Sample Category Title

Weekly Focus – US Inflation Shakes Up Markets

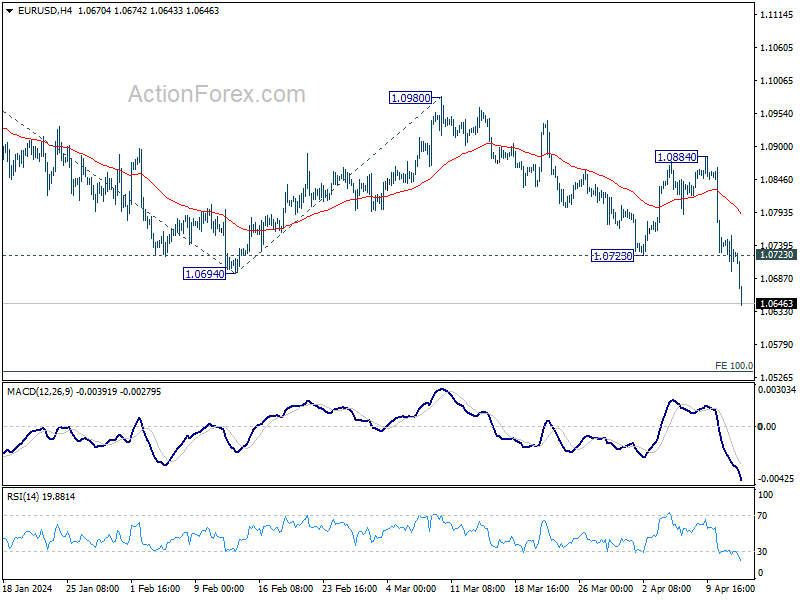

A surprisingly high US inflation print this week triggered the biggest shake-up in US bond markets in more than a year. The US 2-year government bond yield closed 23bp higher on the day, which was the biggest one-day move since March last year. It reflects a further repricing of expectations for Fed policy with money markets now pushing the first cut out to September (priced with 90% probability). The reason was not so much the size of the upward surprise in core CPI which increased 0.36% m/m versus expectations of 0.3%. But it was the third month in a row with an upward surprise and the details showed a renewed worrying upward trend in the 'super-core' inflation of services excluding shelter and health care. The data also triggered a negative response in stock markets, although the decline was overall moderate (S&P500 down 1%). Equities are currently supported by a turn higher in the global manufacturing cycle, but the high inflation data may cap performance in the short term. The USD strengthened significantly on the numbers with EUR/USD moving from 1.087 to 1.07 on Friday, the lowest in two months.

On Thursday, the ECB decided to leave policy rates unchanged as unanimously expected. A rate cut looks set to come in June, subject to further confidence on the three criteria that have guided ECB policy making through the past year. The next to no new policy signals left markets largely unchanged. We continue to like our ECB rate call of a 25bp rate cut call in June, followed by further 25bp rate cuts once per quarter through the end of 2025. We see risks skewed to less than three rate cuts this year, though.

Commodity prices have been on the rise over the past weeks as a gradual recovery in the global manufacturing cycle is lifting demand. This week oil prices moved above USD90 per barrel coming from USD80 at the beginning of the year. The LMEX metal price index has saw a further increase this week and is now up 10% since early March. The upward pressure implies that global goods price inflation has likely passed the bottom and central banks will get no further help from this side.

While US inflation is too high, China is still struggling with too low inflation. Headline CPI fell back to 0.1% y/y in March from 0.7% y/y as a temporary lift in February related to the Chinese New Year holiday dropped out again. The low inflation reflects too weak demand and the government shortly after vowed to provide further consumer stimulus.

Over the coming week focus turns to US retail sales on Monday. The numbers have been softer lately, but decent income growth should keep it supported. US also releases the surveys from Empire and Philadelphia. In the euro area the main indicators due being German ZEW and Euro industrial production. For the UK, we get the labour market report for February/March on Tuesday, where focus will be on developments in wage growth. On Wednesday, inflation for March is released where we expect both headline and core inflation to moderate. In China we get GDP for Q1 as well as the batch of industrial production, retail sales and housing data for March. Japan releases CPI inflation on Friday, which will be interesting following the change in BoJ policy lately. February inflation spiked to 2.8% on a base effect. Tokyo data indicated that price pressures remain well in line with the 2% target.

