Sample Category Title

April CPI Preview: The Clock Is Ticking for a September Cut

Summary

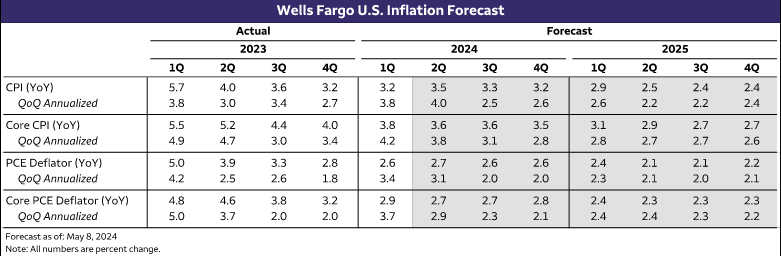

A string of uncomfortably-hot inflation readings in the first quarter leaves a narrow window for inflation to downshift before a late summer rate cut by the Federal Open Market Committee (FOMC) is no longer on the table. We expect the April CPI report to demonstrate that while inflation is not as sticky as the Q1 pace indicated, the journey back to 2% remains slow-going.

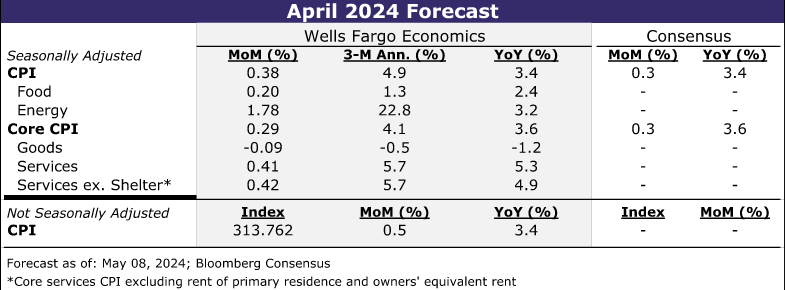

Headline CPI likely rose by 0.4% for a third consecutive month in April, which would leave overall prices running at nearly a 5% three-month annualized rate. Progress in lowering core inflation, however, likely resumed. Excluding food and energy, we estimate prices rose 0.3%, which would break the streak of 0.4% gains since January and push the year-over-year rate down to 3.6%, a three-year low. Ongoing deflation in the goods sector is expected to help keep a lid on core inflation in April, but services are likely to be the bigger driver of the softer print. We look for shelter inflation to have eased a bit further in April, and we anticipate a bigger step-down in core services ex-housing (+0.4% following a 0.6% rise in March).

While inflation has been stubborn in recent months, we do not believe the underlying trend is re-accelerating. Supply chain pressures are not easing as rapidly as a year or two ago, but they are not building either. Shelter inflation looks set to moderate further this year, while services ex-housing inflation should benefit from tamer growth in goods-related input costs and gradual loosening in the labor market. We expect to see monthly inflation prints trend lower over the remainder of the year as a result, with the core CPI subsiding to a 2.8% annualized rate in Q4 and the core PCE easing to a 2.1% annualized rate in Q4.

