Sample Category Title

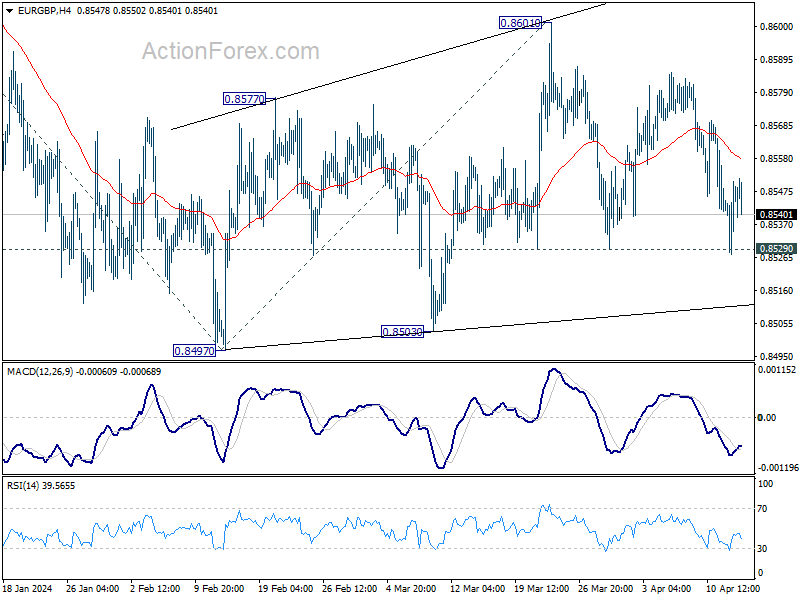

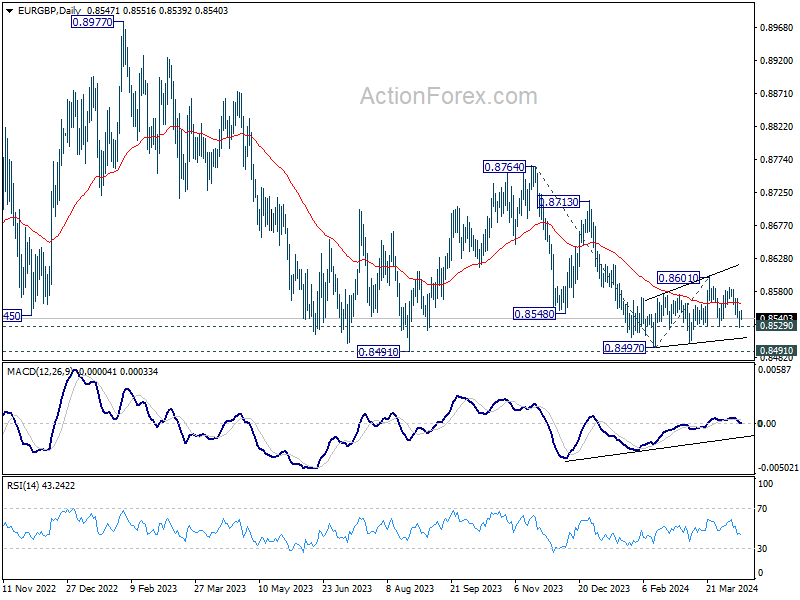

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8533; (P) 0.8542; (R1) 0.8557; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the downside, firm break of 0.8529 support will argue that the corrective recovery from 0.8497 has completed at 0.8601. Intraday bias will be back on the downside for retesting 0.8497 low next. On the upside, break of 0.8601 will resume the rebound instead.

In the bigger picture, there is no clear sign that down trend from 0.9267 has completed, despite loss of downside momentum as seen in D MACD. As long as 0.8601 resistance holds, the down trend will remain in favor to resume through 0.8491 low at la later stage.

