Sample Category Title

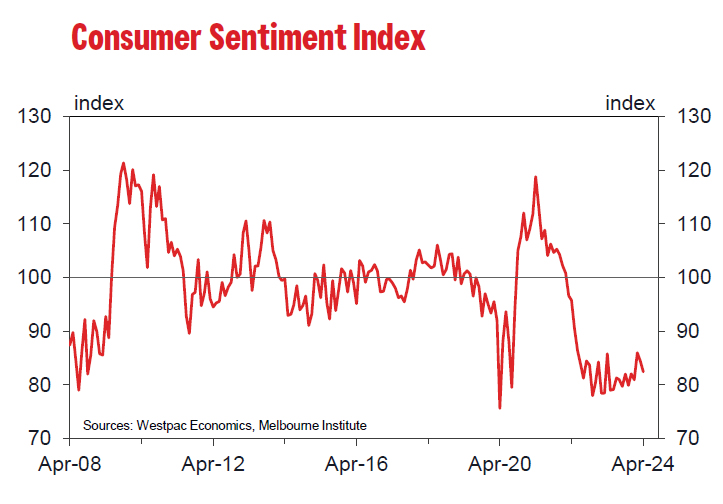

Australia Westpac consumer sentiment falls to 82.4, prolonged pessimism

Australia Westpac Consumer Sentiment Index marked a decrease of -2.4% mom to 82.4 in April. This downturn extends the index's streak below the neutral threshold of 100 to nearly two years, underscoring a prolonged period of consumer pessimism.

Westpac's analysis attributes the lack of recovery in consumer sentiment primarily to the ongoing inflationary pressures that have gripped Australia. Over the past three years, consumer prices have risen significantly, outpacing wage growth by six percentage points. This inflationary trend, coupled with the notable rise in interest rates and increased tax burdens, has significantly strained household incomes, subjecting them to prolonged financial duress.

As attention turns to RBA's next meeting in May, Westpac anticipates no change to the official cash rate. This forecast hinges significantly on the upcoming March quarter CPI update, due on April 24, which is expected to play a crucial role in shaping the RBA's stance.

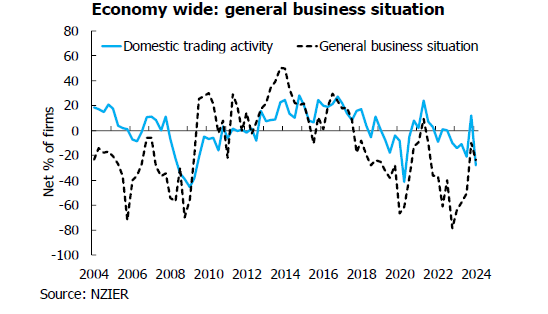

NZ NZIER business confidence tumbles, high interest rates deepen pessimism

In Q1, New Zealand's business community signaled a stark downturn in confidence, with NZIER business confidence index plunging from -9.9 to -23.7 . This dramatic drop is accompanied by reversal in firms' trading activity expectations for the coming quarterly, from 6.6 to -11.5, as well as retrospective decline in past three months' trading activity from 6.7 to -23.2.

NZIER attributes this downturn to the effect of heightened interest rates, which appear to be fulfilling their role in tempering demand to alleviate inflationary pressures. Moreover, the looming uncertainty surrounding the new Government's fiscal strategies, particularly in terms of spending adjustments and cutbacks in the public sector, is exacerbating business caution.

Detailed further illuminates the current economic challenges, with a net 11% of firms having reduced their workforce in the March quarter, albeit with slightly positive hiring intentions moving forward. Investment intentions are also on the downturn, with a net 14% of businesses intending to cut back on plant and machinery investment, and a net 8% planning to curtail investment in buildings over the next year.

Could ECB Adopt Its June 2022 Playbook and Preannounce a Rate Cut?

