Sample Category Title

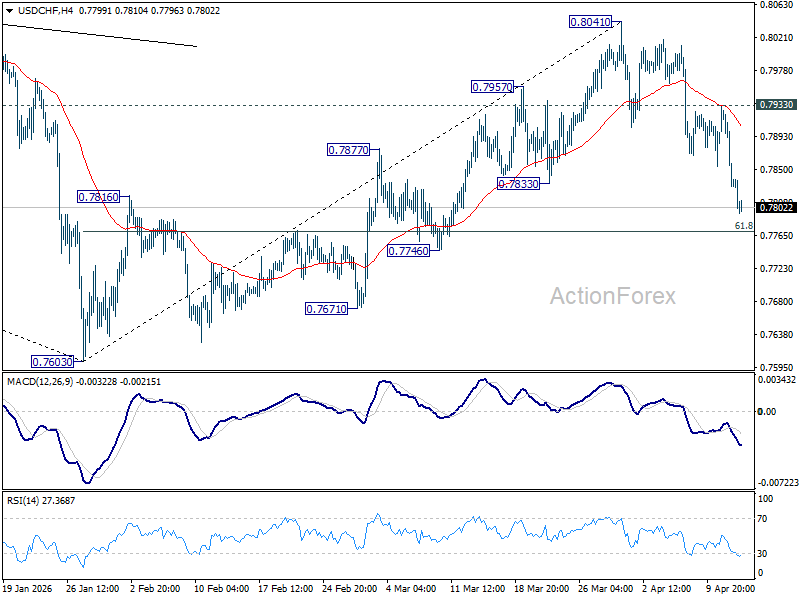

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7801; (P) 0.7867; (R1) 0.7906; More….

Intraday bias in USD/CHF remains on the downside for 61.8% retracement of 0.7603 to 0.8041 at 0.7770 . Firm break there will extend the fall from 0.8041 to retest 0.7603 low. For now, risk will stay on the downside as long as 0.7933 resistance holds, in case of recovery.

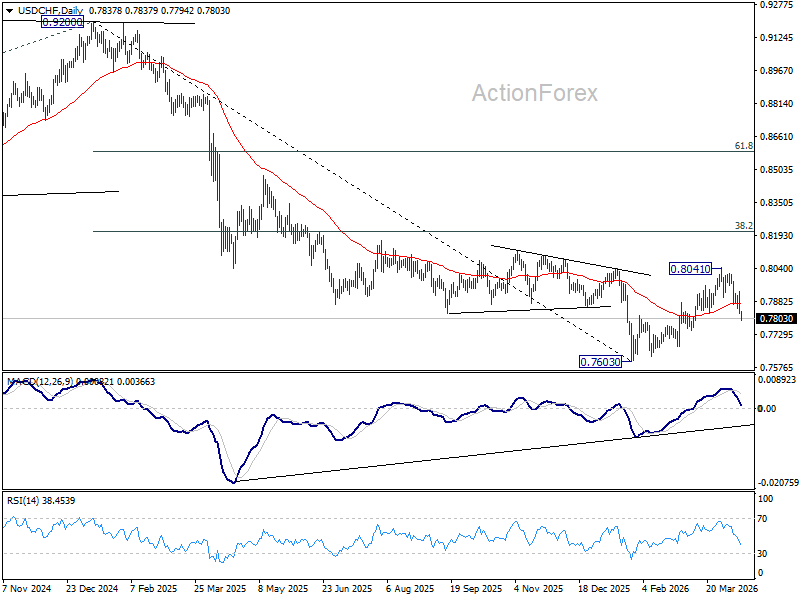

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8071) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

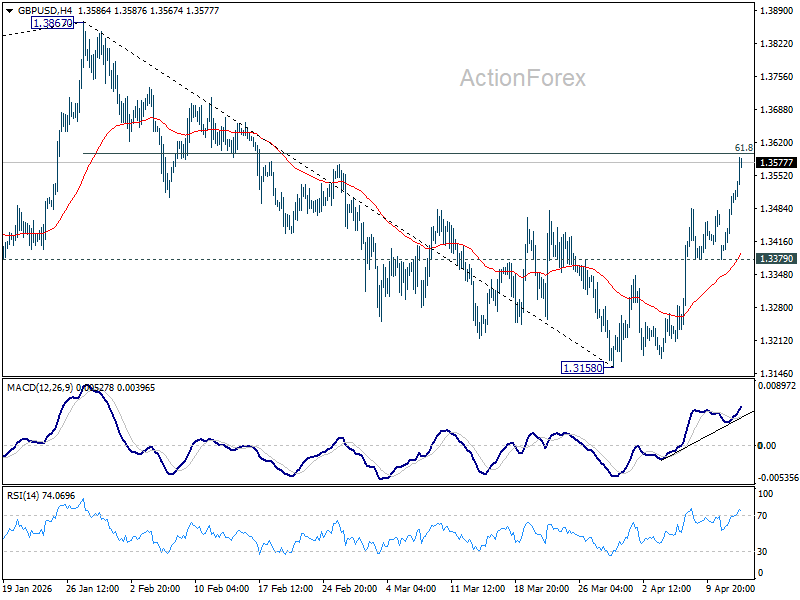

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3422; (P) 1.3466; (R1) 1.3551; More...

