Sample Category Title

GBP/JPY Daily Outlook

Daily Pivots: (S1) 214.95; (P) 215.37; (R1) 215.84; More...

Intraday bias in GBP/JPY remains on the upside for the moment. Current up trend should target 61.8% projection of 199.04 to 214.98 from 209.58 at 219.43. On the downside, below 214.56 minor support will turn intraday bias neutral again first.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 204.47) holds, even in case of another deep pullback.

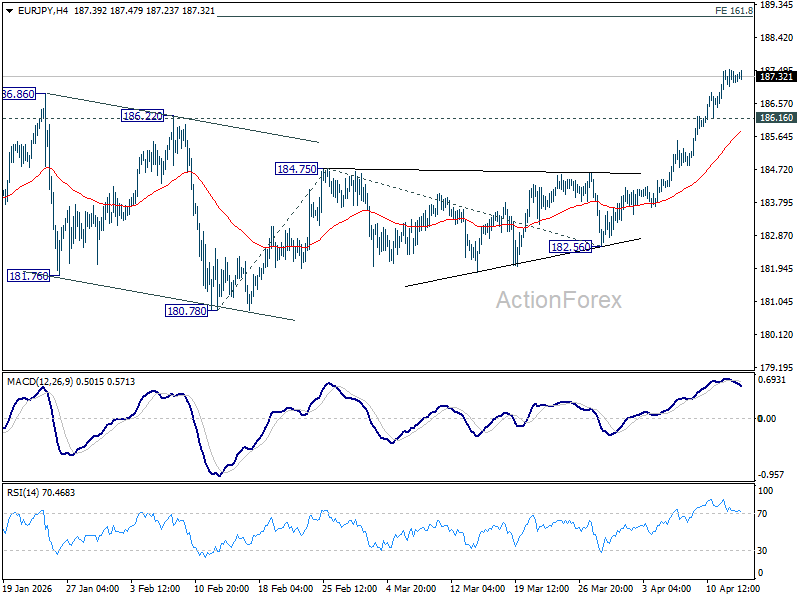

EUR/JPY Daily Outlook

Daily Pivots: (S1) 187.05; (P) 187.32; (R1) 187.57; More...

Intraday bias in EUR/JPY remains on the upside for the moment. Current up trend should target 161.8% projection of 180.78 to 184.75 from 182.56 at 188.98 next. On the downside, below 186.16 minor support will turn intraday bias neutral first. But near term outlook will stay bullish as long as 184.75 resistance turned support holds, in case of retreat.

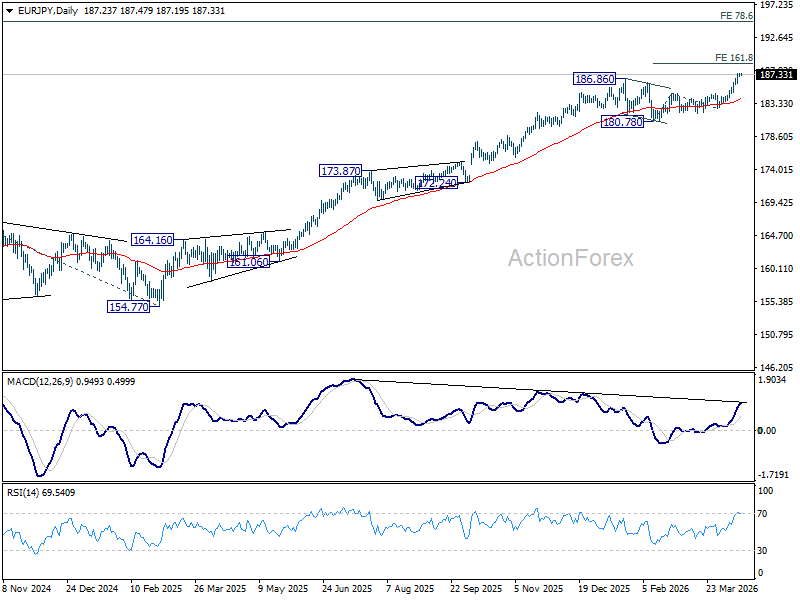

In the bigger picture, up trend from 114.42 (2020 low) in in progress and should be ready to resume. Next target is 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next. For now, medium term outlook will stay bullish as long as 175.41 resistance turned support holds, even in case of deeper pullback.

