Sample Category Title

AUD/USD Pressures Resistance, Breakout Could Trigger Surge

Key Highlights

- AUD/USD started a fresh increase above 0.7000.

- A key bullish trend line is forming with support at 0.6980 on the 4-hour chart.

- GBP/USD extended gains above the 1.3500 resistance.

- WTI Crude Oil prices are under pressure and might test $92.

AUD/USD Technical Analysis

The Aussie Dollar remained supported above 0.6920 against the US Dollar. AUD/USD gained bullish momentum for a move above 0.6980 and 0.7000.

Looking at the 4-hour chart, the pair settled above the 0.7040 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). A high was formed at 0.7102, and the pair is now consolidating gains.

Immediate support is seen near 0.7045 or the 23.6% Fib retracement level of the upward move from the 0.6859 swing low to the 0.7102 high. The first key support sits at 0.7000 and the 200 simple moving average (green, 4-hour).

The next key area of interest might be near 0.6980. There is also a key bullish trend line forming with support at 0.6980. The trend line is close to the 50% Fib retracement level of the upward move from the 0.6859 swing low to the 0.7102 high.

A close below 0.6980 might push the pair toward the 100 simple moving average (red, 4-hour) at 0.6969. Any more losses could initiate a fresh move to 0.6920.

On the upside, the pair faces resistance at 0.7100. The first major resistance sits at 0.7120. The main resistance could be 0.7180. A close above 0.7180 could open the doors for gains above 0.7200. In the stated case, the bulls could aim for a move to 0.7320.

Looking at Oil, the price started a fresh decline, and the bears could soon aim for a new monthly low below $92.

Upcoming Key Economic Events:

- Fed's Goolsbee speech.

- Fed's Barr speech.

- Fed's Barkin speech.

- Fed's Collins speech.

- Fed's Paulson speech.

Critical Crossroads: USD/CHF Tests Key Support at 0.78285. Is a Bounce to 0.7900 Up Next?

- The overall bias for USD/CHF has turned decidedly bearish in the short to medium term following a significant rejection at the 0.80000 psychological handle.

- The pair is currently testing a critical support level at 0.78285, which is described as the "line in the sand" for bulls.

- Lower timeframes show extreme oversold readings on the RSI, hinting at a possible short-term corrective bounce toward resistance around 0.79000 before a potential continuation of the downside.

Daily Timeframe: Structural Shift at Key Resistance

On the Daily chart, USD/CHF has faced a significant rejection at the 0.80000 psychological handle. This level has proven to be a formidable barrier, leading to a sharp reversal that has now brought the pair back down to a critical inflection point.

Trend Dynamics: The pair has been trending higher since early 2026, supported by an ascending trendline (dark navy). However, the recent price action shows a decisive break below the 200-day MA (yellow) and the 100-day MA (blue), signaling a shift in medium-term momentum.

Key Support/Resistance: We are currently testing the 0.78285 - 0.78344 support zone. This area aligns with previous structural pivots and is bolstered by the 200-day MA (black) sitting just above at 0.78279.

Indicator Outlook: The RSI is trending lower but has not yet reached oversold territory, suggesting there may be further room for the downside if the current support level fails to hold on a daily candle closing basis.

USD/CHF Daily Chart, April 13, 2026

Source: TradingView (click to enlarge)

H4 Timeframe: Momentum Accelerating Downward

The H4 chart provides a clearer view of the recent "waterfall" sell-off. The bearish momentum accelerated once the pair lost the confluence of the moving averages near the 0.79400 region.

Moving Averages: The 50, 100, and 200 MAs are now fanning out above the current price, acting as dynamic resistance. The Death Cross (50 MA crossing below the 100/200 MA) is about to take place as well.

Price Action: We see a series of Lower Highs and Lower Lows. The current candle is hovering right at the 0.78285 horizontal support. A sustained break here would likely target the ascending trendline from the daily chart, currently located around the 0.77200 area.

RSI: On this timeframe, the RSI is deep in oversold territory (~30.99), which could hint at a short-term corrective bounce or consolidation before the next leg lower.

USD/CHF Four-Hour Chart, April 13, 2026

Source: TradingView (click to enlarge)

H1 Timeframe: Intraday Exhaustion?

The hourly chart highlights the sheer velocity of the move during the April 13th session. The pair dropped nearly 100 pips in a straight line without a significant retracement.

