British pound experienced some volatility following BoE's rate decision, which revealed a dovish tilt in both the voting pattern and the language used. Sterling dipped initially, but then made a swift recovery, surviving as Governor Andrew Bailey dovish remarks in his follow-up press conference.

Bailey stressed it's not time to cut interest yet. But for June, he's open to the idea, depending on upcoming economic data. He took a non-committal stance and described a June cut as "neither ruled out nor a fait accompli." However, with inflation projected to dip below target to 1.6% in three years, Bailey indicated the necessity for future rate cuts to make monetary policy less restrictive over the forecast period.

Meanwhile, Dollar saw a sharp decline in early US session following unexpectedly weak jobless claims data, fostering hopes that the labor market might be easing. This softening is seen as potentially paving the way for Fed to begin reducing interest rates by September, although this will depend heavily on forthcoming inflation data, particularly next week's U.S. CPI release.

As for the day overall, Yen is currently the worst performer, followed by Dollar and then Euro. Aussie is the best, followed by Kiwi and Canadian. Sterling and Swiss Franc are positioning in the middle.

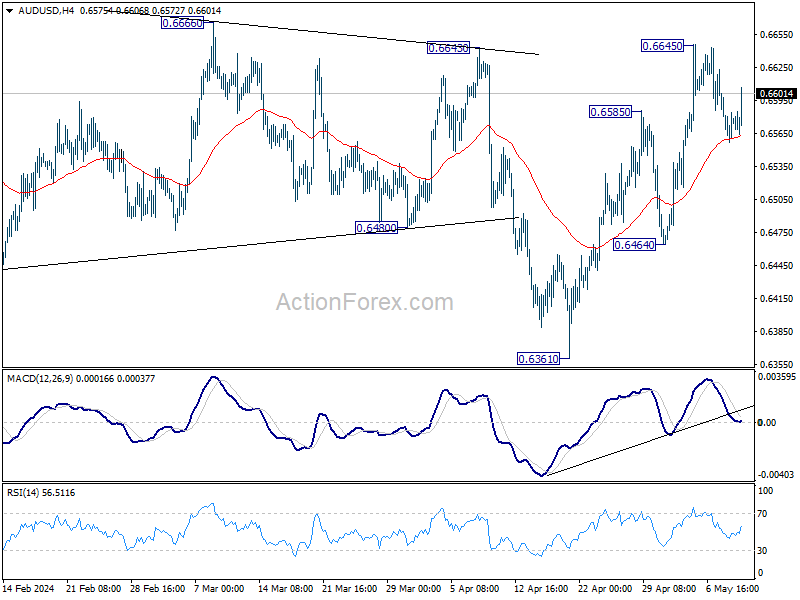

Technically, AUD/USD bounces after drawing support from 55 4H EMA and retains near term bullishness. Focus is back on 0.6645 resistance. Firm break there will resume whole rise from 0.6361. Further break of 0.6666 resistance will solidify the case of near term bullish reversal, and target 0.6870 resistance next.

In Europe, at the time of writing, FTSE is up 0.34%. DAX is up 0.93%. CAC is up 0.31%. UK 10-year yield is up 0.0061 at 4.149. Germany 10-year yield is up 0.018 at 2.484. Earlier in Asia, Nikkei fell -0.34%. Hong Kong HSI rose 1.22%. China Shanghai SSE rose 0.83%. Singapore Strait Times rose 0.04%. Japan 10-year JGB yield rose 0.0298 to 0.913.

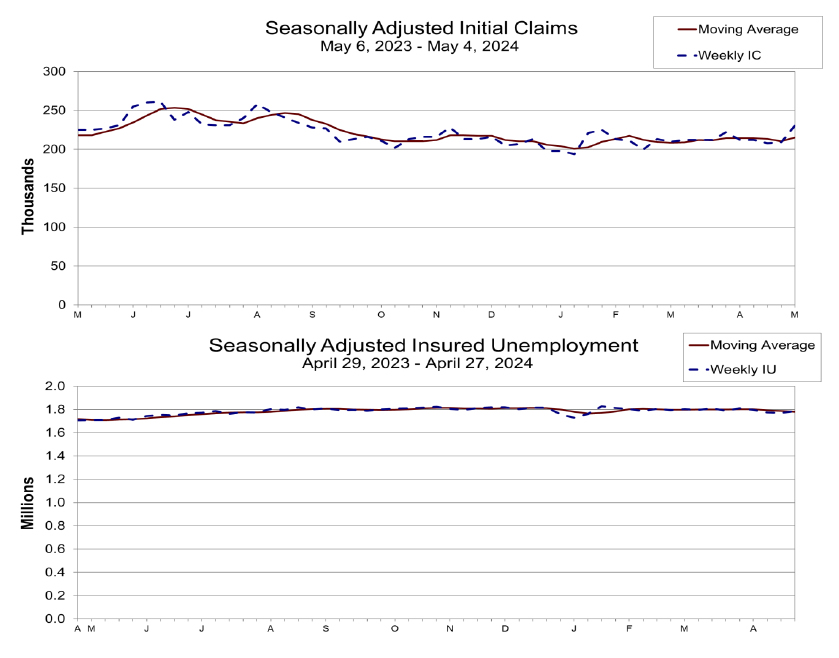

US initial jobless claims rises to 231k, vs exp 210k

US initial jobless claims rose 22k to 231k in the week ending May 4, above expectation of 210k. That's also the highest level since late August 2023. Four-week moving average on initial claims rose 4.75k to 215k. Four-week moving average on initial claims rose 4.75k to 215k. Continuing claims rose 17k to 1785k in the week ending April 27. Four-week moving average of continuing claims fell -6.25k to 1781k.

