Sample Category Title

RBA on Gold and Remains Vigilant to the Upside

Rates unchanged as expected, as Board balances near-term inflation risks with desire to avoid recession.

As expected, the RBA Board left the cash rate target unchanged at 4.35% following its May meeting but strengthened its rhetoric around upside inflation risks. The statement highlighted that inflation is declining, but more slowly than expected. Services inflation is moderating only gradually, driven by a labour market that the RBA now assesses to be tighter than previously thought. It is noteworthy that the more forward-looking indicators in the RBA’s suite have eased more than lag indicators such as the unemployment rate.

Monetary policy is assessed as restrictive, and the current level of the cash rate is seen as supporting continued progress on getting inflation back into the 2–3% target. In the media conference, the Governor confirmed that both a rate hike and holding rates unchanged were discussed at the meeting, with the Board ultimately deciding to hold.

The forward-looking parts of the statement continue to emphasise that the Board is not ruling anything in or out in terms of future policy. While there have been upside surprises in recent inflation and labour market data, these occurred in a context of weak domestic demand and a trajectory for inflation that is still clearly downwards. In the media conference, the Governor emphasised that the Board is trying to get inflation down in good time to ensure inflation expectations remain well anchored, while not going so fast that they tip the economy into recession.

Appropriately, the Board remains circumspect about the volatility in the data, noting that the disinflation journey is ‘unlikely to be smooth’. As we noted last week, reacting to every upside surprise carries its own risks. Recall that an upside surprise on inflation in the September quarter was met with a rate hike at the November meeting, only for the December quarter data to surprise on the downside and the upgrade to the forecasts reversed out for the February 2024 round. Despite the Board’s concerns, they were always going to need more than one quarter of upside surprise to adjust their strategy. In the media conference, the Governor highlighted that the Board had already taken out some insurance in November against inflation risks, and that the current forecasts looked a lot like the forecasts from November.

Given recent data, the RBA’s inflation forecasts for 2024 have been upgraded, but calendar 2025 and beyond are unchanged. The near-term growth forecasts have been downgraded, with GDP growth over 2024 now expected to be 1.6%, in line with Westpac’s forecast, rather than 1.8% as in the RBA’s February forecast round; the language in the Statement on Monetary Policy (SMP) is also more downbeat.

Most of the downgrade to the growth outlook was driven by a weaker outlook for consumption, despite an upgrade to expected income growth; the upgrade to household saving, both in the data and implied by the forecasts, highlights that the pure cashflow effect is not the only way higher interest rates affect consumption. In contrast to household consumption, the expected turnaround in dwelling investment has been shifted earlier. Given the continued decline in approvals, this puzzling revision might imply the RBA expects that the large pipeline of building work underway somehow unclogs.

Despite lower expected near-term GDP growth, the labour market forecasts have been upgraded (a lower unemployment rate in December 2025 and June 2026, now 4.3% from 4.4%), as were the forecasts for growth in the Wage Price Index (WPI). In contrast to previous statements, today’s statement notes ‘Wages growth appears to have peaked but is still above the level that can be sustained given trend productivity growth.’ The previous language was that ‘this level of wages growth remains consistent with the inflation target only on the assumption that productivity growth increases to around its long-run average.’ Our own forecast for WPI shows a turning point this year as last year’s outsized increase in minimum and award wages drops out of the year-ended growth calculation.

The new forecasts key off changed assumptions, including a higher path for market rates (market economist views are no longer an input). The RBA would also be aware that there is still some pass-through of past rate hikes to come, as remaining fixed-rate mortgages roll off.

As for the past few meetings, the media release states that the Board will be attentive to ‘developments in the global economy, trends in domestic demand, and the outlook for inflation and the labour market’. Contrast that with the language in the Bank of Canada’s statement: ‘Governing Council is particularly watching the evolution of core inflation, and continues to focus on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour.’

The RBA language downplays the roles of supply and of firms’ decisions to pass on higher costs in slowing the decline in disinflation. The RBA’s analysis instead remains that high inflation declining slowly is a signal that aggregate demand is still too high. We did, however, note a shift away from the language in the November 2023 minutes, where an inflationary mindset among businesses was noted. In today’s SMP, the box on messages from liaison highlighted that firms were finding it harder to pass on cost increases and were instead focusing on cost containment and boosting productivity.

A special chapter in the SMP focused on potential output. This is a response to the recommendations of the RBA Review and reflects the revised Statement on the Conduct of Monetary Policy with the Government. An outworking of these recommendations is that the RBA staff are now being expected to rely a lot more on theoretical models in their analysis of the economy. While the chapter (and a companion Bulletin article on how full employment is assessed) sensibly highlight that no model is perfect and judgement is needed, one implication is a heightened risk that central banks including the RBA all make the same analytical mistake at the same time.

Overall, we see the policy decision as poised. As the Governor noted in the media conference, it is hoped that they will not need to raise rates further, but they will act if needed. Likewise, our house view is that the most likely outcome is unchanged rates for a period, but further upside surprises will change the calculus.