Downshift Needs to Resume to Keep a September Cut on the Table

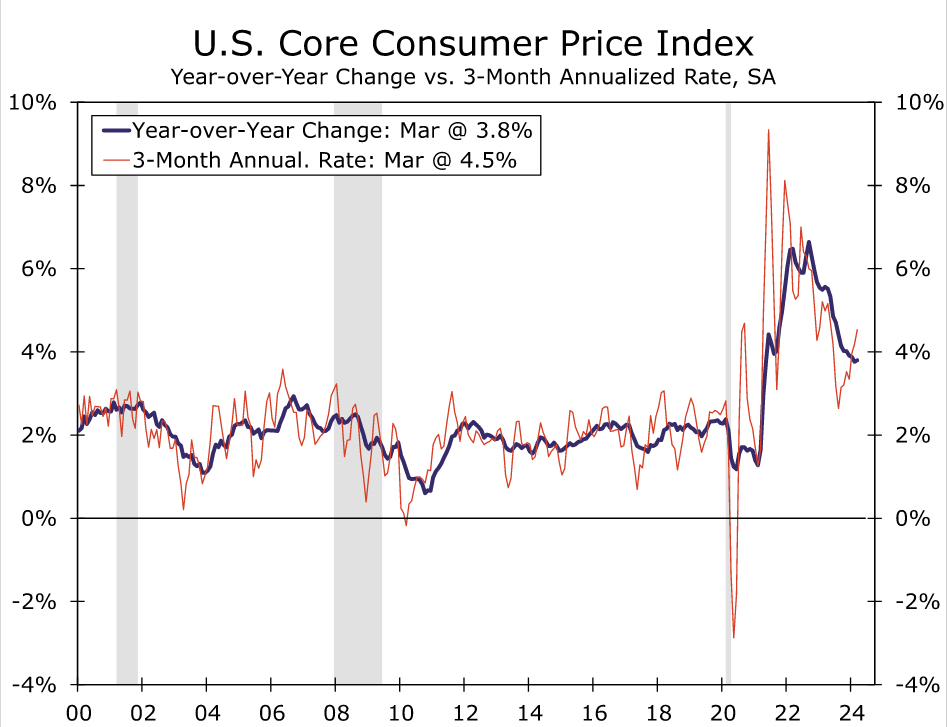

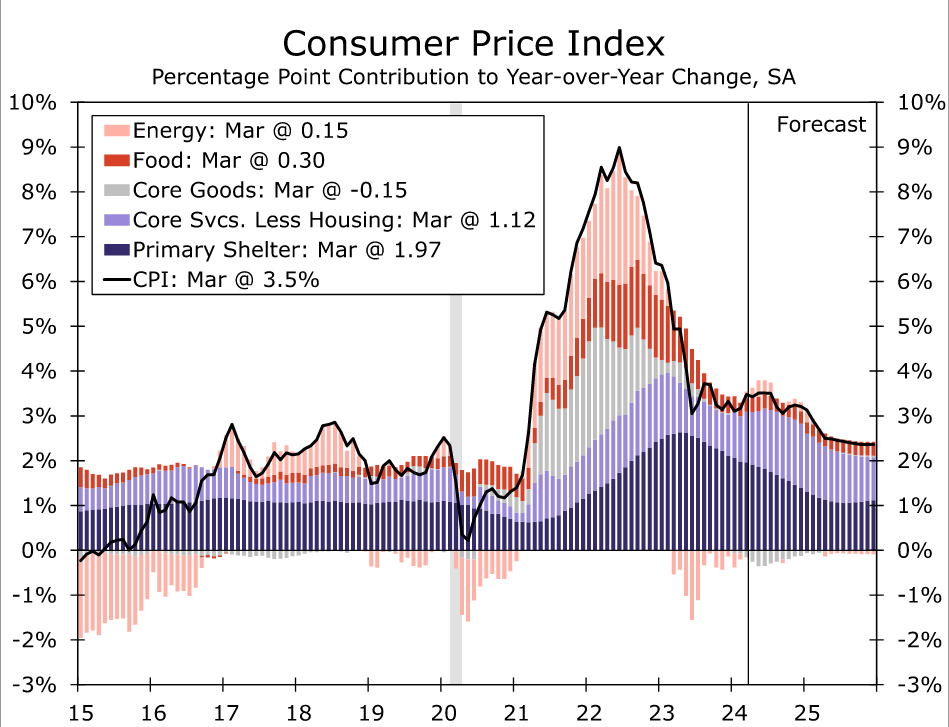

Beginning with the April Consumer Price Index, Q2 inflation data will be crucial in determining whether early-year pricing strength was a brief detour on the road to quieting inflation or if the journey has gotten significantly longer. The FOMC made clear back in January that it would need to see additional benign data to be confident that price growth is on track to return to 2% on a sustained basis before reducing the fed funds target range. However, with core CPI and core PCE in March picking up to three-month annualized rates of 4.5% and 4.4%, respectively, the sufficient confidence has yet to be built (Figure 1). We suspect the FOMC will need to see at least three benign core inflation prints, perhaps even four, before easing policy, absent a rapid deterioration in labor market conditions. Thus, time is running out on the clock for even a late summer rate cut, and it creates the need for core inflation to downshift as soon as the upcoming April CPI report.

We expect to see progress in lowering inflation with the April CPI data, although improvement will likely be slight. Headline CPI looks set for another 0.4% increase, although that should be sufficient for the year-over-year rate to edge down to 3.4%—a tick lower than last month but still above the 3.1% rate registered at the start of the year.

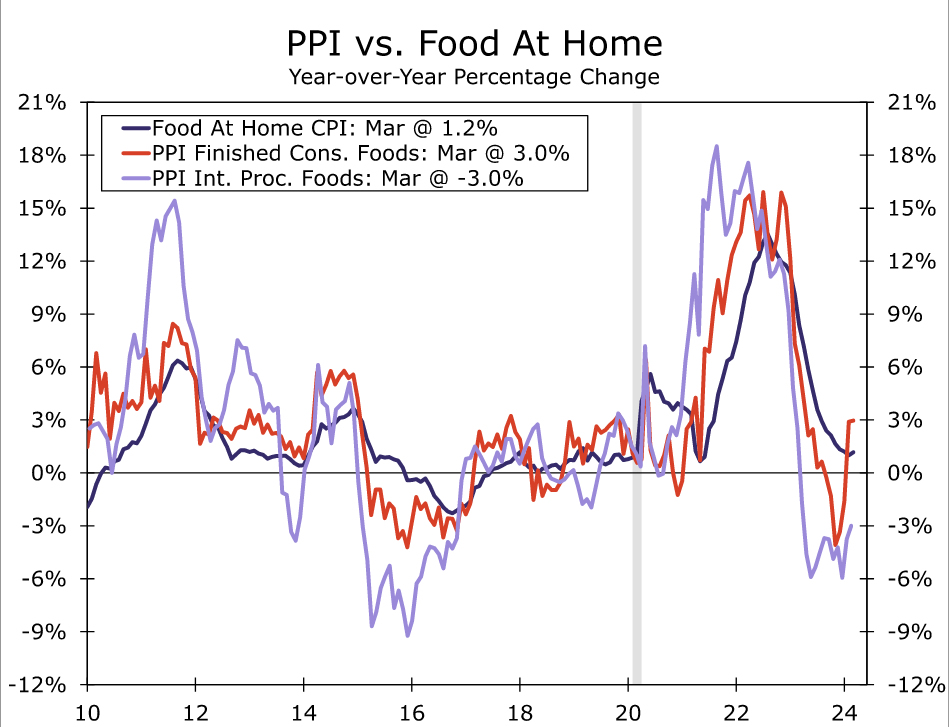

Similar to February and March, April's headline strength will be partly attributable to another jump in gasoline prices. We estimate that once adjusting for the usual rise in prices at the pump this time of year, energy goods rose 3.0% in April. Falling oil prices in recent weeks, however, are teeing up at least a partial reversal in this component in May. Food prices, meanwhile, were likely a little firmer in April. An upturn in producer prices for consumer foods suggests grocery disinflation may be close to running its course, while two months of sub-trend gains in food away from home leaves scope for some mean-reversion in April. We look for food prices to rise 0.2% after a 0.1% gain in March (Figure 2).

