Sample Category Title

Cliff Notes: Four Sets of Circumstances, One Intent

Key insights from the week that was.

In Australia, the RBA Board once again decided to leave the cash rate unchanged at 4.35% after reflecting on recent data. The new information included the Q4 National Accounts, which confirmed the economic slowdown broadened into year-end, and the Q4 Wage Price Index, which revealed an underlying slowdown in private sector wages growth associated with a softening labour market (more below) and benign inflation expectations.

Consistent with the Board’s objectives, these results led to language changes in the final paragraph: “a further increase in interest rates cannot be ruled out” replaced with “the Board is not ruling anything in or out”; and the removal of the Board “will do what is necessary to achieve that outcome” – a significant decision given versions of this language have been in the media release since the first rate hike in May 2022. Concern over upside risks to inflation have not fully dissipated however, keeping the Board open to a range of possibilities.

As discussed by Chief Economist Luci Ellis in a video update mid-week, the tone of RBA communications suggest they will remain on hold for some months yet, with more progress towards target necessary to extinguish concern over lingering risks. We continue to expect a gradual easing cycle from September, a 25bp cut per quarter to take the cash rate to 3.10% at Q3 2025.

Before moving offshore, a quick note on the Australian labour market. The February Labour Force Survey was an eventful update, a much stronger-than-expected +116.5k gain in employment reported alongside a material fall in the unemployment rate, from 4.1% to 3.7%, following weak results over December and January. Abstracting from this volatility, the labour market continues to soften at a modest pace, with employers seeking to adjust labour usage predominately doing so by reducing average hours worked (–1.9%yr). Though we expect employment growth to moderate below the pace of population growth, material economy-wide employment declines seem unlikely.

Offshore, the Bank of Japan raised its policy rate to the range of 0% – 0.1% having “assessed the virtuous cycle between wages and prices” and judged “that the price stability target of 2 percent would be achieved in a sustainable and stable manner toward the end of the projection period”. This was the BoJ’s first hike in 17 years and was accompanied by the scrapping of the YCC target and ETF/ J-REITs purchases. However, government bond purchases will continue broadly at the same pace as before, and the BoJ made clear it will guard against a rapid rise in long-term interest rates.

In a subsequent press conference, Governor Kazuo Ueda noted that they made the move now to avoid “large and rapid rate hikes” in the future. This suggests the BoJ believe inflation is not only expected to achieve the medium-term target, but that it could exceed it sustainably. While this is possible, we believe the inflation pulse is more likely to disappoint, keeping the policy rate at or very near its current level. Momentum in services inflation can only persist if household spending grows robustly, which is not currently the case. And, for consumers to feel comfortable spending, Japan’s deeply entrenched saving mindset must be dislodged by sustained real wage growth.

Over in the US, the FOMC kept rates steady as expected. More importantly, their refreshed forecasts pointed to both a soft landing for activity and inflation at target. GDP growth projections were updated to 2.1% in 2024 and 2.0% in 2025 and 2026 from 1.4%, 1.8% and 1.9%, seeing the economy grow above its potential rate through the entire projection period. The members’ inflation projections are little changed however, recent upside surprises seeing 2024’s core inflation forecast upgraded to 2.6%, but still set to give way to a return to target inflation in 2025-26. It is also important to recognise that Chair Powell saw no material change in inflation dynamics in the recent data, the return to target inflation waiting on shelter’s normalisation.

The fed funds rate profile suggests the FOMC see a degree of medium-term inflation risk. Three rate cuts continue to be forecast for 2024, but the median number of rate cuts in 2025 has been reduced by one to three. The longer run rate was also lifted 10bps to 2.6%. We continue to anticipate four rate cuts in both 2024 and 2025, beginning in June 2024 and ending late-2025 at 3.375%. Our higher terminal rate reflects concern over inflation pressures from tight capacity across housing and infrastructure as well as the likelihood of reshoring delivering higher prices for some goods. A modest contractionary stance will be required to manage both inflation risks and expectations. Activity growth and employment are likely to wear the cost, a higher unemployment rate circa 4.5% forecast through at least 2025.

