Sample Category Title

Forex and Cryptocurrency Forecast

EUR/USD: The Dollar Soars

Last week saw two significant events: the first shocked market participants, while the second passed without surprises. Let's examine the details in order.

Since mid-2022, consumer prices in the US have been declining. In July 2022, the Consumer Price Index (CPI) was at 9.1%, but by July 2023, it had fallen to 3.0%. However, in October, the CPI rose to 3.7%, then decreased again, and by February 2024, it had dropped to 3.2%. As a result, there was a general perception that inflation had finally been brought under control. The market consensus was that the Federal Reserve would soon begin to ease its monetary policy and start reducing interest rates in June. Two weeks ago, the likelihood of this move was estimated at 70%. The DXY index began to fall, reaching a local low of 103.94 on 9 April. However, the dollar bears' joy was short-lived, as fresh US inflation data released on Wednesday, 10 April, quickly changed the sentiment.

In annual terms, the Consumer Price Index (CPI) rose to 3.5%, marking the highest level in six months. The main drivers of this inflation increase were the rises in rental costs (5.7%) and transportation expenses (10.7%), which clearly caught the markets by surprise. The chances of a rate cut in June plummeted to zero, and the DXY dollar index soared, reaching a peak of 105.23 on the evening of 10 April. Alongside this, the yield on 10-year US Treasury bonds grew to 4.5%. As is typical in such scenarios, stock indices such as the S&P 500, Dow Jones, and Nasdaq declined, and the EUR/USD pair, after dropping over 150 points, fell to 1.0728.

Austan Goolsbee, President of the Chicago Federal Reserve Bank, stated that although the regulator is confidently moving towards its 2.0% inflation target, the Federal Reserve leadership still has much work to do to reduce inflation. His colleague, John Williams, President of the New York Fed, noted that the latest inflation data were disappointing and added that economic prospects remain uncertain.

As a result of these and other statements, it is now forecasted that the Fed will begin cutting interest rates only in September. Moreover, investors expect there will be only two rate cuts this year, not three. Some believe that there may not be any rate cuts at all in 2024. However, according to US President Joe Biden, the Fed should still lower the rate in the second half of this year. His insistent request is quite understandable on the eve of the presidential elections. Firstly, it would reduce the cost of servicing the country's enormous national debt, and secondly, it would symbolize a victory over inflation, giving Biden several additional points in the battle for the White House.

After the American inflation reaction, markets took a brief pause, awaiting the European Central Bank (ECB) governing council meeting on 11 April. The ECB has held rates steady at 4.50% since September 2023, which was in line with market expectations as forecasted by all 77 economists surveyed by Reuters. Thus, after some fluctuation, EUR/USD returned to its pre-ECB meeting level.

The ECB press release affirmed the council's firm intention to return inflation to a medium-term target of 2.0% and believed that the key rates contribute significantly to the ongoing disinflation process. Future decisions will ensure that the key rates remain at sufficiently restrictive levels as long as necessary.

It's worth noting that inflation in the 20 Eurozone countries was at 2.4% in March, slightly above the target of 2.0%. In February, the rate was 2.6%, and in January it was 2.8%. Economists surveyed by Reuters believe that inflation will continue to decrease in the coming quarters, but it will not reach 2.0% before the second quarter of 2025.

Christine Lagarde, the head of the European Central Bank (ECB), expressed a similar view during a press conference. However, she mentioned that since the Eurozone economy remains weak, to support it, the ECB will not wait for inflation to return to the 2.0% level at every point. Thus, Ms. Lagarde did not rule out that the regulator might start easing its monetary policy significantly before 2025. Strategists from the Italian bank UniCredit forecast that the ECB will cut rates three times this year, by 25 basis points each quarter. The pace of reduction could remain the same next year. Economists from Deutsche Bank also expect that the pan-European regulator will start cutting rates before the Federal Reserve and will do so at a faster pace. Consequently, the widening interest rate differential between the US and the Eurozone will contribute to the weakening of the euro.

This medium-term forecast was confirmed last Friday: EUR/USD continued its decline, reaching a local minimum of 1.0622 and closing the five-day period at 1.0640. The DXY index peaked at 106.04. As for the near-term outlook, as of the evening of 12 April, 40% of experts anticipate an upward correction of the pair, while the majority (60%) hold a neutral position. Among the oscillators on D1, only 15% are coloured green, and 85% are red, although a quarter of them are in the oversold zone. Trend indicators are 100% bearish. The nearest support levels for the pair are located in the zones 1.0600-1.0620, followed by 1.0495-1.0515, 1.0450, 1.0375, 1.0255, 1.0130, and 1.0000. Resistance zones are situated at levels 1.0680-1.0695, 1.0725, 1.0795-1.0800, 1.0865, 1.0895-1.0925, 1.0965-1.0980, 1.1015, 1.1050, 1.1100-1.1140.

Next week, on Monday, 15 April, US retail sales data will be released. On Wednesday, it will become clear what is happening with consumer inflation in the Eurozone. It is likely that the refined data will confirm the preliminary results, and the Consumer Price Index (CPI) for March will be reported at 2.4% year-on-year. On Thursday, we traditionally expect data on the number of initial jobless claims from US residents and the Philadelphia Fed Manufacturing Index.

GBP/USD: The Pound Plummets

On Friday, 12 February, the UK's GDP data indicated that the economy is on the path to recovery. Although production has declined compared to last year, the latest data suggests that exiting the shallow recession is quite likely. GDP has grown for the second consecutive month, with the Office for National Statistics (ONS) reporting a 0.1% increase in February on a monthly basis, with January's figures revised upwards to show a 0.3% growth from an earlier 0.2%.

Despite these figures, GBP/USD fell below the key 1.2500 mark due to crumbling hopes for an imminent Fed rate cut. Not even a statement from Bank of England (BoE) Monetary Policy Committee member Megan Greene, which highlighted that inflation risks in the UK remain significantly higher than in the US and that markets are mistaken in their rate cut forecasts, could change the situation. "Markets have leaned towards the Fed not cutting rates so soon. In my view, the UK will also not see rate cuts anytime soon," she wrote in her Financial Times column.

Following Greene's remarks, traders now expect no more than two rate cuts from the Bank of England this year, each by 25 basis points. However, this revised forecast did little to support the pound against the dollar, with GBP/USD ending the week at 1.2448.

Analysts are split on the short-term behaviour of GBP/USD: 50% voted for a rebound to the north, and 50% abstained from forecasting. Indicator readings on D1 suggest the following: among oscillators, 10% recommend buying, another 10% are neutral, and 80% indicate selling, with 20% of these signalling oversold conditions. All trend indicators are pointing downwards. If the pair continues south, it will encounter support levels at 1.2425, 1.2375-1.2390, 1.2185-1.2210, 1.2110, and 1.2035-1.2070. In the event of an increase, resistance will be found at levels 1.2515, 1.2575-1.2610, 1.2695-1.2710, 1.2755-1.2775, 1.2800-1.2820, 1.2880-1.2900, 1.2940, 1.3000, and 1.3140.

The most significant days for the British currency next week will be Tuesday and Wednesday. Extensive labor market data from the United Kingdom will be released on Tuesday, 16 April, along with a speech from the Governor of the Bank of England, Andrew Bailey. Wednesday, 17 April, could be even more turbulent and volatile as consumer inflation (CPI) data for the country will be published.

USD/JPY: Is 300.00 Just a Matter of Time?

Bears on USD/JPY continue to hope for its reversal southwards, yet the pair does not stop climbing. Our previous review titled "A Break Above 152.00 – A Matter of Time?" proved true within a very short period. Last week, the pair reached a 34-year high of 153.37, propelled by US inflation reports and increases in the DXY index and yields on 10-year US treasuries. (Considering that it traded above 300.00 in 1974, this is still not the limit).

This surge occurred despite another round of verbal interventions from high-ranking Japanese officials. Finance Minister Suzuki Shunichi reiterated his concern over excessive currency movements and did not rule out any options to combat them. Cabinet Secretary Yoshimasa Hayashi echoed these sentiments almost verbatim. However, the national currency no longer pays any attention to such statements. Only real currency interventions and significant steps towards tightening monetary policy by the Bank of Japan (BoJ) could help, but these have yet to occur.

Analysts at Dutch Rabobank believe the Japanese Ministry of Finance will eventually be forced to act to prevent the price from reaching 155.00. "While a breakthrough of the 152.00 level by USD/JPY might not immediately trigger currency interventions, we see a significant likelihood of such a step," they write. "Assuming that the Bank of Japan may announce a second rate hike later this year and considering expectations that the Fed will indeed cut rates in 2024, Rabobank expects USD/JPY to trade around 150.00 on a monthly horizon and 148.00 on a 3-month horizon.".

Last week, the pair closed at 152.26. Regarding its near future, 25% of experts sided with the bears, another 25% remained neutral, and the remaining 50% voted for further strengthening of the US currency and a rise in the pair. Technical analysis tools are apparently unaware of the fears regarding possible currency interventions, so all 100% of trend indicators and oscillators on D1 are pointing north, with a quarter of them now in the overbought zone. The nearest support level is around 152.75, followed by 151.55-151.75, 150.80-151.15, 149.70-150.00, 148.40, 147.30-147.60, and 146.50. Defining resistance levels after the pair updated 34-year highs is challenging. The nearest resistance lies in the zone 153.40-153.50, followed by levels 154.40 and 156.25. According to some analysts, the monthly high of June 1990 at around 155.80 and then the reversal high of April 1990 at 160.30 can also serve as references.

No significant events or publications regarding the state of the Japanese economy are planned for the upcoming week.

CRYPTOCURRENCIES: On the Eve of Hour X

The next halving, when the reward for mining a BTC block will again be halved, is scheduled for Saturday, 20 April. Although this date is approximate and may shift a day or two either way, the closer the Hour X, the hotter the discussions about how the price of the main cryptocurrency will behave before and after this event.

Historically, the value of bitcoin has risen after halvings: it surged by nearly 9000% to $1162 in 2012, by about 4200% to $19800 in 2016, and by 683% to $69000 following the previous halving in May 2020. However, it then crashed to nearly $16,000.

Lucas Kiely, CIO of the financial platform Yield App, believes that we should not expect a seven-fold increase in the price of bitcoin after the upcoming halving. According to Kiely, during the three previous cycles, the halving of miners' rewards heralded a massive increase in volatility levels. After the halving, BTC fell by 30-40% but then soared to unprecedented heights within 480 days. However, this year, he suspects, the cryptocurrency's flight to the Moon will not occur.