Current State: The price is "hugging" the bottom of the range at 0.78345. Note the RSI on the H1 is at 26.76, indicating extreme intraday exhaustion.

Tactical Levels: * Immediate Resistance: If we see a "mean reversion" play, the first hurdle is the 0.78932 (50 MA) followed by the 0.79000 level.

Support: The 0.78285 level remains the "line in the sand" for bulls on an intraday and larger timeframe basis..

USD/CHF One-Hour Chart, April 13, 2026

Source: TradingView (click to enlarge)

Comprehensive Outlook

The overall bias for USD/CHF has turned decidedly bearish in the short to medium term following the failure at 0.80000.

Bullish Scenario: For the bulls to regain control, we need to see a strong rejection at the current 0.78285 support, followed by a daily close back above the cluster of moving averages at 0.79400.

Bearish Scenario: If the pair fails to hold 0.78285, the path of least resistance points toward the long-term ascending trendline near 0.77500 - 0.77200. Given the oversold RSI readings on the lower timeframes, a minor retracement to retest broken support (now resistance) at 0.79000 would offer a higher-probability entry for trend followers.

Key takeaway: Keep a close eye on the 0.78285 level; a daily candle close below this mark could trigger a fresh wave of selling toward the YTD lows.

WTI (Oil) drops back below $100 After US-Iran Talks Set to Resume – Oil Dynamics and Intraday Analysis

- Oil drops below $100 as US-Iran talks are set to resume on Thursday

- After gapping higher to $105 at the globex open, anxiety shot up but the negotiations talks helped a significant correction back to $98.

- Traders have been looking for direction since

- Exploring an in-depth Technical Analysis of the commodity

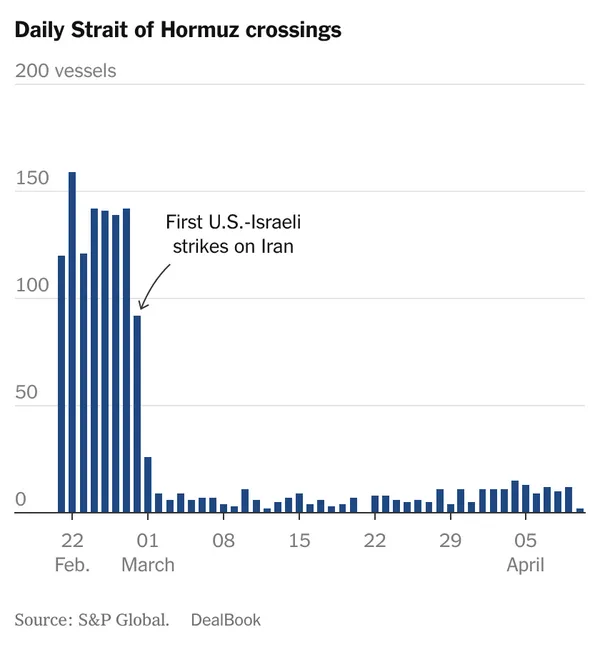

Energy markets started the week with a violent whip-saw, reminding traders that the geopolitical risk premium is still the ultimate driver of price action.

The weekly session kicked off with a massive spike in anxiety after the initial failure of US-Iran talks around the weekend.

WTI Crude gapped aggressively higher at the Globex open, flashing up to the $105 handle as geopolitical uncertainty quickly set back.

This came particularly prominent from the fact that the Strait of Hormuz did not see any form of improvement in its flows since the truce came in effect last Tuesday.

Strait of Hormuz Sea Traffic since February 22 – Source: NYT

However, that panic was short-lived.

Sentiment shifted violently on the news that the high-stakes US-Iran diplomatic talks are officially set to resume this Thursday after fears of a potential early end to the two-week ceasefire.

The prospect of renewed negotiations triggered a massive wave of profit-taking and short-selling, dragging the commodity in a significant correction straight back down to the $98 level.

Since that brutal retracement however, the market has hit a wall of indecision, with prices now stuck between $96 and $104 since last Thursday.

Traders are currently sitting on their hands, desperately looking for a clear sense of direction as they await Thursday's closed-door developments.

The fundamental picture is entirely hostage to the headlines, meaning the charts are more important than ever for mapping out risk.

