Sample Category Title

USD/JPY 160 the Line in Sand for (Hhidden) Interventions?

Markets

Japanese markets were closed for Showa day today. Still, despite (or maybe due to) holiday thinned market conditions, the yen moved sharply up and down this morning. At first, Friday’s post BoJ yen weakening due to persistent policy divergence between the BoJ and colleagues from other developed countries continued and even accelerated. USD/JPY briefly surpassed the 160 barrier, a level not seen since April 1990. However, ‘out of the blue’ the yen regained 5-yen. Was USD/JPY 160 the line in the sand for (hidden) interventions? Japanese authorities see value in keeping their cards close to their chest and didn’t comment, but news agencies, referring to sources familiar with the matter, reported that interventions indeed occurred. Over the next days, in more normal market conditions, we will learn more on how many resources the Japanese Fin Min is prepared to put on the table and how effective their strategy might be to slow the freefall of the currency. The supposed interventions had some brief knock-effects on the dollar overall (DXY currently trades in the 105.60/70 area from 106 early in Asian dealings). However, after all, the impact on the likes of EUR/USD was limited.

Aside from the developments in Japan, preliminary April inflation data from Belgium, Spain and Germany provided a first insight in the potential outcome of the EMU inflation release scheduled tomorrow. Spanish headline inflation slightly reaccelerated to 3.4% from 3.3% on a monthly dynamic of 0.6%. Core inflation slowed slightly more than expected from 3.3% to 2.9%. German HICP inflation showed a similar picture at 0.6% M/M and 2.4% Y/Y (from 2.3%), as higher energy prices put some upward pressure on inflation dynamics. The EMU inflation path might be more bumpy in the months ahead, but today’s data don’t suggest a big upward surprise for tomorrow’s EMU flash CPI release. Such an outcome (2.4% headline, 2.6% core expected) leaves the ECB scenario for a first 25 bps June rate cut intact. After a protracted drift north, US and EMU yields today cautiously build on Friday’s ‘technical correction’. US yields are easing between 1 bp (-2-y) and 2.5 bps (10-y). German yields decline between 3 bps (2-y) and 4.5 bps (30-y). Going into key US and EMU data later this week, we don’t draw firm conclusions from today’s price action. European equites are trading mixed (EuroStoxx 50 -0.3%). The dollar is losing modest ground, maybe partially due to the decline in USD/JPY. EUR/USD rebounded to 1.071, but the technical picture remains neutral for now. In line with last week price action, sterling slightly outperforms the euro. EUR/GBP trades again in the middle of the previous consolidation pattern between 0.85 and 0.86. Markets currently still see less than two 25 bps BoE rate cuts this year compared to almost 75 bps of ECB easing. Contrary to the EMU (GDP data) and the US (ISM, Payrolls, Fed) there are few important UK data scheduled for release this week.

News & Views

The Belgian economy grew by 0.3% in Q1 2024, the National Bank of Belgium’s flash estimate showed today. GBFP as a result was 1.3% bigger compared to the same quarter last year. The initial reading only shows a sectoral breakdown. Value added rose by 0.3% q/q in industry. Activity slowed in the services sector, which nonetheless posted positive growth of 0.3%. Finally, value added in the building industry fell by 0.2%. A separate release from Statbel revealed Belgian inflation picking up from 3.18% to 3.37% in April with energy (from -1.61% to 9.19%) adding the first positive contribution since March 2023. Core inflation declined to 3.26% from 3.85% while a gauge for services inflation proved much stickier (from 5.04% to 4.93%). Inflation for rents has edged down to 5.43% from 5.62% while food (including alcoholic beverages) stood at 0.25% this month, compared to 3.21% last month.

Spanish premier Sanchez is staying in office. The socialist announced that today after withdrawing from all public appearances for several days last week. Sanchez considered quitting after a judge opened a case against his wife Begona Gomez over alleged influence-peddling and corruption on a complaint of an anti-corruption organization with far-right links. Sanchez denounced the move saying the investigation is a right-wing intimidation campaign. His resignation would most likely have toppled the current fragile minority government, resulting in snap elections in an increasingly fragmented political landscape and less than one year after the previous one. Next month is an important one politically, with Catalonia holding regional elections on May 12. It’s not yet clear whether the recent developments have affected Sanchez’s Socialist Party being on course to take power from the incumbent separatists.

