Sample Category Title

(BOE) Bank rate maintained at 5.25%

Monetary Policy Summary, May 2024

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 8 May 2024, the MPC voted by a majority of 7–2 to maintain Bank Rate at 5.25%. Two members preferred to reduce Bank Rate by 0.25 percentage points, to 5%.

The Committee's updated projections for activity and inflation are set out in the accompanying May Monetary Policy Report and are conditioned on a market-implied path for Bank Rate that declines from 5¼% to 3¾% by the end of the forecast period, compared with an endpoint of 3¼% in February.

Internationally, recent growth outturns have tended to be stronger in the United States than in the euro area. Underlying inflationary pressures in both regions have continued to moderate somewhat since the start of the year, though by less than expected in the United States. Forward interest rates have risen in the United States and, as a result, elsewhere.

Following modest weakness last year, UK GDP is expected to have risen by 0.4% in 2024 Q1 and to grow by 0.2% in Q2. Despite picking up during the forecast period, demand growth is expected to remain weaker than potential supply growth throughout most of that period. A margin of economic slack is projected to emerge during 2024 and 2025 and to remain thereafter, in part reflecting the continued restrictive stance of monetary policy.

With respect to indicators of inflation persistence, services consumer price inflation has declined but remains elevated, at 6.0% in March. There remains considerable uncertainty around statistics derived from the ONS Labour Force Survey. It is therefore more difficult to gauge the evolution of the labour market. Based on a broad set of indicators, the MPC judges that the labour market continues to loosen but that it remains relatively tight by historical standards. Annual private sector regular average weekly earnings growth declined to 6.0% in the three months to February, although that series tends to be volatile. Alternative indicators also suggest easing pay growth.

Twelve-month CPI inflation fell to 3.2% in March from 3.4% in February. CPI inflation is expected to return to close to the 2% target in the near term, but to increase slightly in the second half of this year, to around 2½%, owing to the unwinding of energy-related base effects. There continue to be upside risks to the near-term inflation outlook from geopolitical factors, although developments in the Middle East have had a limited impact on oil prices so far.

Conditioned on market interest rates and reflecting a margin of slack in the economy, CPI inflation is projected to be 1.9% in two years' time and 1.6% in three years in the May Report.

The MPC's remit is clear that the inflation target applies at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognises that there will be occasions when inflation will depart from the target as a result of shocks and disturbances. Monetary policy will ensure that CPI inflation returns to the 2% target sustainably in the medium term.

At this meeting, the Committee voted to maintain Bank Rate at 5.25%. Headline CPI inflation has continued to fall back, in part owing to base effects and external effects from goods prices. The restrictive stance of monetary policy is weighing on activity in the real economy, is leading to a looser labour market and is bearing down on inflationary pressures. Key indicators of inflation persistence are moderating broadly as expected, although they remain elevated.

Monetary policy will need to remain restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term in line with the MPC's remit. The Committee has judged since last autumn that monetary policy needs to be restrictive for an extended period of time until the risk of inflation becoming embedded above the 2% target dissipates.

The MPC remains prepared to adjust monetary policy as warranted by economic data to return inflation to the 2% target sustainably. It will therefore continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation. The Committee will consider forthcoming data releases and how these inform the assessment that the risks from inflation persistence are receding. On that basis, the Committee will keep under review for how long Bank Rate should be maintained at its current level.

Minutes of the Monetary Policy Committee meeting ending on 8 May 2024

1: Before turning to its immediate policy decision, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices. The latest data on these topics were set out in the accompanying May 2024 Monetary Policy Report.

2: The MPC discussed developments in consumer price inflation in the United States and in the euro area. In the United States, recent outturns had been higher than expected by market participants on both headline and core PCE inflation. The evidence suggested that this higher-than-expected inflation had reflected surprisingly strong domestic demand rather than inflation persistence. Euro-area inflation data had been more in line with market expectations, and demand had remained relatively subdued. The increased divergence in demand across regions could be consistent with a divergence in monetary policy, with potential implications for exchange rates and broader financial conditions.

3: Given this change in the perceived outlook for US demand and inflation, market participants had revised their expectations for US monetary policy since the MPC's previous meeting, pushing out the expected timing and degree of future reductions in the federal funds rate. Alongside this, the market-implied path for policy rates in other major advanced economies, including the United Kingdom, had also shifted up materially, though by less.

4: The Committee discussed the degree to which these moves in UK interest rates had reflected global or domestic factors. This was not straightforward to separate out. The correlation between US and UK market interest rates had been near the top of its historical range, and the sensitivity of UK rates to both US and domestic data outturns had remained elevated. Nevertheless, market contacts had begun to judge that the increasing divergence of the US outlook from that of other major advanced economies could be reflected in their monetary policies in the near term. That said, contacts had expected that the influence of global factors could lead to greater macroeconomic and monetary policy convergence across major advanced economies beyond 2024.

5: In the United Kingdom, all but one of the respondents to the Bank's latest Market Participants Survey (MaPS) had expected Bank Rate to be left unchanged at this MPC meeting. They had also all expected the next move in Bank Rate to be downwards. The median expected profile for Bank Rate from MaPS implied a cumulative 75 basis point reduction in Bank Rate this year, similar to the profile from the March MaPS, despite the increase in the UK yield curve.

6: Turning to activity, UK GDP growth had strengthened since the start of the year, reversing the fall in output that was estimated to have occurred in the second half of 2023. The Committee expected the recovery in output to be underpinned by a pickup in household consumption, supported by higher real incomes.

7: The Committee discussed the risks around the near-term outlook for consumer spending. House price inflation had held up by more than had been expected, which could suggest upside risks to the outlook for spending. One potential explanation for this would be that higher interest rates had weighed on house prices by less than had been expected. Set against that, a modest expected rise in unemployment could pose downside risks to consumption, for example if those households not directly affected nevertheless chose to save more for precautionary reasons.