With volatility now stalling, let's explore a few key charts and scenarios for WTI (US) Oil to prepare for potential breakout levels.

US Oil Intraday Time-frame Analysis

WTI Daily Chart

WTI Oil Daily Chart – April 13, 2026. Source: TradingView

Recent daily candles haven't shown anything but a cloudy picture, with numbers of daily up and down gaps, and hesitation inside candles in between (implying dead momentum).

The RSI is now back right at the 50.00 neutral level, which also corroborates with a more hesitant picture.

A positive for Markets is the fact that WTI Crude has now officially stopped trending higher, at least for now – This is shown by the fact that bulls could not hold the war bull channel after the morning tumble.

But to maintain their high stakes rallies, they will need to see crude persist on the longer run below $100.

With the daily chart not offering such a clear view, let's take a closer look.

WTI 4H Chart and Technical Levels

WTI Oil 4H Chart – April 13, 2026. Source: TradingView

It only is the second time since the beginning of the War that WTI breaches its 4H 50-period moving average – A sign of further progress but this still fails to translate into more downside ahead.

Even the intraday charts aren't displaying any type of clear pattern.

When you can't trust individual candlesticks and trendlines, the only technical areas to rely on are supply and resistance levels (Support and resistances).

The $98 to $100 zone acts as a significant magnet for action and will retain this role as long as the situation remains unclear.

- Breaking $98 would point to $93 and form a new range in this area.

- Bouncing above $100 would on the other hand point to $106 and form an upper range in this zone.

- These levels are expected to remain until a proper peace deal is reached.

WTI Technical Levels:

Resistance Levels

- 4H 50-period MA (~$103.96)

- $106 to $108 June 2022 Resistance

- $110 psychological level

- 2022 and War highs $117 to $120

Support Levels

- $98 to $100 Major Pivot (testing)

- War Support Pivotal $93.00 to $95

- $87 to $90 mini-Support (4H 200-period MA)

- 2025 Highs Key Support $78 to $80

- Pre-War Support $63.80 to $64

WTI 1H Chart and Technical Levels

WTI Oil 1H Chart – April 13, 2026. Source: TradingView

Oil is now stuck at the $98 level as traders await for further signals.

A sign of hesitancy that points to more rangebound action ahead is the fact that the RSI is already showing signs of rebounding close to overbought levels.

However, this could only point to a thinner $2 range to $100 as participants are still scrambling for further news.

The action could be stuck for the time being, but one important region to look at is Lebanon, with direct Israel-Lebanon talks supposed to start tomorrow (and will be of great assistance to any peace deal).

Safe Trades!