Intraday bias in GBP/USD remains on the upside for 61.8% retracement of 1.3867 to 1.3158 at 1.3596. Decisive break there will extend the rise from 1.3158 to retest 1.3867 high. For now, further rally will remain in favor as long as 1.3379 support holds, in case of retreat.

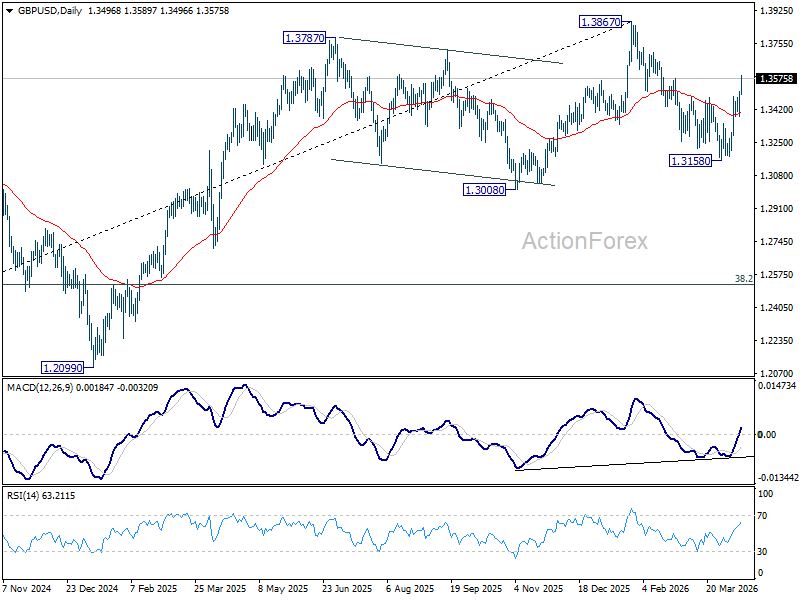

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

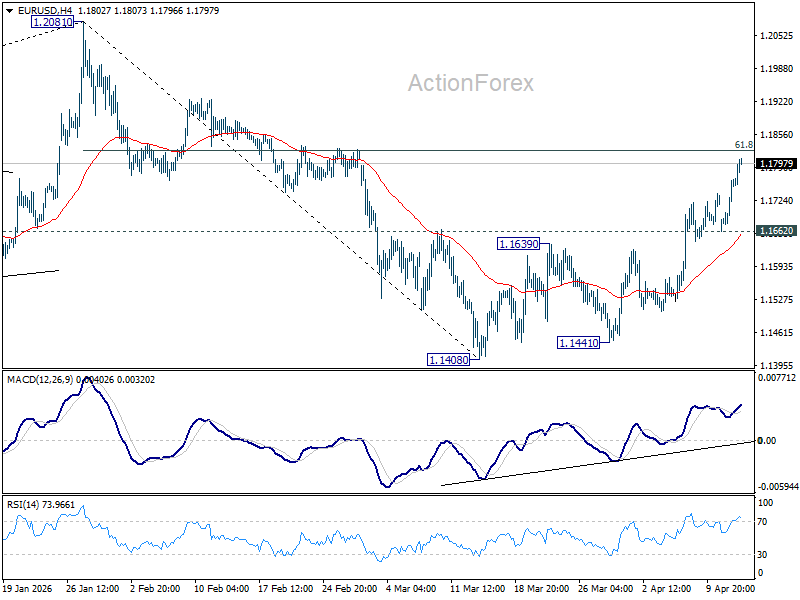

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1694; (P) 1.1729; (R1) 1.1795; More….

Intraday bias in EUR/USD remains on the upside for 61.8% retracement of 1.2081 to 1.1408 at 1.1824. Decisive break there will extend the rally from 1.1408 to retest 1.2081 high. For now, further rally will remain in favor as long as 1.1662 support holds, in case of retreat.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1513). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

Dollar Selloff Intensifies as Soft PPI Eases Fed Pressure, US-Iran Optimism Builds

Dollar is being hit from both sides—soft inflation and warmer diplomacy. A cooler-than-expected PPI reading has eased pressure on the Federal Reserve to turn more hawkish, while renewed optimism around US-Iran negotiations is unwinding the war premium that briefly supported the greenback. Together, these forces are driving an extended, broad-based Dollar selloff in early US session.

The PPI data delivered a key relief signal for markets. Headline producer prices rose just 0.5% mom, well below expectations. But the most important detail came from services, which printed at 0.0% mom. This suggests that the inflation pipeline is not as clogged as feared, with businesses absorbing higher input costs rather than passing them on to consumers.

That dynamic is critical for Fed policy expectations. With margins compressing instead of prices rising across services, the data reinforces the view that underlying inflation pressures remain contained despite the energy shock. This gives the FOMC room to remain patient rather than reactive, validating recent messaging that more data is needed before committing to further tightening.

As a result, the “higher and still rising” rate narrative has been firmly pushed off the table for now. Instead, markets are anchoring expectations around a “higher for longer” stance, with reduced urgency for additional hikes. This repricing has weighed on US yields and removed a key pillar of Dollar support.

At the same time, geopolitics are moving in a more constructive direction. Markets are pricing progress again—not escalation—as signals emerge that US-Iran talks could resume as soon as this week. The breakdown in Islamabad is increasingly being viewed as a pause rather than a failure.