Sunset Market Commentary

Markets

This morning we wrote: “The dollar holds the better cards against both the euro and the pound. EUR/USD is nearing the 1.07 pivot again and GBP/USD holds close to 1.25 this morning. Which will break first?” Well, both, it turned out. A clearer than ever divergent path between the Fed and ECB specifically weighs on the euro. Collins (Boston Fed) picked up on her speech yesterday, adding this time that she only expects two cuts (instead of the three she probably forecasted in the March dot plot). ECB governor Stournaras this morning explicitly made the case for Frankfurt to go solo slim. He sees risks that inflation may undershoot the 2% target while the current monetary policy stance could undermine the economic recovery. A few more sessions like today’s and the former could be the least of Stournaras’ worries. EUR/USD tanked from 1.073 to 1.064, piercing through the 1.0695 support (previous 2024 low). Apart from 1.0611 (76.4% retracement on the 2023Q4 rally), the road to the 2023 low of 1.0448 is free of any obstacle. Cable (GBP/USD) succumbed to gravity. It lost the 1.25 mark with a technical acceleration lower kicking in afterwards. Filling offers around 1.2456, the pair hit a new 2024 low-point and risks losing the 50% retracement (of the October-March ascent) support area as well. The likes of BoE’s Greene over the past few days joined her hawkish colleagues Mann and Haskel in pushing back against the market’s too optimistic rate cut bets. It didn’t help against the almighty USD but EUR/GBP did slip to the lowest level in a month before paring some of the losses again. Speaking of king dollar, DXY is attacking the 106 big figure, the highest level since mid-November. JPY is the only G10 currency outperforming the dollar (USD/JPY 152.83). A steep decline in core bond yields comes an ailing yen to the rescue.

Core bonds indeed rally today. German Bunds outperform peers, probably finding support in Stournaras’ comments as well. Yields drop between 11.3 and 13.4 bps with the belly of the curve outperforming the wings. Treasury yields return some of the sharp gains earlier this week, shedding 7.8 to 9.2 bps in a curve shift similar to Germany. As things stand, the 10y yield won’t close the week above the 4.54% resistance. UK gilt yields drop more or less the same as their US counterparts. Reports of Israel preparing for a potential direct attack from Iran triggered increased core bond buying with investors seeking safety ahead of what could be an explosive weekend. The possible geopolitical escalation left stamps on other markets as well. Stocks temporarily switched from gains to losses in Europe. The EuroStoxx50 still manages to eke out a 0.2% gain. Wall Street opens up to 0.8% lower. Oil prices jumped to $91.7/b and is on track for the highest close since mid-October.

News & Views

Swedish inflation slowed to 0.1% M/M in March, both for the headline figure and for the gauge using a fixed interest rate (CPIF; Riksbank’s preferred gauge). CPIF excluding energy even stabilized on a monthly basis whereas consensus feared an acceleration for different inflation measures to 0.3% or 0.4% M/M. As a result, Y/Y-figures slowed more than forecast on a top level (4.1% Y/Y from 4.5%), using the fixed rate (2.2% Y/Y from 2.5%) and excluding energy (2.9% Y/Y from 3.5%). The monthly change in March was due to increased prices of electricity (+1.8%), (+2.6%) and transport services (+2.7%) while simultaneously, food prices fell (-0.8%). Furthermore, there were price decreases in recreation and culture (-1.3%), partly due to the yearly book sale. Today’s data strengthen the idea that the Swedish Riksbank can cut its policy rate for a first time already at its next, May, meeting. SEK swap rates drop around 15 bps across the curve today, outperforming the global market move. EUR/SEK is testing the YTD high at 11.60 in spite of genuine euro weakness.

Vietnam’s largest shipper of coffee, Intimex Group, expects coffee exports in 2023-24 to be lower than last year at 1.5mn tons. The nation has enough beans to cover exports for the rest of the season, but some farmers may continue limiting sales as they hold out for higher prices. Prices for Robusta coffee climbed to a fresh record with the arabica version advancing to the highest level since September 2022. Apart from restrained supply, the coffee markets is also rumoured to be supported from hedge funds switching from the cocoa market to the coffee one.

