Sample Category Title

Pound Edges Lower Ahead of BoE Meeting

The British pound is slightly lower on Thursday. In the European session, GBP/USD is trading at 1.2766, down 0.16%.

BoE expected to hold rates

The markets will shift focus from the Federal Reserve, which maintained rates on Wednesday, to the Bank of England, which is holding its rate meeting later today.

The BoE is widely expected to maintain the cash rate at 5.25% at today’s meeting but investors will be looking for signals of a rate cut, especially after the inflation report on Wednesday, which was lower than expected.

The central bank hasn’t jumped on the rate-cut bandwagon, although the markets have priced in an initial rate cut in June. The sharp fall in both headline and core CPI for March won’t affect today’s meeting but could prod the Monetary Policy Committee to hint at a rate cut. If the MPC provides such a hint, it would likely weigh on the British pound.

It should be remembered that at the previous meeting in February, two of the nine MPC members voted for a rate increase, which shows that some policy makers are concerned that inflation could rebound if the BoE cuts rates too soon.

Federal Reserve maintain rates, remains cautious

The Federal Reserve held the benchmark rate at a target range of 5% to 5.25%, as was widely expected. The Fed maintained its projection of three rate cuts this year and revised its GDP forecast for 2024 to 2.1%, up from 1.4% in December. Fed Chair Powell acknowledged that inflation was falling and the US economy was strong, but said that the Fed would not start to cut rates until it was clear that inflation was moving sustainably towards the 2% target.

GBP/USD Technical

- GBP/USD is putting pressure on support at 1.2753. Below, there is support at 1.2718

- There is resistance at 1.2820 and 1.2855

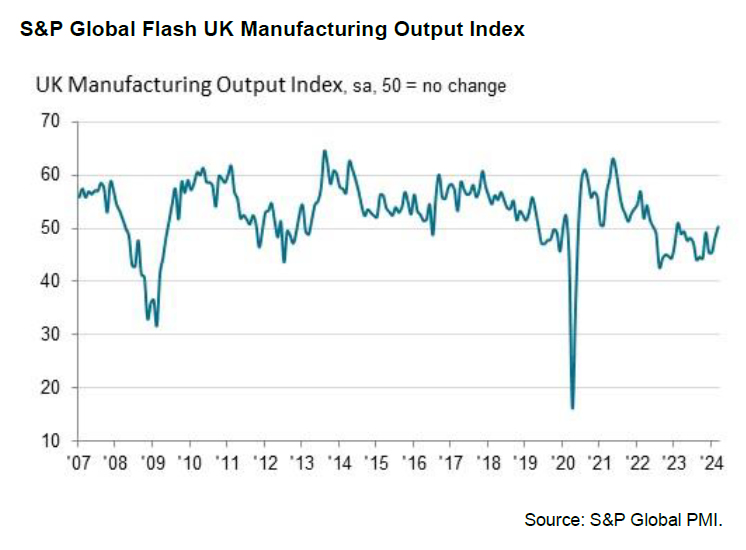

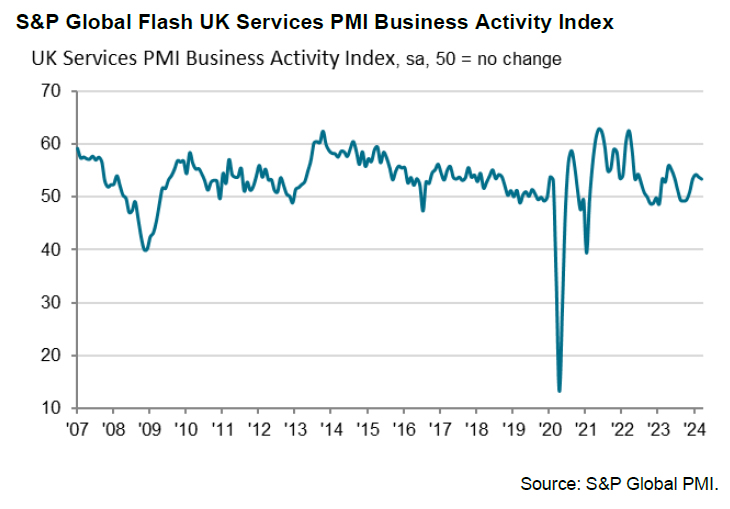

UK PMI manufacturing hits 20-month high, services ease slightly

UK PMI Manufacturing rose from 47.5 to 49.9 in March, above expectation of 47.9, a 20-month high. PMI Services fell slightly from 53.8 to 53.4, below expectation of 53.8. PMI Composite ticked down from 53.0 to 52.9.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, interprets the data as evidence of UK's recovery from the recession in the latter half of 2023. The aggregate business activity for Q1 suggests 0.25% GDP growth, marking the best quarter since mid-last year

Despite the optimistic growth indicators, inflation remains a pressing issue, particularly in the services sector, where "stubbornly sticky" inflation pressures continue. Moreover, the manufacturing sector saw "renewed inflation".