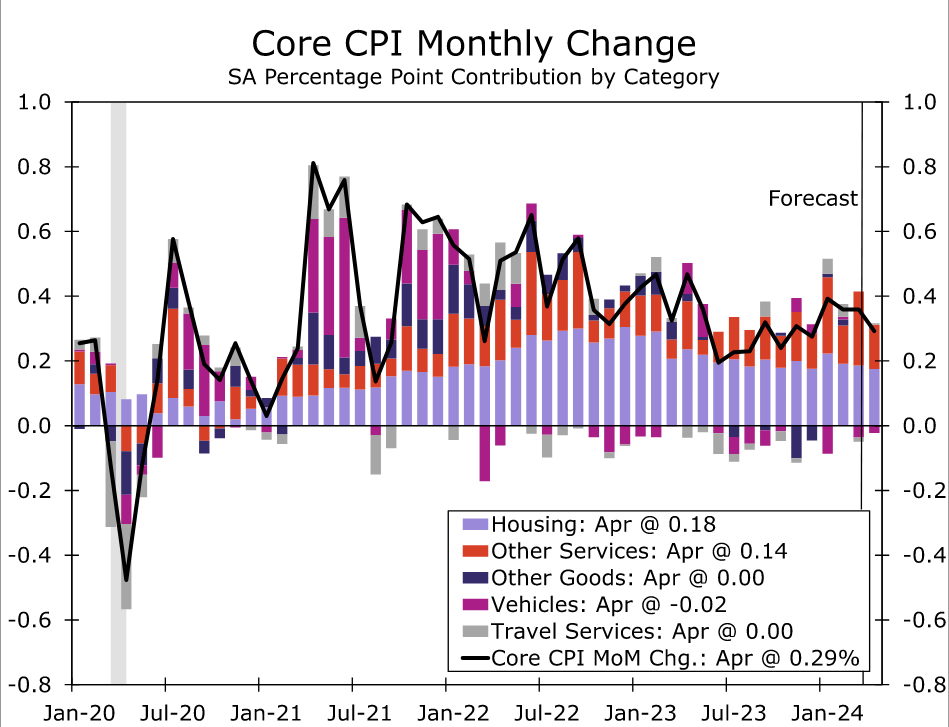

While headline inflation is likely to have remained firm in April, core inflation looks set to resume its downward trek. After three straight 0.4% monthly gains, we estimate core CPI rose 0.3% in April (Figure 3). If realized, the year-over-year rate for prices less food and energy would fall to a three-year low of 3.6%. Some additional deflation in the goods sector is expected to help core CPI slow in April. Both new and used vehicle prices look to have declined again, albeit at a more modest pace than in March. Elsewhere, goods prices were likely little changed in April, although a flat monthly reading would leave prices for core goods ex-autos down 0.8% over the past year—about double the average annual decline from 2014-2019.

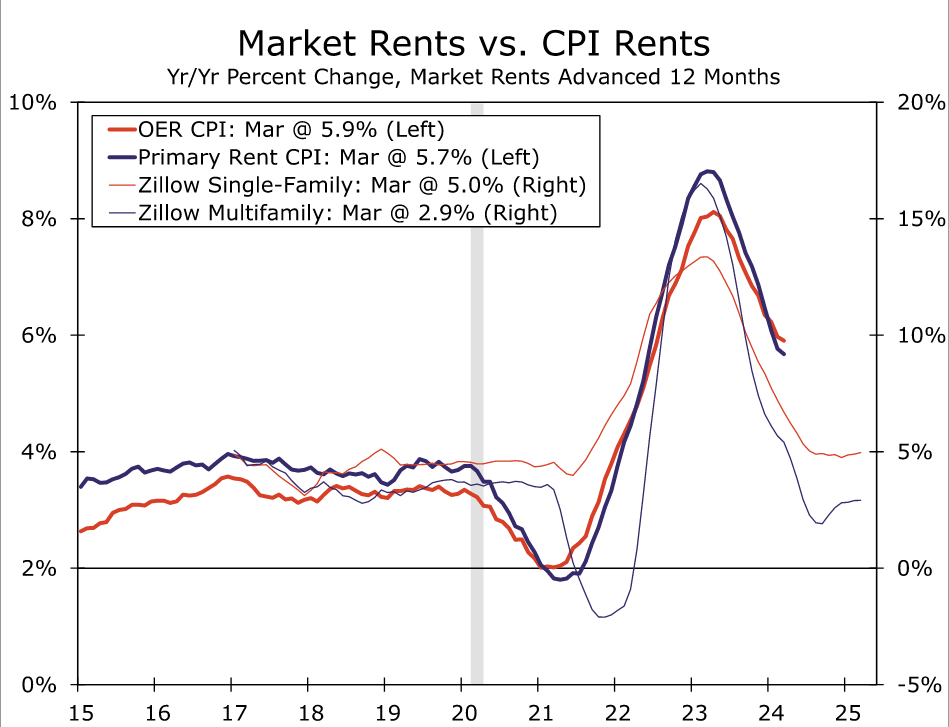

Services have been the more intractable component of inflation recently, making a downshift in this segment key to getting disinflation back on track. We estimate core services rose 0.4% in April, which would be the smallest monthly gain since December. Although the moderation in shelter inflation has unfolded slowly, the trend indicated by private rent measures as well as the CPI's New Tenant Rent Index remains down; we have penciled in a 0.41% rise in primary shelter in April versus a monthly average of 0.46% in Q1 (Figure 4).

Outside of housing, core services inflation also looks to have eased a little in April. After rising 0.6% in March, we estimate the CPI equivalent of “super core” inflation rose 0.4% last month amid smaller monthly gains in medical care, motor vehicle, internet and personal services. If realized, the three-month annualized rate of CPI core services less housing would slow from 7.6% in March to 5.7% and suggest that the PCE “super core” advanced 0.3% month-over-month in April.

Outlook: Inflation Pressures Continue to Subside

The first quarter's hotter price growth was indicative that further progress taming inflation will be slower ahead. Businesses remain more apt to raise prices than prior to the pandemic with sturdy consumer spending limiting the need to hold the line on prices. That said, we do not believe that the underlying trend in inflation is re-accelerating.