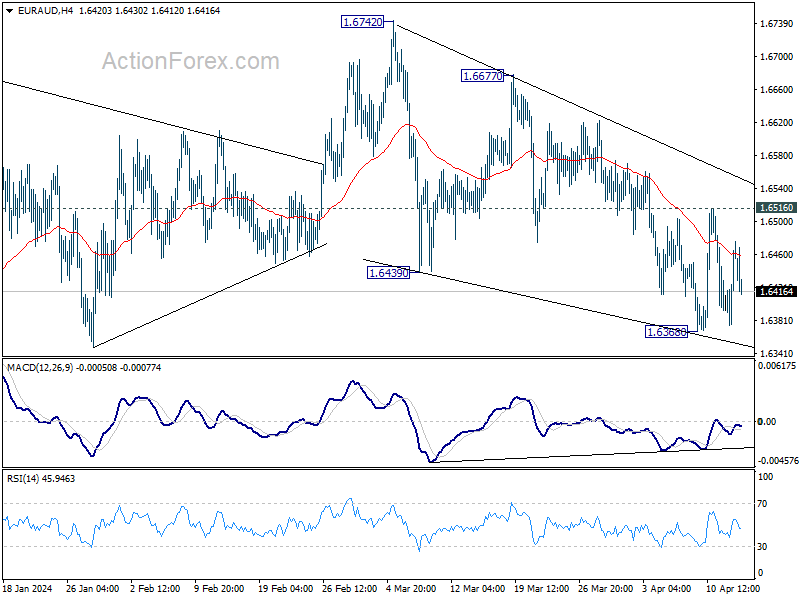

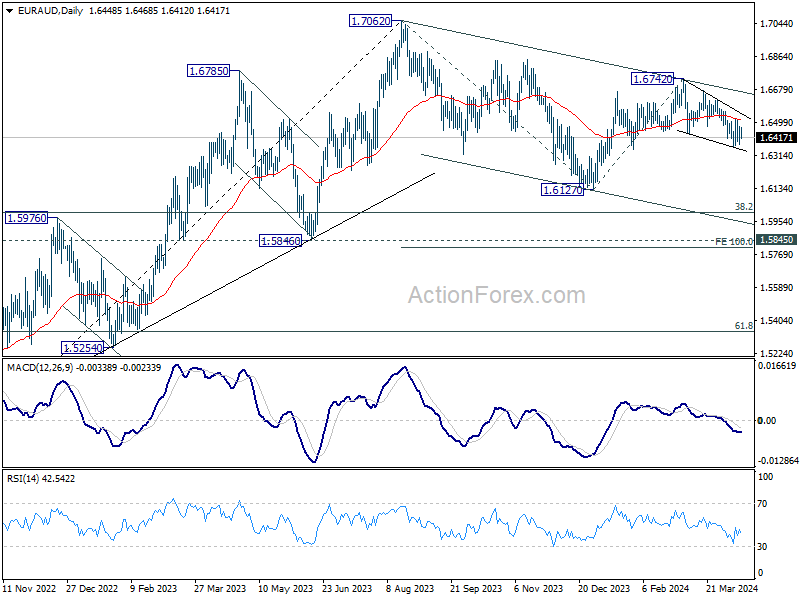

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6403; (P) 1.6442; (R1) 1.6505; More...

Intraday bias in EUR/AUD remains neutral for the moment. Risk will stay on the downside as long as 1.6516 resistance holds. On the downside, below 1.6368 will resume the fall from 1.6742 towards 1.6127 low. Nevertheless, break of 1.6516 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). The correction is probably still in progress with fall from 1.6742 as the third leg. Strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

