Sample Category Title

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1694; (P) 1.1729; (R1) 1.1795; More….

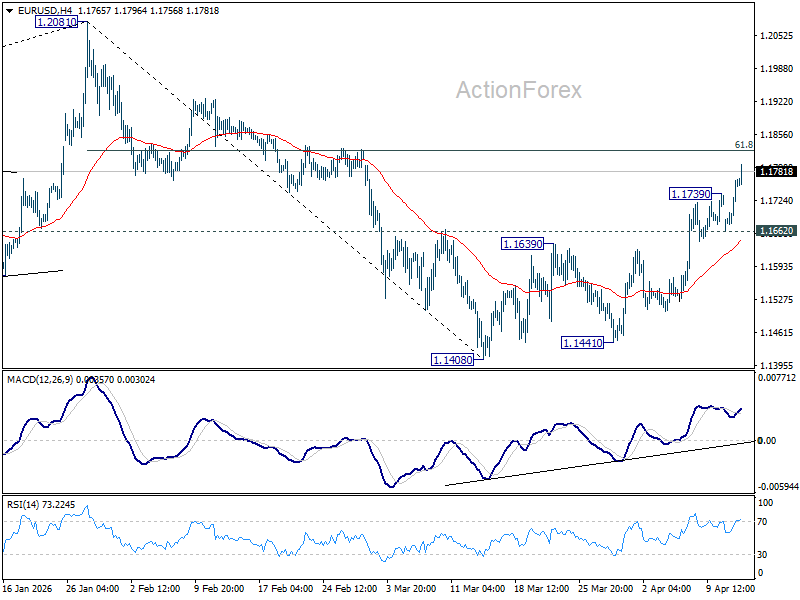

EUR/USD's rise from 1.1408 resumed after brief consolidations. Intraday bias is back on the upside for 61.8% retracement of 1.2081 to 1.1408 at 1.1824. Decisive break there will pave the way to retest 1.2081 high. For now, further rally will remain in favor as long as 1.1662 support holds, in case of retreat.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1513). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

European Currencies Advance Amid Shifting Geopolitical Outlook

The initial rise in EUR/USD and GBP/USD was driven by reports of a temporary ceasefire between the United States and Iran, which reduced demand for the US dollar as a safe-haven asset. However, over the weekend, reports emerged that negotiations had stalled, leading to a bearish gap at the start of the new trading week. Subsequently, rumours of a possible resumption of dialogue once again shifted market sentiment, restoring interest in risk-sensitive assets.

This supported a swift recovery in the euro and the pound, while also increasing pressure on the US dollar. Additional downside pressure on the dollar comes from declining Treasury yields and a reassessment of expectations regarding the Federal Reserve’s monetary policy, which continues to limit the upside potential of the US currency.

Market attention today will focus on upcoming macroeconomic releases from the euro area and the United States, including producer inflation (PPI), business activity data, and speeches from Federal Reserve officials. These factors may adjust current interest rate expectations and influence the dollar’s short-term trajectory.

EUR/USD

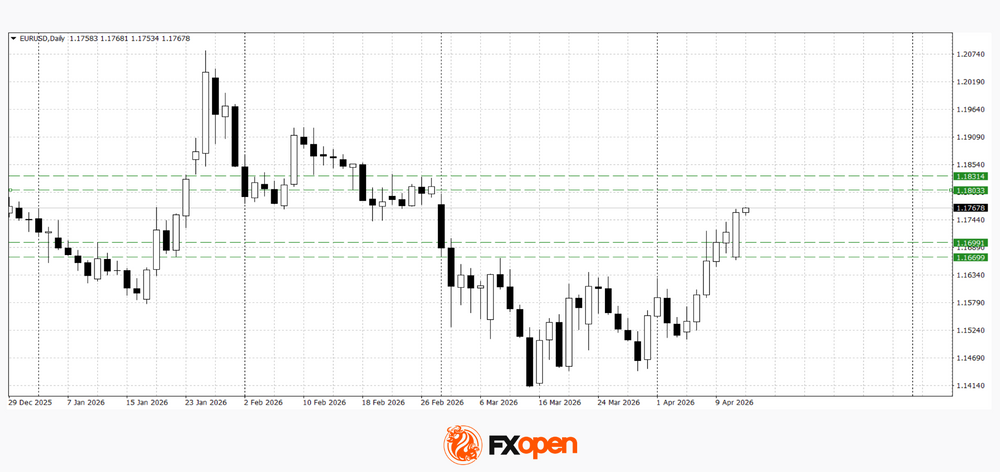

The pair continues to move higher following a breakout from last week’s consolidation range. The week opened with a price gap, but after a retest of support at 1.1660, the pair quickly recovered above 1.1700. Technical analysis suggests the potential for further gains towards the 1.1800–1.1830 area. However, any negative developments in US–Iran negotiations could trigger a sharp pullback towards 1.1700–1.1660.

