Sample Category Title

NZ government drastically cuts 2024 growth forecast to 0.1%, lowers inflation outlook

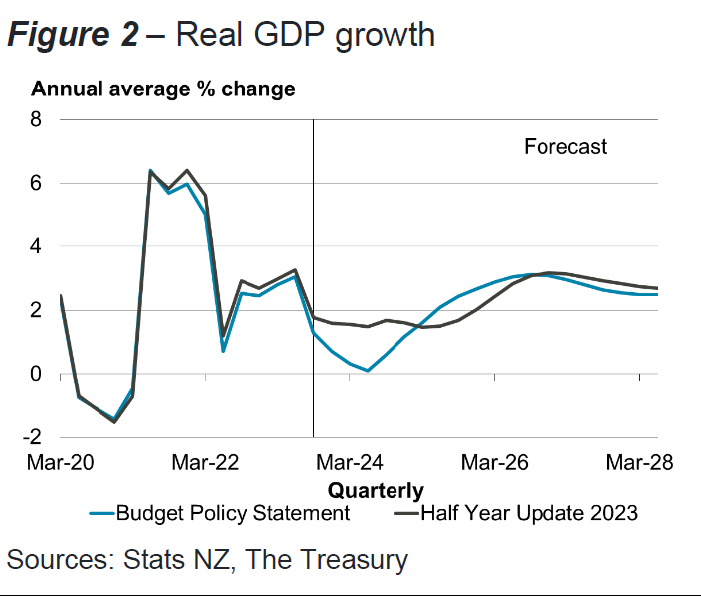

New Zealand government has made significant revisions to its economic forecasts, projecting a notably subdued GDP growth of just 0.1% for this fiscal year, as revealed in its latest budget statement. Additionally, inflation outlook for both 2024 and 2025 was revised downwards.

The government said a "wide range of data" collected since December highlighted "further deterioration in the economic outlook." The expected slowdown in economic activity materialized "sooner than expected," while inflationary pressures have "eased more than expected."

Specifically, GDP growth projections for 2024 have been significantly lowered from prior forecast of 1.5% to 0.1%. However, there is a silver lining with GDP growth forecast for 2025 being adjusted upwards from 1.5% to 2.1%.

On the inflation front, CPI forecast for 2024 was lowered from 4.1% to 3.3%, and for 2025, forecast was revised down from 2.5% to 2.2%.

BoJ’s Tamura stresses gradual withdrawal of stimulus for steady policy normalization

BoJ board member Naoki Tamura said that Japan's moderate economy recovery path is expected to continue, positive cycle of wage increases leading to higher inflation rates.

"The risk of our medium- and long-term forecasts being derailed is likely small," he remarked in a speech today.

He underscored the importance of a deliberate and gradual approach to policy normalization, ensuring that the transition away from aggressive monetary support is managed with precision and foresight.

"How to manage monetary policy ahead is very important to ensure we deftly roll back our massive stimulus program, and move slowly but steadily toward policy normalization," he articulated.

Central to Tamura's vision is the restoration of interest rate flexibility, positioning BoJ to effectively modulate demand and influence price dynamics through rate adjustments.

"In my view, the central bank's ultimate goal is to bring interest rates back to levels where they can be pushed up or down to adjust demand, and influence price moves," he stated.