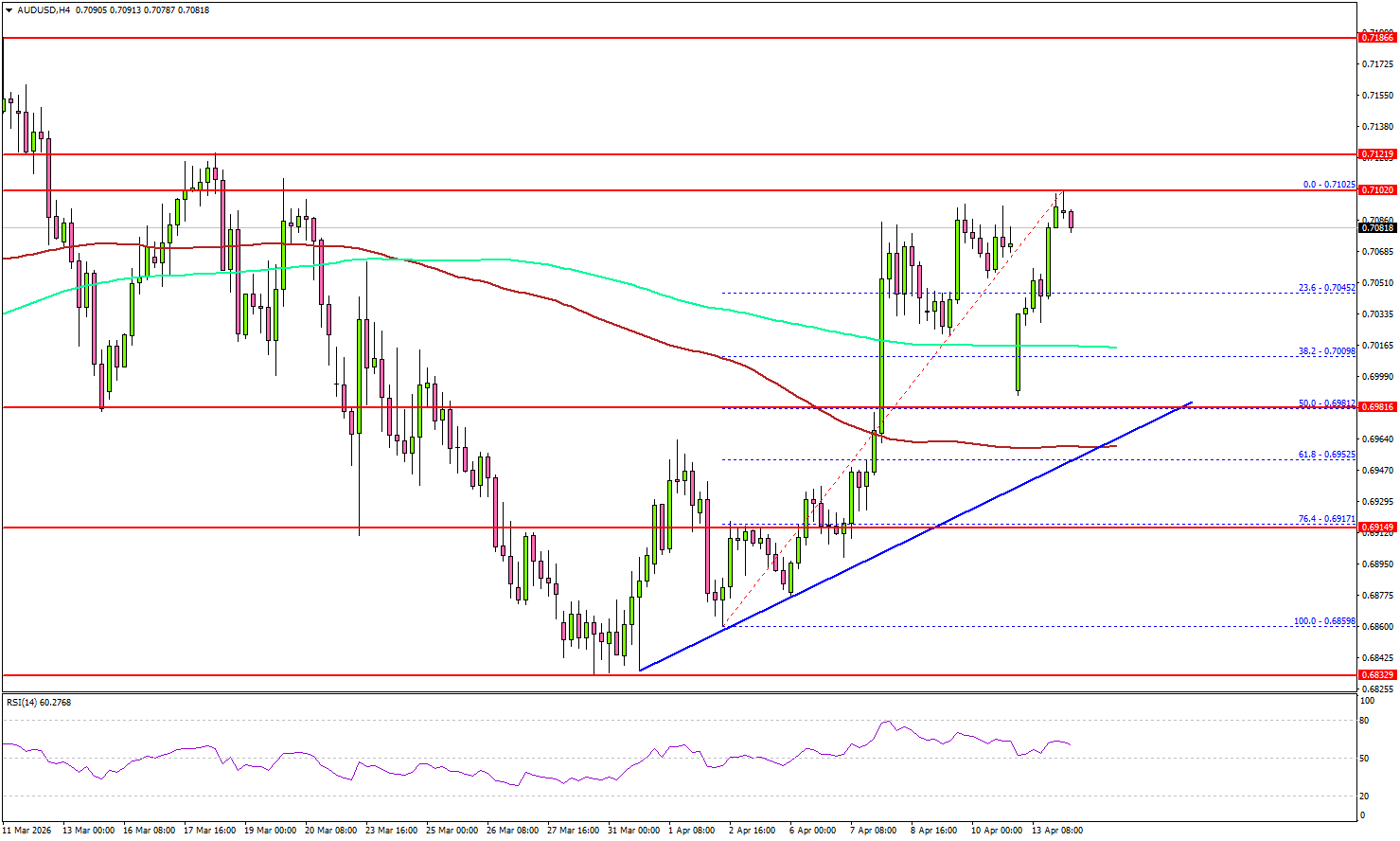

AUD/USD Technical Analysis: Bulls Regain Control as Key Psychological Level Holds

- The AUD/USD technical outlook is decidedly bullish, with the path of least resistance to the upside.

- The pair successfully broke out above the primary descending trendline on the Daily chart.

- Bullish momentum is reinforced by a "Golden Cross" formation on the 4-hour chart.

- The 0.7130 level stands as the next major hurdle for the bulls.

The Australian Dollar has undergone a significant shift in momentum over the past few sessions. After a period of corrective price action, AUD/USD appears to be finding its feet, buoyed by a successful defense of critical support zones and a breakout of descending trendline resistance.

The Daily Chart: The Big Picture

On the daily timeframe, AUD/USD remains in a broad constructive phase despite the volatility seen through February and March. The pair recently came within a whisker of the 100-day MA printing a low around the 0.6833 handle.

The most notable development on this timeframe is the breakout above the primary descending trendline (black line) originating from the year-to-date highs. After consolidating near the 0.7000 psychological handle, price action is now challenging the 0.7080 resistance. A daily close above this level would clear the path for a retest of the 0.7130 mark before the YTD highs at 0.7187 comes into focus.

AUD/USD Daily Chart, April 13, 2026

Source:TradingView.com

The H4 Chart: Bullish Momentum Accelerates

Shifting to the 4-hour chart, the bullish narrative is reinforced by the "Golden Cross" formation, where the 50-day MA has crossed above the 100 and 200-day MAs. This technical signal often precedes sustained trending moves.

We can see a clear "V-shaped" recovery from the late March lows. The pair has successfully flipped the 0.7000 level from resistance to support. Currently, the RSI (Relative Strength Index) is hovering near the 66 level; while this indicates strong bullish momentum, it suggests there is still some "headroom" before the pair reaches overbought territory, allowing for further upside in the short term.

AUD/USD Four-Hour Chart, April 13, 2026

Source:TradingView.com

The H1 Chart: Intraday Precision

The 1-hour chart provides a granular look at the recent breakout. After a brief period of consolidation between 0.7034 and 0.7080, the pair has just printed a strong bullish candle, piercing the upper boundary of this range.