8: The Committee discussed the degree of persistence in UK wage growth and domestic price inflation. Consistent with the recent easing in short-term inflation expectations and a loosening in the labour market, wage growth had fallen somewhat further. Services consumer price inflation had also continued to ease. Although both wage growth and services price inflation had been slightly higher than expected in the February Monetary Policy Report, that difference was small in the context of typical data volatility. Both series still indicated elevated domestic inflationary pressures.

9: The Committee discussed the relative weights to put on different indicators of inflation persistence, particularly in the event that they were to give divergent signals in the future. There remained considerable uncertainty around estimates of labour market tightness derived from the Labour Force Survey (LFS), owing to small sample sizes. A range of labour market indicators, including the vacancies to unemployment ratio and survey indicators of recruitment difficulties, suggested that the labour market had continued to loosen, however, while remaining relatively tight by historical standards.

10: Although less severe than the issues surrounding the LFS, the Committee noted that the private sector regular average weekly earnings (AWE) series tended to be volatile, especially when compared with services price inflation. While AWE growth had fallen sharply since last year, the decline suggested by other indicators appeared more gradual and from a lower peak. Possibly reflecting past falls in real wages and a relatively tight labour market, nominal pay growth had continued to be elevated.

11: The appropriate weight to place on different indicators of inflation persistence would also depend on wider economic developments. Depending on the expected path for demand, for example, indicators of inflation persistence might be expected to diverge. In an environment of subdued demand, firms might be expected to absorb higher wage growth into their profit margins. Higher wage growth would then not pass through to higher services price inflation. But as demand recovered, firms might choose to pass through that wage growth, resulting in higher services price inflation. Initial reports indicated that the Agents' contacts generally expected lower pass-through of higher labour costs to prices than last year, owing to weaker demand. Consumer-facing services firms surveyed in the Decision Maker Panel in the three months to April had said that they expected to raise prices by 4.7% over the next year. The Committee would consider evidence from different indicators of persistence and would continue to monitor them in context.

The immediate policy decision

12: The MPC sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment.

13: Indicators of inflation persistence had evolved broadly as expected, albeit a little stronger than had been anticipated in the February Monetary Policy Report.

14: Services consumer price inflation had declined but remained elevated, at 6.0% in March. Higher-frequency measures of services price inflation showed somewhat more of a slowdown than annual rates but still indicated elevated domestic inflationary pressures. Services price inflation was expected to continue to ease gradually over the course of this year, as wage growth and indirect effects from energy and other goods prices weakened further.

15: There remained considerable uncertainty around statistics derived from the ONS Labour Force Survey. It was therefore more difficult to gauge the evolution of the labour market. Based on a broad set of indicators, the MPC judged that the labour market continued to loosen but that it remained relatively tight by historical standards. Annual private sector regular average weekly earnings growth had declined to 6.0% in the three months to February, although that series tended to be volatile. Alternative indicators also suggested easing pay growth.

16: The Committee noted that this year's pay settlements, which tended to be concentrated in the early part of the year, would provide an important indication of the extent to which pay growth continued to moderate as expected. Firmer information on April settlements would soon become available, including from the Bank's Agents' intelligence.

17: Twelve-month CPI inflation had fallen to 3.2% in March from 3.4% in February, broadly as expected in the February Report. In the MPC's May Report projections, CPI inflation was expected to return to close to the 2% target in the near term, but to increase slightly in the second half of this year, to around 2½%, owing to the unwinding of energy-related base effects. Conditioned on market interest rates and reflecting a margin of slack in the economy, CPI inflation was projected to be 1.9% in two years' time and 1.6% in three years.

18: There continued to be upside risks to the modal CPI inflation projection from geopolitical factors during the first half of the forecast period, but the risks overall were more evenly balanced over the second half.

19: The MPC's remit was clear that the inflation target applied at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognised that there would be occasions when inflation would depart from the target as a result of shocks and disturbances. Monetary policy would ensure that CPI inflation returned to the 2% target sustainably in the medium term.

20: Monetary policy would need to remain restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term in line with the MPC's remit. The Committee had judged since last autumn that monetary policy needed to be restrictive for an extended period of time until the risk of inflation becoming embedded above the 2% target dissipated. The Committee recognised that the stance of monetary policy could remain restrictive even if Bank Rate were to be reduced, given that it was starting from an already restrictive level.

21: Seven members judged that maintaining Bank Rate at 5.25% was warranted at this meeting. Headline CPI inflation had continued to fall back, in part owing to base effects and external effects from goods prices. The restrictive stance of monetary policy was weighing on activity in the real economy, was leading to a looser labour market and was bearing down on inflationary pressures. Key indicators of inflation persistence were moderating broadly as expected, although they remained elevated. There was a range of views among these members regarding the risks around the assumptions on persistence embodied in the May CPI projection. There was also a range of views about the extent of the evidence that was likely to be needed to warrant a change in Bank Rate, and the degree to which these members anticipated that incremental information in forthcoming data outturns would lead them to update materially their assessment of inflation persistence. All of these members would continue to consider the degree of restrictiveness of policy at each meeting.

22: Two members preferred a 0.25 percentage point reduction in Bank Rate at this meeting. For these members, Bank Rate needed to become less restrictive now to enable a smooth and gradual transition in the policy stance, and to account for lags in transmission. Consumer price inflation was already, and had been for some time, on a firm downward trajectory. The latest forecasts showed inflation returning close to the target in the short term, and this was consistent with forward-looking indicators of output price inflation falling behind input price inflation. As the outlook for demand remained subdued, with vacancies continuing to fall and nominal pay growth easing, the risks to inflation returning sustainably to the target in the medium term were to the downside.

23: The MPC remained prepared to adjust monetary policy as warranted by economic data to return inflation to the 2% target sustainably. It would therefore continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation. The Committee would consider forthcoming data releases and how these informed the assessment that the risks from inflation persistence were receding. On that basis, the Committee would keep under review for how long Bank Rate should be maintained at its current level.

24: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be maintained at 5.25%.

25: Seven members (Andrew Bailey, Sarah Breeden, Ben Broadbent, Megan Greene, Jonathan Haskel, Catherine L Mann and Huw Pill) voted in favour of the proposition. Two members (Swati Dhingra and Dave Ramsden) voted against the proposition, preferring to reduce Bank Rate by 0.25 percentage points, to 5%.