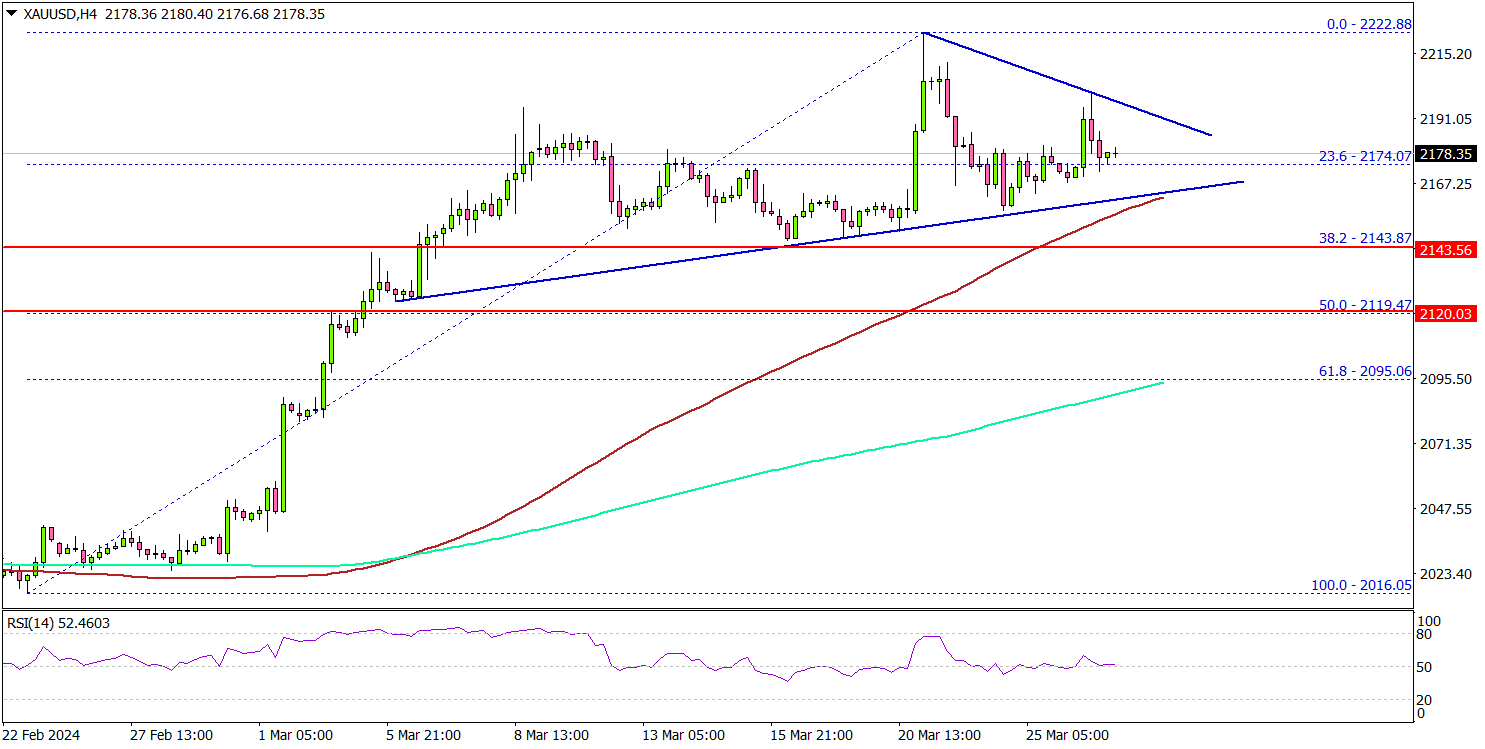

Gold Price Could Resume Rally Unless This Level Gives Way

Key Highlights

- Gold rallied above the $2,150 and $2,170 resistance levels.

- A key contracting triangle is forming with support at $2,160 on the 4-hour chart.

- EUR/USD struggled to continue higher above the 1.0865 resistance.

- Bitcoin price regained strength for a move above the $70,000 resistance.

Gold Price Technical Analysis

Gold prices started a fresh increase from the $2,020 support against the US Dollar. The bulls cleared the $2,120 resistance to start a strong rally.

The 4-hour chart of XAU/USD indicates that the price settled above the $2,150 level, the 100 Simple Moving Average (red, 4 hours), and the 200 Simple Moving Average (green, 4 hours).

The bulls were able to pump the price above the $2,180 and $2,200 levels. Finally, the price traded close to the $2,225 level before the bears appeared. A high was formed at $2,222 and there was a minor downside correction.