Kiely predicts that bitcoin will update its historical maximum reached this March at $73,743. However, the new peak will not exceed the previous one by as much as before, due to the low level of volatility. The specialist attributes the drop in volatility to two factors: 1. an increase in the number of bitcoins in the wallets of hodlers, who own more than 70% of the issued coins, and 2. the creation of spot Bitcoin ETFs, which remove a huge amount of coins from circulation. (In the three months since their inception, the capitalization of 10 such ETFs (excluding the Grayscale fund) has exceeded $12 billion). As a result, bitcoin is becoming a more traditional asset that is less risky but also less likely to yield massive profits. Kiely believes that this factor makes the coin more attractive to institutional investors and older people who prefer to invest in reliable assets and are not interested in gambling.

Ex-CEO of the BitMEX exchange, Arthur Hayes, expects a price drop. In his view, the halving is certainly a bullish catalyst for the crypto market in the medium term. However, prices might fall immediately before and after the event. "The narrative that the halving of block rewards will positively affect cryptocurrency prices has firmly taken root," says the expert. "However, when most market participants agree on a certain outcome, the opposite usually happens."

Hayes noted that the market would face a reduction in US dollar liquidity in the second half of April, driven by tax season, Fed policies, and the strengthening of the US Treasury's balance sheet. This reduction in liquidity will provide additional stimulus for a "furious sell-off of cryptocurrencies," he believes. "Can the market defy my bearish forecasts and continue to grow? I hope so. I have been involved with cryptocurrency for a long time, so I welcome being proven wrong."

The situation before this halving is indeed very different from before. This change is linked to the large influx of institutional investors through the newly launched Bitcoin ETFs in early January. The influence of ETFs on spot trading is clearly reflected in the reduced market activity on weekends and US public holidays when the exchange funds do not operate. The tax season has also significantly impacted the market for risky assets. Over the last two weeks, inflows into these funds have been significantly below the average mark of $203 million, with recent days seeing an outflow of funds from Grayscale and Ark Invest. Other ETFs are also reporting reduced inflows. All this suggests that Arthur Hayes' concerns are well-founded, and a 30% drop from the current price could send bitcoin down to around $50,000.

Miners, who will lose half their income after the halving, while the costs of obtaining the same amount of coins will increase, could also contribute to a market crash. After the halving in May 2020, the costs of mining rose to $30,000. Currently, the average cost of mining one BTC is $49,900, but after 20 April, according to Ki Young Ju, CEO of the analytical platform CryptoQuant, it will exceed $80,000. Therefore, the asset must trade above this level for miners to continue making any profit. However, as previously mentioned, a rapid price surge may not occur. This means that small mining companies and individual miners are facing a wave of bankruptcies and acquisitions.

According to Arthur Hayes, the situation might improve in May-June: the US Treasury will "most likely release an additional $1 trillion of liquidity into the system, which will pump the markets," he says. Anthony Scaramucci, CEO of Skybridge, also holds that spot Bitcoin ETFs, acting as "selling machines," will continue to stimulate demand for the first cryptocurrency from both retail customers and institutional investors. Scaramucci believes that in this cycle, bitcoin's value could increase by 2.5 times, and then continue to rise. "I'm just saying that the capitalization of bitcoin could reach half that of gold, i.e., increase six or even eight times from its current levels," the businessman declared. It's noteworthy that the current capitalization of bitcoin stands at $1.35 trillion, while gold's is at $15.8 trillion. Thus, if BTC reaches half the capitalization of the precious metal, its price would be around $400,000 per coin.

Brad Garlinghouse, CEO of Ripple, also places his hopes on spot Bitcoin ETFs. According to him, BTC-ETFs have attracted real institutional investments into the industry for the first time, so he is "very optimistic" about the macroeconomic trends in the crypto industry. In this context, Garlinghouse allowed that the market capitalization of digital assets could double by the end of the year, exceeding $5.0 trillion.

As of the evening of Friday, 12 April, BTC/USD is trading at around $66,900. The total capitalization of the crypto market is $2.44 trillion ($2.53 trillion a week ago). The Crypto Fear and Greed Index remains in the Extreme Greed zone at 79 points.

In conclusion, a bit of curious statistics: In anticipation of the halving, Deutsche Bank conducted a survey regarding the future price of bitcoin. 15% of respondents stated that within this year, BTC would trade in the range above $40,000 but below $75,000. A third of respondents were confident that the value of the main cryptocurrency would fall below $20,000 early in the next year. Meanwhile, 38% of those surveyed believed that BTC would cease to exist in the market altogether. And finally, about 1% of respondents called bitcoin a complete misunderstanding and speculation.

Bets on June Fed Rate Cut Abandoned, Dollar Asserts Dominance

The financial markets were jolted last week by data confirming the stall in disinflation progress in the US. This development prompted traders to quickly revise their expectations regarding Fed's monetary policy, withdrawing bets on a June rate reduction. This shift in sentiment led to strong rise in treasury yields and corresponding deep decline in stock markets, reflecting heightened investor caution and risk aversion.

In the currency markets, Dollar was the primary beneficiary of these shifts, as it capitalized on the confluence set bullish factors including Fed rate expectations, rally in treasury yields, and a broad movement toward risk aversion. These factors collectively propelled Dollar to finish the week as the runaway winner.

There is ample room for last week's movements in the stocks, bonds, and Dollar to continue. Recent bull runs in industrial metals and oil prices are likely the make the last mile of disinflation even harder. Increasing geopolitical tensions in the Middle East is another wild card that could further sink market sentiments.

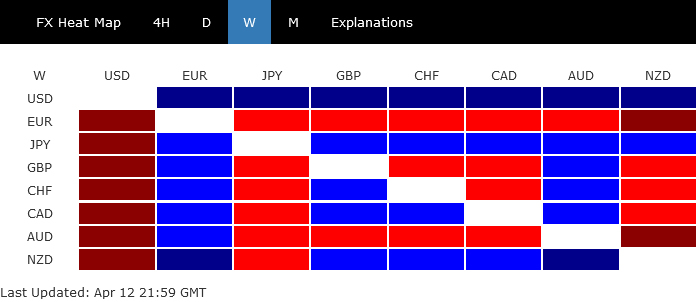

In the broader currency markets, Euro ended the week as the weakest performer, as it encountered additional downward pressure due to late selloff against Swiss Franc and Sterling. The Australian Dollar also struggled, ranking as the second weakest currency, dragged down by its underperformance against other commodity-linked currencies.

Persistent Inflation Adjusts Fed Rate Cut Expectations, Shaking US Stock Markets

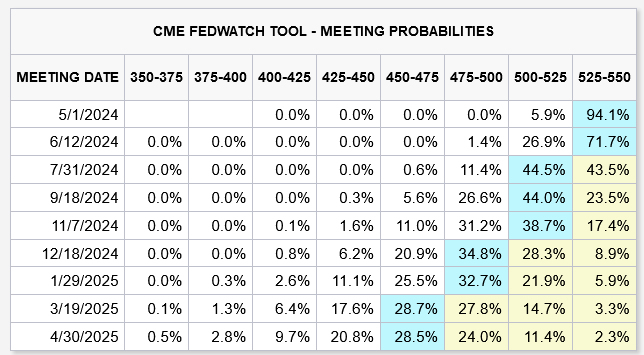

The markets seemed to have abandoned hope for a June rate cut by Fed after stronger than expected March US CPI data. Core CPI unchanged from February's reading at 3.8%. More importantly, it was down just marginally from 4.1% six months ago. The decline in core inflation has been very gradual, and clearly, the path to 2% inflation is not assured.

Fed fund futures now reflect a recalibrated outlook, with the probability of a rate cut in September falling to 76.5%. The prospects for more aggressive monetary easing within the year have also diminished, evidenced by only a 62.8% chance of a cumulative 50 basis points cut by year's end. This more conservative forecast suggests that while the market still largely anticipates one rate cut from Fed in 2024, the possibility of a second cut is now viewed with greater skepticism.

