Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0720; (P) 1.0766; (R1) 1.0809; More...

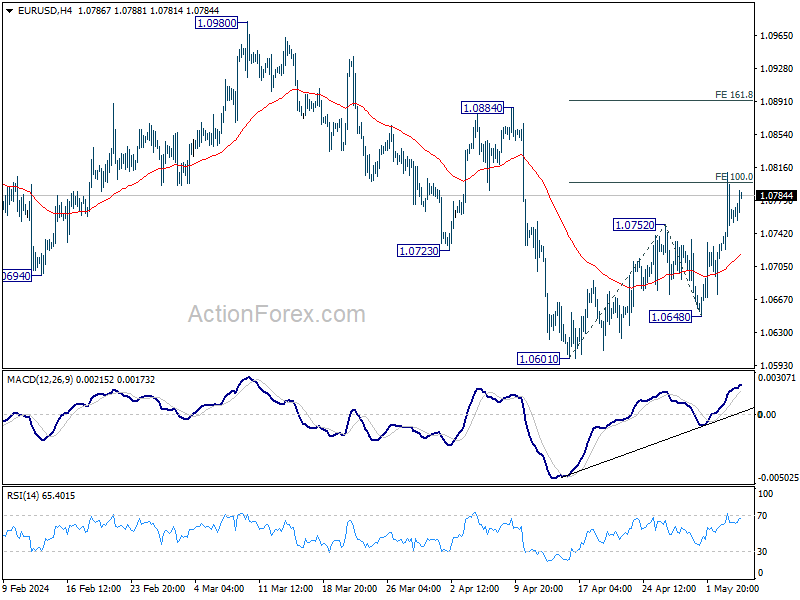

Intraday bias in EUR/USD stays on the upside at this point. Fall from 1.0980 could have completed with three waves down to 1.0601. Further rally is expected and firm break of 100% projection of 1.0601 to 1.0752 from 1.0648 at 1.0799 will pave the way to 161.8% projection at 1.0892. For now, risk will stay on the upside as long as 1.0648 support holds, in case of retreat.