- The ECB meets on Thursday with strong indications for a dovish tilt

- Low chances of a rate cut being announced this week

- The euro could enjoy a short-term rally against the US dollar if ECB proves hawkish

- Decision will be announced on Thursday 12.15 GMT, press conference at 12:45 GMT

The ECB meets this week

The European Central Bank is hosting its third rate-setting gathering for 2024 on Thursday, April 11. The chances of significant announcements are quite low, but the market appears ready to start the countdown for the first rate cut since 2016.

Since the March ECB meeting when the ECB staff projections pointed to a 2% headline inflation rate at the end of 2025, the ECB doves have come out in force guiding the market to a June rate cut.

Interestingly, the ECB hawks have recognized that the tide has turned in favour of easier monetary policy. They have probably decided to keep their powder dry for the next key decisions, for example an increase in the Minimum Reserve Requirement being discussed behind closed doors.

Could the ECB surprise with an April rate cut?

Economic data releases since the early March meeting have been mixed. Inflation continues to surprise on the downside with the core indicator excluding energy, foods, alcohol and tobacco falling below 3% for the first time since March 2022. In addition, producer prices prints point to weaker inflationary pressures down the line.

However, there appears to be some faint light at the end of the tunnel as the main business surveys including the various PMIs and the German IFO survey have managed to show some improvement. Most of these surveys remain subdued but the outlook might be a bit less murky than currently perceived.

Therefore, despite the plethora of dovish commentary, an April rate cut looks unlikely for Thursday’s meeting.

Could the ECB preannounce a June rate cut?

President Lagarde, at both the March ECB meeting and a key speech in late March, focused on wages and two key pieces of data to be made available by the June meeting. While the ECB wants to avoid making reckless monetary policy decisions, Lagarde could be just trying to gain time in order to achieve unanimity in the ECB council before pre-committing to a rate move.

Having said that, Lagarde’s stance could also reveal some hesitation about preannoucing a rate cut in such a fluid economic environment, especially following the new 5-month high recorded in WTI oil futures. A rally towards the $100 mark would open the door to a new bout of inflation. Moreover, the next Fed meeting is being held in three weeks and the recent strong run of US data prints has almost pushed the first Fed rate cut to September.

However, if there is an overwhelming consensus for such a communication move at Thursday’s meeting, we could have a repeat of the June 9, 2022 gathering when “the Governing Council intends to raise the key ECB interest rates by 25 basis points at its July monetary policy meeting”.