Finally, the Bank of England also kept rates steady at 5.25% this week. Of significance though, it was an 8-1 decision, the two members who had previously dissented in favour of a hike now with the ‘on hold’ majority. The lone dissenter in March argued instead for an immediate cut. Contained in the minutes were diverse views on wages and inflation, particularly for services. Overall though, outcomes were seen as evolving broadly as expected, and there was a degree of comfort that downside risks for activity were contained. The BoE Agents Report, which gathers the views of businesses across the country, was constructive on both inflation (albeit with lingering concerns over services pricing) and activity. The BoE will be hoping these views prove prescient and allow the UK to experience its own version of a soft landing. We continue to expect the BoE to follow the FOMC and ECB through this cutting cycle, though there is a higher chance of sticky inflation causing delays in the UK.

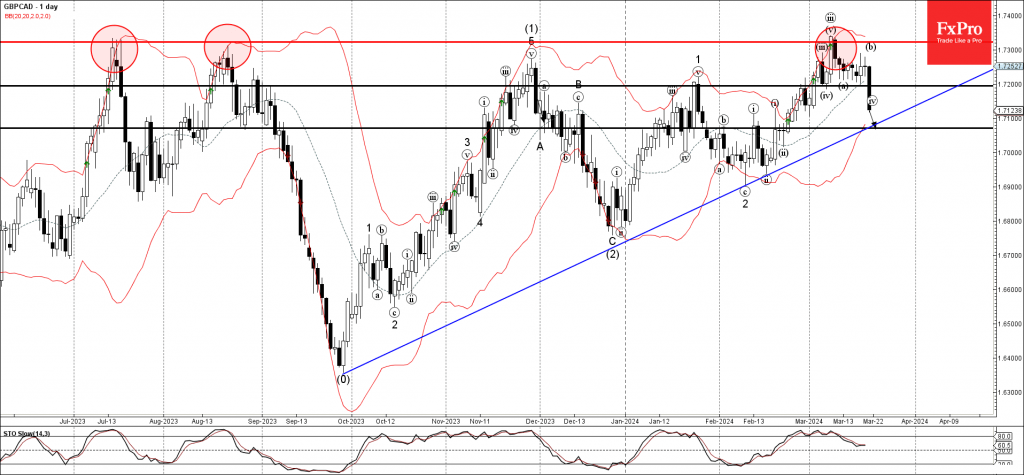

GBPCAD Wave Analysis

- GBPCAD broke support level 1.7200

- Likely to fall to support level 1.7070

GBPCAD currency pair continues to fall after recently breaking the support level 1.7200 (former monthly high from February, which has been reversing the pair from last month).

The breakout of the support level 1.7200 accelerated the active short-term impulse wave c.

Given very strongly bearish sterling sentiment seen today, GBPCAD currency pair can be expected to fall to the next support level 1.7070, coinciding with the support trendline from September.

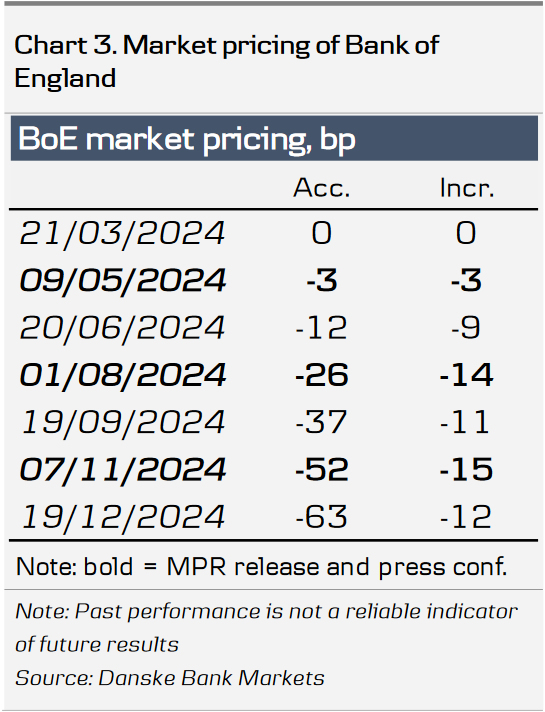

Bank of England Review – Gearing Up for a June Cut

- At today's monetary policy meeting the BoE left the Bank Rate unchanged at 5.25% as widely expected.