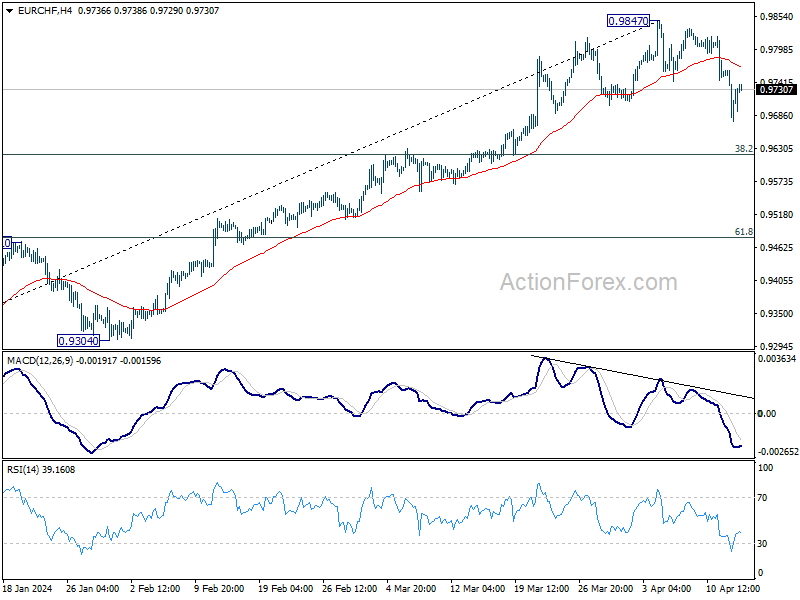

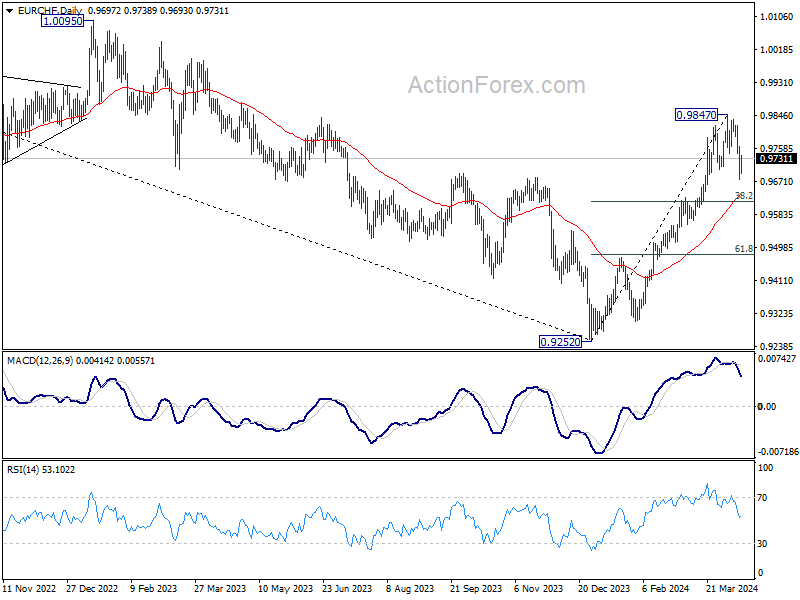

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9684; (P) 0.9724; (R1) 0.9770; More...

Intraday bias in EUR/CHF remains mildly on the downside for 38.2% retracement of 0.9252 to 0.9847 at 0.9620. But strong support is expected from there to contain downside to bring rebound, and set the range for the consolidation pattern from 0.9847. Nevertheless, for now, risk will stay on the downside as long as 0.9847 resistance holds, in case of recovery.

In the bigger picture, a medium term bottom should be in place at 0.9252 already, on bullish convergence condition in W MACD. Rise from there now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. This will remain the favored case as long as 55 D EMA (now at 0.9633) holds.

Iranian Drone Strike on Israel Escalates Middle East Tensions

In focus today

The key focus today will be the escalation of the Middle Eastern conflict following the Iranian strike on Israel and signals on the extent of Israeli retaliation, see more below.

In the euro area, we receive industrial production data for February. The industry has been weak the past years, but we are currently receiving tentative signs of a bottoming out of activity. German industrial production rose 2.1% in February, so we could be in for a decent monthly increase in the euro area today.

In the US, focus will be on March retail sales. Control group sales are likely to recover after weak prints in January and February. Unusually low seasonal adjustment factor weighed on sales growth at the start of the year, but the effect will fade from March. Besides technicalities, higher oil prices, recent upticks in immigration and the early timing of Easter may have all lifted sales towards spring.