AUD/NZD: Aussie Medium-Term Outperformance Against Kiwi Intact Supported by RBA

- Today’s RBA monetary policy decision statement has kept the possibility of a rate hike before 2024 ends “alive”.

- The narrowing of the discount between Australia-New Zealand sovereign bonds yield spread has supported the potential continuation of the AUD/NZD medium-term uptrend phase.

- Watch the key medium-term support of 1.0940 on the AUD/NZD.

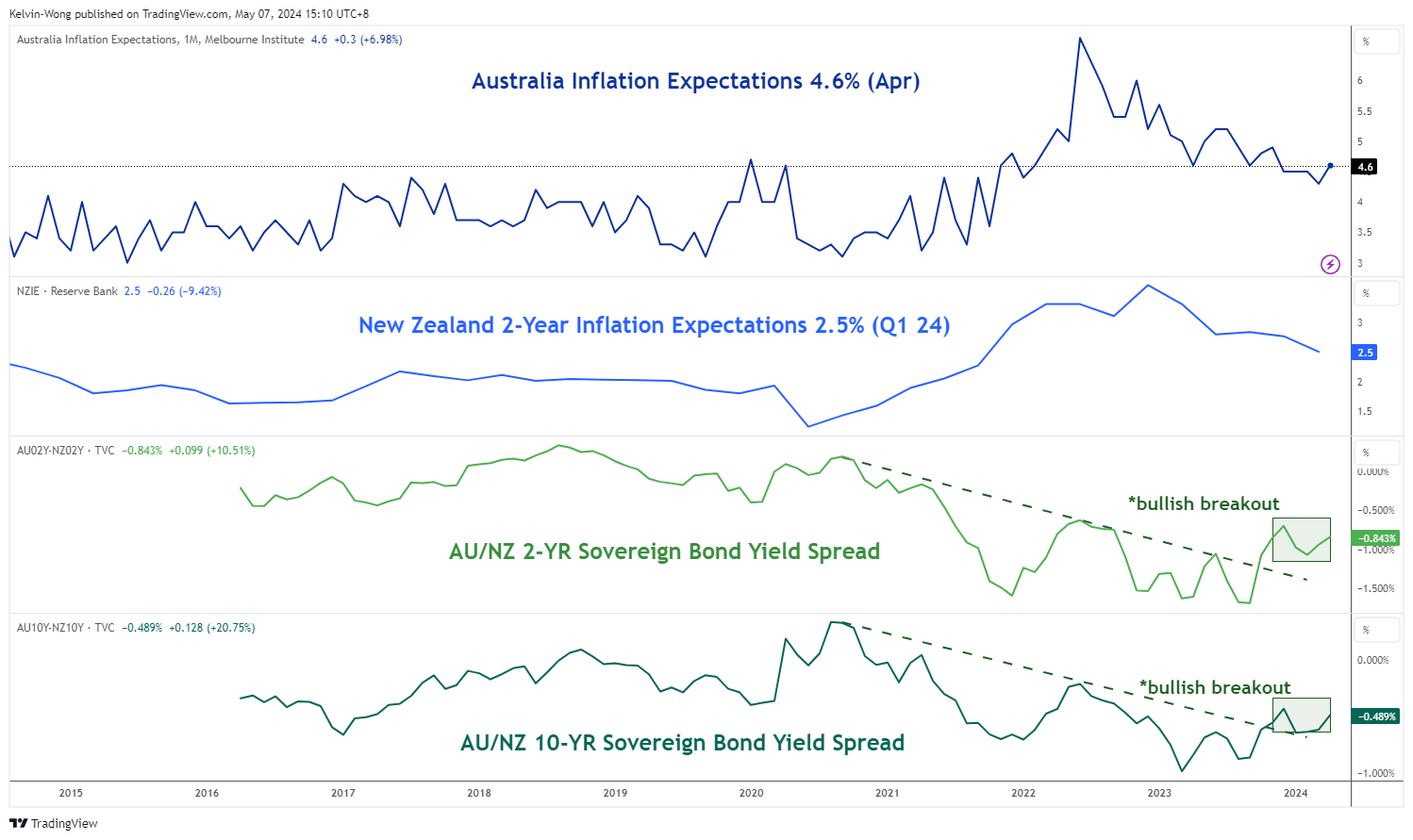

The paths of inflationary trends between the two Antipodean countries have started to diverge in the past month.

Higher inflationary pressures in Australia versus New Zealand

Fig 1: Inflationary expectations of Australia & New Zealand with AU/NZ sovereign bond yield spreads as of 7 May 2024 (Source: TradingView, click to enlarge chart)

Forward-looking consumer inflation expectations in Australia have inched higher to 4.6% in April from 4.3% printed in March, its highest pace of increase since November 2023 amid elevated prices in services components. In contrast, New Zealand’s 2-year inflation expectations fell to 2.5% in Q1 2024, its lowest level since Q3 2021 from 2.76% recorded in Q4 2023 (see Fig 1).

Therefore, the Australian central bank, RBA has adopted a more cautious and prudent stance on its monetary policy guidance and opted to have a more hawkish tilt in keeping the doors open for a hike above the current policy cash rate at 4.35%.