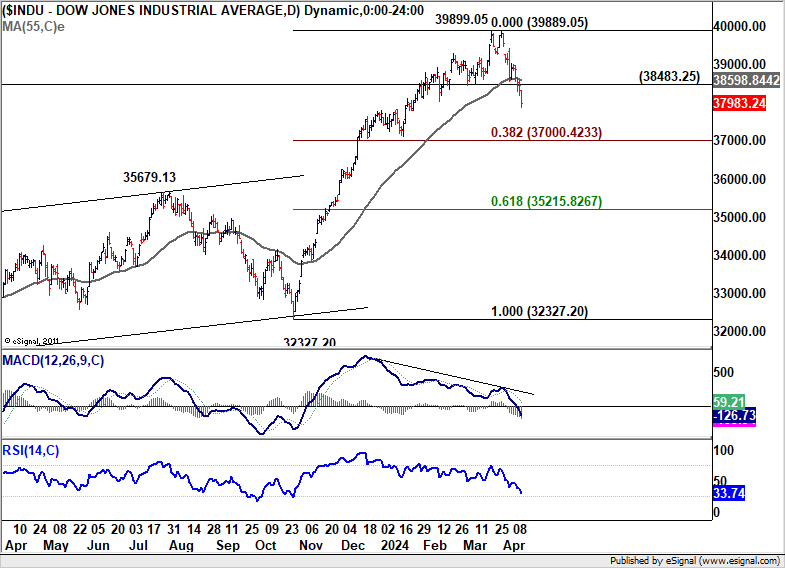

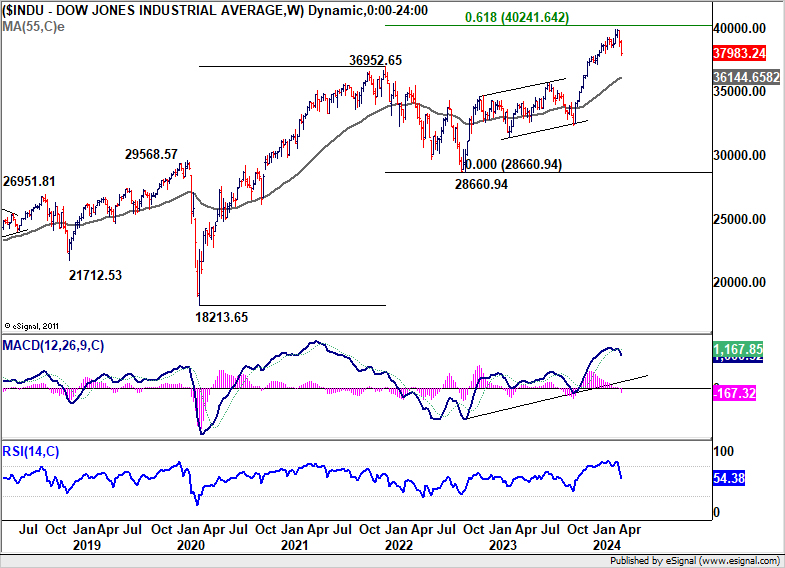

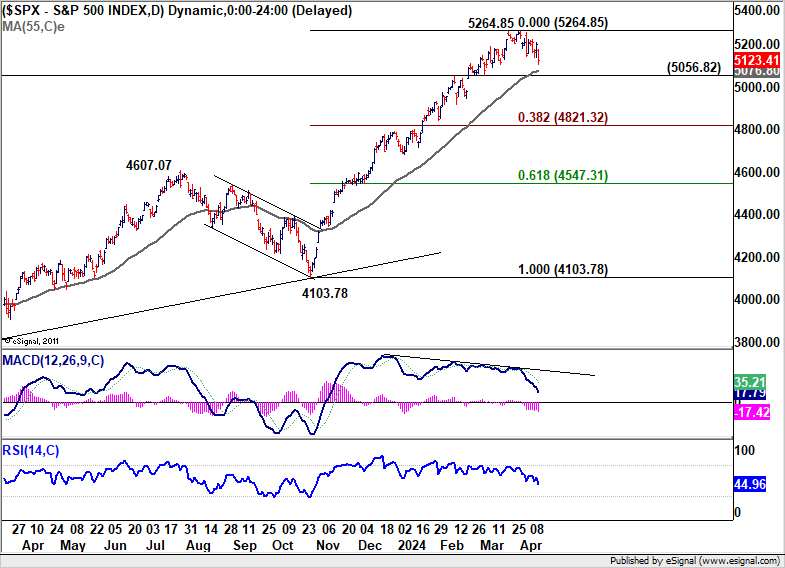

The market's reaction to these adjusted expectations was stark, particularly in the equity sectors. Dow Jones Industrial Average bore the brunt of the downturn, plunging by -2.37% over the week. Similarly, S&P 500 and NASDAQ declined -1.56% and -0.45%, respectively.

Technically, DOW's fall from 39889.05 is now seen as a correction to the rally from 32327.20. Deeper fall should be seen to 38.2% retracement of 32327.20 to 39899.05 at 37000.42. Strong support is expected there, at least on first attempt, to bring rebound. Meanwhile, firm break of 55 D EMA (now at 38598.84) will argue that the range of the corrective pattern could have been set already.

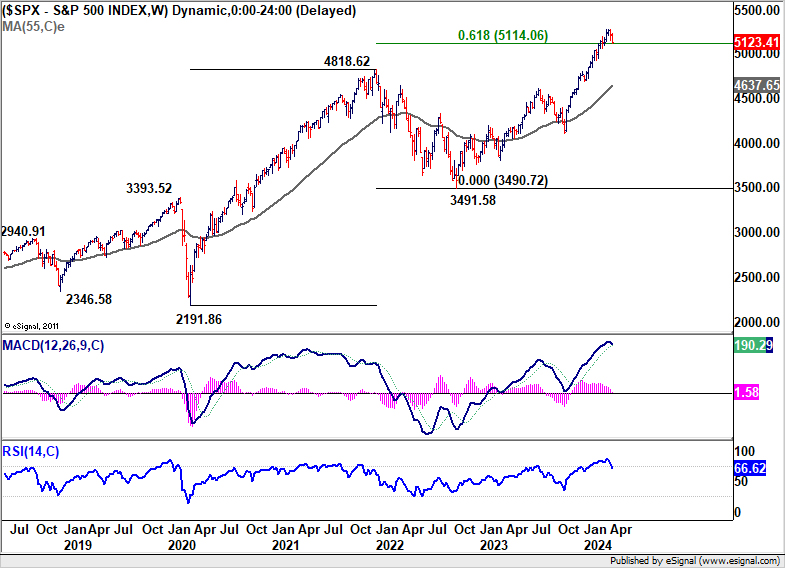

However, strong break of 37000.42 will put the second line of defense at 55 W EMA (now at 36144.65) in focus, and raise the chance of a larger correction to the up trend from 28660.94, which is currently seen as a less likely scenario.

S&P 500 has been relatively more resilient, but it's also starting to look vulnerable. Break of 5056.82 support and sustained trading below 55 D EMA (now at 5076.80) will align the outlook with DOW, and confirm each other's. In this case, deeper fall would be seen to 38.2% retracement of 4103.78 to 5264.85 at 4821.32.

Surge in 10-Year Yield and Dollar Index

10-year yield surged sharply too to close at 4.499 after reaching as high as 4.591. There is no change in the outlook that rebound from 3.780 is the second leg of the corrective pattern from 4.990 (2023 high). The stronger than expected rise reflected the shift in market expectations for a less aggressive Fed policy easing cycle.

For now, the focus is on whether 10-year yield could sustain above 61.8% retracement of 4.997 to 3.785 at 4.534. If it does, further rally would then be seen to retest 4.997, which could be in expectation that Fed might not cut interest rates this year. Meanwhile, break of 4.307 support will indicate that 10-year yield has topped, at least for the near term.

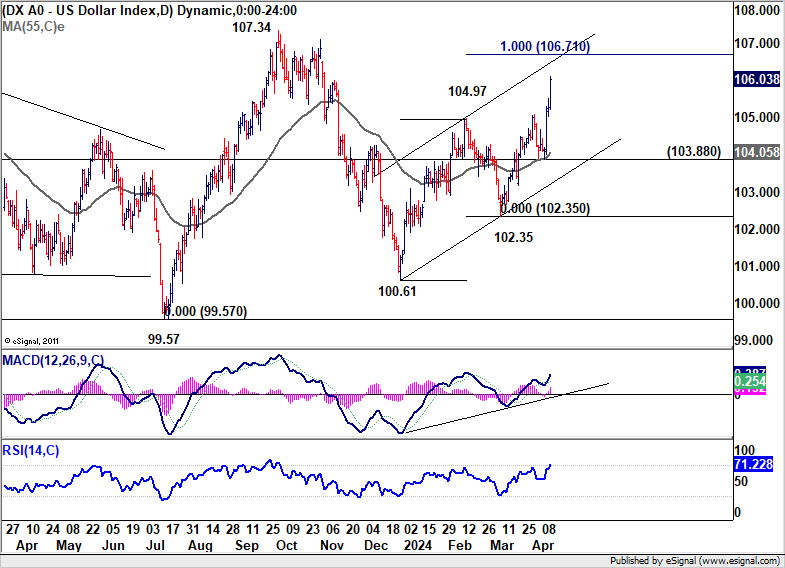

Dollar index's rally resumed after drawing support from 55 EMA and surged to close at 106.03. Current rise from 100.61 is in progress for 100% projection of 100.61 to 104.97 from 102.35 at 106.71.

Price actions from 99.57 is currently seen as a corrective pattern with rise from 100.61 as the third leg. Break of 107.34 resistance could be seen. But upside would likely be capped by 100% projection of 99.57 to 107.34 from 100.61 at 108.38.

Euro May Begin to Falter Against Sterling and Franc

Euro is starting to appear vulnerable against its European counterparts, Swiss Franc and more so Sterling, following ECB latest communications that hinted strongly at forthcoming rate cut.

To be specific ECB articulated that, "If the Governing Council's updated assessment of the inflation outlook, the dynamics of underlying inflation, and the strength of monetary policy transmission were to further increase its confidence that inflation is converging to the target in a sustained manner, it would be appropriate to reduce the current level of monetary policy restriction."

ECB President Christine Lagarde emphasized the significance of this new sentence in the post meeting press conference, describing it as a "loud and clear indication" of ECB's stance.

While the SNB has already initiated rate cut in March with another possibly on horizon in June, its policy rate at 1.50% offers related limited scope for further reductions compared to ECB's deposit rate at 4.00%. Meanwhile, expectations for BoE have been adjusted, with market bets scaling back to two rate cuts this year, starting in September.

Technically, with last week's steep pullback, EUR/CHF should have formed a short term top at 0.9847. Risk is mildly on the downside in the near term for 38.2% retracement of 0.9252 to 0.9847 at 0.9620. But strong support is expected from there to contain downside to bring rebound, and set the range for sideway trading.

EUR/CHF's rally from 0.9252 would be ready to resume once clarity is obtained regarding the terminal rates of ECB and SNB in their easing cycles, given the significant interest rate disparity that is likely to persist. Bearish trend reversal in EUR/CHF is not expected unless significant geopolitical risks materialize, prompting massive safe-haven flow into Franc.

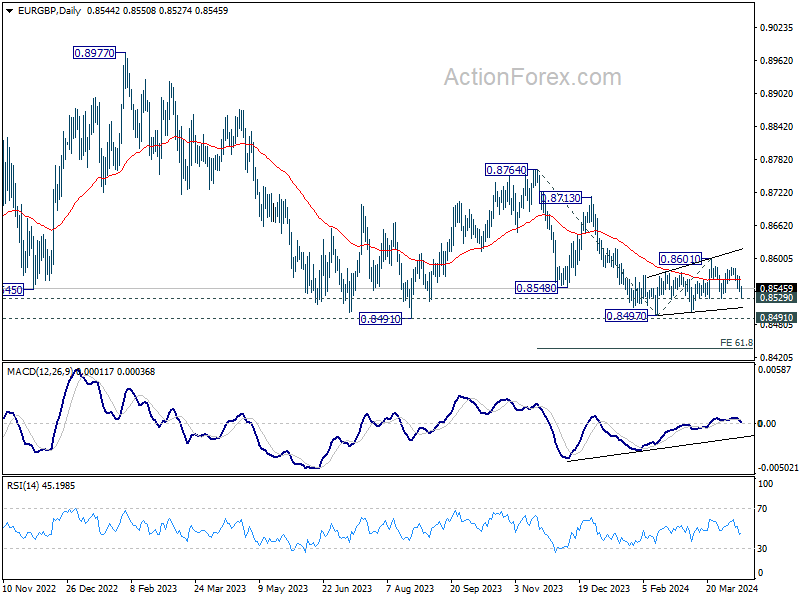

EUR/GBP might now be on the verge of resuming its medium term down trend. Break of 0.8529 support should prompt deeper decline through 0.8491/7 support zone. Next target will be 61.8% projection of 0.8764 to 0.8497 from 0.8601 at 0.8436. The downside breakout could be catalyzed by incoming data indicating that BoE is on track for only two rate cuts this year, or fewer.