In Sweden, the government presents its Spring Fiscal Policy Bill and amending budget bill for the current budget year. As the government already announced that the additional reforms will amount to only SEK 16.8bn it is fair to say that they maintain their restrictive fiscal policy. The number of additional reforms can be set into comparison of a SEK 33bn better than expected central government budget outcome of the last two months, or the fact that it amounts to only roughly 0.3% of the current Swedish GDP.

Overnight China will release GDP for Q1 on top of the monthly data dump across sectors. GDP is expected to rise 4.9% y/y in Q1 down from 5.2% y/y in Q4. However, it reflects a tough comparison with the high Q1 level last year after the covid reopening. On a q/q basis we look for around 1.5% growth corresponding to 6% annualised growth. Focus will also be on the data on retail sales and home sales. Consumers may hold back a bit on spending now after signals from the government that a trade-in scheme is coming, where people can trade in old durable goods and get a discount on new goods. Home sales and housing prices will provide key information on the state of the housing crisis.

Later in the week, focus will be on German ZEW data for April (Tuesday), final euro area inflation for March (Wednesday), and nation-wide March CPI from Japan (early Friday).

Economic and market news

What happened over the weekend

Tensions in the Middle East escalated as Iran attacked Israel with drones and missiles Saturday night, in retaliation for the alleged Israeli killing of military personnel at the Syrian embassy of Iran earlier this month. Damage was modest as the IDF reported to have shot down most of the weaponry. The attack was to some extent anticipated as Iran had vowed to retaliate, but both the US and several regional powers had urged restraint. The market reaction has so far been somewhat muted as markets weigh the probability of further escalation, though gold was slightly up this morning and oil slightly down. Iran says it considers 'the matter concluded' but could use greater force if Israel responds in kind while the Israeli war cabinet said on Sunday it was 'unclear when and how big' the response should be, FT reports. The US has urged Israel to show restraint. Iran has previously threatened it could close the Strait of Hormuz, through which 20% of the volume of the world's oil consumption passes through as well as a significant share of gas.

China kept a key policy rate unchanged, even after Chinese credit data surprised to the soft side on Friday suggesting China is still 'muddling through' with no bust but no strong recovery either. Despite this, the MLF rate remained unchanged on Monday as there has been pressure on the Chinese currency lately due to expectations of higher US rates for longer. Going forward, we think the PBOC stays put for a while and waits for clearer signals that the Fed is cutting as it gives them more space to lower rates without adding depreciation pressure on the currency.

In an effort to reduce Russian metals' production revenue, the US and UK expanded sanctions by banning aluminium, copper and nickel produced by Russia from being imported to the two countries, as well as banning metal exchanges (LME and CME) from accepting new contracts trading Russian-produced metals.

What happened Friday

EUR/USD continued to decline during the day as the ECB has indicated rate cuts are near while recent upside US macro surprises have lowered market expectations of rate cuts from the Fed, the latest example of this being the University of Michigan consumer sentiment showing both 1Y and 5Y inflation expectations have risen with the former showing 3.1% (+0.2).

Swedish inflation surprised to the downside with the CPIF printing at 2.2% y/y (cons: 2.6%) and core at 2.9% (cons: 3.2%) which gave further merit to a May rate cut from the Riksbank, for which markets are currently pricing 20bp. The SEK was initially weaker, then erased some losses but closed weaker with EUR/SEK up 0.68%.

Equities: Global equities were lower on Friday and lower for the week, dragged down by the US. Despite the leg lower in equities cyclicals still outperformed last week, which shows how equity investors are more nervous for overheating than recession. On Friday we saw big banks in the US massively underperforming led by JPM as their earnings and not least guidance failed to impress. In the US on Friday Dow -1.2%, S&P 500 -1.5%, Nasdaq -1.6% and Russell 2000 -1.9%. Asian markets are mostly lower this morning following Friday session on Wall Street. US and European futures are higher which might be slightly surprising for some given the Iranian attack on Israel.