Key events for EUR/USD:

- today at 10:00 (GMT+3): Spain HICP

- today at 15:30 (GMT+3): US Producer Price Index (PPI)

- today at 20:00 (GMT+3): speech by Bundesbank representative Balz

GBP/USD

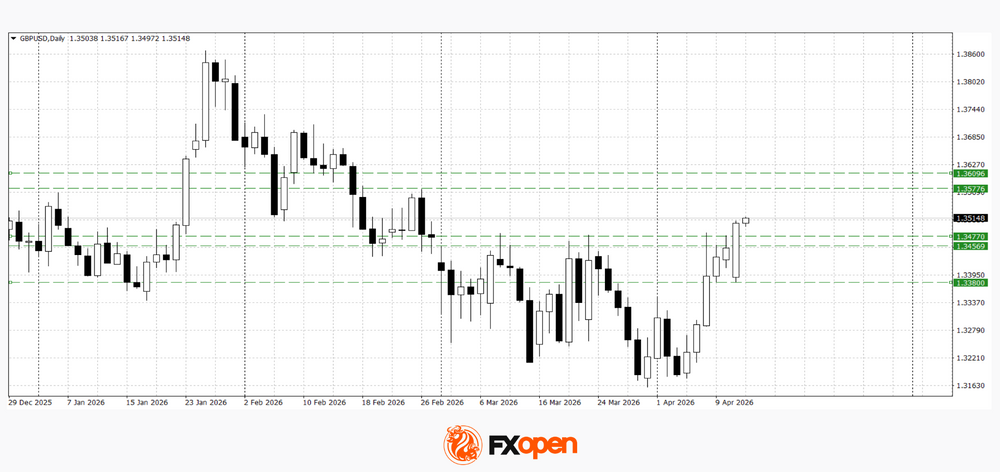

The pair is showing a similar pattern, largely mirroring the euro’s dynamics. Following the overnight gap, the price managed to break above last week’s highs and test key resistance at 1.3500. Technical analysis points to a possible move towards 1.3570–1.3600. In case of a pullback, a retest of recent levels near 1.3450–1.3470 is possible.

Key events for GBP/USD:

- today at 11:50 (GMT+3): speech by Bank of England MPC member Mann

- today at 19:00 (GMT+3): speech by Bank of England Governor Bailey

- today at 19:45 (GMT+3): speech by Federal Reserve Vice Chair for Supervision Michael S. Barr

Overall, European currencies maintain an upward bias amid an unstable geopolitical environment and declining US yields. However, the current rally remains highly sensitive to developments in the negotiation process, increasing the likelihood of short-term volatility. The next directional move in EUR/USD and GBP/USD will depend on both geopolitical signals and incoming macroeconomic data.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

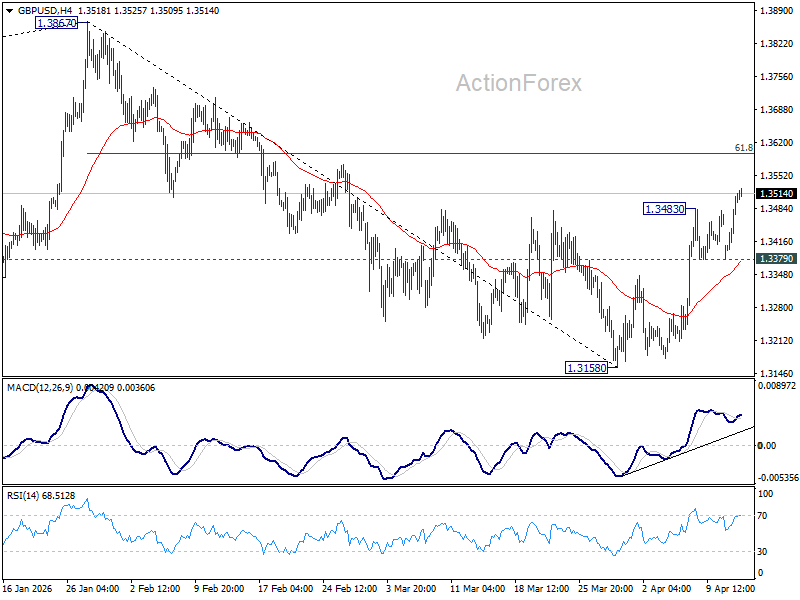

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3422; (P) 1.3466; (R1) 1.3551; More...