RBA has kept the door open for a rate hike in 2024

RBA has chosen to maintain its policy cash rate at 4.35% in today’s monetary policy meeting for the fourth consecutive time, its highest level in almost 12 years. No major surprises and the tonality of the accompanying monetary policy statement is almost the same as the prior March’s meeting; the persistence of services inflation is a key uncertainty, some time is required for inflation to hit the target range of 2% to 3%, vigilant to upside risks, and not ruling anything in or out on future decisions are the key takeaways.

During RBA Governor Bullock’s press conference, she reiterated the key takeaways from the current momentary policy statement and added that current market pricing on the cash rate futures is “reasonably balanced” which implies that an RBA rate hike before 2024 is still a “live” event as the cash rate futures has priced in an implied yield of 4.43% on the September and October 2024 contracts as of 6 May 2024, above the policy cash rate of 4.35% by 7 basis points.

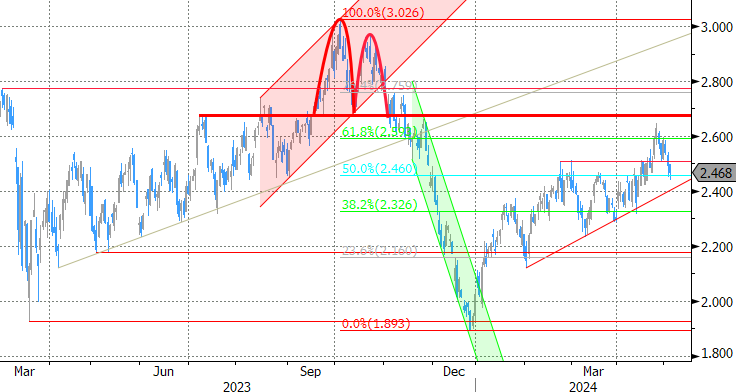

Bullish breakout in AUD/NZD

Fig 2: AUD/NZD major & medium-term trends with Gold/Copper ratio as of 7 May 2024 (Source: TradingView, click to enlarge chart)

In the medium-term (multi-week) horizon, recent price actions of the AUD/NZD cross pair via the late April’s bullish breakout above its former medium-term descending resistance from 20 December 2023 swing high has reinforced a medium-term uptrend phase in play since its 22 February 2024 low of 1.0570 (see Fig 2).

The daily MACD trend indicator has inched higher above its signal line which supports the ongoing medium-term uptrend phase of the AUD/NZD.

Intermarket analysis also reinforces a further potential outperformance of AUD against NZD via the narrowing of the 2-year and 10-year yield spread discount of Australia-New Zealand sovereign bonds in the past two months (see Fig 1).

Watch the 1.0940 key medium-term pivotal support on the AUD/NZD to maintain the bullish tone for the next medium-term resistance to come in at 1.1090 and 1.1165 (also the upper boundary of the ascending channel from the 22 February 2024 low).

On the other hand, a break below 1.0940 negates the bullish tone to expose the next intermediate support at 1.0870 (also the 50-day moving average).

UK100 Analysis: Stock Market Optimistic Ahead of Bank of England News

On Monday, the UK observed a bank holiday for May Day, and on Tuesday, the stock market demonstrated accumulated optimism.

The FTSE index (UK100) today surpassed the 8300 mark. Additionally:

→ The opening occurred with a bullish gap;

→ On the daily chart of UK100, today the RSI indicator is in overbought territory, unseen since the beginning of 2023.

One of the significant drivers of bullish sentiments could be considered events on Thursday – at 14:00 GMT+3, news from the Bank of England is expected: market participants will learn about the decision on the interest rate, followed by a press conference.

As Econoday writes:

→ A decision to cut interest rates is unlikely at Thursday's meeting, with autumn being seen as the most probable period for a 0.25-point rate cut from the current level of 5.25 points.

→ Members of the rate-setting committee are concerned that inflation is slowing down too slowly. However, the trend is in the right direction, and the Bank of England has already stated that the 2 percent target does not necessarily need to be reached before interest rates are lowered.

Perhaps the anticipation of signals for monetary policy easing instils confidence in the bulls, but how sustainable can the current growth be?

As shown by the technical analysis of the UK100 chart:

→ The price is moving within a long-term ascending channel (shown in blue). Meanwhile, its upper boundary is around the price level of 8500, which could serve as resistance if market sentiment remains equally optimistic;

→ On the other hand, the price of UK100 is vulnerable to some correction. If it occurs, former resistance at 8200 may provide support. As indicated by the violet lines, successful tests of former resistance underscore the bullish nature of the market.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