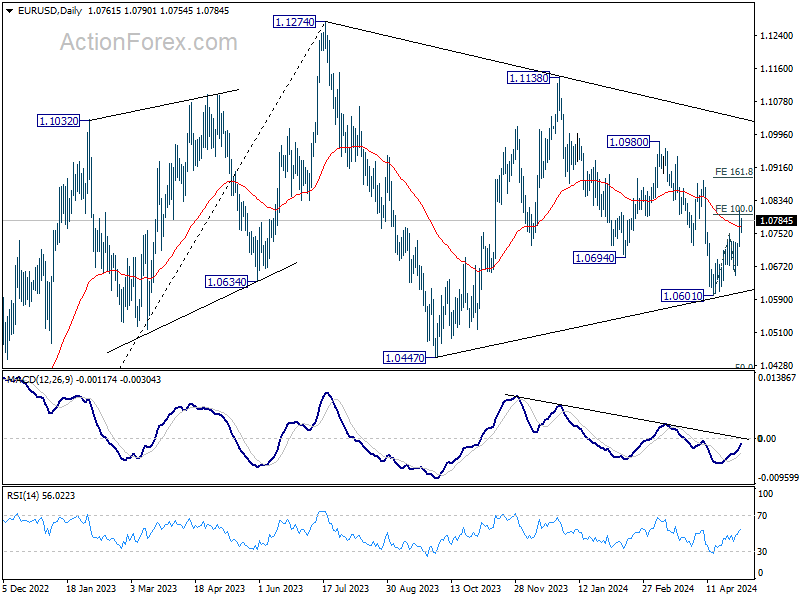

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

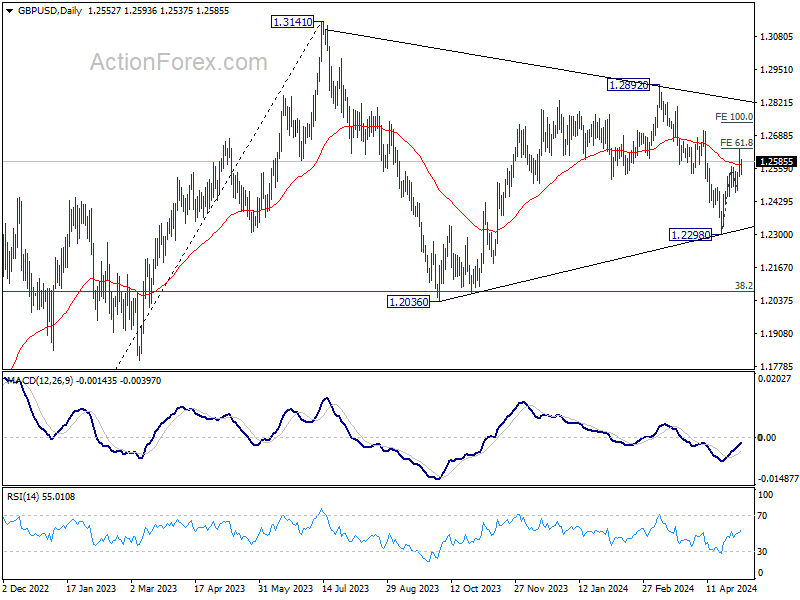

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2491; (P) 1.2564; (R1) 1.2619; More...

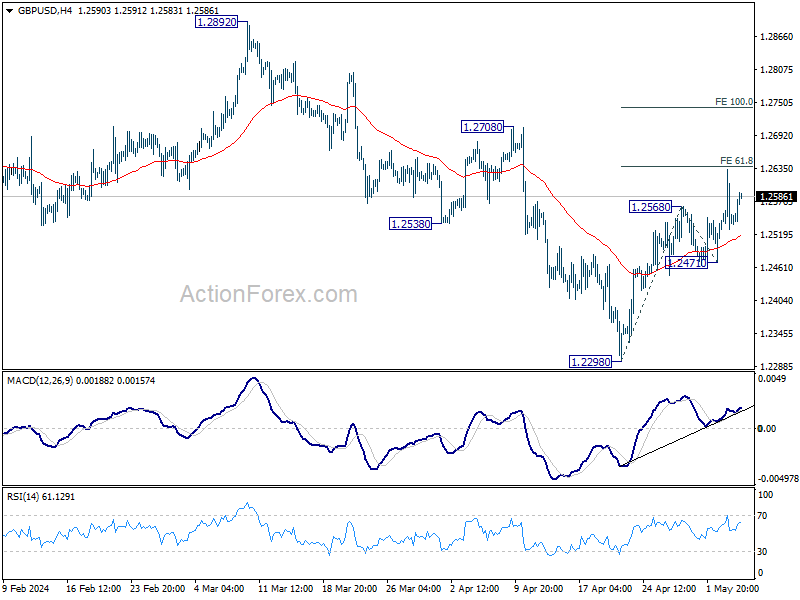

Intraday bias in GBP/USD remains mildly on the upside at this point. Fall from 1.2892 could have completed with three waves down to 1.2298. Further rise should be seen and break of 61.8% projection of 1.2298 to 1.2568 from 1.2471 will target 100% projection at 1.2741. For now, further rally will be expected as long as 1.2471 support holds, in case of retreat.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