GBP/USD's rebound from 1.3158 resumed after brief consolidations. Intraday bias is back on the upside for 61.8% retracement of 1.3867 to 1.3158 at 1.3596. Firm break there will bring retest of 1.3867 high. For now, further rally will remain in favor as long as 1.3379 support holds, in case of retreat.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

Dollar Selloff Resumes as Markets Price Second Round of US-Iran Talks, War Premium Unwinds

Dollar is under broad selling pressure today, giving back its war premium as markets pivot back to diplomacy. Yesterday’s pessimism is already being unwound, with traders reassessing the outcome of the US-Iran talks in Islamabad. Rather than pricing a breakdown, markets are now positioning for continuation of negotiations.

The initial risk-off reaction was driven by the perceived failure of the talks and the subsequent US naval blockade targeting Iranian-linked shipping. That combination briefly pushed markets toward a defensive stance. But the narrative has now shifted.

US President Donald Trump signaled that diplomatic channels remain open, noting that appropriate people had reached out and that Tehran is still interested in a deal. This has reframed the weekend outcome as a pause rather than a collapse.

Reports that the two sides were “80% there” before hitting a wall have further reinforced this shift in sentiment. For markets, that figure provides a concrete basis to believe that a second round of talks is not only possible, but likely. The remaining gap—primarily around nuclear commitments—is seen as political rather than structural.

White House spokeswoman Olivia Wales clarified that while the "red lines" (no nuclear weapons) haven't moved, "engagement continues toward an agreement." This confirmed that the departure of J.D. Vance and the Iranian delegation from Islamabad was not a "walk out," but a "recess" to consult with their respective leadership.

Markets are pricing progress again—not a breakdown. This shift is visible across assets. Oil has stabilized rather than spiking and dipped back to around $100, equities are holding up, and Dollar is weakening as safe-haven demand fades. The war premium that drove yesterday’s moves is now being unwound.

As long as diplomacy remains alive—even if incomplete—the bias is toward further unwinding of the war premium. Markets are not waiting for a deal; they are pricing the path toward one. Until that path is clearly broken, Dollar is likely to remain under pressure.

In the currency markets, Dollar is now the worst performer of the week so far, followed by Yen, and then Aussie. Swiss Franc is the best, followed by Kiwi, and then Sterling. Euro and Loonie are trading in the middle of the pack.

In Asia, at the time of writing, Nikkei is up 2.30%. Hong Kong HSI is up 0.45%. China Shanghai SSE is up 0.43%. Singapore Strait Times is up 0.55%. Japan 10-year JGB yield is down -0.046 at 2.428. Overnight, DOW rose 0.63%. S&P 500 rose 1.02%. NASDAQ rose 1.23%. 10-year yield fell -0.020 to 4.297.

RBA’s Hauser Warns of ‘Central Banker’s Nightmare’ as Oil Shock Lifts Inflation, Hits Growth

RBA Deputy Governor Andrew Hauser warns that rising oil prices are delivering a “central banker’s nightmare,” with inflation climbing as growth risks build. With a potential income shock looming and policy uncertainty rising, the RBA faces a difficult balancing act. Read more.