The intraday moving averages (50, 100, and 200) are perfectly fanned out in a bullish alignment, suggesting that any minor pullbacks are likely to be met with fresh buying interest. The immediate focus for intraday traders will be the 0.7080 level; as long as price holds above this on a retest, the next logical target is the swing high at 0.7130.

Key Levels to Watch

- Resistance: 0.7080, 0.7130, 0.7150

- Support: 0.7034, 0.7000 (Psychological), 0.6913

AUD/USD One-Hour Chart, April 13, 2026

Source:TradingView.com

The RSI across multiple timeframes is not yet flashing "exhaustion" signals, though the Bearish Divergence labels on the H1 indicator suggest that the slope of the ascent might moderate. Traders should watch for a potential "throwback" to the 0.7034 area for a lower-risk entry if the current breakout stalls.

In short, the technical outlook for AUD/USD is decidedly bullish. The confluence of a trendline breakout on the Daily, a moving average crossover on the H4, and a range breakout on the H1 suggests that the path of least resistance remains to the upside. The 0.7130 level stands as the next major hurdle for the bulls.

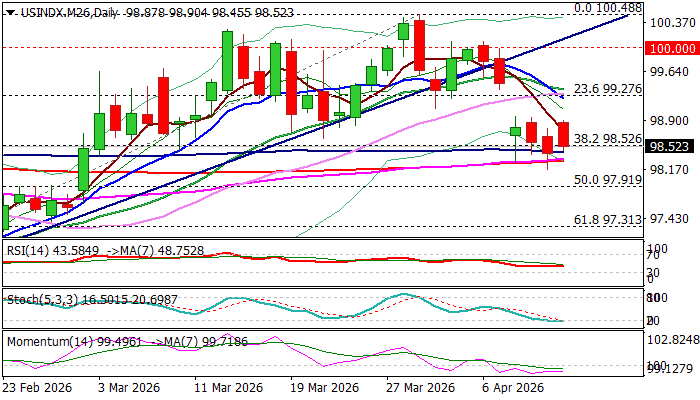

USD Index – Downside Remains at Risk Despite Fresh Signals of War Escalation

The dollar opened higher on Monday, following fresh signs of escalation in the Middle East after US/Iran peace talks failed, but lacked strength to maintain gains, reversing a good part of its overnight advance during European and early US trading.

Although greenback played a role of leading safe-haven asset during the five-week war, last week’s sharp drop on optimistic outlook and easing bets for tighter Fed monetary policy, have dented its firm stance.

Also, today’s quick reversal of overnight’s gains, warns that traders might be changing their perception after disappointing actions of the US military, as well as frequent and conflicting messages from President Trump.

This may add to building pressure on dollar, as near-term action is weighed by last week’s large bearish candle (the dollar was down 1.6% for the week), while technical picture on daily chart is weakening (14-d momentum remains in the negative territory / multiple bear-crosses of 5/10/20/30 DMAs).

However, negative signals remain challenged by strong supports at $98.42/30 zone, consisting of converged100 / 55 / 200 DMAs (including 55/200DMA golden cross) and top rising and thickening daily Ichimoku cloud.

Fresh weakness needs to register a clear break of these supports to signal continuation of the bear-leg from $100.48 (new 2026 high, posted on Mar 31) and open way for deeper correction of $95.35/$100.48 rally (the latest pullback has so far retraced around 38.2% of the move).

Recent tops at $98.95zone formed a lower platform which currently acts as initial but significant resistance, with potential break higher to still require stronger upside action and fill last week’s gap ($99.45/$98.45), to neutralize near-term bearish structure.