Reports that both sides were “80% there” before hitting a deadlock have given traders a tangible reason to expect a second round of negotiations. The remaining gap, largely centered on nuclear commitments, is seen as political and potentially bridgeable within the current ceasefire window.

European diplomacy is also stepping up. French President Emmanuel Macron confirmed that France and the UK will host a conference in Paris aimed at restoring freedom of navigation. The initiative seeks to bring in "non-belligerent countries", raising the diplomatic cost of further escalation.

This combination of factors is driving a rapid unwind of the war premium. Oil has retreated rather than extending its rally, equities are holding firmer, and safe-haven demand for Dollar is fading. The earlier risk-off move is now being reversed as markets reposition for a continuation of diplomacy.

In the currency markets, Dollar remains the worst performer for the day, followed by Euro, and then Loonie. Kiwi is currently the strongest, followed by Aussie and then Sterling. Yen and Swiss Franc are trading in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.13%. DAX is up 1.19%. CAC is up 0.76%. UK 10-year yield is down -0.054 at 4.763. Germany 10-year yield is down -0.038 at 3.060. Earlier in Asia, Nikkei rose 2.43%. Hong Kong HSI rose 0.82%. China Shanghai SSE rose 0.95%. Singapore Strait Times rose 0.47%. Japan 10-year JGB yield fell -0.054 at 2.420.

Silver Rallies, Outperforming Gold, as Supply Shock Risk Builds on Sulphur Shortage and China Export Ban

Silver is outperforming gold as markets begin to price a potential supply squeeze driven by sulphur shortages and China’s export ban. With a key input under pressure and supply tightening from multiple fronts, the rally is shifting from a Dollar-driven move to a structural story. Read more.

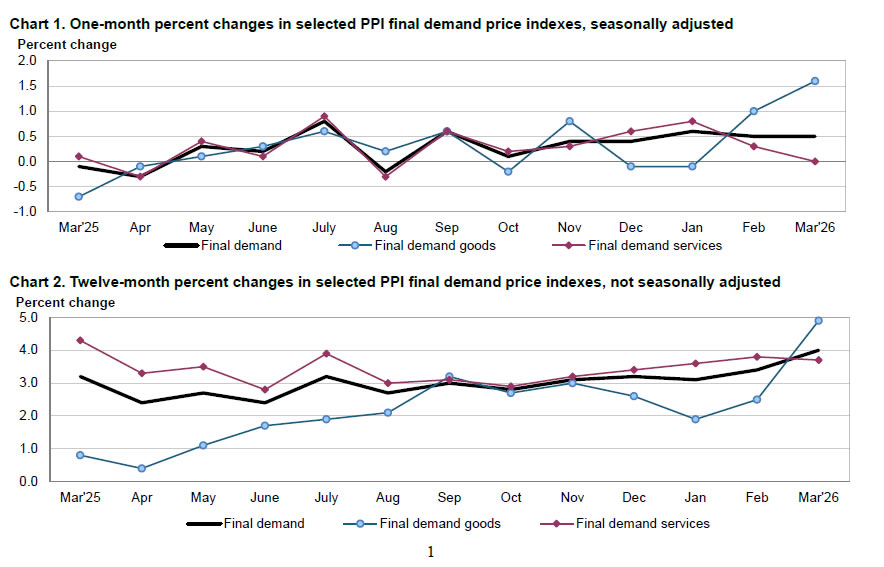

US PPI Inflation Rises 0.5% as Led by 16.7% Surge in Gasoline Prices, But Misses Expectations

US producer price inflation picked up in March, led by a sharp jump in gasoline prices, but the broader picture remains contained. With core pressures steady and services inflation flat, the data suggests energy is driving the move rather than a broad inflation surge. Read more.

RBA’s Hauser Warns of ‘Central Banker’s Nightmare’ as Oil Shock Lifts Inflation, Hits Growth

RBA Deputy Governor Andrew Hauser warns that rising oil prices are delivering a “central banker’s nightmare,” with inflation climbing as growth risks build. With a potential income shock looming and policy uncertainty rising, the RBA faces a difficult balancing act. Read more.

Australian Consumer Sentiment Plunges as Fuel Prices Surge, RBA Still Set to Hike

Australian consumer sentiment has dropped sharply to near crisis levels as fuel prices and rate hikes hit households. But with inflation still elevated, Westpac expects the RBA to raise rates again in May and continue tightening later this year, highlighting the growing tension between weaker demand and persistent price pressures. Read more.

Australian NAB Business Confidence Plunges to -29 as Middle East Shock Hits

Australian business confidence has collapsed to GFC- and COVID-era levels as Middle East tensions hit sentiment, but activity is still holding for now. With cost pressures surging and price growth accelerating, the data highlights a growing tension between weakening outlook and rising inflation risks. Read more.

China Trade Signals Diverge as Weak Exports Meet Import Boom

China’s trade data showed a sharp split in March, with exports slowing to a five-month low while imports surged on commodity demand. Read more.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1694; (P) 1.1729; (R1) 1.1795; More….