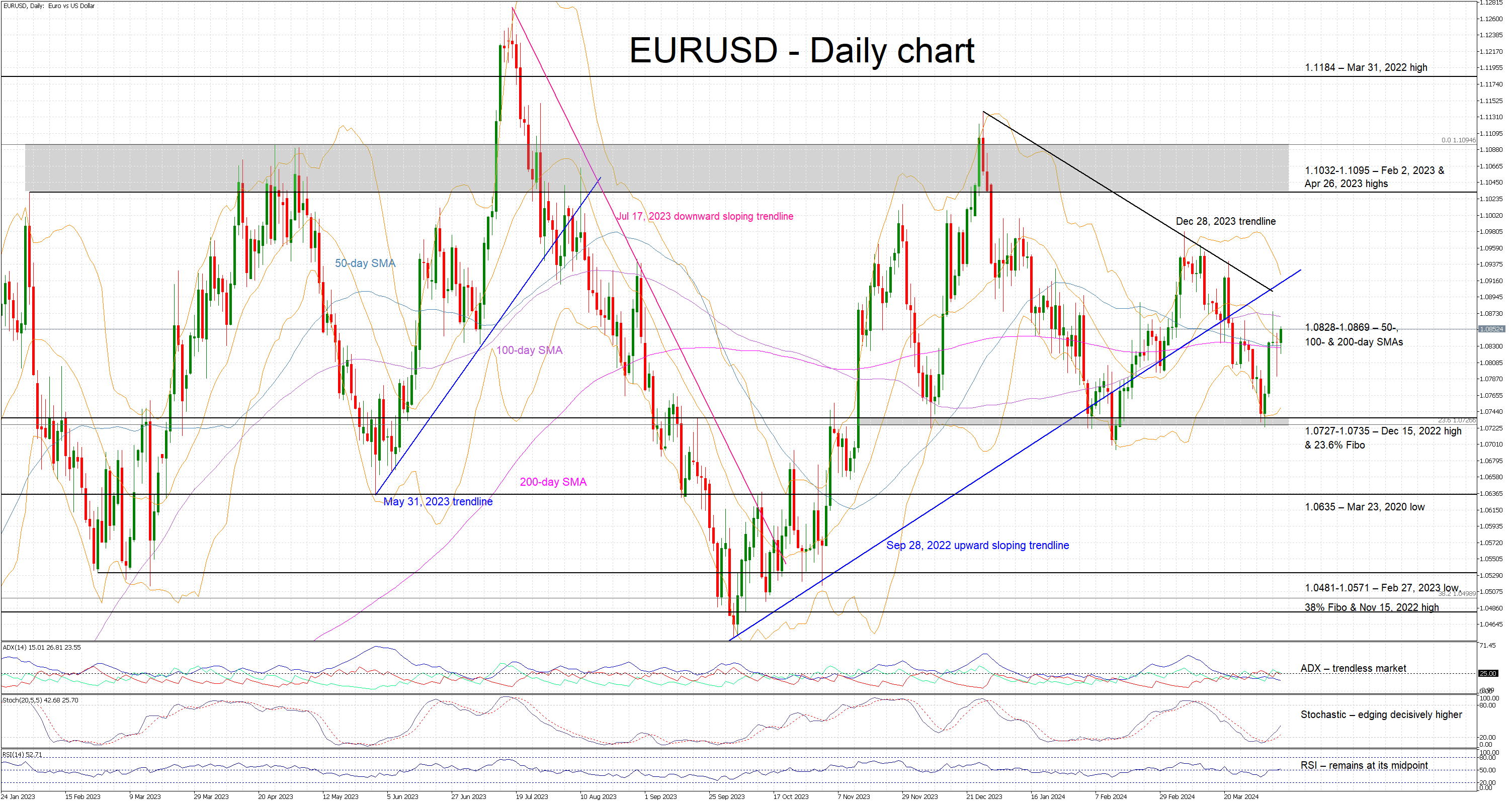

Euro/dollar could see increased volatility on Thursday

It has been a weak first quarter of 2024 for the euro, but its performance could have been much worse considering that the euro area remains the weakest growth link. Market participants are trying to take advantage of this resilience, but this week’s performance against the US dollar clearly depends on the ECB meeting's outcome.

Focusing on Thursday and the market has already priced in a slightly dovish meeting. However, an aggressively dovish gathering with President Lagarde preannouncing a June rate cut, could prove the catalyst for a strong move towards the key 1.0727-1.0735 area.

On the flip side, a hawkish meeting could shock the market and lead euro/dollar higher towards to the September 28, 2022 trendline at around 1.0910. However, the euro’s short-term outlook is unlikely to change dramatically as the market would quickly return to its current mindset for a June rate cut.

First Impressions: NZIER Survey of Business Opinion, Q1 2024

Business confidence slumped in March, after a post-election bounce in December.

Key results (seasonally adjusted)

- General business confidence: -23.7 (Previous: -9.9)

- Trading activity, past three months: -23.2 (Previous: +6.7)

- Trading activity, next three months: -11.5 (Previous: +6.6)

- % reporting a rise in operating costs over the past 3 months: 53.1 (Previous: 54.7)

- % who increased output prices over the past 3 months: 34.5 (Previous: 38.5)

Business confidence came back down to earth with a thud in March, after a strong bounce last December. Businesses reported much tougher conditions over the last quarter, and were downbeat on their investment and hiring plans.

We were wary of the previous quarter’s results, which may have reflected initial hopes about the election of a centre-right government (though this particular survey hasn’t shown a strong political bias in the past). The other positive factor at the time was the sense that inflation was finally easing from its highs. However, the latest survey showed that firms are finding that cost pressures have been slow to recede.

