Sample Category Title

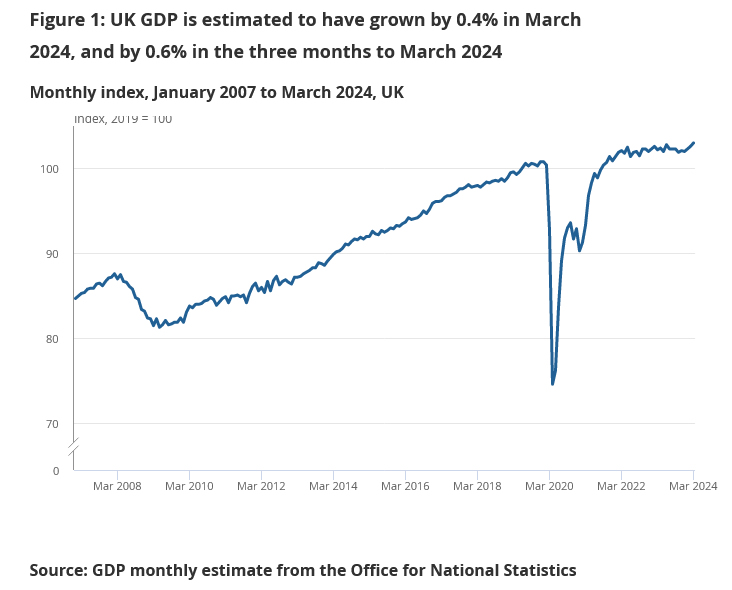

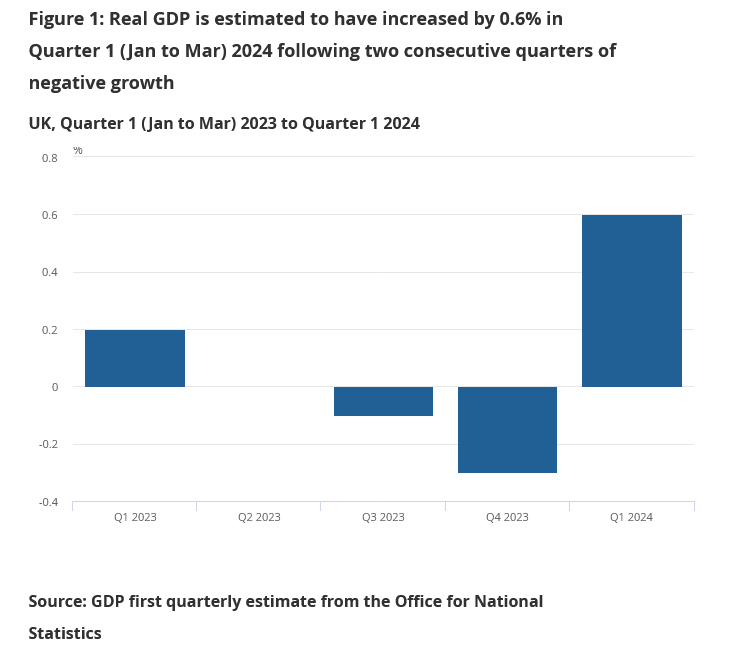

UK GDP grows 0.4% mom in Mar, 0.6% qoq in Apr, above expectations

UK GDP grew 0.4% mom in March, well above expectation of 0.1% mom. Services output rose 0.5% mom. Production output rose 0.2% mom while construction output fell -0.4% mom.

For Q1, GDP grew 0.6% qoq, above expectation of 0.4% qoq. Compared with the same quarter a year ago, GDP is estimated to have increased by 0.2% yoy. In output terms, services grew by 0.7% on the quarter with widespread growth across the sector; elsewhere the production sector grew by 0.8% while the construction sector fell by -0.9%.