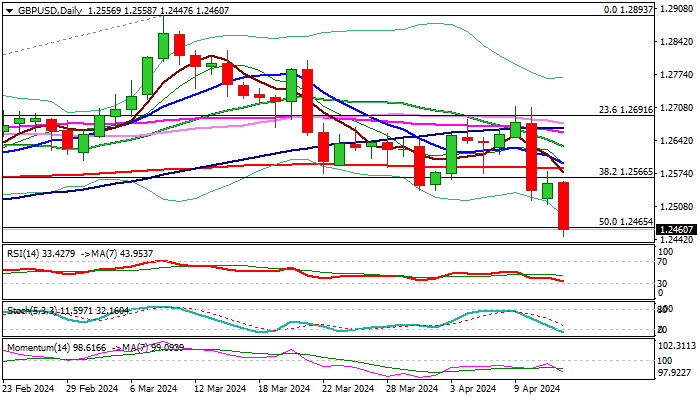

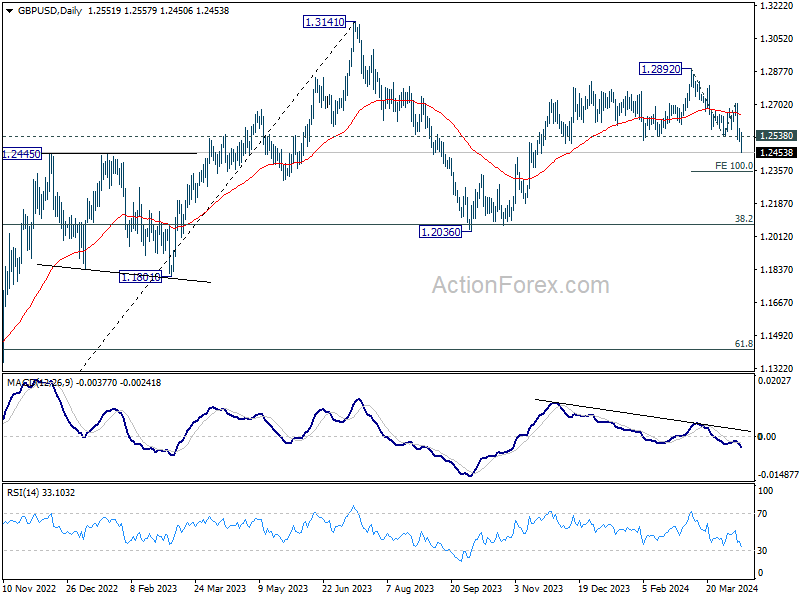

GBP/USD: Break of Pivotal Supports Sparks Fresh Acceleration Lower

Cable fell to the lowest in nearly five months on Friday, following fresh bearish acceleration through psychological 1.2500 support and Fibo level at 1.2465 (50% retracement of 1.2037/1.2893 uptrend.

Breach of a multi-month range floor (1.2518) weakens the structure and increases risk of deeper fall on completion of a double-top pattern on weekly chart.

Bearish daily studies (14-d momentum remains in negative territory / MA’s in bearish setup and formation of 5/200DMA death cross) contribute to negative outlook.

Weekly close below 1.2500 zone is minimum requirement to keep fresh bears in play and to confirm bearish signal for extension towards next target at 1.2364 (Fibo 61.8%).

Corrective upticks should be capped under broken Fibo 38.2% level (1.2566) to offer better selling opportunities.

Caution on firm break above 200DMA (1..2583).

Res: 1.2518; 1.2539; 1.2565; 1.2583.

Sup: 1.2400; 1.2364; 1.2288; 1.2239.

NZ Dollar Slips as Manufacturing Softens

The New Zealand dollar is down sharply on Friday. In the North American session, NZD/USD is trading at 0.5956, down 0.68%. The US dollar has moved higher against the majors and NZD/USD has declined about 1% this week.

NZ manufacturing PMI contracts for 13th straight month

Manufacturing has been an Achilles heel for many of the developed economies and New Zealand’s manufacturers have been hit hard. The Business NZ manufacturing PMI dropped to 47.1 in March, down from 49.3 in February. This was the lowest point this year and marked a 13th consecutive month of contraction, the longest downturn since 2009.