Graphs

USD/JPY: yen rebounds on presumed interventions after weakening beyond USD/JPY 160 barrier.

EUR/SEK: Krone stays in the defensive as Q1 contraction suggests need for Riksbank support.

German 10-y yield: taking a breather as inflation data keep scenario for first ECB rate cut in June alive.

EuroStoxx50: still struggling to avoid sell-on upticks pattern

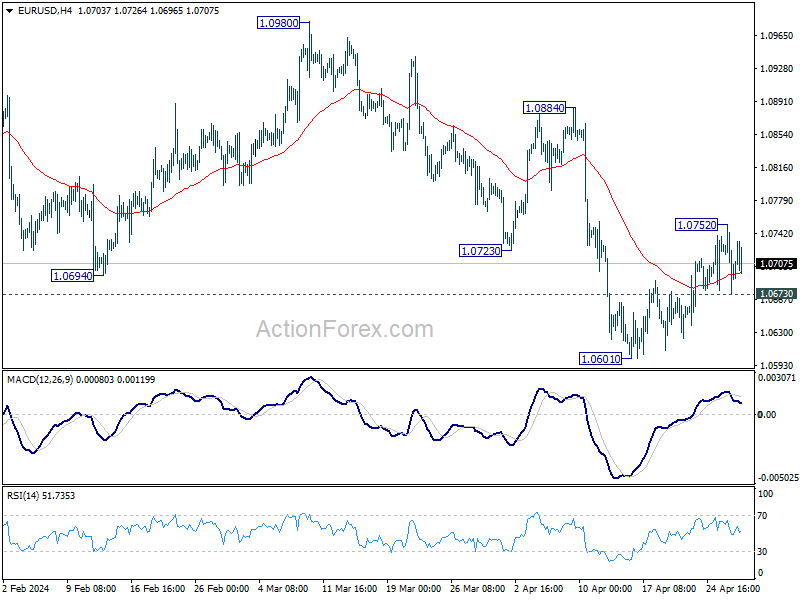

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0660; (P) 1.0707; (R1) 1.0739; More...

Intraday bias in EUR/USD stays neutral and outlook is unchanged. On the upside, above 1.0752 will resume the rebound to 55 D EMA (now at 1.0780). On the downside, break of 1.0673 minor support will turn intraday bias to the downside for retesting 1.0601 low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below, strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