- The BoE delivered a dovish twist to its forward guidance and general communication. This marks an important first step to an eventual cutting cycle.

- EUR/GBP moved slightly higher on the dovish vote split and communication.

As expected, the Bank of England (BoE) decided to keep the Bank Rate unchanged at 5.25%. The vote split indicated a continued split committee but to a much lesser extent than previously. At this meeting, 8 members voted for an unchanged decision and one member for a 25bp cut compared to a former 6-2-1 split vote split with hawks Haskel and Mann changing their vote from a hike to an unchanged decision.

The BoE struck a dovish tone in its statement today noting that "the Committee recognised that the stance of monetary policy could remain restrictive even if Bank Rate were to be reduced, given that it was starting from an already restrictive level". We think this is an important first step in signalling that start to an impending cutting cycle. The BoE retained much of its wording in terms of forward guidance, repeating "Monetary policy will need to remain restrictive for sufficiently long to return inflation to the 2% target" and "the Committee will keep under review for how long Bank Rate should be maintained at its current level".

Before the next meeting on 9 May, which will include updated projections, it is limited what we get of data. Namely one inflation report for March and the labour market report for February/March. While we expect the UK economy to show further signs of weakness and inflation and wage growth to level off, we do not believe that the BoE will feel comfortable enough to opt for a rate cut at the May meeting. We believe that we would have to see significant downside surprises across both inflation and labour market data for this to be the case.

Rates. The reaction in rates markets was muted. 2Y Gilt yields moved slightly lower on the statement but fully retraced the move during the afternoon. Markets stick to expecting the first 25bp cut in August but increased the probability for an earlier move.

FX. Following the release of the statement, EUR/GBP moved higher on both the dovish vote split and guidance from the statement. Overall, we see relative rates as a negative for GBP and see current levels as attractive levels to sell GBP. We forecast EUR/GBP towards 0.88 and stay short GBP/USD.

Our call. We continue to expect the BoE to prime markets for a rate cut at the May meeting, which includes updated projections, delivering the first cut of 25bp in June. We think today's meeting supports that notion. We subsequently expect 25bp cuts in the following quarters, totalling 75bp of cuts for 2024. Markets are pricing 77bp for the remainder of the year with the first 25bp cut fully priced by August.

Sunset Market Commentary

Markets

The EMU economy came close to stabilizing in March with price pressures easing. The composite PMI recovered slightly more than hoped, from 49.2 to 49.9 (vs 49.7 consensus), matching the best (least bad) outcome since June of last year. Divergence between a weak export-oriented manufacturing sector (45.7 from 46.5) and a recovering domestic services industry (51.1 from 50.2) increased. Ongoing falls in output in France (composite 47.7) and Germany (composite 47.4; mainly manufacturing weakness) offset a gathering upturn in the rest of the EMU, pointing to an even more uneven economic picture. Encouragingly, order books fell at a reduced rate and business confidence about the year ahead improved to a 13-month high. In manufacturing, destocking is close to no longer being a drag on production. Supplier delivery times at goods producers improved, facilitating a further fall in manufacturing input prices. Service sector input cost and selling price inflation rates meanwhile remained elevated due to higher wage costs, though a cooling in the pace of increase in cost burdens was recorded. Today’s PMI’s keep the ECB on schedule to conduct a first 25 bps rate cut in June. Following the release, EUR/USD fell back from 1.0940 to just below 1.09. Early US eco data (consensus-beating Philly Fed Business Outlook, another low number of weekly jobless claims and decent PMI’s; composite 52.2) help the greenback out as well. German yields currently lose up to 3.5 bps at the front end of the curve, but that’s mainly because of lower opening catching up with yesterday’s post-Fed market reaction. Changes on the US yields curve vary between -0.9 bps (30-yr) and +3 bps (2-yr).