BoE holds rate at 5.25%, Ramsden joins dove camp

BoE maintained Bank Rate at 5.25%, as widely expected. The announcement revealed a subtle dovish shift as evidenced by the voting and adjustments in the accompanying statement. Although these changes are not strong enough to warrant an immediate rate cut in June, they suggest that the central bank is inching closer to easing monetary policy.

The meeting concluded with a 7-2 voting split, with Deputy Governor Dave Ramsden joining the typically dovish Swati Dhingra in advocating for a rate cut. Additionally, BoE has explicitly stated its intent to monitor incoming data to assess whether risks from "inflation persistence are receding", to determine the duration for which current Bank Rate is maintained.

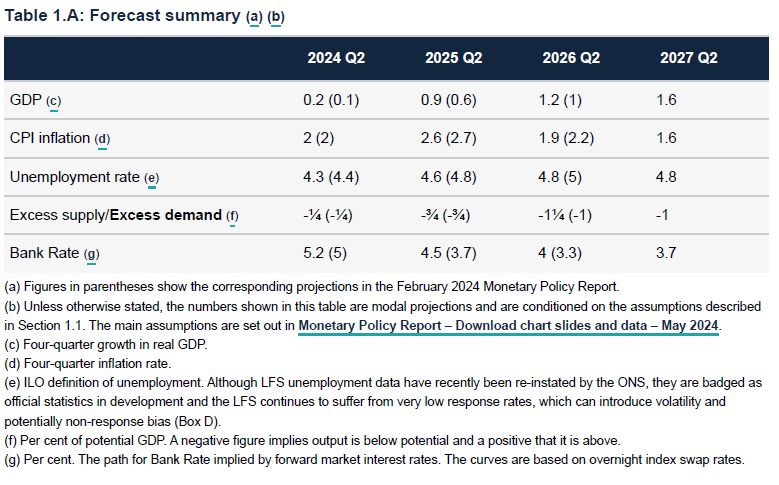

Furthermore, in its updated economic forecasts, BoE revised GDP growth projections upwards across the board and lowered CPI expectations for the coming years.

Four-quarter GDP growth is projected to be at 0.2% in Q2 2024 (revised up from 0.1%), 0.9% in Q2 2025 (up from 0.6%), 1.2% in Q2 2026 (up from 1%) , and then 1.6% in Q2 2027.

CPI inflation is projected to be at 2% in Q2 2024 (unchanged), 2.6% in Q2 2025 (down from 2.7%), 1.9% in Q2 2026 (down from 2.2%, and then 1.6) in Q2 2027.

BoJ meeting summary indicates hawkish shift

Summary of Opinions from BoJ's April meeting revealed a notable hawkish tilt among its board members, with significant dialogue concerning further rate hikes. This development reflects a growing concern over inflationary pressures and the impact of a weaker yen, which could hasten monetary policy normalization.

One board member highlighted that if the economic activity and price forecasts from April are realized, future policy interest rates might be "higher than the path that is factored in by the market."

Further discussions emphasized the necessity of managing transitions carefully to mitigate shocks from sudden and substantial policy changes once price stability target is achieved. One approach proposed involves "moderate policy interest rate hikes".

Another critical point raised was the impact of a weakening yen on inflation. A board member warned that if underlying inflation continues to rise above the baseline scenario due to the currency's depreciation, "it is quite possible that the pace of monetary policy normalization will increase".

Japan's real wages fall -2.5% yoy, declining for 24th consecutive month

In Japan, real wages fell notably by -2.5% yoy in March, marking a worsening trend from the previous month's -1.8% yoy. It also extended the streak of declines to 24 consecutive months—the longest since such data was first recorded in 1991.

Nominal wages, which include total cash earnings, grew modestly by 0.6% yoy in March, a deceleration from February's 1.4% yoy increase. Although regular pay saw a rise of 1.7% yoy , this was offset by -1.5% yoy decline in overtime pay, which has fallen for four consecutive months. Furthermore, special payments, which encompass bonuses and other benefits, saw a sharp decrease of -9.4% yoy.

The persistence of wage declines occurs despite a seemingly favorable outcome from Japan's annual labor-management wage talks this spring, which were described as the most beneficial for workers at major companies in three decades.

However, a labor ministry official noted that the results of the "shunto" wage negotiations were not reflected in the March data. With these results expected to influence the figures from April onwards, there is a focus on whether real wages will show an improvement and turn positive for the first time in two years.