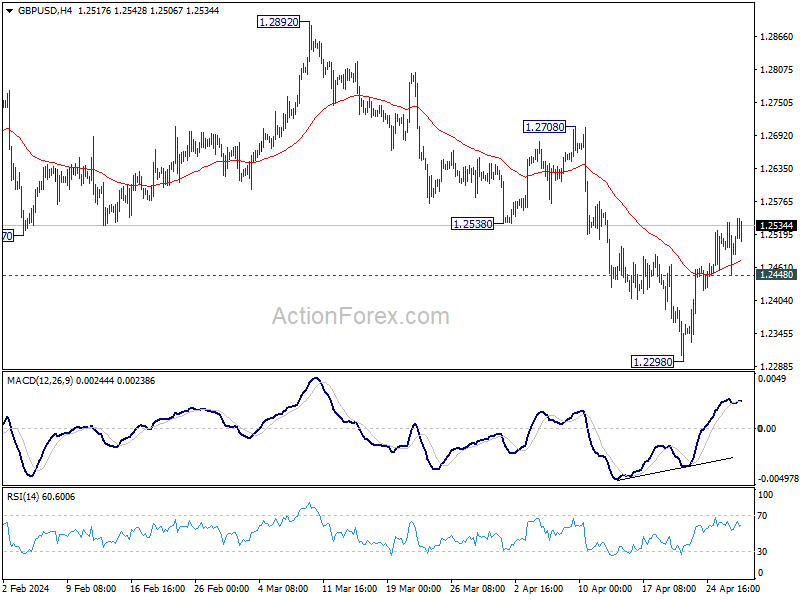

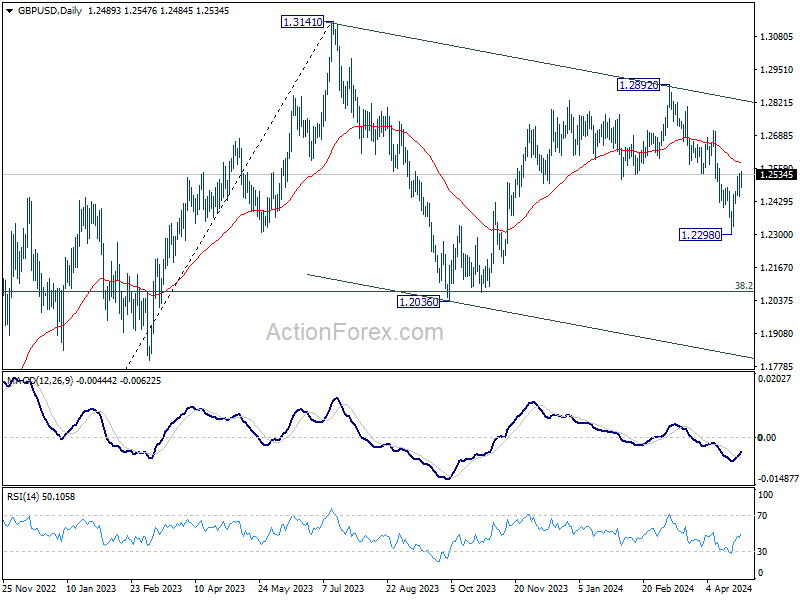

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2448; (P) 1.2495; (R1) 1.2540; More...

Intraday bias in GBP/USD remains on the upside at this point. Rebound from 1.2298 short term bottom would target 55 D EMA (now at 1.2582). Sustained break there will argue that fall from 1.2892 has completed already, and bring further rise to this resistance. Nevertheless, on the downside, break of 1.2448 minor support will bring retest of 1.2298 low instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

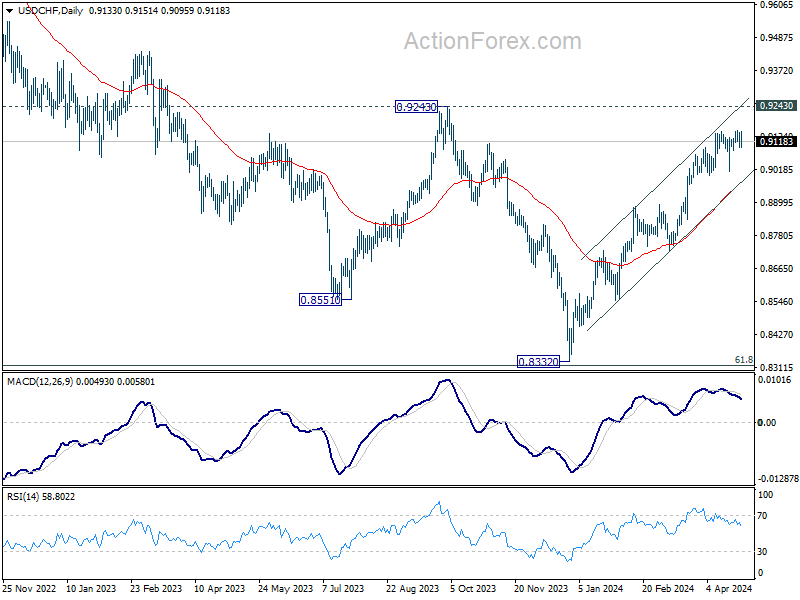

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9111; (P) 0.9130; (R1) 0.9165; More....

Intraday bias in USD/CHF remains neutral as sideway consolidation continues. On the upside, firm break of 0.9151 will resume the rally from 0.8332 and should target 0.9243 key resistance next. On the downside, break of 0.9085 will turn bias to the downside for deeper pullback.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8884 resistance turned support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.