The Bank of England kept its policy rate unchanged at 5.25%, but the voting pattern changed. Hawkish members Mann and Haskel no longer advocate a 25 bps rate hike, joining the majority. BoE Dhingra voted for a second consecutive meeting in favor of a 25 bps rate cut and is now the sole dissenter on the 9-headed MPC. Forward guidance at today’s intermediate meeting was left unchanged as well: the BoE keeps under review how long rates should be kept unchanged. Minutes added that monetary policy could remain restrictive even in case of rate cuts. “Things are moving in the right direction”, BoE chair Bailey later added at the press conference stressing encouraging signs that inflation is coming down. CPI inflation is projected to fall to slightly below the 2% target in 2024 Q2, marginally weaker than previously expected owing to the freeze in fuel duty announced in the Budget. UK Gilts outperform today with yields sliding up to 7 bps for the 2-yr tenor as market thinking shifts from the August to the June meeting for a first BoE rate cut. EUR/GBP rises from 0.8540 to 0.8560.

News & Views

The Swiss National Bank cut its policy rate by 25 bps to 1.50% after recently suggesting that the (real) appreciation of the franc had contributed more than enough to slow inflation. It also further eroded (export) demand. The SNB sharply downwardly revised its 2024-26 inflation forecast. At 1.4%, 1.2% and 1.1% respectively, inflation remains easily within the 0%-2% price stability band. In the short term, goods prices in particular continue to ease while inflation is mainly driven by services prices. Longer term, the risk of second-round effects is significantly reduced. With inflation back on track, the SNB can shift its focus back to stimulating economic growth. The SNB expects (moderate) growth of 1% this year and unemployment may rise a bit further. The Swiss franc takes a logical step back from EUR/CHF 0.9675 to 0.9765. The SNB officially has no exchange rate target, but a further depreciation to EUR/CHF 1.00 would probably be welcomed. If this (real) FX correction doesn’t go according to plan, the SNB may further scale back policy tightening in June given low inflation. We don’t see today’s SNB's action as a harbinger of global "frontloading" of monetary easing. Switzerland is in a unique situation.

The Norges Bank kept its policy rate unchanged at 4.5%. Monetary policy is having a tightening effect and economic growth is low. Inflation is slowing but still markedly above target (4.5% Y/Y in February), mainly because of elevated services inflation. Sharply increased business costs, high wage growth and the Norwegian krone’s depreciation through 2023 will contribute to keeping inflation elevated ahead. Compared to the December policy report, growth was nevertheless higher than expected while inflation cooled more. The MPC remains concerned that prematurely lowering its policy rate could keep inflation high and is ready to raise the policy rate again if necessary. The base scenario assumes unchanged rates until autumn though. EUR/NOK is little changed at 11.55.

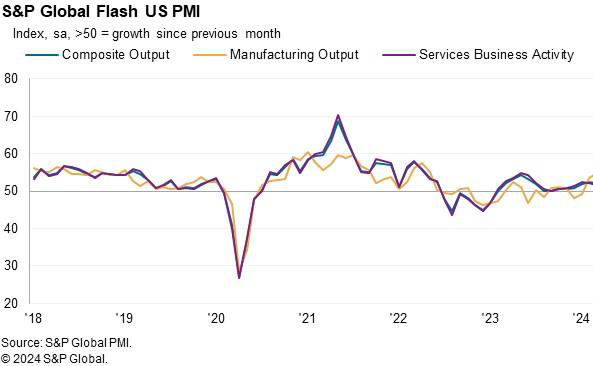

US PMI composite falls to 52.2, unwelcome consumer price pressure in the coming months

US PMI Manufacturing rose from 52.2 to 52.5 in March, a 21-month high. PMI Services fell from 52.3 to 51.7. PMI Composite also fell from 52.5 to 52.2.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

"Further expansions of both manufacturing and service sector output in March helped close off the US economy's strongest quarter since the second quarter of last year. The survey data point to another quarter of robust GDP growth accompanied by sustained hiring as companies continue to report new order growth.