While the overall inflation rate is expected to decline in the coming months, March's PMI data point to "elevated underlying price pressures," possibly influencing BoE to exercise caution. Williamson, suggests that a decisive shift towards lower interest rates should only occur once there is clear evidence of moderating wage growth.

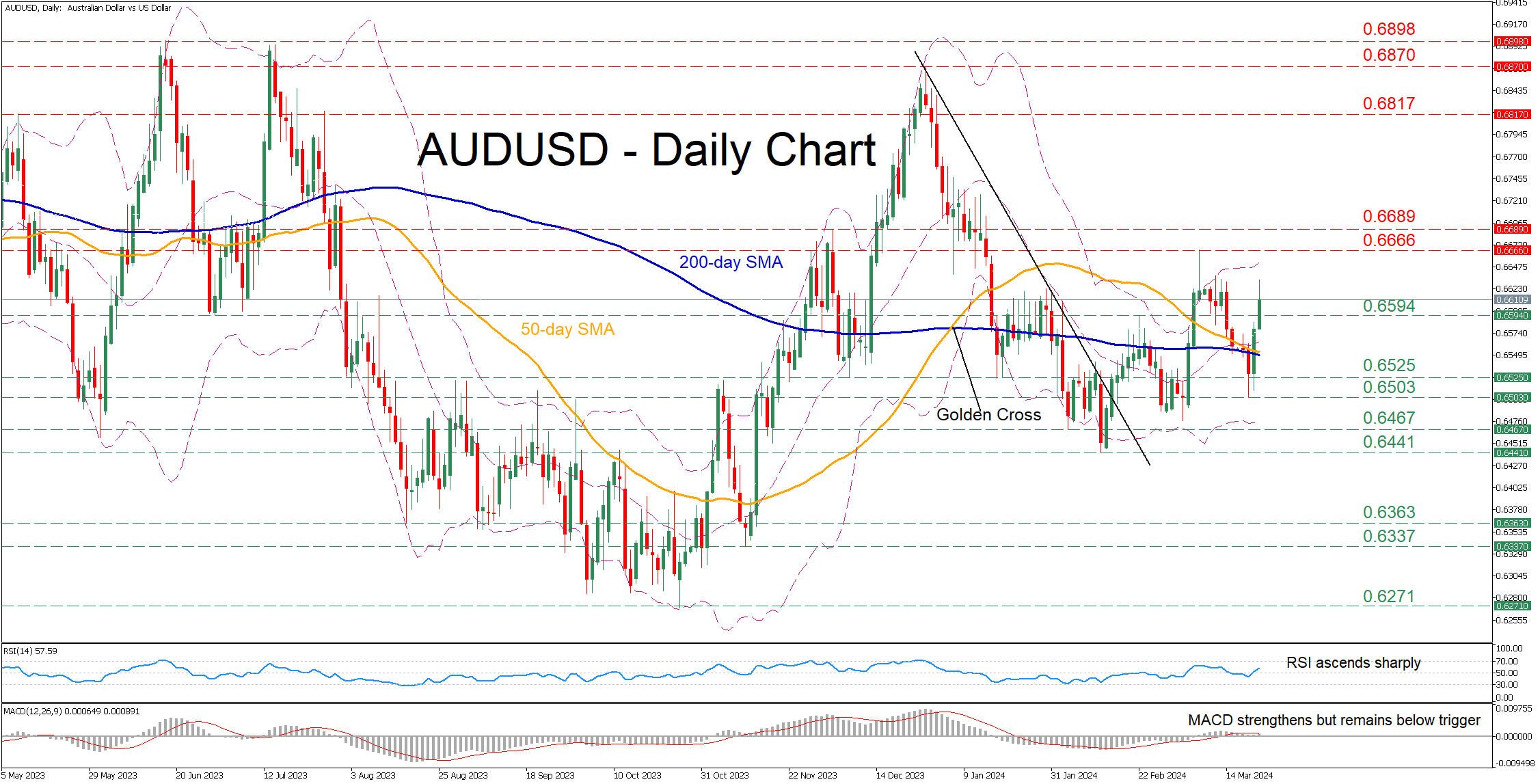

AUDUSD Advances Sharply in the FOMC Aftermath

- AUDUSD was in a steady retreat since early March

- But finds feet and reclaims both SMAs after dovish FOMC

- Momentum indicators improve drastically

AUDUSD had been losing ground since the beginning of March, dropping below its descending 50- and 200-day simple moving averages (SMAs). However, the pair managed to pause its retreat and reverse back higher with some help from the dovish FOMC signals on Wednesday.