FI: There was a solid decline in primary European government bond yields on Friday, where the Bund rallied some 10bp and US 10Y Treasuries rallied 6bp after the negative sentiment had dominated the bond market after the higher-than-expected US CPI-data released earlier last week. Initially, the decline in the was bigger, but at the end of the day there was a minor rebound in bond yields. If we look at the 10Y BTPS-Bund spread the spread has widened since mid-March but has now stabilised around 130bp. Furthermore, the Bund ASW-spread has also stabilised and is now trading above 30bp.

FX: The Iranian attack on Israel and raised tensions in the Middle East have weighed on Asian equities and the JPY. Muted response in oil so far with Brent at just above USD 90/bbl. EUR/USD tumbled more than 2% last week following the US CPI and the ECB news but is stable around 1.065 this morning. EUR/SEK starts the week around 11.56 and EUR/NOK 11.58, both with their eyes on the next leg for risk sentiment and oil.

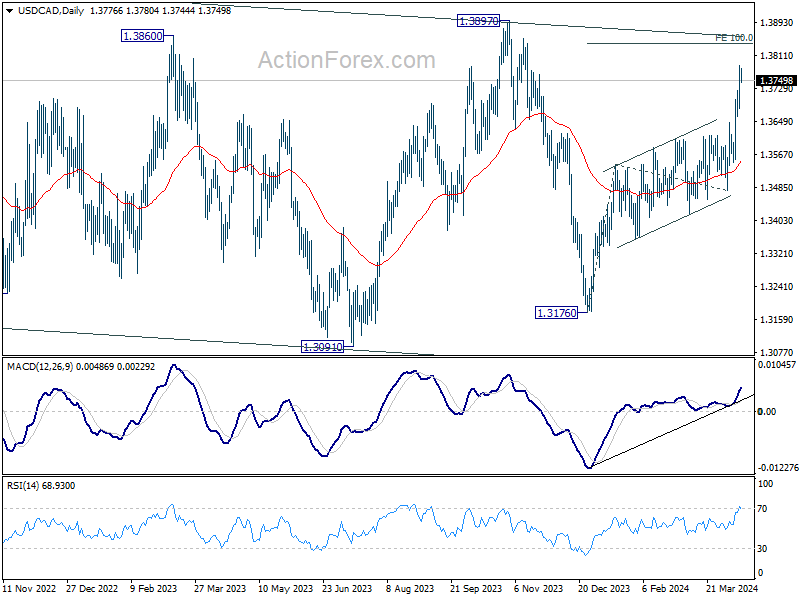

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3708; (P) 1.3748; (R1) 1.3813; More...

Intraday bias in USD/CAD remain son the upside at this point. Current rise from 1.3176 should target 100% projection of 1.3176 to 1.3540 from 1.3477 at 1.3841. On the downside, below 1.3724 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

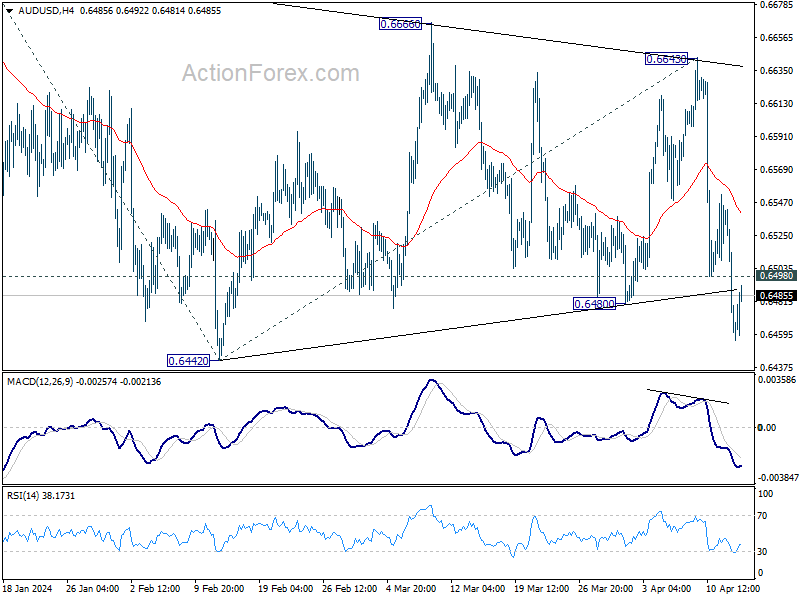

AUD/USD Daily Report

Daily Pivots: (S1) 0.6430; (P) 0.6488; (R1) 0.6520; More...