Res: 98.80; 98.95; 99.23; 99.45

Sup: 98.42; 98.30; 97.91; 97.40

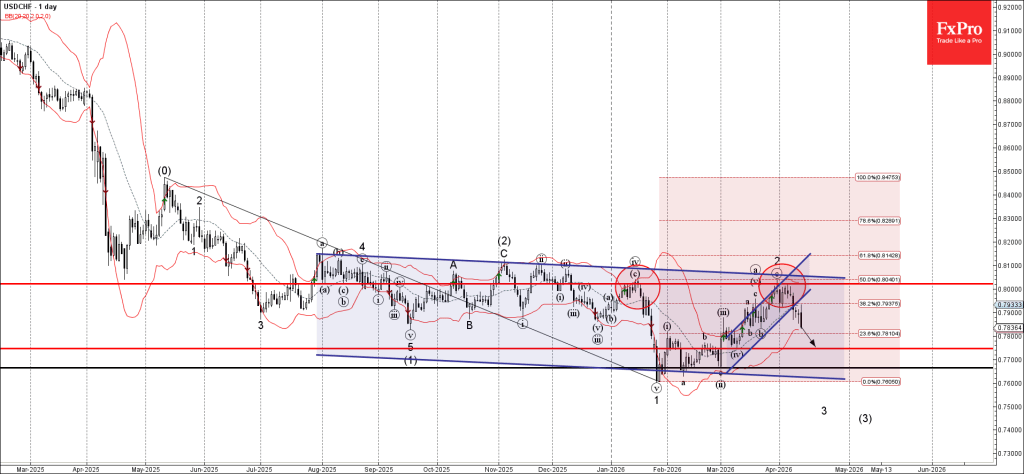

USDCHF Wave Analysis

USDCHF: ⬇️ Sell

- USDCHF broke daily up channel

- Likely to fall to support level 0.7745

USDCHF currency pair recently broke the daily up channel from the start of March – which accelerated the active impulse wave 3.

The active impulse wave 3 belongs to the intermediate impulse wave (3) from the start of November.

Given the clear daily downtrend, USDCHF currency pair can be expected to fall further to the next support level 0.7745 (low of the previous correction iv).

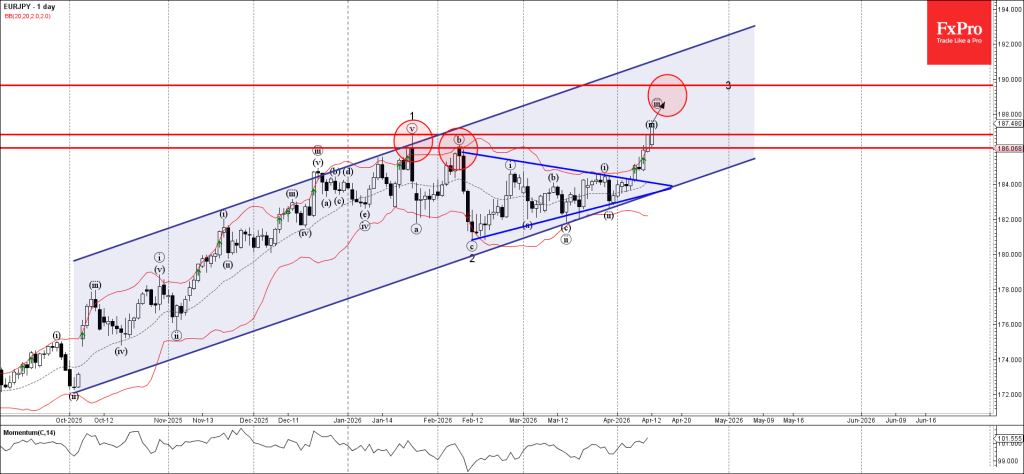

EURJPY Wave Analysis

EURJPY: ⬆️ Buy

- EURJPY broke resistance zone

- Likely to rise to resistance level 190.00

EURJPY currency pair recently broke through the resistance zone between the resistance level 186.0 (top of wave b from February) and resistance level 186.85 (top of wave 1 from January)

The breakout of this resistance zone accelerated the active impulse waves iii and 3.

Given the clear daily uptrend, EURJPY currency pair can be expected to rise to the next resistance level 190.00 (target price for the completion of the active impulse wave 3.).