General business sentiment fell to a net -24% in March, from -10% in December. That was still an improvement on the pre-election readings of -50% or worse. However, firms’ own trading activity (which has a closer relationship with GDP growth) was sharply lower. A net 23% saw worse results over the past quarter, the weaking reading since the Covid lockdown. Expectations for the next quarter turned negative again, as they had been since mid-2022.

These results present some downside risk to our near-term GDP forecasts, where we expect some weakly positive growth (though remaining below population growth). That said, indicators of activity to date, such as the manufacturing PMI, have been more positive that what this confidence survey suggests.

A net 35% of firms reported that they had increased their prices in the last three months, down from 39% last quarter. Intentions to raise prices also receded modestly, from 36% to 32%. These results are consistent with our forecast for CPI inflation to ease further from 4.7% to 4.2% in the March quarter – albeit higher than the Reserve Bank was expecting at this point.

Capacity pressures for businesses have continued to fade. The ease of finding workers remained at its highest levels since 2010, and a lack of demand is increasingly becoming the main constraint on growth.

Even so, cost increases over the last three months remained high, and expectations ticked higher again this quarter. Our discussions with businesses have revealed concerns about costs such as a sharp rise in council rates and a potential rebound in shipping costs.

Today’s survey provides mixed messages for the Reserve Bank. On one hand, higher interest rates are clearly continuing to have a braking effect on activity. However, the fact that inflation is receding only slowly will remain a concern. We think the RBNZ will be looking for more reassurance from the upcoming CPI and labour market reports before they consider signalling an earlier start to OCR cuts.

US Consumer Price Index CPI – USD/JPY Technical Analysis

US Consumer Price Index – CPI

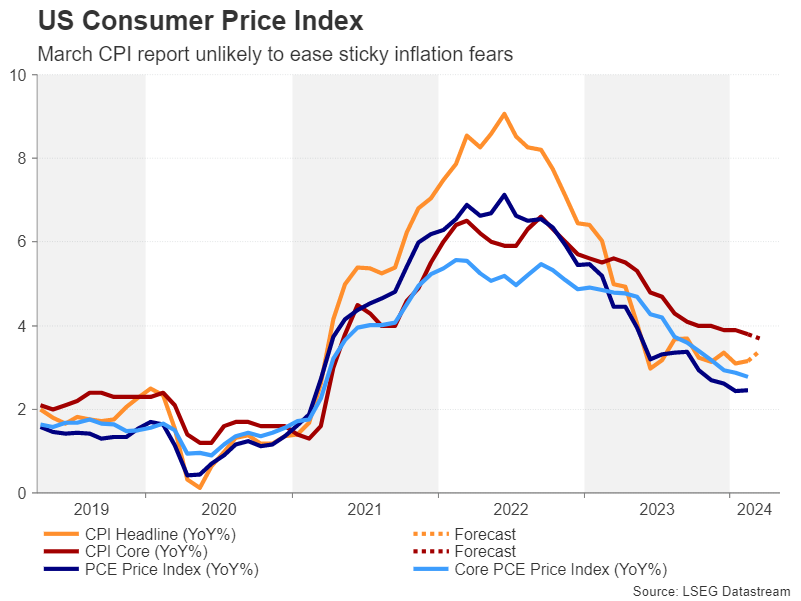

The US Consumer Price Index CPI Y/Y overall trend has been steadily declining after reaching its peak of 9.06% in June 2022. A drop in all CPI components, including Energy, Food, and Durable Goods Prices, mainly drove the decline. However, the decline stalled during the last quarter of 2023, and the index has been moving sideways since then as the changes in the Services sector remained almost unchanged throughout the entire time.