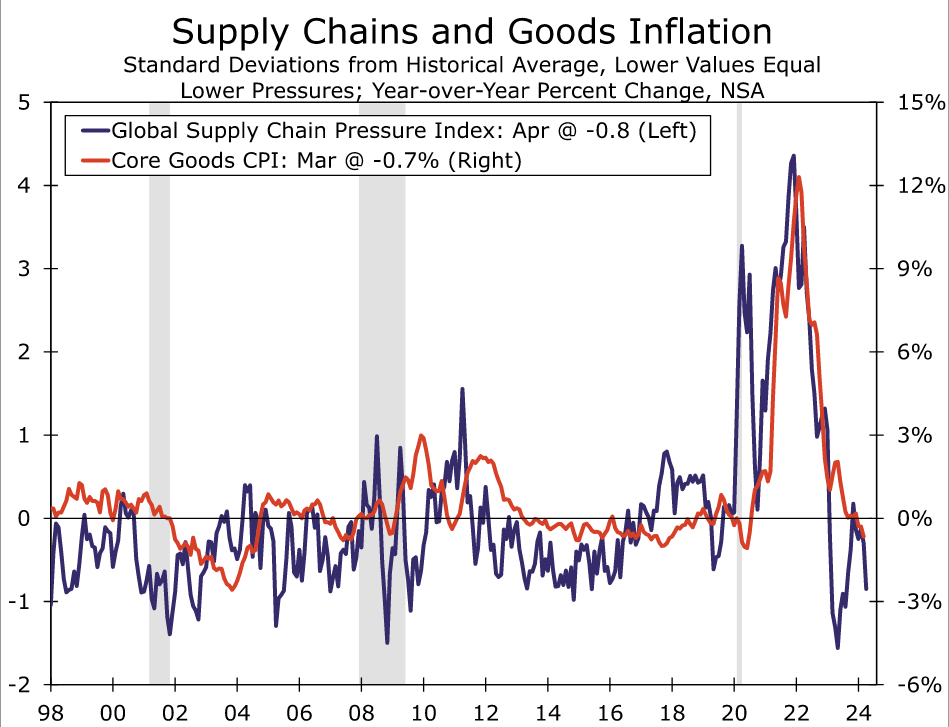

The strong disinflationary tailwinds to the goods sector over the past two years have faded, but upward pressure on goods prices remains minimal. Supply pressures are no longer easing as rapidly as in 2022 and the first half of 2023, but they are not building either (Figure 5). Margins in the goods sector also remain elevated relative to the 2010s, providing space for firms to ease up on pricing as consumers grow more discerning in their purchases. These dynamics should keep core goods in mild deflation territory in the near term. Similarly, food and energy-related commodities are not falling as sharply as over the course of mid-2022/early-2023, but range-bound levels over the past year or so mean food and energy's contribution to headline inflation is not increasing materially.

With goods inflation likely to be little changed ahead, services will need to slow further to keep overall inflation on its downward trajectory. We believe the pieces are in place for services to contribute more to disinflation (Figure 6). Shelter inflation should continue to cool as we move through the year, with apartment vacancy rates climbing and deceleration in more forward-looking spot rents. We estimate primary shelter, currently up 5.9% year-over-year, will slow to 4.1% by December before bottoming out at a little over 3% around the middle of next year.

Outside of housing, upward pressure on services inflation also continues to ease. The steadier state of goods prices should usher in some relief to services inflation via tamer input costs, with motor vehicle insurance inflation likely being the most notable beneficiary of this dynamic. Meantime, the gradual loosening in the labor market is leading to slower nominal wage growth at the same time the trend in productivity has firmed. Overall, we see the still-elevated rate of services inflation early this year as largely a function of services being slower to respond to changes in the broader price environment this cycle, rather than a sign inflation is getting stuck at current levels. We look for core services to slow to 4.9% on a year-ago basis in Q4, which would help drive core inflation down to 3.5%.

Yet even as upward pressure on prices continues to subside, the first quarter flare up in consumer prices signals that inflation will likely take longer to fully stomp out than what the trend in the second half of last year implied. Progress on the Fed's preferred inflation gauge looks set to be particularly slow. Amid the greater near-term momentum indicated by Q1 data and low base readings from late last year, core PCE inflation when measured on a year-ago basis is likely to be stuck around 2.7%-2.8% through the end of the year (Figure 7). Yet we continue to expect to see price growth slow on a monthly basis, with the three-month annualized rate on core PCE inflation falling back below 2.5% this summer. With the labor market continuing to soften, we think such a pace could still be enough for the FOMC to ease at its September meeting, but a string of more benign prints will need to start with the April data.

ECB’s Holzmann decisively against quick and strong interest rate cuts

In an interview published today, ECB Governing Council member Robert Holzmann indicated that while he is open to rate cut in June, "I see absolutely no reason for us to cut key interest rates too quickly, too strongly," he said.

Holzmann also acknowledged the significant influence of Fed on ECB decision-making. He described the Fed as "the gorilla in the room," emphasizing how ECB policies are, to some extent, shaped by actions taken by the US central bank, particularly due to the dollar's pivotal role in the global economy.

ECB’s Wunsch sees path to start rate cut, but not preset course of action

Speaking in Frankfurt, ECB Governing Council member Pierre Wunsch indicated the even though the outlook remains "foggy", he saw a "path for initiating rate cuts this year." He added that the upcoming June meeting would provide clearer insights into wage and service sector dynamics for making the decision.

Wunsch further explained that there is "no sign of de-anchoring" regarding longer-term inflation expectations, which supports the argument the costs of remaining "tight for too long" seem to outweigh those of a "premature loosening".

However, Wunsch also noted "significant risks" related to the path of wage growth and inflation in sectors with high labor costs. Therefore "now is not the time to commit to a preset course of action" he added.