Should the advance resume, the price could initially test the March peak of 0.6666. Further upside attempts could then cease at the December 2023 resistance of 0.6689 ahead of the May 2023 high of 0.6817. If that hurdle also fails, the spotlight could turn to the December high of 0.6870.

On the flipside, bearish actions could send the price lower to test the recent resistance of 0.6594, which could serve as support in the future. A violation of that zone could pave the way for 0.6525, a region that provided both support and resistance in recent months. Even lower, the recent deflection point of 0.6503 could curb further declines.

In brief, AUDUSD managed to put an end to its recent slide and reclaim its converging 50- and 200-day SMAs. For the short-term picture to turn bullish though, the pair needs to jump above its March high of 0.6666.

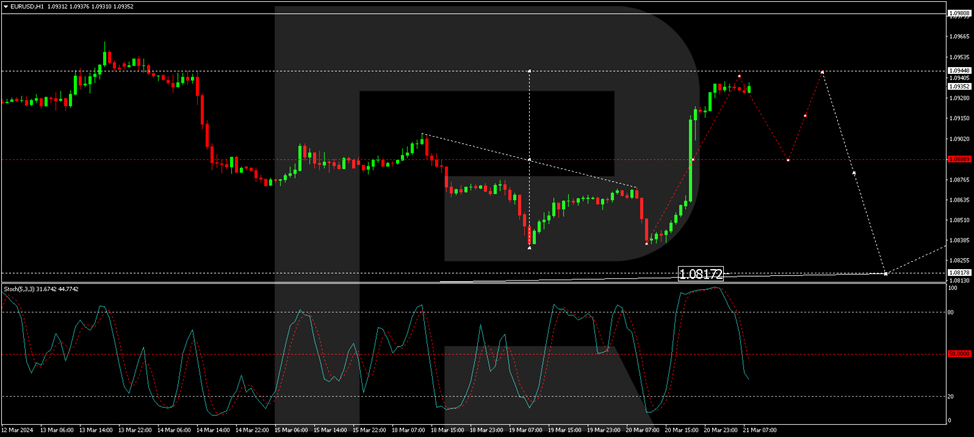

EUR/USD Soars Following Fed’s Decision on Interest Rate Cuts

The EUR/USD pair soared to a weekly high of 1.0933 on Thursday following the Federal Reserve System's announcement of three interest rate cuts planned for 2024. These adjustments will reduce borrowing costs by 75 basis points.

The interest rate remains at 5.5% annually, its highest in 23 years, and has been unchanged for five consecutive meetings.

Federal Reserve Chair Jerome Powell noted that the regulator plans to reduce the rate this year, likely achieving a 75-basis point reduction over three stages by the end of 2024.

The Fed also continues its balance sheet contraction plan, not reinvesting proceeds from matured bonds and having no plans to sell bonds from its portfolio.

The Fed's outlook was relatively optimistic this time, expecting the American economy to grow by 2.1% quarter-on-quarter in Q1 2024. Although the Consumer Price Index is decreasing, it is still high, and the employment market is strong due to new job creation.

The Fed's inflation target remains at 2%, with risks to expectations seen as balanced.

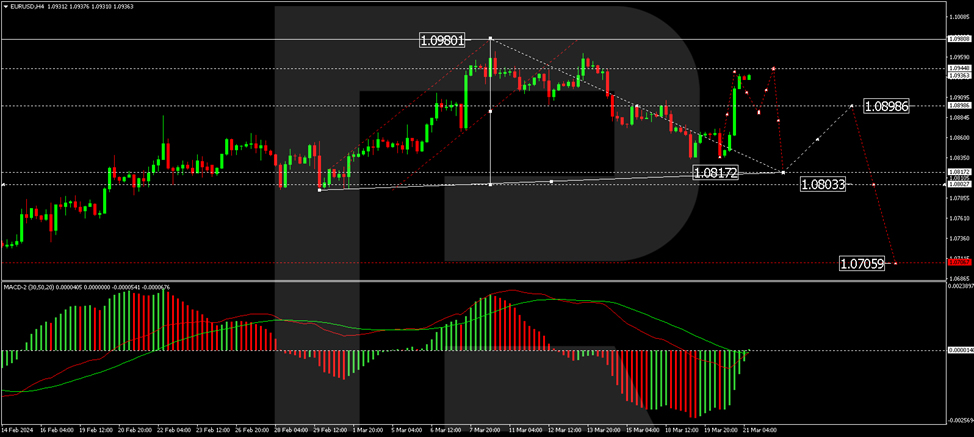

EUR/USD technical analysis

Influenced by the news, the H4 EUR/USD chart found support at 1.0836, leading to a correction. Today, the price is anticipated to reach 1.0944, followed by a subsequent downward movement targeting 1.0818. The MACD indicator supports this scenario, with its signal line below zero, indicating further declines to new lows.