There was a move below the $2,200 level. There was a spike below the 23.6% Fib retracement level of the upward move from the $2,016 swing low to the $2,222 high.

The first major support sits at $2,160. There is also a key contracting triangle forming with support at $2,160 on the same chart. Any more losses might call for a move toward the $2,142 level or the 50% Fib retracement level of the upward move from the $2,016 swing low to the $2,222 high.

On the upside, the price is facing resistance near the $2,190 level. The main resistance is now forming near $2,200, above which the price could accelerate higher toward $2,220.

Looking at Bitcoin, there was a strong upward move above the $70,000 zone but there are again signs of weakness.

Economic Releases to Watch Today

- Euro Zone Economic Sentiment Indicator for March 2024 – Forecast 96.3, versus 95.4 previous.

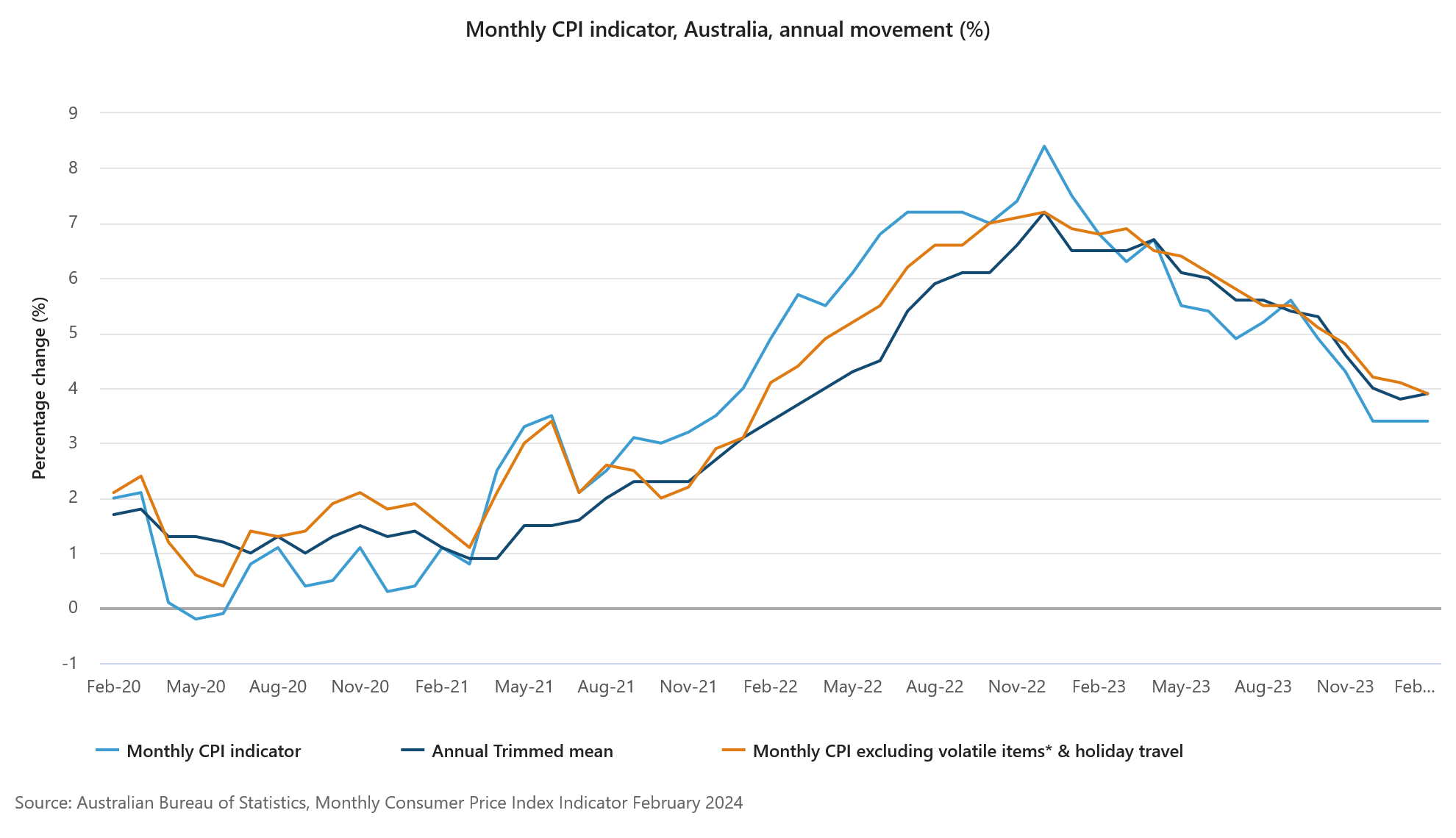

Australia’s monthly CPI holds steady at 3.4% in Feb

Australia monthly CPI was unchanged at 3.4% yoy in February. When stripping out volatile items and holiday travel, the CPI saw a slight deceleration, moving from 4.1% yoy to 3.8% yoy. However, a closer look at the core inflation measure, the annual trimmed mean CPI, reveals a slight uptick from 3.8% yoy to 3.9% yoy, suggesting underlying inflationary pressures remain persistent.