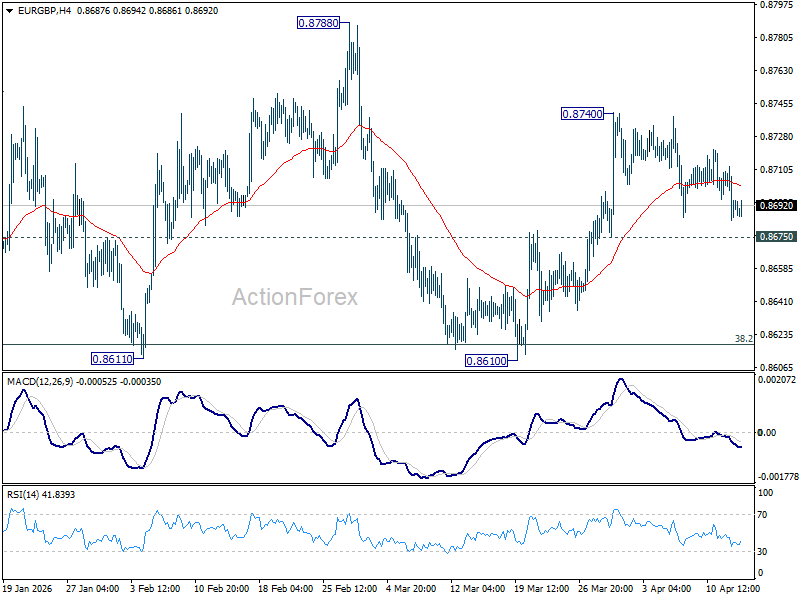

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8681; (P) 0.8699; (R1) 0.8712; More…

Intraday bias in EUR/GBP remains neutral as consolidation pattern from 0.8740 is still extending. Further rise is mildly in favor as long as 0.8675 support holds. Break of 0.8740 will resume the rebound from 0.8610 to 0.8788 resistance. However, firm break of 0.8675 will turn bias back to the downside for retesting 0.8610 low instead.

In the bigger picture, strong support was seen again from 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Break of 0.8788 resistance will argue that larger rise from 0.8221 might be ready to resume through 0.8863 (2025 high). Nevertheless, sustained trading below 0.8618 should confirm bearish reversal, and bring deeper fall to 61.8% retracement at 0.8466 at least.