Operational considerations

26: On 8 May, the total stock of assets held for monetary policy purposes was £703 billion, all of which were UK government bonds. The Corporate Bond Purchase Scheme had been fully unwound on 2 April, such that there were now no holdings of sterling non‐financial investment‐grade corporate bonds.

27: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Ben Broadbent

- Swati Dhingra

- Megan Greene

- Jonathan Haskel

- Catherine L Mann

- Huw Pill

- Dave Ramsden

Sam Beckett was present as the Treasury representative.

David Roberts was also present on 30 April and 2 May, as an observer for the purpose of exercising oversight functions in his role as a member of the Bank's Court of Directors.

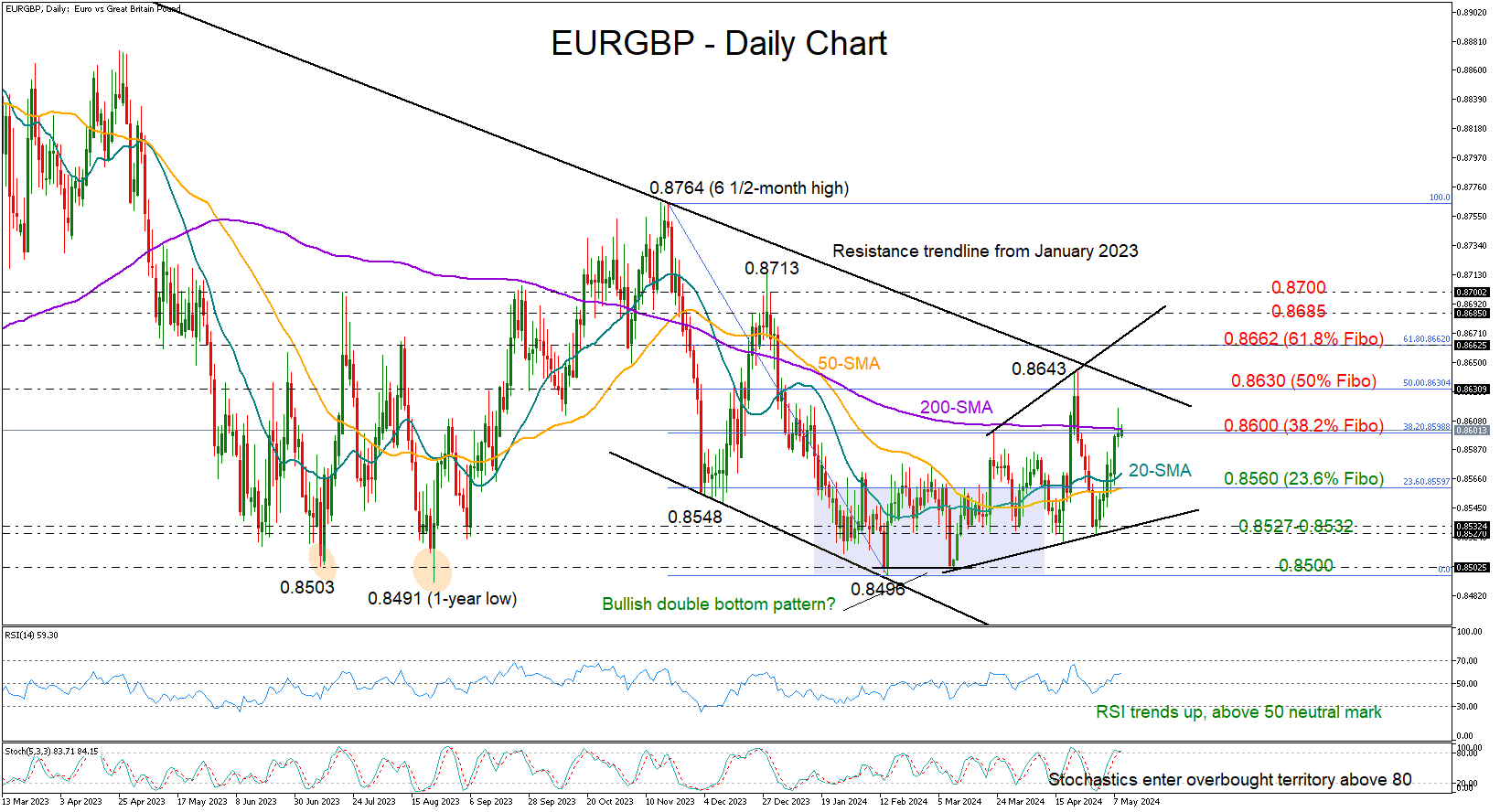

EURGBP Runs Out of Steam Near 0.8600

- EURGBP struggles to surpass 0.8600 and 200-day SMA

- Short-term bias is positive, but signs of oversold market exist

- Bank of England announces rate decision today at 11:00 GMT

EURGBP started May’s session on the right foot, swiftly reversing up after touching the support trendline taken from the March lows.

On Wednesday, the pair reached a high of 0.8616, but it quickly lost most of its gains and closed below the 200-day SMA around 0.8600. The RSI indicates more bullish potential as the price continues to rise, but the stochastic oscillator suggests limited room for improvement.

A step above the 200-day SMA could extend towards the 50% Fibonacci retracement of the November-February downtrend at 0.8630 and the descending trendline drawn from February. Further gains could potentially reach the 61.8% Fibonacci level of 0.8662 and the nearby resistance line. Yet, to access the 0.8700 territory, the bulls might need to secure a close above the 0.8685 constraining zone that eluded them in December.

If the pair remains trapped below 0.8600, it could pivot lower and seek shelter near 0.8559, which is the 23.6% Fibonacci level. If sellers pierce through the latter, the price might tumble towards the familiar 0.8527-0.8532 zone, a break of which might prompt a straight decline to the 0.8500 bottom.

Overall, the market structure of EURGBP appears to be forming a gentle upward pattern, despite ongoing choppiness. The recent crossing of the 20- and 50-day SMAs confirms a gradual bullish movement, although a temporary drop might happen soon, especially if the price holds below 0.8600.