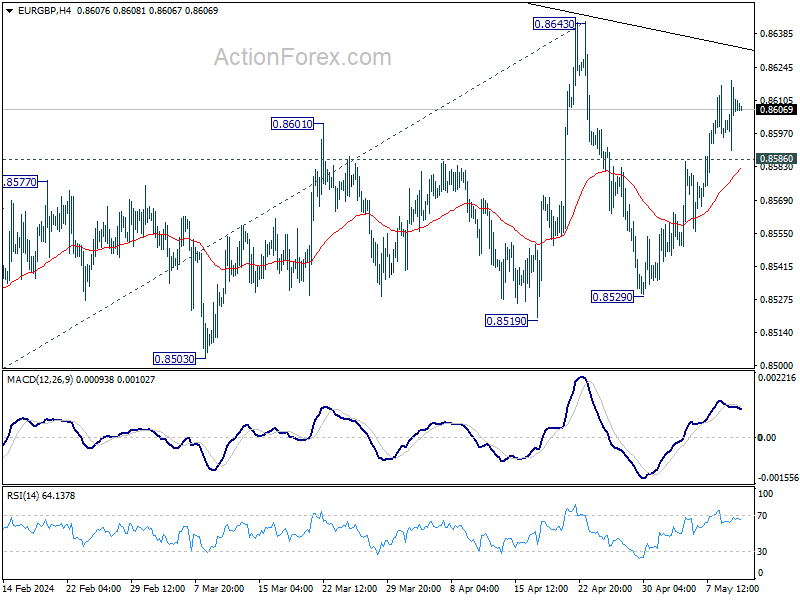

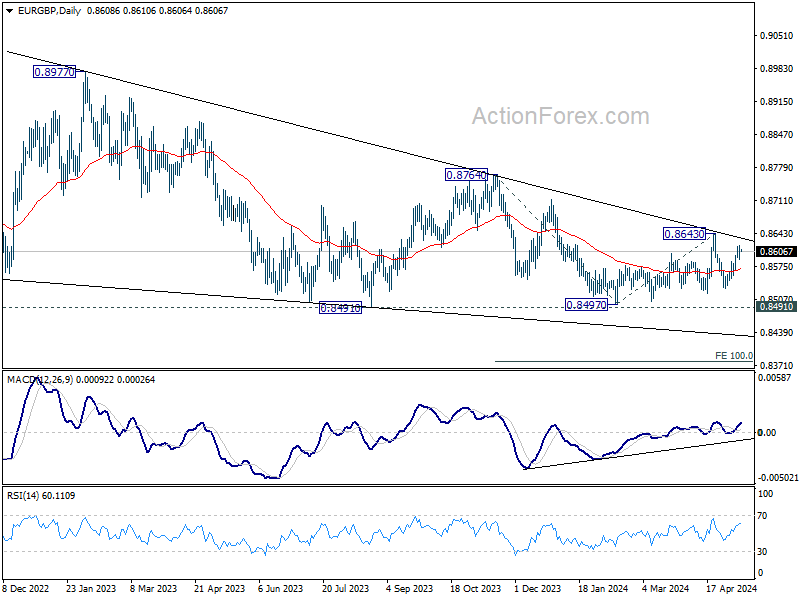

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8593; (P) 0.8607; (R1) 0.8623; More...

Intraday bias in EUR/GBP stays mildly on the upside at this point, and further rally could be seen to 0.8643 resistance. Firm break there will resume the choppy rebound from 0.8497 low. On the downside, below 0.8585 minor support will argue that rebound from 0.8529 has completed, and larger fall might finally be ready to resume. Intraday bias will be back on the downside for 0.8529 support first.

In the bigger picture, outlook remains bearish as EUR/GBP is capped below medium term falling trendline. That is, down trend from 0.9267 (2022 high) is still in progress. Firm break of 0.8491/7 will target 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

Weak Sterling Awaits UK GDP, Gold Poised to Reach Record High

Sterling remains one of the weakest performers this week, despite lack of strong selling momentum. BoE Chief Economist Huw Pill reaffirmed the market's expectations that the central bank would start to consider interest rate cuts in upcoming meetings. These messages echoed the slight dovish shift noted in yesterday's BoE rate decision. Attention is now shifting towards the upcoming UK GDP data, which will provide crucial insights into the strength of the economic rebound from last year's modest recession.

In other developments, Japanese Yen continues to be the weakest overall. But Yen's decline is notably slowing, particularly against Dollar. Swiss Franc is not far behind the Pound, ranking as the third weakest. On the more positive side, New Zealand Dollar stands out as the strongest performer at this moment, finding support from slight improvements in manufacturing data. Euro follows as the second strongest, with the Canadian dollar close behind, which will likely see some volatility with the release of Canada's employment data later today. Dollar and Australian Dollar are positioned in the middle of the pack in terms of performance.