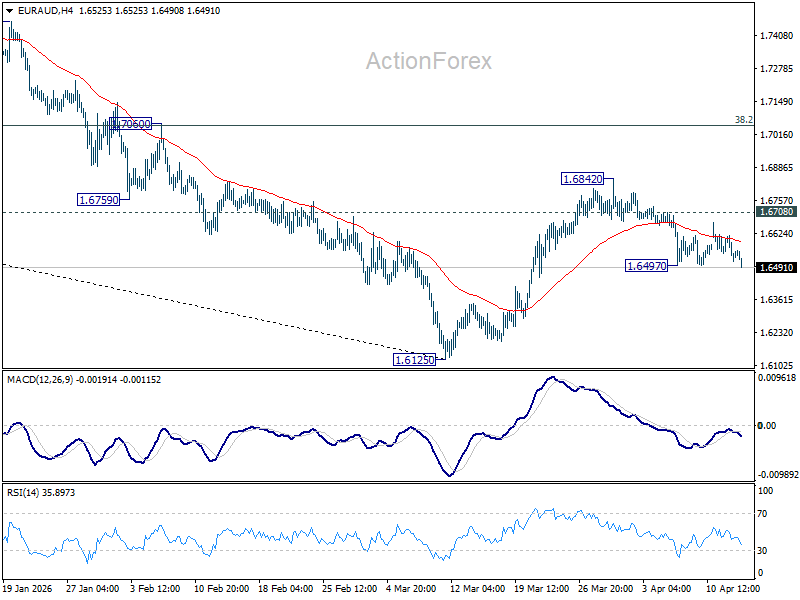

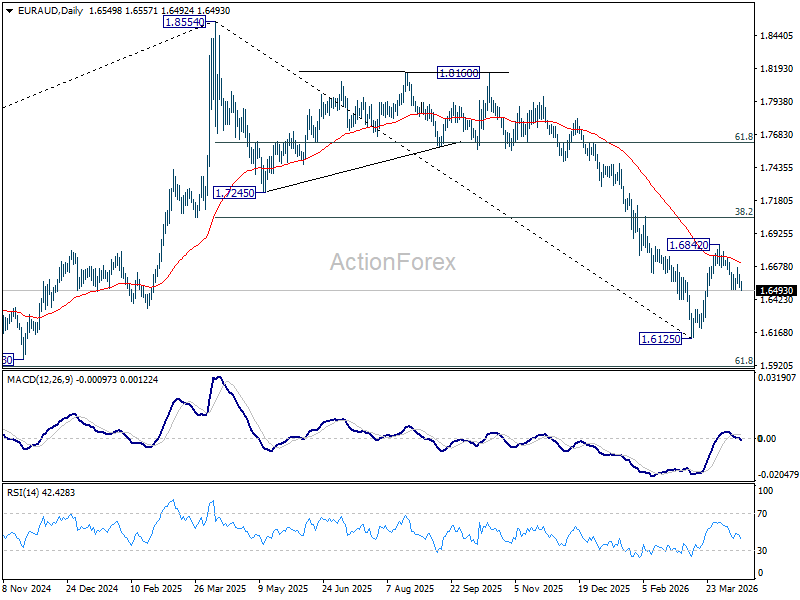

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6507; (P) 1.6562; (R1) 1.6609; More...

Intraday bias in EUR/AUD is back on the downside with breach of 1.6497 temporary low. Fall from 1.6842 is resuming and should target a retest on 1.6125 low. On the upside, above 1.6667 minor resistance will turn intraday bias neutral again first.

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7163) holds, even in case of strong rebound.

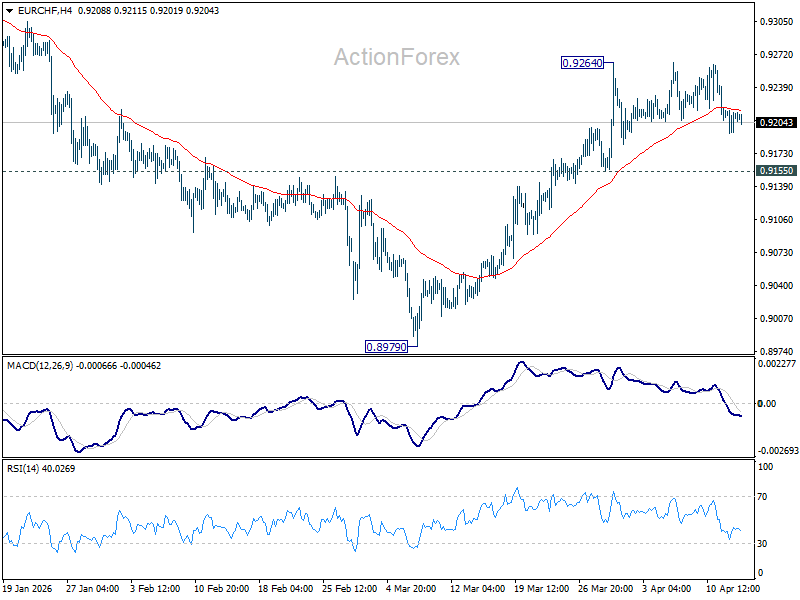

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9198; (P) 0.9209; (R1) 0.9224; More....

EUR/CHF is still extending the consolidation pattern from 0.9264 and intraday bias remains neutral. Further rise is expected with 0.9155 support intact. Firm break of 0.9264 will resume the rebound from 0.8979 to 0.9394 resistance next. However, break of 0.9155 will turn bias back to the downside for deeper pullback.

In the bigger picture, considering bullish convergence condition in W MACD, a medium term bottom should be in place at 0.8979. Sustained trading above 55 W EMA (now at 0.9281) will add more credence to this case. Further break of 0.9394 resistance will pave the way to 0.9660 resistance next. However rejection by the 55 W EMA will set up another fall through 0.8979 low at a later stage.