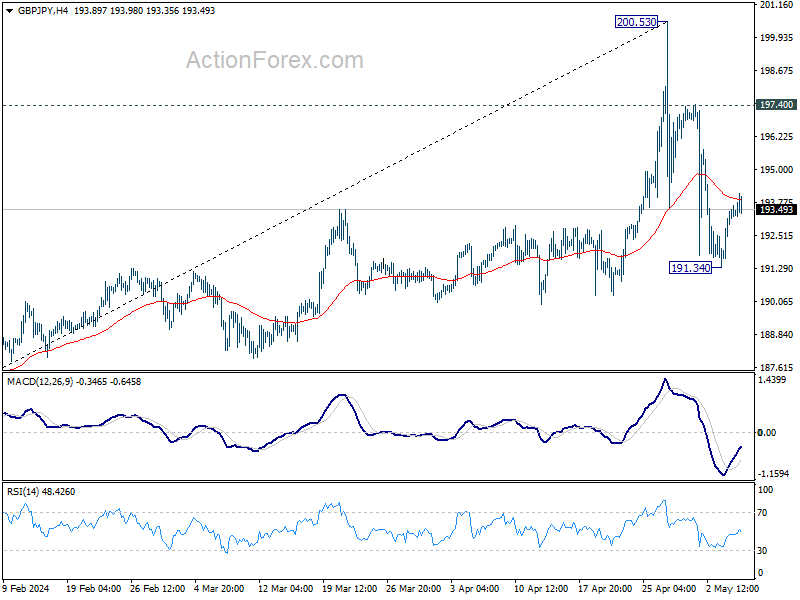

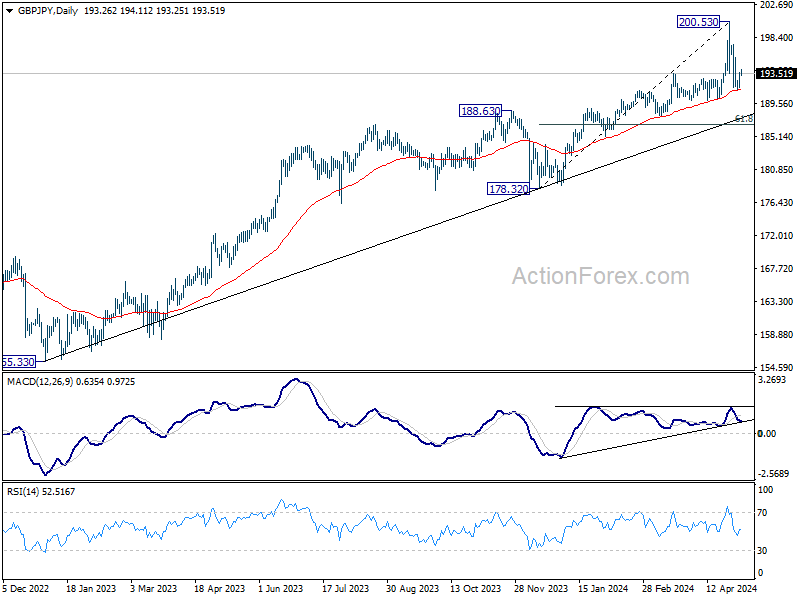

GBP/JPY Daily Outlook

Daily Pivots: (S1) 192.11; (P) 192.89; (R1) 194.11; More..

Intraday bias in GBP/JPY remains neutral at this point. On the upside, sustained break of 55 4H EMA (now at 193.86) will bring stronger rebound back toward 197.40 resistance. On the downside, below 191.34 will resume the correction from 200.53. Sustained trading below 55 D EMA (now at 191.51) will target 61.8% retracement of 178.32 to 200.53 at 186.80.

In the bigger picture, a medium term top could be in place at 200.53 after breaching 199.80 long term fibonacci level. As long as 55 W EMA (now at 183.34) holds, fall from there is seen as correcting the rise from 178.32 only. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 178.32 support.