Intraday bias in EUR/USD remains on the upside for 61.8% retracement of 1.2081 to 1.1408 at 1.1824. Decisive break there will extend the rally from 1.1408 to retest 1.2081 high. For now, further rally will remain in favor as long as 1.1662 support holds, in case of retreat.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1513). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

US PPI Inflation Rises 0.5% as Led by 16.7% Surge in Gasoline Prices, But Misses Expectations

US producer prices rose in March, driven largely by a surge in energy costs, though the overall increase came in below expectations. Headline PPI climbed 0.5% mom, up from prior months but well short of the 1.2% mom forecast. On an annual basis, PPI accelerated from 3.4% yoy to 4.0% yoy, also missing expectations of 4.6% yoy, marking the largest 12-month gain since early 2023.

The details point to a clear energy-driven move rather than broad-based inflation pressure. Goods prices jumped 1.6% , with nearly half of the increase attributed to a 15.7% surge in gasoline prices. In contrast, services prices were unchanged, suggesting limited pass-through into the broader economy so far.

Underlying inflation measures were more contained. The index for final demand excluding foods, energy, and trade services rose just 0.2% mom, following stronger 0.5% gains in the prior two months. On a yearly basis, core PPI held at 3.6% yoy. The data reinforces the view that recent inflation pressures are being driven by volatile energy costs rather than a sustained pickup in underlying price momentum.

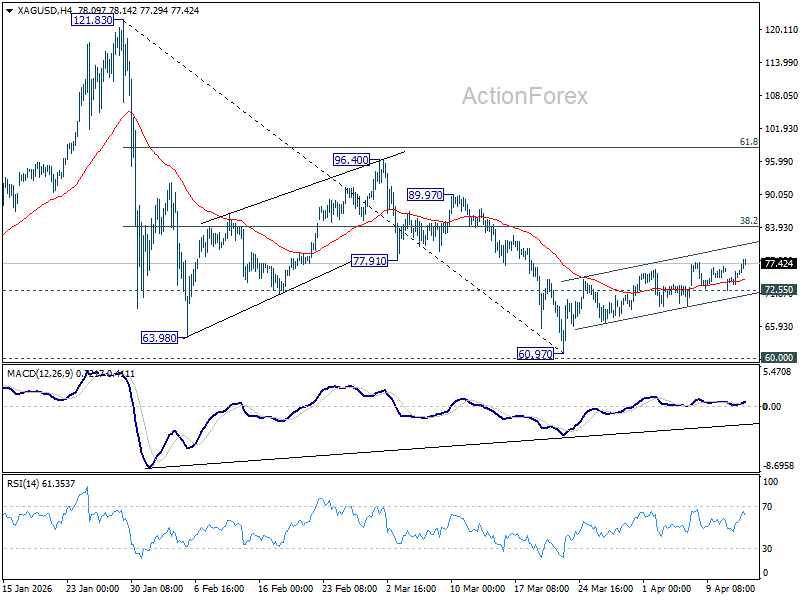

Silver Rallies, Outperforming Gold, as Supply Shock Risk Builds on Sulphur Shortage and China Export Ban

A double supply shock is building beneath the surface of the Silver market—and prices are starting to respond. While the broader metals complex is supported by Dollar weakness today, Silver is clearly outperforming Gold as traders begin to price in tightening supply conditions linked to sulphur shortages and China’s export restrictions.

At the heart of the story is a critical but often overlooked input. Silver production is heavily dependent on base metal mining, where sulfuric acid plays a key role in extraction processes. That creates a direct link between Sulphur availability and Silver output, turning disruptions in the former into constraints on the latter.

Those disruptions are now materializing. The closure of the Strait of Hormuz has hit Middle Eastern Sulphur supply, which accounts for a significant share of global production and an even larger portion of seaborne trade. This alone would tighten conditions, but the situation is being compounded by China’s policy shift.

China, the world’s second-largest exporter of sulfuric acid, will ban exports from May 1 to protect domestic supply for fertilizers and green technology. This move effectively removes the last major source of flexible supply for global markets, amplifying the impact of disruptions in the Middle East.

The result is a tightening feedback loop. As Sulphur supply contracts, mining operations face higher input costs and potential output constraints. This dynamic is particularly relevant for Silver, where production is less responsive to price signals due to its by-product nature.

Markets are beginning to price this risk. The narrative has shifted from macro-driven gains to a more structural supply story, with traders increasingly focused on the potential for a physical squeeze. If China enforces its export ban strictly, industrial users may be forced to secure supply at increasingly elevated prices.

Technically, Silver’s rebound from 60.97 resumed today, supported by improving sentiment and underlying demand. Momentum remains contained within the near rising channel, suggesting that the move is still in a developing phase.

Nonetheless, further rise is expected as long as 72.55 support holds, towards 38.2% retracement of 121.83 to 60.97 at 84.21. This level represents a key inflection point for the broader outlook.

Decisive break above 84.21 would confirm that the corrective decline from 121.83 has completed with three waves down to 60.97, opening the door for a stronger rally toward 61.8% retracement at 98.58.

Conversely, rejection at 84.21 would point to lingering weakness, with scope for another selloff toward the 60 structural floor.

GBP/USD Finds Support: Geopolitics Already Priced In, Focus on Bank of England

GBP/USD rose to 1.3506 on Tuesday. Sterling has moved comfortably away from last week's one-month high of 1.3480. Pressure on the currency had previously increased following the collapse of US-Iran talks over the weekend.