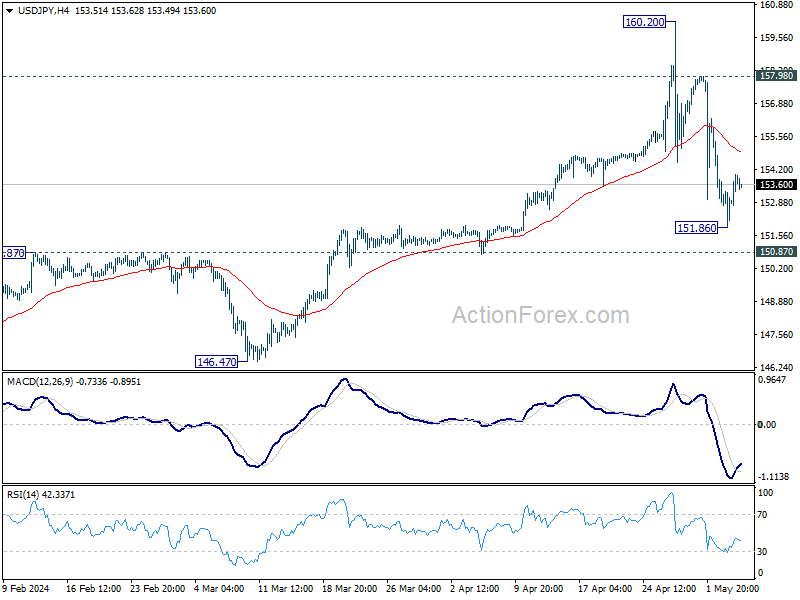

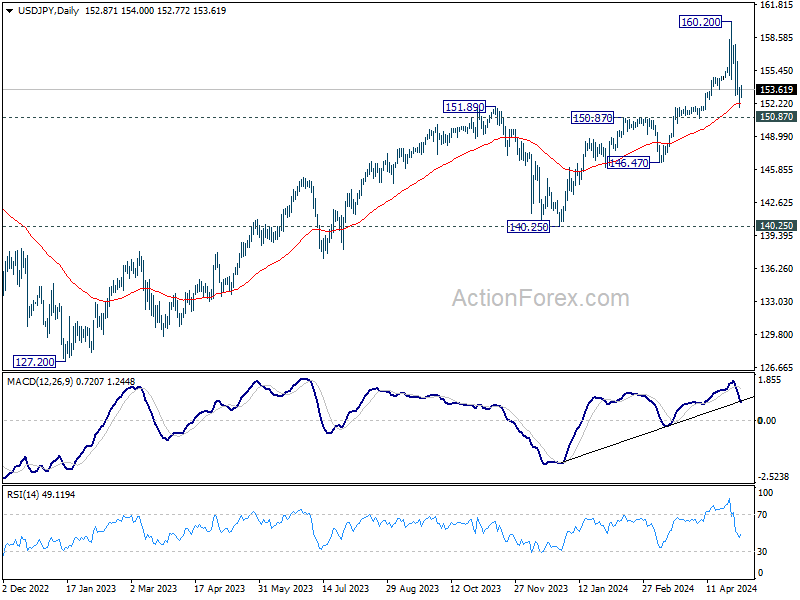

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.95; (P) 152.90; (R1) 153.92; More...

Intraday bias in USD/JPY remains neutral at this point. On the upside, firm break of 55 4H EMA (now at 154.95) will bring stronger rebound towards 157.98 resistance. On the downside, below 151.86 will resume the fall from 160.20. But strong support should be seen from 150.87 resistance turned support to bring rebound.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

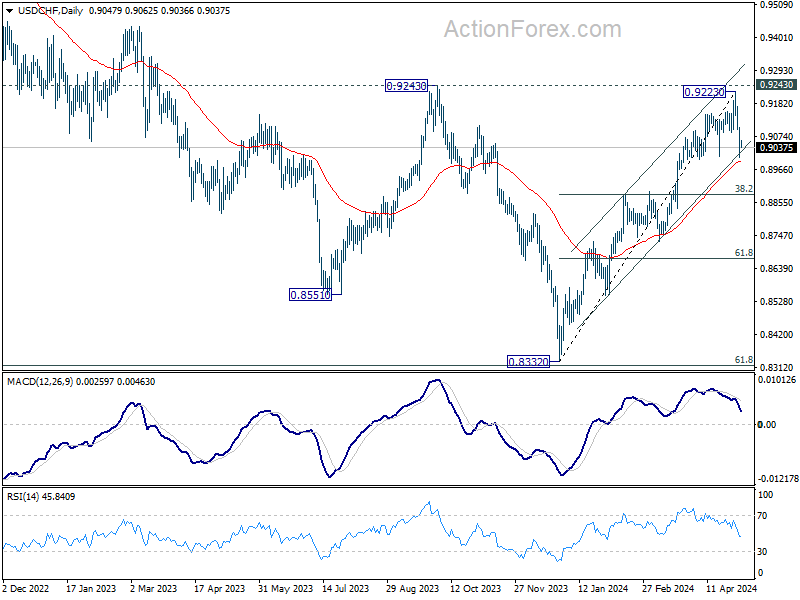

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9001; (P) 0.9055; (R1) 0.9104; More....

Outlook in USD/CHF is unchanged and intraday bias stays on the downside. Sustained break of 55 D EMA (now at 0.8993) will bring deeper fall to 38.2% retracement of 0.8332 to 0.9223 at 0.8883. On the upside, above 0.9087 minor resistance will turn intraday bias again first.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