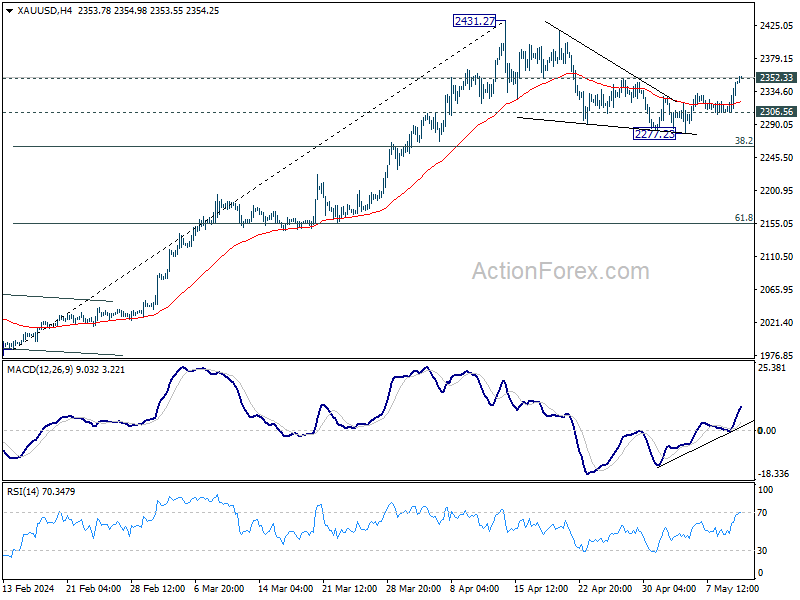

Technically, Gold's break of 2352.33 resistance now suggests that correction from 2431.27 has completed at 2277.23 as a triangle pattern. Further rally should be seen to retest 2431.27 record high. Firm break there will confirm larger up trend resumption. This will remain the favored case as long as 2306.56 support holds, in case of retreat.

In Asia, at the time of writing, Nikkei is up 0.35%. Hong Kong HSI is up 1.74%. China Shanghai SSE is down -0.22%. Singapore Strait Times is up 0.82%. Japan 10-year JGB yield is up 0.0045 at 0.918. Overnight, DOW rose 0.85%. S&P 500 rose 0.51%. NASDAQ rose 0.27%. 10-year yield fell -0.043 to 4.449.

BoE's Pill signals rate cut discussions in upcoming meetings

BoE Chief Economist Huw Pill expressed growing confidence in the possibility of lowering interest rates and stated that the committee would start discussing it "over the next few meetings".

"We're growing more and more confident that we can begin to reduce the restriction that monetary policy is putting in the economy and start to cut interest rate," Pill said at a Q&A session organized by the central bank yesterday.

Pill emphasized that the Bank is not quite ready to make these adjustments, stating, "We're not quite there yet, and we need more evidence."

Yet, he also mentioned, "In the absence of big new disturbances in the economy, we're going to be thinking about moving interest rates over the next few meetings."

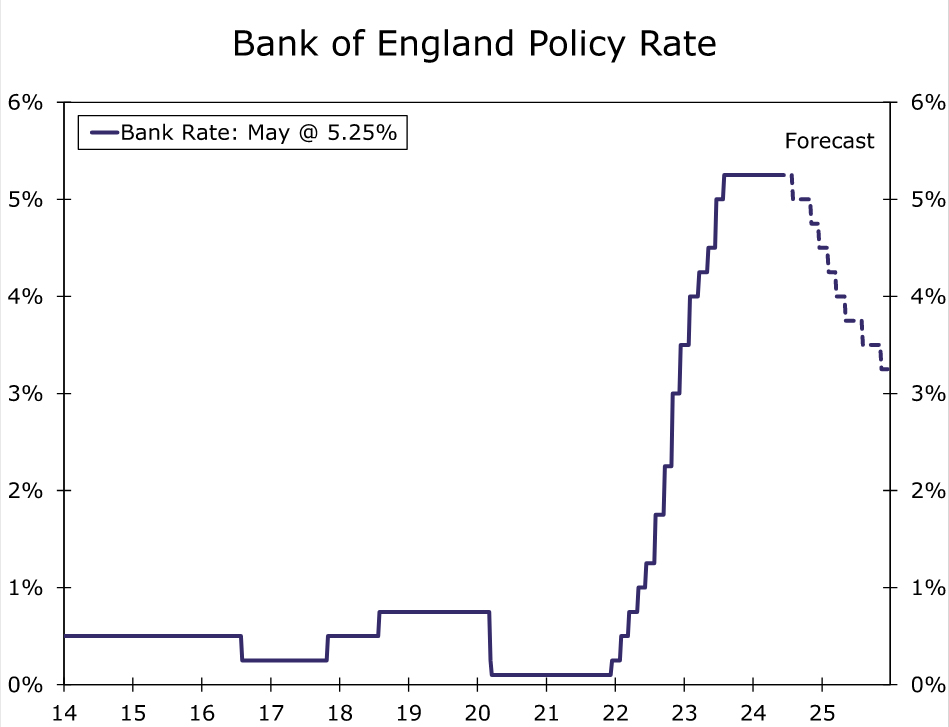

This commentary came after the Bank's decision to maintain the interest rate at 5.25%, a decision supported by an 8-2 vote. Deputy Governor Dave Ramsden joined Swati Dhingra, the usual dove, in voting for a rate cut, signaling a slight shift towards a more dovish stance within policy-setting committee.

Fed's Daly discusses dual scenarios for interest rate amid inflation uncertainty

San Francisco Fed President Mary Daly articulated the challenges surrounding US inflation, describing it as likely to be a "bumpy ride" going forward. In her comments yesterday, Daly highlighted there is "uncertainly about what the next few months of inflation will look like".