On the H1 EUR/USD chart, a corrective growth structure towards 1.0940 has formed. After reaching this level, a decline to 1.0888 is possible, followed by a potential rise to 1.0944. Then, a new downward wave to 1.0818, the first target, may begin. The Stochastic oscillator, with its signal line below 50, indicates a continuation of the decline towards 20.

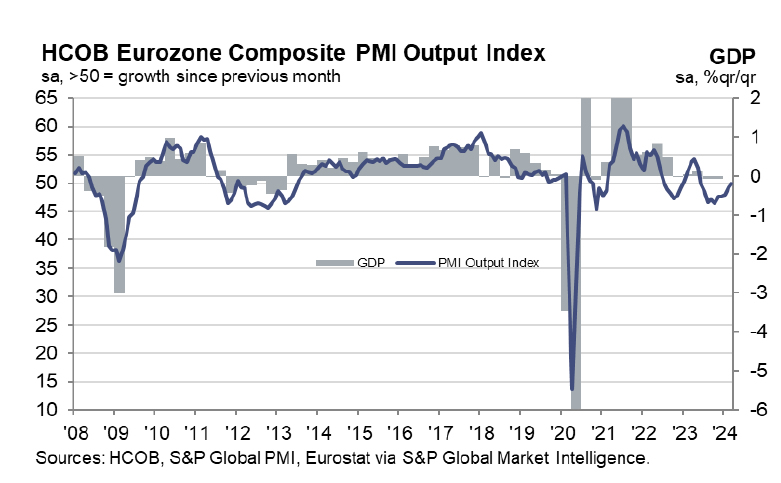

Eurozone PMI composite ticks up to 49.9, price development not enough to alter ECB’s course

Eurozone PMI Manufacturing from 46.5 to 45.7 in March, below expectation of 47.0. PMI services, on the other hand rose from 50.2 to 51.5, above expectation of 50.5 a 9-month high. PMI Composite ticked up from 49.2 to 49.9, also a 9-month high.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, highlighted the "clear weakness" in manufacturing, attributing it largely to Germany's industrial performance. On a brighter note, the further expansion in the services PMI is considered a "positive development."

From a monetary policy perspective, ECB may find some solace in the report's implications on inflationary pressures. Notably, the services sector, which is typically sensitive to wage dynamics, has not seen a further escalation in price pressures.

However, these developments, as de la Rubia notes, are "not enough" to alter the ECB's tentative plan to commence rate cuts in June, rather than an earlier move in April.

Also released, France PMI Manufacturing fell from 47.1 to 45.8. PMI Services fell from 48.4 to 47.8. PMI Composite fell from 48.1 to 47.7.

Germany PMI Manufacturing fell from 42.5 to 41.6. PMI Services rose from 48.3 to 49.8. PMI Composite rose from 46.3 to 47.4.

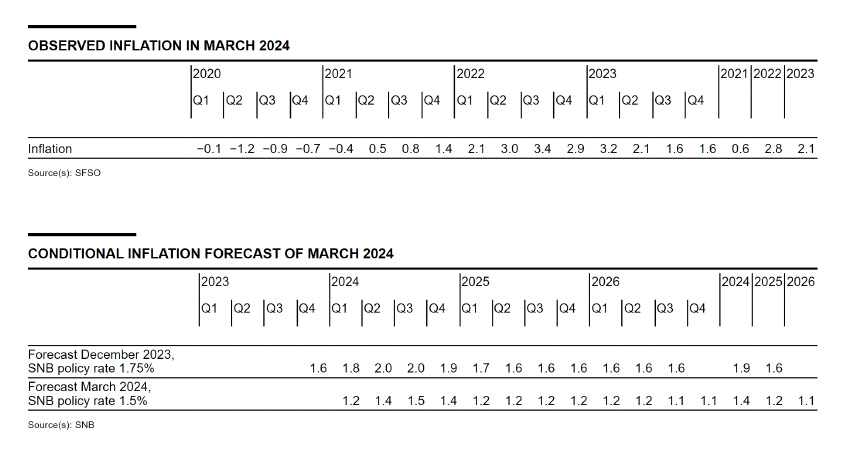

SNB cuts interest rate, sharply slashes inflation forecasts

In a surprising move, SNB announced a -25bps cut in its policy rate, bringing it down to 1.50%. This decision also introduced a tiered system for the remuneration of banks' sight deposits held at SNB. Deposits up to a specified threshold will earn interest at the policy rate, while those exceeding this limit will attract only 1.0% higher rate. Furthermore, SNB affirmed its readiness to intervene in the foreign exchange market if deemed necessary.