The prolonged slump in manufacturing shows no signs of turning the corner anytime soon. China’s slowdown has been a key factor in the downturn, as it is New Zealand’s number one export market. China is grappling with inflation and this week Fitch ratings lowered its credit outlook on China to negative, although the country’s credit rating was not affected.

New Zealand’s economy slipped into a shallow recession in the second half of 2023 but the markets remain confident that the Reserve Bank of New Zealand will lower rates this year. Investors have priced in an initial rate cut in August, while the RBNZ has projected a first rate cut in 2025. The RBNZ held rates for a sixth straight time this week and is reluctant to consider a rate cut until it is confident that inflation will remain sustainable within its 1-3% target.

The US economy continues to shine and the March nonfarm payrolls and CPI releases were stronger than expected. The Fed is concerned as inflation, which has climbed to 3.5%, has accelerated for two straight months. The hot inflation report prompted hawkish reactions this week from New York Fed President Williams and Boston Fed President Collins, who said the was no need to lower lower rates until it was evident that inflation was moving back to the 2% target. The markets have pared expectations for rate cuts as the Fed will likely delay plans to trim rates due to the strong labor market and rise in inflation.

NZD/USD Technical

- NZD/USD is putting pressure on support at 0.5953, which has held since April 3. The next support level is 0.5853

- There is resistance at 0.6000 and 0.6060

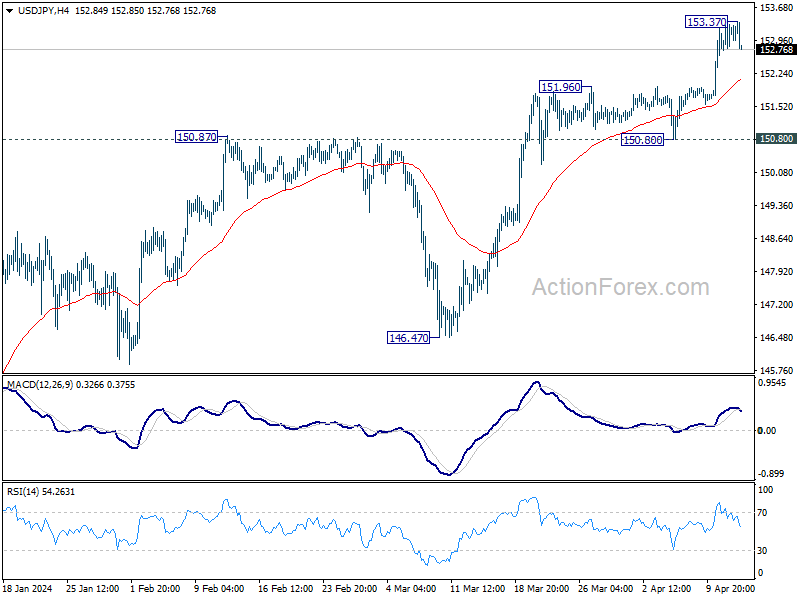

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.92; (P) 153.12; (R1) 153.48; More...

Intraday bias in USD/JPY is turned neutral first with 4H MACD crossed below signal line. Some consolidations could be seen first. But further rally is expected as long as 150.80 support holds. Break of 153.37 will resume larger up trend to 155.20 fibonacci projection level next.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