The detailed breakdown of inflation contributors highlights showed that housing costs had the most substantial rise at 4.6% yoy. Food and non-alcoholic beverages also experienced a notable increase at 3.6% yoy. Additionally, alcohol and tobacco products saw a sharp price escalation at 6.1% yoy, and insurance and financial services costs surged by 8.4% yoy, the latter being the highest among the recorded sectors.

Full Australia monthly CPI release here.

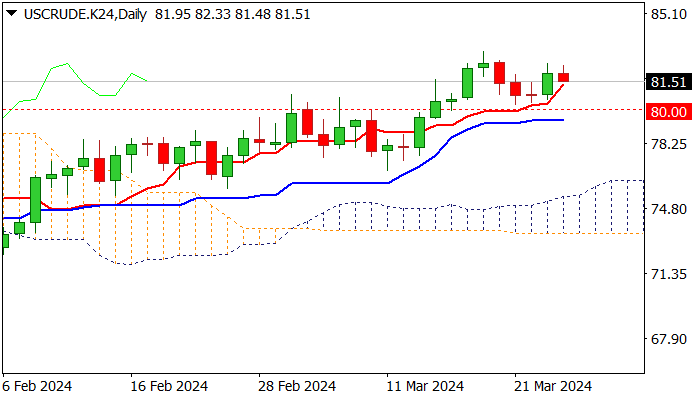

Oil: Russia-Ukraine Crisis Could Boost Oil Prices

Crude oil futures surged on Monday due to disruptions in Russian refining capacity caused by Ukrainian drone strikes and Moscow's decision to cut output to comply with OPEC+ targets. The West Texas Intermediate (WTI) contract for May settled at $81.95 a barrel, up $1.32, while the Brent contract for May settled at $86.57 a barrel, also up $1.32. Russia instructed companies to reduce oil production to fulfill its OPEC+ commitments, with voluntary cuts totaling 2.2 million barrels per day. A Ukrainian drone attack caused a fire at the Kuibyshev oil refinery in Samara, knocking out a major refining unit. According to British intelligence, Ukrainian strikes against Russian energy infrastructure have disrupted at least 10% of Russia's refining capacity, potentially leading to time-consuming and costly repairs.