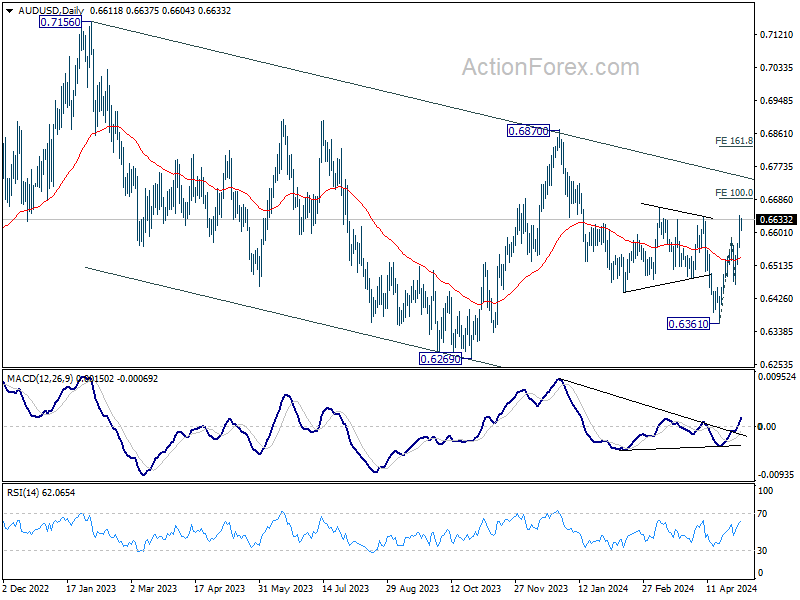

Focus on RBA as Australian Dollar Maintains Strength

As the market transitions into US session, Australian Dollar maintains its position as the strongest currency of the day. While no significant economic data is expected from the US or Canada, the focus shifts to appearances by SNB Chair Thomas Jordan, as well as Fed officials Thomas Barkin and John Williams. However, traders are expected to look through these events, anticipating insights from the RBA's decision.

Expectations are widespread that RBA will maintain its policy rate unchanged at 4.35%. Attention will be directed towards the new economic forecasts and the post-meeting press conference. The key question revolves around whether Governor Michele Bullock will shift her stance from a neutral position of "no ruling anything in or out" to a "tightening bias" stance.

Any shift in Bullock's tone could indicate the central bank's future direction, whether it's on track for either a rate cut as some economists expect in November. Or a hike as forecasted by Judo Bank chief economic adviser Warren Hogan, top economic forecaster in the Australian Financial Review's first annual ranking of economists in 2023.

In the broader currency markets, Sterling and Kiwi are also displaying strength. Yen trails as the weakest currency, followed by Swiss Franc and the Dollar. Euro and the Canadian Dollar occupy middle positions. This picture reflects a prevailing risk-on sentiment mirrored in the rally in major European indexes and US futures.

Technically, a major focus now is on AUD/USD. Current rise from 0.6361 is in progress for 100% projection of 0.6361 to 0.6585 from 0.6464 at 0.6688. Decisive break there could prompt upside acceleration, which would bolster the case that it's indeed resuming the rally from 0.6269. That would in turn shift favor to the case that whole corrective fall from 0.7156 has completed at 0.6269 already. Let's see how it goes.

In Europe, at the time of writing, UK is on holiday. DAX is up 0.99%. CAC is up 0.79%. Germany 10-year yield is down -0.0483 at 2.450. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.55%. China Shanghai SSE rose 1.16%. Singapore Strait Times rose 0.31%.

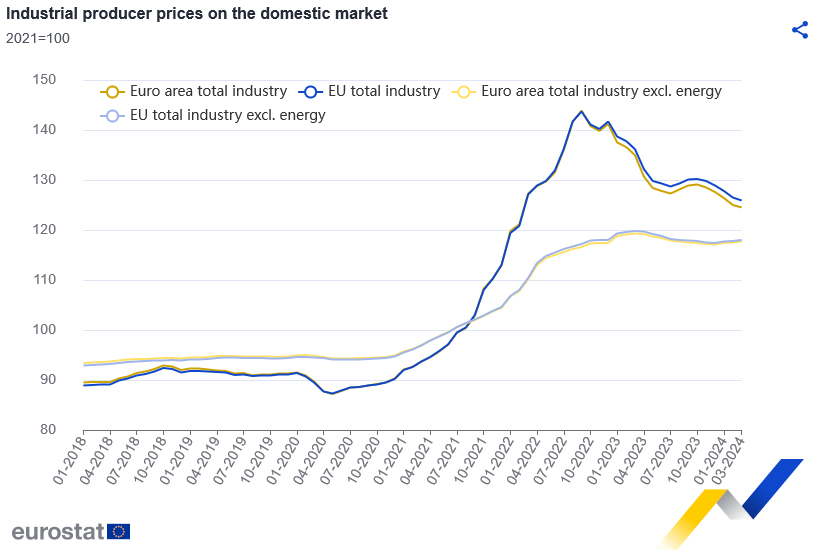

Eurozone PPI falls -0.4% mom, -7.8% yoy in Mar

Eurozone PPI fell -0.4% mom, -7.8% yoy in March. For the month, industrial producer prices increased by 0.1% for intermediate goods, 0.1% for capital goods, 0.1% for durable consumer goods, and 0.4% for non-durable consumer goods. Prices decreased by -1.8% for energy.