"The brightest news came from the manufacturing sector, where production is now growing at the fastest rate since May 2022. Production gains are linked to improving demand for goods both at home and abroad, driving a further upturn in business confidence in the outlook.

"Service providers meanwhile reported a slower pace of expansion than factories, with the rate of increase also moderating slightly compared to February, linked in part to ongoing cost of living pressures. However, service providers have also become increasingly optimistic about the outlook, with confidence striking a 22-month high in March to suggest the broad-based economic expansion seen in March will persist into the summer.

"A steepening rise in costs, combined with strengthened pricing power amid the recent upturn in demand, meant inflationary pressures gathered pace again in March. Costs have increased on the back of further wage growth and rising fuel prices, pushing overall selling price inflation for goods and services up to its highest for nearly a year. The steep jump in prices from the recent low seen in January hints at unwelcome upward pressure on consumer prices in the coming months."

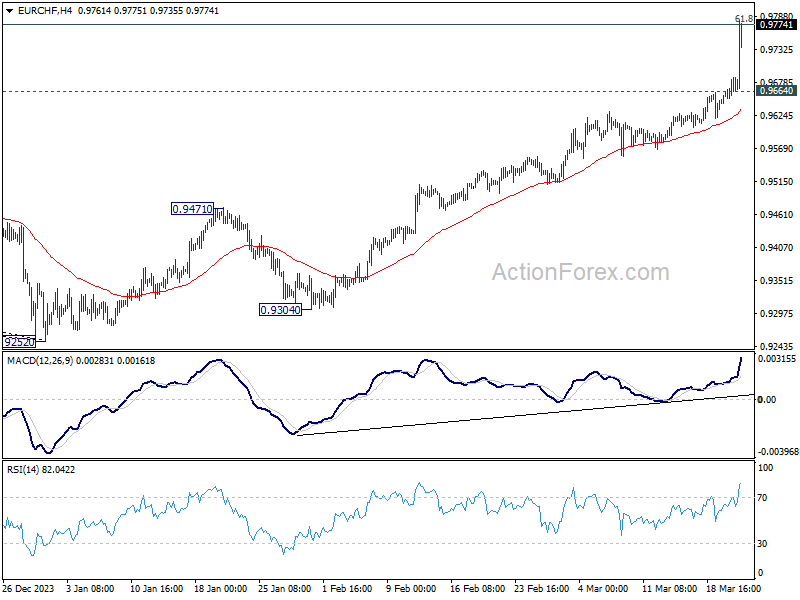

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9656; (P) 0.9672; (R1) 0.9703; More..