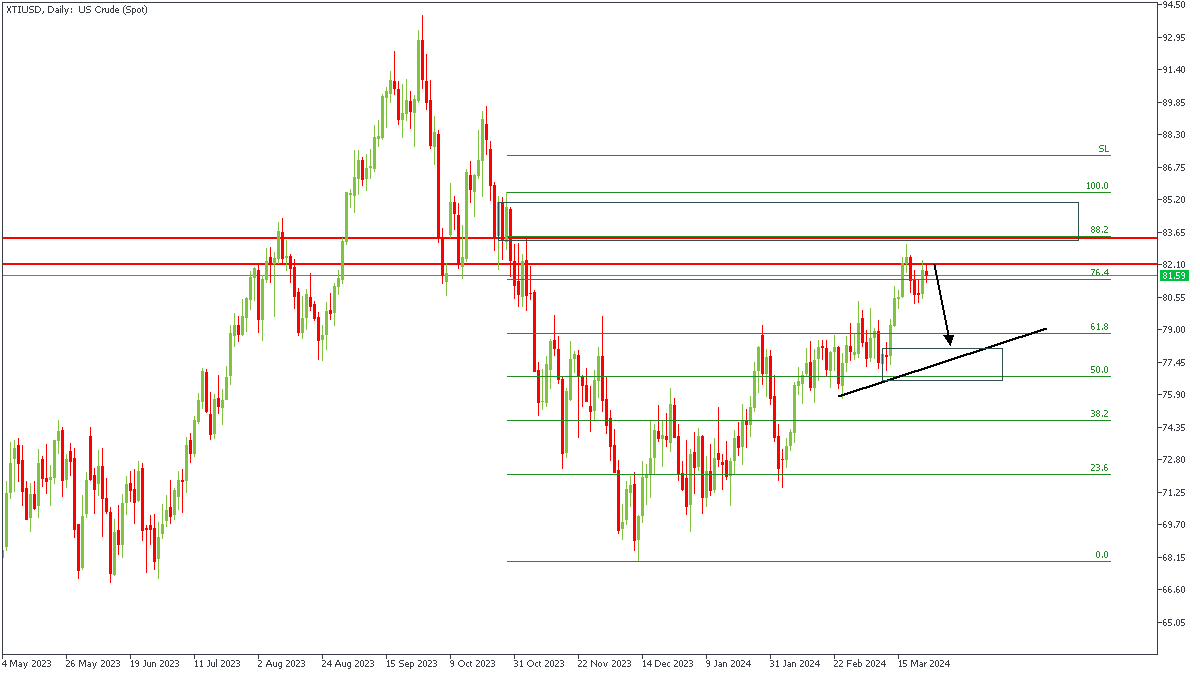

XTIUSD - D1 Timeframe

XTIUSD has made an initial reaction off the pivot zone on the daily timeframe, and may slide even further down. This sentiment is based off of the QMR pattern that I have spotted on the 1-hour timeframe, and the 88% Fibonacci retracement level. The primary target here could very well be the trendline support as shown on the chart.

Analyst’s Expectations:

- Direction: Bearish

- Target: $78.42

- Invalidation: $83.53

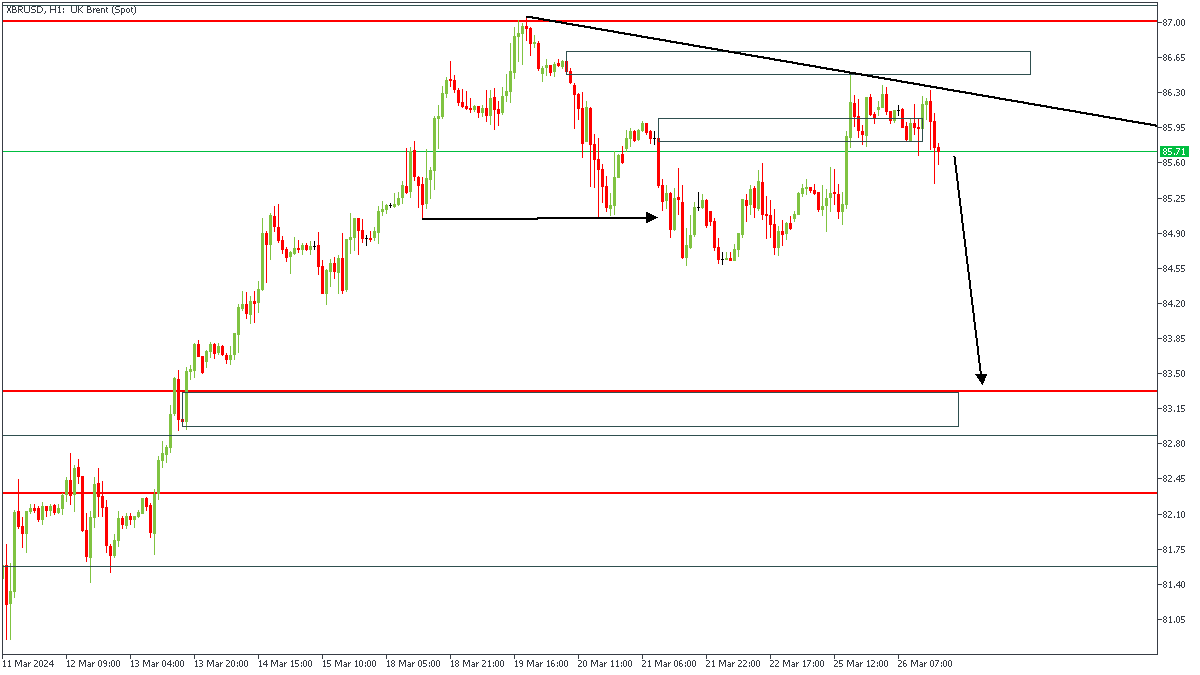

XBRUSD - H1 Timeframe

XBRUSD made a sharp reversal after hitting the pivot zone on the daily timeframe. Following this, price retested a trendline resistance after breaking below the previous lows, indicating the likely onset of a bearish trend. It is my belief that price would try to close below the most recent low, since failure to do so would imply a change in market sentiment. My final target, however, is the demand zone marked out towards the bottom of the chart.

Analyst’s Expectations:

- Direction: Bearish

- Target: $83.36

- Invalidation: $86.73

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

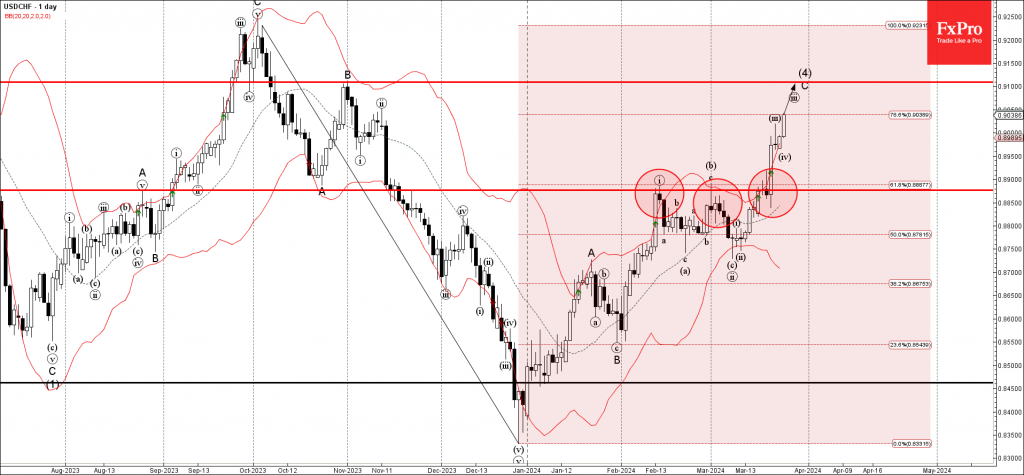

USDCHF Wave Analysis

- USDCHF broke the resistance level 0.8875

- Likely to rise to resistance level 0.9100

USDCHF currency pair recently broke the resistance level 0.8875 (which has been reversing the price from February), intersecting with the 61.8% Fibonacci correction of the downward impulse from October.