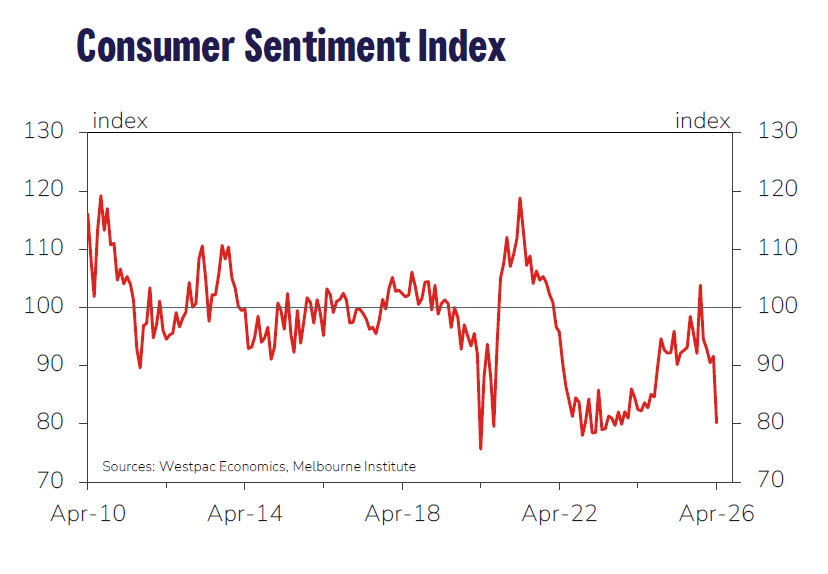

Australian Consumer Sentiment Plunges as Fuel Prices Surge, RBA Still Set to Hike

Australian consumer sentiment has dropped sharply to near crisis levels as fuel prices and rate hikes hit households. But with inflation still elevated, Westpac expects the RBA to raise rates again in May and continue tightening later this year, highlighting the growing tension between weaker demand and persistent price pressures. Read more.

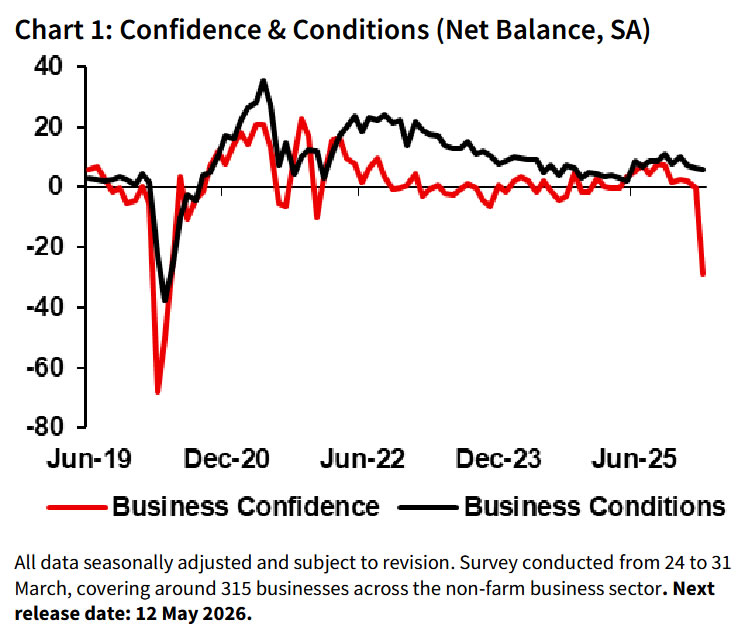

Australian NAB Business Confidence Plunges to -29 as Middle East Shock Hits

Australian business confidence has collapsed to GFC- and COVID-era levels as Middle East tensions hit sentiment, but activity is still holding for now. With cost pressures surging and price growth accelerating, the data highlights a growing tension between weakening outlook and rising inflation risks. Read more.

China Trade Signals Diverge as Weak Exports Meet Import Boom

China’s trade data showed a sharp split in March, with exports slowing to a five-month low while imports surged on commodity demand. Read more.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3422; (P) 1.3466; (R1) 1.3551; More...

GBP/USD's rebound from 1.3158 resumed after brief consolidations. Intraday bias is back on the upside for 61.8% retracement of 1.3867 to 1.3158 at 1.3596. Firm break there will bring retest of 1.3867 high. For now, further rally will remain in favor as long as 1.3379 support holds, in case of retreat.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