EU PPI fell -0.5% mom, -7.6% yoy. Among Member States for which data are available, the largest monthly decreases in industrial producer prices were recorded in Bulgaria (-3.4%), Denmark and Greece (both -2.3%) and Spain (-2.2%). Increases were observed in Ireland and Sweden (both +0.9%) as well as in Germany and Croatia (both +0.2%).

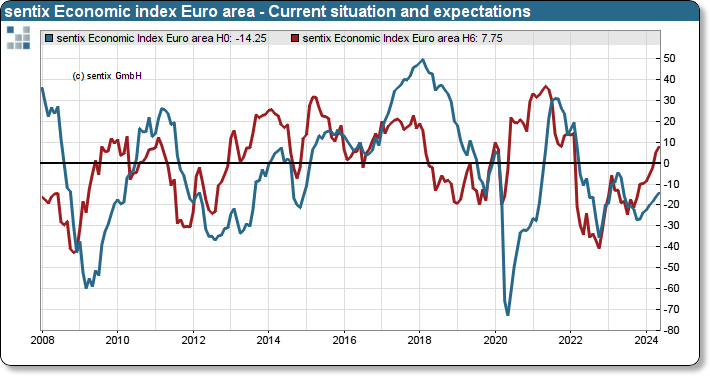

Eurozone Sentix rises to -3.6, window for ECB rate cut limited

Eurozone Sentix Investor Confidence rose from -5.9 to -3.6 in May, above expectation of -4.8. This marks the seventh consecutive increase and the highest level since February 2022. Additionally, Current Situation Index climbed from -16.3 to -14.3, marking seven consecutive increases and reaching its highest point since May 2023. Expectations Index also saw growth, rising from 5.0 to 7.8, marking eight consecutive increases and reaching its highest level since February 2022.

Sentix noted that while the data presents an encouraging picture, indicating a gradual recovery from the economic challenges of the past two years, underlying weaknesses in momentum persist. The rise in expectations, though positive, is described as "very sluggish" and has yet to substantially impact the situation values.

As for ECB, Sentix said the window for cutting interest rate "does not appear to be very large". Despite improvements in the economy, a deteriorating inflation environment adds pressure to bond markets.

Eurozone PMI services finalized at 53.3, highest in 11 months

Eurozone's PMI services index was finalized at to 53.3 in April, marking a notable improvement from March's 51.5. PMI Composite was finalized at 51.7, up from the previous month's 50.3 Both reached the highest levels in 11 months.

Notable country-level performances on PMI Composite include Spain reaching a 12-month high at 55.7, Germany achieving a 10-month high at 50.6, and France hitting an 11-month high at 50.5. However, Italy recorded a two-month low at 52.6, and Ireland saw a six-month low at 50.4.

Chief Economist at Hamburg Commercial Bank, Cyrus de la Rubia, highlighted the positive momentum, noting that service providers have witnessed growth for the third consecutive month, signaling an end to the lackluster performance observed in the latter half of the previous year. He emphasized the uptick in employment, new business, and order book growth, which reached its strongest expansion in eleven months.

However, concerns regarding operating costs persist, with PMI index for operating costs in the service sector continuing to rise rapidly over the past year. De la Rubia cautioned that ECB is likely to adopt a cautious approach regarding potential rate cuts, given this trend. Despite this, service companies have managed to offset some of the cost increases by passing them on to consumers, reflecting improving demand conditions.

China's Caixin PMI services dips to 52.5, weak expectations a major hurdle

China's Caixin PMI Services for April, while dipping slightly from 52.7 to 52.5 as expected, maintains a growth streak for the 16th consecutive month. The sector sees robust expansion in new business, marking its fastest pace in nearly a year. Business confidence also reaches its peak for the year so far. PMI Composite, which edged up from 52.7 to 52.8, reached its highest level since May 2023

"The growth in supply and demand in the manufacturing and services sectors picked up pace, with outstanding export growth," notes Wang Zhe, Senior Economist at Caixin Insight Group. However, Wang cautions, "the pressure on the job market should not be overlooked," with employment metrics experiencing a sharper decline compared to the previous month.

Furthermore, Wang highlights the persistent challenges in pricing dynamics, stating that "input and output prices remained relatively low, particularly due to the drag from manufacturing factory gate prices."

Wang noted, "Weak expectations remain one of the major hurdles facing economic development, leading to increasing pressure on employment and a greater risk of deflation."

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9001; (P) 0.9055; (R1) 0.9104; More....