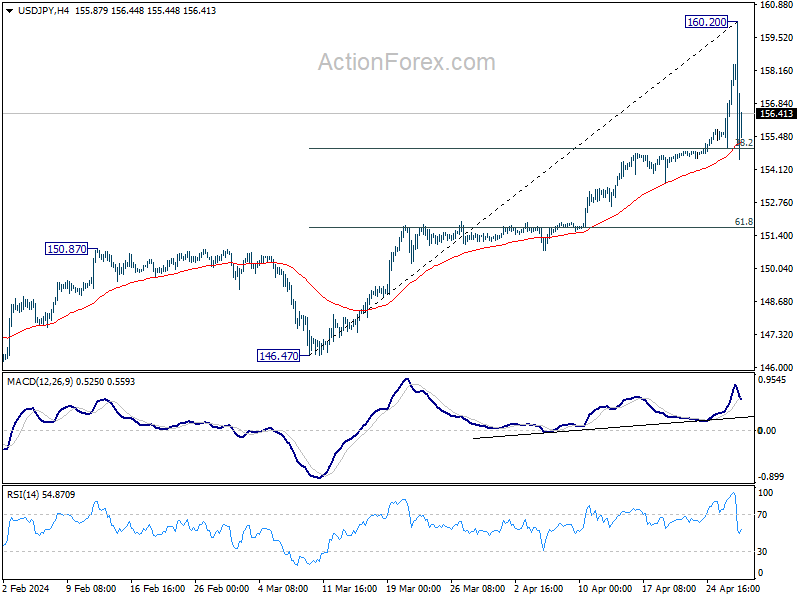

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.06; (P) 157.26; (R1) 159.53; More...

Intraday bias in USD/JPY remains neutral at this point as consolidation from 160.20 short term top is extending. Strong support could be seen from 38.2% retracement of 146.47 to 160.20 at 154.95 to bring recovery. But break of 160.20 is not envisaged for now. However, firm break of 154.95 will turn bias to the downside for deeper correction to 55 D EMA (now at 151.83).

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 100% projection of 127.20 to 151.89 from 140.25 at 164.94. Outlook will remain bullish as long as 150.87 resistance turned support holds, even in case of deep pullback.

Yen Stabilizes After Sharp Rally, Japan Withholds Confirmation of Intervention

Yen is currently trading as the strongest currency for the day as the markets enter into US session. The earlier dip below 160 psychological support against Dollar spurred a wave of buying, propelling Yen sharply higher. However, subsequent trading has not shown clear follow-through momentum, indicating that the initial surge may have been more of a reactive spike.

Amidst speculation about market intervention by Japan, Masato Kanda, Vice Minister for International Affairs, did not confirm any direct actions but emphasized the government's concern over "excessive and abnormal FX fluctuations driven by speculation." He just reiterated Japan's readiness to "take appropriate measures as necessary."

From our perspective, the scale of today's Yen movement suggests it was more likely driven by traders locking in profits from their USD/JPY long positions after the pair hit 160 mark, rather than direct government intervention. After all, Confirmation of any official intervention will likely need to wait until the release of official data at the end of May.

In the broader currency market, New Zealand Dollar and Australian Dollar also show strength, following Yen's lead. Conversely, Dollar is the weakest performer, followed by Canadian and Euro, with British Pound and Swiss Franc holding middle ground.