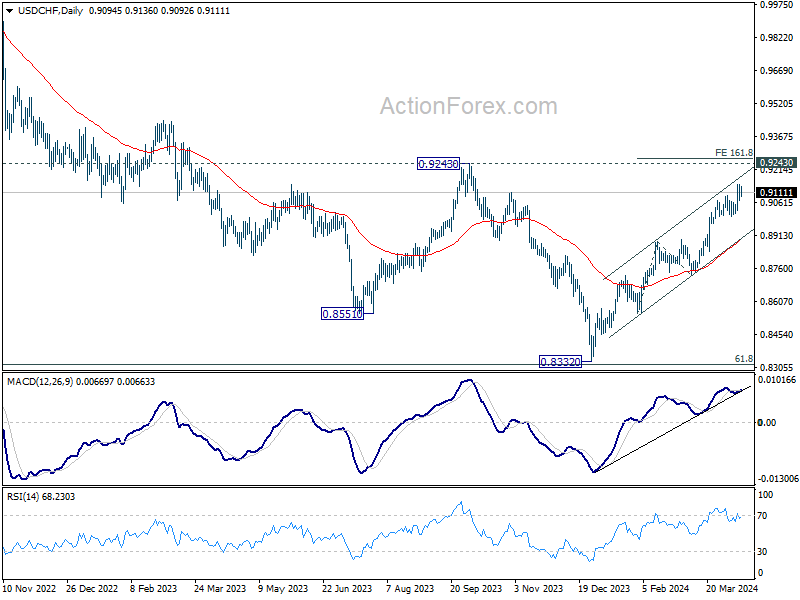

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9068; (P) 0.9107; (R1) 0.9140; More....

Intraday bias in USD/CHF remains neutral for the moment, as consolidation from 0.9146 continues. Further rally is expected as long as 0.8996 support holds. Break of 0.9146 will resume whole rally from 0.8332. Next target is 161.8% projection of 0.8550 to 0.8884 from 0.8728 at 0.8818.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

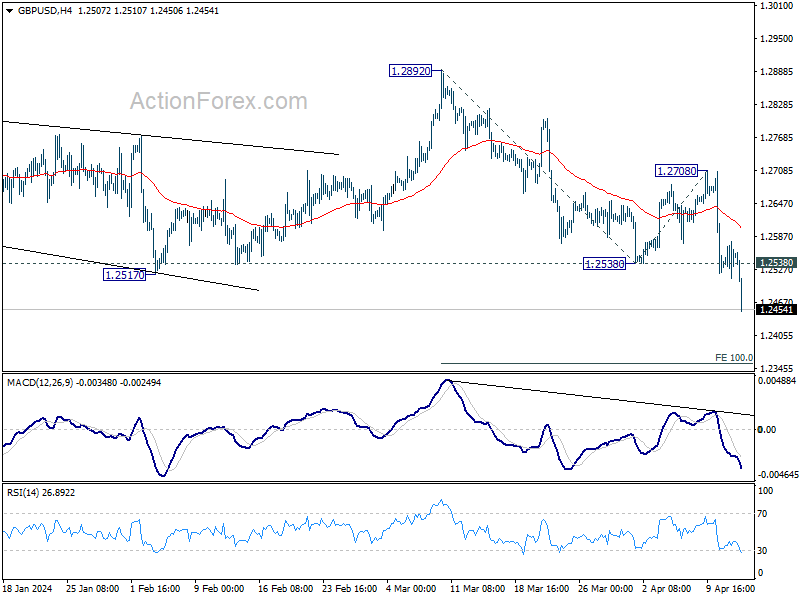

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2516; (P) 1.2548; (R1) 1.2584; More...

GBP/USD's fall continues to as low as 1.2452 so far. Intraday bias stays on the downside for 100% projection of 1.2892 to 1.2538 from 1.2708 at 1.2354 next. On the upside, above 1.2538 support turned resistance will turn intraday bias neutral and bring consolidations, because staging another decline.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0697; (P) 1.0727; (R1) 1.0755; More...

EUR/USD's decline extends through 1.0694 support today. The development confirms resumption of whole fall from 1.1138. Intraday bias stays on the downside for 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next. On the upside, above 1.0723 support turned resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below. Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

Persistent Dollar Rally Accompanied by Yen and Franc Comebacks

Dollar's rally presses on today and extends into early US session, reflecting continued strength even after a period of brief consolidation. Swiss Franc and Japanese Yen are also rebounding notably, indicating a broader trend of currency strength in traditionally safe-haven assets. This pattern is further underscored by the ongoing record rally in Gold, pointing to an underlying risk-off sentiment among global investors.

Despite these movements in the currency markets and previous metals, major European stock indexes are trading positively, while US futures show only a slight downturn. This divergence presents a contrasting picture, leaving the question on the dominant driving force unanswered for now.