GBP/USD Bulls Struggle While USD/CAD Regains Strength

GBP/USD declined below the 1.2550 support zone. USD/CAD is rising and might aim for more gains above the 1.3760 resistance.

Important Takeaways for GBP/USD and USD/CAD Analysis Today

- The British Pound started a fresh decline from the 1.2635 resistance zone.

- There is a key bearish trend line forming with resistance at 1.2500 on the hourly chart of GBP/USD at FXOpen.

- USD/CAD is showing positive signs above the 1.3685 support zone.

- There is a major bullish trend line forming with support at 1.3720 on the hourly chart at FXOpen.

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair started a fresh decline from the 1.2635 zone. The British Pound traded below the 1.2550 support to move into further a bearish zone against the US Dollar.

The pair even traded below 1.2500 and the 50-hour simple moving average. Finally, the bulls appeared near the 1.2465 level. A low was formed at 1.2467 and the pair recently attempted a recovery wave. The pair climbed above the 1.2485 level.

It tested the 23.6% Fib retracement level of the downward move from the 1.2594 swing high to the 1.2467 low. However, the bears were active near 1.2500.

Immediate resistance on the upside is near a key bearish trend line at 1.2500. The first major resistance is near the 50% Fib retracement level of the downward move from the 1.2594 swing high to the 1.2467 low at 1.2530.

A close above the 1.2530 resistance might spark a steady upward move. The next major resistance is near the 1.2595 zone. Any more gains could lead the pair toward the 1.2635 resistance in the near term.

Initial support on the GBP/USD chart sits at 1.2465. The next major support sits at 1.2440, below which there is a risk of another sharp decline. In the stated case, the pair could drop toward 1.2350.

USD/CAD Technical Analysis

On the hourly chart of USD/CAD at FXOpen, the pair formed a strong support base above the 1.3600 level. The US Dollar started a fresh increase above the 1.3645 resistance against the Canadian Dollar.

The bulls pushed the pair above the 1.3685 and 1.3720 levels. The pair cleared the 50-hour simple moving average and climbed above 1.3750. A high was formed at 1.3760 and the pair is now correcting gains.

There was a minor decline below the 23.6% Fib retracement level of the upward move from the 1.3609 swing low to the 1.3760 high. It is now consolidating near the 1.3720 zone. There is also a major bullish trend line forming with support at 1.3720.

Initial resistance sits near the 1.3735 zone. A clear upside break above 1.3735 could start another steady increase. The next major resistance is the 1.3760 level. A close above the 1.3760 level might send the pair toward the 1.3800 level. Any more gains could open the doors for a test of the 1.3850 level.

Initial support is near the 50-hour simple moving average and 1.3720. The next major support is near 1.3685 on the same USD/CAD chart.

The main support sits near the 76.4% Fib retracement level of the upward move from the 1.3609 swing low to the 1.3760 high at 1.3645. A downside break below the 1.3645 level could push the pair further lower. The next major support is near the 1.3610 support zone, below which the pair might visit 1.3500.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