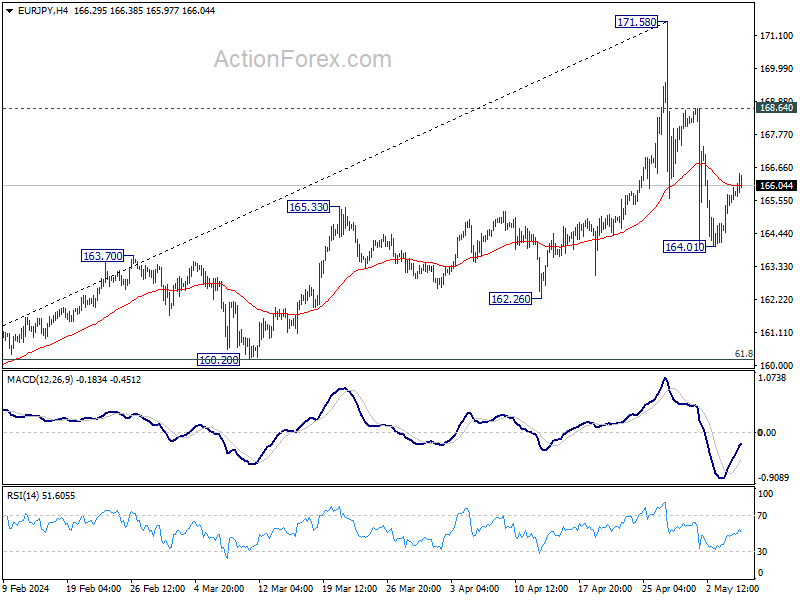

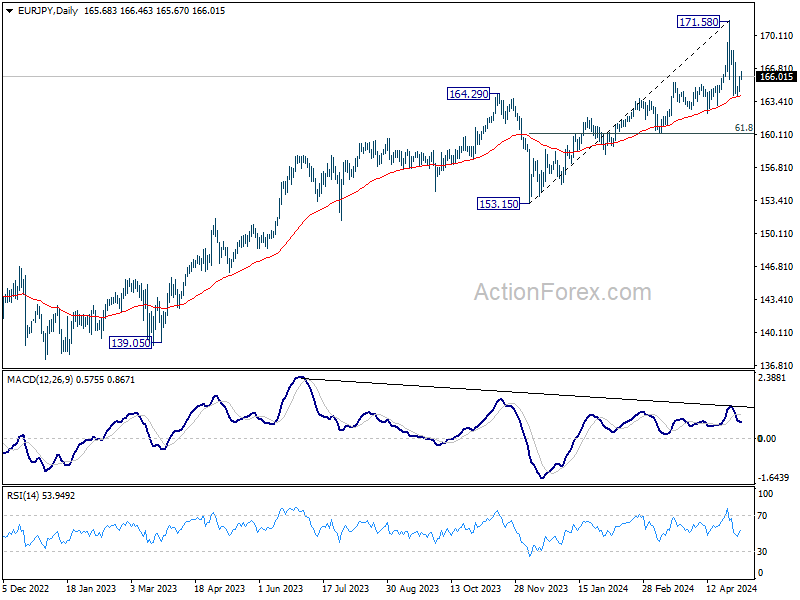

EUR/JPY Daily Outlook

Daily Pivots: (S1) 164.81; (P) 165.40; (R1) 166.34; More...

Intraday bias in EUR/JPY stays neutral at this point. On the upside, firm break of 55 4H EMA (now at 166.084) will bring stronger rebound towards 168.64 resistance. On the downside, break of 164.01, and sustained trading below 55 D EMA (now at 164.06) will extend the fall from 171.58 to 61.8% retracement of 153.15 to 171.58 at 160.19.

In the bigger picture, a medium top could be formed at 171.58 after brief breach of 169.96 (2008 high). As long as 55 W EMA (now at 157.82) holds, fall from there is seen as correcting the rise from 153.15 only. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

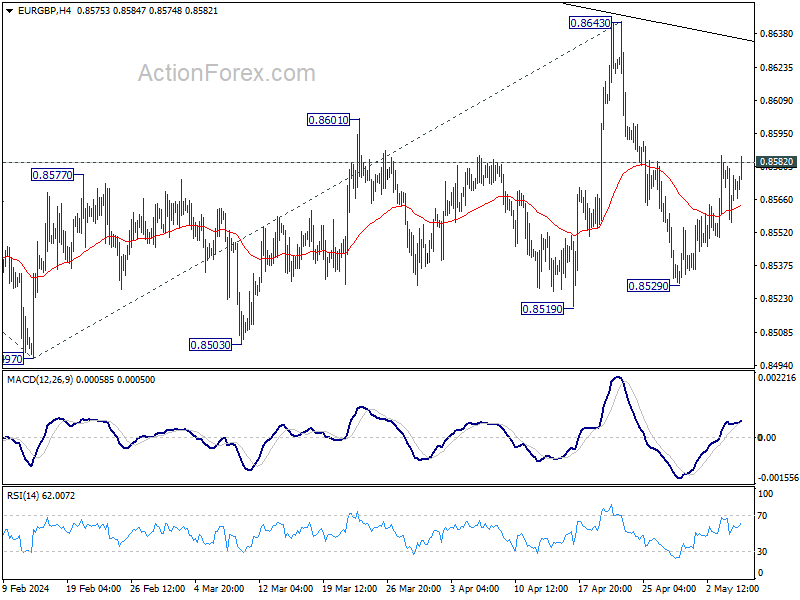

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8559; (P) 0.8571; (R1) 0.8584; More...

Intraday bias in EUR/GBP stays neutral at this point. Focus remains on 0.8582 resistance. Further decline is expected as long as 0.8582 resistance holds. Below 0.8529 will target 0.8491/7 support zone. However, decisive break of 0.8582 will bring stronger rise back to 0.8643 resistance instead.

In the bigger picture, outlook remains bearish as EUR/GBP is capped below medium term falling trendline. That is, down trend from 0.9267 (2022 high) is still in progress. Firm break of 0.8491/7 will target 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