Intraday bias in AUD/USD remains on the downside for 0.6442 support. Decisive break there confirm resumption of the fall from 0.6870 and target 61.8% projection of 0.6870 to 0.6442 from 0.6643 at 0.6378. On the upside, above 0.6498 resistance will turn intraday bias and bring consolidations. But risk will stay mildly on the downside as long as 0.6643 resistance holds, in case of recovery.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

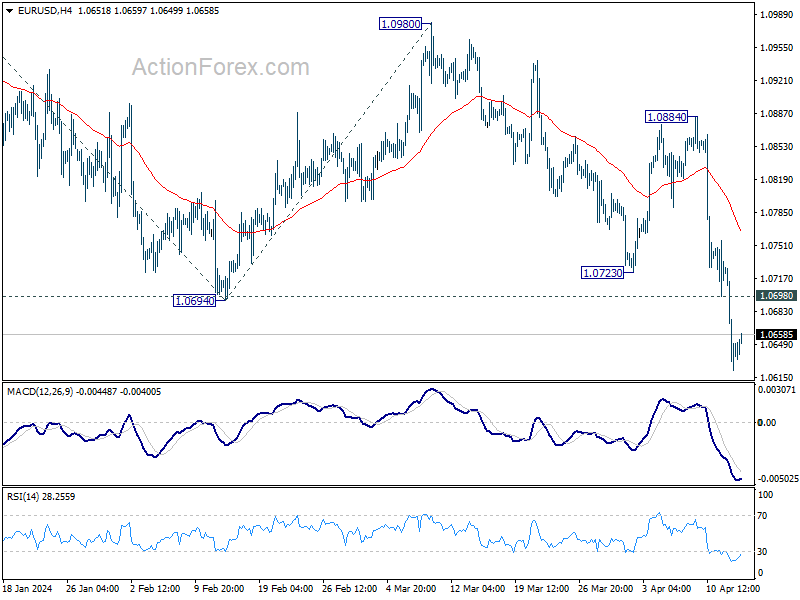

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0599; (P) 1.0665; (R1) 1.0708; More...

Intraday bias in EUR/USD remains on the downside at this point. Current is part of the decline from 1.1138. Next target is 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next. On the upside, above 1.0723 support turned resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below. Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