Core Services M/M peaked in January 2024 at a one-year high of 0.66%; however, it registered 0.457% for February 2024, a 30% decline. Core Services data M/M may be critical this week as investors will watch whether the declining trend will resume toward the pre-pandemic averages of 0.25%—0.35% or reverse and peak again. The index has been registering higher lows since June 2023. A change in the cost of services can be more meaningful if accompanied by a similar percentage change in other CPI components, such as Durable Goods prices. Oil prices have recently been rising, and it is logical to impact the overall production costs; although the increase in oil prices came slightly after the CPI reporting period, it may still have an impact. On the other hand, a stabilization for CPI data at its current levels can be seen as favorable by market participants as it should add another reason for the FED to consider interest rate cuts sooner rather than later.

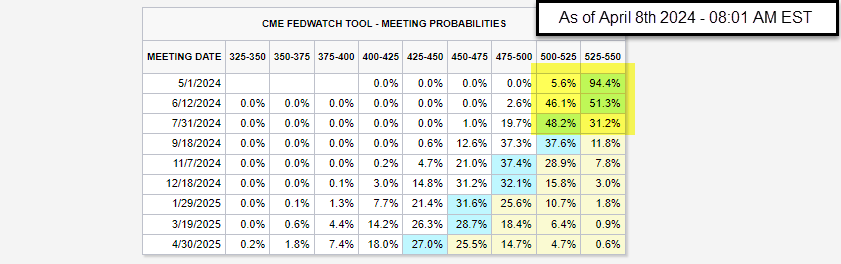

CME FedWatch Tool

Source: CME Group – CME FedWatch Tool

According to the most recent review of the CME FedWatch tool, market participants anticipate two to three rate cuts between March 20th, 2024, and December 31st, 2024. The percentage of participants expecting rates to remain at their current 525-550 range for the meeting on May 1st, 2024, is 94.4%, down from 99.8%. The expectation for a 25-basis points rate cut for the May 1st meeting rose from 0.2% to 5.6%. As for the June 12th, 2024, Fed’s meeting, the percentage of a 25-basis points rate cut fell from 57.2% last week to 46.1%.

USDJPY Technical Analysis – 1 Hour Chart

- Price action continues to trade within a trading range, which began in mid-March 2024.

- Multiple attempts to break above the range upper borders have failed so far; the upper range border intersects with R1 Standard calculations.

- The MACD line crossed below its signal line, and its histogram turned bearish after an extended coiling period.

- Market reaction for Friday, April 5th, 2024: NFP has faded for other currency pairs, such as EURUSD and USDAD; however, for USDJPY, this has not happened, thus adding more weight to the yellow highlighted candle, the candle low intersects with the daily pivot point forming a level of support to follow

- A slight negative divergence can be seen on RSI14 as price action makes higher highs while RSI makes lower highs.

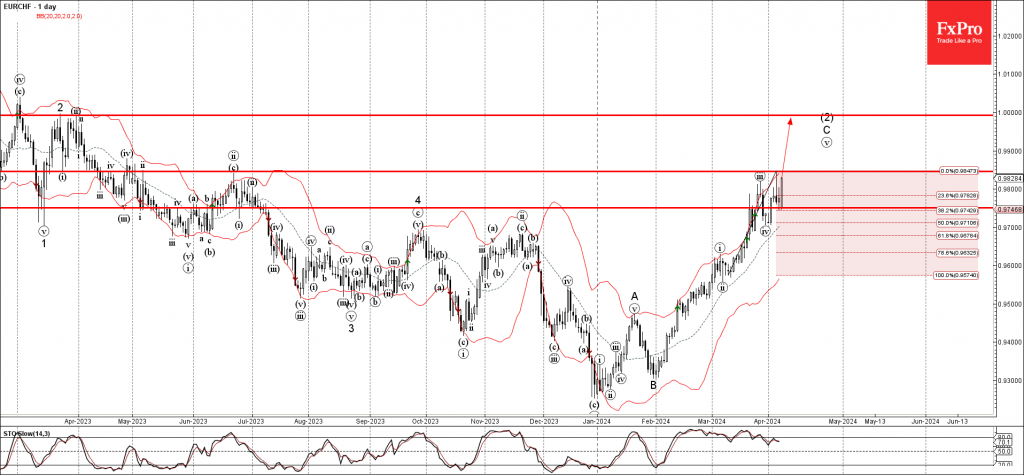

EURCHF Wave Analysis

- EURCHF reversed from support level 0.9750

- Likely to rise to resistance level 0.9845 and 1

EURCHF rising after the recent upward reversal from the support level 0.9750 intersecting with the 38.2% Fibonacci correction of the upward impulse from the start of March.