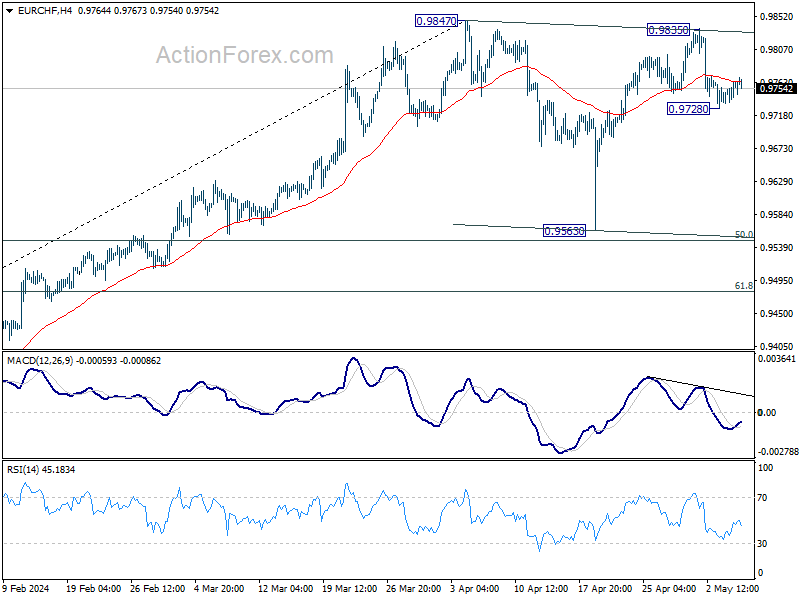

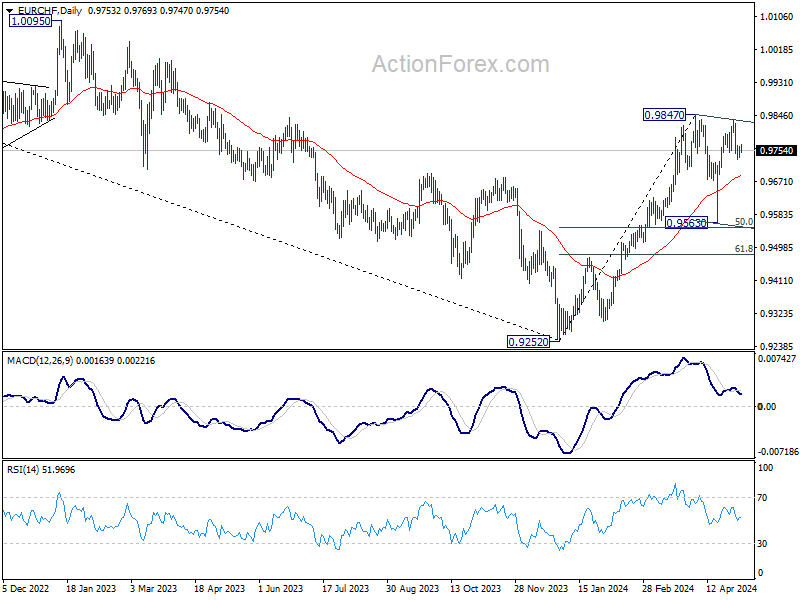

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9740; (P) 0.9753; (R1) 0.9773; More...

Intraday bias in EUR/CHF is turned neutral with current recovery. Outlook is unchanged that fall from 0.9835 is seen as the third leg of the corrective pattern from 0.9847. Risk will stay on the downside as 0.9835 resistance holds. Below 0.9278 will turn bias back to the downside for 0.9563 support.

In the bigger picture, as long as 0.9563 support holds, rise from 0.9252 medium term bottom is still in favor to continue. Break of 0.9847 resistance will target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004.

Dollar Basically Didn’t Go Anywhere

Markets

Markets yesterday staged some follow-through price action on Friday’s post-payrolls/ISM easing, but the move gradually slowed in US dealings. Fed governors Williams and Barkin confirmed last week’s view of Chair Powell that the next Fed move will likely be a rate cut. A restrictive policy is bringing the economy in a better balance and at some point should return inflation back to 2%. Data will decide on the timing. The Fed’s quarterly Senior Loan Officer Opinion Survey on bank lending also indicated that tighter financial conditions are working through toward lending (cf infra). This should gradually slow demand and inflation. At the end of the day, the US 2-y yield rose 1.5 bps. Yields at the long end of the curve still declined up to 3.0 bps (30-y). German yields eased between 1.2 bps (2-y) and 2.7 bps (10-y). Fed guidance that, despite sticky inflation, its next step will likely be a rate cut continues to give comfort to equity investors. US indices added up to 1.19% (Nasdaq). The dollar basically didn’t go anywhere. The DXY index closed unchanged (105.05). EUR/USD gained marginally (close 1.0769). USD/JPY was the exception to the rule, rebounding to 153.9. The US-Japan interest rate differential clearly remains too big to prevent yen selling.

Asian markets mostly join the risk-on sentiment from WS yesterday. Yields decline marginally. The dollar gains a few ticks. The yen remains in the defensive. Headlines of Japan’s currency official Masato Kanda that no interventions are needed when markets move orderly, suggest that any interventions might remain rather selective. The yen weakens further this morning (USD/JPY 154.5). Later today, the eco calendar only contains second tier data. German factory orders and EMU retail sales might bring some additional insight on the EMU recovery. ECB governors De Cos and Nagel are scheduled to speak. The US Treasury will kickoff this week’s refinancing operation with the sale of $58 bln of 3-year notes. It will be interesting to see demand in the wake of last week’s decline in yields. We expect some more technical trading ahead of the April US inflation data to be published next week. We see 4.70% and 4.37% as tough support for the US 2 and 10-y yield respectively. The yield correction slowing also might help to put a floor for the dollar. EUR/USD 1.0807/11 (38% retracement Dec-April decline/ correction top) remains first reference on the EUR/USD chart.