The breakdown in dialogue followed Tehran's refusal to abandon its nuclear program and disagreements over the terms of the agreement, which the Iranian side described as excessive. Against this backdrop, Donald Trump threatened to block the Strait of Hormuz, a critical oil supply route. This pushed Brent crude prices to 102.00 USD per barrel.

Oil has become markedly more expensive, adding tension to the already strained global energy situation and raising the risks of an inflationary shock. As a result, market expectations have shifted towards a tighter Bank of England policy.

As a result, investors are now pricing in at least one interest rate hike by the end of 2026.

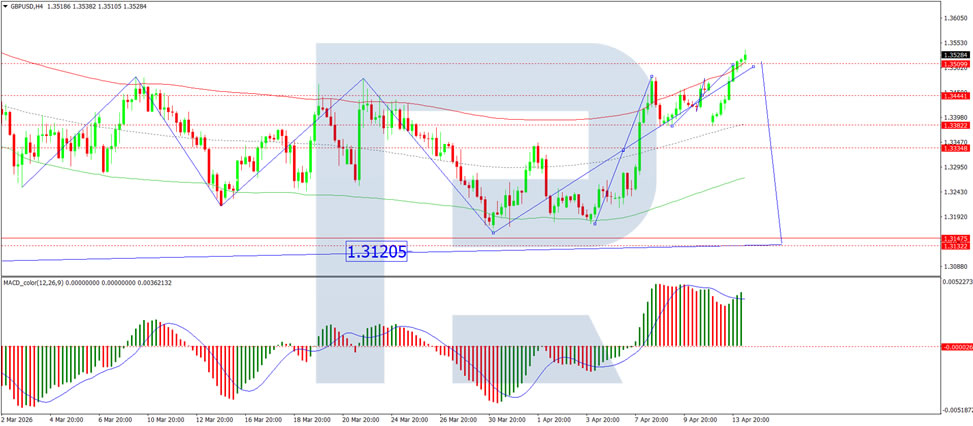

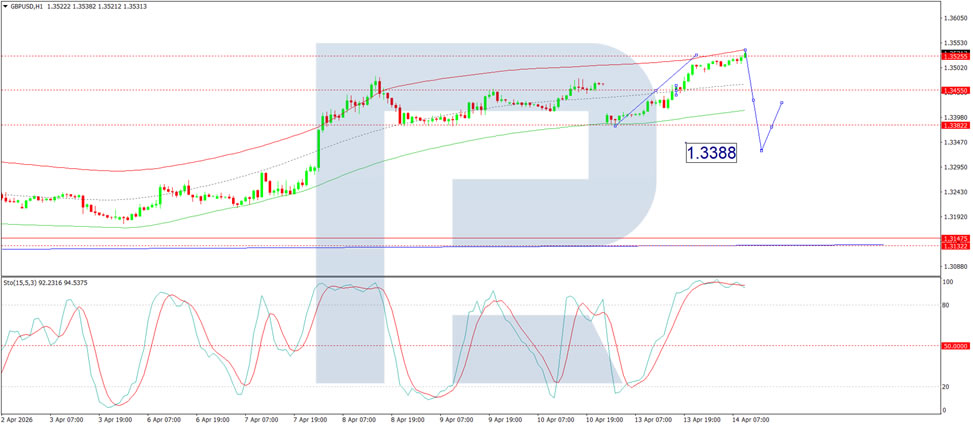

Technical Analysis

On the H4 GBP/USD chart, the market is forming a wide consolidation range around the 1.3333 level, currently extending up to 1.3535. A decline to 1.3333 is expected in the near term. Following the completion of this correction, a new consolidation range is likely to form. An upside breakout would open potential for a continuation wave to 1.3411, while a downside breakout would suggest further movement to 1.3120. Technically, this scenario is confirmed by the MACD indicator, whose signal line is above the zero level and pointing firmly downwards.

On the H1 chart, the market formed a compact consolidation range around the 1.3455 level and, with an upside breakout, completed a wave structure to 1.3535. The start of a decline towards the 1.3388 level is now expected. Technically, this scenario is confirmed by the Stochastic oscillator, with its signal line above the 80 level and pointing firmly downwards towards 20.

Conclusion

GBP/USD has found support as markets appear to have largely priced in the latest geopolitical escalation following failed US-Iran talks. Trump's threat to block the Strait of Hormuz has sent oil prices above 102.00 USD per barrel, intensifying inflationary concerns and shifting expectations towards tighter Bank of England policy, with at least one rate hike now priced for 2026. While sterling has shown resilience, the broader outlook remains clouded by risks related to the energy market. Technical indicators suggest a near-term pullback is likely, but the pair's direction will ultimately depend on whether geopolitical tensions continue to escalate or show signs of easing.