Headlines Around the Middle East Continue Determining Trading

Markets

The US started its own naval blockade of the Straight of Hormuz in an “open-for-all or close-to-all” policy. The move came after collapsed weekend talks between the US and Iran. Oil prices spiked higher at the start of yesterday’s trading, but the reaction in other asset classes was more guarded. Despite mutual military treats over the US decision, the fragile cease-fire still holds for now with a week to go to get parties back around the table or at least extend the cease-fire deadline allowing room for talks. Rumours suggested that back-channel talks are ongoing with Pakistan mediators. US President Trump also said that Iran reached out to his administration to still make a deal. This morning, the option of meeting again in-person on Thursday is floated either in Geneva or Islamabad. Markets eventually took these developments into stride, triggering intraday (risk-on) return action on the (risk-off) opening moves. In the case of Brent, the oil price (June contract) went from $94/b to $104/b before closing at $98. Dated Brent, for physical delivery this month rose back to $132.5/b as final prewar cargoes are set to unload in coming days. Arab officials are also pressing the US to drop its blockade over fears that Iran might eventually retaliate via Houthi rebels in Yemen (closing the Red Sea chokepoint, the Straight of Bab al-Mandeb). China is also entering the mix with Xi Jinping making 4 proposals on maintaining peace (peaceful coexistence) after meeting with the Abu Dhabi crown prince. Iran on its behalf, is asking Gulf states for financial compensation. European stock markets narrowed opening losses of around 1% into a -0.3% close while US indices extended their rebound by 0.6% (Dow) to 1.2% (Nasdaq). Sliding momentum in oil prices and positive US risk sentiment weighed on the dollar with EUR/USD closing at its best level since the start of the Middle East conflict (1.1759). The German and UK yield curves bear flattened with yields ending respectively 4.5 bps and 5.7 bps higher at the front end of the curve. This contrasts sharply with outperforming US Treasuries (2 to 3 bps down across the curve) as the intraday return action only really gained traction during the US session.

Headlines around the Middle East continue determining trading. Their volatile nature makes it hard to draw firm conclusions. Since Trump’s TACO, markets believe there’s a way out of the conflict. The IMF publishes its annual World Economic Outlook and Global Financial Stability Report. Afterwards, several central bankers are scheduled to speak including ECB President Lagarde and BoE Governor Bailey. Central bankers suggested they’ll use a more agile approach this time around to shield those upward inflation risks. They have the opportunity to give an update on their reaction functions. Even since the start of the ceasefire last week, money markets didn’t (completely) close the door on a near-term, April, rate hike especially in Europe because of elevated energy prices and the length of the shock. June action (and later) is more of a done deal.

News & Views

UK retail sales increased by 3.6% y/y in the period covering March 1 to April 4, the British Retail Consortium said in an early morning release. That’s above the 2.6% 12-month average. Food sales rose 6.8% and in-store non-food sales by 1.4%, both topping their 12-month averages as well. Online non-food sales rose by a marginal 0.1% compared to a 1% one-year average. The BRC CEO Dickinson said the early Easter provided a much-needed boost to food sales. Non-food performance was more uneven with categories such as computers, homeware and toys seeing robust demand but clothing and footwear were struggling. Dickinson noted the Middle East conflict had hit sales of travel-related goods and warned supply chains had already been damaged while rising costs (shipping, fertilizers, insurance and commodities) are pilling yet more pressure to already stretched retailers.

The Bank of France’s monthly poll showed the share of firms planning to raise prices this month had doubled from March. Some 23% of the 8500 companies surveyed are eying higher selling prices in April compared to the 11% that did so last month. Outgoing BdF governor and ECB policymaker Villeroy said its “obviously a point to follow carefully”, particularly because economic growth, for all the uncertainty lingering around, remains resilient. Selling price expectations by firms were one of the elements the ECB is “particularly attentive” to, chair Lagarde said at the March policy meeting. Villeroy added that the large majority expected the increase to be “moderate” only, suggesting limited transmission (for now at least) from higher energy prices.

Chinese Tanker Passes the Strait Despite Blockade

In focus today

Focus continues to be in the Middle East with the US blockade of Iranian ports taking effect yesterday afternoon.

For market events, the US releases PPI in the afternoon, where the upwards pressure from February is expected to continue. Markets estimate PPI to increase 1.1% m/m SA, an increase from the already surprisingly high February figures of 0.7% m/m SA, as cost pressures from the oil supply shock continues.

We also get NFIB's Small Business Survey from the US. The index fell for the second consecutive month in February to 98.8 and showed that both hiring plans and the number of job openings that companies were unable to fill had ticked lower already in February.

Today brings final Swedish inflation details. Last week's preliminary print showed lower inflation than expected in March, driven by lower services, food and energy prices. Food and energy prices were expected to fall, but they fell more than expected. As for services inflation, we believe that travel prices may have contributed to the unexpected decline. Today's details will hopefully provide further clarity on this. Furthermore, Riksbank first deputy Governor Aino Bunge will speak at 08.30 CET, discussing among other things the current economic situation.

Tonight, ECB's Lagarde will speak at 23:00 CET and Fed's Barkin will speak at 19:00 CET, where we will look for any signs of forward guidance.