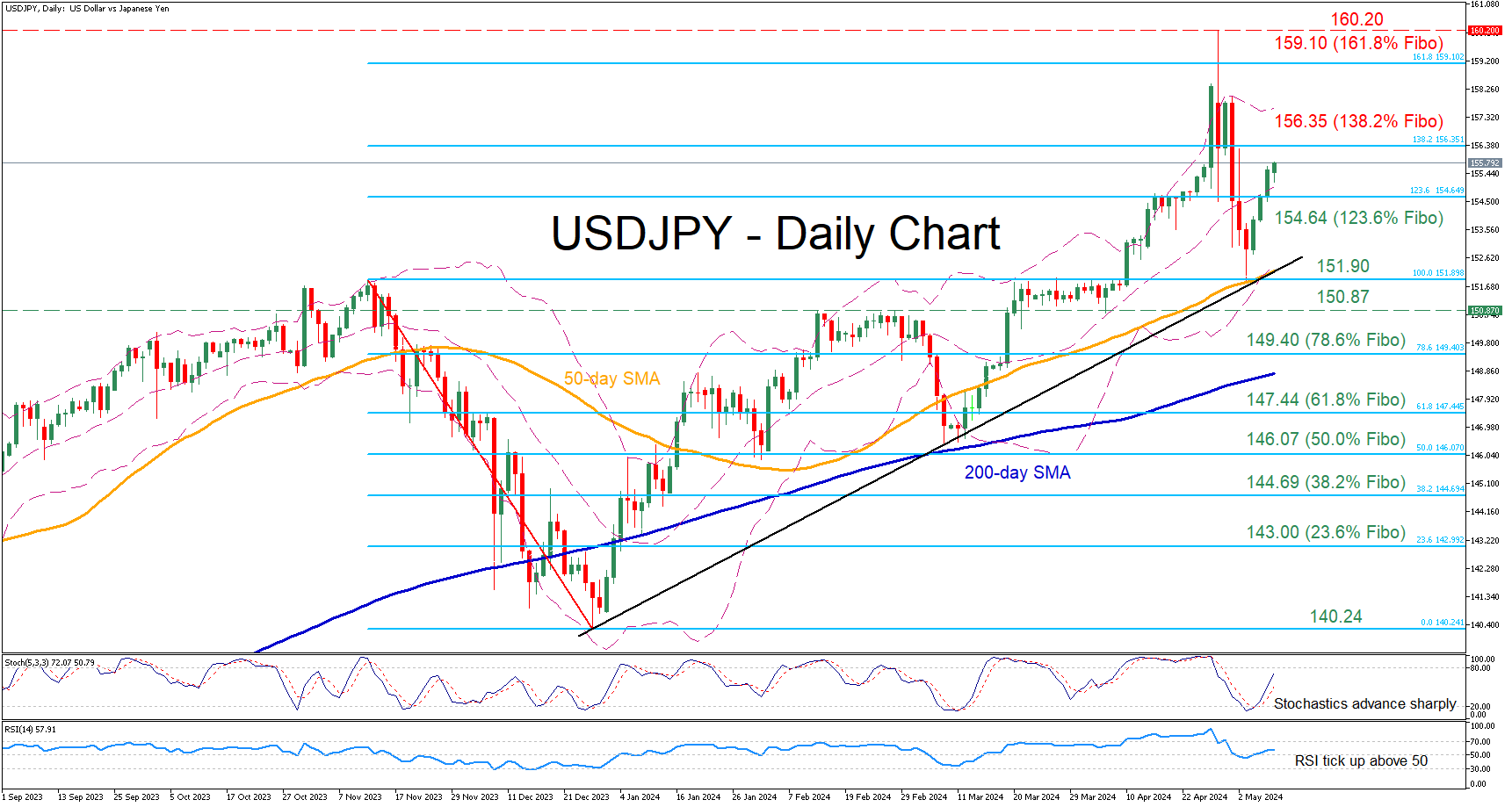

USDJPY Advances After Bouncing Off 50-day SMA

- USDJPY in a recovery mode after pull back comes to a halt

- Momentum indicators suggest intensifying positive momentum

USDJPY experienced a strong pullback from its 34-year high of 160.20 following the intervention by Japanese authorities a week ago. However, the pair managed to find its feet at the 50-day simple moving average (SMA) and recoup a significant part of its recent losses.

Should bullish pressures persist, the price could challenge 156.35, which is the 138.2% Fibonacci extension of the 151.90-140.24 downleg. Further upside attempts could then cease at the 161.8% Fibo of 159.10. Conquering this barricade, the bulls may then attack the 34-year peak of 160.20.

On the flipside, if the pair comes under selling pressure, initial support could be found at the 123.6% Fibo of 154.64. Failing to halt there, the price could descend towards the May deflection point of 151.84, which lies very close to the 50-day SMA. In case of a downside violation, the April support of 150.87 could come under scrutiny.

In brief, after some roller coaster sessions in the aftermath of the Japanese intervention, USDJPY has been in a steady advance towards its recent highs. Therefore, we could see some heightened volatility moving forward as the price approaches levels that the Japanese side seems willing to defend.

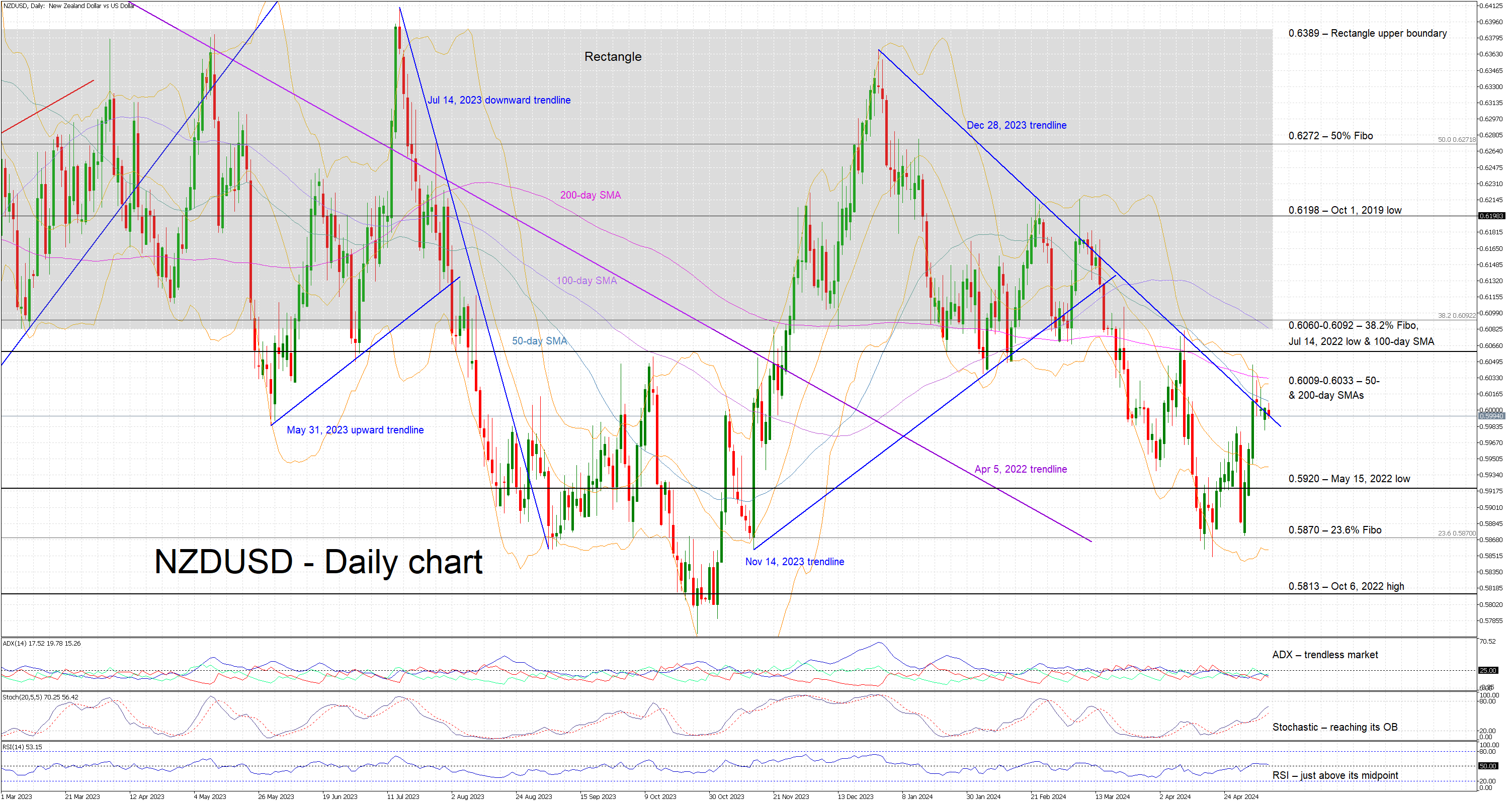

NZDUSD Bulls Face Strong Resistance

- NZDUSD is under pressure following a strong rally from the 2024 lows

- It has met strong resistance at both the 200-day SMA and a key trendline

- Momentum indicators are mixed; a bearish divergence is developing

After testing the 2024 low at 0.5851 and recording a sizeable rally, NZDUSD is now hovering a tad below the 0.6009-0.6033 area. It is trying to record its third consecutive green candle with the upside currently being limited by both the 200-day simple moving average (SMA) and the December 28, 2023 descending trendline. The bears are apparently protecting the developing series of lower highs and lower lows and are possibly preparing for another downleg.