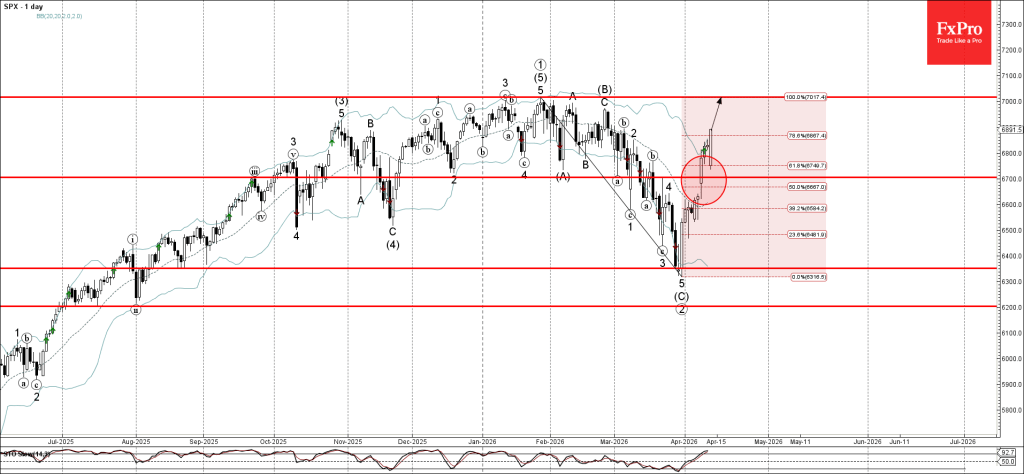

S&P 500 Wave Analysis

S&P 500: ⬆️ Buy

- S&P 500 broke the resistance level 6700.00

- Likely to rise to resistance level 7000.00

S&P 500 index recently broke the resistance level 6700.00 – which was set as the upward target in our earlier forecast for this index.

The breakout of the resistance level 6700.00 coincided with the breakout of the 50% Fibonacci correction of the previous ABC correction 2 from January.

S&P 500 index can be expected to rise further to the next round resistance level 7000.00, which formed monthly Double Top in January.

Eco Data 4/14/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Mar | 3.10% | 0.70% | ||