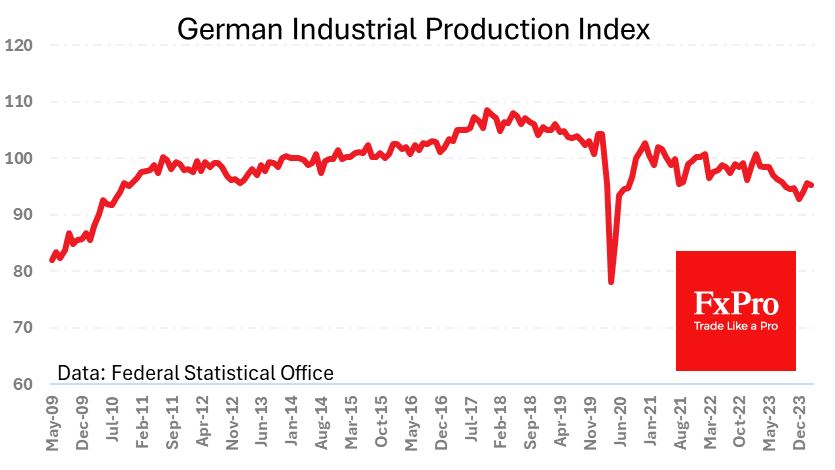

German Industrial Production Slide Brings Closer ECB’s Rate Cut

German industrial production continues to decline. The rate of contraction in March was slightly better than the average forecasts but maintained the downward trend.

The index of industrial production fell by 0.4% in March and by 3.3% y/y, having lost in annual terms for the last ten months.

German industrial production peaked at the end of 2017, and then it was turned down by trade wars, pandemic lockdowns, and the most recent impulse of deglobalisation. Here, you can discern both a cooling of relations with the second-biggest economy and a general slowdown.

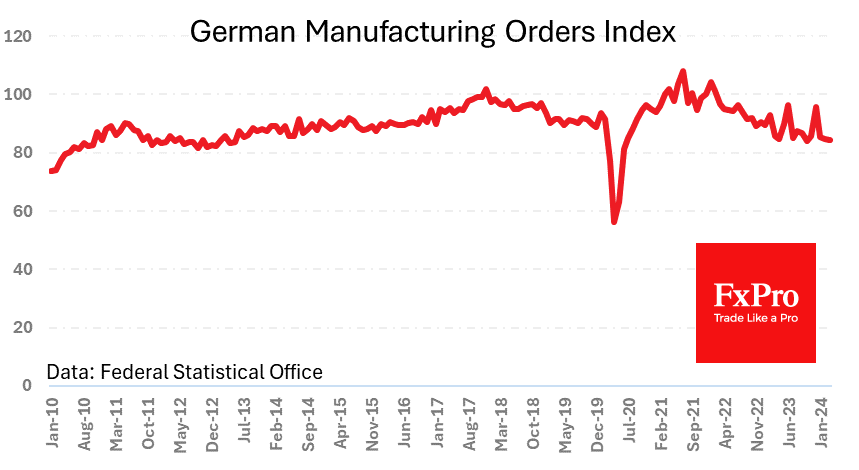

Germany’s industrial orders index, published a day earlier, fell in March to its lowest level since 2013, barring a sharp dip during the pandemic lockdowns.

Weakness in Germany’s industrial sector could bring a rate cut from the ECB closer, softening the Bundesbank’s traditionally hawkish bias.