Kiwi Leads Among Commodity Currencies, Aussie Lags

New Zealand Dollar ended as the stronger one among commodity currencies, bolstered by RBNZ's decisively hawkish stance. After leaving OCR unchanged at 5.50%, RBNZ expressed "limited tolerance" for delay in bringing down inflation to target band. This clear commitment to combating inflation has reinforced expectations that RBNZ might not be ready to cut interest rates this year yet.

Meanwhile, Canadian Dollar found some relief as BoC refrained from dropping any explicit hints about a rate cut in June, contrary to what some market participants had anticipated. Australian Dollar, meanwhile, showed less enthusiastic response to the extended rise in metal prices. Despite Aussie's recent rally seems to have exhausted its momentum, with increased risks of a downturn against its commodity currency counterparts.

Technically, AUD/NZD's decline last week, with D MACD firmly crossed below signal line, indicates short term topping at 1.0952. Further break of 1.0860 support should confirm rejection by medium term falling trend line resistance and target 55 D EMA (now at 1.0803). Sustained trading below this EMA will indicate that the sideway pattern from 1.1085 has already started another falling leg back towards 1.0567 support.

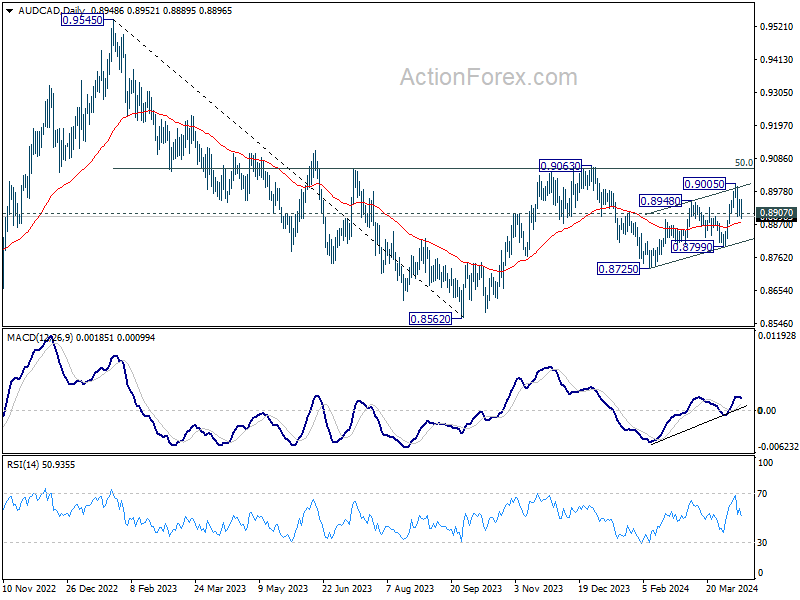

AUD/CAD's break of 0.8907 support argues that corrective rebound from 0.8725 might have completed with three waves up to 0.9005. Sustained trading below 55 D EMA (now at 0.8878) will solidify this bearish case. Deeper decline should then be seen through 0.8725 support to resume the fall from 0.9063.

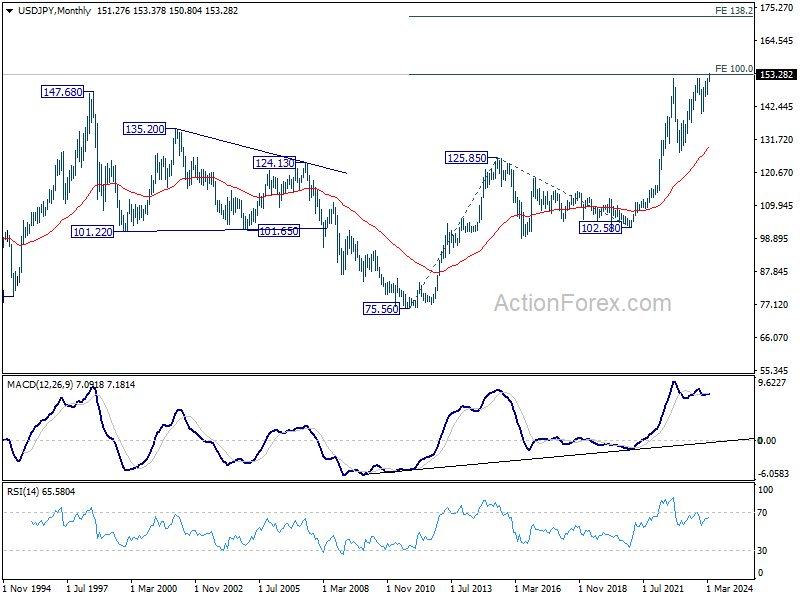

USD/JPY Weekly Outlook

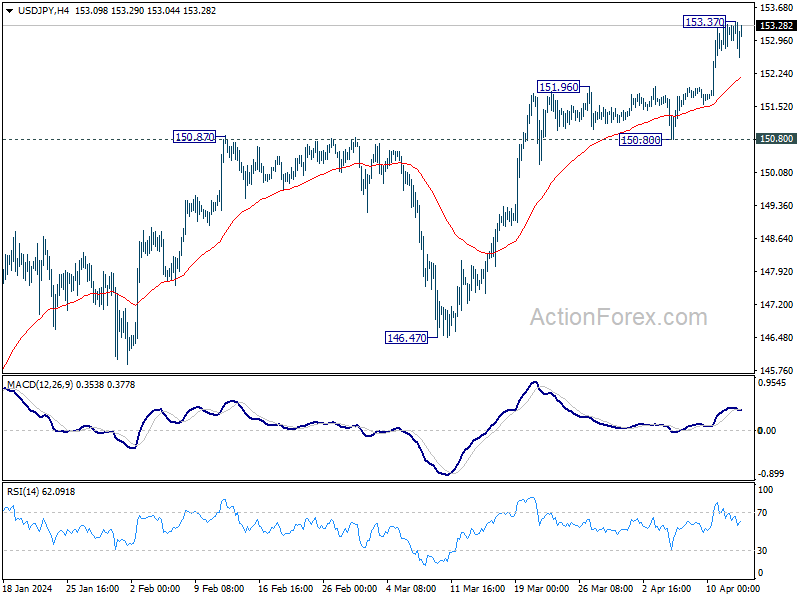

USD/JPY's up trend resumed last week by breaking through 151.93 resistance. But it retreated after hitting 153.37. Initial bias is neutral this week for some consolidations first. Outlook will stay bullish as long as 150.80 support holds. Above 153.37 will target 155.20 fibonacci projection level next.

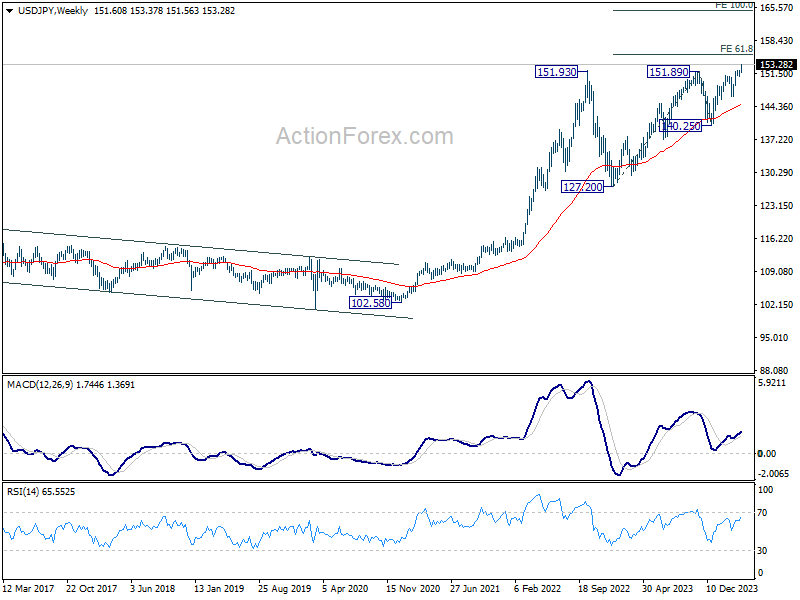

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. Outlook will now remain bullish as long as 146.47 support holds, even in case of deep pullback.

In the long term picture, as long as 127.20 support holds (2023 low), up trend from 75.56 (2011 low) is still in progress. Sustained trading above 100% projection of 75.56 (2011 low) to 125.85 (2015 high) from 102.58 at 152.87 will pave the way to 138.2% projection at 172.08. (This is a pure technical view without considering Japan's intervention.)

EUR/USD Weekly Outlook

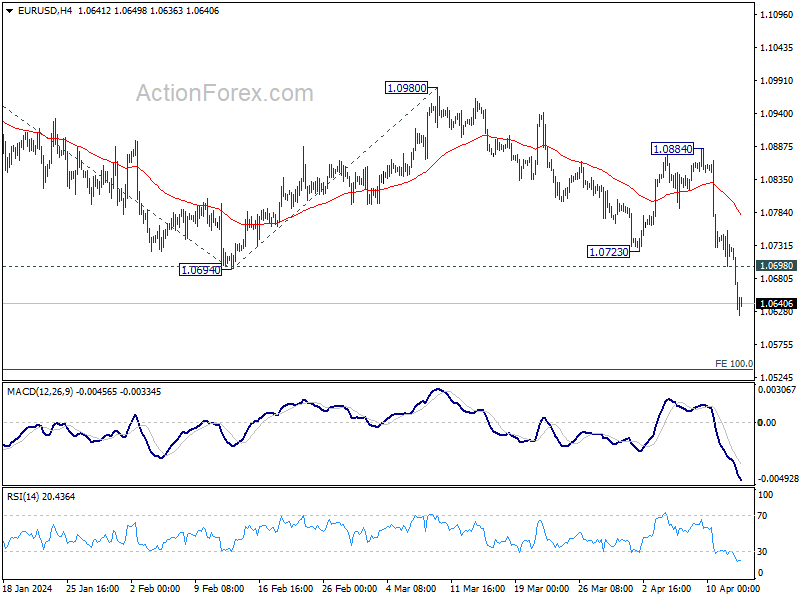

EUR/USD's fall from 1.1138 resumed by break through 1.0694 last week. Initial bias stays on the downside this week for 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next. Firm break there will target 1.0447 support next. On the upside, above 1.0698 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below, Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

In the long term picture, a long term bottom is in place at 0.9534 on bullish convergence condition in M MACD. It's still early to call for bullish trend reversal with the pair staying inside falling channel in the monthly chart. Nevertheless, sustained trading above 55 M EMA (now at 1.1050) and break of 1.1274 resistance will raise the chance of reversal and target 1.2348 resistance for confirmation.