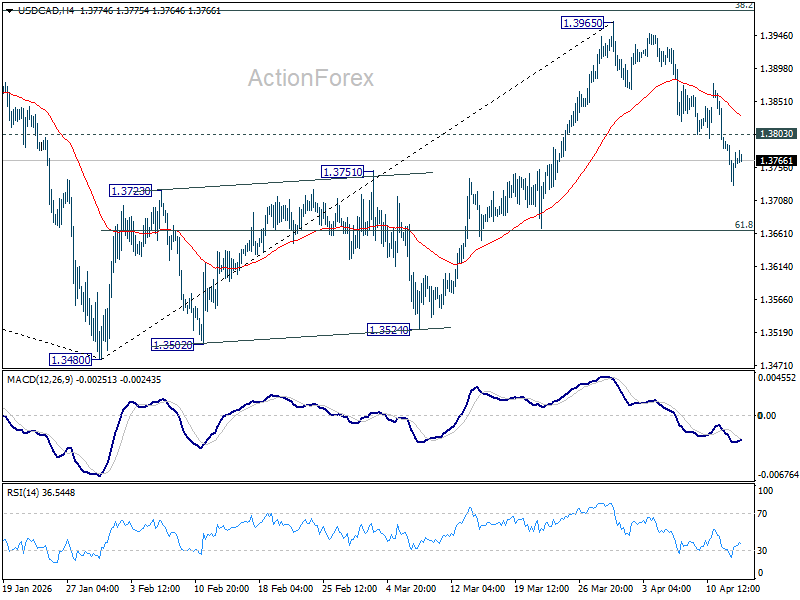

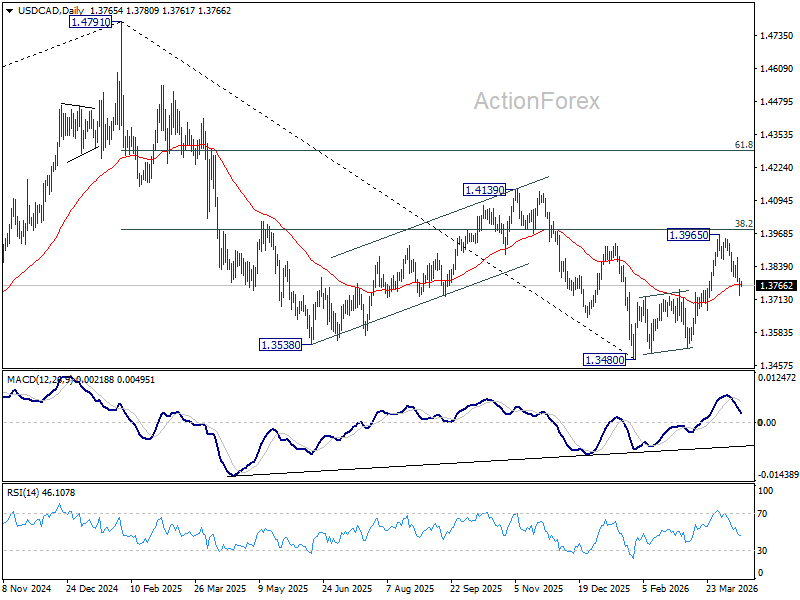

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3733; (P) 1.3766; (R1) 1.3801; More...

USD/CAD's fall from 1.3965 is in progress and intraday bias stays on the downside for 61.8% retracement of 1.3480 to 1.3965 at 1.3665. Decisive break there will extend the decline from 1.3965 to retest 1.3480 low. On the upside, above 1.3803 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already. Further break of 1.4139 will confirm and bring retest of 1.4791 high.