| 00:30 | AUD | Westpac Consumer Confidence Apr | -12.50% | 1.20% | ||

| 01:30 | AUD | NAB Business Conditions Mar | 6 | 7 | 6 | |

| 01:30 | AUD | NAB Business Confidence Mar | -29 | -1 | 0 | |

| 03:00 | CNY | Trade Balance (USD) Mar | 51.1B | 107.5B | 213.6B | |

| 04:30 | JPY | Industrial Production M/M Feb F | -2.00% | -2.10% | -2.10% | |

| 10:00 | USD | NFIB Business Optimism Index Mar | 95.8 | 98.6 | 98.8 | |

| 12:30 | USD | PPI M/M Mar | 0.50% | 1.20% | 0.70% | 0.50% |

| 12:30 | USD | PPI Y/Y Mar | 4.00% | 4.60% | 3.40% | |

| 12:30 | USD | PPI Core M/M Mar | 0.10% | 0.50% | 0.50% | 0.30% |

| 12:30 | USD | PPI Core Y/Y Mar | 3.80% | 4.20% | 3.90% | 3.80% |

| 23:01 | GBP |

| BRC Like-For-Like Retail Sales Y/Y Mar | |

| Actual | 3.10% |

| Consensus | |

| Previous | 0.70% |

| 00:30 | AUD |

| Westpac Consumer Confidence Apr | |

| Actual | -12.50% |

| Consensus | |

| Previous | 1.20% |

| 01:30 | AUD |

| NAB Business Conditions Mar | |

| Actual | 6 |

| Consensus | |

| Previous | 7 |

| Revised | 6 |

| 01:30 | AUD |

| NAB Business Confidence Mar | |

| Actual | -29 |

| Consensus | |

| Previous | -1 |

| Revised | 0 |

| 03:00 | CNY |

| Trade Balance (USD) Mar | |

| Actual | 51.1B |

| Consensus | 107.5B |

| Previous | 213.6B |

| 04:30 | JPY |

| Industrial Production M/M Feb F | |

| Actual | -2.00% |

| Consensus | -2.10% |

| Previous | -2.10% |

| 10:00 | USD |

| NFIB Business Optimism Index Mar | |

| Actual | 95.8 |

| Consensus | 98.6 |

| Previous | 98.8 |

| 12:30 | USD |

| PPI M/M Mar | |

| Actual | 0.50% |

| Consensus | 1.20% |

| Previous | 0.70% |

| Revised | 0.50% |

| 12:30 | USD |

| PPI Y/Y Mar | |

| Actual | 4.00% |

| Consensus | 4.60% |

| Previous | 3.40% |

| 12:30 | USD |

| PPI Core M/M Mar | |

| Actual | 0.10% |

| Consensus | 0.50% |

| Previous | 0.50% |

| Revised | 0.30% |

| 12:30 | USD |

| PPI Core Y/Y Mar | |

| Actual | 3.80% |

| Consensus | 4.20% |

| Previous | 3.90% |

| Revised | 3.80% |

Sunset Market Commentary

Markets

In less than a week 1) an Iranian civilization was about to be wiped out 2) before Pakistani mediation resulted in a two-week ceasefire and the first high-level talks over the weekend only for the latter to 3) break down after 21 hours and bringing us de facto back to 1). After negotiations fell apart, the Trump administration announced its own Strait of Hormuz blockade - effective 4PM (our time) - to deprive Iran from its remaining oil revenue. The Middle East country responded by threatening regional ports if enemy-affiliated vessels try breaching its territorial waters. Trump afterwards upped the ante further by suggesting to go after critical infrastructure such as water and electricity plants, “which are very easy to hit.”

The market reaction to the latest developments is a kneejerk risk off one, but in a guarded manner. The ceasefire in theory is agreed to last until April 21, leaving still some (be it limited) time for de-escalation and diplomacy. News outlet Axios reported that Pakistan, Egypt and Turkey over the coming days will continue mediating with US and Iran and some negotiators, particularly from the Iranian side, kept the door open for further talks. Needless to say the situation is very unpredictable. In awaiting the outcome, stocks lose ground in Europe and the US. The likes of the EuroStoxx50 declines by 1%, Wall Street opens 0.3%-0.7% lower. Global yield curves bear flatten gently with rising oil (Brent back above $100) and gas (Dutch TTF futures +9%) driving rate hike bets. The market implied probability for an April ECB move rose from around a third to 45% with a cumulative 70 bps of rate increases priced in for 2026. German rates rise 2-3 bps, slightly underperforming vs swap and Treasuries. The latter lose minor ground, spurring 1 bp increases. UK gilts are the laggards with rates across the Channel adding 2.5-4 bps. FX investors favour the US dollar slightly over most global peers but gains are technically insignificant. DXY crawls towards the 99 barrier. EUR/USD struggles to maintain the 1.17 but is off the intraday lows. The Japanese yen is among the worst performers. A speech by BoJ governor Ueda (see below) has doused some of the lingering speculation for an April rate hike. USD/JPY is nearing the symbolically important 160 barrier again, EUR/JPY is even hitting new all-time highs. The Hungarian forint in CE space is surging towards the highest levels in four years, breaking through important resistance around EUR/HUF 367.7 (2023 HUF-highs) in the process. The move follows a landslide victory in yesterday’s elections by the pro-European Tisza party. It secured a two-third majority, giving it the power to rewrite the constitution and to some extend undo 16 years of Orban rule which often clashed with the European Commission. Hungarian (swap) rates drop almost 40 bps (!) with lower risk premia driving the move.

News & Views

The German government agreed on a €1.6bn fiscal package to contain fuel prices. Over a period of two months, the gasoline tax will be reduced by 17 cents per liter. Other, smaller, measures include a tax-free employer relief bonus of up to €1000, stricter antitrust oversight of fuel pricing and a potential tax or regulatory measures on oil companies’ excess profits. Earlier this spring, Spain (€5bn) , Italy (€3-4bn), Ireland (€1.6-1.8bn, Greece (€0.3-0.4bn) and France (€0.1-0.2bn) announced similar temporary relief measures. There’s some clear fragmentation between broad, consumer-heavy packages in Southern Europe and the more limit response in the likes of Germany and France which are either fiscally-constrained or wary of repeating huge subsidies like 4 years ago.

Japanese money markets reduced April rate hike bets by the Bank of Japan from 55% to 33% following a speech by BoJ governor Ueda read out by his deputy, Himono. He suggested that oil prices push up energy costs in the short term, but that their impact on underlying inflation is uncertain. “If the output gap worsens, that could weigh on underlying inflation. On the other hand, if rising crude oil prices heighten the public’s medium- and long-term inflation expectations, that could push up underlying inflation.” Given lingering uncertainty over the Middle East, the BoJ will scrutinize how future developments affect the outlook. While vigilance is necessary and core CPI is still on track to hit the 2% target, BoJ Ueda didn’t fully embrace the near-term rate hike scenario.