Economic and market news

What happened overnight

In China, March exports increased 2.5% y/y (Jan/Feb: 21.8% y/y), sharply missing expectations of 8.3% y/y, while imports surprised to the upside and increased 27.8% y/y (Jan/Feb: 19.8%, cons: 11.2%). Note that the data is very volatile from month to month and exports were extraordinarily high in February alone at 39.6% y/y, so we expected to see some correction. However, the data still does not cover the full impact of the war in Iran and will likely weaken in the coming months.

What happened yesterday

In the Middle East, tensions escalated after the US 4pm CET deadline passed, with the US naval blockade of Iranian ports. US Central Command warned vessels that non‑compliance could lead to "interception, diversion and capture". Despite the blockade, a sanctioned Chinese tanker appears to have been the first vessel to transit the Strait this morning. In response to the US blockade, Iran threatened retaliation against ports in neighbouring Gulf states. While NATO allies declined to participate in the blockade in the evening, Trump later said to reporters that he will reveal details today about countries that are willing to help in the Strait. According to media reports, in weekend talks, the US proposed a 20-year suspension of all Iran's nuclear activity, while Iran would have conceded to 5 years. The fact that the two sides seem to be discussing the timeline, and apparently back-channel diplomacy has continued, we think a deal is possible but it will most likely require several rounds of talks, and meanwhile, the war could escalate.

In the Oil market, oil prices fell back below USD100/bbl overnight on the news that US and Iran might resume talks ahead of the end of the two-week ceasefire. Amid the additional US blockade of the Strait of Hormuz and an end to the Russian sanctions' waiver that allowed purchasing of oil from Russian tankers already at sea, the oil market seems optimistic that supply constraints will start to ease in the short term. The waiver that allowed purchasing of Iranian oil is set to expire on 19 April, but its significance is reduced due to the ongoing blockade in the Strait.

In Hungary, newly elected Peter Magyar on Monday pledged to "restore the rule of law, plural democracy and the system of checks and balances". With a two‑thirds majority in parliament, he said he would seek a constitutional amendment to cap prime ministerial terms at two.

Equities: What looked to be a muted opening in the futures markets turned out to be a solid rebound session in the US. The S&P 500 rose 1% and Nasdaq and the small-cap Russell closer to 1.5%. European and Nordic markets, which had started the day 1% lower, rebounded into the close, ending little changed.

One trigger for the rebound in equities, outside geopolitics, was the tech sector. US software rebounded a full 5.4% yesterday and companies like Oracle rallied 13%. Again, the trigger for this rebound is not entirely obvious; however, we think the approaching earnings season has something to do with it.

The US is expected to deliver another impressive quarter. Consensus looks for 12% earnings growth in Q1 for the S&P 500, with an impressive 9% coming from the top line. Tech is the standout, expected to print nearly 40% y/y earnings growth.

With this kind of stellar growth, we expect tech to come back into focus, but for different reasons than in the Q4 reporting season. AI monetization will admittedly be scrutinized, and consensus could be forced to lift its AI capex spend projections once again. All of this could admittedly trigger fear among investors, as has been the case over the last six months. However, the difference is that software multiples have already corrected to be closer to the market average. In fact, the global tech sector (including hardware) trades at more than a 15% discount to global industrials, although the former is expected to grow 40% in Q1 while industrials are barely expected to grow at all. Tech has seen massively lifted earnings estimates this year - 2026 earnings estimates are up 15% YTD - while industrials have seen no earnings upgrades at all. We think the surging earnings growth, on top of this unprecedented valuation discount, will capture investors' focus.

FI and FX: The broad USD slipped and risk appetite improved after Trump indicated that peace talks will resume. In the US session, EUR/USD rose from 1.170 to 1.176 and has flat-lined overnight. EUR/SEK lost close to ten figures yesterday, mainly in the European session and thus repeated the time-zone pattern seen over the last many weeks. The cross then held steady around 11.80. EUR/NOK also dropped yesterday but has erased some of the losses overnight amid weaker oil prices - Brent crude is back below USD 100 per barrel. Global bond yields are generally lower while Japan's 20y auction met strong demand fueling lower yields across the curve. US government bond yields are lower as well, where UST10y sits at 4.28%.