In the meantime, the momentum indicators are mixed. More specifically, the Average Directional Movement Index (ADX) is tentatively hovering below its 25-threshold and thus signalling a trendless market. Similarly, the RSI has climbed above its 50-midpoint, but it appears unable to stage a strong move higher.

More importantly, the stochastic oscillator is edging towards its overbought territory (OB), maintaining a good gap from its moving average. However, a bearish divergence is developing as the lower highs in NZDUSD are countering the higher highs in the stochastics, and thus opening the door to a correction.

If the bulls remain confident, they could try to lead NZDUSD above the 0.6009-0.6033 area, which is populated by the 50- and 200-day SMAs. They could then have a go at testing the resistance set by the 0.6060-0.6092 range, which is defined by the 38.2% Fibonacci retracement, the July 14, 2022 low and the 100-day SMA, and return back inside the one-year-old rectangle.

On the flip side, the bears appear ready to retake the market reins and push NZDUSD below the December 28, 2023 trendline. They could then gradually stage a move towards the May 15, 2022 low at 0.5920 and, if successful, eye the recent 2024 lows.

To sum up, if the bulls want to break the recent series of lower highs and change the market momentum, they need to push NZDUSD back above the 0.6092 level.

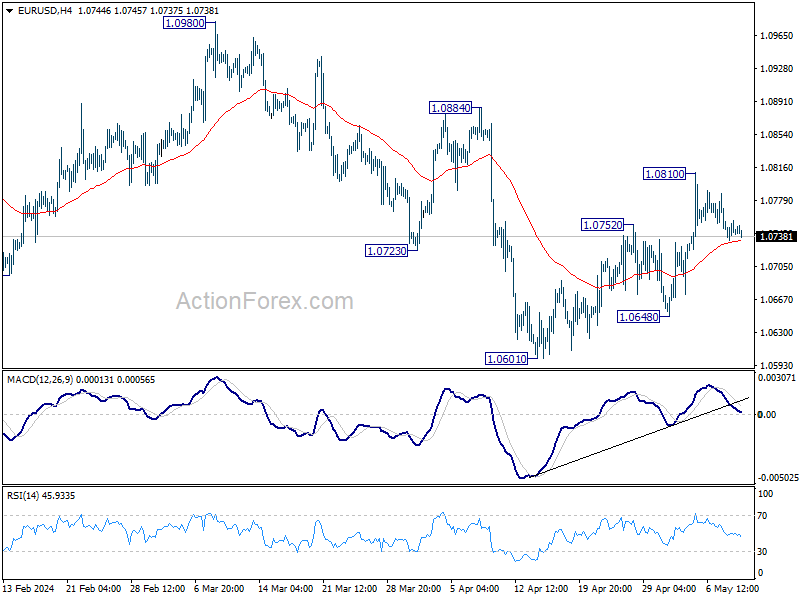

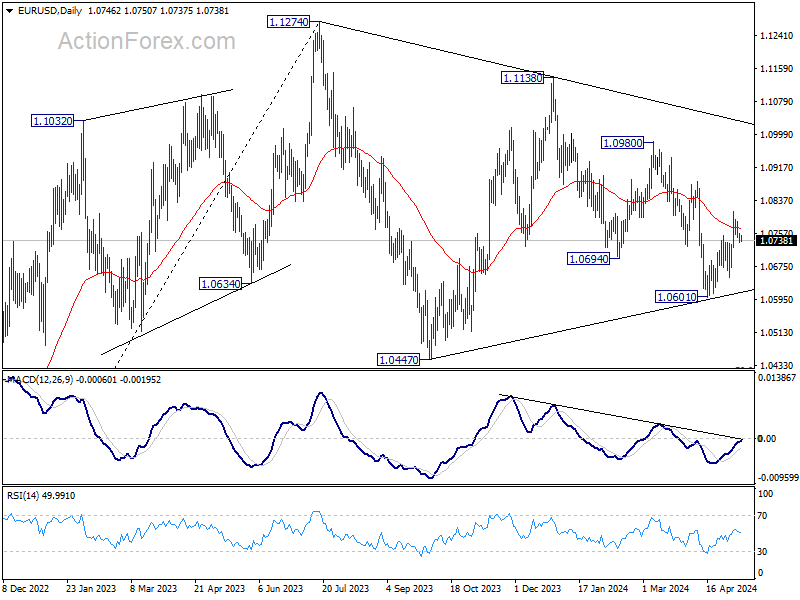

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0736; (P) 1.0747; (R1) 1.0759; More...

Intraday bias in EUR/USD stays neutral and outlook is unchanged. Further rally is expected as long as 55 4H EMA (now at 1.0733) holds. On the upside, above 1.0810 will resume the rebound from 1.0601 to 1.0884 resistance next. However, firm break of 55 4H EMA will argue that the rebound has completed, and turn bias to the downside for 1.0648 support instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