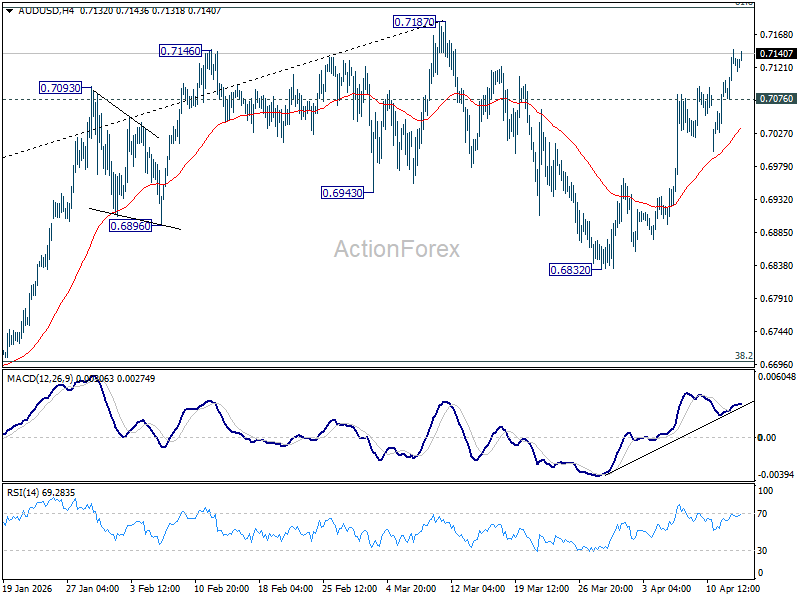

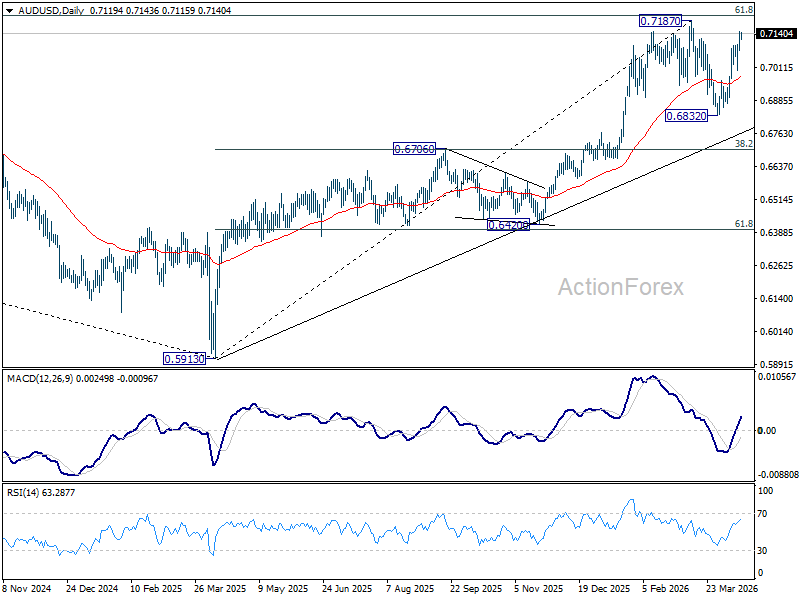

AUD/USD Daily Report

Daily Pivots: (S1) 0.7085; (P) 0.7116; (R1) 0.7157; More...

AUD/USD's from 0.6832 is in progress and intraday bias stays on the upside for retesting 0.7187 high. Strong resistance could be seen there on first attempt. Below 0.7076 minor support will turn intraday bias neutral first. Meanwhile, decisive break of 0.7187 will confirm larger up trend resumption.

In the bigger picture, as long as 0.6706 cluster support holds, rise from 0.5913 (2024 low) should still be in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). However, firm break of 0.6706 will dampen this bullish case, and bring deeper fall back to 0.6420 support, and possibly below.