The rationale behind the rate cut, as outlined by the SNB, is the "effective" management of inflation over the past two and a half years, which has allowed inflation rates to settle below the 2% mark for several months. This achievement aligns with the SNB's definition of price stability and sets the stage for a conducive economic environment in the foreseeable future.

The new conditional inflation forecasts are revised sharply lower even with a lower policy rate. SNB project a modest increase in inflation from 1.2% in Q1 to 1.5% in Q2 of this year, followed by a decline to 1.2% in Q1 2025, and a further decrease to 1.1% in the second half of 2026.

(SNB) Swiss National Bank Eases Monetary Policy and Lowers SNB Policy Rate to 1.5%

The Swiss National Bank is lowering the SNB policy rate by 0.25 percentage points to 1.5%. The change applies from tomorrow, 22 March 2024. Banks' sight deposits held at the SNB will be remunerated at the SNB policy rate up to a certain threshold, and at 1.0% above this threshold. The SNB also remains willing to be active in the foreign exchange market as necessary.

The easing of monetary policy has been made possible because the fight against inflation over the past two and a half years has been effective. For some months now, inflation has been back below 2% and thus in the range the SNB equates with price stability. According to the new forecast, inflation is also likely to remain in this range over the next few years.

With its decision, the SNB is taking into account the reduced inflationary pressure as well as the appreciation of the Swiss franc in real terms over the past year. The policy rate cut also supports economic activity. Today's easing thus ensures that monetary conditions remain appropriate.

The SNB will continue to monitor the development of inflation closely, and will adjust its monetary policy again if necessary to ensure inflation remains within the range consistent with price stability over the medium term.

Inflation has declined further since the beginning of the year, and stood at 1.2% in February. This decrease was attributable to lower goods inflation. Inflation is currently being driven above all by higher prices for domestic services.

The new conditional inflation forecast is significantly lower than that of December. In the short term, this is above all due to the fact that price momentum in the case of some categories of goods has slowed more quickly than had been expected in December. In the medium term, lower second-round effects are leading to a downward revision. Over the entire forecast horizon, the conditional inflation forecast is within the range of price stability (cf. chart). The forecast puts average annual inflation at 1.4% for 2024, 1.2% for 2025 and 1.1% for 2026 (cf. table). The forecast is based on the assumption that the SNB policy rate is 1.5% over the entire forecast horizon.

The global economy grew moderately in the fourth quarter of 2023. Having declined rapidly in many countries in 2023, inflation has decreased at a somewhat slower pace in recent months. Inflation in many countries remains above central banks' targets. Against this background, many central banks have left their restrictive monetary policy unchanged for the time being.

Global economic growth is likely to remain moderate in the coming quarters. Inflation is likely to decline further, not least due to the restrictive monetary policy.

This scenario for the global economy is still subject to significant risks. Inflation could remain elevated for longer in some countries, necessitating a tighter monetary policy there than expected in the baseline scenario. Equally, geopolitical tensions could increase. It therefore cannot be ruled out that global economic activity will be weaker than assumed.

Swiss GDP growth was moderate in the fourth quarter of last year. The services sector expanded again, while value added in manufacturing stagnated. Unemployment rose somewhat further, and the utilisation of overall production capacity was normal.

Growth is likely to remain modest in the coming quarters. The weak demand from abroad and the appreciation of the Swiss franc in real terms over the past year are having a dampening effect. Overall, Switzerland's GDP is likely to grow by around 1% this year. In this environment, unemployment is likely to continue to rise gradually, and the utilisation of production capacity is likely to decline somewhat further.

Our forecast for Switzerland, as for the global economy, is subject to significant uncertainty. The main risk is weaker economic activity abroad.

Momentum on the mortgage and real estate markets has weakened noticeably in recent quarters. However, the vulnerabilities in these markets remain.