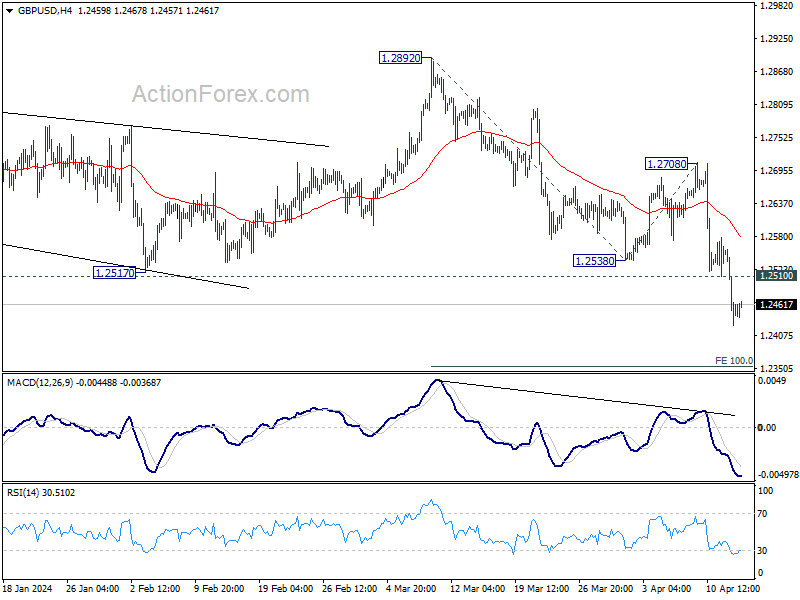

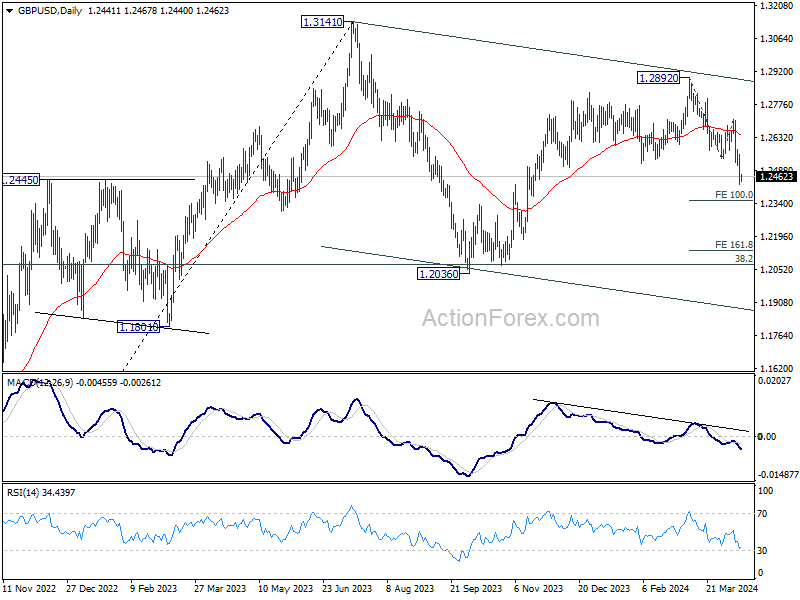

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2396; (P) 1.2481; (R1) 1.2535; More...

Intraday bias in GBP/USD remains on the downside at this point. Current fall from 1.2892 is in progress for 100% projection of 1.2892 to 1.2538 from 1.2708 at 1.2354. Firm break there will target 161.8% projection at 1.2207 next. On the upside, above 1.2510 minor resistance will turn bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

Could Have Been Worse

Risk appetite is better this Monday morning than it was last Friday when the world was bracing for the Iranian retaliation on Israel. Iran fired more than 300 drones and missiles on Israel on Saturday night, but only a small number reached Israel, limiting damages. There were no fatalities, just an army base was slightly damaged. Good news is Teran called the operation a success and declared that it won’t take further actions unless Israel responds. Oil traded slightly lower as the first reaction to the weekend news, while gold gapped higher at the open as last week’s rising tensions left a sour taste in investors’ mouth. Elsewhere, base metals including copper, iron and aluminum surged after the US and the UK decided to impose sanctions on Russian supplies. Spot aluminum jumped more than 5% while copper futures advanced to the highest levels since last summer. The dollar index consolidated on Monday after a 2% jump last week.

Too strong to cut

The US dollar strengthens on the back of a severe deterioration in Federal Reserve (Fed) rate cut expectations following strong jobs and inflation data, and the dollar outlook remains comfortably bullish.

The US 2-year yield hit 5% post-US CPI data, and the probability of a June Fed rate cut fell to around 22%. July cut expectations is around 50-50, and a September rate cut is given around 73% chance.

And you know the election narrative that the Fed may not opt for a rate cut approaching the November presidential election, which would delay the first cut to after the election. And some believe that the Fed’s next move won’t be a cut, but a rate hike to tame rising inflationary pressures. That’s a significant readjustment compared to the expectation of six rate cuts in January.