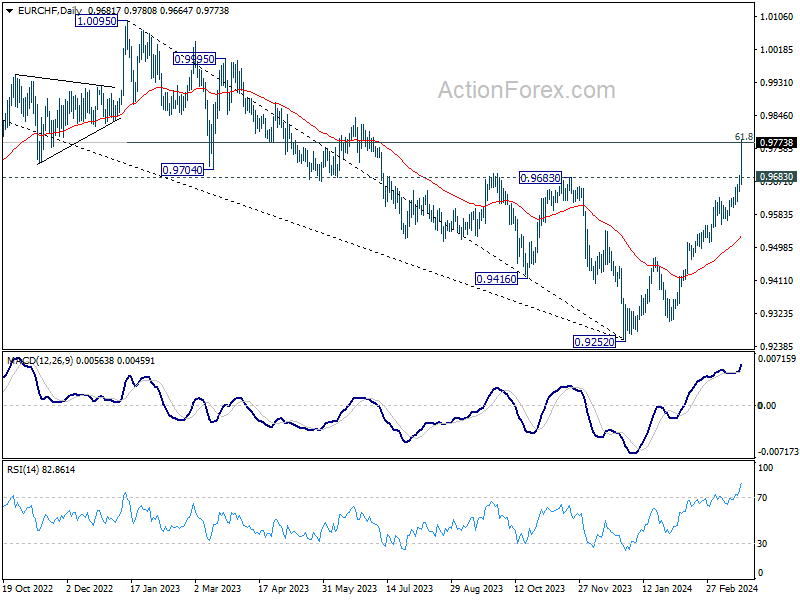

EUR/CHF surges to as high as 0.9780 today and met 61.8% retracement of 1.0095 to 0.9252 at 0.9773 already. The strong break of 0.9683 resistance carries larger bullish implications. Intraday bias stays on the upside. Sustained trading above 0.9773 will pave the way to 1.0095 key resistance next. On the downside, below 0.9664 minor support will turn intraday bias neutral and bring consolidations, before staging another rally.

In the bigger picture, the strong break of 0.9683 resistance indicates medium term bottoming at 0.9252 already, on bullish convergence condition in W MACD. Rise from there would now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303. This will remain the favored case as long as 55 D EMA (now at .9530) holds.

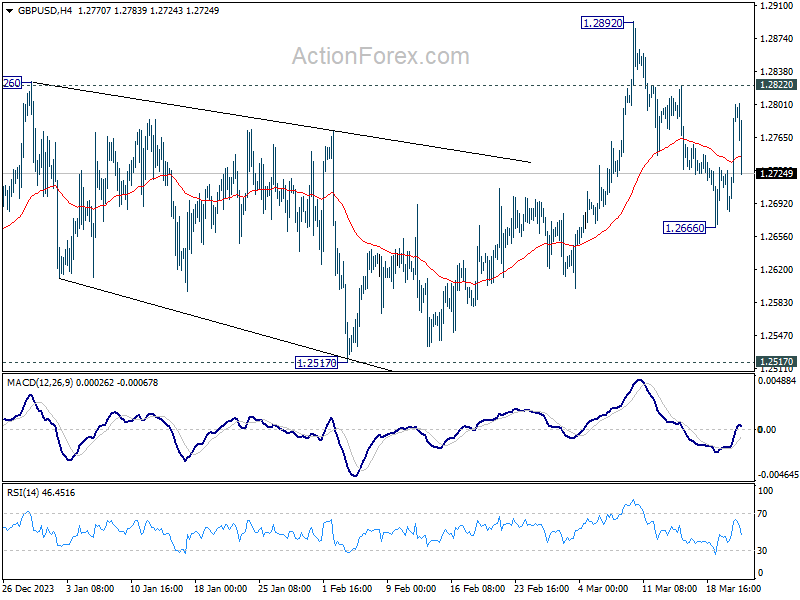

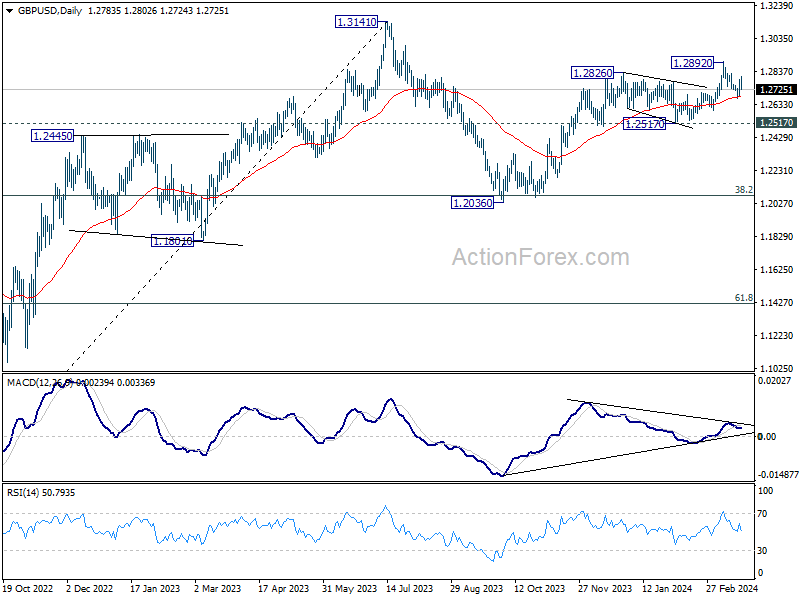

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2718; (P) 1.2753; (R1) 1.2820; More...