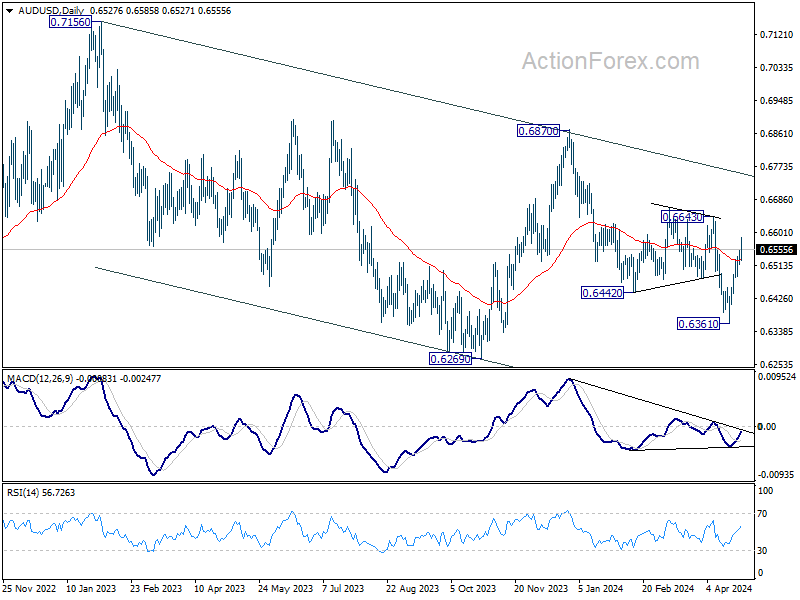

Looking ahead to the upcoming Asian session, Australian Dollar will be in the spotlight with the release of local retail sales data and China's PMI figures. Technically, AUD/USD's fall from 0.6870 could have completed with three waves down to 0.6361. Further rise is now in favor to 0.6643 resistance first. Decisive break there will strengthen this bullish case and target 0.6870 next. Nevertheless, sustained trading below 55 D EMA will neutralize the near term bullishness and mix up the outlook.

In Europe, at the time of writing, FTSE is up 0.37%. DAX is flat. CAC is up 0.12%. UK 10-year yield is down -0.0284 at 4.298. Germany 10-year yield is down -0.052 at 2.527. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.54%. China Shanghai SSE rose 0.79%. Singapore Strait Times rose 0.06%.