China Trade Signals Diverge as Weak Exports Meet Import Boom

China’s trade data showed a sharp divergence in March, with exports slowing while imports surged amid volatile commodity markets. Exports rose 2.5% yoy, down from prior strength and well below expectations of 8.6%, marking a five-month low. In contrast, imports jumped 27.8% yoy, far exceeding forecasts of 11.2% and recording the strongest growth since November 2021, pushing the trade surplus to USD 51.13 billion.

The weakness in exports points to softer external demand, while the surge in imports suggests front-loading of commodity purchases amid rising price risks. However, energy imports showed strain from geopolitical disruptions. Crude oil imports fell -2.8% yoy, while natural gas imports dropped -10.7% yoy to their lowest since October 2022. The Iran war and disruptions in the Strait of Hormuz have begun to affect flows, with some Chinese vessels reportedly delayed.

Officials acknowledged the challenging backdrop. Customs Vice Minister Wang Jun said global oil prices have seen “fierce fluctuation,” creating a “complex and severe” trade environment. With Middle East supply disruptions expected to weigh further on April imports, the data highlights rising uncertainty for China’s trade outlook, where external demand softness and energy volatility are beginning to converge.

RBA’s Hauser Warns of ‘Central Banker’s Nightmare’ as Oil Shock Lifts Inflation, Hits Growth

The RBA is facing a “central banker’s nightmare” as rising oil prices push inflation higher while threatening economic activity. Speaking in New York, Deputy Governor Andrew Hauser warned that the Middle East conflict is delivering a significant income shock to Australia, complicating the policy outlook at a time when inflation is already “too high.”

Hauser highlighted the growing tension between price pressures and growth risks. “It is the central bankers nightmare, you know, inflation up, activity down,” he said. While recent consumer sentiment surveys have plunged, he cautioned that they may not fully capture the extent of the hit to consumption. “If they are right, we have a big income shock coming our way,” he added, pointing to the impact of higher fuel costs on household spending.

At the same time, Hauser acknowledged the high degree of policy uncertainty. “I wouldn’t say we have high confidence that we’ve set interest rates at the right level,” he said, emphasizing the need to closely monitor how the shock feeds through to the economy. With inflation pressures clearly skewed to the upside and energy costs yet to fully pass through, the RBA is likely to remain focused on medium-term inflation risks, even as growth headwinds intensify.

Australian NAB Business Confidence Plunges to -29 as Middle East Shock Hits

Australian business confidence has collapsed at a pace only seen during the GFC and COVID, highlighting the immediate impact of Middle East tensions on sentiment. NAB Business Confidence plunged from 0 to -29 in March, marking the second-largest monthly decline in the survey’s history. As NAB’s Gareth Spence noted, declines of this magnitude have “previously only been seen in the GFC and the onset of COVID,” underscoring the severity of the shock.

However, the breakdown in confidence has not yet translated into a sharp deterioration in activity. Business Conditions were little changed at 6, suggesting the economy is still carrying underlying momentum. Spence emphasized that “while the global news backdrop has impacted sentiment, it is still early days in terms of the flow through to activity,” pointing to a lag between sentiment and real economic performance.

At the same time, inflation pressures are already building. NAB reported that purchase cost growth more than doubled to 3% on a quarterly basis, while product price growth rose to 1.1%. Spence noted the impact on costs and prices has been “immediately obvious,” reinforcing the view that the shock is feeding directly into the inflation pipeline.

Australian Consumer Sentiment Plunges as Fuel Prices Surge, RBA Still Set to Hike

Australian consumer sentiment has collapsed back to crisis-era levels as fuel prices and rising interest rates bite. but the RBA is still expected to press ahead with rate hikes as inflation remains the dominant concern.

Westpac Consumer Sentiment plunged -12.5% mom from 91.5 to 80.1 in April, marking the biggest monthly decline since the onset of the COVID pandemic. The index is now hovering near historical lows, underscoring the sharp deterioration in confidence.

The details point to a broad-based weakening in outlook. Near-term expectations have dropped back to levels last seen during the 2022–23 cost-of-living crisis. Job loss fears surged to a 5½-year high, or a 10-year high excluding the pandemic period. According to Westpac, the combination of spiking fuel prices and higher borrowing costs is weighing heavily on real incomes, suggesting another phase of declining per capita consumption.

Yet, weaker sentiment is unlikely to alter the monetary policy path. Inflation remains above target, and the full impact of higher energy costs has yet to be reflected in the data. Westpac expects the RBA to deliver a 25bps rate hike in May, followed by further tightening in the second half of the year, reinforcing the tension between slowing growth and persistent inflation pressures.