The upward reversal from this support level 0.9750 continues the C-wave of the active intermediate ABC correction (2) from January.

Given the string Swiss franc sales, EURCHF can be expected to rise further to the next resistance level 0.9845 (multi month high from June) – followed by parity (target for the completion of the active impulse wave C).

US CPI Data Unlikely to Ease Sticky Inflation Worries, But Will Markets Care?

- US CPI inflation expected to have ticked up in March

- But markets may shrug it off if core figure inches lower

- Data due at 13:30 GMT, Wednesday, will be followed by FOMC minutes at 18:00 GMT

Will CPI report boost rate cut bets?

Inflation data according to the CPI and PCE measures have started to diverge lately, clouding the outlook just as the Fed seeks more clarity on where prices are headed. Headline CPI has persisted above 3.0% since last summer, while core CPI has been declining at a snail’s pace.

It’s a somewhat more favourable trend when looking at the personal consumption expenditures (PCE) metric that the Fed prefers to focus on. The headline PCE price index rose marginally to 2.5% in February, but core PCE eased to 2.8%.

But for the consumer price index, there probably wasn’t much of a convergence in March. The yearly headline rate of CPI is expected to have edged up to 3.4% in March from 3.2%, with the month-on-month rate moderating to a 0.3% pace from 0.4%. Core CPI is also expected to have fallen slightly, both on a monthly and annual basis, expected at 0.3% and 3.7% respectively.

June rate cut no longer a done deal

Whilst such figures would not necessarily raise any alarm bells, neither would they calm fears about inflation bottoming out before reaching the Fed’s 2% target. But for the moment, Fed officials remain optimistic that inflation will decline further in the coming months, allowing it to cut rates at some point in the second half of the year. It’s unlikely that the minutes of the March FOMC meeting will sway much from this message.

The expectation that one way or another, rates cuts are coming, and that the US economy will almost certainly avoid a recession is what has negated the disappointment from the fading bets for a June rate cut.

The odds for a 25-basis-point cut in June have been scaled back sharply in recent weeks, and even more so after Friday’s bumper payrolls report. Markets are evenly split on the odds of the Fed beginning its rate cutting cycle in June, compared to it being almost fully priced in a few weeks ago.

Markets hopeful inflation will fall

The US dollar has been in a broad uptrend this year as investors have been repeatedly forced to re-evaluate the timing of Fed easing. Yet, there’s still a tendency to put more weight to the soft indicators than the hot data and this is keeping a lid on dollar gains.

For example, the drop in the ISM services prices paid index more than offset the impact from the jump in manufacturing prices days earlier as well as hawkish commentary from Fed officials during the week. Meanwhile, cooling wage pressures in the March NFP numbers were enough to keep jitters over accelerating jobs growth to a minimum.

A goldilocks economy

To be fair, the notion that the US labour market can continue to grow without fuelling faster pay increases is not entirely unreasonable amid the influx of migrants into the country that is boosting the supply of labour and thus meeting the rise in demand.