Outlook in USD/CHF is unchanged and intraday bias stays on the downside. Sustained break of 55 D EMA (now at 0.8993) will bring deeper fall to 38.2% retracement of 0.8332 to 0.9223 at 0.8883. On the upside, above 0.9087 minor resistance will turn intraday bias again first.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | AUD | TD Securities Inflation M/M Apr | 0.10% | 0.10% | ||

| 01:45 | CNY | Caixin Services PMI Apr | 52.5 | 52.5 | 52.7 | |

| 07:45 | EUR | Italy Services PMI Apr | 54.3 | 54.7 | 54.6 | |

| 07:50 | EUR | France Services PMI Apr | 51.3 | 50.5 | 50.5 | |

| 07:55 | EUR | Germany Services PMI Apr F | 53.2 | 53.3 | 53.3 | |

| 08:00 | EUR | Eurozone Services PMI Apr F | 53.3 | 52.9 | 52.9 | |

| 08:30 | EUR | Eurozone Sentix Investor Confidence May | -3.6 | -4.8 | -5.9 | |

| 09:00 | EUR | Eurozone PPI M/M Mar | -0.40% | -0.70% | -1.00% | -1.10% |

| 09:00 | EUR | Eurozone PPI Y/Y Mar | -7.8% | -8.30% | -8.50% |

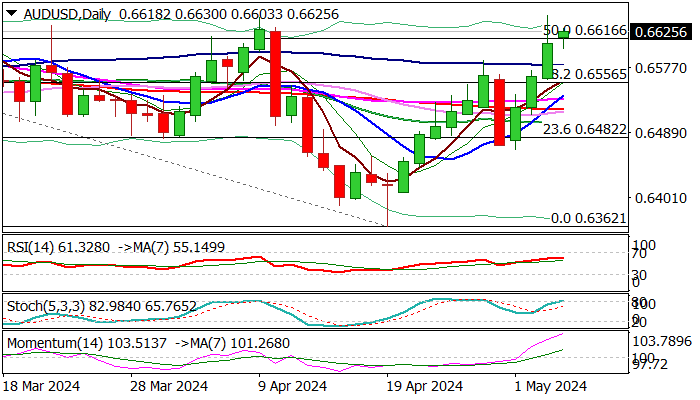

AUD/USD: Bulls Hold Grip Ahead of RBA Policy Meeting on Tuesday

AUDUSD keeps firm tone on Monday, despite Friday’s spike and subsequent pullback, though with initial warning that traders may opt for a partial profit taking after strong rally in past two days, when the pair advanced 2%.

Stretched daily studies add to signals of correction, but dips are likely to be shallow and ideally contained by 100DMA (0.6579) to position for fresh attack at key 0.6660/70 zone (multiple tops of Mar/Apr /May, also near Fibo 61.8% of 0.6871/0.6362) violation of which to spark acceleration towards 0.6750 zone.

The action is also supported by two large consecutive bullish weekly candles, with expectations that Australia’s policymakers may show more hawkishness in Tuesday’s RBA policy meeting (rate hike is still on the table) expected to further underpin Aussie dollar.

Res: 0.6644; 0.6667; 0.6676; 0.6750.

Sup: 0.6600; 0.6579; 0.6556; 0.6520.