USD/JPY Weekly Outlook

USD/JPY's up trend resumed last week by breaking through 151.93 resistance. But it retreated after hitting 153.37. Initial bias is neutral this week for some consolidations first. Outlook will stay bullish as long as 150.80 support holds. Above 153.37 will target 155.20 fibonacci projection level next.

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. Outlook will now remain bullish as long as 146.47 support holds, even in case of deep pullback.

In the long term picture, as long as 127.20 support holds (2023 low), up trend from 75.56 (2011 low) is still in progress. Sustained trading above 100% projection of 75.56 (2011 low) to 125.85 (2015 high) from 102.58 at 152.87 will pave the way to 138.2% projection at 172.08. (This is a pure technical view without considering Japan's intervention.)

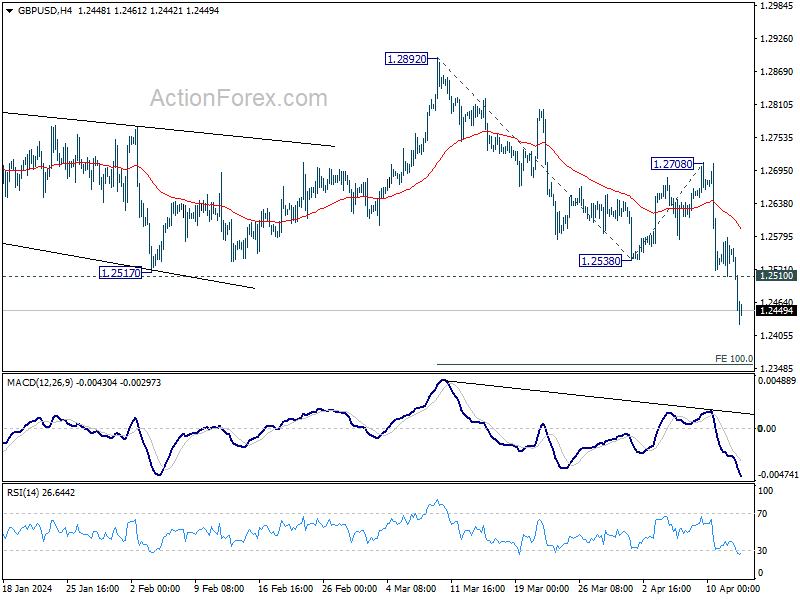

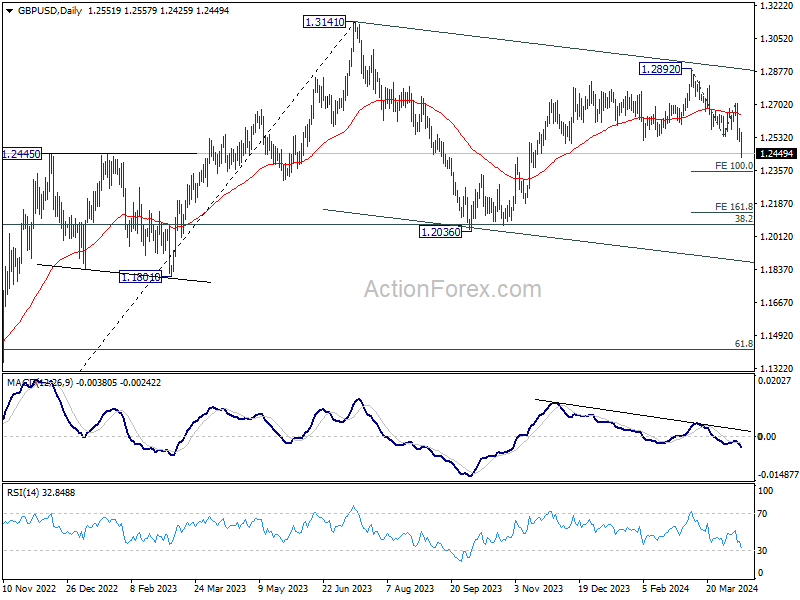

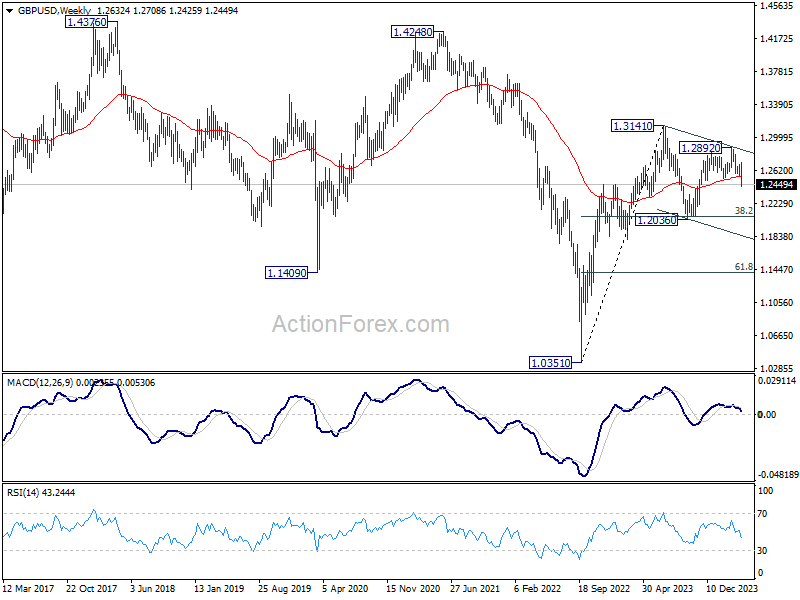

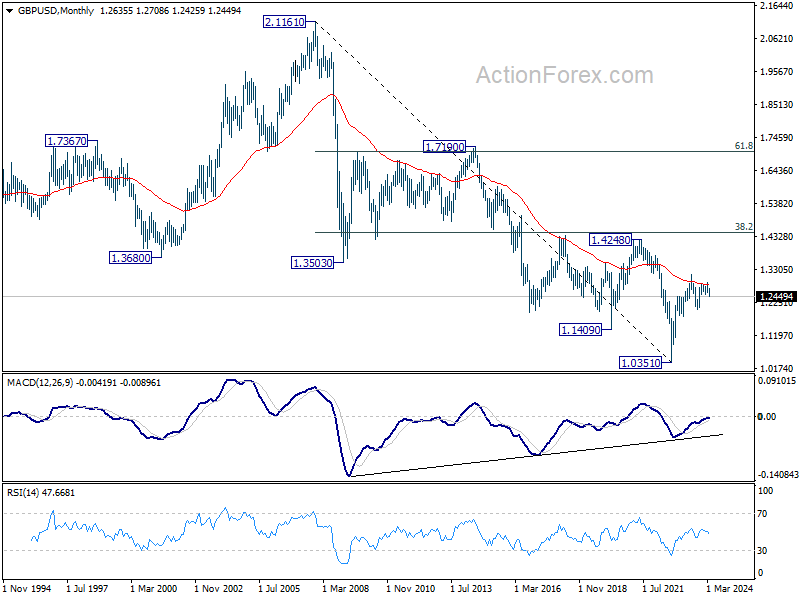

GBP/USD Weekly Outlook

GBP/USD's fall from 1.2892 resumed accelerated to as low as 1.2425 last week. Initial bias stays on the downside this week for 100% projection of 1.2892 to 1.2538 from 1.2708 at 1.2354. Firm break there will target 161.8% projection at 1.2207 next. On the upside, above 1.2510 minor resistance will turn bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

In the long term picture, a long term bottom should be in place at 1.0351 on bullish convergence condition in M MACD. But momentum of the rebound from 1.3051 argues GBP/USD is merely in consolidation, rather than trend reversal. Range trading is likely between 1.0351/4248 for some more time.