Intraday bias in GBP/USD remains neutral at this point. On the downside, break of 1.2666 support and sustained break of 55 D EMA (now at 1.2685) will target 1.2517 structural support next. However, break of 1.2822 will bring further rally to retest 1.2892 instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

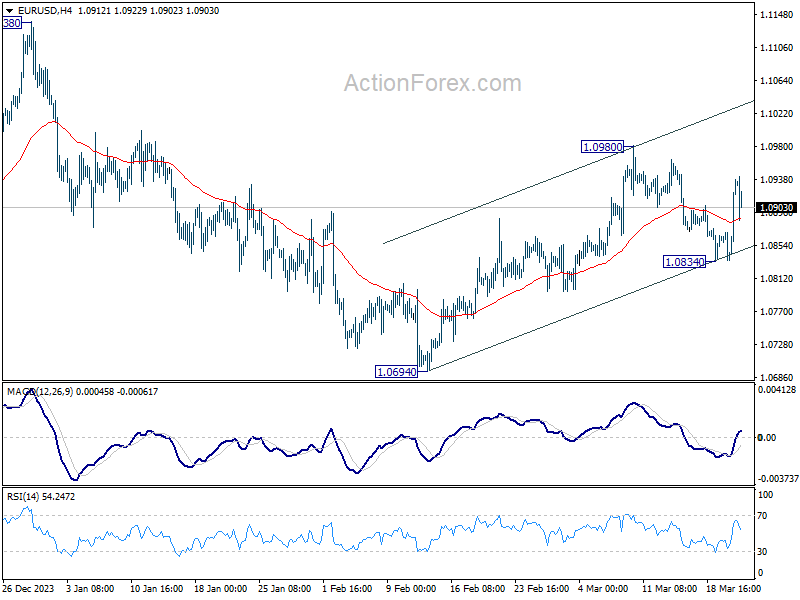

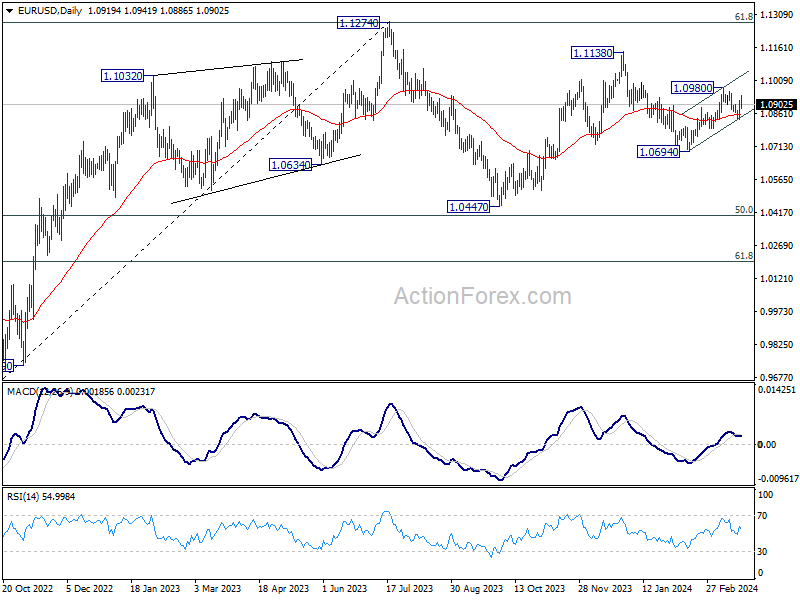

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0864; (P) 1.0894; (R1) 1.0951; More...