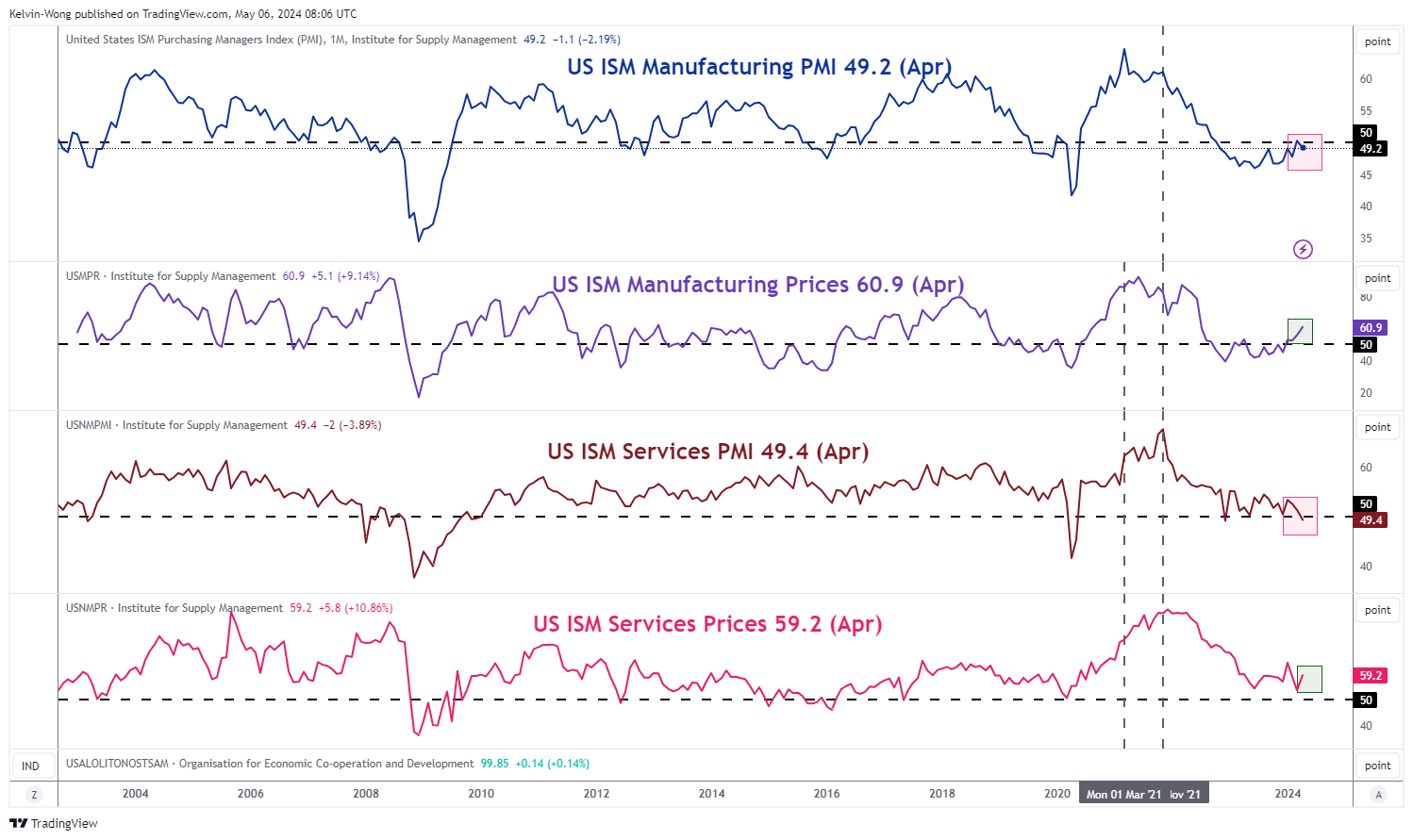

Gold Technical: A Floor May Have Been Formed for the Bulls

- Stagflation risk is still lingering as indicated by the latest April US ISM Manufacturing and Services PMI data.

- A not fully priced-in stagflation risk scenario may support another bullish impulsive upmove sequence for Gold (XAU/USD).

- Watch the key medium-term pivotal zone of US$2,260/2,210 for Gold (XAU/USD).

Since our last publication, Gold (XAU/USD) has inched lower to print a low of US$2,277 last Friday, 03 May. All in all, it has declined by -6.3% from its current all-time high of US$2,431 on 12 April amid key risk events and data such as the outcome of Fed Chair Powell’s monetary policy press conference and the US non-farm payrolls jobs date for April.

Stagflation risk is still “alive”

Fig 1: US ISM Manufacturing and Services PMI data as of 3 May 2024 (Source: TradingView, click to enlarge chart)

The markets do not seem to pay much attention to the US ISM Services PMI data which is considered a leading economic indicator to gauge the state of the US economy. Market participants embraced a risk-on behaviour mentality triggered by a weaker-than-expected April NFP that added only +175K jobs, below the consensus of +243K, and below March’s print of +315K which suggests that the US jobs market is still expanding at a brisk pace that reduces the odds of an interest rate hike by the Fed; a state of “Goldilocks” scenario for the US economy.

On the other hand, the services sector which contributes close to two-thirds of US economic growth is showing signs of an acute slowdown as indicated by the latest data from the US ISM Services PMI that contracted to 49.4 in April, its first contraction since December 2022, below consensus of 52.0.

In addition, one of its sub-components, the ISM Services Prices (considered as a gauge of business costs for the services sector in the US) rose to 59.2 in April from 53.4 in March and above expectations of 55.

Overall, we have seen similar trends in April ISM Manufacturing PMI and its Manufacturing Prices sub-component albeit at a steeper pace of increase versus Services Prices (see Fig 1).

These latest data points suggest a potential stagflation environment akin to the 1970s when the Fed had its hands tied to prevent it from enacting an accommodating monetary policy which in turn may support the ongoing major bullish trend in Gold (XAU/USD) in place since September 2022.