News & Views

The Fed’s latest Senior Loan Officer Opinion Survey (SLOOS) showed that banks grew more cautious about lending while higher interest rates continued to weigh on loan demand. Standards were raised for all loan categories except some residential real estate products. Higher standards were applied to commercial real estate loans in particular. That said, the net share of banks tightening conditions fell for most loan products in what is potentially a sign of loan growth moving beyond the trough. More banks reported tighter conditions for commercial and industrial loans but the net share remains well below last July’s peak. The share of banks tightening standards for auto loans ticked up but a smaller proportion reported higher standards for credit card and other consumer loans. Demand for all types of consumer loans remains in retreat.

The Reserve Bank of Australia (RBA) kept the policy rate stable at 4.35% this morning. The status quo followed the observation that inflation was declining more slowly than expected (3.6% q/q in Q1 this year from 4.1%). Underlying inflation was higher and declined by less, in large part due to services inflation. The RBA said there’s still excess demand while labour market conditions are tighter than is consistent with inflation at target. New forecasts are based on a market-implied policy rate path which assumes a steady rate through mid-2025. This compares to the February projections assuming rate cuts from 2024H2 on. Yet, inflation was revised higher across the horizon with an EoY target of 3.8% (vs 3.2%) only to enter the RBA’s 1-3% band in December 2025 (2.8%). The RBA singled out the persistence of services inflation as a key uncertainty to this trajectory. GDP growth was marginally cut to 1.6% this year amid particularly weak household consumption. The central bank repeated that it does not rule anything in or out in terms of rates and sticks to a data-dependent approach. Markets were clearly hoping for something a little more aggressive after the recent string of strong labour and inflation data. The Aussie dollar loses some ground to AUD/USD 0.661 and swap yields ease up to 9 bps at the front end of the curve.

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June) rate cut which has broad backing. EMU disinflation continued in April and brought headline CPI closer to the 2% target. Together with weak growth momentum, this gives backing to deliver a first 25 bps rate cut. A more bumpy inflation path in H2 2024 and the Fed’s higher for longer strategy make follow-up moves difficult. Markets have come to terms with that.

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective, but Fed’s Powell left the door open for rate cuts later this year. Soft US ISM’s and weaker than expected payrolls supported markets’ hope on a first cut post summer, triggering a correction off YTD peak levels. Sticky inflation suggests any rate cut will be a tough balancing act. 4.37% (38% retracement Dec/April) already might prove strong support for the US 10-y yield.

EUR/USD

Economic divergence, a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead and higher than expected US CPI data pushed EUR/USD to the 1.06 area. From there, better EMU data gave the euro some breathing space. The dollar lost further momentum on softer than expected early May US data. Some further consolidation in the 1.07/1.09 are might be on the cards short-term.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view, suggesting that the disinflation process provides a window of opportunity to make policy less restrictive (in the near term). Sterling’s downside turned more vulnerable with the topside of the sideways EUR/GBP 0.8493 - 0.8768 trading range serving as the first real technical reference.

RBA Stays Pat, AUD Falls

The week started on a positive note for the global equities which continue to surf on the optimism that the Federal Reserve’s (Fed) next move won’t be a rate hike, which I think is overdone and that next week’s US inflation data could be a rude awakening.

But one thing is sure, the earnings season is going well and analysts project that the S&P500 earnings will grow 17% this year. The S&P500 jumped 1% yesterday above the 50-DMA. FTSE futures are up 1% and will likely push the British blue-chip index to a fresh record at the open.

Stocks in Japan remain supported by the loose Bank of Japan (BoJ) policy and a soft yen, Chinese equities continue to recover and the CSI index is back above its 200-DMA since last week. The index is up by nearly 20% since the February dip on Chinese efforts to boost its economy and investors looking to diversify following record highs in major Western markets.

On the geopolitical front, things hardly move toward the right direction. This week, Xi Jinping is visiting Europe. Behind the forces smiles, Xi asks Macron to avoid a new cold war, while the EU doesn’t want China to dump prices of solar panels and electric cars, and Ukraine is a major headache. We all know that we are not going back to the old good days of happy globalization anytime soon, and the latter will continue to weigh on China appetite. Without the help of the rest of the world, China will hardly go back to its pre-2020 glorious days.

In the Middle East, tensions remain. US crude remains bid near the 100-DMA – and near oversold market conditions – as Israel refused a ceasefire deal and is preparing for a big offensive in Rafah. The $80-80.50pb range - where the 200-DMA meets the major 38.2% on ytd rise - is the key technical area to watch. Right now, oil is trading in the bearish consolidation zone, but the reflation trade, the geopolitical setup and OPEC risks point that we could see a dip near the $77/78pb zone and recovery. OPEC and its allies will likely extend supply cuts into the second half of the year to prevent from a global surplus to press prices. Iraq and Kazakhstan are working on curbing their production to get back into their quotas. But the US’s got the world’s back covered. The daily production there has almost reached 13 mio barrels per day – that’s more than Saudi Arabia which pumps around 9 mio barrels a day. Beyond the possibility of a short term spike, we will unlikely see the price of a barrel of crude go too, high too fast. And that’s good news for your global inflation battle.