As the trading week nears its close, Dollar stands out as the clear frontrunner, significantly outpacing other major currencies. New Zealand Dollar holds the second strongest position, although it appears vulnerable to being overtaken by the surging Japanese Yen, currently in third place. At the other end of the spectrum, Euro is the week's weakest performer, with British Pound and Australian Dollar following. Swiss Franc and Canadian Dollar are positioning in the middle of the pack.

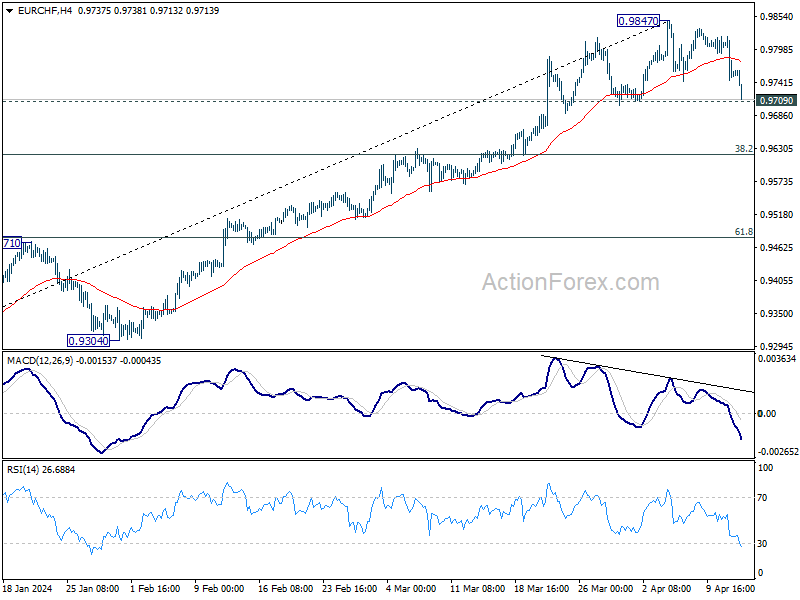

Technically, immediate focus is now on 0.9709 in EUR/CHF with current deep decline. Firm break there will at least bring deeper correction to 38.2% retracement of 0.9252 to 0.9847 at 0.9620. If realized, that would probably trigger downside acceleration in EUR/USD too.

In Europe, at the time of writing, FTSE is up 1.43%. DAX is up 0.85%. CAC is up 0.76%. UK 10-year yield is down -0.0612 at 4.142. Germany 10-year yield is down -0.105 at 2.362. Earlier in Asia, Nikkei rose 0.21%. Hong Kong HSI fell -2.18%. China Shanghai SSE fell -0.49%. Singapore Strait Times fell -0.33%. Japan 10-year JGB yield rose 0.0094 to 0.867.

Fed's Collins in the range of two rate cuts this year

In a Reuters interview, Boston Fed President Susan Collins revealed that she "in the range of two" rate cuts for this year, as per the quarterly forecast she submitted during the Fed's March meeting.

Collins was clear that an increase in interest rates is "not part of my baseline". However, she remained open to adjustments based on upcoming economic data, emphasizing, "I don't think you can take possibilities as not being on the table, it really depends on where the data take us."

Looking ahead, Collins anticipates slowdown in demand which she expects to continue into 2024. She believes this deceleration will be crucial in reducing inflationary pressures later in the year.

ECB's Stournaras advocates for insurance rate cut to nurture Eurozone recovery

ECB Governing Council member Yannis Stournaras expressed the need for an "insurance rate cut" to bolster the nascent recovery within Eurozone. Speaking to Bloomberg, Stournaras highlighted the critical balance the ECB aims to maintain in fostering economic growth without stifling it with persistently high interest rates.

Stournaras detailed the emerging signs of economic recovery across the Eurozone, particularly noting positive developments in Germany. "We see the first seeds of a recovery in Europe — also in Germany," he remarked, emphasizing "We don't want to kill these first seeds of recovery."

The concept of an insurance rate cut, as described by Stournaras, is intended to preemptively address potential downturns, mirroring the approach taken last September when rates were increased to guard against surging inflation.

Reflecting on the past year's policy decisions, Stournaras acknowledged that the situation has reversed, with new risks that "fall too far below the 2% target". Hence, "We now need an insurance in order not to get behind the curve," he added.