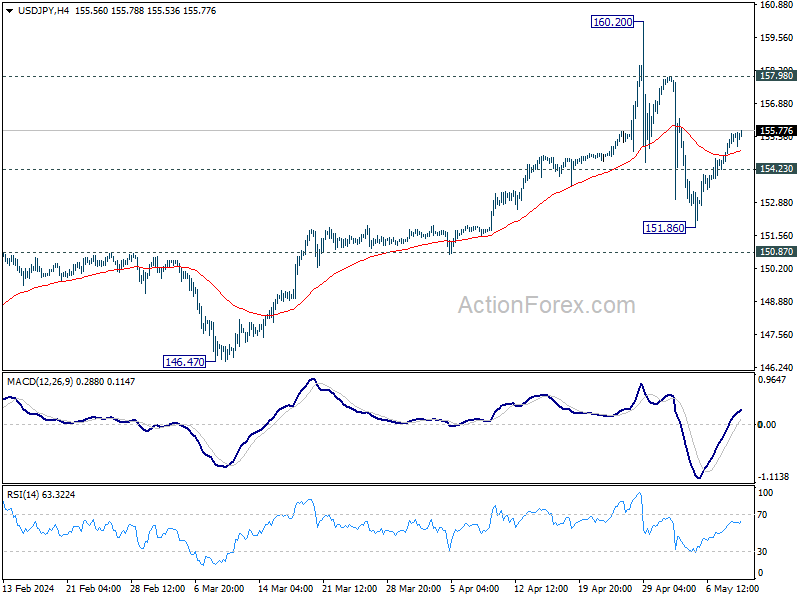

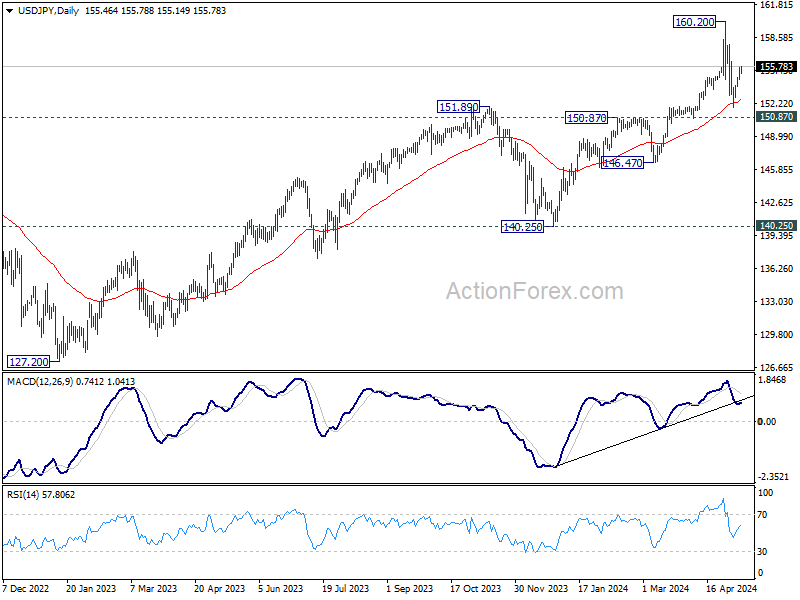

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.76; (P) 155.22; (R1) 155.96; More...

Intraday bias in USD/JPY stays on the upside for the moment. Rebound from 151.86 is seen as the second leg of the corrective pattern from 160.20 high. Further rise would be seen to 157.98 resistance. On the downside, below 154.23 minor support will turn intraday bias neutral.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

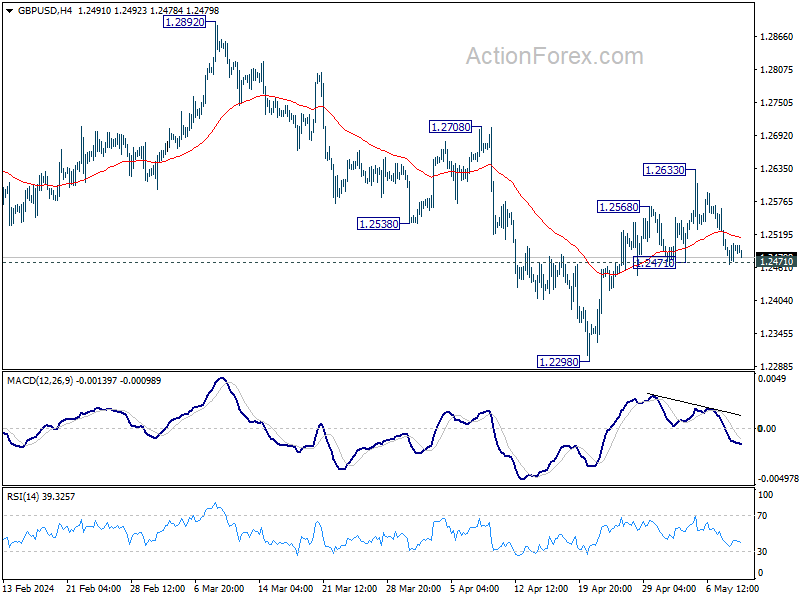

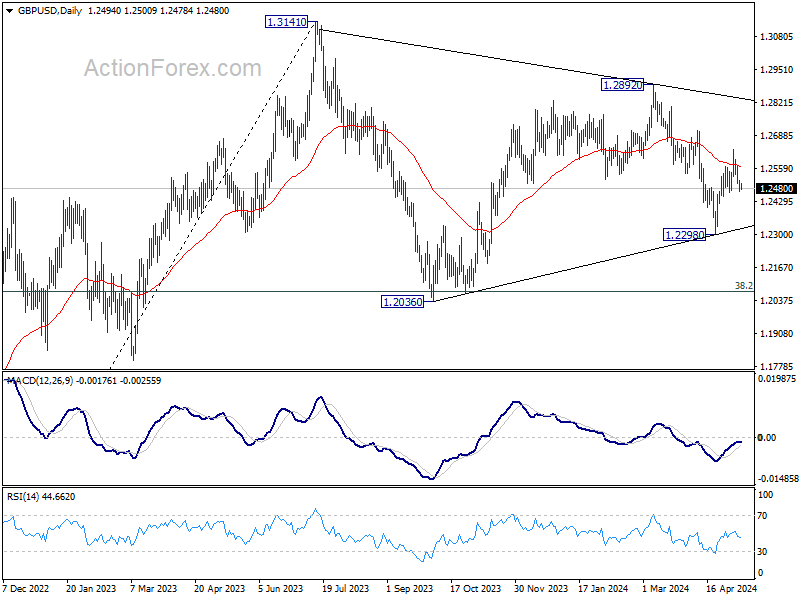

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2468; (P) 1.2497; (R1) 1.2525; More...