Speaking of that, the Reserve Bank of Australia (RBA) left its policy rate unchanged today and warned that inflation is declining more slowly than expected, that persistence of services inflation is a key uncertainty, that it will be some time yet before inflation is sustainably in the target range and that they will remain vigilant to upside risks. Surprisingly, the kneejerk reaction to the decision has been a decline in the AUDUSD to the 66 cents level. Elsewhere, the USDJPY recovers timidly after last week’s presumed intervention from the Bank of Japan (BoJ), the EURUSD tests the 200-DMA resistance while Cable trades timidly above its own 200-DMA with the risk of seeing the recent gains melt rapidly if the Bank of England (BoE) gives a clearer sign of an approaching rate cut at this week’s meeting.

We Now Expect Two Rate Cuts from Fed This Year

In focus today

Today is a quiet day on the data front. In the euro area, focus is on March retail sales and German factory orders. Consumers are still cautious with spending amid low unemployment and rising real incomes so we expect muted spending.

We revise our Fed call to 2 rate cuts of 25bp this year in September and December. It will be a close call between July and September but with macro indicators showing no signs of sudden weakening, we lean towards September as our base case.

Economic and market news

What happened overnight

Mixed signals from the Israel-Hamas war, as yesterday afternoon first brought reports of explosions in Rafah, the southernmost area of the Gaza strip, and that the IDF were evacuating residents in the area which indicated that Israel could be preparing for an attack on the area which houses 2.3 million refugees. In the evening, Hamas then announced it had accepted a ceasefire deal from Egyptian/Qatari mediators to which Israeli officials responded that no such deal had been reached, according to Reuters. As of this morning it is clear Israel has not agreed to a ceasefire, but says it is sending a delegation to negotiate with mediators while continuing operations in Rafah which is yet to turn into a major operation.

This morning the Reserve Bank of Australia kept its cash rate fixed at 4.35% as widely expected. Markets have pushed back their rate cut expectations significantly recently after the clear upside surprise in Q1 inflation data.

Markets seemed to continue to challenge the Japanese authorities' fortitude after last week's suspected intervention which brought USD/JPY to 152.98 (-3.1%) on Friday, as the cross gained 0.6% during the day and climbed further past 154 overnight, up some 0.5% as of this morning, after top currency official Kanda said there was no need to intervene if "the market is functioning properly". The dovish signals from the US have supported the yen, but authorities continue to be in a bind as there are still signs of substantial rate differentials in the near-term, which complicates any persistent effects of an intervention.

What happened yesterday

In the US, both Richmond Fed President Barkin and NY Fed President Williams on separate occasions said the current rate target was appropriate indicating we are not in for hikes any time soon, with Williams stating that "eventually we'll have rate cuts". This echoes last week's FOMC meeting and overall market sentiment, which currently has 2 cuts priced in for the year.

Three ECB policymakers said the ECB was more confident about cutting rates, with both Phillip Lane, Boris Vujcic and Gediminas Simkus saying they were confident that inflation was enroute to target. The April PPI gave the same signals as the print showed a 0.4% m/m decline and thus continued to hover around the -8% y/y as it has for the past half year. This indicates no pressure on goods prices from producer prices meaning we should expect core goods inflation to remain subdued in the near term.

Market movements

Equities: Global equities saw an increase yesterday in a session devoid of major news, making it a relatively quiet session. It is not necessarily disadvantageous when the absence of news is perceived as good news. In other words, the news received during the previous busy weeks may have a positive influence on subsequent weeks, giving investors time to digest and reconsider the cumulative past data. Yesterday's risk-on session was dominated by small-caps, cyclicals, high-beta, and long momentum, while value and minimum volatility lagged. In the US, the Dow increased by 0.5%, S&P 500 by 1.0%, Nasdaq by 1.2%, and Russell 2000 by 1.2%. Asian equity markets continued to rise this morning, led by South Korea with a 2.4% increase and markedly higher in Japan despite the USDYEN at 154. European futures higher this morning, while US futures are more mixed.

FI: The UK bank holiday left a solid mark on European rates markets resulting in very limited volumes and volatility. Some initial catch up to the US treasury trading on Friday sent yields marginally lower from the start, yet after grinding higher through the day, the 10y German Bund yield ended 2bp lower on the day in what can be characterised as a bull flattening move. There was no significant market news.

FX: We were off to a quiet start to the week with UK markets out due to Spring Bank Holiday yesterday. EUR/USD stabilized around the mid 1.07 mark while NOK gained modestly. EUR/CHF edged higher still recovering from last wee'’s topside inflation surprise. For the SEK, the Riksbank meeting tomorrow is in focus where we see the potential for a move higher on the back of our expectation of an unchanged decision. More broadly however, the Scandies continue to be closely tied to movements in USD rates, where we see the balance of risk for lower rates and hence potential for temporary Scandi strength.