Moreover, Stournaras argued for a divergence from Fed's current monetary policy approach, citing fundamental differences between the economic environments in Eurozone and the US. He pointed out that unlike the US, where demand is buoyed by significant governmental budgetary measures, the Eurozone's inflation dynamics have been primarily driven by supply-side factors, not by demand or wage increases.

UK GDP rises 0.1% mom in Feb, led by production

UK GDP grew 0.1% mom in February, matched expectations. Services grew by 0.1% mom. Production output grew 1.1% mom, and was the largest contributor to growth in the month. Construction output fell -1.9% mom.

For the three months to February, compared with the three months to November 2023, GDP has grown 0.2%. Services rose 0.2%. Production grew 0.7%. Construction fell -1.0%.

NZ BNZ manufacturing falls to 47.1, 13th month of contraction

New Zealand BusinessNZ Performance of Manufacturing Index PMI fell from 49.1 to 47.1 from 49.1 in February, marking the lowest level since last December and indicating that the sector has been in contraction for 13 consecutive months.

Key components painted a concerning picture. Production experienced a notable decline from 49.1 to 45.7. Employment also fell from 49.2 to 46.8, suggesting that businesses are reducing their workforce in response to reduced demand. New orders, a critical indicator of future activity, decreased from 47.5 to 44.7.

Finished stocks were the only component of the index to show an increase, from 48.8 to 49.2. This could indicate that products are remaining in inventory longer due to lower sales volumes. Delivery times also worsened from 51.1 to 47.8, which could reflect logistical issues or supply chain disruptions.

The proportion of negative comments from survey respondents increased to 65% in March, up from 62% in February and 63.2% in January. Many cited a lack of orders and the general economic slowdown as major concerns.

Looking ahead

UK GDP is the main focus in European session, and trade balance will also be released. Germany will publish CPI final. Later in the day, US will release import price index and U of Michigan consumer sentiment.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0697; (P) 1.0727; (R1) 1.0755; More...

EUR/USD's decline extends through 1.0694 support today. The development confirms resumption of whole fall from 1.1138. Intraday bias stays on the downside for 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next. On the upside, above 1.0723 support turned resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below. Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Mar | 47.1 | 49.3 | 49.1 | |

| 04:30 | JPY | Industrial Production M/M Feb F | -0.60% | -0.10% | -0.10% | |

| 06:00 | EUR | Germany CPI M/M Mar F | 0.40% | 0.40% | 0.40% | |

| 06:00 | EUR | Germany CPI Y/Y Mar F | 2.20% | 2.20% | 2.20% | |

| 06:00 | GBP | GDP M/M Feb | 0.10% | 0.10% | 0.20% | 0.30% |

| 06:00 | GBP | Manufacturing Production M/M Feb | 1.20% | 0.20% | 0.00% | -0.20% |

| 06:00 | GBP | Manufacturing Production Y/Y Feb | 2.70% | 2.10% | 2% | 1.50% |

| 06:00 | GBP | Industrial Production M/M Feb | 1.10% | 0.00% | -0.20% | -0.30% |

| 06:00 | GBP | Industrial Production Y/Y Feb | 1.40% | 0.60% | 0.50% | 0.30% |

| 06:00 | GBP | Goods Trade Balance (GBP) Feb | -14.2B | -14.5B | -14.5B | |

| 11:00 | GBP | NIESR GDP Estimate Mar | 0.40% | 0.00% | 0.20% | |

| 12:30 | USD | Import Price Index M/M Mar | 0.40% | 0.30% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Apr P | 79 | 79.4 |

Fed’s Collins in the range of two rate cuts this year

In a Reuters interview, Boston Fed President Susan Collins revealed that she "in the range of two" rate cuts for this year, as per the quarterly forecast she submitted during the Fed's March meeting.

Collins was clear that an increase in interest rates is "not part of my baseline". However, she remained open to adjustments based on upcoming economic data, emphasizing, "I don't think you can take possibilities as not being on the table, it really depends on where the data take us."

Looking ahead, Collins anticipates slowdown in demand which she expects to continue into 2024. She believes this deceleration will be crucial in reducing inflationary pressures later in the year.