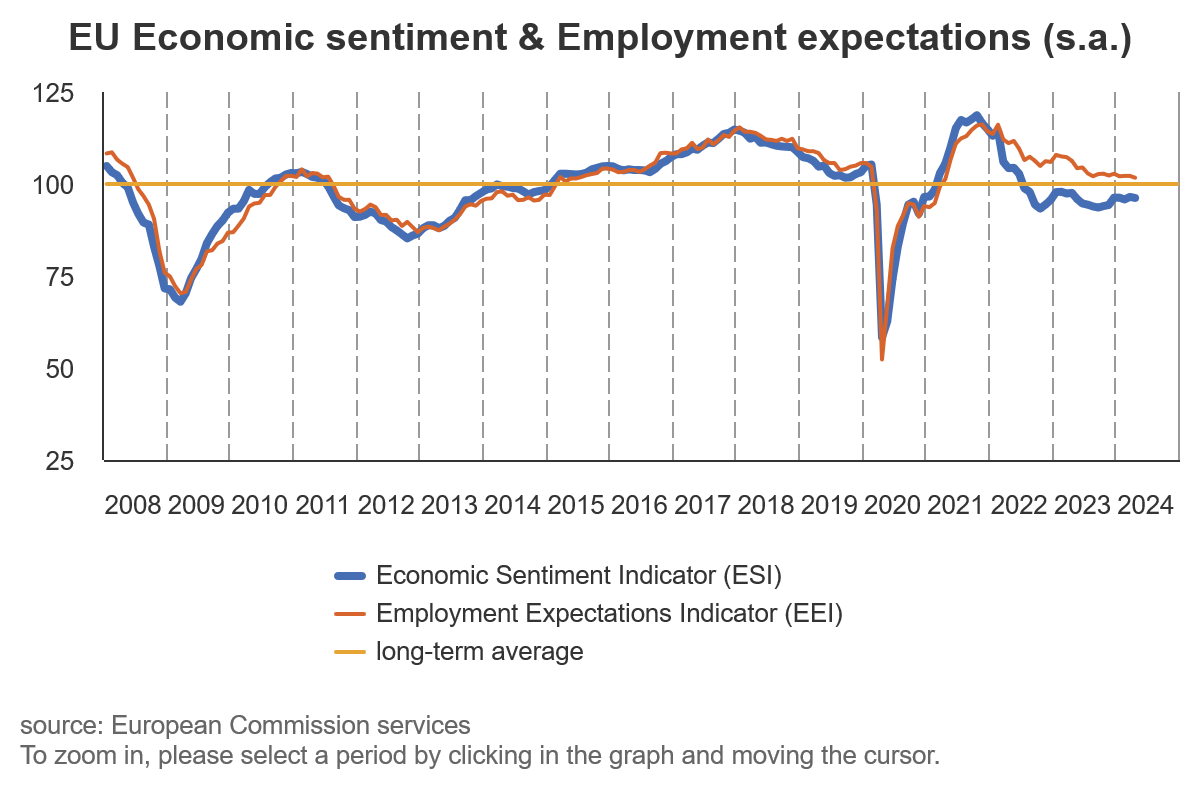

Eurozone economic sentiment falls to 95.6, EU down to 96.2

Eurozone Economic Sentiment Indicator fell from 96.2 to 95.6 in April, below expectation of 96.9. Employment Expectations Indicator fell from 102.5 to 101.8. Economic Uncertainty Indicator fell from 19.3 to 18.8.

Eurozone industry confidence fell from -8.9 to -10.5. Services confidence fell from 6.4 to 6.0. Consumer confidence improved slightly from -14.9 to -14.7. Retail trade confidence fell from -6.0 to -6.8. Construction confidence fell from -5.6 to -6.0.

EU Economic Sentiment Indicator fell from 96.5 to 96.2. Employment Expectations Indicator fell from 102.2 to 101.7. Economic Uncertainty Indicator fell from 18.8 to 18.1.

For the largest EU economies, the ESI deteriorated significantly in France (-4.8) and more moderately in Italy (-1.3), while it improved markedly in Spain (+2.3), Germany (+1.5) and Poland (+1.5). The ESI remained broadly stable in the Netherlands (+0.3).

ECB's Wunsch: Successive rate cuts in Jun and Jul could trigger excessive repricing

ECB Governing Council member Pierre Wunsch expressed today that he is "very comfortable" with rate cut in June. He also anticipates that at least two rates cuts this year, "barring any bad news".

However, Wunsch was careful to temper expectations regarding the pace of future rate cuts, particularly stressing that a reduction in rates in July, following a potential June cut, is "not a done deal".

He highlighted the importance of "managing expectations," noting that too rapid a sequence of rate reductions could lead the markets to anticipate cuts at every ECB meeting. Such a perception could trigger an excessive repricing in the markets, which Wunsch views as problematic.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.06; (P) 157.26; (R1) 159.53; More...

Intraday bias in USD/JPY remains neutral at this point as consolidation from 160.20 short term top is extending. Strong support could be seen from 38.2% retracement of 146.47 to 160.20 at 154.95 to bring recovery. But break of 160.20 is not envisaged for now. However, firm break of 154.95 will turn bias to the downside for deeper correction to 55 D EMA (now at 151.83).

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 100% projection of 127.20 to 151.89 from 140.25 at 164.94. Outlook will remain bullish as long as 150.87 resistance turned support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Apr | 95.6 | 96.9 | 96.3 | 96.2 |

| 09:00 | EUR | Eurozone Industrial Confidence Apr | -10.5 | -8.5 | -8.8 | -8.9 |