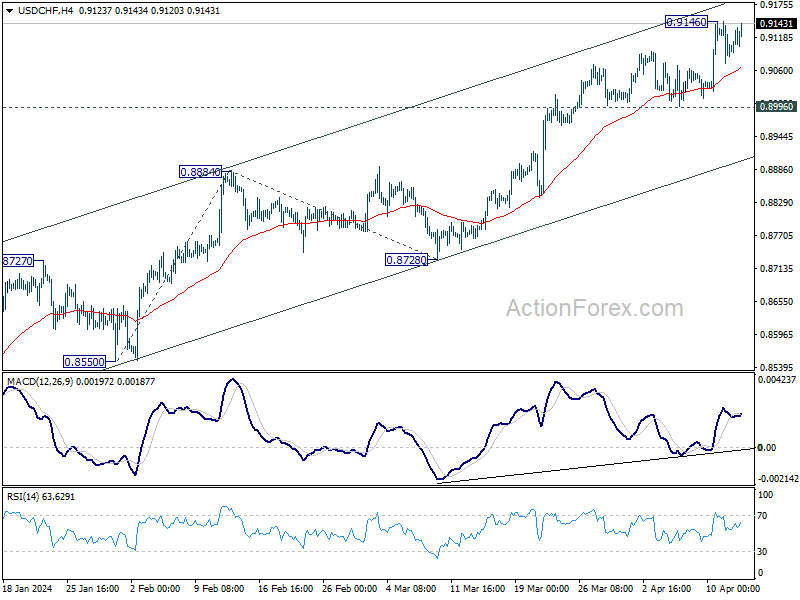

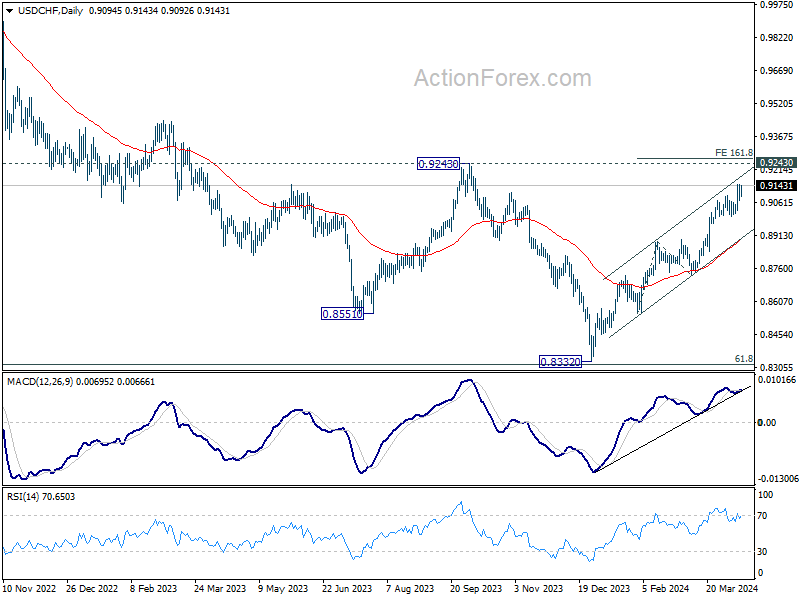

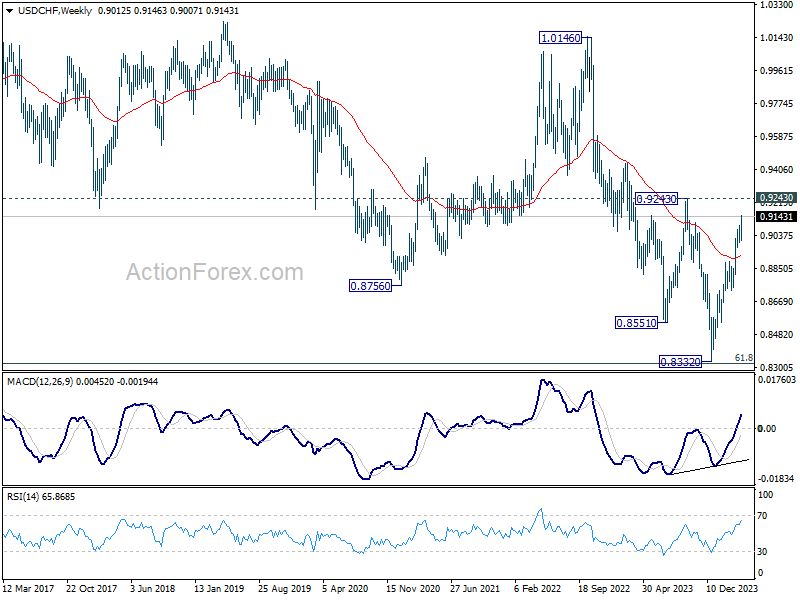

USD/CHF Weekly Outlook

USD/CHF's up trend from 0.8332 resumed last week but turn sideway again after hitting 0.9146. Initial bias remains neutral this week first. Further rally is expected as long as 0.8996 support holds. Above 0.9146 will target 161.8% projection of 0.8550 to 0.8884 from 0.8728 at 0.9268.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.

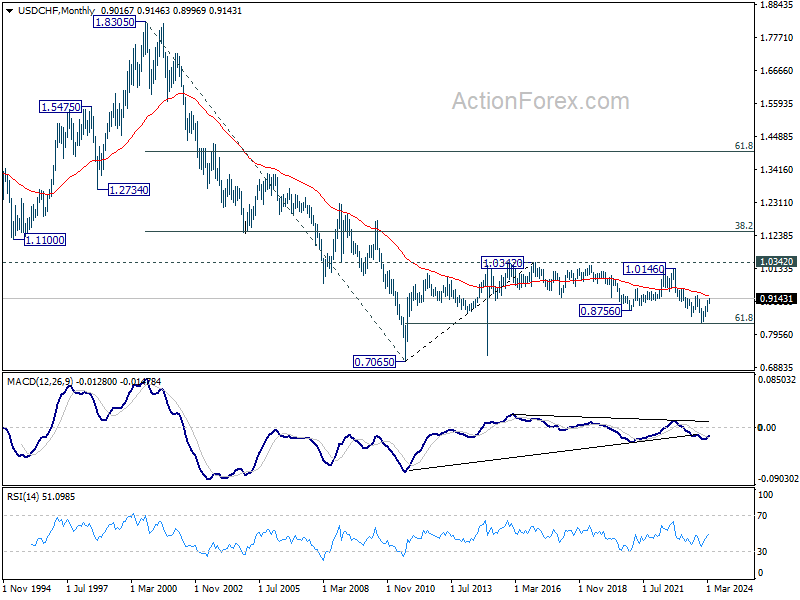

In the long term picture, price action from 0.7065 (2011 high) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). Strong rebound from 61.8% retracement of 0.7065 to 1.0342 (2016 high) will start the third leg as a medium term rally. But there will be no sign of long term reversal until firm break of 38.2% retracement of 1.8305 to 0.7065 at 1.1359.

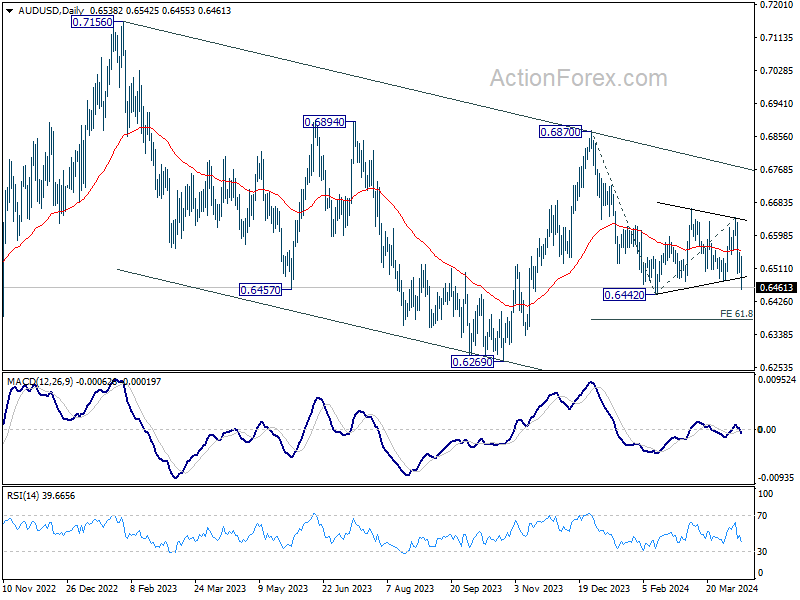

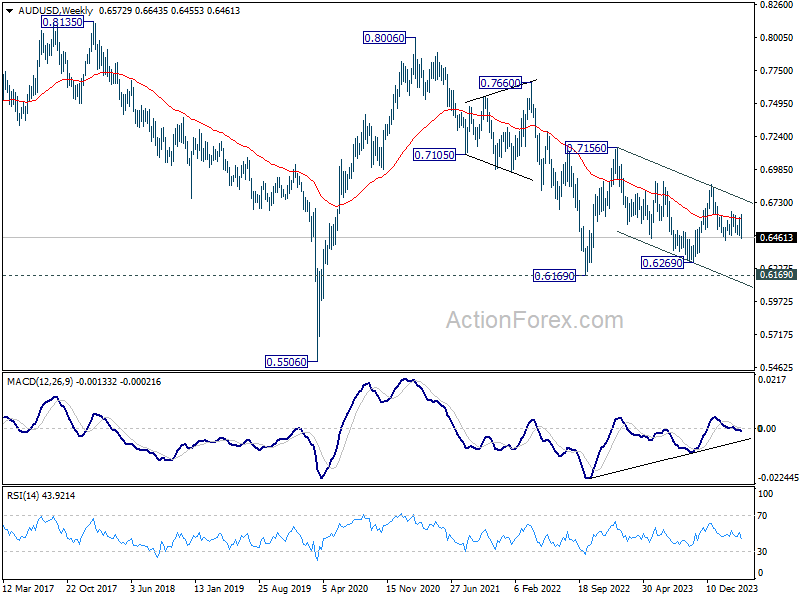

AUD/USD Weekly Report

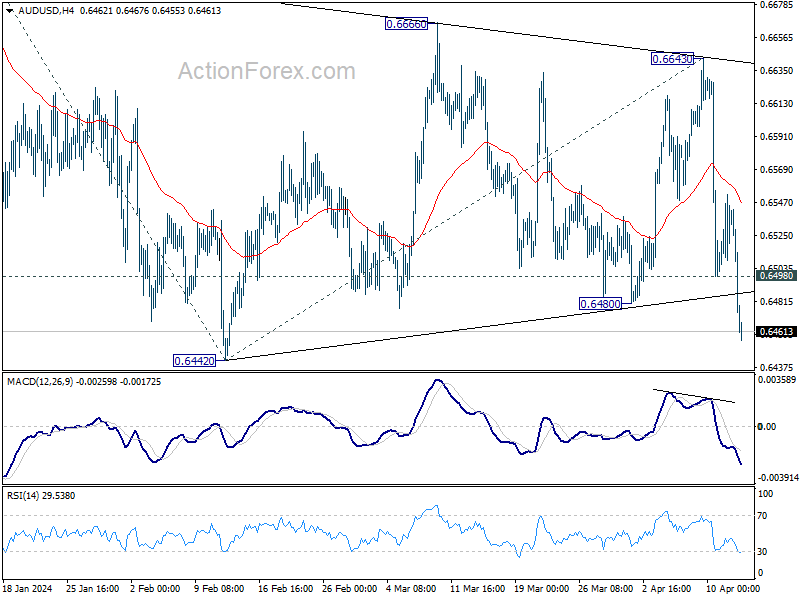

AUD/USD's steep decline last week suggests that consolidation from 0.6442 has completed at 0.6643 already. Initial bias stays on the downside this week. Firm break of 1.6442 will confirm resumption of the fall from 0.6870 and target 61.8% projection of 0.6870 to 0.6442 from 0.6643 at 0.6378. On the upside, above 0.6498 resistance will turn intraday bias and bring consolidations. But risk will stay mildly on the downside as long as 0.6643 resistance holds, in case of recovery.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

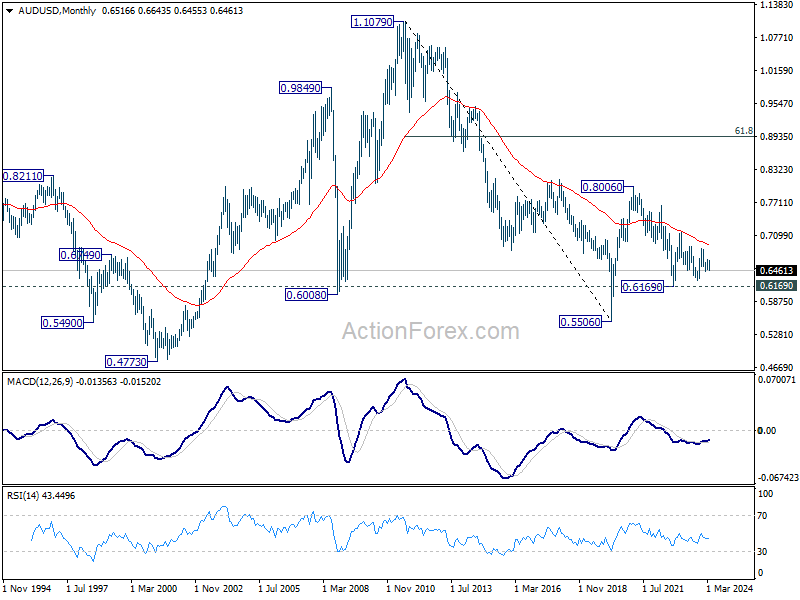

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen the second leg of the pattern. Hence, in case of deeper decline, strong support should emerge above 0.5506 to bring reversal.