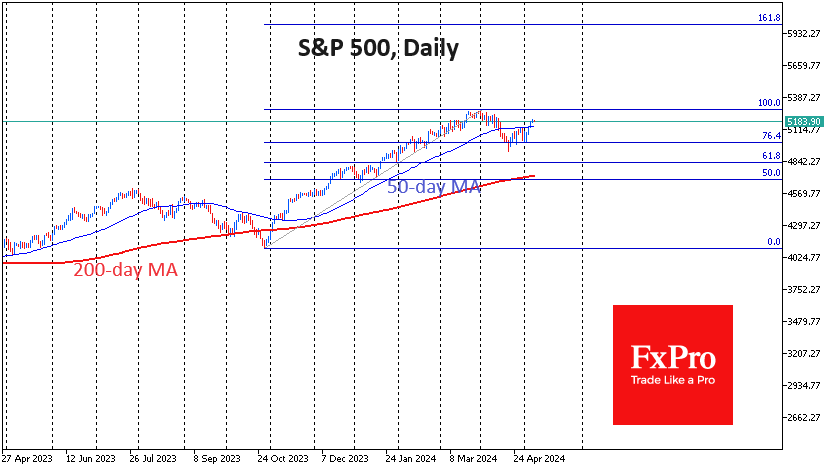

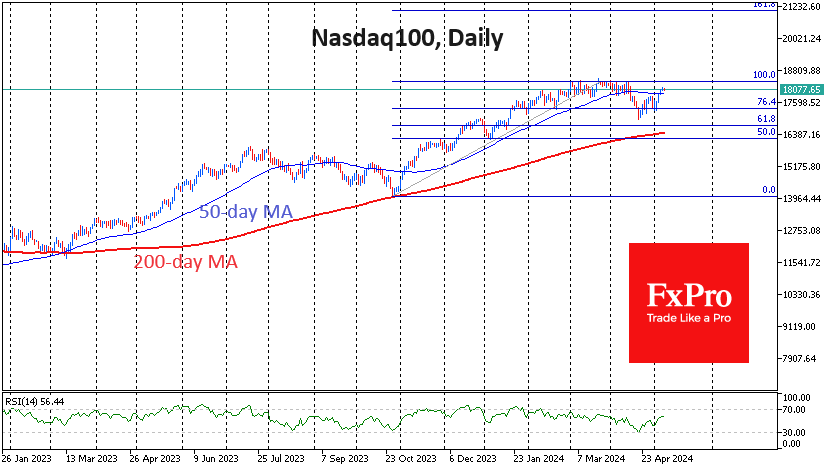

US Indices Heading Towards Highs

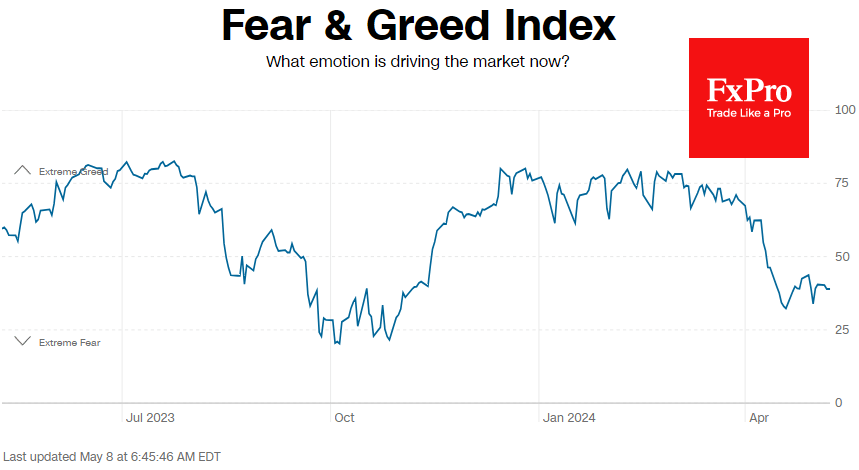

US indices have been gaining daily since the beginning of May. They have found strength amid relatively weak job reports and quite upbeat quarterly earnings. The S&P500 and Nasdaq100 indices are just 1.5% below the all-time highs set in March.

The market downturn in the first three weeks of April has whetted bargain hunters’ appetite. Investors returned to buying on signs that the economy and labour market were cooling.

The decline in April effectively removed the overbought condition on the equity market, dipping into “fear” territory from the “extreme greed” seen in early March.

We see the return of all three key US indices – Dow Jones, Nasdaq100 and S&P500 – back above their 50-day moving averages as a technically important signal. A weak labour market report last Friday shifted the balance in favour of buyers.

While the Japanese market went out of favour with speculators last month, their attention seems to have shifted to Europe. Almost daily, the FTSE100 index is updating all-time highs, adding 8% to the lows of 19 April. Germany’s DAX40 has added 6% over the same time and is just 0.5% below its all-time high. These are indirect but rather important signs of risk appetite in global equity markets, which is also positive for the US market.

The S&P500 corrected in April to 76.4% of the rally from the October lows to the peak in early April. This is not a classic 61.8% Fibonacci retracement, but it is also quite common in strong bull markets.

Confirmation of this bullish scenario would be a rally of the index above 5300 with a renewal of the all-time highs. According to the Fibonacci extension, the next strong correction will only be in the 6000 area in the 6–9-month timeframe. Within this scenario, the bullish targets for the Nasdaq100 will be the territory above 21000.