| 09:00 | EUR | Eurozone Services Sentiment Apr | 6 | 6.5 | 6.3 | 6.4 |

| 09:00 | EUR | Eurozone Consumer Confidence Apr F | -14.7 | -14.7 | -14.7 | |

| 12:00 | EUR | Germany CPI M/M Apr P | 0.50% | 0.60% | 0.40% | |

| 12:00 | EUR | Germany CPI Y/Y Apr P | 2.20% | 2.30% | 2.20% |

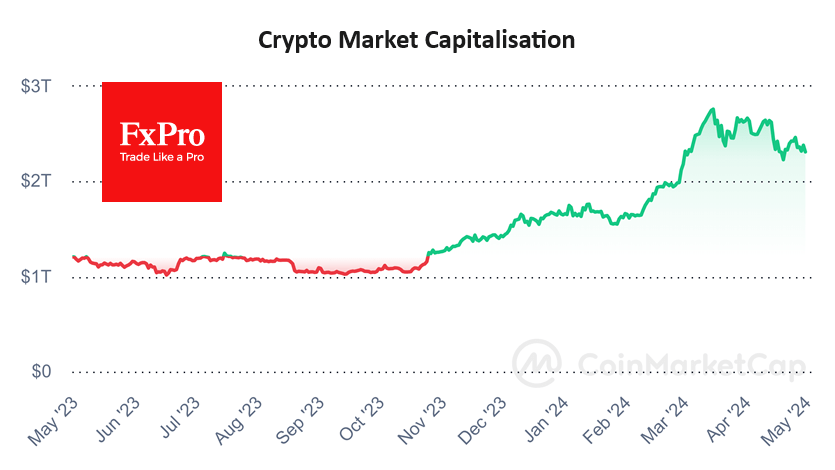

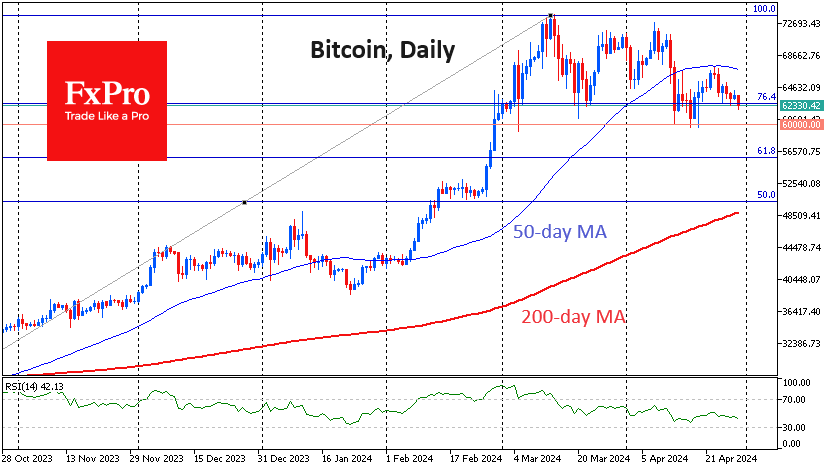

Crypto Market Retreats Due to Overhang of Sellers

Market picture

The crypto market has lost 3.3% in the last 24 hours to $2.3 trillion. The last time this level of capitalisation was on 19th April. Most worrying is the reversal of the trend from up to down last Wednesday. If the market easily pulls back below the previous local lows ($2.2 trillion), the downtrend in the market will be confirmed.

Bitcoin is developing its retreat after failing to climb above the 50-day moving average last Tuesday. With the current price near $62.2K, the first cryptocurrency is trading at the lower end of its trading range, setting up for another test of $60K.

The ability to attract new buyers, as it has since early March, will revitalise the entire crypto market. However, it is more likely that there is a high overhang of selling right now, including miner stocks. From the perspective of 1-2 weeks, we see more chance of a dip into $52-55K than staying above $60K.

News background

According to Watcher Guru, BNY Mellon Bank has officially notified the US SEC about its investments in the spot bitcoin-ETF market.

Former Ethereum team advisor Steven Nerayoff said ETH had been secure since the Initial Coin Offering (ICO) and accused the network’s co-founders of fraud.

The UK’s National Crime Agency and police have been given powers to ‘seize, freeze and destroy’ cryptocurrency used by criminals.

According to CoinShares, institutional investors have significantly increased their investments in altcoins, and one of the beneficiaries is Solana. Altcoin market capitalisation is poised to reach new records, and in general, a ‘cryptocurrency summer’ is coming, according to Real Vision CEO Raul Pal.

‘95 per cent of blockchains are just junk’, said DFINITY president Dominic Williams. He noted the usefulness of the Bitcoin, Ethereum, Solana, and Avalanche blockchains. He called the Internet Computer Protocol (ICP) ‘the only third-generation network’ that could create a new on-chain era of online interactions.

US payment service Stripe announced the resumption of cryptocurrency transactions after a six-year hiatus.

Japanese Yen Shows Volatility Amid Speculation of Intervention

The USD/JPY pair is hovering around 155.00 on Monday, having earlier touched a new 34-year peak at 160.00. Market rumours suggest that the Japanese authorities might have intervened in the currency market, although there has been no official confirmation. Today's market movement is particularly notable due to a public holiday in Japan, which has resulted in minimal market liquidity. This scenario made it relatively easy for investors to prompt significant changes in the quotes.