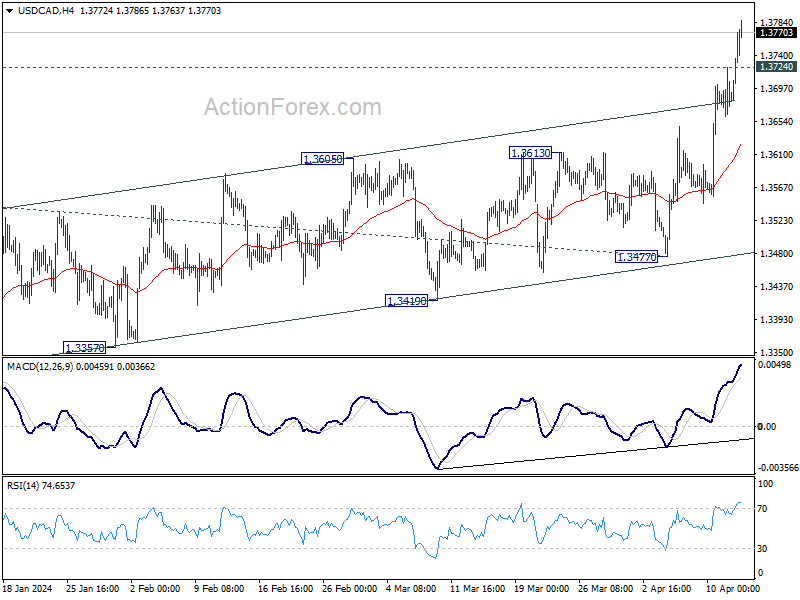

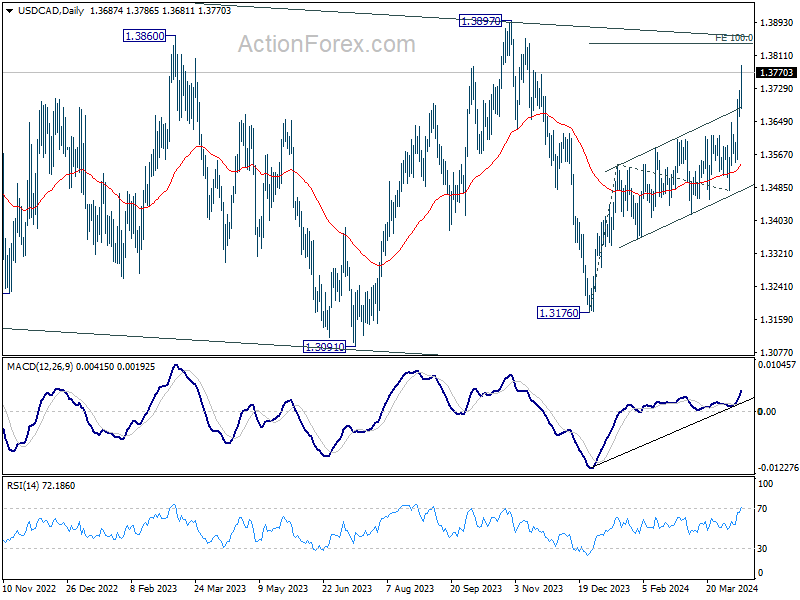

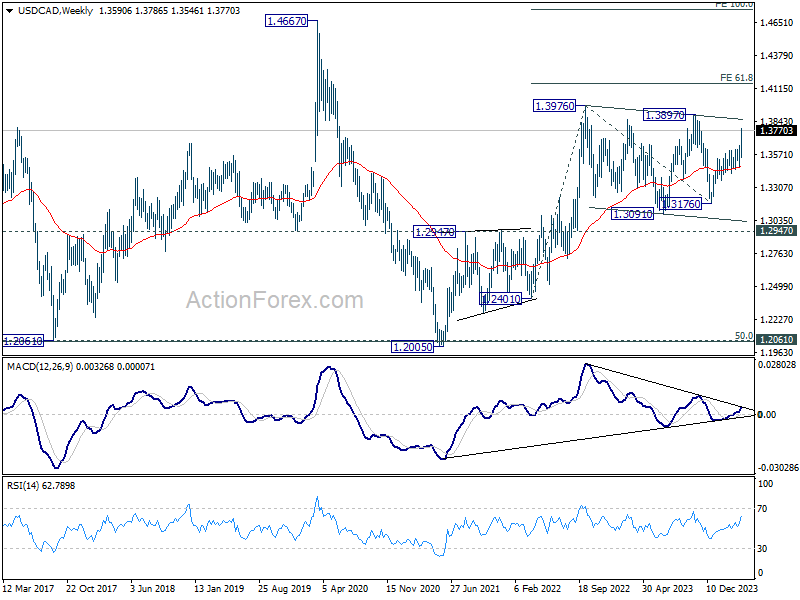

USD/CAD Weekly Outlook

USD/CAD's rally from 1.3176 resumed last week and accelerated to close at 1.3770. Initial bias stays on the upside this week. Next target is 100% projection of 1.3176 to 1.3540 from 1.3477 at 1.3841. On the downside, below 1.3724 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

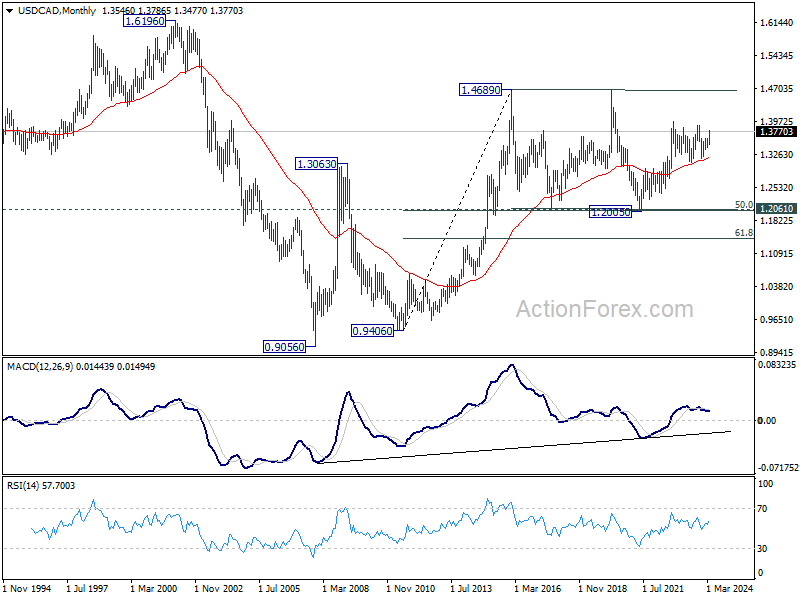

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.2947 resistance turned support holds.