Daly presented two potential scenarios that could influence Fed's interest rate decisions. In the first scenario, if inflation continues on its recent downward trend alongside a cooling job market, Daly noted that lowering interest rates would be appropriate.

Conversely, Daly outlined a second scenario where inflation does not decline as expected but instead remains stagnant, as observed in the first quarter of this year. In such a situation, Daly stated that it would not be appropriate to cut interest rates, unless there is a concurrent weakening in the job market.

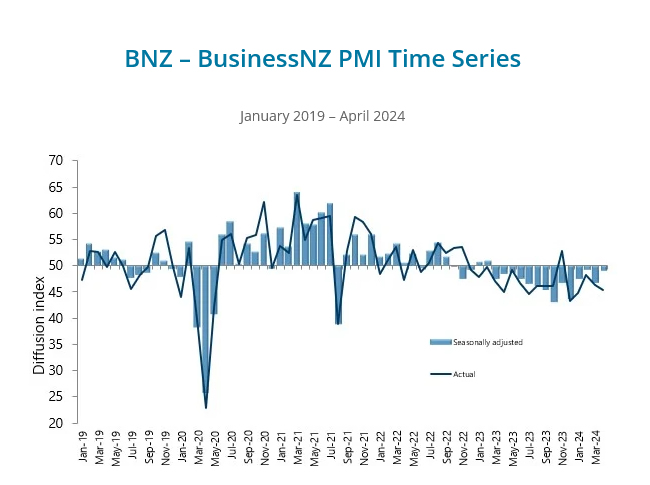

NZ BNZ manufacturing rises to 48.9, signs of life despite prolonged contraction

New Zealand BusinessNZ Performance of Manufacturing Index rose from 46.8 to 48.9 in April. Despite this improvement, the sector remains in contraction for the 14th consecutive month.

Breaking down the components of the index, there were some positive developments in April. Production notably increased to 50.8 from 46.0, and employment also rose to 50.8 from 46.8, both crossing into expansion territory. However, new orders still lagged behind, albeit with a slight improvement to 45.3 from 44.6, indicating that demand continues to be tepid. Additionally, finished stocks and deliveries edged closer to a neutral stance, registering at 50.4 and 48.4, respectively.

Catherine Beard, BusinessNZ's Director of Advocacy, , noted slight improvement in April but also increase in negative sentiment among businesses. She highlighted that "the proportion of negative comments again increased to 69%, compared with 65% in March and 62% in February," with lack of sales and orders being a recurrent concern alongside the broader struggles of the economy.

BNZ Senior Economist Doug Steel provided further insights, stating that "the PMI this year to date is consistent with manufacturing GDP trailing year earlier levels." He also noted that the details for April were "a bit more mixed," and they presented a less uniformly weak picture than in recent months.

Looking ahead

UK GDP is the main focus in European while production and trade balance will also be released. Italy will publish industrial output. Later in the day, Canada employment will take center stage. US will release U of Michigan consumer sentiment too.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8593; (P) 0.8607; (R1) 0.8623; More...

Intraday bias in EUR/GBP stays mildly on the upside at this point, and further rally could be seen to 0.8643 resistance. Firm break there will resume the choppy rebound from 0.8497 low. On the downside, below 0.8585 minor support will argue that rebound from 0.8529 has completed, and larger fall might finally be ready to resume. Intraday bias will be back on the downside for 0.8529 support first.

In the bigger picture, outlook remains bearish as EUR/GBP is capped below medium term falling trendline. That is, down trend from 0.9267 (2022 high) is still in progress. Firm break of 0.8491/7 will target 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Apr | 48.9 | 47.1 | 46.8 | |

| 23:30 | JPY | Overall Household Spending Y/Y Mar | -1.20% | -2.40% | -0.50% | |

| 23:50 | JPY | Current Account (JPY) Mar | 2.01T | 2.05T | 1.37T | |

| 05:00 | JPY | Eco Watchers Survey: Current Apr | 47.4 | 49.8 | ||

| 06:00 | GBP | GDP M/M Mar | 0.10% | 0.10% | ||

| 06:00 | GBP | GDP Q/Q Q1 P | 0.40% | -0.30% | ||

| 06:00 | GBP | Manufacturing Production M/M Mar | -0.50% | 1.20% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Mar | 1.80% | 2.70% | ||

| 06:00 | GBP | Industrial Production M/M Mar | -0.50% | 1.10% | ||

| 06:00 | GBP | Industrial Production Y/Y Mar | 0.30% | 1.40% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) Mar | -14.5B | -14.2B | ||

| 08:00 | EUR | Italy Industrial Output M/M Mar | 0.30% | 0.10% | ||

| 12:30 | CAD | Net Change in Employment Apr | 17.5K | -2.2K | ||

| 12:30 | CAD | Unemployment Rate Apr | 6.20% | 6.10% | ||

| 13:00 | GBP | NIESR GDP Estimate (3M) Apr | 0.40% | |||

| 14:00 | USD | Michigan Consumer Sentiment Index May P | 77 | 77.2 |

NZ BNZ manufacturing rises to 48.9, signs of life despite prolonged contraction

New Zealand BusinessNZ Performance of Manufacturing Index rose from 46.8 to 48.9 in April. Despite this improvement, the sector remains in contraction for the 14th consecutive month.