Last week, the Bank of Japan (BoJ) maintained its monetary policy foundation, keeping the interest rate steady at 0-0.1% per annum. Market participants were left disappointed, as they had anticipated a more pronounced reaction from the BoJ.

The primary driver of the yen's ongoing weakness is the significant discrepancy between the interest rates set by the BoJ and the US Federal Reserve. This interest rate gap exerts substantial pressure on the yen, making any actual intervention largely ineffective. The BoJ, aware of this reality, has thus far limited its actions to verbal interventions to influence the yen's value.

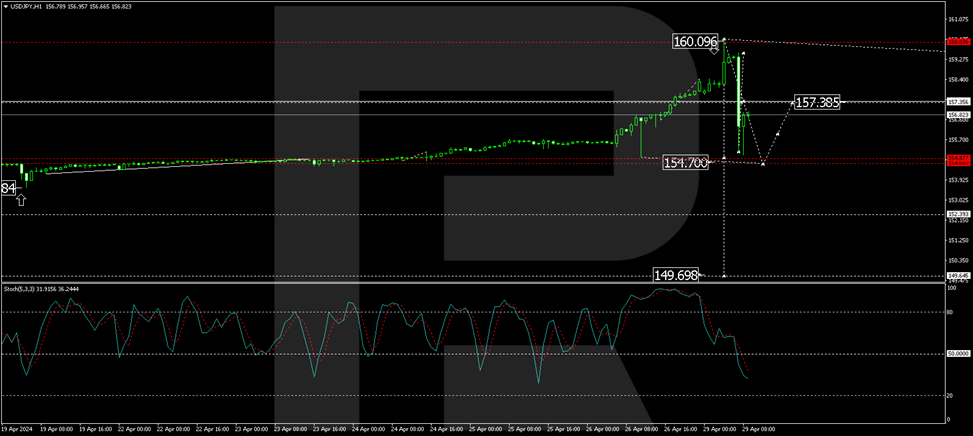

Technical analysis of USD/JPY

On the H4 chart of USD/JPY, a growth wave reaching the level of 160.16 was realised. The structure of the first impulse of decline to 154.70 is currently forming. Once this level is reached, a correction to 157.35 (testing from below) is anticipated, potentially followed by a new wave of decline towards 152.32, with the prospect of continuing the trend to 149.65. This scenario is technically supported by the MACD oscillator, which is positioned above zero at the highs but is expected to decline to new lows.

On the H1 chart, the upward growth wave to 160.16 has been completed. We are now observing the formation of the first impulse of the decline wave. The local target of this downside impulse at 155.15 has been achieved. We anticipate a corrective move to 157.35 (testing from below). Subsequently, the next phase of the downward trend to 154.65 is expected, which is the primary target. After completing this, a correction back to 157.35 may be considered. The Stochastic oscillator confirms this bearish outlook, with its signal line below 50 and pointing strictly downwards.

Eurozone economic sentiment falls to 95.6, EU down to 96.2

Eurozone Economic Sentiment Indicator fell from 96.2 to 95.6 in April, below expectation of 96.9. Employment Expectations Indicator fell from 102.5 to 101.8. Economic Uncertainty Indicator fell from 19.3 to 18.8.

Eurozone industry confidence fell from -8.9 to -10.5. Services confidence fell from 6.4 to 6.0. Consumer confidence improved slightly from -14.9 to -14.7. Retail trade confidence fell from -6.0 to -6.8. Construction confidence fell from -5.6 to -6.0.

EU Economic Sentiment Indicator fell from 96.5 to 96.2. Employment Expectations Indicator fell from 102.2 to 101.7. Economic Uncertainty Indicator fell from 18.8 to 18.1.

For the largest EU economies, the ESI deteriorated significantly in France (-4.8) and more moderately in Italy (-1.3), while it improved markedly in Spain (+2.3), Germany (+1.5) and Poland (+1.5). The ESI remained broadly stable in the Netherlands (+0.3).