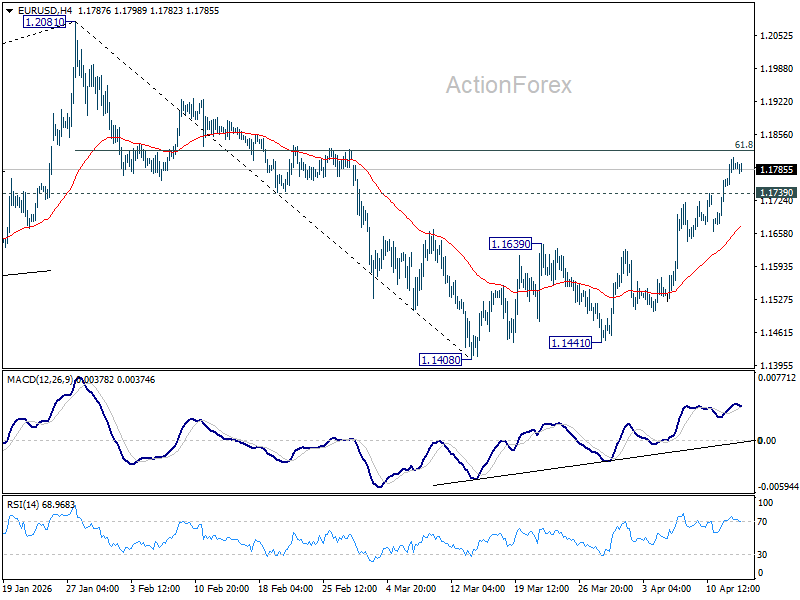

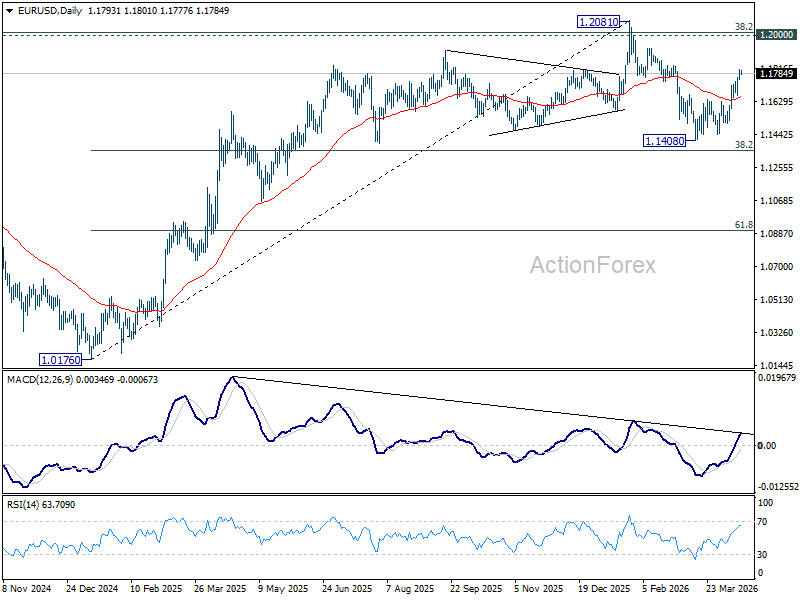

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1763; (P) 1.1788; (R1) 1.1820; More….

Intraday bias in EUR/USD remains on the upside for the moment. Decisive break of 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will extend the rally from 1.1408 to retest 1.2081 high. On the downside, below 1.1739 minor support will turn intraday bias neutral first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1513). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

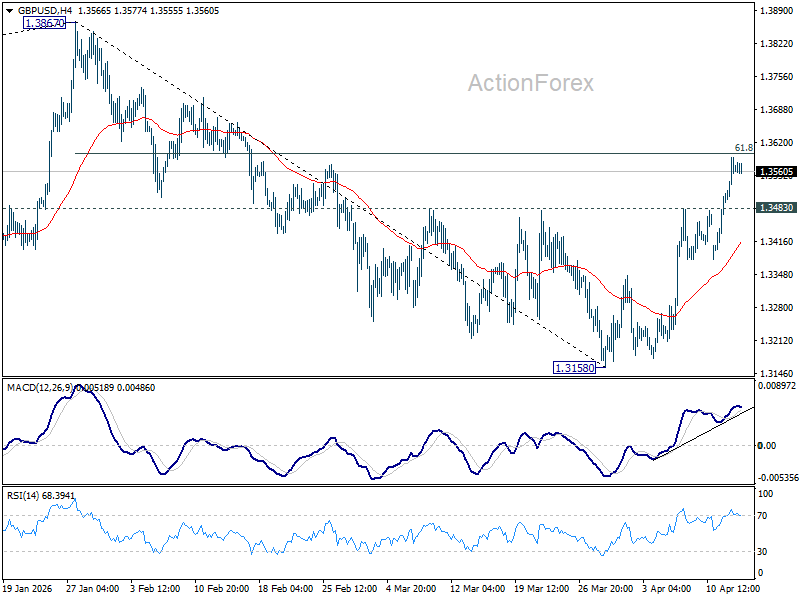

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3512; (P) 1.3551; (R1) 1.3605; More...