Breaking down the components of the index, there were some positive developments in April. Production notably increased to 50.8 from 46.0, and employment also rose to 50.8 from 46.8, both crossing into expansion territory. However, new orders still lagged behind, albeit with a slight improvement to 45.3 from 44.6, indicating that demand continues to be tepid. Additionally, finished stocks and deliveries edged closer to a neutral stance, registering at 50.4 and 48.4, respectively.

Catherine Beard, BusinessNZ's Director of Advocacy, , noted slight improvement in April but also increase in negative sentiment among businesses. She highlighted that "the proportion of negative comments again increased to 69%, compared with 65% in March and 62% in February," with lack of sales and orders being a recurrent concern alongside the broader struggles of the economy.

BNZ Senior Economist Doug Steel provided further insights, stating that "the PMI this year to date is consistent with manufacturing GDP trailing year earlier levels." He also noted that the details for April were "a bit more mixed," and they presented a less uniformly weak picture than in recent months.

Fed’s Daly discusses dual scenarios for interest rate amid inflation uncertainty

San Francisco Fed President Mary Daly articulated the challenges surrounding US inflation, describing it as likely to be a "bumpy ride" going forward. In her comments yesterday, Daly highlighted there is "uncertainly about what the next few months of inflation will look like".

Daly presented two potential scenarios that could influence Fed's interest rate decisions. In the first scenario, if inflation continues on its recent downward trend alongside a cooling job market, Daly noted that lowering interest rates would be appropriate.

Conversely, Daly outlined a second scenario where inflation does not decline as expected but instead remains stagnant, as observed in the first quarter of this year. In such a situation, Daly stated that it would not be appropriate to cut interest rates, unless there is a concurrent weakening in the job market.

BoE’s Pill signals rate cut discussions in upcoming meetings

BoE Chief Economist Huw Pill expressed growing confidence in the possibility of lowering interest rates and stated that the committee would start discussing it "over the next few meetings".

"We're growing more and more confident that we can begin to reduce the restriction that monetary policy is putting in the economy and start to cut interest rate," Pill said at a Q&A session organized by the central bank yesterday.

Pill emphasized that the Bank is not quite ready to make these adjustments, stating, "We're not quite there yet, and we need more evidence."

Yet, he also mentioned, "In the absence of big new disturbances in the economy, we're going to be thinking about moving interest rates over the next few meetings."

This commentary came after the Bank's decision to maintain the interest rate at 5.25%, a decision supported by an 8-2 vote. Deputy Governor Dave Ramsden joined Swati Dhingra, the usual dove, in voting for a rate cut, signaling a slight shift towards a more dovish stance within policy-setting committee.