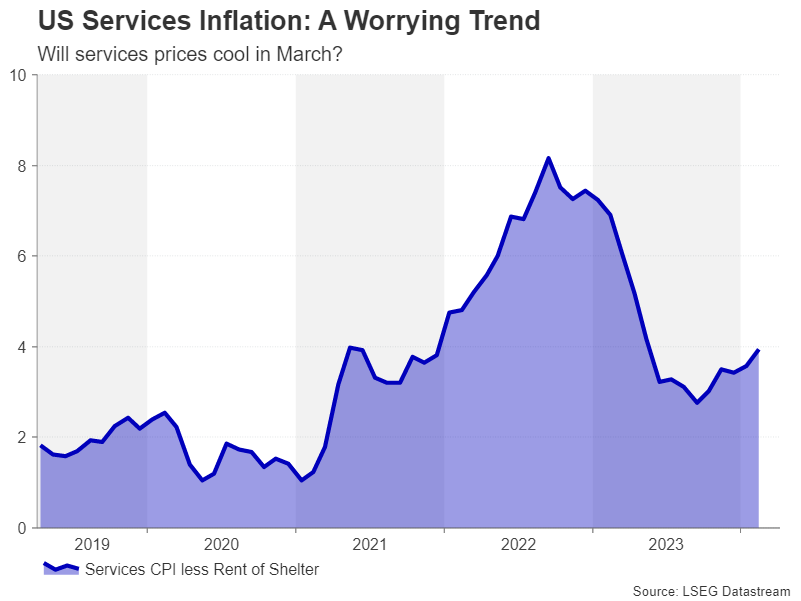

But even if this goldilocks scenario can last, solid consumer demand on the back of the tight labour market will be a hindrance to getting inflation down all the way to 2%, particularly for services inflation. CPI less rental costs edged up to 3.9% in February, having reversed from a low of 2.8% last September. If the decline in the ISM services price gauge translates to a softer reading for the CPI component as well, that could be enough to sustain the current positive sentiment in the markets even if the headline figure ticks higher.

However, if either or both the core and services CPI prints are stronger than forecast in March, the upbeat mood may fade, lifting the dollar, but weighing on Wall Street.

Optimism keeps a check on dollar gains

The dollar index appears to be forming a double top around the 105.00 region, so this level is likely to be tested again if the CPI numbers are hotter than expected. But holding above the 50- and 200-day moving averages (MA) at 103.94 and 103.81, respectively, is crucial to maintaining the positive bias. So, a surprisingly weak CPI report could pull the dollar index below its MAs, tilting the near-term risks to the downside.

Overall, it’s striking how well risk appetite has held up even as investors have started to price out the third expected rate cut for 2024. The soft-landing narrative seems to be slowly evolving to one of US exceptionalism, whereby the American economy keeps outperforming its peers. It remains to be seen whether the risk rally can survive rate cut hopes being dimmed any further.

Euro Edges Lower, German Industrial Production Jumps

The euro is calm at the start of the trading week. In the North American session, EUR/USD is trading at 1.0830, down 0.07%.

German industrial production rises 2.1%

Is the German economy coming out of a downswing? The week started on a positive note as industrial production jumped 2.1% y/y in February, up from a revised 1.3% gain in January and crushing the market estimate of 0.3%. This was the strongest expansion since January 2023 and a second straight expansion after eight straight declines. The strong industrial production release comes on the heels of Friday’s factory orders, which rebounded in February with a 0.2% m/m gain after sliding 11.4% in January.

The improvement in these readings has raised hopes that Germany’s manufacturing sector has turned a corner and will show improvement in the first quarter which would help boost a struggling economy. The economy contracted 0.3% in Q4 2023 and another decline in the first quarter would indicate a technical recession.

US nonfarm payrolls much stronger than expected

US nonfarm payrolls surged to 303,000 in March, up from a revised 270,000 in February and blowing past the market estimate of 200,000. The unemployment rate dipped lower to 3.8%, down from 3.9% and below the market estimate of 3.9%. Wage growth matched expectations at 4.1%, down from 4.3%.

The strong employment numbers are a sign of a robust US economy and that could mean that the Fed will push back a rate cut. The markets have lowered expectations for a rate cut in June or July due to the US employment report and a cut isn’t considered likely until September. The Fed is widely expected to hold rates at the May 1st meeting.