Sunset Market Commentary

Markets

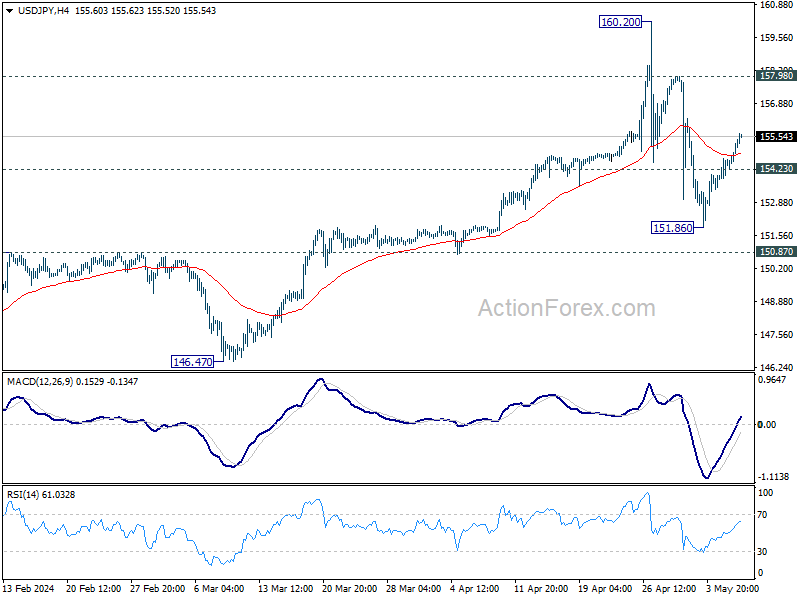

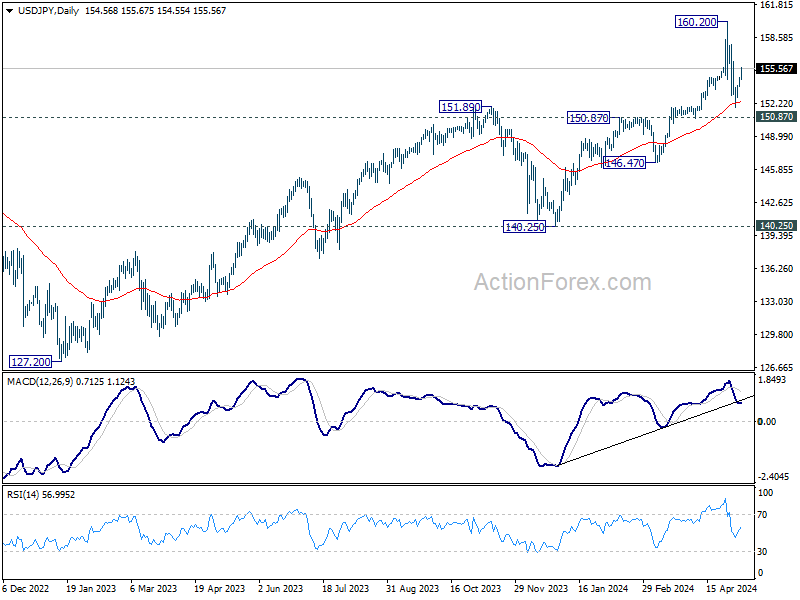

In yet another dull trading day the weak SEK (cf. below) and JPY stand out. The yen is not impressed by Ueda ramping up warnings. It began in Asian dealings, where the BoJ governor said that a policy response (i.e. rate hike) could be needed depending on the currency’s moves. Ueda said a weak JPY affects inflation and is therefore a key variable in the analysis. Finance minister Suzuki around the same time aired the usuals: that they are watching the market closely and will take all possible measures as needed. Well into European trading hours, Ueda said he’s seeing signs of a virtuous wage-price cycle strengthening. He also noted that should risks to the inflation outlook grow, it would be appropriate for the BoJ to increase rates at a faster pace. Ignoring all that, USD/JPY for a third day straight rises and pierces through the 155 barrier again with ease. This compared with a close last Friday at 153.05. Monday last week the pair hit 160 for the first time in 34 years, prompting an intervention by Japanese authorities. They returned to the market two days later. Moves this week once again show that unilateral interventions rarely have a lasting market impact. The dollar is overall better bid today, recovering some of the losses incurred in the wake of Friday’s sub-consensus payrolls and services ISM. The trade-weighted index rises towards 105.58, EUR/USD eases slightly to 1.0748. Sterling remains under pressure going into tomorrow’s potentially market-moving Bank of England meeting. EUR/GBP breaks above 0.86, a move we expected to happen in case the likes of governor Bailey indicate some decoupling from the Fed to walk a rate path more akin to the ECB. Leaping (and closing the week) beyond 0.8644 would be a technical sign of the pair looking to break loose from the monthslong stalemate.

Core bonds lost ground in a sign the recent rally is running out of steam. Technical charts are coming to the rescue here and there as well (e.g. the upward sloping trendline in the US and German 10-yr yield). Yields in the US add between 0.8 (2-yr) and 3.7 bps (30-yr). Bunds underperform, rising 3.4 (2-yr) to 5.3 bps (30-yr). Belgian ECB policymaker Wunsch said there’s room to cut this year but did not want to pre-commit to anything beyond June. Wunsch warned that risks to the inflation outlook remain, in particular around the trajectory of wage growth and inflation in wage-sensitive services. He also singled out the euro, which could weaken significantly amid diverging economic conditions and monetary policy between the euro area and US. Austrian member Holzmann hinted that follow-up action to a June cut, if any, is likely for September or December rather than July.

News & Views

The Swedish Riksbank cut its policy rate by 25 bps to 3.75% today. Inflation is approaching the target while economic activity is weak, allowing the central bank to make monetary policy less restrictive. If the outlook for inflation still holds, the policy rate is expected to be cut two more times during the second half of the year. Gradual cuts are warranted given uncertainty around the outlook. Risks that may cause inflation to rise again are primarily linked to the strong US economy, the geopolitical tension and the krona exchange rate. The Swedish krona lost marginally ground after the decision with EUR/SEK approaching the 11.77 YTD high. Money markets discount the next 25 bps rate cut by the August meeting.

A new report by the Semiconductor Industry Association (SIA) and the Boston Consulting Group on the semiconductor supply chain forecasts significant improvements in the resilience of the supply chain in both the US and globally in coming years. US fab capacity is projected to increase by 203% by 2032, a tripling of US capacity. That will take the US share of the industry from currently 10% to 14%. The US will secure more than one-quarter (28%) of global capital expenditures between 2024-2032 – an estimated $646bn – an amount second only to Taiwan.

Graphs

USD/JPY: yen loses for a third day straight, ignoring Ueda warnings

EUR/SEK: Swedish crown loses ground in the wake of the Riksbank’s first rate cut since 2016

EUR/GBP breaks above 0.86 going into tomorrow’s Bank of England meeting

European 10y swap yield is close in finding a bottom after the recent retreat

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.11; (P) 154.43; (R1) 155.01; More...

Intraday bias in USD/JPY remains mildly on the upside at this point. Rebound from 151.86 is seen as the second leg of the corrective pattern from 160.20 high. Further rise would be seen to 157.98 resistance. On the downside, below 154.23 minor support will turn intraday bias neutral.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