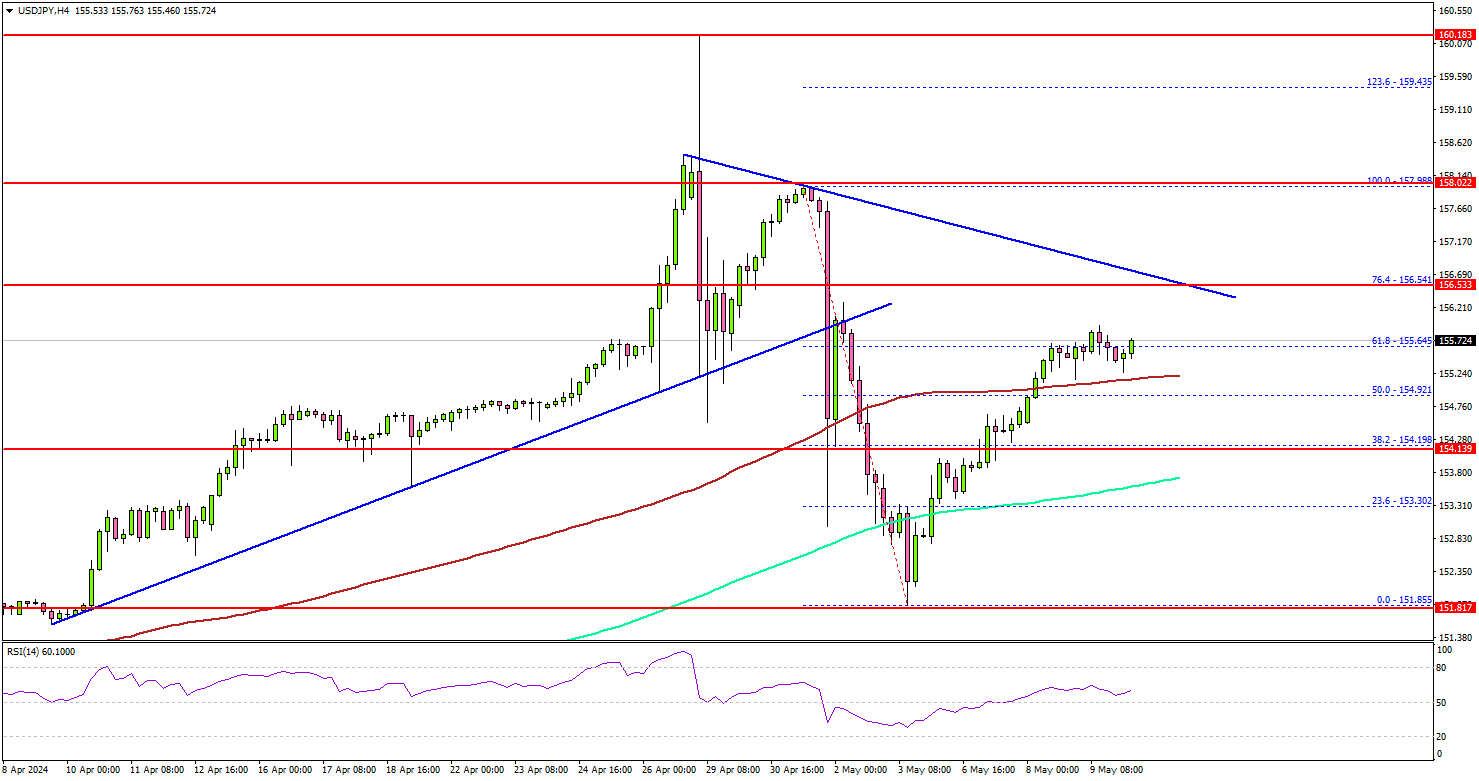

USD/JPY – Upsides Could Be Capped Near 156.50

Key Highlights

- USD/JPY started a recovery wave above the 154.00 resistance.

- A major bearish trend line is forming with resistance at 156.50 on the 4-hour chart.

- EUR/USD could aim for a steady increase if it clears 1.0820.

- Oil prices are facing many hurdles near $80.80 and $81.80.

USD/JPY Technical Analysis

The US Dollar found support at 151.85 and started a steady upward move against the Japanese Yen. USD/JPY cleared the 153.20 and 154.00 resistance levels.

Looking at the 4-hour chart, the pair surpassed the 50% Fib retracement level of the downward move from the 157.98 swing high to the 151.85 low. It also settled above the 100 simple moving average (red, 4-hour) and tested the 200 simple moving average (green, 4-hour).

However, there are a couple of hurdles waiting to prevent upsides. Immediate resistance is near the 156.20 level. The first major resistance is near 156.50.

There is also a major bearish trend line forming with resistance at 156.50 on the same chart. The trend line is close to the 76.4% Fib retracement level of the downward move from the 157.98 swing high to the 151.85 low.

A clear move above the 156.50 resistance might send it toward the 158.00 level. Any more gains might call for a move toward the 160.00 level in the near term.

Immediate support is near the 155.20 level and the 200 simple moving average (green, 4-hour). The next major support is at 154.00. If there is a downside break below the 154.10 support, the pair might test 153.50 and the 100 simple moving average (red, 4-hour). Any more losses might send the pair toward 152.20.

Looking at EUR/USD, the pair is consolidating, and the bulls might soon aim for an upside break above the 1.0820 resistance.

Economic Releases

- UK GDP Q1 2016 (Preliminary) (QoQ) - Forecast +0.4%, versus -0.3% previous.

- Fed's Kashkari speech.

- Fed's Logan speech.

Cliff Notes: Staying the Course

Key insights from the week that was.

Please complete this form before arriving for your appointment In Australia, the RBA Board left the cash rate unchanged at 4.35%. This decision, following an upside surprise on inflation data and stronger-than-expected labour market data but weaker partials for consumption, highlights the Board’s cautious approach amid volatile data.

The Board is certainly not ignoring incoming information regarding inflation. Refreshed staff projections incorporate recent upside momentum into both the headline and trimmed mean inflation forecasts, the year-end figures revised up from 3.2% and 3.1% to 3.8% and 3.4% respectively. Dec-25 and Jun-26 were unchanged, however. The profile for unemployment is slightly firmer too, Dec-24 and Dec-25 revised down 0.1ppt to 4.2% and 4.3% respectively. The weak state of consumption meanwhile saw year-end GDP revised down from 1.8% to 1.6% for 2024. 2025-26 is unchanged.