Positive technical elements have resurfaced

Fig 2: Gold (XAU/USD) major & medium-term trends with Gold/Copper ratio as of 6 May 2024 (Source: TradingView, click to enlarge chart)

Fig 3: Gold (XAU/USD) short-term trend as of 6 May 2024 (Source: TradingView, click to enlarge chart)

The daily RSI momentum indicator of Gold (XAU/USD) has shaped a rebound right above a key parallel ascending support at around the 50 level which suggests a positive medium-term momentum revival while price actions are still holding above the 50-day moving average, an indication that the medium-term uptrend phase in place since 14 February 2024 is still intact (see Fig 2).

Secondly, the short-term corrective pull-back from the 12 April 2024 all-time high of US$2,431 has transformed into a potential bullish “Descending Wedge” configuration since 26 April which implies that the short-term downside momentum inherent in the two weeks of corrective pull-back has started to ease.

Watch US$2,260 (upper limit of the medium-term pivotal support) and the first short-term hurdle the bulls face is likely the US$2,350/365 near-term resistance zone. A clearance above it sees the next immediate resistance coming in at US$2,420 (current all-time high area) and US$2,450 in the first step (see Fig 3).

However, failure to hold at US$2,260 may see an extension of the short-term corrective decline to expose the next supports at US$2,235 and US$2,210 (lower limit of the medium-term pivotal support & the 50-day moving average).

AUD/USD Hits One-month High, RBA Decision Next

The Australian dollar has started the week with modest gains. AUD/USD is up 0.25%, trading at 0.6624 in the European session at the time of writing. The Aussie is coming off a strong week, having gained 1.19%.

RBA widely expected to pause

The Reserve Bank of Australia meets on Tuesday and is widely expected to hold the cash rate at 4.35%, a 12-year high. The central bank has maintained rates three straight times and there is a strong likelihood that the rate statement will be hawkish, as inflation in the first quarter dropped from 4.1% to 3.6% but was above the market estimate of 3.4%.

Inflation has come down significantly but remains sticky as the RBA tries to bring it back down to the 2%-3% target range. The RBA is making its rate decisions based on the data and that has the markets guessing as to what the rate path will look like. A rate cut isn’t coming until inflation falls and the RBA doesn’t expect inflation to fall within the target range before 2025.

If inflation resumes its downward path in the next few months we could see a rate cut in November but at the same time, the risk of a rate hike has increased since the Q1 inflation report. As well, the job market has been tighter than anticipated, which makes it more difficult to lower rates. The RBA was very late in starting its rate-tightening cycle and policy makers will be very hesitant to lower rates until they are confident that inflation won’t rebound.

US nonfarm payrolls lower than expected

US nonfarm payrolls eased to 175,000 in April, well below the market estimate of 240,000. The unemployment rate rose from 3.8% to 3.9%, above the forecast of 3.8%. Wage growth rose 0.2% m/m, lower than the 0.3% gain in March and shy of the market estimate of 0.2%. We haven’t seen all three components of the employment report miss their estimates for quite some time, which could point to cracks in the US labor market.

AUD/USD Technical

- AUD/USD tested support at 0.6606 earlier. Below, there is support at 0.6564

- 0.6651 and 0.6693 are the next resistance lines

Eurozone PPI falls -0.4% mom, -7.8% yoy in Mar

Eurozone PPI fell -0.4% mom, -7.8% yoy in March. For the month, industrial producer prices increased by 0.1% for intermediate goods, 0.1% for capital goods, 0.1% for durable consumer goods, and 0.4% for non-durable consumer goods. Prices decreased by -1.8% for energy.

EU PPI fell -0.5% mom, -7.6% yoy. Among Member States for which data are available, the largest monthly decreases in industrial producer prices were recorded in Bulgaria (-3.4%), Denmark and Greece (both -2.3%) and Spain (-2.2%). Increases were observed in Ireland and Sweden (both +0.9%) as well as in Germany and Croatia (both +0.2%).

Eurozone Sentix rises to -3.6, window for ECB rate cut limited

Eurozone Sentix Investor Confidence rose from -5.9 to -3.6 in May, above expectation of -4.8. This marks the seventh consecutive increase and the highest level since February 2022. Additionally, Current Situation Index climbed from -16.3 to -14.3, marking seven consecutive increases and reaching its highest point since May 2023. Expectations Index also saw growth, rising from 5.0 to 7.8, marking eight consecutive increases and reaching its highest level since February 2022.

Sentix noted that while the data presents an encouraging picture, indicating a gradual recovery from the economic challenges of the past two years, underlying weaknesses in momentum persist. The rise in expectations, though positive, is described as "very sluggish" and has yet to substantially impact the situation values.

As for ECB, Sentix said the window for cutting interest rate "does not appear to be very large". Despite improvements in the economy, a deteriorating inflation environment adds pressure to bond markets.