Intraday bias in GBP/USD remains neutral and outlook is unchanged. Further rally is in favor with 1.2471 support intact. On the upside, above 1.2633 will resume the rebound from 1.2298 to 1.2708 resistance next. However, firm break of firm break of 1.2471 will indicate that this rebound has completed, and revive near term bearishness. Retest of 1.2298 should then be seen in this case.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

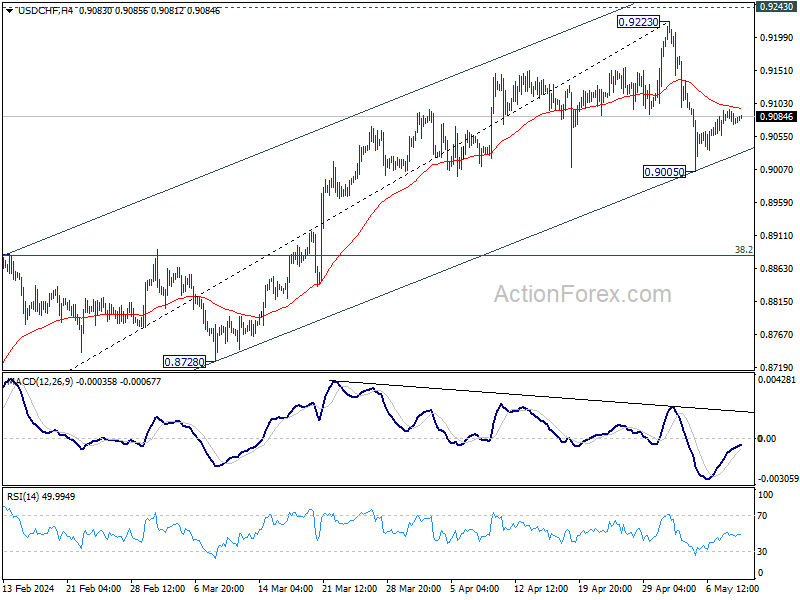

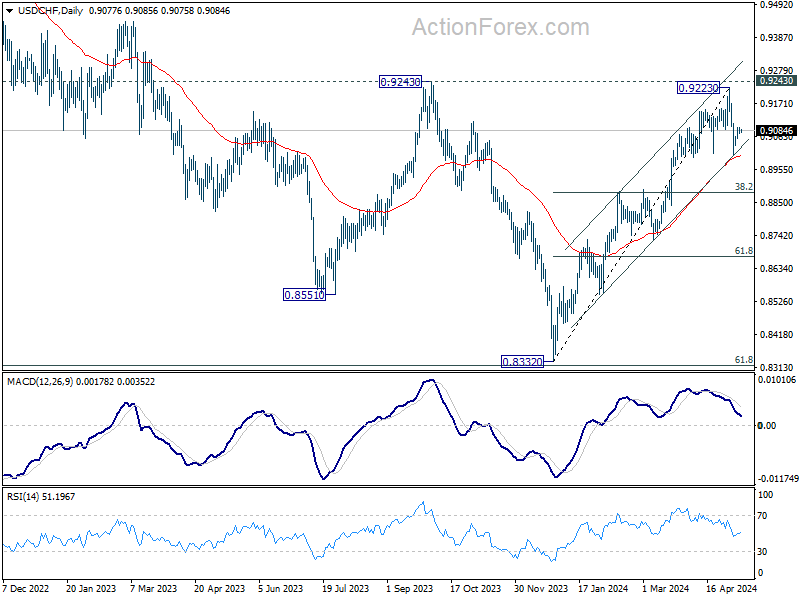

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9071; (P) 0.9083; (R1) 0.9093; More....

Intraday bias in USD/CHF stays neutral at this point. Further decline is in favor as long as 55 4H EMA (now at 0.9096) holds. On the downside, break of 0.9005 and sustained trading below 55 D EMA (now at 0.9000) will bring deeper fall to 38.2% retracement of 0.8332 to 0.9223 at 0.8883. However, firm break of 55 4H EMA will suggest that the pull back has completed, and bring stronger rebound to retest 0.9223 high.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

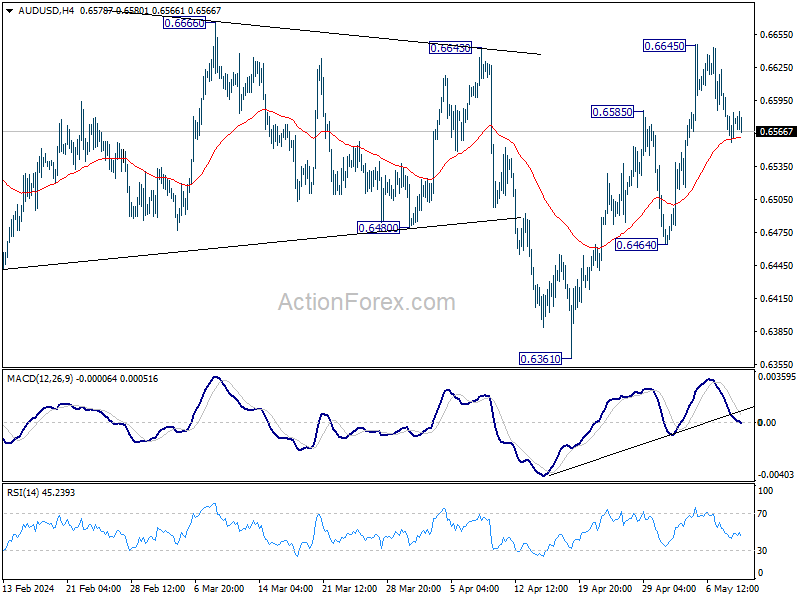

AUD/USD Daily Report

Daily Pivots: (S1) 0.6557; (P) 0.6580; (R1) 0.6602; More...

Intraday bias in AUD/USD remains neutral at this point. Further rise is in favor as long as 55 4H EMA (now at 0.6562) holds. Above 0.6645 will resume the rebound from 0.6361. On the downside, however, firm break of 55 4H EMA will bring deeper fall back to 0.6464 support instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.