As discussed by Chief Economist Luci Ellis in a video update mid-week, we view the Board’s forecasts, language and ultimate decision as striking a delicate balance. Recent data has put the Board back on high alert for further near-term upside risks. But, the Board’s confidence in returning inflation sustainably to target in the medium-term without undue cost to the economy remains. Rate cuts are therefore unlikely to be delivered until late in the year, November being our forecast for the first move, with policy relief ensuing at a measured pace thereafter – 25bp per quarter, taking the cash rate to 3.10% at Q4 2025.

Highlighting the consequence of elevated inflation and rates for the consumer, real retail sales contracted again in Q1, declining –0.4% (–1.3%yr). The modest gain in nominal sales (0.2%) suggests retail prices posted a solid increase (0.6%) despite enduring weakness in sales volumes. Perhaps even more stark, real retail sales have fallen 5.9% since mid-2022 on a per capita basis – a result that stands in stark contrast to most other advanced economies. Alongside other consumption partials for vehicle and fuel sales, this release suggests consumer spending was near flat in Q1.

Next week on May 14, the Federal Government will deliver Budget 2024/25. For more detail, see our preview published earlier this week. For more information on our broader views on the state of the domestic and global economy, our latest Market Outlook will be published today on WestpacIQ.

The international data flow has been relatively quiet this week, leaving last Friday’s US employment and ISM services reports front of mind. Much has already been written about these releases, so we will be brief. Key is that April saw a material step down in the pace of nonfarm payrolls growth, to 175k from 269k per month in the three months to March. Household survey employment was weak again at 25k (having averaged 94k per month in Q1) and average hourly earnings were benign, rising just 0.2%. One month does not make a trend, but the labour market continuing on this path is consistent with US inflation sustainably returning near target.

Ahead, the FOMC will have to scrutinise downside risks for activity and the labour market more closely. Both the ISM surveys, but particularly the services measure, are pointing to outright job losses in coming months. This week’s Senior Loan Officers Survey for April also highlighted that banks continue to tighten standards across most lines of lending. Credit demand from businesses and households was also said to have weakened broadly in the last reporting period.

Turning to the UK, in their May meeting communications, the Bank of England’s MPC made clear a return to target inflation is within sight and consequently that they will likely be able to ease policy soon. Indeed, two members of the MPC voted for a 25bp cut at this meeting and “Conditioned on market interest rates [which include several rate cuts]… CPI inflation is [now] projected to be 1.9% in two years’ time and 1.6% in three years”, below the BoE’s 2.0% medium-term target. Demand has certainly been weaker in the UK than many other developed markets, particularly the US; but this revised projection highlights the success policy makers are having globally in the fight against inflation.

Bank of England Closing In On Rate Cuts

Summary

- The Bank of England (BoE) held its policy rate at 5.25% at today's monetary policy announcement, but offered a dovish outlook that suggests rate cuts are now approaching.

- The BoE said restrictive monetary policy is weighing on activity in the real economy, is leading to a looser labor market and is bearing down on inflationary pressures. That is reflected in the BoE's updated economic projections. The inflation forecast of 1.9% in two years' time suggests the BoE is very close to easing, in our view, while the inflation forecast of 1.6% in three years suggests the BoE might lower interest rates more quickly than markets currently expect.

- A June rate cut would likely require consistently favorable price and wage data, and for three more BoE policymakers to switch their vote from "hold" to "cut" within one meeting. While those outcomes are possible, they are perhaps not probable. For now, therefore, we remain comfortable with our current outlook which sees the Bank of England delivering an initial 25 bps rate cut to 5.00% at its August meeting, an outcome that is fully priced by market participants. We also forecast 25 bps rate cuts in November and December, for a cumulative 75 bps of easing this year, more than the 60 bps currently reflected in market pricing.

Bank of England Holds Steady, Offers A Dovish Outlook

The Bank of England (BoE) held its policy rate steady at 5.25% at today's monetary policy announcement, an outcome that was unanimously expected by economists. While the Bank of England did not explicitly signal near-term easing in its accompanying statement, there were several dovish elements that suggest rate cuts are approaching. For now, we maintain our call for an initial 25 bps BoE rate cut in August, while acknowledging that the risk of an earlier June move has increased.

Among the key elements of the Bank of England's announcement:

- the restrictive stance of monetary policy is weighing on activity in the real economy, is leading to a looser labor market, and is bearing down on inflationary pressures.

- key indicators of inflation persistence are moderating broadly as expected, although they remain elevated.

- importantly, the BoE repeated that "monetary policy will need to remain restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term" and that it "will keep under review for how long Bank Rate should be maintained at its current level."