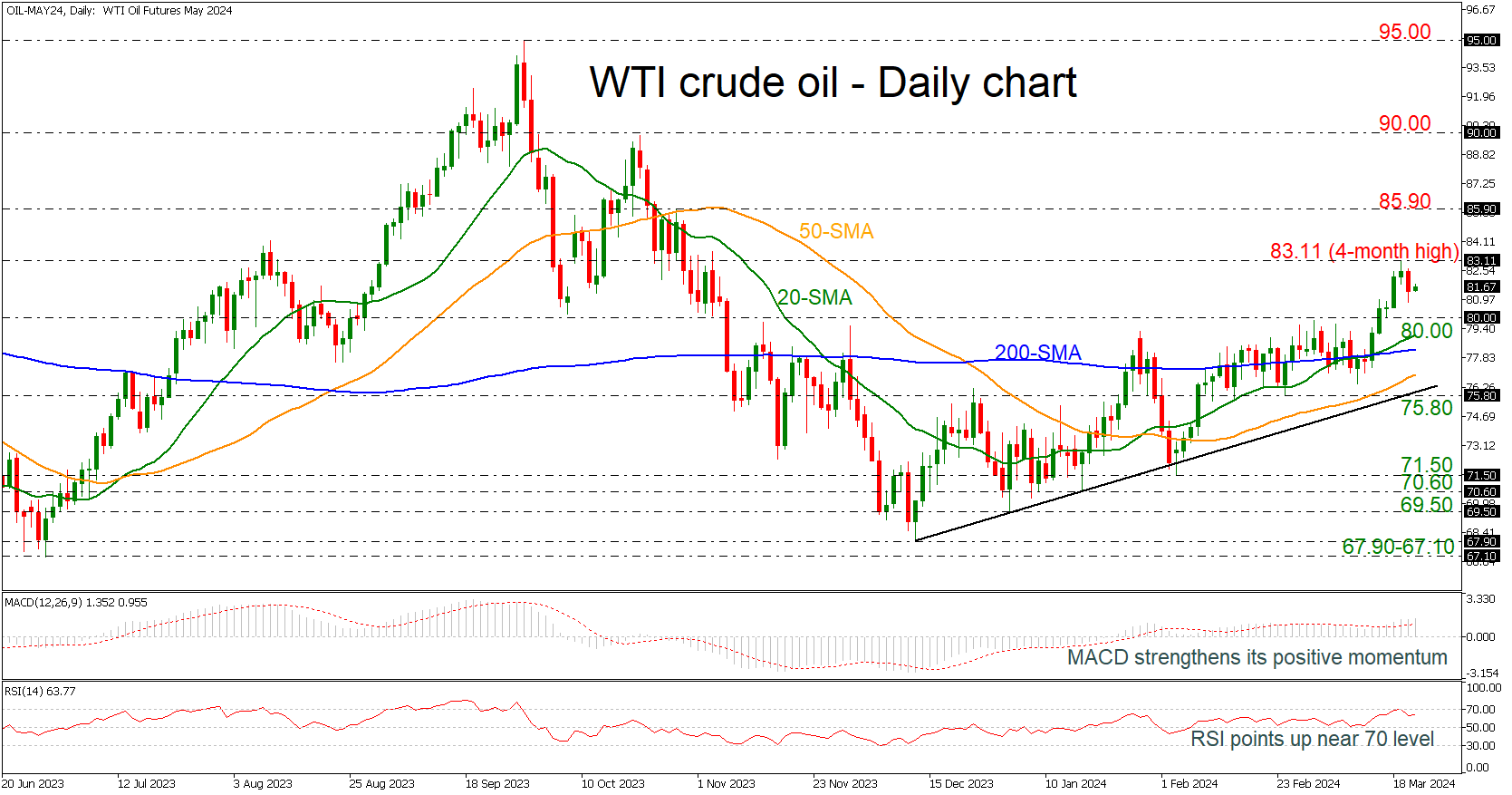

WTI Crude Oil Futures Slip from 4-Month Peak

- WTI crude oil looks positive despite the latest drop

- 20- and 200-day SMAs post bullish cross

- MACD and RSI show positive signs

WTI crude oil futures are easing after the climb towards the new four-month high of 83.11 but the broader outlook remains bullish, especially after the rally above the 80.00 round number.

According to technical oscillators, the MACD is extending its positive momentum above its trigger and zero lines, while the RSI is pointing slightly up near the 70 threshold. Also, the 20- and the 200-day simple moving averages (SMAs) posted a golden cross, confirming the upside structure.

If the market continues to fall, immediate support for traders to have in mind is the 80.00 mark ahead of the 20- and the 200-day SMAs currently at 79.00 and 78.20 respectively. Beneath these lines, the 50-day SMA at 76.87 and the short-term uptrend line around the 75.80 support may halt bearish actions.

In the positive scenario, a jump beyond the 83.11 resistance may drive the price towards the 85.90 barricade before meeting the 90.00 handle, switching the medium-term outlook to a more bullish one.

To sum up, WTI crude oil has been developing in an ascending tendency since December 13 and only a dive below the rising trend line may change the current trend.