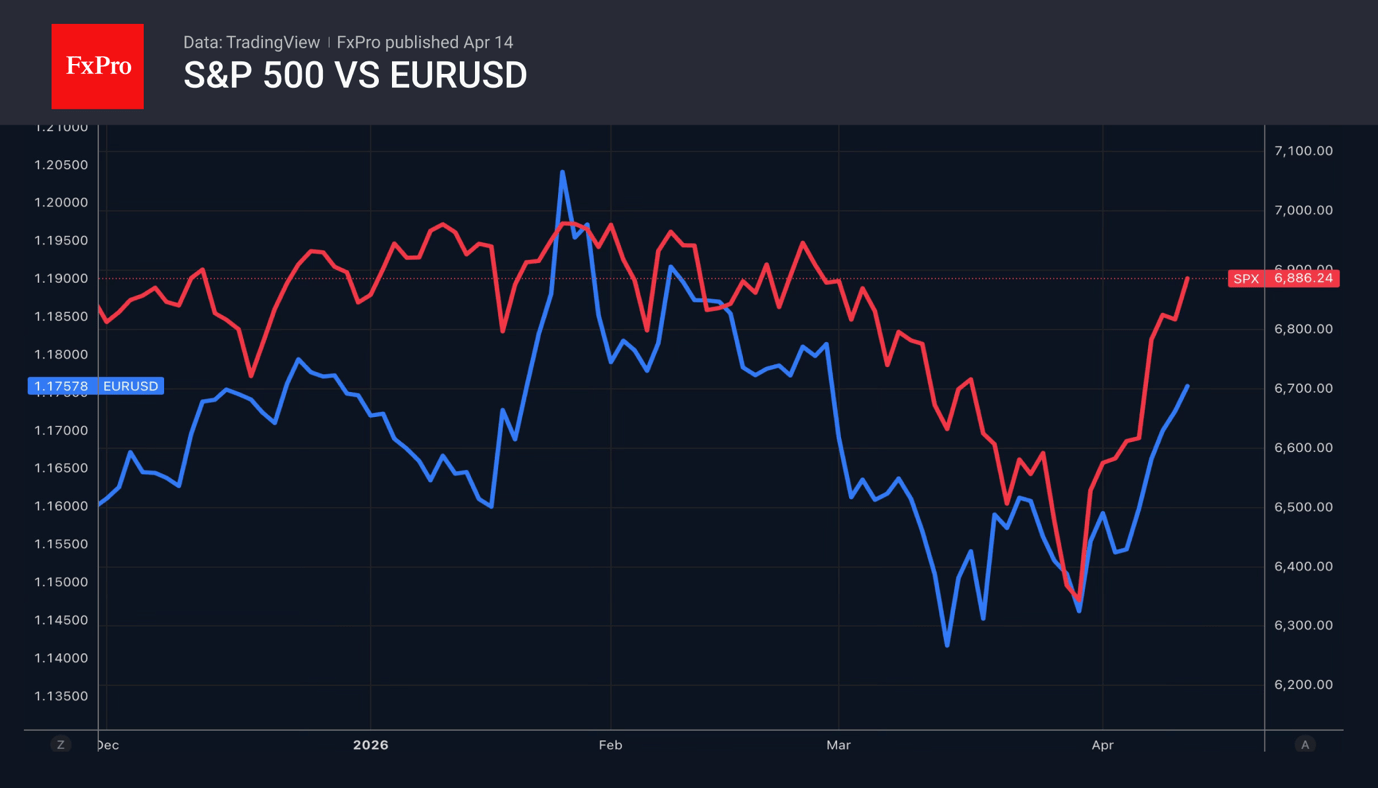

Markets Return to Pre-War Levels

- The S&P 500 and the pound are trading higher than before the conflict in the Middle East.