China's exports rises 1.5% yoy in Apr, imports surges 8.% yoy

China's trade figures for April showcased significant recovery, with exports increasing by 1.5% yoy to USD 292.5 B, exceeding the expected 1.0% yoy growth. This rebound is particularly noteworthy given the -7.5% yoy decline observed in March.

On the import side, there was a notable surge of 8.4% yoy to USD 210.1B, substantially higher than the forecasted 5.4% yoy. This rise marks a recovery from the -1.9% decline in March. The significant increase in imports, driven partly by a weaker comparison base from the previous year, also reflects an uptick in economic activity as domestic conditions improve.

Trade surplus for April stood at USD 72.4B, smaller than the expected USD 81.4B but still an improvement from USD 58.6B recorded in March.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2468; (P) 1.2497; (R1) 1.2525; More...

GBP/USD breached 1.2471 support briefly but quickly recovered. Intraday bias stays neutral first. Strong bounce from current level will retain near term bullishness. Further break of 1.2633 will resume the rebound from 1.2298 to 1.2708 resistance next. However, firm break of firm break of 1.2471 will indicate that this rebound has completed, and revive near term bearishness. Retest of 1.2298 should then be seen in this case.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance Apr | -5% | 4% | -4% | -5% |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 03:00 | CNY | Trade Balance (USD) Apr | 72.4B | 81.4B | 58.6B | |

| 05:00 | JPY | Leading Economic Index Mar P | 111.4 | 111.3 | 111.8 | |

| 11:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% | 5.25% | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 0--2--7 | 0--1--8 | 0--1--8 | |

| 12:30 | USD | Initial Jobless Claims (May 3) | 231K | 210K | 208K | 209K |

| 14:30 | USD | Natural Gas Storage | 87B | 59B |

US initial jobless claims rises to 231k, vs exp 210k

US initial jobless claims rose 22k to 231k in the week ending May 4, above expectation of 210k. That's also the highest level since late August 2023. Four-week moving average on initial claims rose 4.75k to 215k.

Continuing claims rose 17k to 1785k in the week ending April 27. Four-week moving average of continuing claims fell -6.25k to 1781k.

Japanese Yen Lower After BoJ Minutes

The Japanese yen has posted a three-day slide and is in negative territory on Thursday. USD/JPY has risen 0.26% on the day and is trading at 155.93 at the time of writing.

Is the BoJ turning hawkish?

The Bank of Japan released its Summary of Opinions from its April 26th meeting earlier today. The meeting was uneventful as the BoJ maintained policy settings. The yen proceeded to slide and just a few days later broke below the 160 line, triggering a suspected intervention by Japan’s Ministry of Finance. Governor Ueda was criticized for failing to send a clear message at the meeting about further rate hikes, which may have boosted the ailing yen.

Ueda may have tried to rectify matters by stating on Wednesday that he was ready to tighten policy if inflation was higher than expected. The BoJ Summary of Opinions showed that many members called for the central bank to continue raising rates in order to reduce risks of inflation rising more than expected.

Will the hawkish BOJ Summary of Opinions push Ueda into action? That remains to be seen, as inflation will have to move higher before the BoJ tightens again. The Japanese economy remains fragile and a significant rate hike could risk tipping the economy into a recession.

The BoJ took the plunge in March and lifted rates into positive territory. Still, rates remain close to zero and the yen will remain under pressure as the US/Japan rate differential remains wide. The BoJ is showing signs of becoming more hawkish, such as the Summary of Opinions, but the path to normalization remains long.

USD/JPY Technical

- USD/JPY continues to rise is testing resistance at 155.96. Above, there is resistance at 156.42

- There is support at 155.22 and 154.76

BoE holds rate at 5.25%, Ramsden joins dove camp

BoE maintained Bank Rate at 5.25%, as widely expected. The announcement revealed a subtle dovish shift as evidenced by the voting and adjustments in the accompanying statement. Although these changes are not strong enough to warrant an immediate rate cut in June, they suggest that the central bank is inching closer to easing monetary policy.

The meeting concluded with a 7-2 voting split, with Deputy Governor Dave Ramsden joining the typically dovish Swati Dhingra in advocating for a rate cut. Additionally, BoE has explicitly stated its intent to monitor incoming data to assess whether risks from "inflation persistence are receding", to determine the duration for which current Bank Rate is maintained.

Furthermore, in its updated economic forecasts, BoE revised GDP growth projections upwards across the board and lowered CPI expectations for the coming years.

Four-quarter GDP growth is projected to be at 0.2% in Q2 2024 (revised up from 0.1%), 0.9% in Q2 2025 (up from 0.6%), 1.2% in Q2 2026 (up from 1%) , and then 1.6% in Q2 2027.

CPI inflation is projected to be at 2% in Q2 2024 (unchanged), 2.6% in Q2 2025 (down from 2.7%), 1.9% in Q2 2026 (down from 2.2%, and then 1.6) in Q2 2027.

Full BoE statement and Monetary Policy Report.