Intraday bias in GBP/USD remains on the upside at this point. Firm break of 61.8% retracement of 1.3867 to 1.3158 at 1.3596 will extend the rise from 1.3158 to retest 1.3867 high. On the downside, below 1.3483 minor support will turn intraday bias neutral first.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

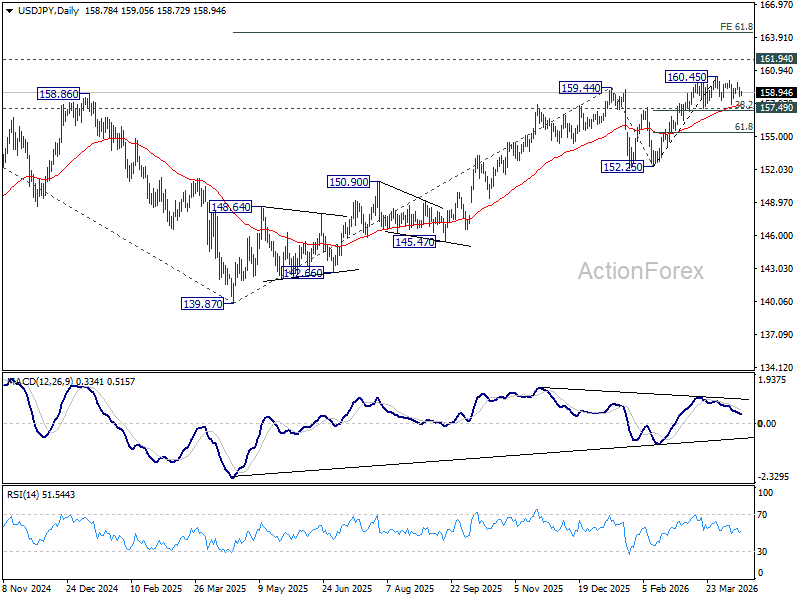

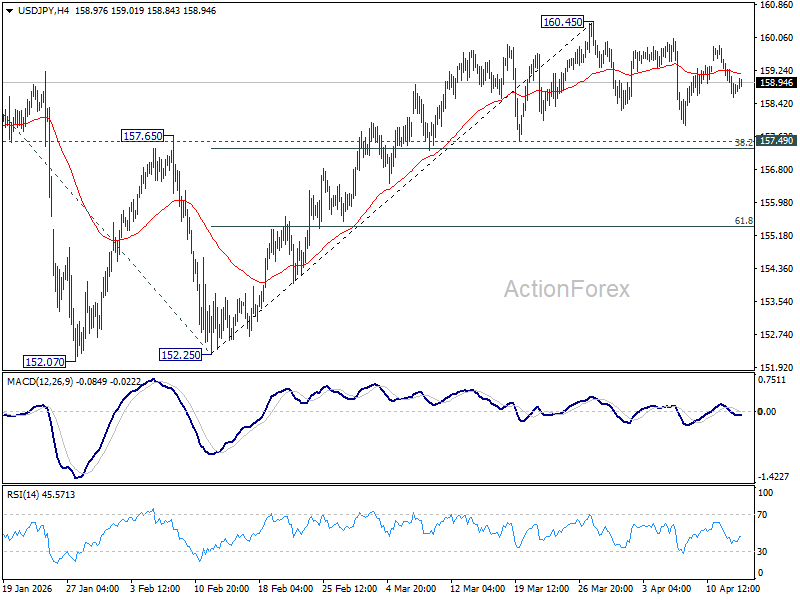

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.43; (P) 158.98; (R1) 159.36; More...

USD/JPY is still extending consolidations from 160.45 and intraday bias remains neutral. Outlook will stay bullish as long as 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) holds. On the upside break of 160.45 will target a retest on 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 155.24) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.