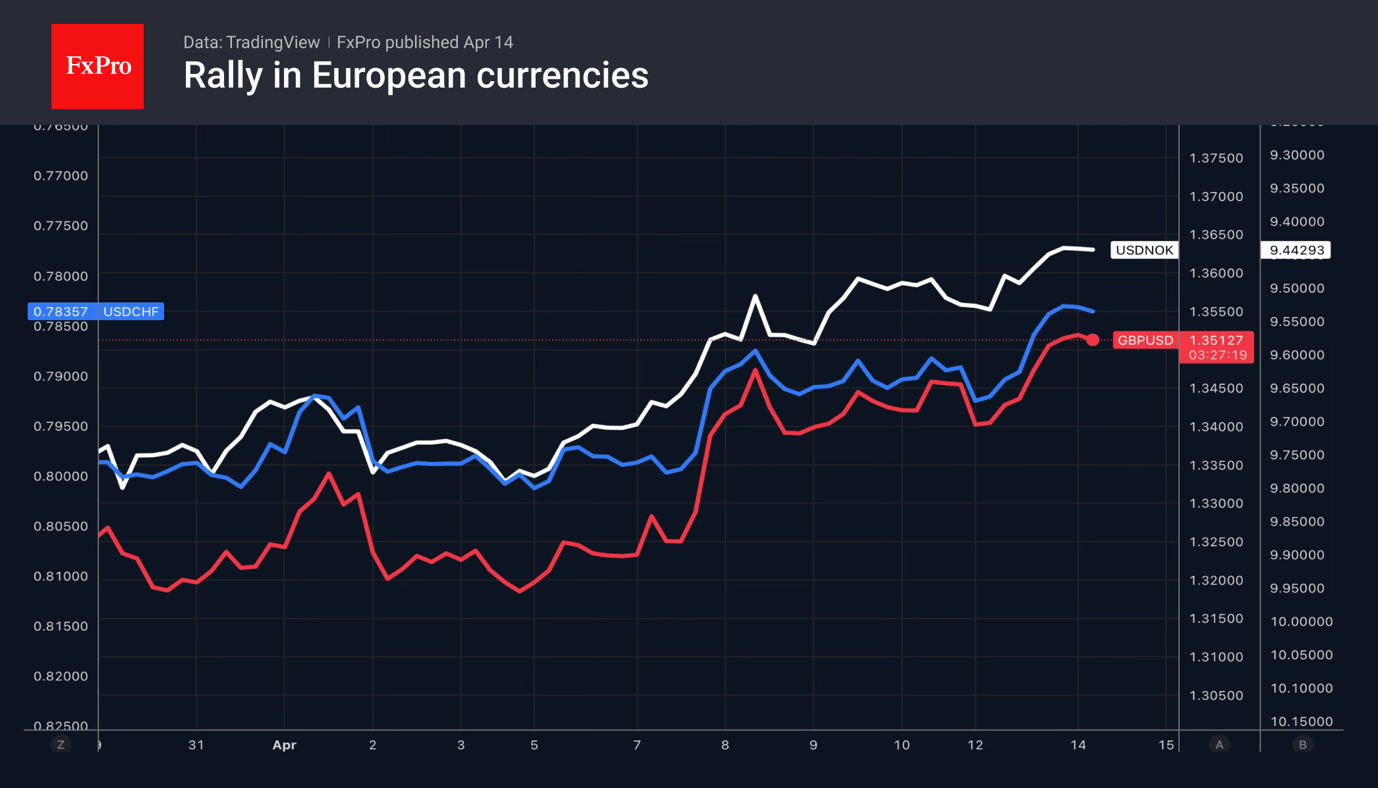

- European currencies are steadily regaining the ground lost in March.

Markets are tired of geopolitics. The S&P 500 has returned to pre-war levels on expectations of a strong first-quarter earnings season and undervalued fundamentals. Oil has not risen as much as it might have amid news of a breakdown in US-Iran talks. The US dollar is no longer able to capitalise on its safe-haven status. Investors are latching onto positive news from the Middle East and ignoring the negative. In such conditions, a recovery of the EURUSD to the 1.1800 region, near where trading took place in February, appears justified.

Donald Trump, keen to see stock indices rise, is trying the hardest of all. The president claims he has received a call from Iran, and that the Iranians want to strike a deal. Then he asserts that the right people in Tehran are not averse to returning to the negotiating table. Pakistan is making titanic efforts to resolve the differences. China is ready to offer its assistance in achieving peace in the Middle East. Iran itself notes that a compromise has been reached with the US on various aspects.

Markets are more inclined to believe in a de-escalation of the conflict than in a ceasefire breach and renewed bombing in the region. This optimism is driving the EURUSD higher. Even more so as the US blockade of the Strait of Hormuz represents a de-escalation of the confrontation, compared to active military operations.

Despite the uncertainty, hopes for peace in the Middle East are growing, allowing speculators who have built up net long positions in the US dollar to 14-month highs to wind them down. The unwinding of greenback positions is in full swing, adding momentum to EURUSD buying.

Other European currencies are also performing strongly. The pound has returned to pre-war levels, whilst the Swiss franc and Swedish krona are very close to doing so. The Norwegian krone is poised to hit its highest level since June 2022.

Gold has recovered quite quickly. Investors are restoring their share in their portfolios, which had fallen due to the need to meet margin requirements on equities. Consequently, the rise in the S&P 500 is also supporting demand for risk assets, including precious metals.

Natural Gas: Key Support Amid Renewed Escalation

A key development on 13 April was the start of a naval blockade of Iranian ports, a direct consequence of the collapse of negotiations in Islamabad on 12 April. The blockade covers all vessels entering and leaving Iranian ports in the Persian Gulf and the Gulf of Oman. Around 20% of global natural gas trade passes through the Strait of Hormuz, and the renewed escalation has once again heightened risks to global LNG supplies. European TTF has previously reacted with sharp widening spreads during earlier flare-ups, while the Asian JKM benchmark also remains sensitive to regional disruptions.

Against this backdrop, natural gas as an asset class is caught between two opposing forces: a geopolitical risk premium is providing price support at the global level, while a structural supply surplus — record production, accelerated injections into storage, and an unusually warm spring in the Northern Hemisphere — is weighing on prices from a fundamental perspective.

Technical picture

On the daily chart of XNGUSD, the move from the December 2025 high near 5.200 remains downward but structurally uneven: the sequence of interim highs and lows does not form a classic trending impulse. Volatility is compressing, and each rebound is shorter than the previous one, indicating a gradual loss of selling momentum as price approaches a key support level. Quotes are now trading close to the psychological 2.600 level, which has acted as an important reference point since late 2024.

The volume profile shows a Point of Control (POC) in the 3.150–3.200 range, where the bulk of trading activity is concentrated. This zone acts as the first major barrier to any recovery. The 3.400 level remains the next significant resistance above.

The RSI with Moving Averages reads 34 / 40 / 42, with all three metrics remaining below the neutral 50 level and the moving averages pointing lower, signalling continued downside pressure.