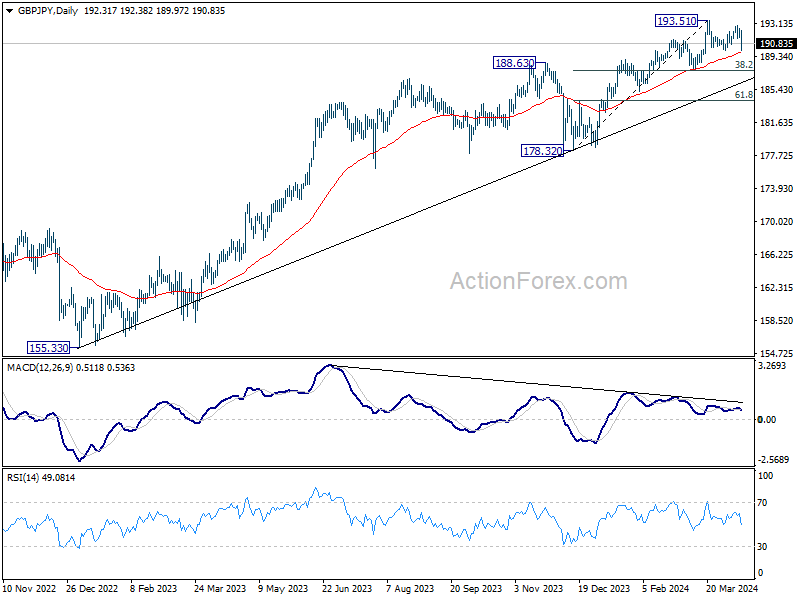

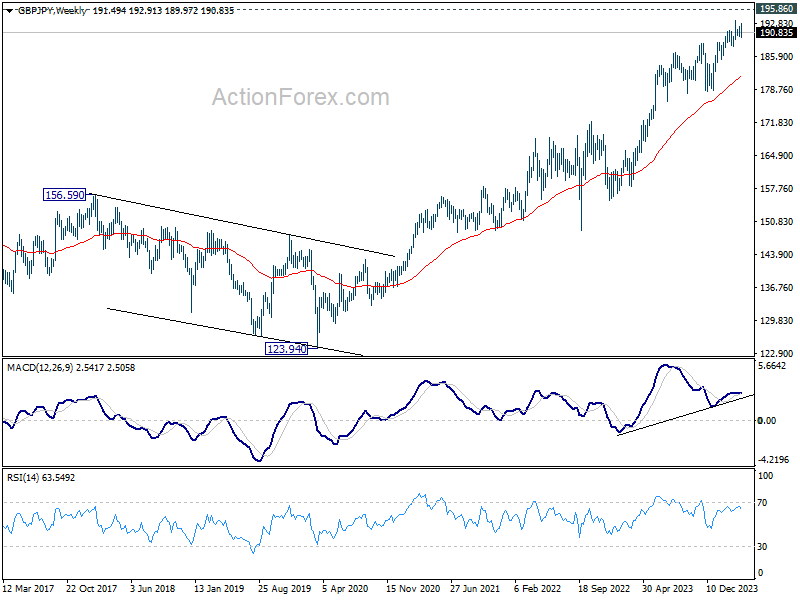

GBP/JPY Weekly Outlook

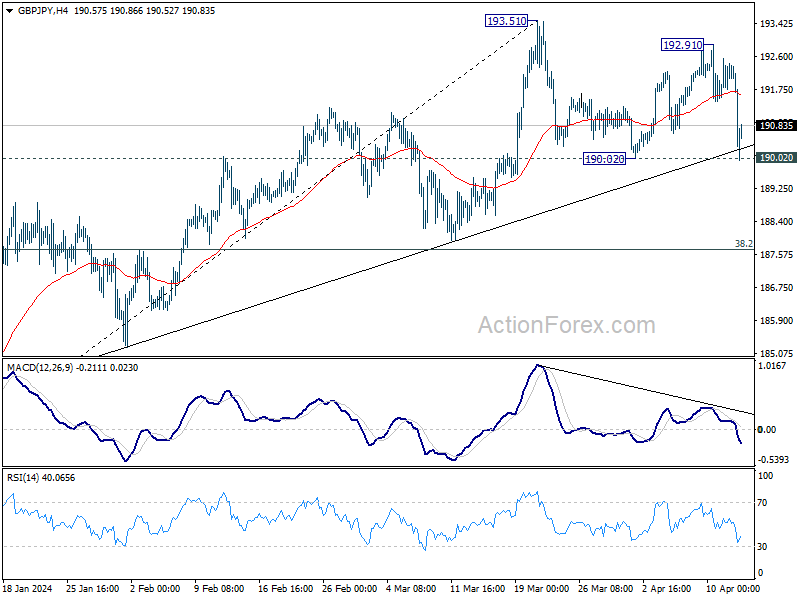

GBP/JPY retreated deeply after failing to break through 193.51 resistance, but recovered after breaching 190.02 support. Initial bias remains neutral this week first. On the upside, break of 193.51 will resume larger up trend to 195.86 long term resistance. Nevertheless, decisive break of 190.02 will indicate that it's at least correcting the rise from 178.32, and target 38.2% retracement of 178.32 to 193.51 at 187.70.

In the bigger picture, current rally is part of the up trend from 123.94 (2020 low), and is in progress for 195.86 long term resistance (2015 high). Break of 187.94 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish in case of retreat.

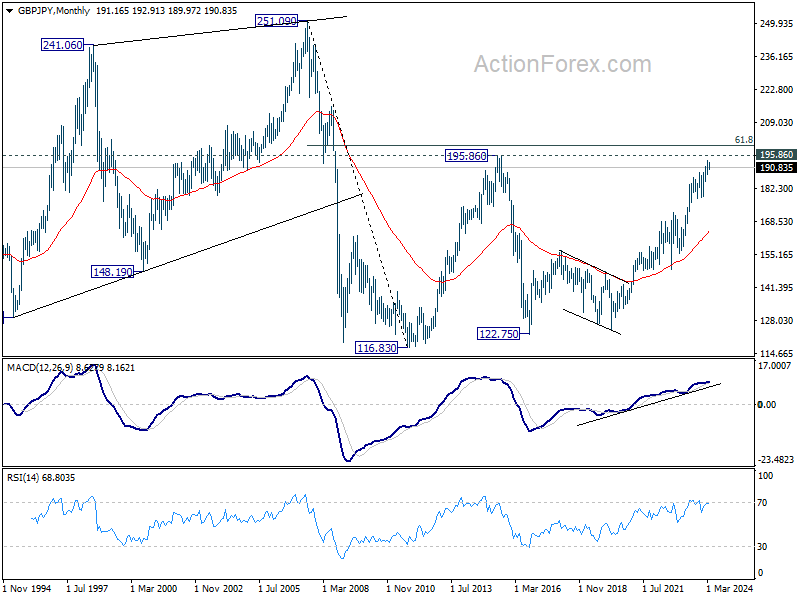

In the longer term picture, rise from 122.75 (2016 low) is seen as the third leg of the pattern from 116.83 (2011 low). Further rally will remain in favor as long as 178.32 support holds. Break of 195.86 (2015 high) is possible. But strong resistance could be seen from 61.8% retracement of 251.09 (2007 high) to 116.83 at 199.80 to limit upside, at least on first attempt.

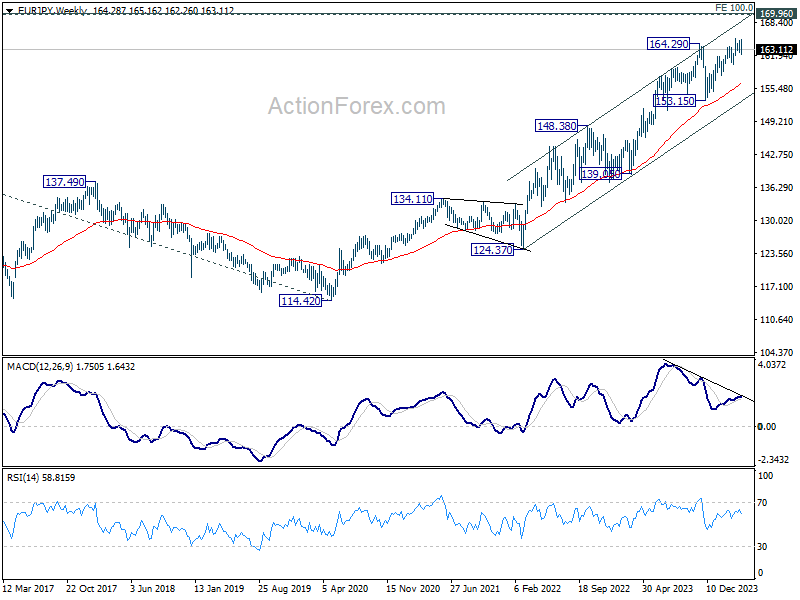

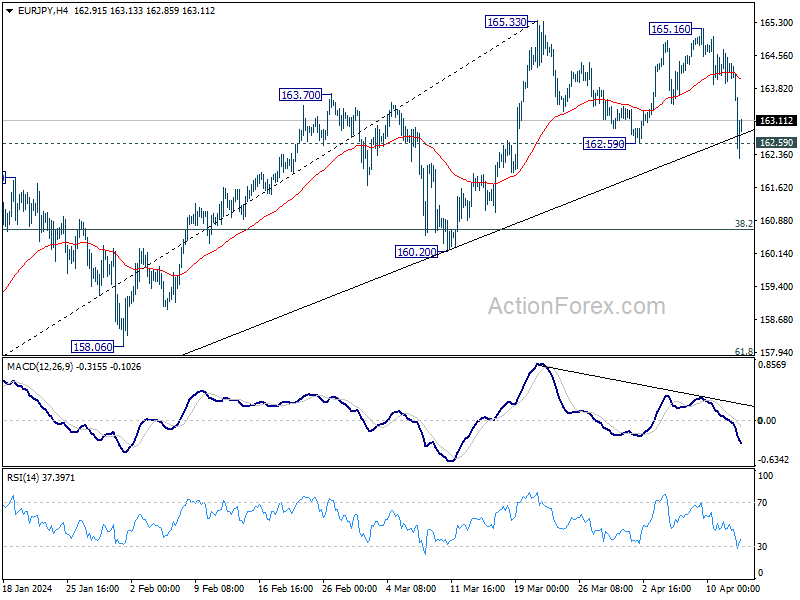

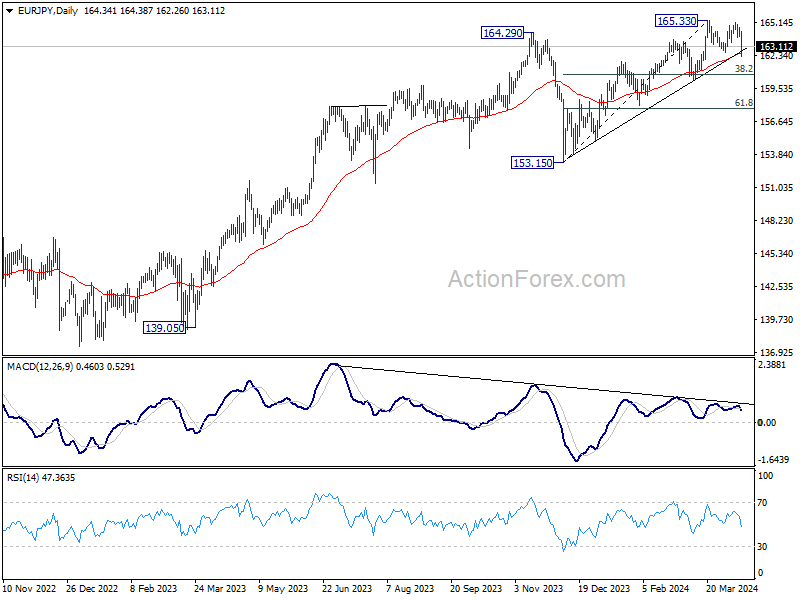

EUR/JPY Weekly Outlook

EUR/JPY failed to break through 165.33 last week and retreated sharply since then. Despite brief breach of 162.59 support, it recovered quickly. Initial bias remains neutral this week first. On the upside, firm break of 165.33 will resume larger up trend towards 169.96 key resistance next. However, decisive break of 162.59 will argue that it's at least correcting the rise from 153.15, and target 38.2% retracement of 153.15 to 165.33 at 160.67.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Break of 160.20 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

In the long term picture, rise from 114.42 (2020 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high). This will remain the favored case as long as 153.15 support holds.