- policymakers voted 7-2 to hold rates steady compared to the 8-1 vote split at the previous meeting. A second policymaker joining the rate cut camp represents a dovish development.

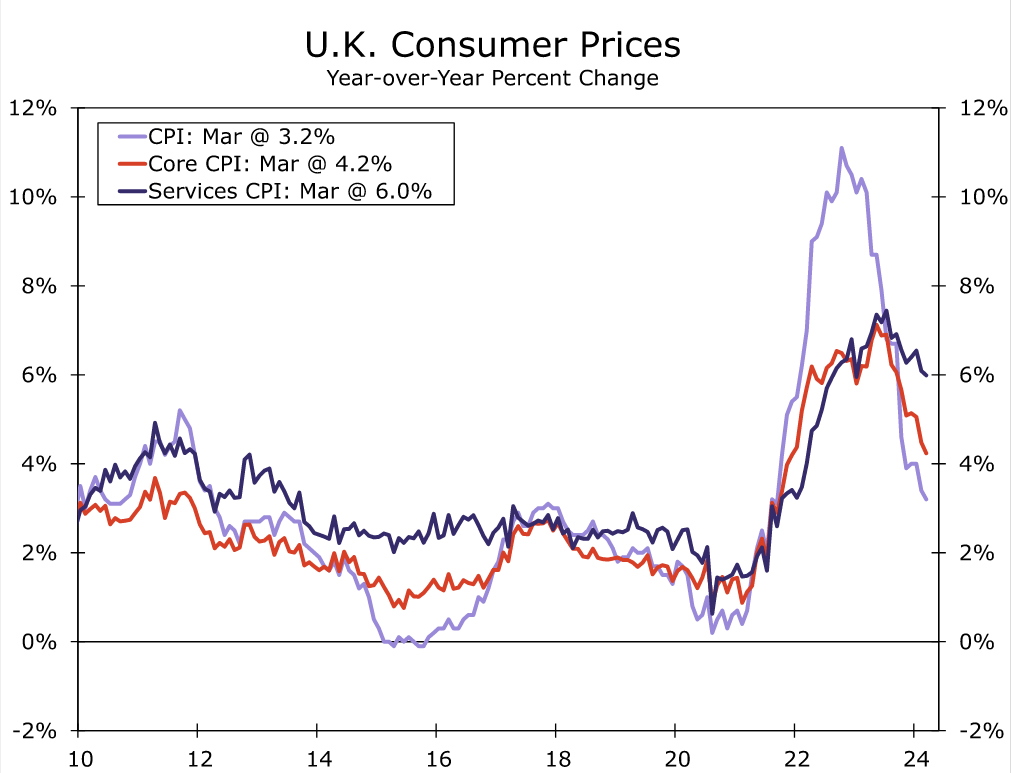

The Bank of England's updated economic projections are also informative, in our view. Based on market-implied interest rates, the BoE sees inflation slowing close to 2% in Q2-2024 before rebounding close to around 2.5% later this year. The BoE forecasts inflation at 1.9% in two years' time, and 1.6% in three years. The forecast of inflation close to target in two years suggests to us that the BoE is very close to beginning its rate cut cycle, while the forecast of below-target inflation in three years suggests the BoE may lower interest rates more quickly than markets currently anticipate.

The overall dovish message was reinforced by BoE Governor Bailey who said he was optimistic things are moving in the right direction, that more evidence was needed regarding inflation staying low before a rate cut, and that he expected inflation to fall close to target in the next two months. Bailey said that a June rate cut is not ruled out or a done deal, and more broadly that interest rates may fall more sharply than markets expect.

In terms of reviewing how long the policy rate should stay at its current level, the Bank of England said it will continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labor market conditions, wage growth and services price inflation. In that context, we expect the key upcoming U.K. data releases ahead of the Bank of England's next monetary policy announcement on 20 June will be March wage data (14 May), April CPI (22 May), April wage data (11 June) and the May CPI (19 June). Should those wage and price data prove to be consistently favorable, which is clearly a distinct possibility, we expect the Bank of England would be comfortable beginning a rate cut cycle in June. That said, U.K. price and wage data have had some tendency to disappoint during the current disinflation process. Moreover, a June rate cut would require three policymakers to switch their vote from "hold" to "cut" within one meeting, a not insignificant shift. For now, therefore, we remain comfortable with our current outlook which sees the Bank of England delivering an initial 25 bps rate cut to 5.00% at its August meeting, an outcome that is fully priced by market participants. We also forecast 25 bps rate cuts in November and December, for a cumulative 75 bps of easing this year, more than the 60 bps currently reflected in market pricing. That outlook is also consistent with the Bank of England's signal that rates might be lowered more quickly than markets expect.