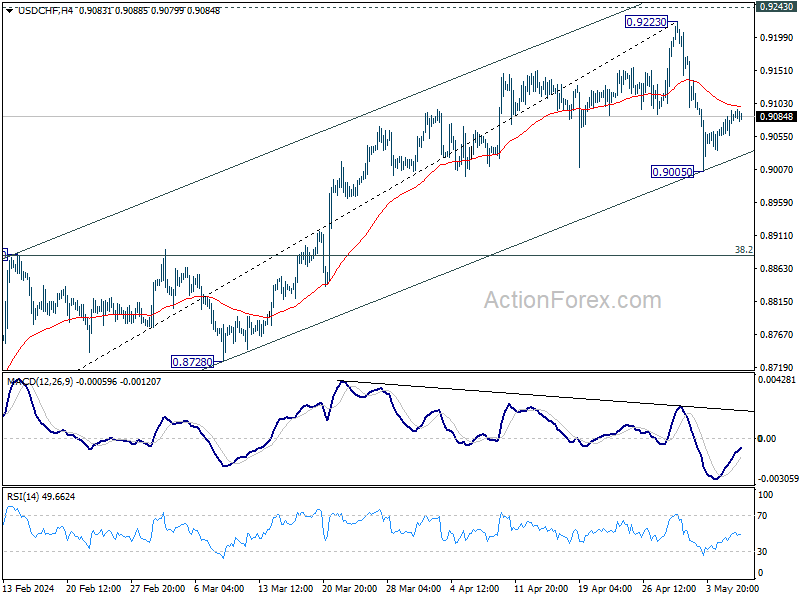

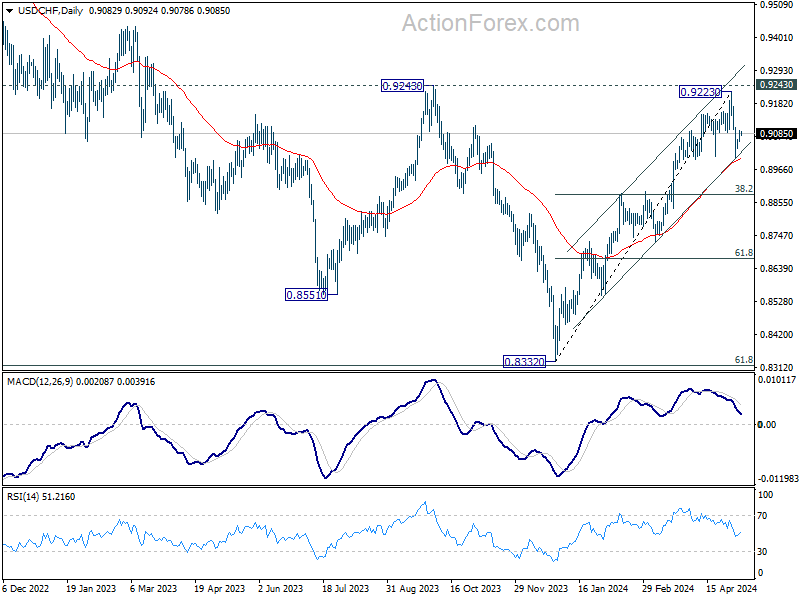

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9061; (P) 0.9078; (R1) 0.9100; More....

No change in USD/CHF's outlook as intraday bias stays neutral. Further decline is in favor as long as 55 4H EMA (now at 0.9099) holds. On the downside, break of 0.9005 and sustained trading below 55 D EMA (now at 0.9000) will bring deeper fall to 38.2% retracement of 0.8332 to 0.9223 at 0.8883. However, firm break of 55 4H EMA will suggest that the pull back has completed, and bring stronger rebound to retest 0.9223 high.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

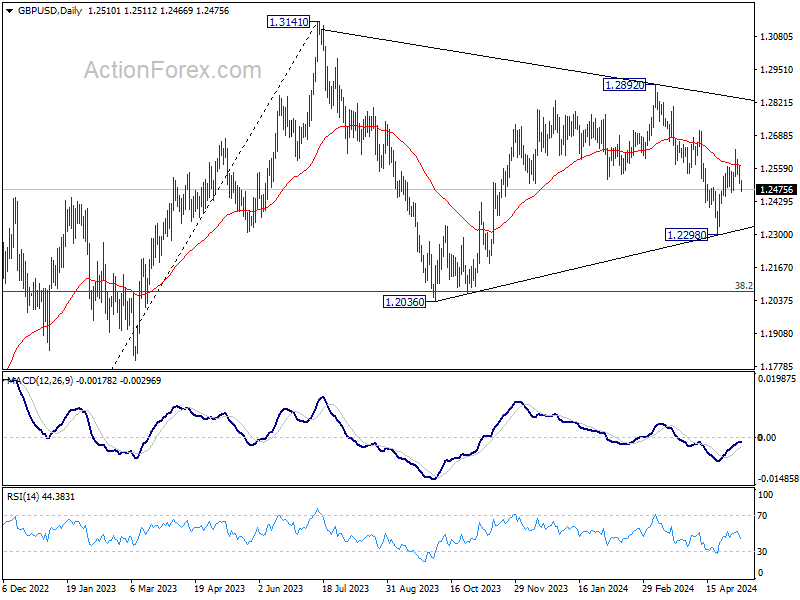

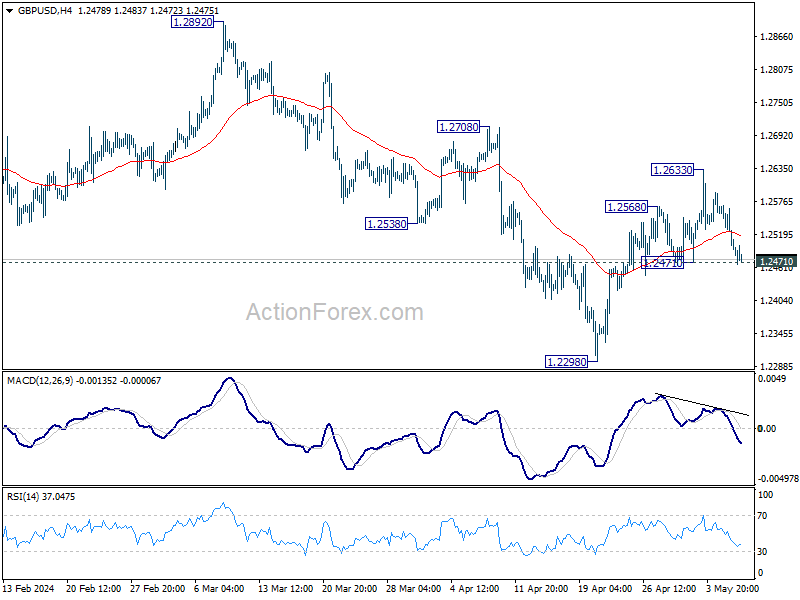

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2481; (P) 1.2528; (R1) 1.2554; More...

Intraday bias in GBP/USD stays neutral at this point. Further rally is in favor with 1.2471 support intact. On the upside, above 1.2633 will resume the rebound from 1.2298 to 1.2708 resistance next. However, firm break of firm break of 1.2471 will indicate that this rebound has completed, and revive near term bearishness. Retest of 1.2298 should then be seen in this case.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.