Diverging fortunes

While the US data continues to cement the strength of the US economy and the fact the US doesn’t need to cut rates – and should not be cutting rates with heating inflation - the rate cut expectations elsewhere remain pretty solid. Last week’s European Central Bank (ECB) meeting gave another hint that the bank will more likely than not cut its own rates in June. ECB Chief Christine Lagarde said that the ECB is data dependent and not Fed dependent and other members noted that it’s time to ‘diverge’ from the Fed, as the US consumers are relentless – and the US government is very supportive – with Biden looking to cancel $7.4bn in student debt to please young voters before the election.

As a result, the gap between the Fed and the ECB rate cut expectations widened to the highest level this year following a dovish ECB stance and another set of strong jobs and inflation read in the US. And the chatter of a further euro depreciation to parity against the US dollar is being brought back on the table. At the current levels, the RSI indicator is very close to the oversold territory, meaning that the euro was sold too rapidly in a too short period of time and a correction could be needed. But most traders will be looking to sell the tops in the EURUSD on the back of the growing divergence between the soft ECB and the Fed – that simply can’t justify a rate cut this summer.

Earnings

The S&P 500 posted its worst weekly performance since late October 2023. Mixed bank earnings didn’t help improve mood on Friday. JPM tanked 6.5% as net interest income missed expectations and slipped from the previous quarter as investors chased higher returns. The latter is a real joy killer among investors who were expecting to hear how much more net interest income the bank could gain with a delayed rate cut from the Fed. Similarly, deposits that don’t pay interest at Wells Fargo slumped 18% in Q1

This week, the earnings season gains momentum with the rest of the US big banks, Netflix and TSM due to announce their Q1 results. The expectation is a 3.8% annual growth in S&P500 companies’ earnings per share in the Q1, while profits for the Magnificent Seven are expected to have risen around 38%. Another strong quarter in terms of earnings could slow a potential selloff in the S&P500 – that sees the selling pressure rise on the back of rising hawkish voices. But a softer-than-expected earnings season will likely trigger profit taking.

Halving

Bitcoin slumped over the weekend as rising geopolitical tensions weighed on risk appetite. Bitcoin halving is expected to happen in the coming days. Lower supply is fundamentally supportive of an asset’s valuation, but we might not see a clear kneejerk reaction to Bitcoin halving as most of it is already priced in.

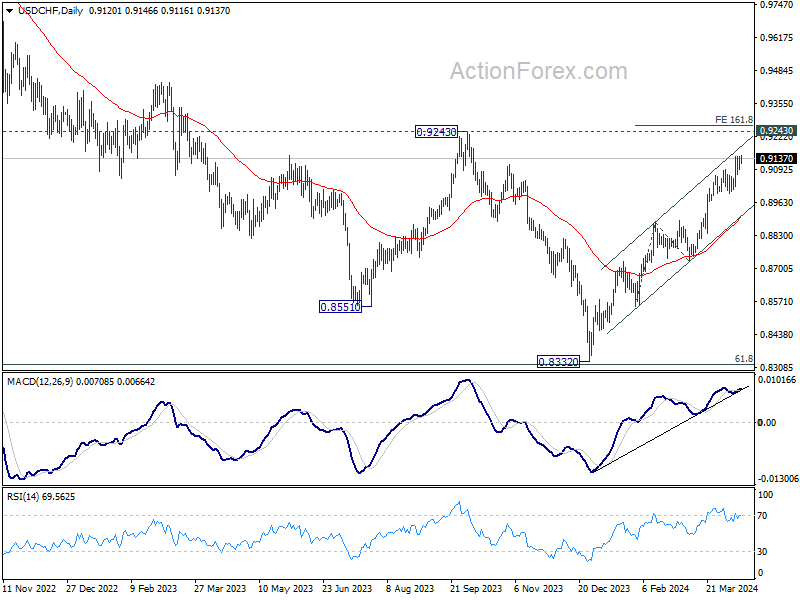

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9105; (P) 0.9126; (R1) 0.9164; More....

Intraday bias in USD/CHF remains neutral as consolidation from 0.9146 might extend. Further rally is expected as long as 0.8996 support holds. Above 0.9146 will target 161.8% projection of 0.8550 to 0.8884 from 0.8728 at 0.9268.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.