Summary

Natural gas prices are approaching the key psychological level of 2.600, the lower boundary of a consolidation range that has been in place since late 2024, while the blockade of Iranian ports keeps global energy markets in a state of heightened uncertainty. The RSI with Moving Averages remains below the neutral threshold across all three readings.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

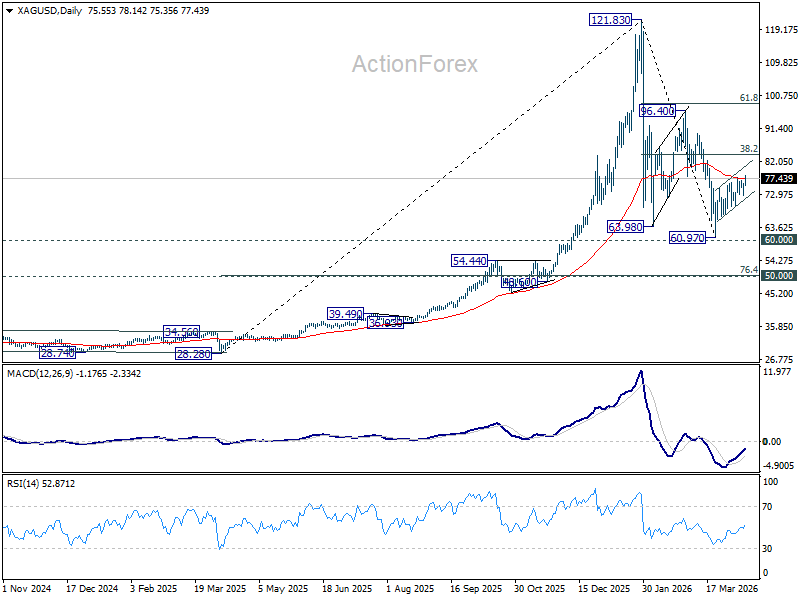

Silver (XAG/USD) at a Crossroads: Bullish Breakout Meets Overbought Momentum

- Silver (XAG/USD) has broken above a multi-month bearish trendline.

- The short-term target for bulls is the psychological $80.00 level, with $75.00 confirmed as key support.

- Overbought momentum indicators on multiple timeframes suggest caution and patience for a pullback to support may be warranted.

Daily Timeframe: Confronting a Multi-Month Bearish Trendline

The daily chart for Silver (XAG/USD) presents a fascinating technical battleground. After a period of significant volatility earlier in 2026, the price action has stabilized into a recovery phase that is now testing a major structural hurdle.

The Trendline Constraint: The primary focus on the daily is the long-term descending trendline (navy blue) originating from the highs of late January. Price is currently attempting a sustained breakout above this line, which has historically acted as a ceiling for upside momentum.

Moving Average Confluence: Silver is currently trading above its 200-day MA (yellow). However, the 100-day MA (purple) remains above current prices, with a daily candle close above a sign that the long-term bull trend remains very much intact.

Support and Resistance: The psychological level of $75.00 has shifted from resistance to support. To the upside, the next major target for bulls is the 80.00 handle, followed by the technical resistance zone at 82.16.

Momentum: The RSI is currently just above the 50 neutral level, suggesting that the bullish momentum may be returning.

Silver (XAG/USD) Daily Chart, April 14, 2026

Source: TradingView.com (click to enlarge)

H4 Timeframe: Bullish Momentum Gains Traction

Moving down to the H4 chart, the bullish narrative becomes more pronounced. We are seeing a classic stair-stepping pattern of higher highs and higher lows.

Breakout Confirmation: The H4 chart shows a decisive break above the 75.00 horizontal level. This area is now bolstered by the fact that price continues to hold above immeidate dynamic support provided by the 100-day MA.

SMA Alignment: The MAs on the H4 are beginning to tilt to the upside with the 200-day MA just resting above current prices. A break above this 200-day MA at 78.46 will reinforce the bullish narrative and bring 80.00 level and beyond into focus.

Indicator Outlook: The RSI on the H4 is holding steady near 59.55, indicating that there is still plenty of room for price appreciation before reaching extreme overbought conditions on this timeframe.

Silver (XAG/USD) Four-Hour Chart, April 14, 2026

Source: TradingView.com (click to enlarge)

H1 Timeframe: Tactical Upside Grind

The H1 chart highlights a very clean intraday trend. The metal has spent the last several sessions grinding higher, guided by its short-term moving averages.

Immediate Support: The 75.35 level (100-day MA) is the immediate line in the sand for intraday traders. As long as price holds above this level, the "buy the dip" mentality remains the dominant play.

Price Targets: The immediate target is the 78.00 psychological level, with a clear path toward the $80.00 resistance if the current momentum persists.

Divergence Watch: While the price is making higher highs, the RSI is starting to show signs of exhaustion. This may lead to a minor retracement back toward the 75.00 - 75.50 zone before the next leg higher.

Silver (XAG/USD) One-Hour Chart, April 14, 2026

Source: TradingView.com (click to enlarge)

Silver is currently in a "Show Me" phase. The breakout above the daily descending trendline is a significant technical milestone, but it requires a daily close above 77.00 to confirm that the bears have truly lost control.

The Bullish Play: Bulls will be looking for a successful retest of the 75.00 area. If price can hold this level on a pullback, the next logical objective is the 80.00 psychological resistance. A break there opens the door for a move toward the 82.00 - 83.00 region.

The Bearish Play: For the bears to regain the upper hand, they need to force a "fakeout" scenario where price dives back below the descending trendline and the 75.00 support. A move back below 74.00 would invalidate the current bullish setup and suggest a return to the 70.00 support zone.

Key takeaway: The path of least resistance is currently to the upside, but with oscillators reaching overbought levels on multiple timeframes, patience for a "value entry" near support may be rewarded over chasing the current breakout.