Intraday bias in EUR/USD stays mildly on the downside at this point. Pull back from 1.0980 has possibly completed at 1.0834, after drawing support from 55 D EMA. Firm break of 1.0980 resistance will resume the rise from 1.0694. On the downside, sustained trading below 55 D EMA (now at 1.0861) will argue that rebound from 1.0694 has completed and bring retest of this low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

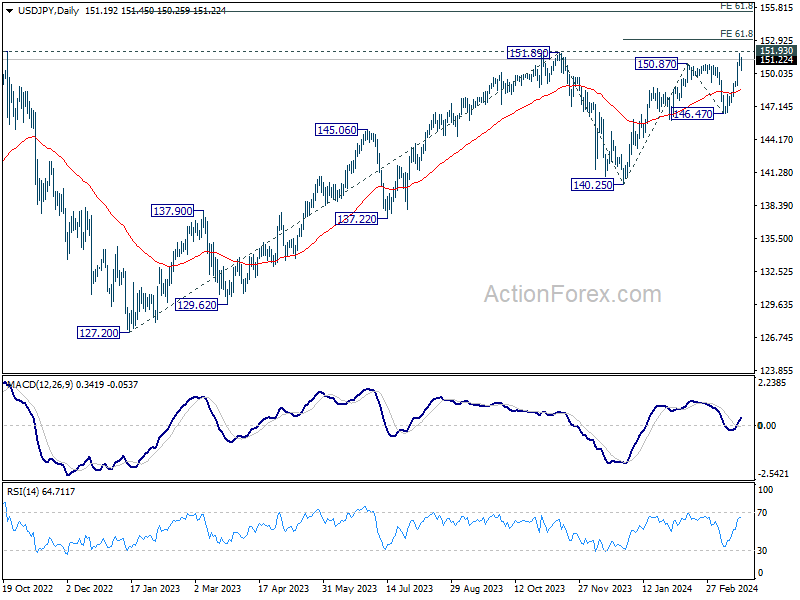

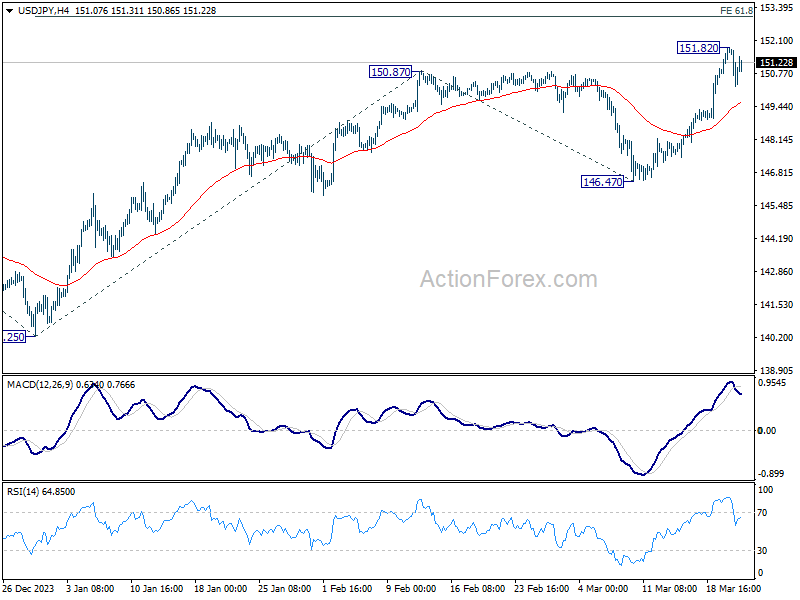

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.71; (P) 151.26; (R1) 151.80; More...

Intraday bias in USD/JPY remains neutral as consolidations continue below 151.82 temporary top. Further rise is expected as long as 55 4H EMA (now at 149.63) holds. On the upside, decisive break of 151.93 key resistance will confirm long term up trend resumption. Next near term target will be 61.8% projection of 140.25 to 150.87 from 146.47 at 153.03. However, sustained trading below 55 4H EMA will bring deeper fall back to 146.47 support instead.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.