The breakout of the resistance level 0.8875 accelerated the C-wave of the active intermediate ABC correction (4).

Given the strongly bearish Swiss France sentiment seen today, USDCHF currency pair can be expected to rise further to the next resistance level 0.9100 (target for the completion of the active impulse wave C).

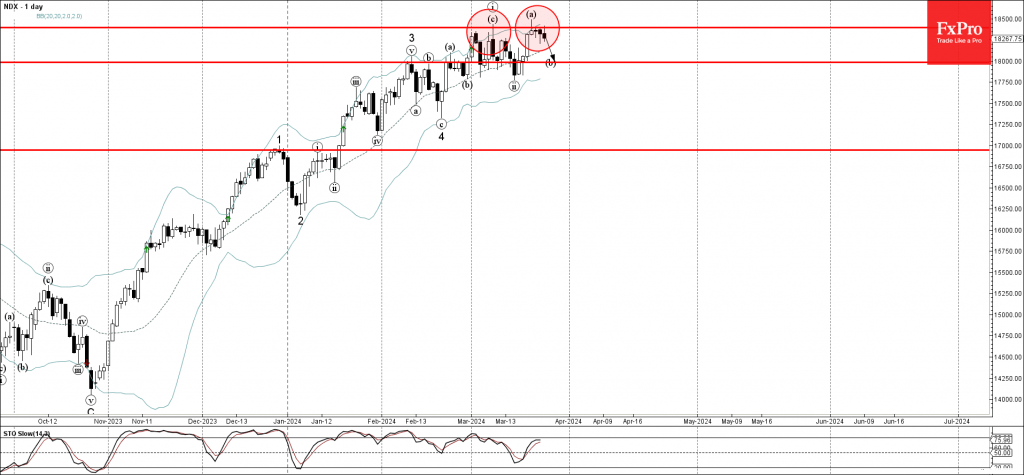

Nasdaq-100 Index Wave Analysis

- Nasdaq-100 index reversed from resistance level 18400.00

- Likely to fall to support level 18000.00

Nasdaq-100 index recently reversed down from the key resistance level 18400.00 (strengthened by the upper daily Bollinger Band), which has been reversing the index from the start of March.

The downward reversal from the resistance level 18400.00 started the active minor correction (b).

Given the strength of the resistance level 18400.00 and the bearish divergence on the daily Stochastic, Nasdaq-100 index can be expected to fall further to the next round support level 18000.00.

Sunset Market Commentary

Markets

The eco calendar in Europe and the US this week is backloaded with the publication of key (national) EMU inflation data starting tomorrow and the Fed’s preferred inflation measure (PCE deflator) scheduled for release on Friday. Some less high profile data and CB comments in the meantime have to guide the day-to-day market dynamics post-Fed. However, data published today, were too close to expectations to provide any clear directional bias. German GFK consumer confidence improved slightly more than expected (-27.4 from -28.8), but this evidently won’t change the ECB’s assessment on (the start of/extent of) policy easing. German yields are ceding less than 1 bp across the curve. Somewhat of a similar wait-and-see narrative in the US. The March Philly Fed non-manufacturing business activity index in dropped more than expected from -8.8 to -18.3. Durable goods statistics were mixed. Headline orders printed slightly stronger than expected (1.4% M/M) as was the case fore core orders ex transportation (0.7%). At the same time, capital goods shipments non-defense ex aircraft delivered a slight miss with a -0.4% monthly decline. US house prices rises (S&P CoreLogic CS 20 city) slowed to 0.14% M/M, but this still resulted in a strong 6.59 Y/Y rise (from 6.15%). There is no one-on-one link with housing related components in the inflation gauges, but it probably won’t translate into a sharp decline in this key factor anytime soon. Last but not least, consumer confidence of the Conference Board, stabilized at 104.8 but last month was downward revised. Consumer remain upbeat in their current situation (151 from 147.8), but are turning more cautions in the future. Again a difficult mix from a market point of view. US yields currently are rising 1- 2 bps across the curve (benchmark change for the 2-y, -1.8 bps). The US 10-y real yield post Fed dropped back from 2%+ levels to 1.85% and last week/early this week and tries to turn north again. However, for now this has only a limited impact on risk assets or on the dollar. US equities again succeed modest gains (Nasdaq + 0.5%). Eurostoxx 50 also sets a new cycle top. Oil also holds north of $86 p/b.