Interesting Divide Between Markets’ and Our Interpretation on Fed

Markets

Let’s dive right into yesterday’s Fed meeting. There’s an interesting divide between markets’ and our interpretation. For the former it was nothing but an outright dovish, cuts-are-coming-soon tribute. The three major US stock indices simultaneously closed at record highs. US yields turned south, slipping more than 8 bps at the front. The dollar tanked. EUR/USD bounced of an intraday low around 1.084 to finish around 1.092. DXY returned sub 104 to 103.38. USD/JPY aborted the test of the 2022-multi-decade high while still closing the day with net gains (151.26). This sharp reaction was mainly rooted in the March dot plot confirming the three 2023 rate cuts from December. After two CPI beats, ongoing strong hiring and broad economic resilience, some feared the Fed would have backtracked. Chair Powell also downplayed the consensus-topping inflation outcomes, saying “they haven’t really changed the overall story, which is that of inflation moving down gradually on a sometimes bumpy road toward 2%.” The updated forecasts tell us a completely different story. Growth was revised upwards across the policy horizon, especially for this year (2.1% from 1.4%). Unemployment rate saw some minor downward revisions from already low levels. Core PCE was lifted from 2.4% to 2.6% this year before easing to 2.2% and 2% in the years thereafter with FOMC participants in a shift with December seeing upside (instead of balanced) risks. The 2024 policy rate median prognosis indeed reflects three cuts. But the Fed removed one rate cut for both 2025 (3.75-4%) and 2026 (3-3.25%). In addition: the neutral rate gently nudged higher. It’s marginal (from 2.5% to 2.6%) but highly symbolical. The forecast distribution has generally shifted higher with the one for the equilibrium rate in particular catching the eye. There are now 7 out of 18 members seeing a neutral rate of at least 3% compared to 4 in December and only one member (down from 3) believes the neutral rate is <2.5%. Gut feeling tells us that yesterday’s market reaction won’t last very long. It takes one good labour market report, consensus-topping inflation outcome or other high-profile data point for markets to reconsider. Fortunately for the Fed, these won’t show up on the eco calendar for at least another week. There are, however, the PMIs today. The US edition is usually of secondary importance (compared to the ISMs), but a strong reading may already challenge yesterday’s market view. Those for the euro area are expected to further bottom out. The services series in particular is seen edging further north of 50. Bear in mind, though, that the EMU wide figure has been dramatically weighed down by the German and to a lesser extent the French malaise. EMU PMIs ex Germany and France already suggested moderate expansion. Barring a major upside surprise, however, we don’t expect them to alter ECB-forged expectations for a June rate cut. Breaking above EUR/USD 1.0981 (March interim high) looks implausible, especially should US Treasuries underperform in some counteraction today.

News & Views

The Czech National Bank cut its policy rate by 50 bps to 5.75% in a split decision. Two out seven governors voted in a favour of a 75 bps rate cut. Czech inflation declined to the CNB’s 2% inflation target, but risks to the outlook remain modestly inflationary. Therefore, the CNB will continue with a cautious approach when it comes to further rate cuts taking into account FX developments, the effect of fiscal policy on the economy, the labour market situation and the evolution of domestic and external demand as well. EUR/CZK ticked lower from 25.30 to 25.20 after the expected CNB meeting outcome. CZK swap rates added 3 to 4 bps.

Australian employment growth surged by 116.5k in February (vs 40k expected). Both full-time occupations (78.2k) and part-time jobs (38.3k) contributed. January figures were upwardly to 15.3k. The unemployment rate dropped from 4.1% to 3.7% (vs 4% consensus) though the participation rate only slightly advanced from 66.6% to 66.7%. The large increase in employment in February followed larger-than-usual numbers of people in December and January who had a job that they were waiting to start or to return to. This translated into a larger-than-usual flow of people into employment in February and even more so than February last year. Seasonally adjusted monthly hours worked rose by 2.8%. Following today’s labour market data, money markets pushed their expected start to a rate cut cycle lower from August to September. AUD swap rates add 6 to 8 bps across the curve this morning, pushing AUD/USD from the low 0.65 area yesterday morning to 0.6630 currently, approaching first resistance at 0.6639.