EUR/USD Technical

- EUR/USD tested support at 1.0826 earlier. Below, there is support at 1.0803

- 1.0859 and 1.0882 are the next resistance lines

Sunset Market Commentary

Markets

Trading to the new week took a slow start data-wise. European production data for sure are no market movers. However, for once, we mention German February production coming out on the stronger side of expectations for the second consecutive month (+2.1% M/M; -4.9% Y/Y vs -6.8% expected). The report won’t change the ECB’s assessment on the timing of the start to the rate cut cycle. Even so, it reminds markets that EMU activity probably passed the trough, potentially easing the need for aggressive, pre-emptive rate cuts further out this year. German yields also still had some catching up to do on Friday’s US move, currently adding between 2.5 bps (30-y) and 4.0 bps (5 & 10-y). Still, in a broader perspective EMU/German yields for now hold within a sideways pattern capped by the YTD top levels reached end February. US graphs in this respect are telling a different story. Excellent March US payrolls on Friday only reinforced the idea that the Fed is facing growing risks if it would move too early with cutting rates. US yields on Friday closed at/slightly above the YTD peak levels and this technical break higher is extended today. Yields adds between 1.5 bps (2-y & 30-y) and 3.0 bps (5 & 10-y). The US 10-y real yield also decisively regains the 2.0% mark (2.05%). Higher-than-expected (or maybe even in-line) March US CPI data on Wednesday (expected 0.3% M/M for both core and headline) probably will be enough to confirm this break and further push back expectations for a first cut to September rather than in July or June (currently priced at 90% and 50% respectively). In this context, we also keep a close eye on this week’s US Treasury auctions (3-y Tuesday, 10-y Wednesday and 30-y Thursday). Dwindling buying interest, if it were to happen, also might reinforce the break higher in yields.

For now, there is only limited (negative) spill-over from higher (real) US yields to other markets including commodities, equities and FX. The likes of copper are trading at the strongest level since mid-2022. After a hesitant start, European equities are gradually catching up part of Friday’s US rally (EuroStoxx +0.7%). US indices open little changed, but still have the all-time record levels within reach (<2% for the S&P 500 and the Nasdaq). The USD basically is going nowhere. DXY gains marginally (104.35). EUR/USD trades little changed (1.0835). USD/JPY is the exception to the rule resting the 151.95 multi-year top, but this probably is mainly yen softness with markets testing Japanese authorities’ resolve to prevent further yen losses. Sterling still sightly underperforms the euro, but EUR/GBP stays below first technical resistance in the 0.8600/02 area.

News & Views

The Swedish crown is among the best performers in the G10 currency landscape today. EUR/SEK dipped from 11.53 at the open to 11.46 currently. SEK lost ground rapidly since mid-March, amongst others on speculation that the Riksbank would soon start to lower rates following stronger-than-expected disinflation. Stockholm at the March meeting indeed hinted at a first move in May or June, tilting earlier “H1 2024” guidance slightly to the dovish side. But in speeches from the likes of Breman, Jansson and governor Thedeen as recent as Friday and today (Thedeen again), Riksbank officials are increasingly paying attention to the risk of major central banks such as the ECB and especially the Fed delaying the cutting cycle. Thedeen today explicitly noted the need to focus on krona effects coming from a strong US dollar, referring to the possibility of a weaker SEK bringing unwanted inflation. He also called for a cautious approach when the central bank eventually does kick off the easing cycle, saying he wants to avoid a demand boost that could potentially reignite inflation too.

The Kingdom of Belgium announced it intends to issue a new syndicated euro benchmark bond in the near future, most likely tomorrow. The new OLO102 will carry a five year maturity (22/10/2029) and is the last syndicated benchmark deal for the year. The two previous ones were issued in January (€7 bn) and February (€5 bn) with a 10-year and 30-year tenor respectively. Belgium plans to raise €41 bn through OLOs this year of which it printed €17.785bn (43.38%) so far. The Kingdom last Friday launched its first USD benchmark deal (10/06/2055) since 2020. The inaugural 30-year transaction falls under the EMTN programme (a €2bn envelope) and successfully raised $1.25 bn.