On FX market, the dollar is again locked in tight ranges, with a tentative negative bias. DXY eases to 104.12, EUR/USD ‘rises’ to 1.085. The yen fails to gain against the US currency despite strong verbal interventions from Japanese authorities of late. At USD/JPY 151.4 the multi-year top (weakest for the yen) remains dangerously close-by. Sterling underperforms, even as BoE’s Mann (admittedly one of the hawkish members within the MPC) says markets are pricing in too many rate cuts. EUR/GBP (0.8585) again nears first resistance (support for sterling) at 0.8600/02.

News & Views

In spite of Glapinski’s olive branch this weekend, Poland’s ruling coalition kicked off a probe into the NBP governor today. The Tusk government accuses the central bank head and PiS appointee of political partisanship with the surprise rate cuts ahead of the October elections and the change of heart shortly thereafter being one of the most contentious decisions. The fall-out on the zloty remains limited for now and EUR/PLN continues to hover near the multiyear lows around 4.30. Even if Glapinski was ousted or resigns himself, it would probably not change a lot to the current higher for longer rates regime. His successor, first deputy Kightley, is known for her Glapinski-alike views.

The Hungarian central bank (MNB) already scaled back the recently increased cutting pace. It lowered the policy rate by 75 bps to 8.25%. Inflation eased more than projected in the December report and could average between 3.5 and 5% this year and 2.5-3.5% in 2025 and 2026. In addition, labour market tightness eased and growth forecasts were lowered compared to December to mostly reflect weak external demand. GDP should expand 2-3% this year before picking up to 3.5-4.5% in 2025. Offsetting these arguments for continuing on the same monetary path of February (ie 100 bps cut), was the volatile international environment. MNB said that raised the risk premium on Hungarian assets recently. It clearly alluded to the latest sell-off of the forint when EUR/HUF came close to the symbolically important 400. But we are looking at the sharper (compared to regional peers) uptick in (swap) yields in recent weeks through a similar lens. With “risks surrounding global disinflation, volatility in international investor sentiment and the temporary rise in domestic inflation expected in the middle of the year”, the MNB said the monetary policy approach needs to be a careful one. This reveals a preference to stick to the current pace (or lower). The forint breathes a sigh of relief but isn’t out of the woods, with EUR/HUF holding north of 395.

WTI Oil Outlook: Takes a Breather after Monday’s 1.40% Advance

WTI oil price is holding within a tight range on Tuesday and consolidating Monday’s 1.40% advance, sidelined by mixed fundamentals.

Supply concerns following recent attacks on Russian oil installation, which may cause longer disruptions from one of world’s top oil producers and exporters, weigh on oil price, while weaker dollar underpins.

Technical studies remain firmly bullish on daily chart and contribute to positive near-term outlook, as positive momentum is strong and daily Tenkan-sen / Kijun-sen are in bullish configuration and steeply ascending Tenkan-sen, which contained the latest pullback from new 2024 high ($83.10) is diverging.

Near-term bias is expected to remain with bulls while the price stays above Tenkan-sen ($81.32), guarding lower pivots at $80.30/$80.00 (March 21 higher low / psychological).

Res: 82.44; 83.10; 83.76; 84.17.

Sup: 81.32; 80.30; 80.00; 79.47.