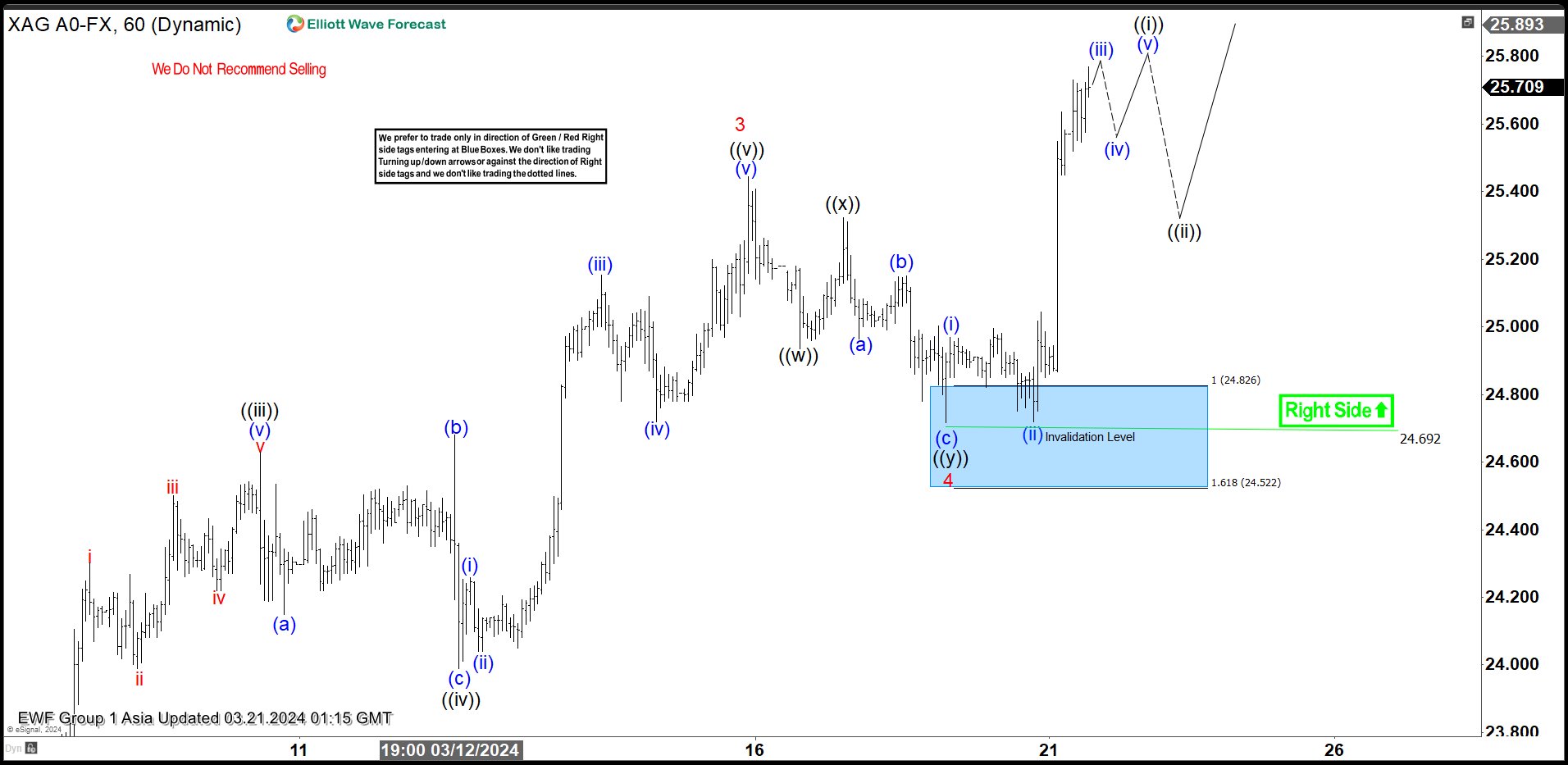

Silver (XAGUSD) Should Continue to Extend Higher

Short Term Elliott Wave view in Silver (XAGUSD) suggests that rally from 1.22.2024 low is in progress as a 5 wave impulse. Up from 1.22.2024 low, wave 1 ended at 23.32 and pullback in wave 2 ended at 21.94. Up from there, wave ((i)) ended at 23.49 and wave ((ii)) ended at 22.25. Wave ((iii)) higher ended at 24.62 and pullback in wave ((iv)) ended at 23.98. Final leg wave ((v)) ended at 25.44 which completed wave 3.

Wave 4 pullback unfolded as a double three Elliott Wave structure as the 1 hour chart below shows. Down from wave 3, wave ((w)) ended at 24.93 and wave ((x)) ended at 25.32. The metal then extended lower in wave ((y)) towards 24.69 which completed wave 4. The metal then turns higher in wave 5. Up from wave 4, wave (i) ended at 24.96 and wave (ii) ended at 24.72. Silver should end wave (iii) soon, then pullback in wave (iv) before turning higher again in wave (v) to end wave ((i)). Afterwards, it should pullback in wave ((ii)) to correct cycle from 3.19.2024 low in 3, 7, or 11 swing before it resumes higher again. Near term, as far as pivot at 24.69 low stays intact, expect dips to find support in 3, 7, 11 swing for further upside.

Silver (XAGUSD) 60 Minutes Elliott Wave Chart

XAGUSD Elliott Wave Video

https://www.youtube.com/watch?v=aOuLWp1yc98